Global Electric Vehicle Market Size, Share, Trends & Growth Forecast Report, Segmented By Vehicle (Passenger Car, Commercial Vehicle, and Two Wheeler), Propulsion (BEV, FCEV, and PHEV, HEV), Components (Battery Cells And Packs, O-Board Charge, Infotainment, Electric Motor), Charging Station (Normal Charging, and Super Charging), Vehicle Class (Mid-Priced, Economy, and Luxury), Power Output (Less than 100 KW, 100-250 KW, and Above 250 KW) And Region (North America, Europe, Aisa-Pacific, Latin America, Middle East And Africa), Industry Analysis From 2026 to 2034

Global Electric Vehicle Market Size

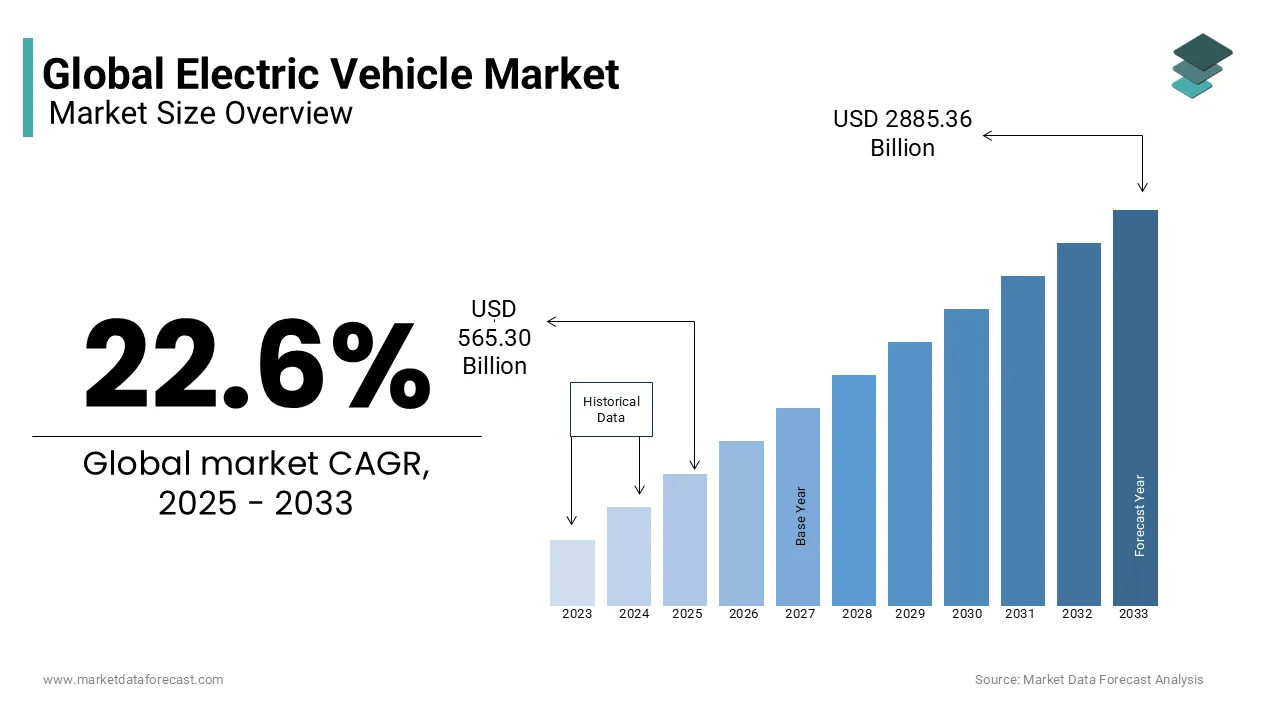

The global electric vehicle market was valued at USD 565.30 billion in 2025 and is anticipated to reach USD 693.06 billion in 2026 from USD 3537.47 billion by 2034, growing at a CAGR of 22.6% during the forecast period from 2026 to 2034.

