Europe Agricultural Drones Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Product, Application, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Agricultural Drones Market Size

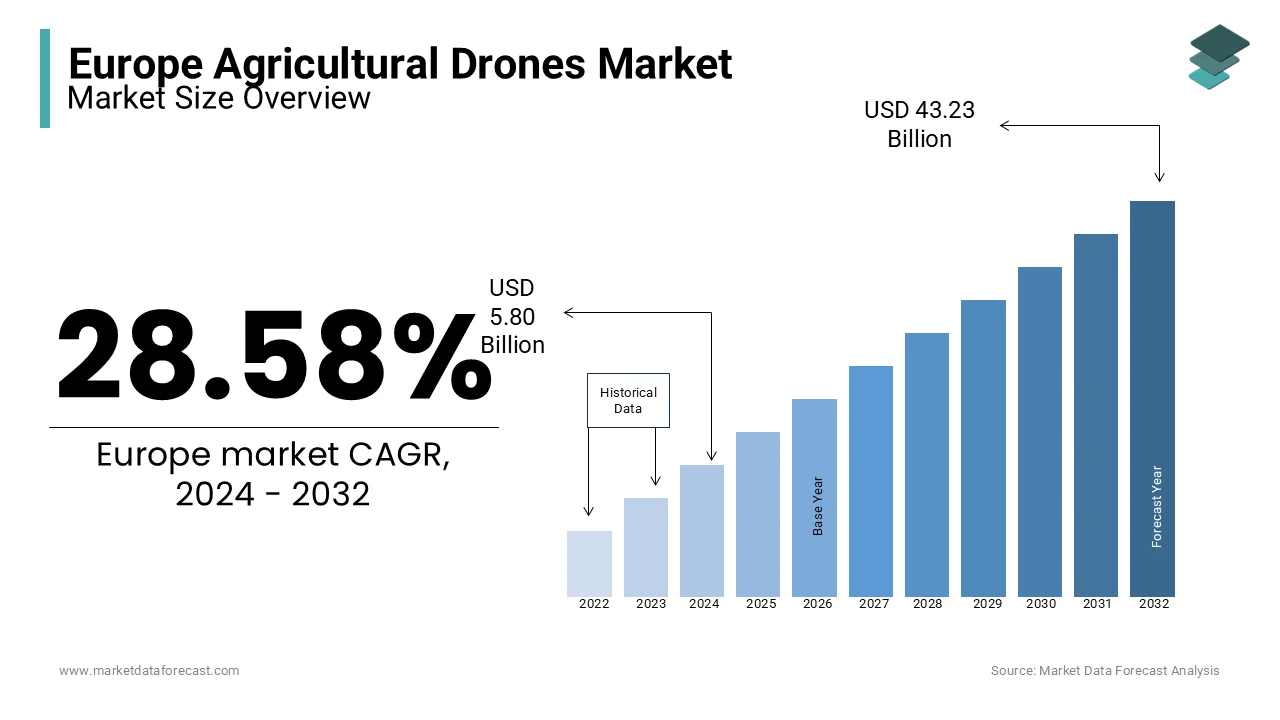

The Europe agricultural drones market size was valued at USD 7.46 billion in 2025 and is anticipated to reach USD 9.59 billion in 2026 to reach from USD 71.66 billion by 2034, estimated to growing at a CAGR of 28.58% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Agriculture Drone Market

Agriculture drone encompasses a specialized sector of unmanned aerial vehicles designed specifically for agronomic applications including crop monitoring precision spraying seeding and livestock management. This industry represents the convergence of advanced robotics artificial intelligence and agronomy to optimize yield while minimizing environmental impact. The definition extends beyond simple flight hardware to include multispectral sensors thermal cameras and variable rate application systems that enable data driven decision making. According to Eurostat, the aging demographic of farm managers in the European Union highlights a critical need for automated solutions to sustain food production. As per the European Commission, agricultural land use efficiency must improve significantly by 2030 to meet sustainability targets under the Green Deal framework. These insights underscore the urgency for adopting aerial technologies that can cover vast areas with high precision. The market is characterized by a diverse ecosystem ranging from small fixed wing units for mapping to heavy lift multirotors for payload delivery. Regulatory bodies across the region are increasingly supporting innovation through funding programs that encourage the transition toward smart farming practices. This technological evolution transforms traditional agriculture into a data intensive industry where drones serve as essential tools for resource conservation and labor supplementation in an era of climate uncertainty.

