Europe Biofuels Market Size, Share, Trends & Growth Forecast Report – Segmented By Equipment Type (Biodiesel, Ethanol, and Other Types), Feedstock, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Biofuels Market Summary

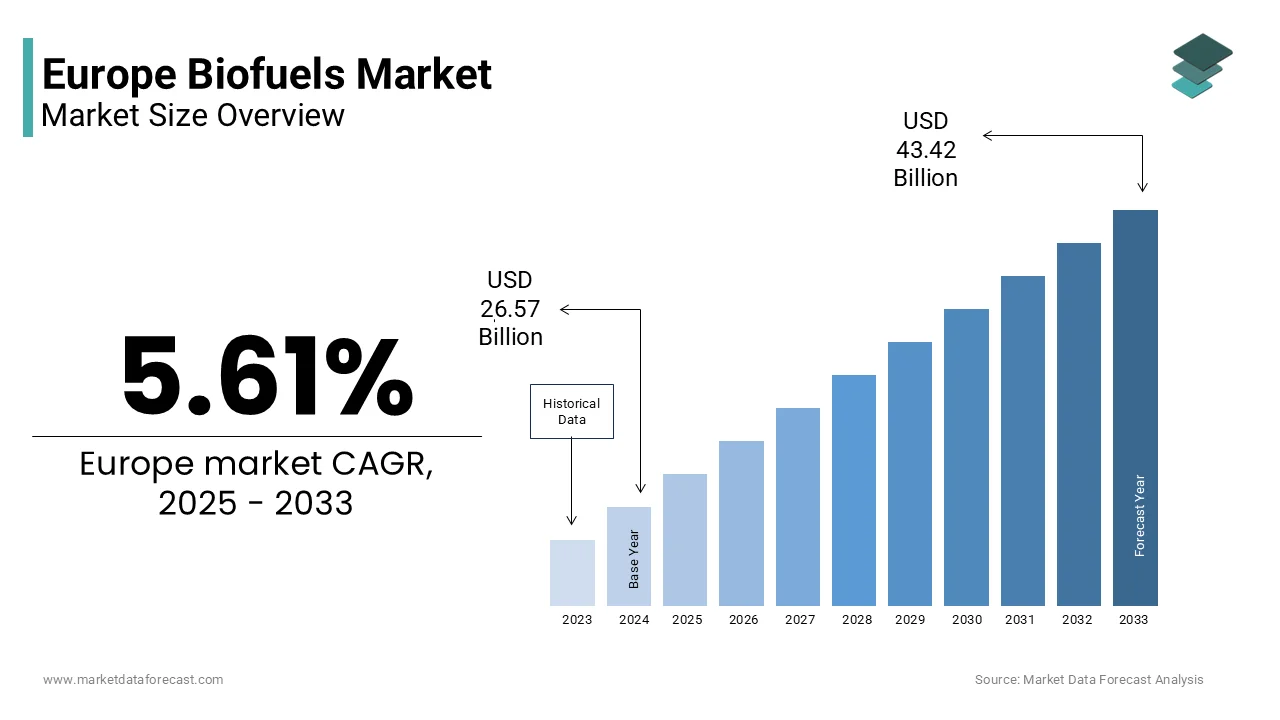

The Europe biofuels market size was valued at USD 26.57 billion in 2024, is estimated to reach USD 28.06 billion in 2025, and is projected to grow significantly to USD 43.42 billion by 2033, registering a CAGR of 5.61% from 2025 to 2033. Market growth is driven by the region’s strong push toward renewable energy adoption, stringent EU decarbonization targets, and increasing demand for sustainable fuel alternatives in transportation and industrial applications. Rising investment in next-generation biofuels, expanding bio-refinery capacities, and government incentives promoting low-carbon fuel adoption are further accelerating market expansion across Europe.

Key Market Trends

- Increasing adoption of advanced and second-generation biofuels to meet EU Green Deal and 2030 climate targets.

- Rising consumption of biodiesel supported by blending mandates and growing demand from the automotive and heavy-duty transport sectors.

