Europe 3D Bioprinting Market Size, Share, Trends & Growth Forecast Report By Material Type, Technologies, Components, Applications and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2025 to 2033)

Europe 3D Bioprinting Market Report Summary

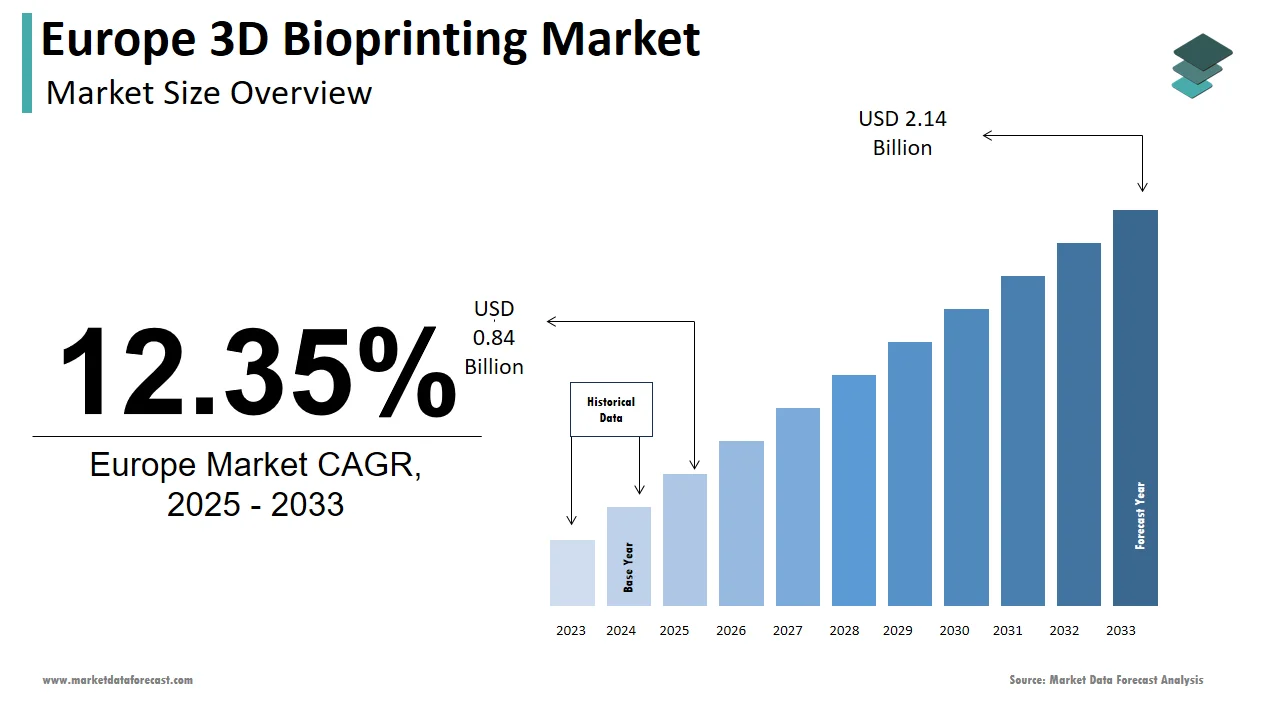

The Europe 3D bioprinting market was valued at USD 0.75 billion in 2024, is estimated to reach USD 0.84 billion in 2025, and is projected to reach USD 2.14 billion by 2033, growing at a CAGR of 12.35% during the forecast period from 2025 to 2033.

The growth of the European 3D bioprinting market is driven by rising investments in regenerative medicine, advancements in bioink formulations, and expanding applications in drug research and tissue engineering. The increasing collaboration between academic institutions, biotech startups, and research laboratories, along with the emergence of biofabrication technologies, is further accelerating market expansion across the region.

Key Market Trends

- Growing adoption of 3D bioprinting for personalized medicine and drug testing applications.

