Europe AI Data Center Market Size, Share, Trends, and Growth Analysis Report, Segmented by Data Center Type, Component, Tier Standard, End-user Industry, and Country – Industry Forecast From 2026 to 2034

Europe AI Data Center Market Size

The Europe AI data center market was valued at USD 17.45 billion in 2025, is estimated to reach USD 21.75 billion in 2026, and is projected to reach USD 126.96 billion by 2034, growing at a CAGR of 24.67% from 2026 to 2034. The rapid expansion of the market is driven by increasing adoption of artificial intelligence across industries, rising demand for high-performance computing, and the growing deployment of cloud-based AI infrastructure. Organizations are investing heavily in AI data centers to support machine learning, generative AI, big data analytics, and real-time processing workloads. Additionally, strong government initiatives to strengthen digital sovereignty, expansion of hyperscale cloud infrastructure, and increasing enterprise reliance on AI-powered applications are accelerating the growth of AI data center investments across Europe.

Key Market Trends

- Rising demand for AI infrastructure to support generative AI, machine learning, and advanced analytics workloads.

- Increasing expansion of hyperscale and cloud-based AI data centers across major European economies.

- Growing investments in GPU-accelerated computing and specialized AI hardware infrastructure.

- Strong government focus on digital sovereignty, AI innovation, and local data processing capabilities.

- Increasing enterprise adoption of AI-driven automation, predictive analytics, and intelligent applications.

Segmental Insights

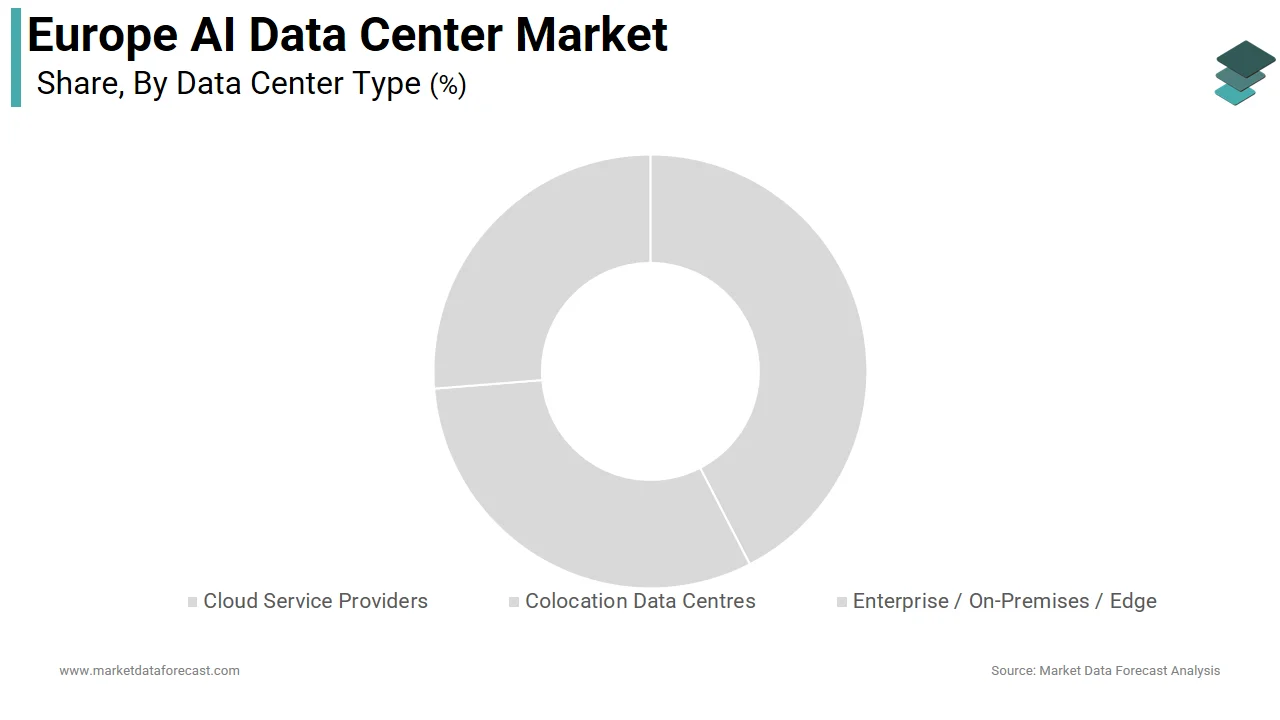

- Based on data center type, the cloud service providers segment dominated the Europe AI data center market by accounting for a 54.9% share in 2025, driven by the rapid expansion of hyperscale cloud platforms and increasing demand for scalable AI computing infrastructure.