- Strong shift toward feedstocks such as vegetable oils, used cooking oils, and agricultural residues to improve sustainability and reduce dependency on fossil fuels.

- Expanding investments in bio-refineries and cross-border renewable fuel supply chains across major European economies.

- Growing participation of major energy companies and pulp & paper manufacturers in biofuel production to diversify their renewable portfolios.

Segmental Insights

- Based on equipment type, the biodiesel segment dominated the Europe biofuels market in 2024, accounting for 58.3% of the market share. Its leadership is attributed to its widespread use in transportation, high compatibility with existing diesel infrastructure, and strong regulatory support for biodiesel blending across the EU.

- Based on feedstock, the vegetable oil segment held the largest share of 47.3% in 2024, driven by abundant agricultural production, strong supply availability, and the preferred use of rapeseed oil and soybean oil in biodiesel manufacturing.

Regional Insights

The Europe biofuels market continues to expand steadily across leading EU economies, backed by progressive renewable energy policies and strong demand from the transportation sector.

- Germany emerged as the largest contributor in 2024, accounting for 19.2% of the total market. The country’s advanced biofuel infrastructure, strong environmental regulations, and increasing adoption of biodiesel in road transport support its dominant position.

- Other key markets across Western and Northern Europe—including France, Italy, the Netherlands, Sweden, and Finland—are also witnessing growing investments in low-carbon fuels and next-generation biofuel projects.

Competitive Landscape

The Europe biofuels market is moderately consolidated, with leading companies focusing on capacity expansions, feedstock optimization, technological innovation, and partnerships to meet the region’s ambitious renewable energy targets. Key strategies include developing advanced biofuels, enhancing supply chain transparency, and integrating circular economy principles.

Prominent players in the European biofuels market include: UPM-Kymmene Oyj, Neste Oyj, Preem AB, SunPine AB, Svenska Cellulosa AB (SCA), Galp Energia SGPS SA, Green Fuel Nordic Oy, Beta Renewables SpA, Biomethanol Chemie Nederland BV, Borregaard ASA, and others.

Europe Biofuels Market Size

The Europe biofuels market size was valued at USD 26.57 billion in 2024 and is projected to reach USD 43.42 billion by 2033 from USD 28.06 billion in 2025, growing at a CAGR of 5.61%.

The biofuels are composed of liquid and gaseous fuels derived from biomass, such as vegetable oils, animal fats, used cooking oil, and lignocellulosic residues, primarily used for road transport, aviation, and maritime applications. Unlike fossil fuels, biofuels offer a renewable alternative that can significantly reduce lifecycle greenhouse gas emissions when sustainably sourced. The European Union’s regulatory architecture, particularly the Renewable Energy Directive II and the upcoming RED III, establishes binding targets for renewable energy in transport, driving both policy-induced and voluntary adoption. As per Eurostat, more than 14 million metric tons of biodiesel and bioethanol were consumed in the EU in 2023, predominantly blended into diesel and gasoline pools. The European Commission has also restricted the use of food crop-based biofuels from 2023 onward, accelerating the shift toward advanced feedstocks. These developments illustrate a structural transition from conventional to sustainable biofuels, underpinned by decarbonization imperatives and evolving supply chain ethics.

MARKET DRIVERS

EU Renewable Transport Mandates Accelerate Biofuel Consumption

The European Union’s legally binding renewable energy obligations for the transport sector serve as the most potent demand driver for biofuels. The EU renewable transport mandates are solely accelerating the growth of the European biofuels market. Under the Renewable Energy Directive II, member states must ensure that at least 14% of energy in transport comes from renewable sources by 2030, with specific sub-targets for advanced biofuels. According to the European Commission, this translates to an estimated annual biofuel demand of over 35 million metric tons by 2030, nearly double the 2023 volume. The directive also phases out high indirect land use change risk biofuels, effectively capping conventional biodiesel from palm and soy at 2019 levels and pushing refiners toward waste and residue-based alternatives. These regulatory levers create predictable offtake requirements by enabling long-term investment in biofuel production capacity. Moreover, the inclusion of renewable fuels of non-biological origin in the policy mix does not diminish liquid biofuels’ near-term role, given their compatibility with existing engines and distribution infrastructure.