- Advancements in bioinks and scaffold materials are improving tissue viability and print resolution.

- Increasing focus on organ and tissue regeneration research supported by EU-funded biomedical projects.

- Expansion of academic and commercial partnerships is driving bioprinting innovation and clinical translation.

- Rising interest in ethical and sustainable bioprinting practices aligns with European research governance standards.

Segmental Insights

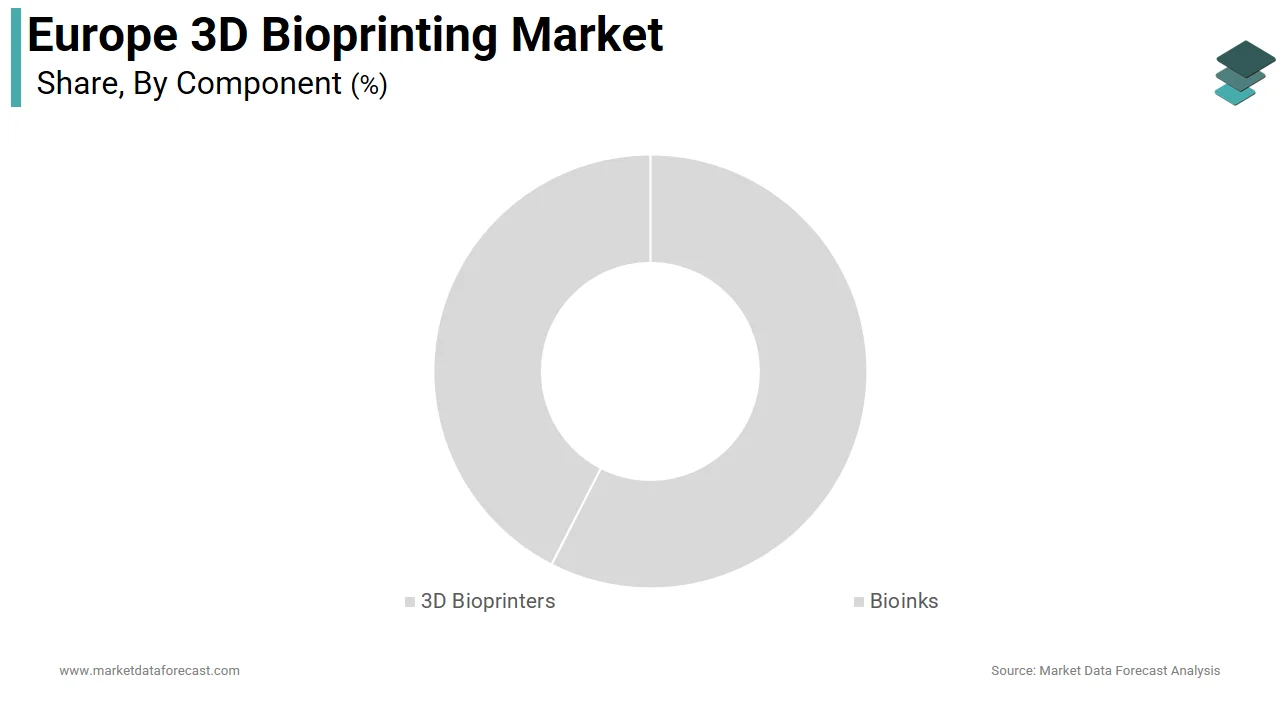

- Based on component, the bioinks segment dominated the Europe 3D bioprinting market and accounted for a 58.2% share in 2024, driven by ongoing innovation in hydrogel-based and cell-laden bioinks that enhance tissue growth and cell differentiation.

- Based on application, the drug research segment led the Europe 3D bioprinting market and held a 34.6% share in 2024, attributed to the growing use of bioprinted tissue models for drug toxicity testing, pharmaceutical screening, and personalized therapy validation.

- Based on end user, the research organizations and academic institutes segment held the leading share of 65.1% of the Europe 3D bioprinting market in 2024, supported by government-backed R&D initiatives, university-led innovation centers, and grants for regenerative medicine research.