- Based on component, the software segment held a significant share of 41.6% in 2025, supported by the growing adoption of AI frameworks, orchestration tools, and data management platforms required for efficient AI model training and deployment.

- Based on end-user industry, the IT and ITES segment led the Europe AI data center market by capturing a 34.3% share in 2025, driven by the increasing use of AI for automation, cloud services, cybersecurity, and digital transformation initiatives.

Regional Insights

The Europe AI data center market is witnessing strong growth across major economies, supported by increasing AI adoption, expanding cloud infrastructure, and strategic investments in digital and AI capabilities.

- Germany dominated the Europe AI data center market in 2025, supported by its strong industrial base, advanced digital infrastructure, and growing investments in AI research and hyperscale data center facilities.

- The United Kingdom held the second-largest position in the Europe AI data center market in 2025, driven by its leadership in AI innovation, strong cloud ecosystem, and presence of major hyperscale cloud providers.

- France is emerging as a rapidly growing market for AI data centers, supported by its national AI strategy, strong government funding, and focus on building sovereign AI infrastructure.

Competitive Landscape

The Europe AI data center market is highly competitive, with major global technology companies and semiconductor manufacturers investing heavily in AI infrastructure, high-performance computing, and specialized AI hardware. Companies are focusing on expanding hyperscale data center capacity, developing advanced AI processors, and strengthening cloud-based AI platforms to meet growing enterprise demand.

Leading companies operating in the Europe AI data center market include NVIDIA, Microsoft, Advanced Micro Devices, Intel, Arm, Google, Equinix, and Graphcore.

Europe AI Data Center Market Size

The size of the Europe AI data center market was worth USD 17.45 billion in 2025. The regional market is anticipated to grow at a CAGR of 24.67% from 2026 to 2034 and be worth USD 126.96 billion by 2034 from USD 21.75 billion in 2026.

The AI data center refers to specialized computing infrastructure engineered to support the immense computational, storage, and cooling demands of artificial intelligence workloads, including large language model training, real-time inference, and multimodal data processing. Unlike conventional data centers, these facilities feature high-density GPU or ASIC clusters, ultra-low latency networking, and advanced liquid cooling systems tailored for sustained AI operations. The market operates within a unique regulatory and environmental framework shaped by the EU Code of Conduct for Data Centre Energy Efficiency, the Corporate Sustainability Reporting Directive, and national grid constraints. According to Eurostat, data centers consumed a notable portion of the EU’s total electricity in 2024, with AI workloads representing a significant share despite accounting for a relatively small fraction of the total server count. As per the European Environment Agency, the average power usage effectiveness of new AI data centers is lower compared to legacy facilities, although absolute energy consumption remains a concern due to scale. According to the European Commission’s Net Zero Industry Act, all new data centers above 5 megawatts must disclose carbon intensity and water usage starting in 2025. This convergence of technological intensity, sustainability mandates, and strategic digital sovereignty defines the evolution of Europe’s AI data center landscape.

MARKET DRIVERS

Surge in Sovereign AI Initiatives Drives National Infrastructure Investment

European governments are accelerating investment in domestic AI data centers to ensure strategic autonomy in foundational model development and sensitive data processing, which is a key factor propelling the growth of the European AI data center market. According to the European Commission, many member states launched national AI strategies in 2024 that include dedicated compute infrastructure for public sector and research use. As per GENCI, France expanded its AI partition to support national projects such as Mistral AI and public health modeling. According to the Gauss Alliance, Germany allocated significant funding to build sovereign AI data centers in Bavaria, Baden-Württemberg, and North Rhine-Westphalia. As per the UK’s AI Research Resource, the country committed substantial investment to deploy GPU clusters across Cambridge, Edinburgh, and Bristol. According to the European High Performance Computing Joint Undertaking, several AI-specific data centers were funded under the EuroHPC program with a combined capacity exceeding previous benchmarks. These initiatives aim to reduce reliance on US cloud providers for critical applications in defense, healthcare, and climate science while ensuring compliance with GDPR and the EU AI Act. This state-led push creates a structural demand for secure, high-performance infrastructure insulated from global geopolitical tensions.