MARKET DRIVERS

Stringent Environmental Regulations and Precision Input Reduction

The rigorous environmental legislation enforced across the European Union is majorly driving the growth of the European agriculture drone market. The European Green Deal and its Farm to Fork strategy mandate substantial reductions in pesticide and fertilizer usage to protect biodiversity and water quality. According to the European Environment Agency, agricultural runoff remains a leading cause of water pollution, prompting strict limits on chemical applications. Traditional blanket spraying methods are becoming obsolete as they fail to meet these new compliance standards efficiently. As per the Joint Research Centre of the European Commission, precision spraying drones are recognized for their ability to significantly reduce herbicide use by targeting individual weeds rather than entire fields. This level of accuracy is only achievable through advanced computer vision and robotic manipulation which identify and treat plants on a case-by-case basis. Farmers face heavy fines for non-compliance, which is creating a strong financial incentive to adopt technologies that guarantee adherence to regulatory thresholds. Furthermore, consumers increasingly demand residue free produce, pushing retailers to source from farms utilizing low chemical inputs. Drones enable spot treatment of diseases and pests, minimizing ecological footprints while maintaining crop health. The alignment of drone capabilities with legislative goals makes them indispensable tools for modern European agriculture striving for carbon neutrality and resource efficiency.

Acute Labor Shortages and Demographic Shifts in Rural Areas

The severe scarcity of available agricultural workforce is further contributing to the growth of the European agriculture drone market. Rural depopulation and an aging farmer demographic have created a structural deficit in manual labor that threatens food security and operational continuity. According to Eurostat, the number of people employed in agriculture within the European Union has declined significantly over the last decade while the average age of workers continues to rise. Seasonal peaks for harvesting and crop monitoring often go unmet because migrant labor flows have become unpredictable due to changing immigration policies and global health crises. As per the European Federation of Agricultural Workers, many farms in Southern Europe reported operational delays in 2023 due to insufficient field hands. This chronic shortage forces growers to seek reliable alternatives that do not depend on human availability or physical endurance. Drones offer the distinct advantage of operating autonomously over large areas, completing tasks like scouting and spraying in a fraction of the time required by ground crews. Governments are responding by subsidizing automation projects to mitigate the risk of farmland abandonment. The inability to recruit sufficient staff for physically demanding tasks makes investment in autonomous aerial systems not just an option but a necessity for survival. This demographic reality drives sustained demand for machines that can replicate complex human observations with increasing dexterity.

MARKET RESTRAINTS

Complex Regulatory Frameworks and Airspace Restrictions

Navigating the intricate web of aviation regulations and airspace restrictions for unmanned aerial vehicles poses a major restraint on market deployment across diverse European jurisdictions. Agricultural drones often operate in low altitude airspace shared with manned aircraft, emergency services, and private properties, raising concerns about safety and liability. As per the European Union Aviation Safety Agency, the implementation of unified drone rules is still evolving, leading to fragmented national interpretations that complicate cross border operations. Manufacturers and operators face lengthy certification processes to prove that their machines can detect obstacles and fail safely under all conditions. According to the European Machinery Directive, approval timelines for novel agricultural drone systems can extend significantly, delaying market entry and revenue generation. The legal ambiguity regarding responsibility in the event of an accident involving an autonomous drone creates hesitation among farmers and insurance providers. Different member states interpret safety protocols differently, forcing companies to customize products for each jurisdiction which increases development costs. Furthermore, restrictions on beyond visual line of sight flights in many rural areas limit the scalability of drone fleets for large scale farming operations. These regulatory complexities slow down innovation cycles and discourage startups from entering the market due to the high compliance burden. Until harmonized guidelines are fully established, the full potential of agricultural drones remains constrained by bureaucratic inertia.