Regional Insights

The European 3D bioprinting market is witnessing significant growth across major economies, supported by advancements in life sciences research, strong regulatory frameworks, and interdisciplinary academic collaborations.

- Germany led the market, accounting for a 22.5% share in 2024, driven by world-class biomedical research infrastructure, public funding, and industrial partnerships in biofabrication.

- France followed closely with a 16.5% share in 2024, supported by national biotechnology programs and rising adoption of 3D bioprinting in pharmaceutical R&D.

- The United Kingdom maintains a notable position in the market, leveraging academic leadership from institutions such as the University of Cambridge and Queen Mary University of London, alongside a strong private innovation ecosystem.

- Sweden is progressing steadily, recognized for its leadership in bioink innovation, ethical bioprinting standards, and sustainable biomedical technology development.

Competitive Landscape

The European 3D bioprinting market is moderately consolidated, with key players emphasizing product innovation, research collaboration, and biofabrication technology advancement. Companies are focusing on next-generation bioprinters, custom bioinks, and cell-based tissue models to expand their clinical and pharmaceutical applications.

Prominent players in the market include 3Dynamic Systems Ltd., Organovo Holdings, Inc., CELLINK, Bio3D Technologies, Advanced Solutions, Inc., EnvisionTEC GmbH, Ourobotics, 3D Bioprinting Solutions, BioBots, Inc., Poietis, Cyfuse Biomedical K.K., Aerotech, Inc., Aspect Biosystems, GeSIM, Nano3D Biosciences, Inc., regenHU Ltd, and GeSIM

Europe 3D Bioprinting Market Size

The 3D bioprinting market size in Europe was valued at USD 0.75 billion in 2024. The European market is estimated to be worth USD 2.14 billion by 2033 from USD 0.84 billion in 2025, growing at a CAGR of 12.35% from 2025 to 2033.

3D bioprinting in Europe refers to the additive manufacturing of living tissues and organ constructs using bioinks composed of cells, biomaterials, and growth factors precisely deposited layer by layer to replicate biological structures. Unlike conventional 3D printing, this technology operates at the intersection of regenerative medicine, tissue engineering, and digital health, requiring stringent sterility, biocompatibility, and functional maturation protocols. Europe’s approach to 3D bioprinting is distinctively shaped by its regulatory philosophy under the European Medicines Agency and the Medical Devices Regulation, which classifies most bioprinted constructs as advanced therapy medicinal products or Class III medical devices. The European Commission's Horizon Europe program has actively funded research into bioprinting and regenerative medicine, including topics such as wound healing, cartilage regeneration, and vascularized tissue models, as part of its multi-billion-euro budget for global challenges like health. The field of bioprinting and tissue engineering is growing rapidly across the EU, with a significant number of academic and clinical centers involved in research and development, and the European market for 3D bioprinting generating hundreds of millions in revenue. The European Chemicals Agency further regulates bioink constituents under REACH, ensuring cytotoxicity and environmental safety. This ecosystem positions Europe not as a volume-driven market but as a science-led regulatory pioneer where clinical validation and ethical oversight define the trajectory of bioprinting innovation.

MARKET DRIVERS

Stringent Regulatory Frameworks Enabling Clinical Translation Pathways

Harmonized regulatory structure fuels the growth of the Europe ED bioprinting market. According to research, the number of bioprinted tissue constructs entering clinical trials in the EU has seen a general increase in recent years, reflecting growing interest and advancements in regenerative medicine and tissue engineering. The European Commission emphasizes streamlining regulatory processes for advanced therapies, with the centralized authorization process aiming to provide a more efficient and harmonized path to market compared to varied national systems. National competent authorities support this framework. Regulatory bodies like Germany's Paul Ehrlich Institute are increasingly focusing on the specific challenges of advanced therapies, including the need to evaluate cell sourcing, bioink stability, and sterility validation for complex products. Similarly, there is an ongoing trend among national regulatory agencies, such as France's ANSM, to develop clearer guidance for the quality control of bioprinted medical products as the technology matures. These structured pathways incentivize academic and industrial investment by de risk de risk of the translation from lab to patient.