Decarbonization of Heavy Transport Fuels Biofuel Adoption

The road, freight, ht aviation and maritime sectors, collectively responsible for over 25% of EU transport emissions, represent a frontier for biofuel deployment due to limited electrification pathways. The decarbonization of heavy transport is additionally prompting the growth of the European biofuels market. The EU’s Fit for 55 package introduces a mandate requiring fuel suppliers to reduce the carbon intensity of transport fuels by 13% by 2030, with biofuels offering the most scalable compliance pathway. In aviation, ReFuelEU mandates that 2% of jet fuel must be sustainable aviation fuel by 2025, rising to 6% by 2030, with bio-based pathways dominating current supply. These trends underscore biofuels’ irreplaceable role in decarbonising transport segments where batteries and hydrogen remain logistically or economically unviable.

MARKET RESTRAINTS

Land Use Competition Constrains Feedstock Availability

The expansion of biofuel production faces persistent constraints due to competition for agricultural land with food production, and biodiversity conservation is restricting the growth of the European biofuels market. According to the Joint Research Centre of the European Commission, some EU arable land was dedicated to biofuel feedstock cultivation in 2023, primarily rapeseed and wheat, raising concerns about indirect land use change and food price volatility. The EU’s progressive cap on food crop-based biofuels is limited to 7% of transport energy as per RED II, which reflects this tension, which is effectively stalling growth in conventional biodiesel. Furthermore, the European Court of Auditors warned in 2024 that inconsistent national reporting on feedstock origins risks inflating sustainability claims. This scarcity of verified low-risk feedstocks limits scalability and increases procurement costs, particularly for producers seeking certification under the International Sustainability and Carbon Certification scheme.

Inconsistent National Implementation Undermines Policy Cohesion

The divergent national policies on biofuel taxation, blending mandates, and sustainability verification create market fragmentation, and investment uncertainty is also hampering the growth of the European biofuels market. According to the European Federation for Transport and Environment, only 15 of 27 member states had fully transposed RED II’s advanced biofuel sub-targets into national law by mid-2024, leading to uneven demand signals. Germany suspended its bioethanol blending obligation in 2023 due to concerns over engine compatibility, while Italy maintained generous tax exemptions for hydrotreated vegetable oil, distorting cross-border trade. Additionally, variations in double-counting rules, where advanced biofuels count twice toward renewable targets, have led to regulatory arbitrage, with producers favouring markets like Sweden and the Netherlands that offer the most favourable treatment.

MARKET OPPORTUNITIES

Scaling of Advanced Biofuel Production Opens New Feedstock Pathways

The commercialisation of advanced biofuel technologies is unlocking non-food feedstocks at scale, transforming waste streams into high-value energy carriers is certain to elevate the growth of Europe's biofuels market. Hydroprocessed esters and fatty acids plants across Europe are increasingly utilising animal tallow, used cooking oil, and sewage sludge, while emerging alcohol-to-liquid and biomass-to-liquid facilities process forestry residues and agricultural straw. Similarly, Italy’s ENI converted its Venice and Gela refineries to produce renewable diesel exclusively from non-food sources by achieving 1.5 million tons of annual output. According to the study, 2.3 billion euros have been allocated since 2022 to support such retrofits by recognising their alignment with circular economy principles. This shift not only circumvents food vs fuel debates but also enhances carbon savings, with advanced biofuels achieving up to 90% lifecycle emission reductions compared to fossil equivalents.

