Europe Filters Market Size, Share, Trends & Growth Forecast Report By Product Type, Application, and By Country (Germany, France, United Kingdom, Italy, Netherlands, Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Filters Market Summary

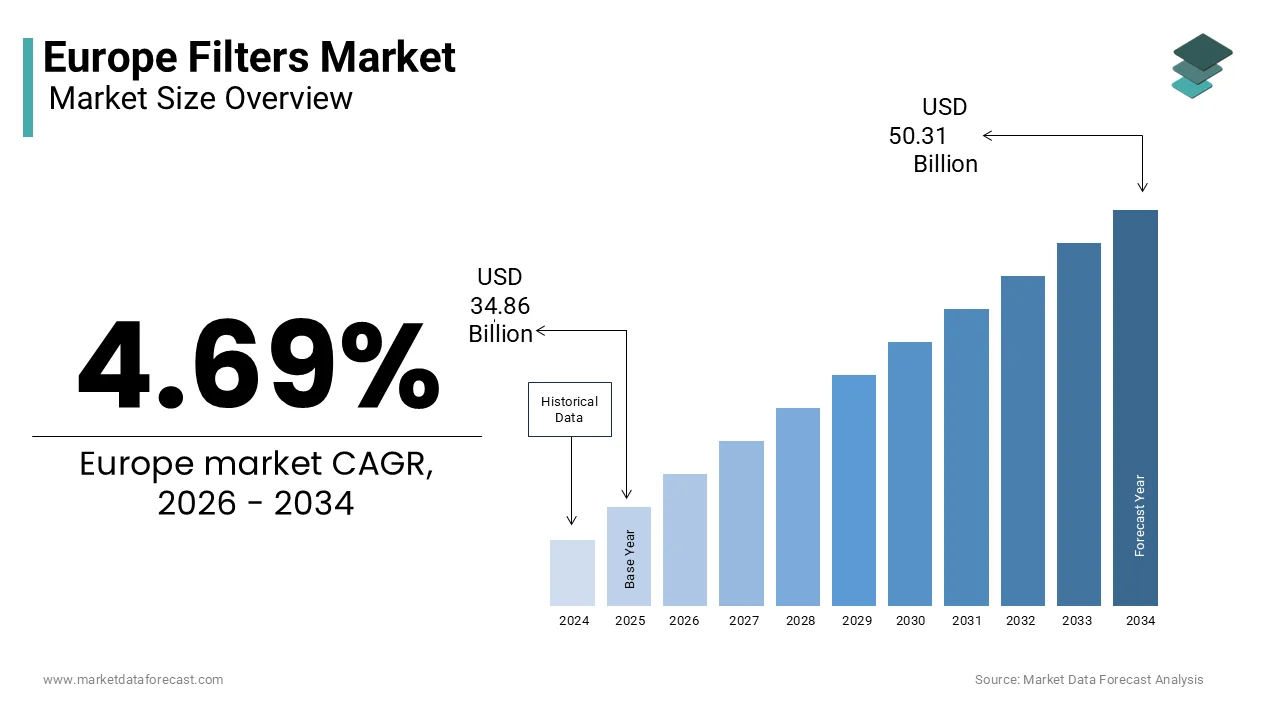

The Europe filters market, valued at USD 33.30 billion in 2025, is projected to reach USD 50.31 billion by 2034, growing at a CAGR of 4.69% driven by stringent EU air and water regulations, biopharmaceutical expansion, and infrastructure retrofitting.

Key Market Highlights

- 2025 Market Size: USD 33.30 billion

- 2026 Market Size: USD 34.86 billion

- 2034 Forecast: USD 50.31 billion

- CAGR (2026–2034): 4.69%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Enforcement of EU air quality and Industrial Emissions Directives

- Expansion of biopharmaceutical and advanced therapy manufacturing

- Mandatory HEPA and ULPA filtration in healthcare and laboratories

- Rising municipal wastewater and drinking water treatment upgrades

- Automotive demand for cabin air and emission control filters

Principal Restraints

- Complex certification and validation requirements across EN, ISO, and EU MDR standards

- Lengthy time-to-market for innovative filter media

- Volatility in critical raw material supply chains (PTFE, glass microfiber)

- Limited domestic production of specialty filtration materials

High-Value Opportunities

- Growth of hydrogen infrastructure requiring ultra-pure gas filtration

- Retrofitting of aging municipal water treatment plants with membrane systems

- Rising adoption of single-use filtration in biologics manufacturing

- Demand for microplastic and PFAS removal under revised EU Drinking Water Directive