The electric vehicle market includes the production, sales, and ecosystem supporting battery-electric and plug-in hybrid transport solutions. Globally, around 18% of all new cars sold in 2023 were electric, indicating a marked shift toward electrified mobility, up from just 14% in 2022, as per the International Energy Agency. Electric registrations surpassed 14 million that year, increasing new electric-car stock to approximately 40 million globally, reinforcing the transition’s momentum. Similarly, BloombergNEF projects a further leap to nearly 22 million EVs sold in 2025, driven by declining battery costs and expanding affordable models. This surge paints a landscape where EVs are swiftly transitioning from niche offerings to mainstream transport alternatives.

MARKET DRIVERS

Declining Battery Costs and Affordability Gains

A pivotal catalyst for rising EV adoption has been the sharp decline in battery prices. In 2024, average battery pack costs plummeted to $115 per kWh, representing a 20% drop, the steepest in recent years, primarily due to oversupply, cheaper materials, and the rise of lithium-iron-phosphate (LFP) chemistry, according to BloombergNEF. This cost reduction directly lowers vehicle prices and improves the total cost of ownership (TCO), making EVs more accessible to a broader audience. In fact, in key markets like the United States, owning an EV has become cheaper over its lifecycle than a gasoline vehicle, thanks to lower fuel costs and reduced maintenance, as per the Rocky Mountain Institute. These economic shifts are fueling demand across diverse consumer segments.

Policy Incentives and Market Momentum

Supportive policies continue to power EV adoption momentum. In 2023, electric vehicle registrations in China comprised around 45% of the total auto market, reflecting sustained uptake even without central purchase subsidies, as explained in the IEA Global EV Outlook. Additionally, cumulative global sales of EVs in early 2024 ramped up by 25% year-on-year, aided by battery and car affordability improvements and ongoing regulatory support. Meanwhile, BloombergNEF anticipates EV penetration will reach 25% of all light-vehicle sales globally in 2025, buoyed by policy frameworks and rising consumer interest. Incentives, ranging from purchase rebates to tax breaks, remain effective displacement tools for accelerating transition in major economies.

MARKET RESTRAINTS

Incentive Roll-backs and Regulatory Uncertainty

Incentive structures, once foundational to EV growth, now face withdrawal in key markets. BloombergNEF revised its global EV adoption outlook downward for the first time, attributing it to policy pullbacks in the U.S., notably the phase-out of EV tax credits and loosened fuel-economy mandates. These shifts threaten future growth, especially if automakers and consumers react with caution. Thus, policy inconsistency poses a real constraint, potentially slowing market expansion as governmental backing ebbs.

Slowing Growth in China Amid Waning Adoption Curves

China, which accounted for roughly 60% of global EV sales in 2023, is showing signs of deceleration. As the world’s largest EV market, any slowdown there markedly impacts global trajectories. While growth may rebound with policy restoration, such lulls highlight the market's dependency on transitional support. The shaping of future Chinese policy will play a critical role not just domestically but in sustaining global EV expansion.

MARKET OPPORTUNITIES

Surge in Emerging-Market EV Growth

Emerging economies are awakening as EV opportunities. BloombergNEF finds markets experiencing dramatic EV sales upticks, often outpacing wealthier countries in adoption rate growth. This signals the potential for leapfrogging transitions, where these nations bypass ICE dominance altogether. As affordability improves and new EV models penetrate, a new wave of mass adoption emerges outside traditional strongholds. Targeting these markets with tailored offerings could unlock substantial incremental volume and diversify the global EV footprint.

Improving Total Cost of Ownership and EV Truck Proliferation

EVs are rapidly becoming the economic choice. In the U.S., EVs now cost less to own than gas cars through fuel and maintenance savings, even with federal incentives ending, as reported by RMI. Meanwhile, the EV truck segment is burgeoning. Efficiency gains and economies of scale are driving battery costs lower, projecting parity in the truck sector within five years. Together, these trends expand EV beyond passenger cars, capturing commercial fleets and new emissions profiles, cementing deeper electrified transport ecosystems.

MARKET CHALLENGES

Charging Infrastructure Limitations and Disparities

Insufficient charging infrastructure remains a systemic bottleneck. In regions like Andhra Pradesh, India, EV penetration stalls at just 1.85% despite national subsidies, hindered by only 601 charging stations statewide, roughly one per 205 kilometers of road, according to The Times of India. This deficiency stalls consumer confidence and dampens adoption rates. Without strategic infrastructure expansion, especially in rural and underserved areas, EV adoption remains uneven and vulnerable to grid and access constraints.

