Europe Electrostatic Precipitator Market Size, Share, Trends & Growth Forecast Report, Segmented By Type, End User, Offering, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Electrostatic Precipitator Market Report Summary

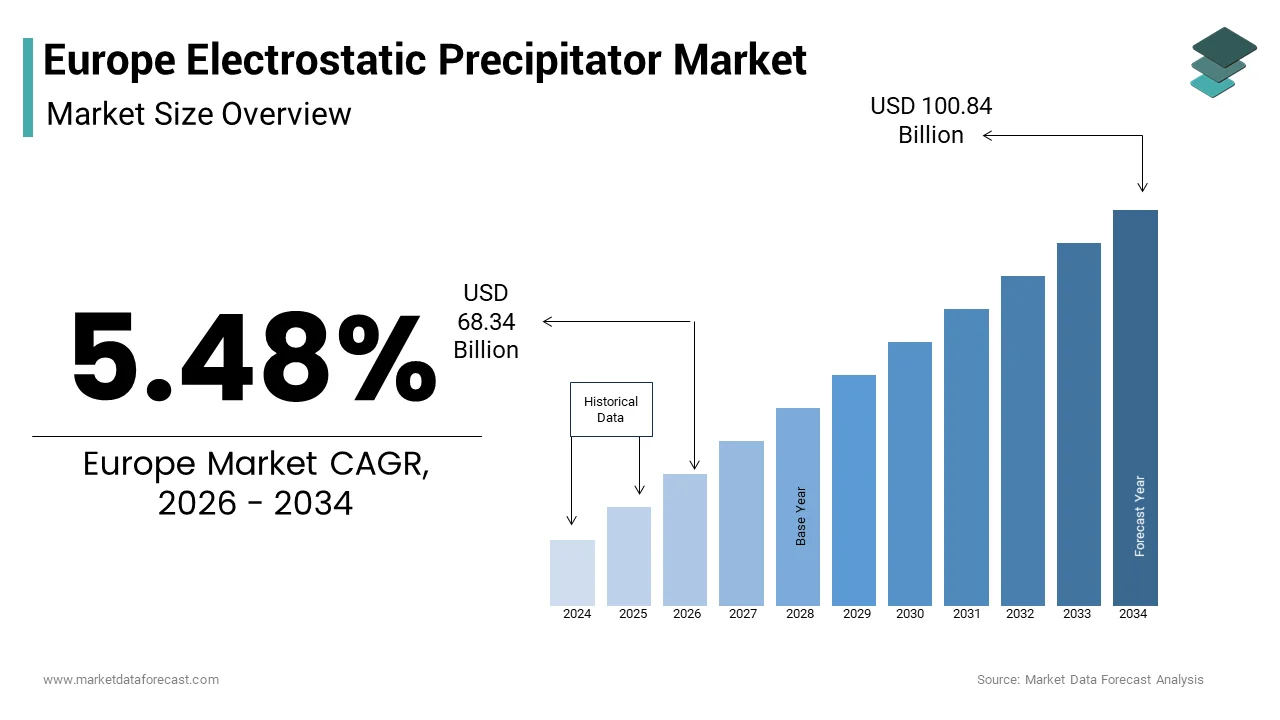

The Europe electrostatic precipitator market was valued at USD 64.77 billion in 2025, is estimated to reach USD 68.34 billion in 2026, and is projected to reach USD 100.84 billion by 2034, growing at a CAGR of 5.48% during the forecast period from 2026 to 2034. The growth of the Europe electrostatic precipitator market is driven by stringent environmental regulations, increasing focus on air pollution control, and the rising need for efficient emission reduction technologies across industrial sectors. The expansion of power generation, cement, and metal industries, along with growing investments in retrofitting and upgrading existing pollution control systems, is further fueling market growth. Additionally, the transition toward cleaner energy sources and stricter EU emission standards are accelerating the adoption of advanced electrostatic precipitator systems.

Key Market Trends

- Increasing implementation of strict emission norms across Europe to reduce particulate matter and industrial air pollution.

- Growing adoption of advanced and high-efficiency electrostatic precipitators in power plants and heavy industries.