Key Market Challenges

- Shortage of skilled filtration system technicians across Europe

- Improper installation and maintenance impacting system integrity

- Fragmented end-of-life recycling and disposal infrastructure

- Limited circular economy pathways for spent filter media

Fastest-Growing Segments

- Water Filters: 8.1% CAGR — membrane filtration and contaminant removal

- Food & Beverage Applications: 8.9% CAGR — clean label and shelf-life extension

- Single-Use Biopharma Filters: rapid uptake under GMP Annex 1 compliance

Regional Leadership & Dynamics

- Germany (25.3%) — industrial density, pharma manufacturing, strict emissions law

- France (12.3%) — nuclear energy, water treatment upgrades, biopharma demand

- United Kingdom — life sciences, healthcare filtration, offshore oil & gas

- Italy — food & beverage processing, wastewater modernization

- Netherlands — logistics hub, chemicals, port-based filtration demand

What Wins Commercially

- Compliance with EU GMP Annex 1, ISO 16890, and EN 1822 standards

- High-efficiency membrane and HEPA technologies

- Integrated digital monitoring and integrity testing

- Local manufacturing and rapid validation support

- Proven performance in regulated, mission-critical environments

Top Strategic Ask for Executives

Invest in membrane innovation, secure critical raw material supply, and expand circular filtration solutions while aligning product roadmaps with EU regulatory milestones in air, water, and pharmaceutical safety.

Leading Players

Some of the companies that are playing a dominating role in the Europe filters market include:

- Donaldson Company

- MANN+HUMMEL

- Freudenberg Filtration Technologies

- Pall Corporation

- Camfil

- Parker Hannifin

- Eaton

Europe Filters Market Size

The europe filters market was valued at USD 33.30 billion in 2025 and increased to USD 34.86 billion in 2026. The market is projected to reach USD 50.31 billion by 2034, growing at a CAGR of 4.69% during the forecast period from 2026 to 2034.

Filters are engineered devices or media designed to remove particulate contaminants or impurities from air, liquids, and gases across industrial,l commercial, and residential applications. These range from high efficiency particulate air (HEPA) filters in healthcare settings to coalescing filters in petrochemical processing and membrane cartridge,s in pharmaceutical water systems. According to Eurostat, over 220 million cubic meters of municipal wastewater were treated daily across the EU in 2025, necessitating advanced filtration trains to meet discharge limits under the Urban Wastewater Treatment Directive. As per the European Environment Agency, more than 14000 industrial installations operate under the Industrial Emissions Directive, requiring continuous emission monitoring and filtration to control dust, heavy metals, and volatile organic compounds. Furthermore, the European Centre for Disease Prevention and Control mandates HEPA or equivalent filtration in all biosafety level 3 laboratories, of which there are over 120 in the EU, to contain a,irborne pathogens. This regulatory density, combined with Europe’s aging infrastructure retrofitting needs and commitment to circular water and air economy, es positions filtration not as an ancillary component but as an enabler of public health, environmental compliance, and industrial efficiency.

MARKET DRIVERS

Stringent EU Air Quality Directives Drive Adoption of Advanced Filtration in Industrial and Urban Settings

The aggressive legislative frameworkon ambient air pollution for high-performance filter deployment across energy manufacturing and transportation sectors, which is a major driving factor for the growth of Europe filters market. This target compels industrial facilities to upgrade from conventional baghouses to pulse jet fabric filters with PTFE membrane surfaces capable of capturing submicron particles. The European Environment Agency reported that in 2025, over 18000 industrial plants submitted filtration upgrade plans to comply with Best Available Techniques conclusions under the Industrial Emissions Directive. In Germany, the Federal Immission Control Act now requires cement kilns and steel mills to achieve dust emission limits below 10 milligrams per cubic meter, only attainable with advanced cartridge or sintered metal filters. Similarly, urban initiatives like Paris’s Low Emission Zone mandate particulate filters on all diesel delivery vans registered before 2011.