High Initial Investment Costs and Technical Skill Gaps

The exorbitant upfront cost associated with acquiring advanced agricultural drones equipped with multispectral sensors and precision spraying systems acts as a significant barrier to entry, particularly for small and medium sized farms, which is further hindering the growth of the European agriculture drone market. High technology units require substantial capital expenditure that often exceeds the annual revenue of family owned operations dominating the European landscape. According to the European Investment Bank, professional spraying drones are recognized as high-cost equipment, making them unattainable for many without extensive financing. Interest rate hikes implemented by the European Central Bank to combat inflation have further increased the cost of borrowing, making loans for equipment purchases less attractive. As per the European Association of Agricultural Contractors, many smallholders consider drone automation financially unviable due to long return on investment periods. Additionally, the rapid pace of technological obsolescence creates fear that expensive units will lose value quickly before paying for themselves. The lack of skilled pilots and data analysts in rural areas further compounds the issue as farmers struggle to operate and interpret data from these sophisticated systems. Training programs are scarce and expensive, deterring adoption among older demographics. Without robust subsidy programs or innovative leasing structures, the high price point remains a formidable restraint limiting widespread market penetration across diverse farm sizes.

MARKET OPPORTUNITIES

Expansion of Drone Services in Specialty Crop Cultivation

The cultivation of high value specialty crops such as berries, grapes, and vegetables present a lucrative opportunity for the European agriculture drone market. These crops require careful handling and frequent monitoring which has historically limited automation to broad acre cereals. As per the European Fruit and Vegetable Organization, the fresh produce sector in Europe represents a strong economic case for investing in aerial technologies. Recent advancements in payload capacity and spray nozzle precision allow drones to apply treatments in dense canopies without damaging fragile fruits. According to research institutions in the Netherlands, prototype drones for vineyard management have demonstrated application uniformity comparable to ground tractors while reducing soil compaction. The labour-intensive nature of pruning and thinning vines also offers vast potential for drone assisted monitoring to improve grape quality and reduce labor costs. Growers of organic produce see particular value in drones that can mechanically or chemically remove weeds without heavy machinery, preserving certification status. The shift toward local food systems and urban farming further increases demand for compact drones suitable for greenhouse and vertical farming environments. Companies that develop versatile platforms adaptable to various specialty crops will capture significant market share as growers seek to secure their supply chains against labor volatility.

Integration of Swarm Robotics and Collaborative Farming Models

The emergence of swarm robotics offers another prominent opportunity in the European agriculture drone market. Unlike large heavy machines that cause soil compaction, swarms of lightweight drones can traverse fields simultaneously performing tasks like seeding, monitoring, and spraying with minimal environmental impact. As per the European Commission Horizon Europe program, significant funding is allocated to research projects focusing on cooperative drone fleets that communicate and coordinate actions in real time. Pilot projects in Germany have shown that swarm systems can improve fuel consumption and field coverage efficiency compared to traditional tractors. This model allows farmers to scale operations flexibly by adding or removing units based on seasonal needs without massive capital outlays for single large vehicles. The collaborative nature of these systems enables continuous operation even if individual units require maintenance, ensuring no downtime for critical tasks. Shared ownership models where cooperatives purchase and manage drone fleets provide an accessible entry point for smaller farms. The ability to collect granular data from multiple points simultaneously enhances decision making regarding irrigation and fertilization. Embracing swarm intelligence positions the market to address scalability and sustainability challenges simultaneously, opening new avenues for service-based agriculture.