High Concentration of Academic and Clinical Research Infrastructure

The region hosts a dense network of interdisciplinary research hubs that boost the expansion of the Europe 3D bioprinting market. It serves as an engine of 3D bioprinting innovation, bridging engineering, biology, and clinical medicine. According to research, there is a significant increase in European research funding for projects focused on developing advanced bioprinting applications, particularly the creation of complex tissues like vascularized models and automated biofabrication processes. Institutions have developed breakthrough bioinks with embedded microchannels enabling nutrient perfusion in thick tissues. Collaboration between European academic, healthcare, and industry sectors is intensifying to create standardized, regulatory-compliant bioprinting manufacturing workflows. National investments amplify this ecosystem. This concentration of talent, infrastructure, and collaborative funding creates a self-reinforcing cycle of discovery and standardization that sustains Europe’s scientific leadership in the field.

MARKET RESTRAINTS

Limited Scalability of Bioink Production Under GMP Standards

The absence of industrial-scale Good Manufacturing Practice-compliant bioink production facilities is creating barriers in clinical translation, which is a major impediment to the Europe 3D bioprinting market. According to sources, fewer bioink formulations in the EU have received full GMP certification due to stringent requirements on endotoxin levels, sterility, and batch-to-batch consistency. Logistical and regulatory hurdles, such as the need for specialized manufacturing conditions (hospital clean rooms), do cause delays in bioprinting clinical trials. This fragmented production model inflates costs. The cost of GMP-grade materials for clinical use is significantly higher than that of R&D/preclinical materials due to the rigorous quality control and manufacturing standards required. Commercial viability and the ability to conduct multi-center trials for bioprinted therapies remain limited by the absence of dedicated bioink manufacturing infrastructure that complies with EU pharmacopoeia standards.

Ethical and Legal Ambiguity Surrounding Bioprinted Human Tissues

Lack of unified ethical and legal definitions for bioprinted human tissues creates uncertainty around ownership, consent, and commercialization. This uncertainty negatively impacts the expansion of the Europe 3D bioprinting market. This ambiguity affects clinical deployment. In Germany, bioprinted cartilage is regulated as a medical device, while in France, the same construct may be classified as an advanced therapy medicinal product depending on cell viability. Until the EU establishes a harmonized legal taxonomy for bioprinted products, innovation will remain fragmented, and investors will be cautious.

MARKET OPPORTUNITIES

Integration of Bioprinting in Personalized Oncology Drug Testing

The region’s dominance in precision oncology is creating a key opportunity for the growth of the Europe 3D bioprinting market. This opportunity enables the development of 3D bioprinted tumor models that replicate patient-specific cancer microenvironments for drug screening. According to studies, there is a growing adoption of bioprinted tumor avatars within EU clinical centers to help guide chemotherapy selection for difficult-to-treat cancers. Moreover, the European Commission is significantly increasing funding to scale the development and use of advanced bioprinted organoid platforms that provide more realistic drug response predictions.. National cancer plans reinforce this trend. This clinical utility transforms bioprinting from a research tool into a diagnostic asset with reimbursable potential under EU health technology assessment frameworks.