Enterprise Adoption of Generative AI Fuels Hyperscaler Expansion

The rapid integration of generative AI into corporate workflows has triggered unprecedented demand for scalable cloud-based AI infrastructure across European industries, which is further boosting the expansion of the European AI data center market. According to the European DIGITAL SME Alliance, a majority of large enterprises deployed at least one generative AI application in 2024, ranging from customer service chatbots to design copilots. Financial institutions such as BNP Paribas and ING now run proprietary large language models for risk analysis and document processing, requiring dedicated GPU instances. Automotive OEMs, including Volkswagen and Stellantis, use AI data centers for autonomous driving simulation and factory optimization. As per announcements from Microsoft Azure, Google Cloud, and AWS, billions of euros in new AI data center investments were committed across Europe in 2024. According to Microsoft, its AI hub in Amsterdam will house large GPU clusters by 2026, while AWS expanded its Tallinn region with an AI-optimized availability zone. This enterprise-driven demand ensures sustained hyperscaler growth even as public cloud markets mature, creating a dual engine of innovation and scale in the European AI infrastructure ecosystem.

MARKET RESTRAINTS

Stringent Grid Capacity Limits Delay Project Approvals

The availability of reliable high-capacity electrical connections has become a critical bottleneck for AI data center development across Europe, which is impeding the regional market growth. According to the European Network of Transmission System Operators for Electricity, only a small proportion of requested grid connections for data centers were approved in 2024 due to congestion and renewable integration priorities. As per EirGrid, Ireland imposed a moratorium on new data center connections in Dublin after they consumed a significant share of the capital’s electricity. Similarly, according to TenneT, the Netherlands rejected multiple data center grid applications in 2024, citing insufficient transmission capacity in the Randstad region. As per Germany’s Federal Network Agency, permitting timelines for new substations now exceed previous benchmarks. Without a guaranteed power supply, operators cannot commit to long-term leases or hardware deployment. This infrastructure gap forces hyperscalers to relocate projects to regions such as Sweden or Finland, where hydropower and grid headroom exist, but increases latency for core European markets. Until grid modernization accelerates through the EU’s Grid Action Plan, AI data center growth will remain constrained by physical energy limits rather than market demand.

Water Scarcity Regulations Restrict Cooling System Deployment

The high-water consumption of advanced cooling systems required for AI data centers faces growing restrictions in water-stressed regions of Southern and Western Europe, which further hamper the expansion of the European AI data center market. According to the European Environment Agency, a single large AI data center using evaporative cooling can consume water volumes equivalent to the needs of hundreds of thousands of people annually. In response, Spain’s Ministry for Ecological Transition banned new water-intensive data centers in Catalonia and Madrid in 2024. Similarly, France’s Loire Basin authority denied cooling permits for proposed facilities near Paris due to drought conditions. As per Dutch regulations, all new data centers must achieve zero water withdrawal for cooling through closed-loop liquid or direct chip cooling. While these technologies exist, they increase capital costs significantly, as per the European Data Centre Association. Without access to abundant water or investment in alternative cooling, AI operators must either pay premium prices for dry cooling or relocate to Nordic countries, fragmenting the market and increasing latency for end users in high-demand urban centers.

MARKET OPPORTUNITIES

Integration of AI Data Centers with Renewable Energy Microgrids Creates Green Premium Segment

The development of co-located renewable energy microgrids presents a strategic opportunity for the European AI data center market. According to the International Energy Agency, hyperscalers signed 8.2 gigawatts of corporate power purchase agreements for wind and solar in Europe in 2024, the highest on record. Microsoft’s AI data center in Denmark sources 100 %of its power from offshore wind via a dedicated subsea cable, while Google’s Finnish facility uses geothermal and biomass. The European Investment Bank allocated 1.5 billion euros in 2024 to support hybrid renewable data centers that combine solar PV battery storage and grid backup. These projects not only reduce carbon intensity but also qualify for tax incentives under national green industrial policies. As the EU’s Corporate Sustainability Reporting Directive mandates Scope 2 emissions disclosure by 2025, clean-powered AI infrastructure becomes a competitive differentiator for both cloud providers and their enterprise customers seeking to meet net zero targets.