Sustainable Aviation Fuel Mandates Create Dedicated Growth Corridor

The ReFuelEU Aviation regulation has established a legally binding trajectory for sustainable aviation fuel adoption by creating a high value for bio-based jet fuels, which is additionally creating new opportunities for the growth of the European biofuels market. Starting in 2025, fuel suppliers must ensure that 2% of aviation fuel is sustainable, rising to 6% by 2030 and 70% by 2050, with biofuels expected to dominate supply through 2035. According to some reports, this will require over 4 million metric tons of sustainable aviation fuel annually by 2030, which is equivalent to 15% of current EU jet fuel demand. Major European airlines, including Lufthansa, Air France and SAS, have signed offtake agreements with biofuel producers such as TotalEnergies and World Energy to secure supply. In 2023, over 200,000 commercial flights in Europe used blended sustainable aviation fuel, a 300% increase from 2021, as per the European Business Aviation Association. The EU’s inclusion of aviation in the Emissions Trading System further incentivises uptake through carbon cost pass-through.

MARKET CHALLENGES

Feedstock Price Volatility Threatens Production Margins

The economics of biofuel production remain highly sensitive to fluctuations in feedstock costs, which constitute 70 to 85% of total operating expenses. The feedstock price volatility is also one of the challenging factors for the growth of the European biofuels market. According to the European Commission’s Agricultural Market Observatory, the price of used cooking oil, which is a key advanced feedstock, increased by 42% between January and December 2023 due to surging demand and limited collection infrastructure. Similarly, rapeseed oil prices spiked by 35% in 2022 following the Ukraine war, directly impacting conventional biodiesel margins. As per the International Energy Agency, the average production cost of hydrotreated vegetable oil in the EU exceeded 1,200 euros per ton in 2023, while wholesale diesel prices averaged 950 euros, rendering operations unprofitable without policy support. This volatility deters private investment in new capacity, particularly for smaller producers lacking hedging mechanisms or long-term offtake contracts, thereby constraining market resilience and innovation.

Carbon Accounting Disputes Undermine Environmental Credibility

The persistent disagreements over the methodology for calculating biofuels’ lifecycle greenhouse gas emissions risk eroding their environmental legitimacy and policy support are additionally limiting the growth of Europe's biofuels market. According to a 2024 study by the Potsdam Institute for Climate Impact Research, indirect land use change emissions from certain European rapeseed biodiesel pathways can exceed those of fossil diesel when modelled over a 20-year horizon. While the EU’s default emission factors under RED II assign a 50% reduction to conventional biodiesel, real-world studies using satellite-based land monitoring suggest actual savings may be as low as 20% in high-pressure regions like Eastern Europe. Furthermore, the inclusion of co-products like glycerol and protein meal in allocation models introduces significant variability, with carbon intensity estimates differing by up to 30% depending on the method used. As per the European Academies’ Science Advisory Council, inconsistent accounting practices enable “greenwashing” and complicate cross-technology comparisons with electric vehicles or hydrogen.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.61% |

| Segments Covered | By Equipment Type, Feedstock, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | UPM-Kymmene Oyj, Neste Oyj, Preem AB, SunPine AB, Svenska Cellulosa AB (SCA), Galp Energia SGPS SA, Green Fuel Nordic Oy, Beta Renewables SpA, Biomethanol Chemie Nederland BV, Borregaard ASA, and other |

SEGMENTAL ANALYSIS

By Equipment Type Insights

The biodiesel segment accounted in holding 58.3% of the European biofuels market share in 2024, from Europe’s extensive adoption of biodiesel in the transport sector, or driven by policies under the Renewable Energy Directive, which mandates a 14% renewable energy target in transport by 2030. Biodiesel production in the European Union reached 13.6 billion litres in 2023, as reported by EurObserv’ER, confirming its status as the most utilised biofuel. The primary feedstock for biodiesel in Europe is rapeseed oil, followed by used cooking o, il, which aligns with sustainability mandates discouraging food crop-based feedstocks. Additional support comes from blending mandates such as the French biofuel blending obligation, which requires a minimum of 8.5% biodiesel in diesel fuel, a figure projected to rise to 9.5% by 2025, as per France’s Energy Regulatory Commission. Infrastructure readiness, including existing biodiesel blending facilities at fuel terminals and compatibility with conventional diesel engines, further solidifies biodiesel’s leadership position across the region.