- Rising demand for retrofitting and modernization of existing air pollution control systems.

- Integration of digital monitoring and automation technologies to enhance system performance and efficiency.

- Shift toward sustainable and low-emission industrial processes supporting market expansion.

Segmental Insights

- Based on type, the dry electrostatic precipitator segment was the largest and held a dominant share of the Europe electrostatic precipitator market in 2025. The segment’s dominance is attributed to its cost-effectiveness, high collection efficiency, and widespread use in power generation and industrial applications.

- Based on end user, the power and electricity segment accounted for 40.2% of the Europe electrostatic precipitator market share in 2025. The demand is driven by the need to control emissions from coal-fired and thermal power plants.

- Based on offering, the hardware and software segment held a significant share of the Europe electrostatic precipitator market in 2025, supported by increasing adoption of integrated systems combining equipment with advanced monitoring solutions.

Regional Insights

The Europe electrostatic precipitator market is witnessing steady growth across major countries, driven by industrial expansion and stringent environmental policies.

- Germany was the largest contributor, accounting for 22.3% of the Europe electrostatic precipitator market share in 2025, supported by its strong industrial base and focus on emission control technologies.

- Poland ranked second with 18.2% share, driven by its coal-based power generation sector.

- Italy is expected to present significant growth opportunities during the forecast period due to increasing industrial activities.

- The France continues to grow steadily, supported by its diverse industrial base and energy policies.

- The United Kingdom market is influenced by the gradual reduction in coal-fired power generation and the transition toward cleaner energy sources.

Competitive Landscape

The Europe electrostatic precipitator market is highly competitive, with key players focusing on technological advancements, product innovation, and strategic collaborations to strengthen their market position. Companies are investing in high-efficiency systems, digital solutions, and sustainable technologies to meet evolving regulatory standards. Prominent players in the Europe electrostatic precipitator market include FLSmidth, Siemens, Babcock & Wilcox Enterprises, Inc., John Wood Group PLC, SEI-Group Inc., KC Cottrell India, Balcke-Dürr GmbH, ELEX AG, S.A. HAMON, Mitsubishi Hitachi Power Systems Ltd., GEA Group Aktiengesellschaft, Thermax Limited, Sumitomo Heavy Industries Ltd., BHEL, General Electric, AirPol, ECP Group Oy, among others.

Europe Electrostatic Precipitator Market Size

The Europe electrostatic precipitator market size was valued at USD 64.77 billion in 2025 and is anticipated to reach USD 68.34 billion in 2026 to reach USD 100.84 billion in 2034, growing at a CAGR of 5.48% during the forecast period from 2026 to 2034.

Introduction and Market Definition

The electrostatic precipitator is the specialized industrial air pollution control systems designed to remove fine particulate matter from exhaust gases using electrostatic forces. These devices are critical components in heavy industries, such as power generation cement production steel manufacturing and waste incineration, where compliance with stringent emission standards is mandatory. The technology operates by charging particles in the gas stream and collecting them on oppositely charged plates thereby achieving high removal efficiency for submicron particles. According to the European Environment Agency, industrial facilities in the European Union are responsible for approximately 40% of total particulate matter emissions necessitating robust filtration solutions. The need to adhere to the Industrial Emissions Directive, which sets strict limits on pollutants released into the atmosphere. Technological advancements have led to the development of wet electrostatic precipitators capable of handling high moisture content and sticky particles expanding their application scope. The transition towards cleaner industrial processes and the closure of coal fired power plants also influence market dynamics.

MARKET DRIVERS

Stringent environmental regulations and emission standards mandate advanced filtration adoption

The implementation of rigorous environmental regulations is majorly propelling the growth of Europe electrostatic precipitator market. The European Union’s Industrial Emissions Directive mandates that large combustion plants and industrial facilities limit their particulate matter emissions to extremely low levels often below 10 milligrams per normal cubic meter. According to the European Commission, over 50000 industrial installations across the EU are required to operate under best available techniques reference documents, which frequently specify electrostatic precipitation as the preferred technology for high volume gas streams. Non-compliance results in substantial fines and operational shutdowns forcing companies to invest in high efficiency filtration systems. The National Emission Ceilings Directive further reinforces these requirements by setting national limits for pollutants including PM2.5 and PM10. Countries such as Germany Poland and Italy have implemented even stricter national standards prompting upgrades to existing infrastructure. The legal imperative to maintain operating licenses ensures a consistent demand for electrostatic precipitators particularly in sectors like cement and steel where particulate loads are high.

