Europe Automotive E-Commerce Market Size, Share, Trends, & Growth Forecast Report By By Components (Tires & Wheels, Engine Components, Infotainment & Multimedia, Electrical Products, Interior Accessories, Exterior Accessories, Others), Consumer, Vehicle Type and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Automotive E-Commerce Market Report Summary

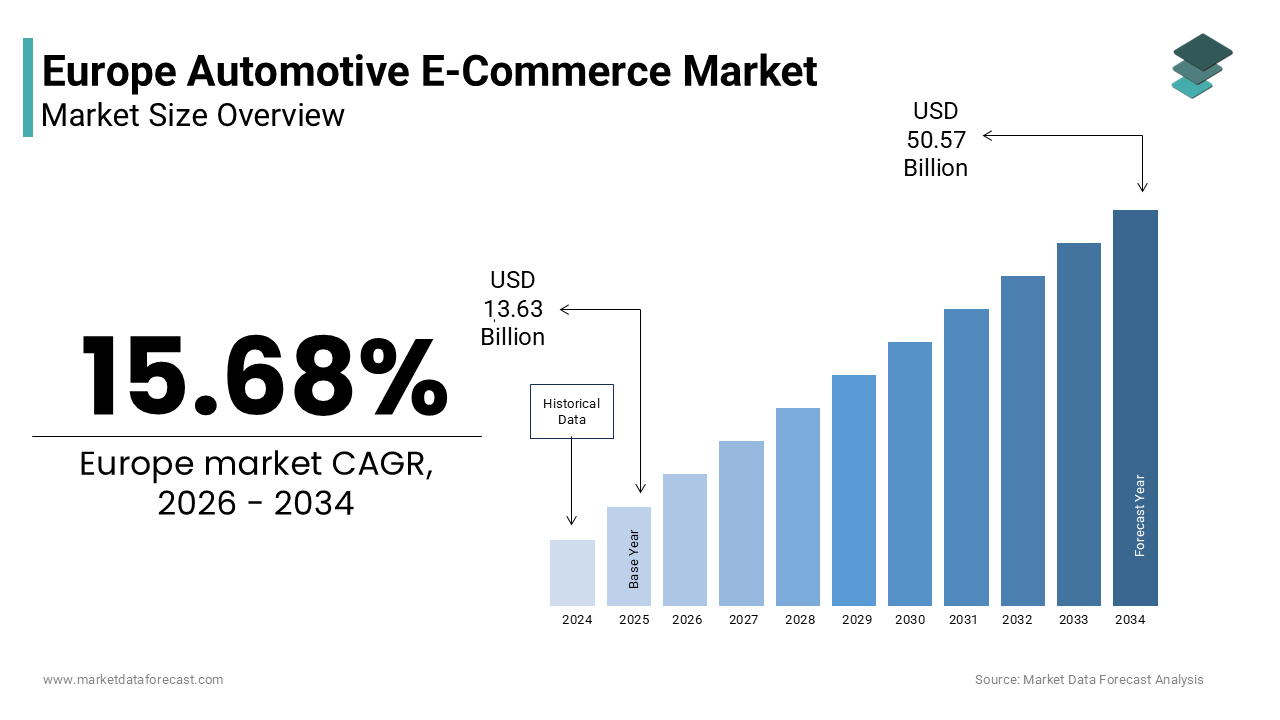

The Europe automotive e-commerce market was valued at USD 13.63 billion in 2025, is estimated to reach USD 15.77 billion in 2026, and is projected to reach USD 50.57 billion by 2034, growing at a CAGR of 15.68% during the forecast period from 2026 to 2034. The growth of the European automotive e-commerce market is driven by increasing internet penetration, rising digital literacy, and growing consumer preference for convenience and transparent pricing. The expansion of online platforms for vehicles, spare parts, and accessories, along with advancements in virtual showrooms and digital payment systems, is further accelerating market growth. Moreover, the shift toward direct-to-consumer sales models and subscription-based mobility solutions is transforming traditional automotive retail across Europe.

Key Market Trends

- Rising adoption of online platforms for purchasing automotive parts, accessories, and even vehicles is driven by increasing digital penetration.

- Growing use of augmented reality and virtual showrooms to enhance the online buying experience and improve customer engagement.

- Increasing preference for transparent pricing and hassle-free purchasing compared to traditional dealership models.

- Expansion of direct-to-consumer (D2C) and subscription-based vehicle ownership models across Europe.

- Strong growth in mobile commerce, enabling consumers to shop for automotive products via smartphones.

Segmental Insights

- Based on components, the tires and wheels segment was the largest and held a significant share of the Europe automotive e-commerce market in 2025. The segment’s dominance is attributed to high replacement frequency, standardization, and ease of online purchasing.