The ethanol segment is expected to witness the fastest CAGR of 7.2% from 2025 to 2033, owing to the advancements in second-generation ethanol technologies that utilise lignocellulosic biomass such as wheat straw and forestry residues, thereby circumventing the food versus fuel debate. Furthermore, the European Union’s ReFuelEU Aviation initiative mandates a minimum of 2% sustainable aviation fuel by 2025, which includes bioethanol-derived synthetic paraffinic kerosene. Investing heavily in ethanol to jet fuel conversion plants with Neste and KLM launching a commercial-scale facility in 2024 capable of producing 100000 tons annually, as confirmed by the Dutch Ministry of Economic Affairs and Climate Policy.

By Feedstock Insights

The vegetable oil segment was the largest by holding 47.3% of Europe’s biofuels market share in 2024, with the region’s reliance on domestically produced rapeseed oil and the increasing utilisation of waste-based oils such as used cooking oil and animal fats. The European Union imported 2.1 million metric tons of used cooking oil in 2023, primarily from Southeast Asia, to meet growing biodiesel demand, according to the United States Department of Agriculture Foreign Agricultural Service. The preference for vegetable oil stems from its high lipid content, which enables efficient transesterification into biodiesel and compatibility with existing refining infrastructure. Policy frameworks under the Renewable Energy Directive II classify used cooking oil as a low indirect land use change risk feedstock, granting double-counting status toward renewable targets as explained by the European Environment Agency.

The sugar cane segment is likely to witness the fastest CAGR of 12.4% from 2025 to 2033, with imports from Brazil, the world’s largest sugar cane ethanol producer, which exported 1.4 billion litres of ethanol to the European Union in 2023. The European Commission’s delegated act on indirect land use change recognised Brazilian sugarcane ethanol as achieving 70% lower greenhouse gas emissions compared to fossil fuels, enabling its inclusion in renewable blending quotas. Europe’s primary ethanol import hub receives over 60% of Brazil’s ethanol exports destined for the EU, as per a recent survey. Additionally, sugarcane bagasse is increasingly used in cogeneration plants to produce renewable electricity, with facilities in southern Europe exploring integrated biorefinery models as per the European Biomass Association.

REGIONAL ANALYSIS

Germany Market Analysis

Germany was the largest contributor, by occupying 19.2% of the European biofuels market share in 2024. The country maintains a robust biodiesel production capacity exceeding 4.5 million metric tons annually, supported by over 30 dedicated refineries. Germany’s Biokraftstoff Quote mandates minimum biofuel blending levels, which stood at 7.1% in 2024 and is slated to increase to 8.3% by 2026 as per the National Renewable Energy Action Plan. The transport sector consumed 6.8 billion litres of biofuels in 2023, with biodiesel from used cooking oil accounting for 42% of this volume, according to the German Biomass Research Centre. Strong policy continuity combined with advanced waste-to-fuel infrastructure positions Germany as Europe’s biofuels powerhouse.

France Market Analysis

The French biofuels market was ranked second by holding 16.3% of share in 2024. The nation’s biofuel consumption reached 4.1 billion litres in 2023, driven by the SP95 E10 gasoline blend, nd which contains up to 10% ethanol and is available at over 90% of service stations nationwide. France is also the largest producer of beet-based ethanol in Europe, generating 1.3 billion litres in 2023 from domestic sugar beet processing.

United Kingdom Market Analysis

The United Kingdom biofuels market is likely to grow with prominent opportunities in the coming years. Post Brexit, the UK retained the Renewable Transport Fuel Obligation, which mandated 9.95% renewable content in transport fuels in 2023, where a figure set to rise to 14.5% by 2030. The UK imported 1.8 billion litres of biofuels in 2023, with 65% being ethanol primarily from Brazil. The government’s Jet Zero Council is accelerating the adoption of sustainable aviation fuels with a target of 10% blend by 2030, driving demand before ethanol-derived synthetic fuels are approved by the Civil Aviation Authority.