Development of Regulatory Science Platforms for Bioprinting Standards

The region is pioneering dedicated regulatory science initiatives to establish metrology standards and validation protocols essential for bioprinting commercialization, which provides fresh prospects for the expansion of the Europe 3D bioprinting market. The European Union is actively working on developing standardized reference materials and testing protocols for bioprinting to ensure consistency across research and clinical applications. Standardization bodies such as CEN are working on developing and finalizing technical specifications for testing methods concerning bioink properties like rheology, sterilization, and degradation kinetics. National metrology institutes are contributing. National metrology institutes like Germany's PTB are researching and developing metrological standards and reference materials for bioinks, such as those based on alginate, to improve cross-laboratory comparability. The EMA and related regulatory bodies are engaging with industry and academia through various initiatives and working groups to establish and align the preclinical evidence requirements for the regulatory approval of bioprinted medical products. These efforts reduce regulatory uncertainty and accelerate market entry for compliant platforms. This proactive standard-setting positions Europe to shape global bioprinting norms while fostering domestic innovation.

MARKET CHALLENGES

Shortage of Multidisciplinary Talent in Biofabrication Engineering

There is a serious gap in professionals who combine expertise in tissue biology, additive manufacturing, and regulatory science, a shortage that impedes the growth of the Europe 3D bioprinting market. According to sources, there is a shortage of professionals in the EU who possess certified training in both bioink formulation and GMP-compliant bioprinting operations. The demand for these roles substantially outpaces the current supply of qualified specialists. In addition, bioprinting is rarely integrated into higher education curricula in the EU. Only a small number of master's programs currently offer relevant training in this field. This talent deficit manifests in project delays. National initiatives are emerging, but fragmented. Europe's bioprinting potential will stay limited by a lack of skilled personnel until coordinated education and certification frameworks are put in place.

Inconsistent Reimbursement Pathways for Bioprinted Therapies

The region lacks harmonized health technology assessment and reimbursement mechanisms for 3D bioprinted products, which obstructs the expansion of the Europe 3D bioprinting market. A minority of EU member states have evaluated bioprinted skin grafts for reimbursement, showing wide divergence in pricing and coverage criteria. Despite moves toward aligning clinical assessments, the relevant EU regulation does not currently include advanced therapy medicinal products, which limits patient access to bioprinted chronic wound dressings to clinical trials or self-pay models in most countries. Bioprinted therapies experience significant delays in achieving market access and reimbursement compared to conventional medical devices. The absence of reliable funding routes means that access for patients and the development of sustainable business models remain a challenge for bioprinted products, even those that are clinically validated.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Component, Application, End-user, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | 3Dynamic Systems Ltd., Organovo Holdings, Inc., CELLINK, Bio3D Technologies, Advanced Solutions, Inc., EnvisionTEC GmbH, Ourobotics, 3D Bioprinting Solutions, BioBots, Inc., Poietis, Cyfuse Biomedical K.K., Aerotech, Inc., Aspect Biosystems, GeSIM, Nano3D Biosciences, Inc., regenHU Ltd, and GeSIM |

SEGMENTAL ANALYSIS

By Component Insights

The bioinks segment dominated the Europe 3D bioprinting market and accounted for a 58.2% share in 2024. The dominance of the bioinks segment is attributed to their foundational role as the biological matrix that determines cell viability, structural fidelity, and functional maturation of printed constructs. As per research, regulatory bodies are increasingly focusing on the characterization and standardization of bioink properties as critical quality attributes for advanced therapeutic products. Also, stricter compliance and safety regulations are being enforced for synthetic polymers used in bioinks to ensure they meet specific safety thresholds. National research programs amplify demand. Government funding agencies are increasingly directing research grants toward innovative bioink development, particularly for complex applications like creating vascularized tissues. These regulatory and scientific imperatives make bioinks not a consumable but a strategic determinant of clinical success.

The hybrid bioinks segment is estimated to register the fastest CAGR of 21.4% from 2025 to 2033 due to their ability to merge the biocompatibility of natural polymers like collagen with the mechanical tunability of synthetic hydrogels such as Pluronic or PEG. According to research, the use of hybrid bioinks creates more physiologically relevant 3D cancer models (tumor avatars) that better mimic the native tumor microenvironment for advanced research and personalized medicine applications. As per sources, hybrid formulations show lower batch variability than pure natural bioinks, enhancing GMP compliance. National metrology institutes are supporting standardization. These performance and regulatory advantages position hybrid bioinks as the material frontier for complex tissue engineering.