- Based on consumer type, the business-to-consumer (B2C) segment accounted for the largest share of the Europe automotive e-commerce market in 2025. This dominance is driven by increasing individual consumer preference for online shopping and convenience.

- Based on vehicle type, the passenger car segment was the largest, occupying a prominent share of the Europe automotive e-commerce market in 2025. The segment’s leadership is due to high passenger car ownership and strong demand for aftermarket parts and accessories.

Regional Insights

The Europe automotive e-commerce market is experiencing rapid growth across major countries, supported by strong digital infrastructure, high vehicle ownership, and increasing online retail adoption.

- Germany was the largest contributor, accounting for 25.1% of the Europe automotive e-commerce market share in 2025, driven by its strong automotive industry, advanced logistics, and high consumer trust in online platforms.

- The United Kingdom holds a significant position, supported by a mature e-commerce ecosystem, high online shopping penetration, and strong demand for aftermarket parts.

- France continues to perform well, fueled by increasing adoption of digital platforms, strong aftermarket demand, and government support for digital transformation.

- Italy is emerging as a growing market, driven by rising internet usage, strong automotive culture, and increasing preference for online automotive purchases.

Competitive Landscape

The Europe automotive e-commerce market is highly competitive and fragmented, with a mix of global e-commerce giants, specialized automotive platforms, and traditional manufacturers entering digital channels. Leading companies focus on enhancing user experience, improving logistics, and offering value-added services such as installation and warranties. Strategic partnerships, mobile app development, and investments in cybersecurity are key strategies shaping competition. Prominent players in the Europe automotive e-commerce market include Amazon, eBay, Alibaba Group, Auto1 Group, Cdiscount, Oscaro, Mister Auto, Autodoc GmbH, Delticom AG, PartsTech Inc., RockAuto, Advance Auto Parts, Bosch Automotive Aftermarket, Continental AG, and Michelin.

Europe Automotive E-Commerce Market Size

The Europe automotive e-commerce market size was valued at USD 13.63 billion in 2025 and is anticipated to reach USD 15.77 billion in 2026 from USD 50.57 billion by 2034, growing at a CAGR of 15.68% during the forecast period from 2026 to 2034.

Automotive e-commerce encompasses the digital transaction of vehicles, spare parts, accessories, and related services through online platforms, which is fundamentally altering traditional dealership models. This sector integrates business to consumer and business to business interactions, facilitating seamless procurement and sales processes via web-based portals and mobile applications. The region is experiencing a structural shift as consumers increasingly prefer the transparency and convenience of digital channels for researching and purchasing automotive products. According to Eurostat, 89% of individuals in the European Union aged 16 to 74 used the internet in 2023, which is creating a vast digital base for automotive retailers. Furthermore, according to the European Commission, 57% of internet users in the EU made online purchases in the first quarter of 2023, which is indicating a robust cultural acceptance of e-commerce. The automotive industry leverages this digital penetration to offer virtual showrooms, augmented reality features, and direct to consumer sales models. According to the International Organization of Motor Vehicle Manufacturers, Europe produced approximately 17.5 million motor vehicles in 2022, providing a substantial inventory for digital distribution channels. The integration of secure payment gateways and advanced logistics networks supports the efficient delivery of heavy and specialized automotive goods. Regulatory frameworks such as the General Data Protection Regulation ensure consumer data security, fostering trust in online transactions. This digital transformation enables manufacturers and retailers to reach broader audiences, reduce overhead costs, and provide personalized customer experiences, thereby redefining the competitive landscape of the European automotive sector.

MARKET DRIVERS

Increasing Internet Penetration and Digital Literacy among Consumers

The widespread availability of high speed internet and rising digital literacy rates across Europe is fuelling the growth of the European automotive e-commerce market. According to Eurostat, broadband access in European households reached 93% in 2023, ensuring that potential customers have the necessary infrastructure to engage with online automotive platforms. This connectivity allows consumers to research vehicle specifications, compare prices, and read reviews extensively before making purchase decisions. According to the European Commission, approximately 54% of Europeans possess at least basic digital skills, enabling them to navigate complex e-commerce interfaces with confidence. This proficiency reduces hesitation in buying high value items such as cars and specialized parts online. Automakers and retailers capitalize on this trend by developing user friendly websites and mobile applications that offer immersive experiences, including 360-degree virtual tours and configuration tools. The ability to access detailed product information and customer feedback empowers buyers, leading to more informed and satisfactory purchasing decisions. Furthermore, the proliferation of smartphones facilitates mobilE-Commerce, allowing users to shop for automotive products on the go. According to Eurostat, 70% of EU internet users shopped online in 2023, with a significant portion of traffic originating from mobile devices. This digital readiness creates a fertile environment for automotive e-commerce, driving demand for online sales channels and encouraging traditional dealerships to adopt digital strategies to remain competitive in an increasingly connected marketplace.