Deployment of Edge AI Micro Data Centers in Urban Cores Enables Low Latency Applications

The emergence of compact high-density micro data centers in city centers offers a transformative opportunity for the European AI data center market. According to the European Telecommunications Standards Institute, over 400 edge AI nodes were deployed across Berlin, Paris, and Milan in 2024, each occupying less than 20 square meters, yet delivering 5 petaflops of inference capacity. Telecom operators like Deutsche Telekom and Orange integrate these units into 5G base stations, enabling sub-10 millisecond response times for industrial robotics and augmented reality. The European Commission’s Digital Europe Programme funded 120 million euros for urban AI edge infrastructure in 2024, focusing on hospitals and transport hubs. These micro facilities use immersion cooling and modular design to overcome space and noise constraints in dense environments. By bringing AI compute closer to data sources, they reduce bandwidth pressure on core networks and enable new classes of real-time intelligent services that centralized clouds cannot support.

MARKET CHALLENGES

Fragmented National AI Compute Policies Undermine EU-Wide Scale Economies

Despite the Digital Europe Programme, Europe lacks a harmonized strategy for AI data center development, leading to inefficient resource allocation and duplicated investments, which is challenging the growth of the European AI data center market. According to the European Court of Auditors, only 9 of 27 member states have published clear criteria for allocating public AI compute resources, creating market distortion. France prioritizes sovereign cloud, while Germany funds regional clusters, and the Netherlands focuses on commercial hyperscalers. This fragmentation prevents the creation of a unified European AI compute fabric that could rival US or Chinese scale. The European Commission’s 2024 review found that national AI data centers operate at only 45 %average utilization due to a lack of interoperability and workload-sharing protocols. Without common standards for API security and data governance, Europe’s AI infrastructure remains a patchwork of isolated islands, resulting in increasing costs for researchers and enterprises while weakening strategic competitiveness in foundational model development.

High Cost of Skilled AI Infrastructure Talent Constrains Operational Maturity

The scarcity of engineers skilled in AI-specific data center operations poses a significant barrier to efficient deployment and scaling, which is further challenging the expansion of the European AI data center market. According to the European Institute for Innovation and Technology, there is a shortfall of over 180000 AI infrastructure specialists across the EU as of 2024, with Germany, France, and the Netherlands experiencing the most acute gaps. Academic programs remain focused on software AI rather than hardware infrastructure, leaving graduates unprepared for roles in thermal design, power distribution, and fault tolerance. As per a 2024 survey by the European Data Centre Association, 72 %of operators delayed AI cluster commissioning due to the inability to hire staff capable of tuning NVIDIA DGX SuperPOD configurations or managing optical interconnects. This talent bottleneck not only extends time to value but also increases reliance on costly vendor professional services, raising total cost of ownership by up to 35 %and discouraging mid-sized firms from building dedicated AI infrastructure despite clear business need.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Data Center Type, Component, Tier Standard, End-user Industry, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | NVIDIA Corporation, Microsoft Corporation, Advanced Micro Devices, Inc., Intel Corporation, Arm Ltd., Google Inc., Equinix, Graphcore Ltd., and Others. |

SEGMENTAL ANALYSIS

By Data Center Type Insights

The cloud service providers segment dominated the European AI data center market in 2025 with 54.9% of the regional market share. This segment's leadership is primarily driven by the massive investments from hyperscalers like Microsoft, Google, and Amazon Web Services, who are building dedicated AI infrastructure across the region. These companies require vast, scalable, and highly efficient facilities to train and run complex AI models, which only their own cloud platforms can provide at the necessary scale and performance. The European Union's push for digital sovereignty has also led to strategic partnerships between these global cloud providers and local entities to establish sovereign cloud offerings, further consolidating their market position. The sheer volume of data generated by European businesses and consumers, coupled with the need for low-latency AI services, creates an environment where the economies of scale and technical expertise of Cloud Service Providers are unmatched.