MARKET CHALLENGES

Technical Limitations in Unstructured and Dynamic Field Environments

Operating autonomous drones in the unpredictable and unstructured conditions of real-world farms is a significant challenge to the growth of the European agriculture drone market. Agricultural fields vary significantly in terrain, slope, wind patterns, and obstacle density, making consistent navigation difficult for current sensor suites. As per the Joint Research Centre of the European Commission, dust, rain, and varying light conditions frequently interfere with lidar and camera systems, causing localization errors and operational failures. Field trials across France and Italy indicate that autonomy levels drop during adverse weather, forcing human intervention to resume tasks. The complexity of identifying crops versus weeds in dense foliage or distinguishing ripe fruit from leaves remains a computationally intensive problem that strains onboard processing capabilities. Battery life limitations further restrict the duration of continuous operation, requiring frequent recharging which disrupts workflow efficiency. The lack of robust connectivity in remote rural areas impedes real time data transmission and remote monitoring capabilities essential for fleet management. Developing algorithms that can adapt to every possible scenario without explicit programming requires vast datasets that are often unavailable for specific regional crops. Until drones can match the adaptability of human workers in chaotic environments, trust in their reliability will remain limited among practical farmers.

Data Privacy Concerns and Cybersecurity Vulnerabilities

The increasing reliance on connected drone systems generates vast amounts of sensitive farm data, which is raising critical issues regarding privacy, ownership, and cybersecurity threats and further challenging the expansion of the European agriculture drone market. Autonomous drones collect detailed information on yield patterns, soil health, and operational practices which constitutes valuable intellectual property for farmers. As per the European Data Protection Board, there is growing apprehension about how this data is stored, shared, and potentially exploited by technology providers or third parties without explicit consent. Data breaches could expose proprietary farming strategies or allow malicious actors to hijack drone fleets, causing physical damage or crop destruction. According to the European Union Agency for Cybersecurity, attacks on critical infrastructure including agricultural systems are on the rise, highlighting the vulnerability of interconnected devices. Farmers fear that sharing data might lead to unfavorable market positioning if competitors or commodity traders access their production forecasts. The lack of clear legal frameworks defining data ownership rights creates uncertainty and hesitancy in adopting fully connected solutions. Ensuring end to end encryption and secure communication protocols adds complexity and cost to drone design. Building trust requires transparent data governance policies and robust security architectures that protect farmer interests. Without addressing these digital risks, the full integration of smart drones into the agricultural ecosystem faces significant resistance from cautious stakeholders.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 28.58% |

| Segments Covered | By Product, Application, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Trimble Navigation Ltd., DJI Technology, 3D Robotics, PrecisionHawk, AeroVironment, Inc., Parrot SA, and DroneDeploy. |

SEGMENT ANALYSIS

By Product Insights

By Product Insights

The hardware segment dominated the market by commanding for the leading share of the European agriculture drone market in 2025. The leading position of hardware segment in the European market is driven by the fundamental necessity of physical aerial platforms to execute any agronomic task and the widespread adoption of rotary blade drones which offer superior maneuverability and vertical takeoff capabilities essential for operating in the fragmented and often irregularly shaped fields common across European landscapes. According to the European Union Aviation Safety Agency, multirotor configurations are the most widely authorized for agricultural drone operations because their ability to hover allows for precise spot spraying and detailed low altitude imaging that fixed wing units cannot match. The second major driver is the continuous technological advancement in battery energy density and payload capacity which has enabled hardware to carry heavier multispectral sensors and larger liquid tanks for extended flight durations. As per the European Agricultural Machinery Industry Association, heavy lift drones capable of carrying larger payloads are increasingly being adopted as farmers seek to replace manual labor with automated spraying solutions. The durability of modern carbon fiber frames also ensures longevity in harsh outdoor conditions, reducing the total cost of ownership for professional operators. Furthermore, the modularity of current hardware designs allows users to swap between cameras and sprayers, maximizing the utility of a single investment. These functional advantages and the tangible nature of the asset solidify the leading position of hardware in the regional market structure.