Growing Preference for Convenience and Transparent Pricing Models

Consumer demand for convenience and transparent pricing is further contributing to the expansion of the European automotive e-commerce market as shoppers seek to avoid the often opaque and time consuming processes associated with traditional dealerships. Online platforms provide clear, upfront pricing for vehicles and parts, eliminating the need for prolonged negotiations and reducing purchase anxiety. As per a survey by the European Consumer Organisation, 72% of respondents stated that price transparency was a key factor in their decision to shop online for automotive products. The ability to browse extensive inventories from the comfort of home or office saves time and effort, appealing to busy professionals and younger demographics. E-commerce platforms often offer home delivery services for parts and accessories, further enhancing convenience. For vehicle purchases, many online retailers provide door step delivery and flexible return policies, mimicking the ease of standard online shopping. The European Automobile Manufacturers Association notes that the average time spent visiting physical dealerships has decreased by 30% as consumers rely more on digital research and purchasing tools. This shift is particularly evident in the spare parts segment, where users can quickly identify compatible components using vehicle identification numbers. The transparency and efficiency of online transactions build trust and loyalty, encouraging repeat business. As consumers become accustomed to the seamless experiences offered by other retail sectors, they expect similar standards from the automotive industry, driving sustained growth in the e-commerce channel.

MARKET RESTRAINTS

Complex Logistics and High Costs for Heavy Item Delivery

The logistical complexities and high costs associated with delivering heavy and bulky automotive items pose significant restraints to the Europe automotive e-commerce market. Unlike standard retail goods, vehicles and large parts require specialized handling, secure transportation, and often white glove delivery services, which increase operational expenses. According to the European Logistics Association, the cost of transporting oversized goods can be up to three times higher than standard parcel delivery, impacting profit margins for online retailers. The fragmented nature of European infrastructure, with varying road conditions and regulatory requirements across borders, further complicates last mile delivery. Delays and damages during transit are common concerns, leading to customer dissatisfaction and increased return rates. The European Transport Safety Council highlights that the risk of damage to vehicles during transport remains a critical issue, necessitating expensive insurance coverage. Additionally, the lack of standardized packaging solutions for irregularly shaped parts increases the likelihood of damage and returns. Retailers must invest in robust logistics networks and partnerships with specialized carriers to ensure timely and safe delivery, which can be prohibitive for smaller players. The environmental impact of transporting heavy items also faces scrutiny under European green deal initiatives, potentially leading to stricter regulations and higher compliance costs. These logistical hurdles limit the scalability of automotive e-commerce operations and deter some consumers from purchasing large items online, thereby restraining market growth and expansion.

Consumer Hesitation Regarding High Value Online Transactions

Persistent consumer hesitation regarding high value online transactions is further hampering the expansion of the Europe automotive e-commerce market, particularly for full vehicle purchases. Despite increasing digital literacy, many buyers remain skeptical about buying expensive assets without physical inspection and test drives. According to Eurostat, approximately 30% of EU internet users who did not shop online in 2023 cited security or payment concerns as a primary reason. The fear of fraud, misrepresentation of vehicle condition, and lack of immediate recourse in case of disputes discourages potential buyers. The tactile experience of touching and driving a car is considered essential by many, and virtual alternatives often fail to fully replicate this sensory engagement. The European Consumer Centre reports that complaints related to online vehicle purchases, such as undisclosed defects and warranty issues, are higher than for other product categories. This perception of risk is exacerbated by the complexity of financing and insurance processes, which are often easier to manage in person. Trust deficits regarding after sales support and maintenance services further inhibit adoption. While digital platforms offer convenience, the emotional and financial significance of buying a car leads many consumers to prefer traditional dealerships where they can interact directly with sales staff. Overcoming this psychological barrier requires significant investment in trust building measures, such as verified reviews, comprehensive warranties, and hassle free return policies, which remain challenging to implement effectively.

MARKET OPPORTUNITIES

Integration of Augmented Reality and Virtual Showroom Technologies

The integration of augmented reality and virtual showroom technologies is a lucrative opportunity for the Europe automotive e-commerce market, which is enhancing the online shopping experience and bridging the gap between digital and physical interactions. These technologies allow consumers to visualize vehicles in their own environments, explore interior features in 3D, and customize options in real time. According to the European Institute for Innovation and Technology, the adoption of augmented reality in retail is expected to grow by 25% annually, driven by consumer demand for immersive experiences. Virtual showrooms enable buyers to inspect vehicles from every angle, reducing uncertainty and increasing confidence in online purchases. Automakers such as BMW and Audi have already implemented these tools, reporting higher engagement rates and conversion ratios. The European Commission’s Digital Europe Programme supports the development of such innovative technologies, providing funding and resources for startups and established firms. By offering interactive and personalized experiences, retailers can differentiate themselves in a crowded market and attract tech savvy consumers. Furthermore, augmented reality can assist in the sale of spare parts by allowing users to verify compatibility and visualize installation processes. This technological enhancement not only improves customer satisfaction but also reduces return rates by ensuring that buyers make informed decisions. As hardware capabilities improve and costs decrease, the widespread adoption of augmented reality and virtual showrooms will likely become a standard feature in automotive e-commerce, driving growth and innovation.