Expansion of waste to energy and biomass power generation facilities fuels demand

The growing emphasis on circular economy principles and renewable energy sources has led to a significant expansion of waste to energy and biomass power plants, which is additionally escalating the growth of Europe electrostatic precipitator market. These facilities generate electricity by incinerating municipal solid waste or burning biomass materials which produces flue gases containing high levels of particulate matter and corrosive compounds. Electrostatic precipitators are essential in these applications due to their ability to handle large gas volumes and varying particle characteristics efficiently. The European Biomass Association reports that biomass energy production grew by 5% annually driven by policies aimed at reducing carbon dependency. Wet electrostatic precipitators are particularly favored in these settings as they can effectively capture fine particles and acid mists that dry systems may miss. The European Investment Bank has allocated billions of euros for green energy projects including waste to energy infrastructure further supporting market growth. These investments enable the construction of new facilities and the retrofitting of older ones with modern emission control systems.

MARKET RESTRAINTS

High initial capital investment and operational costs limit adoption among small enterprises

The substantial financial burden associated with the procurement installation and operation of electrostatic precipitators is additionally hampering the growth of Europe electrostatic precipitator market. These systems require complex engineering specialized materials and extensive infrastructure integration leading to high upfront costs. According to the European Federation of Chemical Industries, small and medium sized enterprises often face budget constraints that make it difficult to justify such large capital expenditures especially when profit margins are thin. The cost of high voltage power supplies collecting electrodes and rapping mechanisms contributes to the overall expense. Additionally, operational costs including electricity consumption for maintaining the electric field and regular maintenance of mechanical parts add to the financial strain. While larger corporations can absorb these expenses or access green financing smaller players struggle to compete. The return on investment period for electrostatic precipitators can extend several years depending on usage intensity and regulatory penalties avoided. This financial barrier slows down the replacement of outdated filtration systems with more efficient models. Consequently, many smaller facilities continue to operate with less effective technologies risking non-compliance. The lack of affordable financing options tailored for environmental upgrades further exacerbates this issue limiting market penetration in the fragmented industrial landscape.

Competition from alternative filtration technologies such as baghouses reduces market share

The intense competition from alternative air pollution control technologies, particularly fabric filters or baghouses, which offer distinct advantages in certain applications is also hindering the growth of Europe electrostatic precipitator market. Baghouses are often perceived as more effective for capturing very fine particulate matter and are less sensitive to changes in dust resistivity which can impair electrostatic precipitator performance. According to the International Society for Automation baghouse installations in European industrial facilities increased by 10% in 2024 due to their modular design and ease of maintenance. Fabric filters do not require high voltage power supplies reducing electrical complexity and potential safety hazards. They are also more compact making them suitable for facilities with limited space for retrofitting. Data from the European Industrial Filtration Association shows that baghouses are increasingly preferred in the pharmaceutical and food processing industries where hygiene and precise particle control are paramount. The versatility of filter media allows for customization based on specific chemical and thermal conditions providing a competitive edge. While electrostatic precipitators excel in high temperature and high volume applications baghouses are gaining ground in sectors requiring lower emission limits. This technological substitution threatens the dominance of electrostatic systems particularly in new installations where decision makers weigh the pros and cons of each technology. The ongoing improvement in baghouse materials and longevity further strengthens their position as a viable alternative.

