Africa Food Ingredients Market Size, Share, Trends, Forecast, Research Report - Segmented By Ingredient Type (Flavors and flavor enhancers, Sweeteners, Sweeteners, Colors, Preservatives, Enzymes, Acidulants, Nutritional ingredients), Source, and Region (Sudan, Egypt, Kenya, Ethiopia, South Africa, and the rest of Africa) – Regional Industry 2025 to 2033

Africa Food Ingredients Market Size

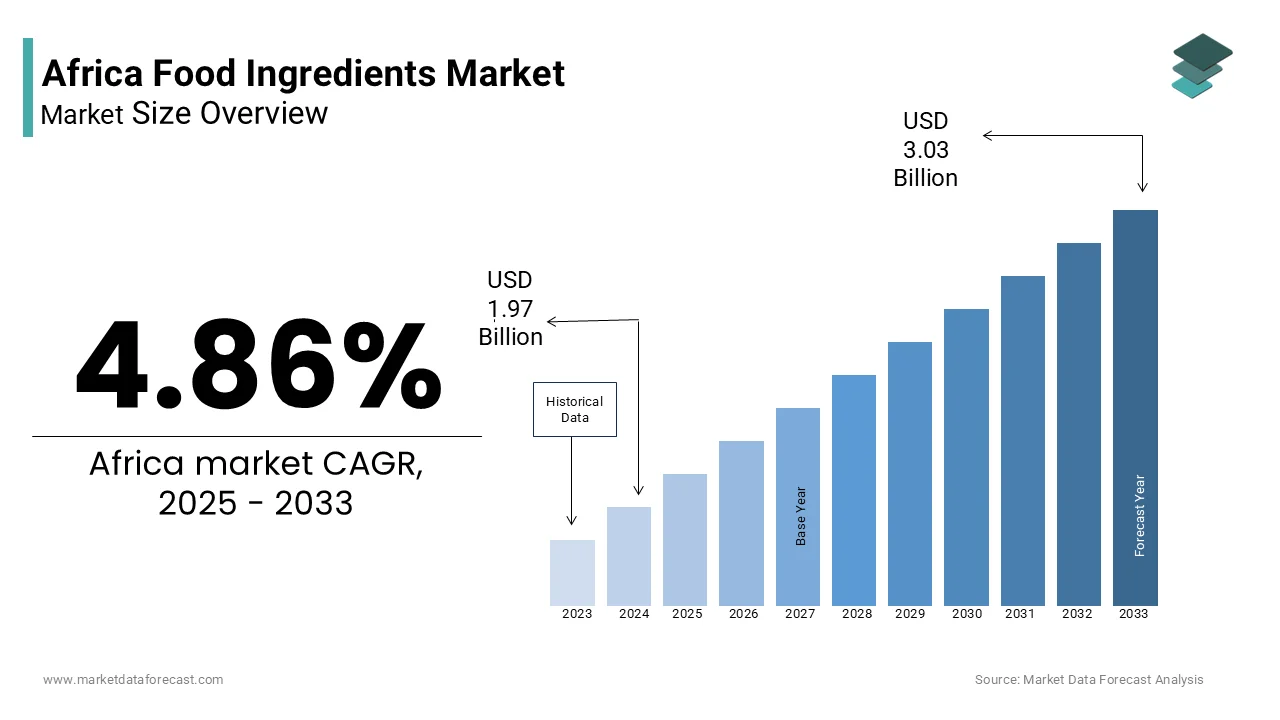

The Africa food ingredients market size was valued at USD 1.97 billion in 2024, and is expected to reach USD 3.03 billion in 2033 from USD 2.07 billion in 2025, at a CAGR of 4.86%.