Expansion of Subscription Based and Direct to Consumer Sales Models

The expansion of subscription based and direct to consumer sales models offers significant opportunities for growth in the Europe automotive e-commerce market and catering to changing consumer preferences for flexibility and ownership alternatives. Subscription services allow users to access vehicles for short periods without long term commitments, appealing to urban dwellers and younger generations who prioritize access over ownership. According to the European Automobile Manufacturers Association, the number of car sharing and subscription users in Europe has increased by 20% in recent years, reflecting a shift in mobility trends. Direct to consumer sales enable manufacturers to bypass traditional dealerships, offering lower prices and a more streamlined purchasing process. Tesla’s success with this model has inspired legacy automakers to explore similar strategies, leveraging online platforms to sell vehicles directly to buyers. The European Commission’s focus on fair competition and consumer rights supports these disruptive models, encouraging innovation in sales practices. Subscription platforms often include maintenance, insurance, and roadside assistance, providing a hassle free experience that appeals to busy consumers. This holistic approach enhances customer loyalty and generates recurring revenue streams for providers. By embracing these new business models, automotive companies can tap into emerging market segments and adapt to the evolving landscape of personal mobility. The flexibility and convenience offered by subscription and direct sales models position them as key drivers of future growth in the European automotive e-commerce sector.

MARKET CHALLENGES

Cybersecurity Threats and Data Privacy Concerns

Cybersecurity threats and data privacy concerns is a major challenge to the Europe automotive e-commerce market, as online platforms handle sensitive personal and financial information. The increasing connectivity of vehicles and e-commerce systems makes them vulnerable to hacking, data breaches, and identity theft. According to the European Union Agency for Cybersecurity, the number of reported cyber incidents in the transport sector increased by 25% in 2023 compared to the previous year, highlighting the growing risk landscape. Consumers are increasingly aware of these threats, with many hesitant to share personal data online due to fears of misuse. The General Data Protection Regulation imposes strict requirements on data handling, and non-compliance can result in severe penalties and reputational damage. Retailers must invest heavily in advanced security measures, such as encryption, multi factor authentication, and regular security audits, to protect customer data. However, the complexity of securing interconnected systems, including supply chain partners and third party service providers, remains a significant challenge. Any breach can erode consumer trust and lead to loss of business. The European Data Protection Board emphasizes the need for transparency and accountability in data processing, requiring companies to demonstrate robust security practices. Balancing the need for data collection to personalize experiences with the imperative to protect privacy is a delicate task. Failure to address these cybersecurity challenges effectively can hinder the growth of automotive e-commerce and undermine consumer confidence in digital transactions.

Regulatory Fragmentation across European Member States

Regulatory fragmentation across European member states poses a significant challenge to the Europe automotive e-commerce market, which is further creating barriers to cross border trade and operational efficiency. Each country has its own set of laws regarding consumer protection, taxation, vehicle registration, and environmental standards, complicating compliance for online retailers. According to the European Single Market Scoreboard, discrepancies in national regulations increase administrative burdens and costs for businesses operating in multiple jurisdictions. For instance, value added tax rates vary significantly across Europe, requiring complex accounting systems to manage transactions accurately. Vehicle registration processes also differ, with some countries requiring physical inspections that cannot be completed online, hindering the seamless sale of vehicles across borders. The European Commission has initiated efforts to harmonize digital single market rules, but progress has been slow and uneven. Retailers must navigate a labyrinth of legal requirements, often needing local expertise to ensure compliance. This fragmentation limits the ability of e-commerce platforms to offer standardized services and prices across Europe, reducing economies of scale. Furthermore, differing return policies and warranty laws create confusion for consumers, potentially discouraging cross border purchases. The lack of a unified regulatory framework impedes the full realization of the digital single market’s potential, forcing companies to adopt fragmented strategies that increase operational complexity and limit market expansion opportunities.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 15.68% |

| Segments Covered | By Components, Consumer, Vehicle Type, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Key Market Players | Amazon, eBay, Alibaba Group, Auto1 Group, Cdiscount, Oscaro, Mister Auto, Autodoc GmbH, Delticom AG, PartsTech Inc., RockAuto, Advance Auto Parts, Bosch Automotive Aftermarket, Continental AG, and Michelin. |