Expansion of Biopharmaceutical Manufacturing Intensifies Demand for Sterile Liquid Filtration Systems

The elevated requirements for sterile and viral retentive liquid filtration in drug production and quality controareis leveraging the growth of Europe filters market. According to the European Medicines Agency, 42 monoclonal antibody therapies and 28 advanced therapy medicinal products received marketing authorization in the EU in 2025, therapies that rely on multi-stage filtration for buffer clarification, virus removal, and final sterile filtration. These processes demand 0.22 micron sterilizing grade membrane filters validated under ASTM F838 and capable of withstanding aggressive cleaning agents like sodium hydroxide. In Ireland, the IDA r,,eported that biopharma investments exceeded 5.2 billion euros in 2025, with new facilities from Pfizer and AbbVie incorporating single-use filtration skids to minimize cross-contamination. Similarly, Germany’s BioPharma Cluster Alliance documented a 29% increase in filter cartridge consumption across contract development and manufacturing organizations in 2025. The European Pharmacopoeia’s updated monograph 2.6.1 now requires extractable profiling for all filters in parenteral production, further raising technical barriers. This emergence of therapeutic innovation, regulatory stringency,y and manufacturing scale ensures robust and non-cyclical demand for high-integrity liquid filtration solutions.

MARKET RESTRAINTS

Complex Certification and Validation Requirements Prolong Time to Market for New Filter Technologies

The significant delays in commercializing innovative media due to fragmented and evolving regulatory validation protocols are restraining the growth of Europe filters market. According to the European Committee for Standardization,n over 27 distinct EN and ISO standards govern filter performance testing from EN 779 for general ventilation to ISO 16890 for particulate air filters, yet these lack harmonized test aerosols or efficiency metrics for emerging nano,ib er, or electrostatic media. In the medical device segment, the EU Medical Device Regulation requires extensive biocompatibility and sterility validation for any fluid pathway component, including filter housings, which can extend product launch timelines by 14 to 18 months, as per MedTech Europe’s 2025 compliance survey. Similarly, the European Chemicals Agency’s REACH regulation mandates full substance disclosure for all filter media components even at trace level,s complicating proprietary formulations. Moreover, notified bodies remain backlogged, ed with only 19 authorized for Class IIa filtration devices.

Volatility in Critical Raw Material Supply Chains Disrupts Filter Media Production

The i,mported specialty materials for high-performance filter media are limited by geopolitical and logistical instability that directly impacts production continuity, which is additionally limiting the growth of Europe filters market. Similarly, glass microfiber is essential for HEPA filters, which is predoare subject minantly manufactured in Japan and South Korea, with European converters facing 30% price increases in 2025, due to energy-driven production cuts in Asia. The European Commission’s Critical Raw Materials Act 2025 identified PTFE and specialty glass fibers as “strategically vulnerable”; no domestic alternatives exist. In Sweden, a major HVAC filter producer halted production for three weeks in Q2 2025 due to PTFE shortages. This supply fragility undermines Europe’s ambition for technological sovereignty in clean air and water infrastructure.

MARKET OPPORTUNITIES

Growing Deployment of Hydrogen Infrastructure Creates New Demand for Ultra-Clean Gas Filtration

The strategic investment in green hydrogen is unlocking a high-value niche for ultra-high purity gas filters in production, storage, and refueling systems. This factor expectedlly to create new opportunities for the growth of Europe filters market. According to the European Hydrogen Backhigh-valueiative over 28000 kilometers of hydrogen pipelines are planned by 2030, requiring particulate and coalescing filters at every compressor station to prevent turbine erosion and fuel cell contamination. The EU’s Fuel Cell and Hydrogen Joint Undertaking mandates that hydrogen for mobility must meet I, SO 14687 purity standard,s allowing no more than 0.1 milligrams per cubic meter of particulates, necessitatinmulti-stagege filtration with absolute-rated membrane elements. In Germany, the National Hydrogen Strategy allocated 2.3 billion euros in 2025 forelectrolyzers andd refueling infrastructure, where each refueling station integrates 4 multi-stage pressure filters rated for 1000 bar service. Similarly, the Port of Rotterdam’s Hydrogen Hub project installed over 200 coalescing filters in its pilot pipeline network in 2025 to remove moisture and lubricants from recycled hydrogen streams. As per the European Committee for Standardization, a new technical specification for hydrogen gas filters (CEN/TS 17900) was published in late 2025, creating a dedicated regulatory pathway.