Food ingredients are raw and processed substances used in the formulation of food and beverages, including proteins, carbohydrates, fats, vitamins, preservatives, flavorings, and functional additives. These ingredients are essential in enhancing nutritional value, texture, shelf life, and sensory appeal of both traditional and modern food products. The sector is shaped by the continent’s rich agricultural biodiversity, evolving dietary habits, and increasing demand for processed and fortified foods. In addition, urbanization and rising health awareness are driving demand for clean-label, organic, and nutrient-enriched components. The African Union’s Agri-Transformation Agenda emphasizes local ingredient valorization, promoting the shift from raw commodity exports to domestic processing and innovation in food science.

MARKET DRIVERS

Rapid Urbanization and Rising Demand for Processed and Convenient Foods

Africa’s accelerating urbanization is transforming consumption patterns, fueling demand for ready-to-eat meals, packaged snacks, and shelf-stable products that require functional food ingredients. Also, the continent’s urban population is expanding at 3.4% annually, with over 56% of Africans projected to live in cities by 2050. This shift is accompanied by changing lifestyles, with time-constrained consumers favoring convenience foods. Similarly, in Kenya, sales of bread, breakfast cereals, and flavored yogurts, dependent on emulsifiers, preservatives, and fortificants, rose year-on-year. This structural shift is compelling manufacturers to invest in stabilizers, texturizers, and nutrient premixes to meet quality and safety standards, thereby expanding the demand for industrial food ingredients.

Government-Led Nutrition Fortification Programs to Combat Micronutrient Deficiencies

Public health initiatives across Africa are mandating the fortification of staple foods with essential vitamins and minerals, creating institutional demand for food ingredients. According to the Global Alliance for Improved Nutrition (GAIN), over 40% of children under five in sub-Saharan Africa suffer from anemia, largely due to iron and folic acid deficiencies. In response, 28 African nations have implemented mandatory fortification policies for wheat flour, maize meal, edible oils, and salt. As of 2023, Nigeria, Tanzania, and South Africa require all industrially milled flour to be enriched with iron, zinc, vitamin A, and B-complex vitamins. These programs have institutionalized the use of micronutrient premixes, driving procurement by millers and creating a stable, policy-backed market for ingredient suppliers.

MARKET RESTRAINTS

Limited Local Production Capacity for Specialty and Functional Ingredients

Africa’s food ingredient sector is heavily reliant on imports for advanced additives such as hydrocolloids, enzymes, amino acids, and encapsulated flavors, constraining cost efficiency and supply chain resilience. According to the African Development Bank, most of specialty food ingredients used in processed foods are imported from Europe, Asia, and North America. Local manufacturing is limited to basic items like starches and sweeteners. High capital costs, lack of technical expertise, and inconsistent energy supply hinder investment in specialty ingredient plants. This dependency exposes African food producers to currency fluctuations and shipping delays, particularly evident during global supply chain disruptions like those in 2022.

Inadequate Cold Chain and Storage Infrastructure Leading to Ingredient Degradation

Perishable and sensitive food ingredients such as probiotics, enzymes, and liquid flavors require temperature-controlled logistics, yet Africa’s cold chain infrastructure remains underdeveloped. Also, only 15% of perishable food in sub-Saharan Africa moves through refrigerated transport, compared to 90% in North America and Europe. In Nigeria, post-harvest losses for temperature-sensitive ingredients exceed 30%, as reported by the Federal Ministry of Agriculture and Food Security. Poor warehousing, unreliable electricity, and fragmented distribution networks further compromise ingredient integrity, discouraging investment in high-value, biologically active components and limiting product innovation.

MARKET OPPORTUNITIES

Valorization of Indigenous Crops into Functional Food Ingredients

Africa’s biodiversity offers vast potential for developing novel, market-ready food ingredients from underutilized native crops such as teff, fonio, baobab, moringa, and shea. These crops are rich in protein, fiber, antioxidants, and phytonutrients, aligning with global clean-label and plant-based trends. Thousands of traditional African crops remain underexploited for commercial food production. In Ethiopia, teff flour is now exported to Europe and North America as a gluten-free alternative. With growing interest in sustainable and culturally authentic ingredients, African producers have a strategic window to develop value-added extracts, flours, and oils for both domestic and international markets.