Italy Market Analysis

Italy's biofuels market growth is likely to grow, with the biofuel consumption totalling 1.9 billion litres in 2023, with biodiesel derived from used cooking oil and tallow representing 55% of the mix. Italy benefits from a Mediterranean climate suitable for energy crops such as cardoon and sorghum, which are being piloted in integrated biorefineries under the Bioenergy Cities initiative funded by the European Regional Development Fund. Legislative Decree 155 of 2022 updated Italy’s National Integrated Energy and Climate Plan, reinforcing biofuel mandates and incentivising waste-based feedstocks through feed-in tariffs and tax credits.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the notable key players in the European biofuels market are

- UPM-Kymmene Oyj

- Neste Oyj

- Preem AB

- SunPine AB

- Svenska Cellulosa AB (SCA)

- Galp Energia SGPS SA

- Green Fuel Nordic Oy

- Beta Renewables SpA

- Biomethanol Chemie Nederland BV

- Borregaard ASA

- Others

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the European biofuels market focus on vertical integration by securing reliable feedstock supply chains through partnerships with waste collectors and agricultural cooperatives. Companies invest in retrofitting conventional refineries into advanced biorefineries to produce low-carbon-intensity fuels. Strategic collaborations with airlines, logistics firms and public transport authorities enable long-term offtake agreements that ensure market stability. Regulatory alignment is prioritised through active participation in policy dialogues to shape favourable frameworks like ReFuelEU and RED III. Additionally, firms emphasise research and development to commercialise second and third generation biofuels from non-food biomass, algae and synthetic pathways, thereby enhancing sustainability credentials and future proofing their portfolios against evolving environmental standards.

COMPETITION OVERVIEW

The competition in the European biofuels market is characterised by a blend of integrated oil majors, specialised renewable fuel producers and emerging biotech firms. Incumbents leverage existing infrastructure and policy expertise to dominate large-scale production, while niche players focus on innovative feedstocks and conversion technologies. Regulatory compliance, particularly under the Renewable Energy Directive II and the upcoming RED I, II, creates a high barrier to entry, favouring established entities with certification capabilities and traceability systems. Intense rivalry exists in securing sustainable feedstocks such as used cooking oil and animal fats, which are limited in supply yet critical for meeting double-counting rules. Companies also compete on carbon intensity metrics as buyers increasingly demand fuels with verified lifecycle emission reductions. Strategic alliances with transport and aviation sectors further intensify competition, as firms vie for long-term supply contracts that anchor future revenue streams in a rapidly decarbonising energy landscape.

TOP PLAYERS IN THE MARKET

- Neste is a Finnish company renowned for its leadership in renewable diesel and sustainable aviation fuel production. The company operates one of the largest renewable fuels refineries in Europe, located in Rotterdam, and has consistently expanded its production capacity to meet growing demand. In 202,4, Neste announced a strategic partnership with Lufthansa to supply sustainable aviation fuel for flights departing from Frankfurt and Munich. This initiative aligns with the European Union’s ReFuelEU mandate and reinforces Neste’s commitment to decarbonising the aviation sector. The company also invests heavily in research to develop next-generation feedstocks such as algae and municipal waste, thereby strengthening its position as a technology-driven biofuels pioneer in Europe and globally.

- TotalEnergies is a French multinational energy company that has significantly diversified into low-carbon fuels, including biodiesel and bioethanol. The company leverages its extensive refining and distribution infrastructure across Europe to integrate biofuels into conventional fuel supply chains. In early 202,4, TotalEnergies inaugurated a new biofuel blending terminal in Le Havre, France, which enhances its capacity to deliver certified sustainable fuels to maritime and road transport sectors. The company also collaborates with agricultural cooperatives to source non-food feedstocks such as camelina and used cooking oil. These efforts support TotalEnergies’ broader strategy to achieve net zero emissions by 2050 while scaling its renewable fuel offerings in alignment with European policy frameworks.

- Eni is an Italian integrated energy company that has emerged as a key player in the European biofuels landscape through its proprietary Ecofining technology. The company converted its traditional refineries in Venice and Gela into biorefineries capable of processing waste-based feedstocks into high-quality biodiesel and hydrotreated vegetable oil. Eni signed a long-term agreement with Italian logistics firm Poste Italiane to supply renewable diesel for its delivery fleet. Eni also expanded its used cooking oil collection network across Southern Europe to secure sustainable raw materials. These actions like Eni’s strategic pivot toward circular bioeconomy models and its ambition to export advanced biofuels expertise to global markets beyond Europe.