The colocation data centers segment is expected to register a CAGR of 14.4% over the forecast period in this regional market. This rapid growth is fueled by enterprises that want to leverage AI but lack the capital or expertise to build their own facilities. Colocation providers offer a compelling alternative by providing access to high power density racks, advanced cooling solutions, and robust connectivity in prime locations. This model allows businesses to deploy AI workloads quickly and cost effectively while maintaining physical control over their hardware. The rise of specialized AI chipsets that require unique power and thermal management has also made the flexible, carrier neutral environment of colocation centers highly attractive for a new wave of AI startups and research institutions.

By Component Insights

The software component segment commanded a significant share of 41.6% in the European AI data center market in 2025. This dominance stems from the critical role software plays in managing the unprecedented complexity of AI infrastructure. AI workloads demand sophisticated orchestration, resource scheduling, and workload management tools that can efficiently allocate computing power across thousands of GPUs. Furthermore, the entire AI lifecycle from data preparation and model training to deployment and monitoring is governed by a suite of specialized software platforms. The shift towards software defined infrastructure, where compute, storage, and networking resources are abstracted and managed through code, has made software the central nervous system of the modern AI data center. This trend is amplified by the need for seamless integration between different hardware vendors and cloud environments, a challenge that is solved primarily through software layers.

The hardware component segment is the fastest growing segment and is poised to expand at a remarkable CAGR of 25.5% over the forecast period in this regional market owing to the insatiable demand for specialized AI chips, primarily Graphics Processing Units and newer AI accelerators. The computational requirements for training large language models and other advanced AI systems have skyrocketed, necessitating a massive build out of physical infrastructure. Dell'Oro Group reported that data center semiconductors and components saw a 44 %year on year increase in the second quarter of 2025, driven almost entirely by AI hardware demand. This surge is not limited to processors; it extends to high bandwidth memory, advanced networking equipment like InfiniBand and high-speed Ethernet switches, and power delivery systems capable of supporting racks with densities far exceeding traditional data centers. Every new AI cluster deployed requires a complete hardware stack, making this segment the primary engine of market expansion.

By End User Industry Insights

The IT and ITES segment was the leading end user industry in the European AI data center market and captured 34.3% of the regional market share in 2025. This segment's dominance is foundational, as IT and ITES companies are both the primary developers and the largest consumers of AI infrastructure. They build and manage the cloud platforms, provide managed services for AI workloads, and develop the enterprise software that increasingly incorporates AI features. Their deep technical expertise and constant need to innovate to stay competitive drive continuous investment in cutting edge data center capacity. Moreover, they serve as the conduit for other industries to access AI capabilities, acting as system integrators and consultants who design, deploy, and manage AI solutions for clients across all sectors, thereby consolidating their position as the central hub of AI adoption in Europe.

The internet and digital media segment is emerging as the fastest growing end user category and is estimated to grow at a promising CAGR in the European AI data center market during the forecast period. This acceleration is powered by the integration of AI into every facet of digital content. Social media platforms use AI for real time content moderation, personalized feed curation, and targeted advertising. Streaming services rely on AI for recommendation engines, automated video editing, and even AI generated content. The proliferation of user generated content, from videos to live streams, creates a massive data processing burden that can only be handled by dedicated AI infrastructure. As these companies compete on the quality and personalization of their user experience, their investment in AI data centers becomes a core strategic priority, driving this segment's rapid expansion.

COUNTRY-LEVEL ANALYSIS

Germany AI Data Center Market Analysis

Germany dominated the AI data center market in Europe in 2025 with the highest share of the regional market. Germany stood as a cornerstone of the European AI data center market by hosting the highest number of data centers on the continent. It is already the European country with the most data centers, with DataCenterMap listing around 490 facilities, and more than 100 of them located in key hubs like Frankfurt. The German market is proving extremely robust in 2025, growing to a total capacity of 2,980 megawatts, with colocation and AI serving as the primary growth drivers according to FirstColo. The nation's strong industrial base, particularly in automotive and manufacturing, is a major catalyst for AI adoption, as companies seek to implement smart factory solutions and predictive maintenance. Frankfurt's status as a global financial and internet exchange hub provides unparalleled connectivity, making it a magnet for hyperscalers. The German government's proactive stance on digital infrastructure and its stable regulatory environment further solidify its position as a top destination for AI data center investment.