Market Deceleration with Maturing Demand

Even as EV markets mature, their rapid ascent is showing signs of tapering. Global EV sales growth eased to 21% year-on-year in July 2025, the slowest since January, according to Rho Motion via Reuters. This deceleration, influenced by subsidy pauses and market saturation in leading regions, suggests that early explosive growth rates cannot be sustained indefinitely. Manufacturers and policymakers need to anticipate slower curves and innovate beyond incentives, focusing on utility, affordability, and integration into broader transport systems to sustain long-term adoption.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 22.6% |

| Segments Covered | By Vehicle, Propulsion, Components, Charging Station Type, Vehicle Class, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Tesla, BMW Group, Nissan Motor Corporation, Toyota Motor Corporation, Volkswagen AG, General Motors, Daimler AG, Energica Motor Company S.p.A., BYD Company Motors, Ford Motor Company, and Others. |

SEGMENTAL ANALYSIS

By Vehicle Insights

The two-wheeler segment dominated in volume. In India, for instance, electric two-wheeler sales surpassed 1.14 million units in fiscal year 2025. The appeal lies in affordability and practicality; these vehicles are often 60–70% cheaper to operate than conventional equivalents and fit crowded urban geographies. Besides, targeted policy frameworks like FAME II subsidies and local incentives sharply reduce acquisition costs, and manufacturers are responding with scalable products tailored for city mobility. The result is that two-wheelers firmly lead the segment in both penetration and momentum.

The commercial electric vehicles segment is the fastest-rising category, particularly in larger vehicle classes and fleet applications, and is likely to expand ata 23.3% CAGR. Growth is propelled by fleet electrification mandates, such as clean fleet policies in urban centers, and a strong value proposition for freight and public transport operators, who benefit from lower operating costs, quieter operation, and zero tailpipe emissions. E-commerce expansion and logistics modernization further accelerate demand for electric vans, buses, and trucks.

By Propulsion Insights

The Battery electric vehicles (BEVs) segment dominated both volume and investment. In the electric commercial vehicle subsector, BEVs held a commanding and substantial share of revenue in 2024. BEV dominance stems from technological maturity, advances in lithium-ion chemistry, cost reductions (approaching $100/kWh), and the expanding direct current fast-charging infrastructure. Policymakers in major markets are increasingly aligning incentives, emissions regulations, and urban clean-air initiatives to favour all-electric over hybrid solutions, making BEVs the default choice for full electrification.

The fuel-cell electric vehicles (FCEVs) segment is expected to grow at the fastest trajectory and is projected to deliver a 27.3% CAGR in commercial vehicle applications. Hydrogen-based propulsion appeals in heavy-duty transport where rapid refueling and long-range duty cycles are critical, for example, in trucking, buses, and industrial fleets. Coupled with growing investment in hydrogen infrastructure and national hydrogen strategies, FCEVs are emerging as a promising long-term complement to BEVs in high-duty-cycle sectors.

By Components Insights

The battery systems segment remained the most value-intensive component segment by comprising 30.4% of an EV's total cost in 2024. Global battery production reached approximately 2,000 GWh in 2023, with 772 GWh dedicated to EVs, according to publicly available supply-chain data. The dominance of battery packs is derived from their centrality to EV capability, range, performance, cost, and safety, all of which are all contingent on battery design and chemistry. Economies of scale, supply-chain dominance (notably by China), and continuous improvements in energy density and manufacturing efficiency preserve battery packs as the segment’s bedrock.

The on-board chargers and infotainment systems segment is among the fastest-innovating components. As EV buyers increasingly expect integrated navigation, energy management, over-the-air updates, and high-performance charging interfaces, both segments are evolving swiftly. Innovations like vehicle-to-grid charging, bidirectional on-board units, and immersive infotainment platforms (powered by AI and cloud connectivity) drive both customer value and OEM differentiation—even if formal CAGR data is yet to solidify.