MARKET OPPORTUNITIES

Retrofitting and upgrading existing industrial infrastructure presents significant growth potential

The aging industrial infrastructure through retrofitting and upgrade projects is substantially to level up new opportunities for the growth of Europe electrostatic precipitator market. Many existing systems were installed decades ago and no longer meet current emission standards or operate at optimal efficiency. Upgrading these units with modern components such as high frequency power supplies improved electrode designs and advanced control systems can significantly enhance performance. According to the European Confederation of Iron and Steel Industries over 40% of steel production facilities in Europe are planning major maintenance or upgrade cycles in the next five years. These projects often include the replacement of outdated precipitation systems to comply with tighter regulations. The European Union’s Modernisation Fund provides financial support for investments in modernizing energy systems and improving energy efficiency in lower income member states. This funding facilitates the adoption of advanced technologies without placing excessive burden on operators. Retrofitting is often more cost effective than building new installations allowing companies to extend the life of their assets while meeting regulatory requirements. Manufacturers of electrostatic precipitators can capitalize on this trend by offering customized upgrade packages and service contracts. The demand for digital monitoring and predictive maintenance solutions also creates opportunities for integrating smart technologies into legacy systems.

Integration of digital technologies and IoT for smart monitoring and maintenance

The integration of Internet of Things sensors and digital analytics into electrostatic precipitator systems is likely to boost the growth of Europe electrostatic precipitator market. Smart monitoring enables real time tracking of performance parameters such as voltage current opacity and pressure drop allowing for proactive maintenance and optimization. According to the European Digital Innovation Hubs, network the adoption of Industry 4.0 technologies in manufacturing has increased by 25% since 2022. These technologies facilitate predictive maintenance reducing unplanned downtime and extending equipment lifespan. Advanced algorithms can adjust operating conditions dynamically to maintain optimal efficiency despite variations in gas flow or dust load. This level of control ensures consistent compliance with emission limits and improves energy efficiency. Service providers can offer remote monitoring and diagnostic services creating new business models based on performance guarantees. The ability to collect and analyze large datasets helps identify trends and potential issues before they escalate.

MARKET CHALLENGES

Variability in dust resistivity affects collection efficiency and operational stability

The variability in dust resistivity, which significantly impacts collection efficiency is one of the major challenge for the growth of Europe electrostatic precipitator market. Dust resistivity determines how easily particles retain their charge and adhere to the collecting plates. If resistivity is too high particles may not release their charge quickly enough leading to back corona, which disrupts the electric field and reduces performance. Conversely low resistivity causes particles to lose their charge upon contact with the plate and become re entrained in the gas stream. According to the Institute of Energy and Process Engineering many industrial processes, such as cement kilns produce dust with highly variable resistivity due to changes in fuel composition and operating temperatures. This variability requires precise control systems and sometimes chemical conditioning agents to stabilize performance. Managing these variations requires sophisticated monitoring and adjustment capabilities which increase system complexity and cost. Failure to address resistivity issues can lead to non-compliance with emission standards and increased maintenance requirements. Operators must constantly balance operating parameters to maintain efficiency which demands skilled personnel and advanced automation.

Maintenance complexities and sensitivity to operating conditions hinder reliability

The electrostatic precipitators are complex mechanical and electrical systems that require regular and specialized maintenance to ensure reliable operation, which is another attribute to limit the growth of Europe electrostatic precipitator market. The presence of high voltage components moving parts such as rappers and insulators exposed to harsh environments makes them susceptible to wear and failure. According to the European Maintenance Society, unexpected breakdowns in air pollution control systems account for 20% of unplanned plant shutdowns in heavy industries. Insulator fouling due to dust accumulation or moisture can cause flashovers and power losses disrupting the precipitation process. Mechanical failures in rapping mechanisms can lead to dust buildup on plates reducing collection area and efficiency. The need for periodic shutdowns to clean and inspect internal components affects plant availability and productivity. Skilled technicians are required to perform these tasks safely and effectively but there is a shortage of qualified personnel in many European countries. Additionally, the sensitivity of these systems to changes in gas temperature humidity and flow rate requires constant monitoring and adjustment. Any deviation from optimal conditions can degrade performance rapidly. These maintenance burdens pose a significant challenge for operators seeking to minimize downtime and maximize efficiency in demanding industrial environments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.82% |

| Segments Covered | By Type, End User, Offering, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