By Application Insights

The drug research segment led the Europe 3D bioprinting market and held a 34.6% share in 2024. The growth of the drug research segment is propelled by the EU’s strategic shift toward human-relevant preclinical models to reduce animal testing and improve drug attrition rates. There is an increasing trend for biopharmaceutical companies in the EU to replace traditional 2D cell cultures with advanced in vitro models, such as bioprinted liver tissue, for toxicity screening purposes. Regulatory bodies are moving towards mandatory adoption of non-animal methods for chemical safety assessments within the European Union. National initiatives reinforce this trend. These regulatory, scientific, and ethical drivers solidify drug research as the core application segment.

The bioprinted skin segment is anticipated to witness the fastest CAGR of 23.7% over the forecast period, owing to the rising burden of chronic wounds and burn injuries across aging European populations. Diabetic foot ulcers affect millions of people worldwide, and even with standard treatments, recurrence rates are high, with approximately 40% of patients experiencing a recurrence within one year of healing, which emphasizes a significant unmet medical need. Bioprinted skin substitutes are an area of active research, with projects in the EU, such as the 4D-Bioskin project, conducting clinical trials for autologous skin substitutes for burn patients, with production occurring under specific 'hospital exemption' rules within individual countries (e.g., Spain) rather than a full EMA approval. National healthcare systems are responding. These clinical and reimbursement advances transform skin bioprinting from experimental to reimbursable care.

By End User Insights

In 2024, the research organizations and academic institutes segment held the leading share of 65.1% of the Europe 3D bioprinting market. The prominence of the research organizations and academic institutes segment is driven by Europe’s science-led innovation model, where universities serve as primary incubators for bioprinting discovery and standardization. As per sources, notable funds were awarded to academic consortia for bioprinting vascularized tissues, disease modeling, and biofabrication automation. National funding agencies reinforce this ecosystem. This concentration of talent, infrastructure, and public funding ensures academia remains the central node in Europe’s bioprinting value chain.

The hospitals segment is likely to experience the fastest CAGR of 25.1% from 2025 to 2033 due to factors such as the EU’s hospital exemption pathway under the Advanced Therapy Medicinal Products regulation, which permits point-of-care bioprinting for autologous therapies under strict oversight. National health authorities are enabling scale. The evolution of healthcare payment models is prompting hospitals to shift their focus from R&D sites to therapeutic delivery hubs, which establishes this as the highest-growth end-user segment.

COUNTRY LEVEL ANALYSIS

Germany 3D Bioprinting Market Analysis

Germany was the top performer in the Europe 3D bioprinting market and accounted for a 22.5% share in 2024. Its dual excellence in precision engineering and regenerative medicine, anchored in institutions, drives the dominance of the German market. Government funding for bioprinting projects is increasing, with a specific focus on translating research into commercial and clinical applications. Regulatory bodies are streamlining the approval process for bioprinting clinical trials through the establishment of specialized review units. National medical associations are expanding insurance and hospital funding to cover the use of specific bioprinted tissues for therapeutic applications, and the use of autologous bioprinted tissues in clinical settings is leading to improved patient outcomes, specifically a reduction in graft rejection rates. This integration of the regulation industry and clinical care sustains Germany’s dominant position.

France 3D Bioprinting Market Analysis

France followed closely in the Europe 3D bioprinting market and captured a 16.5% share in 2024 because of a coordinated national strategy that links academic excellence with industrial translation under the France 2030 recovery plan. Funding for interdisciplinary bioprinting platforms in France is increasing, with significant investment directed towards oncology and cardiology applications, as per sources. Regulatory guidance is being developed to streamline hospital exemption applications, and bioprinted models are progressing towards use in clinical trials for personalized medicine. French researchers are maintaining a high volume of scientific output in the field. This policy research and clinical alignment ensure France remains a key innovation hub.