REGIONAL ANALYSIS

Asia Pacific Market Analysis

As the world’s center of gravity for EVs, the Asia Pacific accounts for 67.3% of global EV sales. China alone sold millions of electric cars in 2024, with national charging points reaching the ~12.8 million mark by December 2024, up 49% year over year, which keeps purchase and usage friction low. Beyond China, momentum is coming from Southeast Asia’s factory investments and rising sales, plus steady volumes in Japan, Korea, and Australia. Together, these push APAC well past half the world market.

Europe Market Analysis

Europe represented a significant share of global EV sales. The IEA projected ~3.5 million electric cars sold in Europe in 2024, with EVs “about one in four” new cars despite uneven incentives; that aligns with the global ~17 million baseline. 2025 data points to re-acceleration: Q1 2025 BEV registrations +28% to ~571k (17% share) and new quarterly records in spring/summer. Policy remains the backbone while a broader model mix (including more affordable BEVs) is lifting private demand after a fleet-heavy 2023. Infrastructure scale and regulatory clarity keep Europe a solid #2 even as brand shares shuffle.

North America Market Analysis

North America contributed notably to the global EV sales. The IEA estimated the United States at ~1 in 9 new cars electric for 2024 (roughly ~1.3 million EVs), and Canada’s ZEV penetration topped ~10% in 2023–24, putting the region near ~1.5–1.6 million EVs against a ~17 million global total. Macro headwinds (rates, pricing) cooled the growth curve, but federal and state incentives, the IRA’s supply-chain pulls, and a fast-growing fast-charging network (U.S. >204,600 outlets by early 2025) sustain a large installation base and steady adoption. Pickup launches and more sub-$40k BEVs are the main 2025–26 catalysts for share gains from today’s high-single-digit global slice.

Latin America Market Analysis

Among the smaller global regions by volume, Latin America's contribution was decent, but it’s heating up quickly. Brazil almost doubled to ~177,360 “electrified” sales in 2024 (association ABVE), with plug-ins growing as Chinese brands expand; mid-2024 data showed ~55,000 EVs in H1 alone and ~5.3% share for that semester.

Middle East Market Analysis

Also, with a minor share of global sales, the Middle East sits at a very small share but is laying foundations, especially in the UAE, where public fast-charging is scaling. EVs remain a thin slice of the on-road fleet (UAE reports <1.3% of vehicles), yet rising model availability, high fuel-economy baselines, and heavy grid investment are priming demand. With China’s cost-down models entering and Gulf utilities backing charging corridors, the region’s share is tiny today but set for a multi-year climb from a sub-percent base.

COMPETITIVE LANDSCAPE

Competition in the EV space is fierce and dynamic. Established manufacturers and emerging entrants alike vie through bold regional investments, technological innovations, and ecosystem development. In the Asia-Pacific, localization is a key differentiator—factories in Thailand, Indonesia, and India signal long-term commitment. Model diversity, like premium SUVs, aligns with consumer preferences and market maturity. Companies such as BYD leverage shipping and exports alongside regional plants, while Xpeng and VinFast adopt agile rollout strategies. Beyond manufacturing, investments into charging networks and showrooms amplify brand presence. Meanwhile, OEMs navigate evolving regulations and policy landscapes by embedding flexibility in operations. The race is not just one of production—it’s about building a seamless, locally resonant EV ecosystem.

KEY MARKET PLAYERS

They are playing a dominant role in the global electric vehicle market.

- Tesla

- BMW Group

- Xpeng

- VinFast

- Nissan Motor Corporation

- Toyota Motor Corporation

- Volkswagen AG

- General Motors

- Daimler AG

- Energica Motor Company S.p.A

- BYD Company Motors

- Ford Motor Company

Top Players In The Market

- BYD has dynamically expanded its Asia-Pacific footprint, opening its first wholly owned EV plant in Rayong, Thailand, in July 2024. This facility assembles complete vehicles and employs 10,000 staff, marking a departure from pure exporting and enabling localized production. Such forward-looking infrastructure accelerates regional delivery speed and reduces costs, reinforcing BYD’s adaptability and regional anchoring.

- Xpeng has strengthened its Southeast Asia presence with a bold rollout effort. In July 2024, it launched the G6 SUV in Singapore, ranking among the top three fully electric SUVs in sales. It opened its first Singapore showroom in November, then expanded into Malaysia with dealership plans covering multiple states. In Indonesia, the brand began knock-down assembly in mid-2025 for the G6 and forthcoming X9 models. These efforts reflect Xpeng’s strategy to localize operations and engagement for better market penetration.