Expansion of Public-Private Partnerships to Scale Ingredient Fortification and Local Sourcing

Collaborative initiatives between governments, NGOs, and private enterprises are unlocking scalable models for local ingredient production and fortification. The Scaling Up Nutrition (SUN) Business Network, active in 15 African countries, has facilitated partnerships between millers, ingredient suppliers, and development agencies to ensure consistent access to premixes. In Uganda, the partnership between the Ministry of Health and DSM enabled local production of vitamin A and iron premixes, reducing import costs, as per GAIN in 2023. These models demonstrate how coordinated investment in processing, quality control, and regulatory alignment can transform raw agricultural outputs into standardized, marketable food ingredients, fostering self-reliance and economic inclusion.

MARKET CHALLENGES

Fragmented Regulatory Frameworks and Inconsistent Food Safety Standards

The absence of harmonized food ingredient regulations across African nations creates compliance complexities for manufacturers and importers. In West Africa, a single emulsifier may be permitted in Nigeria but restricted in Côte d’Ivoire, disrupting regional trade. The Economic Community of West African States (ECOWAS) pointed out that cross-border food ingredient shipments faced delays due to regulatory mismatches. Small and medium producers often lack the resources to navigate these variations, limiting market access. Without regional alignment, the free flow of ingredients under the African Continental Free Trade Area (AfCFTA) remains constrained, impeding industrial scalability.

Limited Access to Technical Expertise and R&D in Food Science

Africa faces a critical shortage of trained food scientists, formulation experts, and quality control personnel, hindering innovation and quality assurance in ingredient development. In Kenya, the Kenya Bureau of Standards identified a gap in skilled personnel for food testing laboratories. Private sector R&D investment remains minimal, with less than 0.5% of GDP allocated to agricultural and food innovation, as per the Forum for Agricultural Research in Africa. This deficit limits the ability of local firms to develop proprietary blends, conduct stability testing, or meet international certification standards. As a result, African manufacturers remain dependent on foreign expertise, slowing the pace of indigenous product development and reducing competitiveness in the global food ingredients landscape.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.86% |

| Segments Covered | By Ingredient Type, Source, and Region. |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Sudan, Egypt, Kenya, Ethiopia, South Africa, and the rest of Africa |

| Market Leaders Profiled | Givaudan SA, BASF SE, Chr. Hansen Holding A/S, Firmenich SA, DSM-Firmenich, Sensient Technologies Corporation, Kerry Group, Archer Daniels Midland Company, Cargill, Incorporated, Ingredion Incorporated, Olam International, Cormart Nigeria Limited, Dangote Group, Tiger Brands Limited, Novozymes A/S, DuPont de Nemours, Inc., and Others. |

SEGMENTAL ANALYSIS

By Ingredient Type Insights

The nutritional ingredients segment dominated the Africa food ingredients market by capturing 24.7% of total value in 2024. This lead position is driven by widespread public health initiatives and rising consumer demand for fortified and health-enhancing foods. The continent-wide implementation of mandatory food fortification programs to combat widespread micronutrient deficiencies is a primary driver. According to the Global Alliance for Improved Nutrition (GAIN), over 28 African countries require the enrichment of staple foods such as wheat flour, maize meal, edible oils, and salt with essential nutrients like iron, folic acid, vitamin A, and iodine. In Nigeria, the National Agency for Food and Drug Administration and Control (NAFDAC) mandates fortification of all industrially processed flour. The South African Medical Research Council reported that since the introduction of mandatory fortification in 2003, the prevalence of neural tube defects in newborns dropped, validating the public health impact. These policies institutionalize demand for premixes and vitamins, ensuring consistent procurement by food processors. A further key factor is the growing consumer awareness of health and wellness in urban populations. Also, over 60% of middle-income consumers in cities like Nairobi, Accra, and Johannesburg now prefer fortified cereals, dairy, and beverages. This shift is amplified by rising rates of anemia, stunting, and malnutrition, particularly among children and pregnant women, prompting both government and private sector action. Companies like Tiger Brands and Promasidor have reformulated popular brands such as Mikate and Cowbell to include fortified blends, aligning with health trends and expanding the reach of nutritional ingredients beyond emergency interventions into mainstream consumption.