| Market Leaders Profiled | FLSmidth, Siemens, Babcock & Wilcox Enterprises, Inc., John Wood Group PLC, SEI-Group Inc., KC Cottrell India, Balcke-Dürr GmbH, ELEX AG, S.A. HAMON, Beltran Technologies, Inc., Mitsubishi Hitachi Power, Ltd., Fujian Longking Co., Ltd., GEA Group Aktiengesellschaft, Thermax Limited, Sumitomo Heavy Industries, Ltd., BHEL, General Electric, AirPol, Zauba Technologies & Data Services Private Limited, and ECP Group Oy and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The dry electrostatic precipitator segment was the largest by holding a dominant share of the Europe market in 2025 with the extensive use of dry systems in power generation cement production and steel manufacturing where flue gases are typically low in moisture content. According to the European Cement Association over 90% of cement kilns in Europe utilize dry electrostatic precipitators to capture particulate matter from high temperature exhaust streams. The technology is well established and offers lower operational costs compared to wet systems as it does not require water treatment or corrosion resistant materials. Data from the International Energy Agency indicates that coal and biomass fired power plants which heavily rely on dry precipitation technologies still contribute significantly to the European energy mix despite the green transition. The simplicity of design and ease of maintenance make dry units preferable for large scale industrial applications. Furthermore, the ability to handle high gas volumes with minimal pressure drop enhances energy efficiency. Regulatory frameworks such as the Industrial Emissions Directive mandate strict particulate limits which dry electrostatic precipitators can consistently meet when properly maintained. The mature supply chain and availability of skilled technicians for dry systems further support their market leadership. Industries prefer dry systems for their proven reliability and long service life which reduces the total cost of ownership.

The wet electrostatic precipitator segment is likely to register a fastest CAGR of 7.5% during the forecast period owing to the increasing need to remove submicron particles acid mists and heavy metals from saturated flue gases which dry systems cannot effectively capture. According to the European Environment Agency, new regulations targeting PM2.5 and hazardous air pollutants have prompted industries to adopt wet precipitation technologies as a polishing step after traditional filtration. Waste to energy plants and chemical processing facilities are increasingly installing wet electrostatic precipitators to comply with these stricter standards. The ability of wet systems to achieve ultra low emission levels below 5 milligrams per normal cubic meter makes them indispensable for modern environmental compliance. Additionally, the rise in biomass combustion which produces sticky and hygroscopic ash favors wet technology due to its self-cleaning mechanism. Government incentives for upgrading pollution control infrastructure in older plants further accelerate adoption. The technological advancements in material science have reduced corrosion issues making wet systems more durable and cost effective.

By End User Insights

The power and electricity segment was the largest by capturing 40.2% of the Europe electrostatic precipitator market share in 2025 with the continued operation of coal biomass and waste to energy power plants which require robust particulate control systems to meet emission standards. According to Eurostat, thermal power generation accounted for 35% of total electricity production in the European Union in 2024 necessitating extensive use of air pollution control equipment. Large scale power stations generate vast volumes of flue gas containing fly ash which must be removed before release into the atmosphere. Electrostatic precipitators are the preferred technology due to their high efficiency and ability to handle large gas flows with low pressure drop. The retrofitting of older power plants with high frequency power supplies and improved electrode configurations extends the life of these assets, while ensuring compliance. Regulatory pressure under the Large Combustion Plants Directive mandates strict limits on particulate emissions driving continuous investment in electrostatic precipitation technology. The sector benefits from long term contracts and standardized specifications which facilitate bulk procurement.

The metal industry segment is anticipated to register a fastest CAGR of 6.8% from 2026 to 2034 with the modernization of steel production facilities and the increasing emphasis on recycling scrap metal which generates significant particulate emissions. According to the European Steel Association steel production in Europe reached 130 million tons in 2024 with electric arc furnaces accounting for a growing share of output. These furnaces produce fine dust containing zinc and other metals that require efficient capture systems. Electrostatic precipitators are increasingly used in secondary metallurgy processes to recover valuable metals and reduce environmental impact. Data from the European Bureau of Steel Recyclers indicates that scrap steel usage increased by 10% in 2024 driving demand for advanced filtration solutions in recycling plants. Strict regulations on heavy metal emissions particularly lead and cadmium compel metal producers to upgrade their air pollution control systems. The integration of electrostatic precipitators with oxygen steelmaking processes enhances overall plant efficiency and product quality. Investments in green steel initiatives including hydrogen-based reduction also involve sophisticated gas cleaning requirements.