Retrofitting of Aging Municipal Water Treatment Plants Drives Demand for Membrane Filtration Upgrades

The aging water infrastructure is a transformational shift toward membrane-based filtration to meet stricter drinking water standards and combat emerging contaminants, which is also to level up new opportunities for the growth of Europe filters market. According to the European Environment Agency, over 60% of EU wastewater treatment plants were constructed before 1991 and lack advanced tertiary treatment capabilities. The revised EU-Drinking Water Directive 2020/2184 now requires monitoring and removal of microplastics, perfluoroalkyl substances, and endocrine disruptor contaminants, which can be effectively addressed only by ultrafiltration or nanofiltration membranes. Similarly, Spain’s Ministry fr Ecological Transition reported that 78 municipal fac, ilities installed hollow, fiber ultrafildisruptordules in 2025 to replacan be can be ce outdated sand filters. The government support through investments for membrane retrofits in Central and Eastern Europe will also enhance the growth of the segment. These investments are not cyclical but regulatory driven, creating adecade-longg pipeline for hollow fiber and spiral wound filter elements across the region.

MARKET CHALLENGES

Technical Skill Shortage in Filter System Maintenance Undermines Operational Reliability

A growing deficit of trained technicians capable of installing and maintaining advanced filtration systems is eroding performance reliability across industrial and municipal sectors, and additionally, to leverage new opportunities for the growth of Europe filters market. According to the European Federation of National Engineering Associations, over 430000 skilled maintenance roles remain unfilled in the EU’s i, a, andstrial sector, as of 2025, with filtration specialists particularly scarce in membrane and HEPA applications. This gap leads to improper installation, premature media failure, and undetected bypass issues that compromise entire processes. A Swedish pharmaceutical plant experienced a sterility breach traced to a misaligned filter housing during routine replacement. Similarly, the European Wastewater Association documented that 22% of membrane plant downtime in 2025 resulted from operator error rather than equipment failure. While digital monitoring helps, hands-on expertise in torque calibration, housing alignment, and post installation testing remains irreplaceable.

Fragmented End-of-Life Management and Recycling Infrastructure Limits Circular Economy Potential

The lack of stand-alone systems for recovering and recycling spent media creates environmental and regulatory liabilities, significantly degrading the growth of Europe filters market. According to the European Environment Agency, less than 12% of industrial liquid filters and fewer than 5% of HVAC filters are recycled in the EU due to contamination with oil, heavy metals, or biohazards that complicate material recovery. Used HEPA filters from hospitals are classified as hazardous waste in 18 member states, requiring incineration at over 1100 degrees Celsius, as per national transpositions of the Waste Framework Directive. In 2025, France banned the landfilling of all filter cartridges containing synthetic media, forcing users to seek costly disposal solutions. While companies like Pall and Donaldson have launched ttake-backprograms these cover less than 8% of the market due to logistics costs and lack of reverse collection infrastructure. The European Commission’s upcoming revision of the End of Waste criteria does not include filtration media, leaving producers without clear regulatory pathways for circular claims.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Donaldson Company, Inc., Mann+Hummel GmbH, Freudenberg Filtration Technologies, 3M Company, Parker Hannifin Corporation, Cummins Inc. (Fleetguard), Camfil AB, Bosch Rexroth AG, Sogefi SpA, Pall Corporation (an affiliate of Danaher), Ahlstrom-Munksjö, Eaton Corporation plc, Filtration Group Corporation, Aeroquip (Eaton brand), Clarcor Inc. (now Parker Hannifin), Kolbenschmidt Pierburg AG, Mahle GmbH, Hengst SE, Purafil, Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

The air filters segment accounted in holding 46.3% of the European filters market share in 2025, with the stringent indoor and outdoor air quality mandates across residential, commercial, and industrial domains. The European Environment Agency confirmedt 96% of urban EU citizens experienced PM2.5 levels exceeding World Health Organization guidelines in 2025, intensifying demand for high-efficiency particulate air filtration in HVAC systems. In healthcare, the European Centre for Disease Prevention and Control requires all hospitals to maintain ISO Class 5 or better air cleanliness in operating theatres, a standard only achievable with HEPA or ULPA filters. Germany’s Energy Saving Ordinance mandates M6 or higher efficiency filters in all non-residential buildings undergoing ventilation upgrades, which affected over 120000 facilities in 2025 alone, as per the survey. Additionally, the automotive sector integrated cabin air filters with activated carbon layers in 98% of new passenger vehicles sold in the EU in 2025, according to the study. This regulatory and public health-driven option across multiple sectors solidifies air filtration as the market’s cornerstone.