- VinFast has surged into the Asia-Pacific EV arena through aggressive manufacturing investments. In early 2025, it inaugurated a $500 million EV production facility in Tamil Nadu, India, targeting 50,000 units annually with room to scale. Concurrently, it is introducing premium VF6 and VF7 SUVs tailored to the Indian market, whilst exploring dealership networks and charging infrastructure investments. This multi-layered regional push underscores VinFast’s ambition to become a recognized and integrated player—leveraging localized manufacturing, market-centric models, and ecosystem development.

Top Strategies Used by Key Market Participants

Leaders pursue localized manufacturing, anchoring production in regional markets to cut costs and tariffs. They emphasize tailored model introductions, engineering EVs for local preferences. Network expansion, via showrooms, dealerships, and charging infrastructure, enhances accessibility and consumer trust. They also pursue capital support and strategic alliances to solidify regional ecosystem integration.

RECENT MARKET NEWS

- In July 2024, BYD began EV production at its plant in Thailand, enabling local assembly and reinforcing its Asia-Pacific manufacturing footprint.

- In March 2025, Xpeng initiated knock-down assembly of the X9 in Indonesia, marking its first production outside China and enhancing regional presence.

- In January 2025, VinFast opened its $500 million EV factory in Tamil Nadu, launching Indian manufacturing and signaling long-term regional commitment.

- In November 2024, Xpeng inaugurated its first Singapore showroom following the G6 launch, strengthening direct customer engagement and brand visibility.

- In July 2025, BYD expanded its Indonesia factory workforce plan to 18,000 and accelerated its operational timeline, intensifying regional capabilities.

MARKET SEGMENTATION

This market research report on the global electric vehicle market is segmented and sub-segmented based on vehicle, propulsion, component, charging station type, vehicle class, and Region.

By Vehicle

- Passenger Car

- Commercial Vehicle

- Two Wheeler

By Propulsion

- Battery Electric Vehicle (BEV)

- Fuel Cell Electric Vehicle (FCEV)

- Plug-In Hybrid Electric Vehicle (PHEV)

- Hybrid Electric Vehicle (HEV)

By Components

- Battery Cells & Packs

- On-Board Charge

- Infotainment

- Electric Motor

By Charging Station Type

- Normal Charging

- Supercharging

By Vehicle Class

- Mid-Priced

- Economy

- Luxury

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What Is the current Size Of Global Electric Vehicle Market?

The current size of the global electric vehicle market during the forecast period from USD 565.30 Bn in 2025.

What Is The Growth of Electric Vehicle Market?

The Global Electric Vehicle Market size is expected to reach a valuation of USD 2885.36 Billion by 2033.

What Are The Key Market Players Involved In Electric Vehicle Market?

Tesla, BMW Group, Nissan Motor Corporation, Toyota Motor Corporation, Volkswagen AG, General Motors, Daimler AG, Energica Motor Company S.p.A., BYD Company Motors, Ford Motor Company. Are playing a dominant role in the global electric vehicle market.

What is driving growth in the global automotive wheel market?

Rising vehicle production and consumer preference for larger, styled wheels are boosting demand across passenger and light commercial vehicles.

How are material choices impacting the market?

Aluminum alloy wheels dominate due to their balance of strength, aesthetics, and fuel efficiency.

What role do electric vehicles play in wheel demand?

EVs need stronger, lighter wheels to support heavy batteries while maximizing range and performance.

Which regions lead in automotive wheel production and demand?

Asia Pacific leads in both manufacturing and consumption, with China, Japan, and India at the forefront.

How important is customization in today’s wheel market?

Highly important—consumers increasingly choose vehicles with upgraded or aftermarket wheels for aesthetic and performance gains.

What are the latest trends in wheel technology?

Smart wheels with integrated sensors for monitoring pressure, temperature, and load are entering premium segments.

Are sustainability concerns affecting wheel production?

Yes—manufacturers are focusing on recyclable materials and energy-efficient casting processes to reduce environmental impact.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com