The enzymes segment is the fastest-growing ingredient type and is projected to expand at a CAGR of 10.6% from 2025 to 2033. This rapid growth is fueled by increasing sophistication in food processing and the need for efficiency, quality, and shelf-life extension. The expansion of industrial baking and dairy production across urban centers is a major driver. Enzymes such as amylases, proteases, and lipases are critical in improving dough stability, reducing fermentation time, and enhancing texture in bread and baked goods. In South Africa, Pioneer Foods uses enzyme-modified flours in its Albany and White Star brands to improve loaf volume and crumb softness. The Kenya Dairy Board pointed out that most of commercial yogurt and cheese producers now use microbial enzymes to standardize fermentation and reduce spoilage, improving yield and consistency. An additional contributing factor is the adoption of enzymes in beverage and bio-processing industries. In Ethiopia and Uganda, breweries are using beta-glucanases and proteases to improve wort filtration and clarity in beer production. The International Crops Research Institute for the Semi-Arid Tropics noted that enzyme-assisted processing of cassava and sorghum has reduced processing time by up to 40% while enhancing nutrient bioavailability. With rising investment in food processing zones in Rwanda and Senegal, and support from development agencies like the International Finance Corporation, enzyme use is transitioning from niche applications to essential tools in modern African food manufacturing, driving sustained demand growth.

By Source Insights

The natural source segment led the market by accounting for 52.5% of total consumption in 2024. This dominance shows a growing preference for clean-label, plant-based, and traditionally derived ingredients across both traditional and modern food systems. The deep-rooted reliance on indigenous and plant-based food components in African diets is a key driver. Staple ingredients such as baobab powder, moringa leaf extract, tamarind, and shea butter are naturally sourced and widely used in local cuisine, beverages, and fortified products. According to the United Nations Environment Programme, thousands of edible plant species are consumed across sub-Saharan Africa, many of which are processed into functional ingredients. These ingredients are perceived as safe, culturally authentic, and free from synthetic additives, aligning with consumer trust in traditional food systems. Another factor is the rising demand for clean-label products in urban retail markets. Companies have reformulated products using natural colors from beetroot and paprika, and natural preservatives like rosemary extract. With global trends favoring transparency and sustainability, African producers are leveraging their biodiversity to meet both domestic and export market expectations, reinforcing the dominance of naturally sourced food ingredients.

The synthetic source segment is the fastest-growing, projected to grow at a CAGR of 9.8% during the forecast period. This growth defies the clean-label trend in certain applications due to cost, stability, and scalability advantages. The cost-effectiveness and functional reliability of synthetic preservatives and acidulants in mass-produced foods is a primary driver. In low- and middle-income markets, where affordability is critical, synthetic additives like sodium benzoate, potassium sorbate, and citric acid offer longer shelf life and microbial control at lower prices than natural alternatives. In 2023, the production of shelf-stable tomato paste and fruit juices, key categories in Nigeria and Egypt, increased, driven by synthetic acidulant use to maintain pH and prevent spoilage. A different factor is the industrial demand for synthetic emulsifiers and sweeteners in bakery and confectionery sectors. Polysorbates and mono-diglycerides ensure consistent texture in mass-produced bread and margarine, while synthetic sweeteners like aspartame and sucralose are used in sugar-reduced products targeting diabetic consumers. Also, over 25 million adults in sub-Saharan Africa live with diabetes, creating demand for low-calorie alternatives. In South Africa, Tiger Brands uses synthetic sweeteners in its Zero sugar beverages, which saw a sales increase. Despite consumer skepticism, the performance, availability, and price advantages of synthetic ingredients ensure their growing use in industrial food manufacturing across the continent.