The software segment is projected to register the highest CAGR of 25.5% in the European agriculture drone market over the forecast period owing to the increasing realization that raw data collection is useless without sophisticated processing and actionable insights and the shift toward precision agriculture where decisions regarding irrigation, fertilization, and pest control rely entirely on complex algorithms interpreting multispectral and thermal imagery. As per the European Commission Digital Europe Programme, investments in agri tech software solutions have grown significantly as farmers seek to integrate drone data with existing farm management systems. Industry analysts highlight that the demand for autonomous flight planning software has surged because it enables beyond visual line of sight operations, which are critical for covering large estates efficiently without requiring highly skilled pilots for every mission. The emergence of artificial intelligence powered analytics allows for real time disease detection and yield prediction, transforming drones from simple cameras into diagnostic tools. Additionally, the rise of subscription-based models for cloud storage and data analysis makes advanced capabilities accessible to smaller farms that cannot afford expensive upfront licenses. The ability of software to provide regulatory compliance reporting and automated logkeeping further accelerates adoption among professional service providers. The convergence of big data and machine learning positions software as the most rapidly expanding component of the agriculture drone ecosystem.

By Application Insights

The crop scouting segment held the dominant position in the Europe agriculture drone market in 2025. The dominance of crop scouting segment in the European market is attributed to the critical need for early detection of plant stress, diseases, and nutrient deficiencies to maximize yields and the unparalleled ability of drones equipped with multispectral sensors to capture data invisible to the human eye, allowing agronomists to identify issues before they become visually apparent. According to the Joint Research Centre of the European Commission, monitoring and scouting activities represent the majority of agricultural drone flights because early intervention can significantly reduce crop losses. The cost effectiveness of aerial scouting compared to traditional ground-based sampling that is labor intensive and often provides incomplete spatial coverage is also contributing to the growth of the crop scouting segment in the European market. As per the European Federation of Agricultural Contractors, farms utilizing drone-based scouting have reported substantial reductions in field inspection time while increasing the accuracy of their treatment plans. The integration of normalized difference vegetation index maps generated by drones enables precise variable rate application of inputs, ensuring resources are only applied where needed. Furthermore, the non-invasive nature of drone scouting prevents soil compaction and crop damage associated with heavy machinery traversing wet fields. The universal applicability of scouting across all crop types from cereals to vineyards ensures consistent demand throughout the growing season. These efficiency gains and yield protection benefits secure the top spot for crop scouting in the application landscape.

The crop spraying segment is anticipated to witness the fastest CAGR of 28.8% over the forecast period owing to the urgent regulatory pressure to reduce chemical usage and the severe shortage of manual labor for pesticide application and the unique capability of spraying drones to apply pesticides, herbicides, and fertilizers with centimeter level precision, thereby minimizing drift and environmental contamination. As per the European Food Safety Authority, the push to cut synthetic pesticide use under the Farm to Fork strategy has made precision spraying technology indispensable for compliant farming. Data from national agricultural ministries in France and Germany indicates that approvals for drone spraying operations have increased as regulators recognized the environmental benefits over tractor based broadcasting. The ability of drones to operate in wet or steep terrain where ground vehicles cannot access opens new areas for treatment, ensuring complete field coverage. Moreover, the reduction in water usage required for drone spraying compared to traditional boom sprayers addresses growing concerns about water scarcity in Southern Europe. The development of larger capacity tanks and faster charging stations has improved the economic viability of drone spraying for large scale operations. The synergy between environmental mandates and operational efficiency propels crop spraying to the forefront of market growth.

COUNTRY LEVEL ANALYSIS

Germany Agriculture Drone Market Analysis

Germany led the agriculture drone market in Europe in 2025 commanding for the highest share of the regional market. The leading position of Germany in the European market is driven by its robust engineering sector and progressive approach to integrating automation in farming. The nation serves as the primary testing ground for advanced drone technologies with strict yet clear regulations that foster innovation while ensuring safety. According to the German Federal Ministry of Food and Agriculture, a significant portion of large-scale arable farms in Germany have adopted drone-based scouting or spraying solutions to comply with stringent environmental laws. The country's strong manufacturing base supports the local production of high precision sensors and reliable airframes tailored for European conditions. As per the German Aerospace Center, government funding for agricultural robotics research has reached record levels, accelerating the development of autonomous swarm capabilities. The acute labor shortage in rural German regions further drives the adoption of automated solutions to maintain productivity. Farmers in Germany prioritize data security and quality, leading to high demand for premium hardware and sophisticated analysis software. The presence of major tech companies and research institutes creates a collaborative ecosystem that rapidly translates theoretical advancements into practical field applications. The combination of regulatory clarity, technological expertise, and economic necessity solidifies Germany's position as the dominant force in the regional market.