By Offering Insights

The hardware and software segment was accounted in holding a significant share of the Europe electrostatic precipitator market in 2025 with the capital intensive nature of purchasing and installing electrostatic precipitator units which include collecting plates discharge electrodes high voltage power supplies and control systems. New industrial projects and major retrofits require substantial upfront investment in physical infrastructure. The complexity of modern electrostatic precipitators involves sophisticated software for monitoring and controlling operational parameters such as voltage current and rapping cycles. The hardware component includes durable materials such as stainless steel and specialized alloys designed to withstand harsh industrial environments. Software integration allows for real time data analysis and remote diagnostics which are critical for maintaining optimal performance. The lifecycle of hardware components typically spans 15 to 20 years ensuring long term revenue stability for manufacturers. Regulatory mandates for new facilities drive continuous demand for state of the art hardware solutions.

The services segment is projected to register the highest Compound Annual Growth Rate of 8.2% from 2025 to 2030. This rapid growth is attributed to the increasing need for regular maintenance inspection and optimization of existing electrostatic precipitator systems to ensure continuous regulatory compliance. Aging infrastructure requires frequent servicing including electrode cleaning insulator replacement and performance testing to maintain efficiency. Service providers offer specialized expertise in troubleshooting and upgrading legacy systems which is crucial for meeting evolving emission standards. The complexity of modern control systems requires skilled technicians for software updates and calibration. Regulatory inspections often mandate third party verification of system performance driving demand for auditing and certification services. Companies are shifting from reactive to proactive maintenance strategies to avoid unplanned downtime and penalties. The recurring nature of service contracts provides stable revenue streams for providers.

COUNTRY ANALYSIS

Germany Electrostatic Precipitators Market Analysis

Germany was the top performer in the Europe electrostatic precipitators market by holding 22.3% share in 2025. The country’s robust manufacturing sector, particularly in automotive steel and chemical industries drives significant demand for advanced air pollution control systems. According to the Federal Environment Agency Germany has some of the strictest emission standards in the world requiring industrial facilities to employ high efficiency filtration technologies. The Energiewende policy has led to the closure of coal plants but simultaneously increased the use of biomass and waste to energy facilities, which utilize electrostatic precipitators. The presence of leading technology providers and engineering firms in Germany fosters innovation and adoption of smart precipitation solutions. The country’s focus on Industry 4.0 integrates digital monitoring into industrial processes enhancing the appeal of advanced electrostatic precipitator systems. Regulatory enforcement is rigorous with frequent inspections ensuring compliance. The chemical industry in regions like North Rhine Westphalia relies heavily on these systems to manage hazardous particulates. Germany’s commitment to sustainability and technological leadership ensures sustained demand for high quality electrostatic precipitation equipment.

Poland Electrostatic Precipitators Market Analysis

Poland electrostatic precipitator market was ranked second by holding 18.2% of share in 2025 with its heavy dependence on coal for electricity generation. The European Union’s Industrial Emissions Directive has compelled Polish power plants to upgrade their existing electrostatic precipitators to meet stricter emission limits. The aging fleet of power stations requires frequent retrofitting and maintenance creating a steady demand for hardware and services. Poland’s strategic location and industrial growth in sectors such as cement and steel further contribute to market activity. Government subsidies and EU funds support the transition towards cleaner technologies facilitating the adoption of high efficiency precipitators. The country faces pressure to reduce air pollution levels which are among the highest in Europe driving urgent investments in filtration infrastructure. Local manufacturers and international suppliers compete to provide cost effective solutions tailored to the specific needs of Polish industries.