The water filters segment is expected to witness the fastest CAGR of 8.1% from 2025 to 2033 in the coming years with the EU’s revised Drinking Water Directive, which for the first time established binding limits for emerging contaminants, including microplastics, fluoroalkyl substances, and endocrine disrupting compouthe nds. Municipalities across Western Europe are retrofitting conventional treatment trains with ultrafiltration and nanofiltration membranes to comply with these standards. France’s National Water Agency committed 2.7 billion euros to install membrane filtration systems in 310 water treatment plants serving over 25 million residents. Similarly, the Netherlands’ Delta Programme allocated 850 million euros in 2025 for advanced water purification infrastructure, including ceramic and hollow fiber filters to secure drinking water resilience against drought induced saltwater intrusion. Beyond public supply, the European Food Safety Authority mandated stricter microbial control in bottled water production, prompting Nestlé and Danone to upgrade to 0.2 micronsterilizing filterss.

By Application Insights

The pharmaceuticals and medical application segment held 28.3% of the European filters market share in 2025, due to non-negotiable sterility and purity requirements across drug manufacturing, diagnostics, and patient care. Every parenteral drug produced in the EU must undergo 0.22 micron sterilizing grade filtration validated, per European Pharmacopoeia Chapter 2.6.14, with a protocol that consumes millions ofmembranes, cartridges, annually. In 2025, the European Medicines Agency approved 127 new active substances, the majority of which were biologics requiring virus-retentive filtration during downstream processing. Germanyalone hosts 580 pharmaceutical manufacturing sites, all operating under EU GMP Annex 1, which mandates redundant filtration and integrity testing for all aseptic processes. The rise of advanced therapy medicinal products, such as CAR T cell therapy, has intensified the use of single-use capsule filters to prevent cross-contamination. This combination of regulatory rigor, therapeutic complexity,y and healthcare infrastructure ensures the segment’s continued dominance.

The food and beverage segment is likely to grow at the fastest CAGR of 8.9% thcross-contaminationst period owing to the tightening food safety regulations, rising consumer demand for clean label products,s and the expansion of ambient shelf-life technologies. The European Commission’s Regulation (EC) No 852/2004 requires all liquid food processors to implement validated filtration systems to eliminate spoilage microorganisms, a rule affecting over 28000 dairy, es breweries, and juice producers. Danone reported installing 1200 new cross-flow microfiltration units across its European yogurt lines to replace thermal pasteurization and preserve probiotic viability. Plant-based beverage producers like Oa, tly, and Alpro now use depth and membrane filters to achieve colloidal stability in oat and soy drinks, a necessity given rising exports to Asia with strict clarity requirements.

COUNTRY LEVEL ANALYSIS

Germany Filters Market Analysis

Germany is the largest contributtto of Europe filters market by holding 25.3% of the share in 2025, with its advanced industrial base, stringent environmental rregulations and dense healthcare infrastructure. The country’s 580 pharmaceutical plants represent the highest concentration in Europe, consuming more than 120 million sterilizing-grade filter cartridges annually, as per VDMA Pharma. Additionally, Germany’s Energiewende policy accelerated the adoption of gas filtration in biogas upgrading plants with over 9500 facilities using coalescing and activated carbon filters to purify methane for grid injection. The Federal Ministry for Economic Affairs and Climate Action allocated 320 million euros in 2025 for filter technology innovation under its High-Tech Strategy 2025. This convergence of manufacturing intensity, regulatory enforcement, and public investment ensures Germany’s unrivaled position as the market’s technological and consumption epicenter.

France Filters Market Analysis

France's filter market was positioned next with 12.3% of share in 2025, with the nuclear energy,y water infrastructure, and pharmaceutical production. According to the French Nuclear Safety Authority, all 56 operational reactors usemulti-stagee particulate and ion exchange filters in primary and secondary cooling loops to prevent corrosion and radioactive transport. The National Water Agency reported that 78% of municipal water treatment plants underwent membrane filtration retrofits in 2025 to comply with new microcontaminant limits. Sanofi and Servier operate 34biopharma facilitiess across the country requiring sterile filtration for monoclonal antibodies and vaccines consumption that grew by 22% in 2025. Moreover, France’s Loi Climat et Resilience mandates M6-rated air filters in all public buildings undergoing energy renovation, a rule affecting over 45000 schools and administrative centers.