France Agriculture Drone Market Analysis

France captured the second largest position in the Europe agriculture drone market in 2025. The growth of France in the European market can be credited to its vast agricultural land area and specialized viticulture sector. The country is a global leader in wine production, which has become a key adopter of drone technology for managing steep slopes and dense canopy structures where traditional machinery fails. As per the French National Institute for Agriculture, Food and Environment, vineyards are increasingly monitored or treated using drones to reduce soil compaction and improve grape quality. The French government actively promotes agroecology through subsidies that encourage the adoption of precision spraying drones to minimize chemical runoff into waterways. According to the Ministry of Agriculture, the number of certified drone operators in the agricultural sector has grown significantly, driven by demand from cooperative wineries and large cereal growers. The diversity of French agriculture, ranging from extensive wheat fields to intensive horticulture, creates a broad demand spectrum for different drone types. Research clusters in regions like Bordeaux and Champagne foster collaboration between startups and established manufacturers to develop tailored solutions. The emphasis on preserving terroir while enhancing efficiency makes France a unique and vital market for specialized agricultural drones.

United Kingdom Agriculture Drone Market Analysis

The United Kingdom retains a prominent spot in the Europe agriculture drone market due to a strong tradition of agricultural innovation and a pressing need to address post-Brexit labor challenges. British farmers are increasingly turning to autonomous drone solutions for arable crops and livestock management to mitigate the loss of seasonal workers and rising labor costs. As per the Agriculture and Horticulture Development Board, adoption of drone-based crop scouting in the UK arable sector has increased significantly as growers seek to optimize input usage and reduce costs. The UK government has launched various grants under its farming innovation program to support the trial and deployment of robotic technologies on commercial farms. According to the Department for Environment, Food and Rural Affairs, investment in agri-tech startups focusing on drone analytics has surged, attracting significant venture capital. The diverse landscape of the UK, from rolling hills to flat fenlands, requires versatile drones capable of navigating varied terrains. The strong presence of leading universities drives research into AI-driven decision support systems and automated flight paths. The urgency to maintain food security while meeting net zero targets create a favorable environment for rapid drone adoption. These factors combine to make the UK a dynamic and growing market for agricultural automation.

Spain Agriculture Drone Market Analysis

Spain is estimated to account for a notable share of the European agriculture drone market over the forecast period owing to its extensive arid regions where water conservation and efficient resource management are critical survival strategies for farmers. The Spanish market is characterized by a high adoption of drones for monitoring irrigation systems and detecting water stress in crops such as olives, almonds, and citrus fruits. According to agricultural extensions, water scarcity issues have driven increased use of thermal imaging drones to optimize irrigation schedules. The warm climate allows for year-round drone operations, making the return on investment faster compared to northern European countries. As per the National Statistics Institute, the expansion of intensive agriculture in regions like Andalusia has created strong demand for precision spraying to manage pests without excessive chemical use. The rise of large-scale industrial farming operations in Spain facilitates the economies of scale needed to justify investments in advanced drone fleets. Government initiatives to modernize the agricultural sector include specific lines of credit for purchasing precision agriculture equipment. The combination of climatic necessity, technological readiness, and supportive policy ensures Spain remains a key growth engine for the European drone market.