REGIONAL ANALYSIS

Nigeria Food Ingredients Market Insights

Nigeria led the Africa food ingredients market by accounting for 27.5% of regional demand in 2024. As the continent’s most populous nation, Nigeria’s position is defined by its vast consumer base and rapidly expanding processed food industry. Over 1,000 food processing plants were operational, producing bread, dairy, beverages, and ready-to-eat meals that require emulsifiers, preservatives, and fortificants. The government’s National Fortification Alliance mandates iron and folic acid in flour, driving institutional demand for nutritional premixes. Dangote Sugar and Flour Mills of Nigeria have integrated ingredient sourcing into their supply chains, reducing import reliance. With rising urbanization and a growing middle class, Nigeria remains the most dynamic market for both basic and functional food ingredients.

South Africa Food Ingredients Market Insights

South Africa is distinguished by its advanced food processing infrastructure and regulatory maturity. The country hosts the continent’s most developed food manufacturing sector, with companies like Pioneer Foods, Tiger Brands, and RCL Foods operating under strict quality and labeling standards. As per the South African Bureau of Standards, high percentage of packaged foods undergo nutritional labeling and additive compliance checks. The Department of Health enforces mandatory fortification of maize meal and wheat flour, ensuring steady demand for vitamins and minerals. The country is also a regional hub for ingredient distribution, with major suppliers like Sensient and DSM operating local facilities. With strong R&D capabilities and access to international markets, South Africa sets the benchmark for food ingredient innovation and regulatory alignment in Africa.

Angola Food Ingredients Market Insights

Angola is emerging as a key market due to post-war economic recovery and large-scale food import substitution initiatives. After decades of conflict, the government launched the “Programa de Importação Substituta” to boost local food production, including bread, pasta, and dairy, which require stabilizers, enzymes, and preservatives. Moreover, food processing output grew, supported by investments in Luanda and Cabinda. The country imports over 60% of its food ingredients, primarily from Portugal and Brazil, but is incentivizing local formulation through tax breaks. With rising urban consumption and government backing, Angola’s ingredient demand is poised for sustained growth despite infrastructural challenges.

Kenya Food Ingredients Market Insights

Kenya is positioned as a regional processing and trade hub for East Africa. The country’s strategic location, stable policies, and growing agro-industrial base support a robust demand for food ingredients. The Kenya Bureau of Standards mandates fortification of edible oils with vitamin A and wheat flour with iron, creating institutional procurement channels. According to the Kenya Association of Manufacturers, the food and beverage sector grew in 2023, driven by dairy, baking, and beverage production. Companies like Brookside Dairy and Kevian Kenya use imported and locally sourced ingredients to meet urban demand. The establishment of the Nairobi Food Innovation Hub has accelerated R&D in natural extracts and fortificants. With strong regional trade links and increasing FDI in food processing, Kenya is becoming a model for scalable, compliant ingredient adoption in Africa.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the key players in the Africa food ingredients market are

- Givaudan SA

- BASF SE

- Chr. Hansen Holding A/S

- Firmenich SA

- DSM-Firmenich

- Sensient Technologies Corporation

- Kerry Group

- Archer Daniels Midland Company

- Cargill, Incorporated

- Ingredion Incorporated

- Olam International

- Cormart Nigeria Limited

- Dangote Group

- Tiger Brands Limited

- Novozymes A/S

- DuPont de Nemours, Inc.