MARKET SEGMENTATION

This research report on the European biofuels market has been segmented and sub-segmented based on categories.

By Equipment Type

- Biodiesel

- Ethanol

- Other Types

By Feedstock

- Coarse Grain

- Sugar Cane

- Vegetable Oil

- Other Feedstock

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are biofuels and why are they important in Europe?

Biofuels are renewable fuels made from biomass such as crops, waste, and vegetable oils. They are important in Europe for reducing carbon emissions and supporting energy transition goals.

1. What are biofuels and why are they important in Europe?

Biofuels are renewable fuels made from biomass such as crops, waste, and vegetable oils. They are important in Europe for reducing carbon emissions and supporting energy transition goals.

2. What is driving the growth of the Europe biofuels market?

Key drivers include strict EU emission regulations, renewable energy targets, government incentives, and rising demand for cleaner transportation fuels.

2. What is driving the growth of the Europe biofuels market?

Key drivers include strict EU emission regulations, renewable energy targets, government incentives, and rising demand for cleaner transportation fuels.

3. Which countries lead the Europe biofuels market?

Germany, France, Sweden, Finland, and the Netherlands are among the leading markets due to strong policy support and advanced biofuel production capacities.

3. Which countries lead the Europe biofuels market?

Germany, France, Sweden, Finland, and the Netherlands are among the leading markets due to strong policy support and advanced biofuel production capacities.

4. What are the main types of biofuels used in Europe?

The primary types include biodiesel, ethanol, and advanced/other biofuels derived from waste and non-food feedstocks.

4. What are the main types of biofuels used in Europe?

The primary types include biodiesel, ethanol, and advanced/other biofuels derived from waste and non-food feedstocks.

5. Which feedstocks are most commonly used for biofuel production?

Common feedstocks include coarse grains, sugar crops (e.g., sugar cane), vegetable oils, and waste-based feedstocks such as used cooking oil.

5. Which feedstocks are most commonly used for biofuel production?

Common feedstocks include coarse grains, sugar crops (e.g., sugar cane), vegetable oils, and waste-based feedstocks such as used cooking oil.

6. What industries primarily use biofuels in Europe?

Biofuels are mainly used in transportation, including road vehicles, aviation (sustainable aviation fuel), and marine applications.

6. What industries primarily use biofuels in Europe?

Biofuels are mainly used in transportation, including road vehicles, aviation (sustainable aviation fuel), and marine applications.

7. How does EU policy impact the biofuels market?

Policies such as the Renewable Energy Directive (RED II), carbon pricing, and national blending mandates significantly boost biofuel adoption.

7. How does EU policy impact the biofuels market?

Policies such as the Renewable Energy Directive (RED II), carbon pricing, and national blending mandates significantly boost biofuel adoption.

8. Are advanced biofuels gaining traction in Europe?

Yes, advanced biofuels produced from waste materials, lignocellulosic biomass, and residues are growing faster due to sustainability and EU compliance benefits.

8. Are advanced biofuels gaining traction in Europe?

Yes, advanced biofuels produced from waste materials, lignocellulosic biomass, and residues are growing faster due to sustainability and EU compliance benefits.

9. What challenges does the Europe biofuels market face?

Challenges include feedstock availability, competition with food crops, high production costs, and growing scrutiny over sustainability standards.

9. What challenges does the Europe biofuels market face?

Challenges include feedstock availability, competition with food crops, high production costs, and growing scrutiny over sustainability standards.

10. How is the demand for sustainable aviation fuel (SAF) influencing the market?

The rising need for SAF due to aviation decarbonization goals is creating new opportunities for biofuel producers across Europe.

10. How is the demand for sustainable aviation fuel (SAF) influencing the market?

The rising need for SAF due to aviation decarbonization goals is creating new opportunities for biofuel producers across Europe.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com