Italy Agriculture Drone Market Analysis

Italy represents a key market in Southern Europe. The extensive orchard and vineyard sectors that require specialized drone solutions for delicate harvesting and monitoring tasks is driving the Italian market expansion. The Italian agricultural landscape is characterized by fragmented land holdings and hilly terrain, which poses unique challenges that traditional large machinery cannot address effectively. According to the Italian National Institute of Statistics, the value of fruit and vegetable production creates a strong economic incentive for investing in selective monitoring and spraying drones. The shortage of seasonal pickers has reached critical levels, prompting growers in regions like Emilia Romagna and Puglia to pilot autonomous systems for crop health assessment. As per the Confederation of Italian Farmers, interest in drone-based pest management has grown significantly as labor costs continue to rise. Italian manufacturers are leveraging their design expertise to create compact and agile drones suited for narrow rows and steep slopes. Government incentives for modernizing agricultural equipment further stimulate market activity. The focus on maintaining high quality standards for protected designation of origin products drives the need for gentle and precise monitoring technologies. Italy's specific agronomic needs ensure a distinct and valuable niche within the broader European drone market.

COMPETITIVE LANDSCAPE

The competition in the Europe agriculture drone market is characterized by intense rivalry between established global giants and agile regional specialists who vie for dominance through technological innovation and regulatory adherence. Large incumbents leverage their extensive manufacturing capabilities and brand reputation to offer integrated hardware and software solutions while newer entrants often focus on niche applications such as specialized sensing or custom data analytics. The landscape is highly dynamic with companies constantly striving to improve flight endurance payload capacity and autonomous navigation algorithms to meet the demanding conditions of European farms. Regulatory compliance regarding airspace safety and data privacy acts as a significant barrier to entry ensuring that only well capitalized entities with robust quality assurance systems can thrive. Price competition remains fierce particularly in the scouting segment where margin pressures force manufacturers to optimize production costs continuously. Strategic alliances between drone makers and agrochemical companies are becoming increasingly common as firms seek to offer comprehensive precision farming packages rather than isolated devices. This competitive environment fosters rapid technological advancement and benefits end users through improved productivity and sustainability across the region.

KEY MARKET PLAYERS

A few of the market players in the Europe agricultural drones market include

- Trimble Navigation Ltd.

- DJI Technology

- Airinov (France)

- senseFly (Switzerland)

- 3D Robotics

- PrecisionHawk

- AeroVironment, Inc.

- Parrot SA

- DroneDeploy.

Top Players In The Market

- DJI Agriculture stands as a global pioneer in unmanned aerial systems delivering advanced spraying and spreading drones that redefine precision farming efficiency worldwide. The company contributes significantly to the international market by setting benchmarks for payload capacity flight stability and intelligent obstacle avoidance tailored for diverse agricultural environments. Recently DJI has strengthened its position in Europe by launching next generation agronomic drones equipped with enhanced radar systems for operation in complex terrains like vineyards and orchards. Their strategic focus involves integrating seamless data connectivity between drones and farm management software to optimize variable rate application processes. The firm actively collaborates with European distributors to provide comprehensive training programs ensuring safe and compliant operations under local aviation rules. By continuously refining battery technology and spray nozzle precision DJI ensures its platforms reduce chemical usage while maximizing crop yields. This commitment to innovation and operational reliability solidifies their status as a leading force in transforming traditional farming into high tech digital enterprises across the continent.

- Delair Tech operates as a French specialist in professional fixed wing drones designed specifically for large scale agricultural mapping and detailed crop monitoring applications. The company plays a vital role in the global market by offering long endurance unmanned aerial vehicles capable of covering vast hectares in a single flight with centimetre level accuracy. Recent actions to strengthen its market position include the development of advanced multispectral sensors that integrate directly with popular agronomic software platforms for immediate data analysis. Delair Tech has expanded its service network across Europe to ensure rapid support and maintenance for commercial operators managing extensive farmlands. Their focus on creating ruggedized drones suited for harsh weather conditions addresses the specific needs of European farmers facing unpredictable climates. The firm prioritizes regulatory compliance by designing systems that meet strict European Union Aviation Safety Agency standards for beyond visual line of sight flights. By providing turnkey solutions that combine hardware software and analytics Delair Tech enhances decision making capabilities for agronomists and large estate managers throughout the region.