SEGMENTAL ANALYSIS

By Components Insights

The tires and wheels segment dominated the market by holding 36.1% of the European market share in 2025. The dominance of tires and wheels segment in the European market is primarily driven by the high replacement frequency of tires due to wear and tear, seasonal changes, and regulatory requirements, combined with the standardized nature of these products which simplifies online purchasing. According to the European Tyre and Rim Technical Organisation, the average European driver replaces tires every three to four years, creating a consistent and predictable demand cycle that is well suited for e-commerce platforms. Unlike complex mechanical parts, tires have universal sizing standards that allow consumers to easily identify the correct product using their vehicle registration number or tire sidewall markings, reducing the risk of incorrect purchases. According to Eurostat, the number of registered motor vehicles in the European Union exceeded 290 million in 2023, providing a massive installed base that requires regular tire maintenance. The availability of detailed online filters, customer reviews, and professional installation partnerships further enhances consumer confidence in buying tires online. Major e-commerce retailers often offer bundled services including delivery to local garages for fitting, addressing the logistical challenge of heavy items. This seamless integration of product sales with service networks makes tires an ideal category for online transactions. Furthermore, the competitive pricing available online compared to physical stores attracts cost conscious consumers, reinforcing the segment’s market leadership. The combination of necessity, standardization, and enhanced digital shopping experiences ensures that tires and wheels remain the most traded automotive components in the European online marketplace.

On the other end, the infotainment and multimedia segment is a promising segment and is projected to register the highest CAGR of 15.4% over the forecast period owing to the rapid technological obsolescence of factory installed systems and a strong consumer desire for enhanced connectivity features. According to the Consumer Technology Association, the lifespan of automotive infotainment hardware is significantly shorter than that of the vehicle itself, leading owners to upgrade systems to access modern smartphone integration, navigation, and entertainment options. Modern consumers expect seamless connectivity with their mobile devices, including Apple CarPlay and Android Auto compatibility, which older vehicle models often lack. E-commerce platforms offer a wide variety of aftermarket head units, speakers, and amplifiers that are easy to install and significantly cheaper than dealership upgrades. According to a survey by J.D. Power, connectivity features are among the top three factors influencing customer satisfaction with new vehicles, indicating a strong latent demand that aftermarket solutions can fulfill. The ease of installing plug and play infotainment systems encourages DIY enthusiasts to purchase these components online, where they can find detailed installation guides and video tutorials. Furthermore, the increasing popularity of streaming services and podcasts in cars drives the demand for high quality audio systems and Bluetooth adapters. Online retailers provide extensive comparisons of technical specifications, allowing tech savvy buyers to select products that meet their specific needs. This combination of technological advancement, consumer expectation for connectivity, and the accessibility of aftermarket solutions propels the rapid growth of the infotainment and multimedia segment in the European automotive e-commerce market.

By Consumer Insights

The business-to-consumer segment led the market by holding 64.6% of the European market share in 2025 due to the direct convenience offered to individual car owners who seek easy access to spare parts, accessories, and maintenance products without visiting physical stores. According to Eurostat, 72% of internet users in the European Union purchased goods or services online for private use in 2023, reflecting a strong cultural shift towards digital consumption. B2C platforms leverage personalized marketing strategies, recommending products based on vehicle model and purchase history, which enhances user engagement and conversion rates. The ability to read peer reviews and compare prices across multiple vendors empowers consumers to make informed decisions, fostering trust in online transactions. According to the European Consumer Organisation, transparency in pricing and product availability is the primary reason consumers prefer online shopping for automotive accessories. The proliferation of mobilE-Commerce applications allows users to order parts instantly from their smartphones, further simplifying the purchasing process. Major online retailers offer hassle free return policies and customer support, addressing common concerns about fitment and quality. The vast selection of niche accessories, such as custom seat covers and lighting kits, available online compared to local stores also attracts individual buyers. This combination of convenience, choice, and consumer empowerment solidifies the B2C segment’s leading position in the European automotive e-commerce landscape, catering to the diverse needs of millions of private vehicle owners.

On the other side, the business-to-business segment is a promising segment and is expected to grow at the fastest CAGR of 13.3% over the forecast period owing to the increasing adoption of digital procurement solutions by repair shops, dealerships, and fleet operators to enhance efficiency and optimize supply chains. According to the European Automobile Dealers Association, independent repair shops are increasingly turning to online B2B platforms to source parts quickly and accurately, reducing vehicle downtime and improving customer satisfaction. These platforms offer real time inventory visibility, automated ordering, and integrated invoicing, streamlining operational workflows for businesses. The ability to compare suppliers and negotiate bulk discounts online provides significant cost advantages for small and medium sized enterprises. According to a report by McKinsey and Company, digital procurement can reduce purchasing costs by 5% to 10% and processing time by 50%, making it an attractive option for automotive businesses. The integration of electronic data interchange systems allows for seamless communication between suppliers and buyers, minimizing errors and delays. Furthermore, B2B platforms often provide technical support and warranty management services, adding value beyond simple transactions. The consolidation of the automotive aftermarket industry has led to larger networks of repair shops that require centralized digital procurement solutions. This shift towards digitization in business operations drives the rapid expansion of the B2B segment, as companies seek to remain competitive in an increasingly fast paced and cost sensitive market environment.