United Kingdom 3D Bioprinting Market Analysis

The United Kingdom maintains a notable position in the Europe 3D bioprinting market. Despite its post-Brexit status, the UK maintains leadership through world-class academic centers like the University of Cambridge and Queen Mary University of London. The Medicines and Healthcare products Regulatory Agency pioneered the hospital exemption framework, now emulated across Europe, enabling point-of-care bioprinting. Apart from these, the UK’s Centre for Process Innovation operates a national bioprinting scale-up facility offering GMP manufacturing support to startups. This blend of scientific excellence, regulatory agility, and clinical translation sustains the UK’s prominent role.

Sweden 3D Bioprinting Market Analysis

Sweden is moving ahead steadily in the Europe 3D bioprinting market due to its command in bioink innovation and ethical governance rather than volume. Uppsala University and Chalmers University of Technology pioneered xeno-free and chemically defined bioinks, now adopted across EU trials. As per research, millions of euros were allocated to establish a national bioprinting testbed for regulatory validation under the Swedish Medical Products Agency. Sweden’s progressive stance on animal testing also drives adoption. This focus on material science, regulatory science, and ethics gives Sweden outsized strategic importance.

Netherlands 3D Bioprinting Market Analysis

The Netherlands is expected to grow in the Europe 3D bioprinting market between 2025 to 2033 due to excellence in microfluidics and vascular bioprinting through hubs like TU Delft and the University of Twente. The Netherlands is shifting towards increased investment and collaborative research in developing complex, functional (perfusable) bioprinted tissues for pharmaceutical applications, supported by significant government funding and national consortia. The regulatory landscape for bioprinting in the Netherlands is facilitating the rapid translation of bioprinted medical solutions, such as those for burn care, into clinical practice through streamlined approval pathways like the EU hospital exemption. This specialization in vascularization and regulatory innovation positions the Netherlands as a high-impact niche leader.

COMPETITIVE LANDSCAPE

The Europe 3D bioprinting market features a dynamic mix of homegrown innovators, global entrants, and academic spin-offs competing not on price but on regulatory readiness, scientific credibility, and clinical relevance. Unlike commoditized technology markets, competition here centers on the ability to navigate the EU’s stringent advanced therapy classification and deliver reproducible functional tissues. European players like CELLINK and RegenHU leverage regional expertise in precision engineering and biomaterials, while global firms adapt their platforms to EU standards through local partnerships. The absence of commercialized products creates a pre-competitive environment where collaboration often outweighs rivalry, particularly in vascularization and standardization initiatives. However, as hospital-based therapies gain traction, competition is intensifying around GMP compliance, bioink consistency, and integration with hospital quality management systems. Success increasingly depends on bridging the gap between academic proof of concept and healthcare system adoption.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe 3D bioprinting market include

- 3Dynamic Systems Ltd.

- Organovo Holdings, Inc.

- CELLINK

- Bio3D Technologies

- Advanced Solutions, Inc.

- EnvisionTEC GmbH

- Ourobotics

- 3D Bioprinting Solutions

- BioBots, Inc.

- Poietis

- Cyfuse Biomedical K.K.

- Aerotech, Inc.

- Aspect Biosystems

- GeSIM

- Nano3D Biosciences, Inc.

- regenHU Ltd

- GeSIM

TOP PLAYERS IN THE MARKET

- CELLINK, now operating under the BICO Group, is a pioneering European force in the 3D bioprinting market headquartered in Sweden. The company provides integrated bioprinting platforms, bioinks, and laboratory automation tools used by over one thousand research institutions and biopharmaceutical companies across Europe. It also expanded its GMP-compliant bioink production facility in Gothenburg to support clinical translation under the Advanced Therapy Medicinal Products framework. Globally, CELLINK contributes by setting open standards for bioink characterization and promoting interoperability across bioprinting systems, accelerating adoption in both academic and industrial settings worldwide.