United Kingdom AI Data Center Market Analysis

The United Kingdom maintained second leading position as a leading European market for AI data centers in 2025. The growth of the UK in the European market is driven by the London's status as a global financial and technological capital. London, in particular, is one of the "FLAP" markets (Frankfurt, London, Amsterdam, Paris) that dominate European data center capacity, offering a mature ecosystem of connectivity, power, and skilled labor. The UK's vibrant fintech and AI startup scene, concentrated in London, generates immense demand for high performance computing resources. Despite Brexit, the UK continues to attract significant foreign direct investment in digital infrastructure, as global cloud providers view it as an essential node for serving both the domestic market and as a gateway to the wider European region.

France AI Data Center Market Analysis

France has emerged as a powerful and rapidly growing player in the European AI data center market, driven by a clear national strategy to become a leader in artificial intelligence. The French government's ambitious "France 2030" investment plan has allocated billions of euros to boost the country's AI capabilities, directly stimulating demand for domestic data center capacity. This strategic push has attracted major hyperscalers, with capacity in France up by 15 percent, the highest growth among established European hubs as reported by Savills. Paris serves as the primary hub, benefiting from a strong talent pool from its world class engineering schools and a business-friendly environment. The focus on developing a sovereign European cloud, with French champions like OVHcloud playing a key role, is another critical factor ensuring that a significant portion of the nation's AI data remains within its borders, fueling local infrastructure development.

Netherlands AI Data Center Market Analysis

The Netherlands, and specifically the Amsterdam metropolitan area, is a critical nexus for the European AI data center market due to its exceptional digital infrastructure. Its strategic location at the heart of European fiber networks, with a vast number of subsea cable landings, provides unmatched connectivity to the rest of the continent and beyond. The market has significantly grown due to cloud computing, big data, digitization, and the rising demand for data services as highlighted in CBRE's Netherlands Real Estate Market Outlook for 2025. The sector expects a record investment of more than 1.4 billion euros in 2025, demonstrating strong confidence in its future. The presence of major players like Interxion (a Digital Realty company) and Equinix has created a dense, interconnected ecosystem that is highly attractive for businesses requiring low latency and high reliability for their AI applications.

Ireland AI Data Center Market Analysis

Ireland, while not in your initial list, is a de facto top five market and often supplants Italy or Spain in data center rankings due to its outsized role as a European headquarters for major US tech giants. However, focusing on your list, Spain rounds out the top five, experiencing a notable surge in data center activity. Madrid and Barcelona are becoming increasingly important secondary hubs as hyperscalers look to diversify beyond the saturated FLAP markets. The Spanish government has been actively promoting the country as a data center destination, citing its abundant renewable energy resources, particularly solar power, which aligns with the sustainability goals of major tech companies. This, combined with a favorable climate for free cooling and improving digital infrastructure, has led to a significant uptick in project announcements. While its current market share is smaller than the leaders, its growth trajectory is steep, positioning it as a key market for future AI data center expansion in Southern Europe.

COMPETITIVE LANDSCAPE

The competition in the Europe AI data center market is intense and multifaceted, characterized by a race for power, land, and talent. The market is dominated by American hyperscalers like Microsoft, Google, and Amazon Web Services who leverage their global scale and vast resources to secure prime locations and massive power contracts. They compete directly with each other to offer the most advanced AI infrastructure and services to European customers. Alongside them, a tier of specialized data center operators like Equinix and Digital Realty provides the critical real estate and interconnection fabric that enables the entire ecosystem. The competition is further intensified by the European Union's push for digital sovereignty, which has spurred the growth of local champions like OVHcloud. All players are now locked in a fierce battle to acquire sites with sufficient grid capacity, as the primary bottleneck for new AI data center development has shifted from capital to available power, making strategic partnerships with energy companies a key differentiator.

KEY MARKET PLAYERS

The leading companies operating in the Europe AI data center market include:

- NVIDIA Corporation

- Microsoft Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Arm Ltd.

- Google Inc

- Equinix

- Graphcore Ltd.