By Vehicle Type Insights

The passenger car segment led the market by accounting for 71.7% of the European market share in 2025. The dominance of passenger cars segment in the European market is attributed to the high rate of passenger car ownership in Europe and the corresponding demand for aftermarket parts and accessories. According to the European Automobile Manufacturers Association, there were over 250 million passenger cars in circulation in the European Union in 2023. This vast installed base generates consistent demand for replacement parts, such as brakes, filters, and batteries, as well as aesthetic accessories like seat covers and floor mats. Private car owners are more likely to engage in online shopping for these items due to the convenience and competitive pricing offered by e-commerce platforms. According to Eurostat, passenger cars account for nearly 80% of all road transport kilometers in Europe, highlighting their central role in daily mobility and the consequent wear and tear on components. The diversity of passenger car models and brands creates a fragmented market where online platforms excel in providing specific parts that may not be available locally. The ease of searching by vehicle identification number ensures accurate part matching, reducing return rates and increasing customer satisfaction. Furthermore, the emotional attachment owners have to their personal vehicles drives spending on customization and enhancement products. This combination of high volume, frequent replacement needs, and personalization desires solidifies the passenger car segment’s leading position in the European automotive e-commerce landscape.

However, the commercial vehicle segment is projected to register the highest CAGR of 12.6% over the forecast period owing to the subsequent expansion of delivery fleets across Europe. According to the European Courier Express and Parcel Association, the parcel market in Europe grew by 10% in 2023, necessitating a larger fleet of vans and trucks to handle last mile deliveries. This expansion increases the demand for commercial vehicle parts and accessories, such as tires, braking systems, and cargo management solutions. Fleet operators prioritize minimizing downtime, leading them to adopt digital procurement methods for quick and reliable parts sourcing. According to the International Road Transport Union, the average age of commercial vehicles in Europe is decreasing as companies invest in newer, more efficient models, but the high mileage accumulated by delivery vehicles accelerates wear and tear. E-commerce platforms offer specialized B2B services for commercial clients, including bulk ordering, scheduled deliveries, and technical support. The need for specialized equipment, such as refrigeration units for food delivery or shelving for parcels, also drives online sales of accessories. The professional nature of commercial vehicle maintenance requires precise part matching, which digital platforms facilitate through advanced search tools. This synergy between the growth of online retail logistics and the operational needs of commercial fleets propels the rapid expansion of the commercial vehicle segment in the automotive e-commerce market.

REGIONAL ANALYSIS

Germany Automotive E Commerce Market Analysis

Germany held the largest share of 25.1% of the Europe automotive e-commerce market in 2025. The dominance of Germany in the European market is driven by its robust automotive industry, high internet penetration, and strong consumer confidence in online transactions. The country is home to major automobile manufacturers and a dense network of independent repair shops that actively utilize digital procurement channels. According to the German Federal Statistical Office, e-commerce revenue in Germany reached approximately 79 billion euros in 2023, with automotive parts representing a significant portion of this growth. The high density of vehicles, with over 48 million registered cars, creates a substantial aftermarket demand. German consumers are known for their technical expertise and preference for high quality products, driving sales of premium aftermarket parts and accessories online. The presence of leading e-commerce platforms and specialized automotive retailers facilitates easy access to a wide range of products. According to the German Automotive Industry Association, the trend towards digitalization in the aftermarket is accelerating, with more workshops adopting online ordering systems. The country’s advanced logistics infrastructure ensures fast and reliable delivery of automotive components, enhancing customer satisfaction. Furthermore, strict vehicle inspection regulations encourage regular maintenance and part replacement, sustaining demand for online purchases. This combination of industrial strength, consumer behavior, and regulatory framework positions Germany as the dominant market for automotive e-commerce in Europe.