- RegenHU Ltd, based in Switzerland, is a key European innovator specializing in high-precision 3D bioprinters for research and preclinical applications. The company serves leading academic centers and pharmaceutical firms across Germany, France, and the UK with its RGEN and 3D Discovery platforms, known for thermal and pneumatic control accuracy. Globally, RegenHU advances bioprinting reproducibility by contributing to ISO/ASTM standards for biofabrication and exporting its precision engineering ethos to North American and Asian research markets.

- Although headquartered in Canada, Aspect Biosystems has established a strategic European presence through collaborations with academic hospitals and regulatory bodies to advance its therapeutic bioprinting programs. The company’s RX1 bioprinting platform is deployed in clinical research sites across the Netherlands and the UK for tissue-specific applications in metabolic and respiratory diseases. Globally, Aspect bridges discovery and clinical translation by embedding regulatory science into its platform design, enabling scalable therapeutic development across continents.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe 3D bioprinting market prioritize regulatory alignment by designing platforms and bioinks compliant with the EU Medical Devices Regulation and Advanced Therapy Medicinal Products framework. They invest in GMP-certified bioink production and point-of-care bioprinting workflows to support hospital exemption pathways. Strategic partnerships with academic hospitals and Horizon Europe consortia accelerate clinical validation and standardization. Companies actively contribute to European and international biofabrication standards through CEN and ISO to ensure interoperability and quality. Apart from these, they develop multimodal printing technologies and AI-driven process control to enhance reproducibility and meet the demands of complex tissue engineering applications.

MARKET SEGMENTATION

This Europe 3D bioprinting market research report is segmented and sub-segmented into the following categories.

By Component

- 3D Bioprinters

- Microextrusion bioprinting

- Inkjet 3D Bioprinting

- Laser-assisted Bioprinting

- Magnetic 3D Bioprinting

- Other technologies

- Bioinks

- Natural Bioinks

- Hybrid Bioinks

- Synthetic Bioinks

By Application

- Research Applications

- Drug Research

- Regenerative Medicine

- 3D Cell Culture

- Clinical Application

- Skin

- Bone & Cartilage

- Blood Vessels

- Other Clinical Applications

By End User

- Research Organization & Academic Institutes

- Biopharmaceuticals Companies

- Hospital

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the europe 3d bioprinting market?

The europe 3d bioprinting market involves technologies that create three-dimensional biological tissues, driving innovations in regenerative medicine and personalized implants

2. What drives growth in the europe 3d bioprinting market?

Growth is fueled by advances in biomaterials, increased healthcare investments, expansion of tissue engineering research, and rising demand for organ transplantation alternatives

3. Which countries lead the europe 3d bioprinting market?

Germany, the UK, France, and the Netherlands are key hubs due to their robust biotech infrastructure, research funding, and clinical adoption in the europe 3d bioprinting market

4. What applications are common in the europe 3d bioprinting market?

Applications include orthopedic implants, dental scaffolds, wound healing, pharmaceutical testing, and tissue regeneration within europe

5. How do bioinks impact the europe 3d bioprinting market?

Bioinks improve printing precision and biocompatibility, essential for fabricating functional tissues and expanding the europe 3d bioprinting market

6. What role do public-private partnerships play in the europe 3d bioprinting market?

Collaborations accelerate innovation, funding, and clinical trials, fostering growth and market penetration in europe

7. How does regulatory environment affect the europe 3d bioprinting market?

Regulations under EMA and ATMP frameworks impact product approvals and market accessibility within europe

8. What technological trends shape the europe 3d bioprinting market?

Emerging trends include stem cell integration, AI-driven bioprinting, multimaterial printers, and scalable biomanufacturing

9. How important is personalized medicine in the europe 3d bioprinting market?

Personalized implants and tissue constructs meet patient-specific needs, enhancing market demand in europe

10. How are academic institutions contributing to the europe 3d bioprinting market?

Universities lead R&D, pilot projects, and clinical translations, driving market innovation and adoption

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com