TOP PLAYERS IN THE MARKET

- Microsoft is a central force in the European AI data center market through its Azure cloud platform. The company is heavily investing in dedicated AI infrastructure across the continent to meet surging demand for its Copilot and other AI services. To strengthen its position, Microsoft has secured massive power deals with utilities in Sweden and Spain and is actively developing new AI data center campuses in strategic locations like Sora Italy. These actions ensure it can provide the immense computational resources and low latency required by its European enterprise and government clients.

- Google is aggressively expanding its footprint in Europe to support its Gemini AI models and cloud AI offerings. The company’s strategy involves building new state of the art data centers specifically designed for AI workloads while also retrofitting its existing facilities. A key recent action was Google’s partnership with a major Spanish utility to power its new data centers with renewable energy, directly addressing the dual challenges of high-power demand and sustainability that are critical for operating in the European regulatory environment.

- Equinix serves as the foundational interconnection hub for the European AI ecosystem. As the world’s largest data center provider, its International Business Exchange facilities in London Frankfurt and Paris host a dense network of cloud providers AI startups and enterprises. To solidify its market position, Equinix completed the acquisition of Maincubes a Dutch data center provider in January 2024. This move significantly expanded its capacity in the strategically important Amsterdam market providing more space for high density AI deployments.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe AI data center market are primarily focused on three core strategies. First, they are securing long term power purchase agreements with energy providers to guarantee the massive and stable electricity supply needed for AI operations. Second, they are investing heavily in new construction and expansion of facilities in both established FLAPD hubs and emerging markets like Spain and Portugal to diversify their footprint and capture new demand. Third they are forming strategic partnerships with local governments and utilities to navigate complex regulatory landscapes and ensure access to renewable energy sources which is a critical requirement for sustainable growth in Europe.

MARKET SEGMENTATION

This research report on the Europe AI data center market has been segmented and sub-segmented into the following categories.

By Data Center Type

- Cloud Service Providers

- Colocation Data Centres

- Enterprise / On-Premises / Edge

By Component

- Hardware

- Power Infrastructure

- Cooling Infrastructure

- IT Equipment

- Racks and Other Hardware

- Software Technology

- Machine Learning

- Deep Learning

- Natural Language Processing

- Computer Vision

- Services

- Managed Services

- Professional Services

By Tier Standard

- Tier 3

- Tier 4

By End-user Industry

- IT and ITES

- Internet and Digital Media

- Telecom Operators

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- Manufacturing and Industrial IoT

- Government and Defense

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe AI data center market?

The Europe AI data center market provides GPU-powered facilities for training large models. Hyperscale operators build capacity meeting exploding computational demands efficiently.

How does the Europe AI data center market operate?

The Europe AI data center market operates through colocation providers offering racks optimized for AI workloads. Direct liquid cooling supports dense GPU configurations reliably.

What drives growth in the Europe AI data center market?

Growth in the Europe AI data center market stems from generative AI adoption and sovereign cloud initiatives. Enterprises require scalable infrastructure for model deployment.

Which countries lead the Europe AI data center market?

Germany and Netherlands lead the Europe AI data center market with renewable energy access. Ireland and Sweden follow via hyperscale investments and cold climates.

What technologies define the Europe AI data center market?

GPU clusters and NVLink interconnects define the Europe AI data center market enabling parallel training. Direct-to-chip cooling handles extreme power densities effectively.

How does sustainability shape the Europe AI data center market?

Sustainability drives the Europe AI data center market toward PUE optimization and waste heat reuse. EU green directives favor Nordic locations with hydro power.

What role do hyperscalers play in the Europe AI data center market?

Hyperscalers dominate the Europe AI data center market building custom campuses for proprietary models. They set standards for power density and latency requirements.

What trends influence the Europe AI data center market?

Trends in the Europe AI data center market include edge deployments and modular prefabrication. Quantum-ready designs prepare infrastructure for hybrid computing.

What challenges face the Europe AI data center market?

Challenges in the Europe AI data center market involve grid capacity constraints and skilled talent shortages. Policy reforms accelerate permitting for new campuses.

How has AI demand transformed the Europe AI data center market?

AI workloads have transformed the Europe AI data center market from CPU-centric to GPU-dominated designs. Power consumption patterns now dictate site selection.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com