United Kingdom Automotive E Commerce Market Analysis

The United Kingdom accounted for the second largest share of the European automotive e-commerce market in 2025 due to a mature online retail sector and a large population of car enthusiasts. The UK has one of the highest rates of online shopping in Europe, with consumers comfortable purchasing a wide variety of goods digitally. According to the Office for National Statistics, online sales accounted for 27% of total retail sales in the UK in 2023. The automotive sector benefits from this digital readiness, with numerous specialized online retailers offering competitive prices and extensive product ranges. The prevalence of older vehicles in the UK, with an average age of over 8 years, drives demand for affordable replacement parts available through e-commerce channels. According to the Society of Motor Manufacturers and Traders, the UK aftermarket is valued at billions of pounds, with a growing share captured by online sales. The strong DIY culture among British car owners further boosts online parts sales, supported by abundant online tutorials and forums. The country’s island geography and concentrated population centers facilitate efficient logistics and delivery networks. Additionally, the presence of major global e-commerce players with strong UK operations enhances market accessibility. This vibrant digital ecosystem and active consumer base sustain the UK’s prominent role in the European automotive e-commerce landscape.

France Automotive E Commerce Market Analysis

France holds a notable share of the Europe automotive e-commerce market owing to a large vehicle parc and increasing adoption of digital services among consumers and businesses. The French government’s support for digital transformation in retail and automotive sectors encourages the growth of online platforms. According to the Federation of e-commerce and distance selling (FEVAD), e-commerce sales in France grew by 10.5% in 2023, with automotive accessories and parts showing strong performance. The country has a high number of independent garages that rely on online suppliers for cost effective and timely parts procurement. French consumers are increasingly seeking convenience and value, driving traffic to automotive e-commerce sites that offer competitive pricing and home delivery. According to the French Automotive Equipment Manufacturers Committee, the aftermarket sector is evolving rapidly with digital tools playing a key role in supply chain efficiency. The popularity of car sharing and rental services in urban areas like Paris also contributes to the demand for maintenance parts and accessories through B2B channels. The integration of online and offline services, such as click and collect options at local garages, enhances the customer experience. Furthermore, environmental regulations promoting vehicle maintenance and longevity support the demand for replacement parts. This dynamic market environment fosters the continued growth of automotive e-commerce in France.

Italy Automotive E Commerce Market Analysis

Italy is predicted to showcase a healthy CAGR in the European automotive e-commerce market during the forecast period due to a large number of small and medium sized enterprises in the automotive aftermarket sector. The country has a high vehicle ownership rate, with over 39 million cars registered, creating a substantial base for aftermarket sales. According to the Italian National Institute of Statistics, internet usage for shopping has increased significantly in recent years, reaching approximately 48% of the population. Italian consumers are increasingly turning to online platforms for automotive accessories and performance parts, driven by a strong car culture and enthusiasm for customization. The presence of numerous specialized online retailers caters to this niche demand, offering unique products not available in physical stores. According to the Italian Automotive Aftermarket Association, the market is undergoing a digital transition, with increased focus on e-commerce.

COMPETITIVE LANDSCAPE

The competition in the Europe automotive E-Commerce market is intense and fragmented, featuring a mix of global generalist retailers, specialized automotive platforms, and traditional manufacturers moving online. Generalist giants leverage their vast logistics networks and customer bases to offer convenience and speed, while specialized players compete on expertise, product depth, and niche offerings such as vintage or performance parts. Traditional brick and mortar chains are increasingly integrating digital channels to create omnichannel experiences, allowing customers to buy online and pick up in store. Price transparency is a key competitive factor, forcing retailers to optimize supply chains and offer dynamic pricing. Trust and reliability are paramount, with companies investing in secure payment systems, easy returns, and verified reviews to build consumer confidence. Differentiation often comes from value added services such as installation partnerships, technical support, and extended warranties. The entry of electric vehicle specific accessories and smart car technologies creates new battlegrounds for innovation. Regulatory compliance regarding data privacy and consumer rights adds complexity to operations. Companies must continuously adapt to changing consumer preferences and technological advancements to maintain relevance. Strategic collaborations and acquisitions are common as firms seek to expand capabilities and market reach. This dynamic environment drives continuous improvement in service quality and operational efficiency across the sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Automotive E-Commerce Market include

- Amazon

- eBay

- Alibaba Group

- Auto1 Group

- Cdiscount

- Oscaro

- Mister Auto

- Autodoc GmbH

- Delticom AG

- PartsTech Inc.

- RockAuto

- Advance Auto Parts

- Bosch Automotive Aftermarket

- Continental AG

- Michelin

Top Players in the Europe Automotive E-Commerce Market

Amazon Inc.