Italy Electrostatic Precipitators Market Analysis

Italy electrostatic precipitator market growth is likely to have a prominent opportunities throughput the forecast period with its active cement industry and expanding waste to energy sector. According to the Italian National Institute of Statistics, the construction sector remains a vital part of the economy driving continuous cement production, which requires efficient dust collection systems. The country has been investing heavily in waste to energy plants to reduce landfill usage with many new facilities incorporating wet electrostatic precipitators for superior emission control. Regulatory frameworks such as the Integrated Pollution Prevention and Control permit system enforce strict limits on industrial emissions prompting upgrades to existing infrastructure. The geographical distribution of industrial clusters in Northern Italy creates concentrated demand for air pollution control solutions. Italian companies are increasingly adopting sustainable practices aligning with European Green Deal objectives. The presence of specialized engineering firms facilitates the customization of precipitation systems for diverse applications. Tourism and urban density also drive stricter local air quality regulations influencing industrial operations.

France Electrostatic Precipitators Market Analysis

France electrostatic precipitator market growth is driven with its diverse industrial base and energy policies. While nuclear power dominates electricity generation limiting demand from coal plants the country has a significant presence in steel aluminum and chemical manufacturing. According to the French Ministry of Ecological Transition industrial emissions are tightly regulated under national laws that align with EU directives. The modernization of older industrial facilities particularly in the steel sector has driven demand for upgraded electrostatic precipitators. The waste to energy sector is also expanding as France aims to reduce waste disposal through incineration with energy recovery. These facilities require advanced filtration systems to handle complex flue gas compositions. The government’s support for circular economy initiatives encourages the adoption of technologies that enable resource recovery from industrial dust. French engineering companies are known for their expertise in designing customized air pollution control solutions.

United Kingdom Electrostatic Precipitators Market Analysis

The United Kingdom electrostatic precipitator market growth is likely to drive with the reduced coal fired power generation but has expanded its waste to energy and biomass capacity to meet renewable energy targets. According to the Department for Business Energy and Industrial Strategy, waste incineration with energy recovery accounted for 10% of electricity generation in 2024. These facilities extensively use electrostatic precipitators to control particulate emissions from burning municipal solid waste and biomass. The steel industry in regions such as South Wales and Scotland also contributes to market activity through ongoing modernization projects. The UK’s commitment to net zero emissions by 2050 encourages the adoption of efficient and low carbon technologies. Local manufacturers and international suppliers collaborate to provide innovative solutions tailored to the UK market. The focus on reducing industrial air pollution and improving public health sustains the demand for high performance electrostatic precipitators.

COMPETITIVE LANDSCAPE

The competition in the Europe electrostatic precipitator market is characterized by the presence of established global giants and specialized regional manufacturers who compete on technology quality and service excellence. Major players differentiate themselves through innovative features such as digital monitoring systems and energy efficient designs that appeal to environmentally conscious industries. The market sees intense rivalry in the service segment where companies offer comprehensive maintenance packages to ensure operational continuity and regulatory compliance. Price competition is moderate as buyers prioritize reliability and performance over initial cost savings due to strict emission norms. Strategic collaborations with engineering consultants and plant operators help manufacturers secure large scale projects and retrofits. The entry of new technologies such as wet electrostatic precipitators for fine particle removal adds complexity to the competitive landscape. Companies must continuously adapt to evolving regulations and customer preferences to maintain their market position. Intellectual property protection and brand reputation play crucial roles in sustaining competitive advantage.

KEY MARKET PLAYERS

These are the market players that are dominating the Europe electrostatic precipitator market.

- FLSmidth

- Siemens

- Babcock & Wilcox Enterprises Inc.

- NC, John Wood Group PLC

- SEI-Group Inc

- KC Cottrell India

- Balcke-Dürr GmbH

- ELEX AG, S.A.

- HAMON

- Beltran Technologies, Inc.

- Mitsubishi Hitachi Power, Ltd

- Fujian Longking Co., Ltd

- GEA Group Aktiengesellschaft

- Thermax Limited

- Sumitomo Heavy Industries, Ltd

- BHEL

- General Electric

- AirPol

- Zauba Technologies & Data Services Private Limited

- ECP Group Oy

Top Players In The Market

- General Electric Vernova is a global technology leader providing advanced air pollution control solutions including high efficiency electrostatic precipitators for power and industrial sectors. The company contributes significantly to the global market by offering integrated systems that combine hardware with digital monitoring capabilities. Recent actions include the launch of upgraded high frequency power supplies that enhance collection efficiency while reducing energy consumption. GE Vernova has strengthened its position by expanding service contracts focused on predictive maintenance using artificial intelligence. These initiatives help industrial clients maintain compliance with stringent European emission standards. The company actively collaborates with utility providers to retrofit aging infrastructure ensuring prolonged asset life.