- Parrot Drone SAS serves as a prominent European manufacturer renowned for producing lightweight and versatile drones tailored for precision agriculture and environmental monitoring. The company contributes extensively to the global market by empowering farmers with accessible tools for crop health assessment and targeted intervention strategies. Recently Parrot has strengthened its position by introducing new software suites that leverage artificial intelligence to automatically detect plant stress and generate prescription maps for variable rate application. Their latest innovations include robust quadcopters with extended battery life and high-resolution thermal cameras ideal for irrigation management and livestock monitoring. Parrot actively partners with agricultural cooperatives and research institutions across France and Germany to validate drone efficacy in real world farming scenarios. The firm prioritizes data sovereignty by ensuring all collected information remains secure and compliant with European privacy regulations. By driving the adoption of user friendly yet powerful aerial technologies Parrot SAS positions itself at the forefront of the sustainable agriculture revolution ensuring efficient resource use for a growing population.

Top Strategies Used By Key Market Participants

Key players in the Europe agriculture drone market primarily employ strategic partnerships and localized compliance initiatives to accelerate technology adoption and navigate complex regulatory landscapes effectively. Manufacturers actively collaborate with agricultural cooperatives and research institutes to validate drone performance in diverse European cropping systems and build trust among conservative farming communities. Another major strategy involves investing heavily in proprietary software ecosystems that integrate aerial data with existing farm management platforms to provide actionable insights for precision application. Companies are increasingly focusing on developing beyond visual line of sight capabilities and autonomous flight features to address severe labor shortages and improve operational efficiency. Expanding service networks and training centers in rural areas ensures reliable maintenance and skilled pilot availability which are critical for widespread deployment. Furthermore, firms are pursuing sustainability certifications to align their products with strict European environmental regulations and appeal to eco conscious consumers. These combined approaches enable market participants to overcome barriers and capture growth opportunities in a rapidly evolving sector.

MARKET SEGMENTATION

This research report on the europe agricultural drones market is segmented and sub-segmented into the following categories.

By Product Insights

-

Hardware

- fixed-wing,

- rotary blade

- hybrid whereas

- Software

- data management

- imaging software

- data analysis.

By Application

- field mapping

- variable rate application

- crop scouting

- crop spraying

- livestock

- agriculture photography

- others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe agricultural drones market?

The Europe agricultural drones market includes sales and use of unmanned aerial vehicles (UAVs) designed for farming tasks such as crop monitoring, spraying, mapping, and data collection to improve precision agriculture outcomes.

Why are agricultural drones important for farming?

Agricultural drones improve crop surveillance, irrigation management, pest detection, fertilizer/pesticide application, and yield prediction, enabling more efficient, data-driven farm decisions.

What drives growth in the Europe agricultural drones market?

Market growth is driven by precision farming adoption, labor shortages, rising food demand, government modernization incentives, and advanced imaging and analytics technologies.

What tasks do drones perform in agriculture?

Drones are used for field mapping, crop health monitoring, plant stress detection, spraying of inputs, soil analysis, and livestock tracking, increasing accuracy and reducing input waste.

What technologies are commonly used in agricultural drones?

Key technologies include multispectral and thermal cameras, GPS/GNSS, AI analytics, machine learning, IoT connectivity, and real-time data platforms.

Which crops benefit most from agricultural drones?

Drones are used across row crops (wheat, corn, barley), vegetables, vineyards, orchards, rice, and high-value specialty crops for detailed monitoring and input application.

How do drones support sustainable agriculture?

Drones enable precise application of water, fertilizers, and pesticides, lowering chemical overuse, reducing waste, conserving water, and supporting environmental stewardship.

Which regions in Europe are key markets for agri-drones?

Major markets include Western Europe (Germany, France, UK, Spain, Italy) due to advanced precision agriculture adoption, supportive policies, and strong farming infrastructures.

What challenges does the Europe agricultural drones market face?

Challenges include regulatory restrictions on flight, high upfront costs, pilot training needs, data integration complexity, and rural connectivity issues.

How do regulations impact agricultural drone use?

EU and national rules govern flight altitudes, no-fly zones, pilot certification, data privacy, and safety standards, influencing adoption pace and operational flexibility.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com