Amazon Inc. maintains a dominant presence in the Europe automotive E-Commerce market through its extensive logistics network and vast product catalog. The company offers a wide range of automotive parts, accessories, and tools to both individual consumers and professional mechanics. Its Prime membership program ensures rapid delivery, which is critical for urgent repair needs. Amazon recently expanded its Amazon Garage feature, allowing users to store vehicle information and receive personalized part recommendations. This enhancement improves user experience and reduces return rates by ensuring compatibility. The company also partners with local installation services to provide end to end solutions for customers. By leveraging advanced data analytics Amazon optimizes inventory management and pricing strategies. Its continuous investment in warehouse automation further strengthens its competitive edge. Amazon’s robust platform supports third party sellers, increasing product variety and availability. These initiatives solidify its position as a key player in the European digital automotive landscape.

eBay Inc.

eBay Inc. serves as a crucial marketplace for new and used automotive parts in Europe, connecting buyers with a global network of sellers. The platform specializes in hard to find components and vintage car parts, catering to enthusiasts and professional restorers. eBay’s authenticated guarantee program builds trust for high value transactions, reducing fraud risks. The company recently enhanced its mobile application with improved search filters and image recognition technology. These updates help users identify parts more accurately and quickly. eBay also introduced managed payments to streamline checkout processes and improve security. Its partnership with major automotive brands allows for official storefronts, ensuring authenticity of products. The platform’s auction format remains popular for rare items, driving engagement and competitive pricing. eBay continues to invest in seller tools to improve listing quality and customer service. These efforts reinforce its role as a preferred destination for diverse automotive needs in Europe.

Robert Bosch GmbH

Robert Bosch GmbH is a leading supplier of automotive technology and services with a strong direct to consumer E-Commerce presence in Europe. The company sells a wide array of replacement parts, diagnostic tools, and maintenance products through its online channels. Bosch leverages its brand reputation for quality and reliability to attract professional mechanics and DIY enthusiasts. Recently the company expanded its digital catalog with detailed technical documentation and video tutorials. This content supports customers in selecting and installing parts correctly. Bosch also integrated its online store with local workshop networks for seamless service booking. The company invests heavily in cybersecurity to protect customer data and transaction integrity. Its sustainable packaging initiatives align with European environmental regulations and consumer preferences. Bosch’s commitment to innovation drives the development of smart diagnostic devices compatible with mobile apps. These strategic actions enhance customer loyalty and strengthen its market position in the European automotive E-Commerce sector.

Top Strategies Used by Key Market Participants

Key players in the Europe automotive E-Commerce market primarily focus on enhancing user experience through personalized recommendations and seamless navigation. Companies invest in advanced search algorithms and vehicle specific databases to ensure accurate part matching. Strategic partnerships with local installation workshops provide comprehensive service offerings that combine product sales with professional fitting. Expansion of mobile applications enables convenient shopping and real time order tracking for customers. Retailers emphasize fast and reliable delivery options including same day shipping for urgent repairs. Integration of augmented reality tools helps users visualize products and verify compatibility before purchase. Content marketing strategies involving tutorials and guides educate consumers and build trust in DIY repairs. Competitive pricing dynamics and frequent promotions attract cost sensitive buyers to online platforms. Investment in cybersecurity measures protects sensitive customer data and financial transactions. Sustainability initiatives such as eco friendly packaging appeal to environmentally conscious consumers. These multifaceted approaches drive customer retention and market growth in the competitive European landscape.

RECENT MARKET DEVELOPMENTS

- In March 2024, Amazon Inc. launched an enhanced version of its Amazon Garage tool with improved vehicle compatibility checks. This launch is anticipated to allow Amazon Inc. to offer more comprehensive automotive solutions and strengthen the Europe automotive E-Commerce market presence.

- In January 2024, eBay Inc. introduced new image recognition features in its mobile app for easier part identification. This introduction is anticipated to allow eBay Inc. to offer more comprehensive automotive solutions and strengthen the Europe automotive E-Commerce market presence.

- In November 2023, Robert Bosch GmbH expanded its online catalog with interactive video tutorials for DIY installations. This expansion is anticipated to allow Robert Bosch GmbH to offer more comprehensive automotive solutions and strengthen the Europe automotive E-Commerce market presence.

- In September 2023, Amazon Inc. partnered with a network of local garages across Germany for professional installation services. This partnership is anticipated to allow Amazon Inc. to offer more comprehensive automotive solutions and strengthen the Europe automotive E-Commerce market presence.

- In June 2023, eBay Inc. implemented managed payments for all automotive transactions to enhance security and streamline checkout. This implementation is anticipated to allow eBay Inc. to offer more comprehensive automotive solutions and strengthen the Europe automotive E-Commerce market presence.

MARKET SEGMENTATION

This research report on the Europe automotive E-Commerce market has been segmented and sub-segmented based on the following categories.

By Components

- Tires & Wheels

- Engine Components

- Infotainment & Multimedia

- Electrical Products

- Interior Accessories

- Exterior Accessories

- Others

By Consumer Type

- Business-to-Consumer (B2C)

- Business-to-Business (B2B)

By Vehicle Type

- Passenger Car

- Commercial Vehicle

- Motorcycle

- Electric Vehicle

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com