- Thermax Limited is a prominent international player specializing in energy and environment solutions with a strong presence in the European electrostatic precipitator market. The company delivers customized dry and wet precipitation systems tailored to diverse industrial applications such as cement steel and waste to energy. Thermax contributes to the global market by exporting engineered solutions that meet rigorous international safety and performance standards. Recent actions include the establishment of specialized research and development centers in Europe to innovate low emission technologies. The company has strengthened its market position through strategic partnerships with local engineering firms to enhance installation and support services. Thermax focuses on modular designs that facilitate easier retrofitting in space constrained facilities. Their emphasis on sustainable manufacturing practices aligns with European regulatory requirements. This comprehensive approach enables the company to address complex air quality challenges effectively while maintaining competitive advantage in the evolving market landscape.

- Mitsubishi Power is a leading provider of advanced power generation and environmental solutions including state of the art electrostatic precipitators for industrial use. The company plays a vital role in the global market by delivering reliable and efficient air pollution control technologies for large scale projects. Mitsubishi Power contributes to Europe by supplying robust systems designed to handle high volume flue gases with minimal operational disruption. Recent actions include the integration of Internet of Things sensors into precipitation units for real time performance monitoring. This innovation allows for proactive maintenance and optimized energy usage strengthening its market position. The company has expanded its service network in Europe to provide faster response times and technical support. Mitsubishi Power emphasizes collaboration with clients to develop bespoke solutions that meet specific regulatory and operational needs.

Top Strategies Used By The Key Market Participants

Key players in the Europe electrostatic precipitator market primarily focus on technological innovation and digital integration to enhance system efficiency and reliability. Companies invest heavily in research and development to create advanced power supplies and smart monitoring tools that reduce energy consumption and maintenance costs. Strategic partnerships with local engineering firms enable better customization and faster deployment of solutions tailored to specific industrial needs. Expansion of service portfolios including predictive maintenance and remote diagnostics helps build long term customer relationships and recurring revenue streams. Compliance with stringent environmental regulations drives the adoption of high performance filtration technologies ensuring market relevance. Manufacturers also prioritize sustainability by using recyclable materials and optimizing production processes to minimize carbon footprints.

MARKET SEGMENTATION

This research report on the Europe electrostatic precipitator market is segmented and sub-segmented into the following categories.

By Type

- Dry ESP

- Wet ESP

By End User

- Power & Electricity

- Metal

- Cement

- Chemicals

- Others

By Offering

- Hardware & Software

- Services

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is currently driving growth in the Europe electrostatic precipitator market?

Strict emission regulations and rising focus on air pollution control are driving market growth.

Why are electrostatic precipitators widely used in industrial applications?

They effectively remove particulate matter from exhaust gases.

How would you explain an electrostatic precipitator in simple terms?

It is a device that uses electrical charges to capture and remove dust particles from air or gas streams.

Where are electrostatic precipitators most commonly used across Europe?

They are widely used in power plants, cement plants, and industrial facilities.

What makes electrostatic precipitators important for environmental protection?

They help reduce air pollution and improve emission quality.

From an operational standpoint, are electrostatic precipitators a worthwhile investment?

Yes, they ensure compliance with environmental standards and improve air quality.

What challenges are affecting the Europe electrostatic precipitator market?

High installation costs and maintenance requirements are key challenges.

How is industrial activity influencing demand for electrostatic precipitators?

Growing industrial operations increase the need for effective emission control systems.

Which sectors contribute the most to electrostatic precipitator demand?

Power generation, cement, and manufacturing industries are major contributors.

Is the Europe electrostatic precipitator market growing steadily?

Yes, it is expanding with increasing environmental regulations.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com