The competition in the Africa food ingredients market is evolving into a multi-tiered landscape where global ingredient suppliers, regional manufacturers, and emerging local startups vie for influence. Multinationals like dsm-firmenich and Tate & Lyle dominate in technical expertise and regulatory compliance, particularly in fortified and functional ingredients. Regional players and local blenders are gaining ground by offering cost-effective, context-specific solutions tailored to African processing conditions and taste preferences. The market is fragmented by geography, regulatory standards, and infrastructure quality, preventing any single entity from achieving continental dominance. Differentiation is driven by technical support, supply chain resilience, and alignment with public health mandates. With rising demand for both affordability and nutrition, competition is shifting from price alone to value-added services, innovation in natural extracts, and strategic partnerships with food processors and governments across the Africa food ingredients market.

TOP PLAYERS IN THE MARKET

DSM-Firmenich (now dsm-firmenich)

dsm-firmenich has established a significant presence in the Africa food ingredients market through its focus on nutritional fortification, sustainable sourcing, and public-private health partnerships. The company supplies vitamin premixes, amino acids, and omega-3 fatty acids to major food processors across Nigeria, Kenya, and South Africa. In 2023, it expanded its collaboration with the Global Alliance for Improved Nutrition (GAIN) to support flour fortification programs in Ethiopia and Tanzania, ensuring compliance with national health standards. The company launched a regional nutrition initiative in Accra, providing technical support to local millers on premix blending and quality control. It also partnered with African research institutions to develop biofortified crop-based ingredients, aligning with local agricultural systems. Through science-driven solutions and deep engagement in food security programs, dsm-firmenich is shaping the continent’s approach to functional and fortified food development.

Tate & Lyle

Tate & Lyle has strengthened its footprint in Africa by supplying texturants, sweeteners, and dietary fibers to beverage, dairy, and bakery manufacturers across high-growth urban markets. The company provides specialty ingredients such as sucralose, citric acid, and modified starches that enhance shelf life and sensory qualities in processed foods. In 2023, Tate & Lyle collaborated with South African beverage producers to reformulate sugar-reduced drinks in response to the country’s Health Promotion Levy on sugary drinks. It also engaged with Kenyan and Nigerian food companies to introduce fiber-enriched staples aimed at improving digestive health. The company established a technical service hub in Nairobi to support customer innovation and application testing. By combining global ingredient expertise with localized technical support, Tate & Lyle is enabling African manufacturers to meet evolving consumer demands for healthier, longer-lasting, and better-textured food products.

Sensient Technologies

Sensient Technologies plays a pivotal role in advancing color and flavor innovation in Africa’s food and beverage sector, offering both natural and synthetic solutions tailored to regional tastes and regulatory environments. The company supplies liquid and powder colors, flavor systems, and masking agents to processors of dairy, confectionery, and ready-to-drink products in South Africa, Nigeria, and Egypt. In 2023, Sensient launched a range of heat-stable natural colors derived from African botanicals like hibiscus and turmeric, designed for high-temperature processing common in local manufacturing. It also introduced culturally resonant flavor profiles—such as tamarind, ginger, and palm wine—for use in traditional-inspired modern snacks. With application labs in Johannesburg and Lagos, the company provides on-site formulation support, helping clients meet clean-label trends while maintaining product stability. Sensient’s focus on local relevance and technical agility has made it a preferred partner for brands seeking differentiation in a competitive marketplace.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Key players in the Africa food ingredients market are deploying strategic initiatives to expand reach and strengthen market integration. Major strategies include forming public-private partnerships to support government-led fortification programs, ensuring consistent demand for nutritional premixes. Companies are investing in technical service centers and application labs to assist local manufacturers with formulation, compliance, and product development. Expanding distribution through regional hubs and logistics partnerships enhances supply chain reliability. Firms are also developing hybrid ingredient solutions—blending natural and synthetic components—to balance cost, performance, and consumer preferences. Additionally, multinational players are sourcing raw materials locally, such as baobab and moringa, to support sustainability and reduce import dependency. Digital engagement and training programs for food producers are further strengthening brand loyalty and technical adoption across the continent.

RECENT HAPPENINGS IN THE MARKET

- In March 2023, dsm-firmenich expanded its technical support program in Addis Ababa, partnering with Ethiopia’s Ministry of Health to train 150 millers on vitamin premix blending for fortified flour production, strengthening its role in national nutrition initiatives across the Africa food ingredients market.

- In July 2023, Tate & Lyle launched a sugar-reduction pilot with Promasidor Nigeria, reformulating popular dairy-based drinks using sucralose and fiber blends to comply with emerging health regulations and meet consumer demand for low-calorie options in the Africa food ingredients market.

- In October 2023, Sensient Technologies introduced a new line of natural food colors derived from hibiscus and beetroot at the Africa Food Manufacturing Expo in Lagos, targeting processors seeking clean-label alternatives without compromising stability in high-heat applications in the Africa food ingredients market.

- In December 2023, dsm-firmenich co-launched a biofortification research project with the International Institute of Tropical Agriculture in Ibadan, focusing on enhancing nutrient content in cassava and maize-based foods using scalable ingredient solutions in the Africa food ingredients market.

- In February 2024, Tate & Lyle established a customer innovation hub in Nairobi to provide formulation support, sensory testing, and regulatory guidance to East African food manufacturers, enhancing its technical engagement and market responsiveness in the Africa food ingredients market.

MARKET SEGMENTATION

This research report on the Africa food ingredients market is segmented and sub-segmented into the following categories.

By Ingredient Type

- Flavors and flavor enhancers

- Natural flavors

- Artificial flavors

- Flavor enhancers

- Spices and herbs

- Sweeteners

- Natural sweeteners

- Artificial sweeteners

- High-intensity sweeteners

- Bulk sweeteners

- Emulsifiers

- Natural emulsifiers

- Synthetic emulsifiers

- Lecithin

- Others

- Colors

- Natural colors

- Synthetic colors

- Nature-identical colors

- Preservatives

- Natural preservatives

- Synthetic preservatives

- Antimicrobials

- Antioxidants

- Enzymes

- Carbohydrases

- Proteases

- Lipases

- Others

- Hydrocolloids

- Starches

- Gums

- Gelatin

- Others

- Acidulants

- Citric acid

- Lactic acid

- Acetic acid

- Others

- Nutritional ingredients

- Proteins

- Vitamins

- Minerals

- Fibers

- Others

- Others

By Source

- Natural

- Plant-based

- Animal-based

- Microbial

- Mineral

- Synthetic

- Artificial flavors

- Artificial sweeteners

- Synthetic colors

- Synthetic preservatives

- Others

- Nature-identical

- Nature-identical flavors

- Nature-identical colors

- Others

By Region

- Sudan

- Egypt

- Kenya

- Ethiopia

- South Africa

- Rest of Africa

Frequently Asked Questions

1. What is the Africa food ingredients market?

It covers natural and processed ingredients like flavors, colors, sweeteners, and preservatives used in food and beverages across Africa.

2. What drives growth in this Africa food ingredients market?

Rising urbanization, changing diets, and demand for packaged and healthy foods fuel the Africa food ingredients market.

3. Which countries lead the Africa food ingredients market?

South Africa, Nigeria, Egypt, and Kenya hold the largest share of the Africa food ingredients market.

4. What types of products are used in the Africa food ingredients market?

The Africa food ingredients market covers flavors, sweeteners, colors, preservatives, emulsifiers, enzymes, and nutrients.

5. Which industries consume the most in the Africa food ingredients market?

Bakery, beverages, dairy, snacks, and meat processing dominate the Africa food ingredients market.

6. How does the beverage industry influence the Africa food ingredients market?

The Africa food ingredients market benefits from rising demand for juices, soft drinks, and functional beverages.

7. What challenges affect the Africa food ingredients market?

Import reliance, infrastructure issues, and regulatory barriers impact the Africa food ingredients market.

8. What is the outlook for the Africa food ingredients market?

The Africa food ingredients market is set for steady growth with rising health awareness and modern food habits.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com