United Kingdom Market Analysis

The United Kingdom's filtermarket is expected to have steady opportunities in the coming years with its strong life sciences sector and post regulatory autonomy. According to the Medicines and Healthcare products Regulatory Agency, over 90 new Kingdom's filter-entered clexpectedrials in the UK in 2025, each requiring extensive sterile and virus filtration during development and manufacturing. The National Health Service maintains 132 high containment isolation units, all equipped with ULPA filters meeting EN 1822 standards, as mandated by Public Health England. Additionally, the UK’s Environmental Improvement Plan 2025 introduced stricter emission limits for industrial combustion plants, driving the adoption of fabric filter bags with PTFE membranes. The Oil & Gas Authority reported that 68% of North Sea platforms upgraded their produced water filtration systems in 2025 to meet OSPAR Commission discharge standards.

Italy Filters Market Analysis

Italy's filter market growth is expanding with its extensive food and beverage processing sector, automotive manufacturing, and aging municipal infrastructure. The country’s 17000 wineries alone consumed over 45 million filtration moItaly's filter, as per the Italian Wine Union. In automotive, Fiat’s Mirafiori plant integrated cabin air filters with electrostatic media in all new vehicles to comply with EU urban air quality targets. Moreover, Italy’s National Recovery and Resilience Plan allocated 1.2 billion euros in 2025 for wastewater treatment upgrades, including membrane bioreactor installations in 210 cities. The Italian National Institute of Health also mandated HEPA filtration in all regional diagnostic laboratories following pandemic preparedness reviews. This combination of agro-industrial heritage infrastructure, modernization, and public health policy generates consistent multi-sectoral demand.

Netherlands Filters Market Analysis

The Netherlands ' filter market growth is expected to grow with the logistics hub, advanced horticulture, and chemical cluster. According to the Dutch Ministry of Infrastructure and Water Management, the Port of Rotterdam is the largest in Europe, requiring all bunkering and expectedties to install coalescing filters to prevent hydrocarbon discharge into the Rhine Meuse delta. Additionally, the Chemelot industrial park in Geleen hosts 120 chemical plants,s all operating under strict Best Available Techniques requiring sintered metal and cartridge filters for solvent recovery. This concentration of high-tech agriculture, energy, and chemical operations makes the Netherlands a high val,ue niche market with outsized technological influence.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe filters market include

- Donaldson Company, Inc.

- Mann+Hummel GmbH

- Freudenberg Filtration Technologies

- 3M Company

- Parker Hannifin Corporation

- Cummins Inc. (Fleetguard)

- Camfil AB

- Bosch Rexroth AG

- Sogefi SpA

- Pall Corporation (an affiliate of Danaher)

- Ahlstrom-Munksjö

- Eaton Corporation plc

- Filtration Group Corporation

- Aeroquip (Eaton brand)

- Clarcor Inc. (now Parker Hannifin)

- Kolbenschmidt Pierburg AG

- Mahle GmbH

- Hengst SE

- Purafil, Inc.

COMPETITIVE LANDSCAPE

Competition in the European filters market is highly segmented, featuring a mix of global technology leaders and regional specialists, each dominating distinct application niches. Large multinational corporations such as Pall Donaldson and MANN+HUMMEL lead in high-value regulated sectors like pharmaceuticals, automotive, and semiconductor manufacturing, ng where certification, technical support, and reliability outweigh price. Meanwhile,e hundreds of mid-sized European firms compete in municipalhigh-valueC and general industrial filtration based on customization,omization local service, and cost efficiency. Innovati is concentrated in membrane science digital integration, nd sustainablmid-sizedith significant R&D collaboration between industry and institutions like Fraunhofer and TNO. Despite intense competition, price pressure remains moderate in technical segments but acute in commoditized areas such as standard HVAC filters. This bifurcated landscape rewards regulatory agility, technological differentiation,n and deep application expertise.

TOP LEADING PLAYERS IN THE MARKET

- Pall Corporation is a global leader in filtration, separation, and purification technologies with a deeply entrenched presence across Europe’s pharmaceutical, biotech,h and industrial sectors. The company supplies critical sterile liquid and gas filtration systems compliant with EU G, MP Annex 1, and European Pharmacopoeia standards. Its Mustang membrane chromatography and Supor capsule fil,ters are widely used in monoclonal antibody and vaccine production across Ireland, Germany, and Switzerland. Pall expanded its single-use filtration manufacturing capacity at its Portsmouth,th UK, facility to meet rising demand from European contract development and manufacturing organizations. It also launched a digital integrity testing platform enabling real-time remote validation of filter performance in regulated environments. These initiatives reinforce Pall’s role as a technology enabler of Europe’s advanced therapy and biologics ecosystem.

- Donaldson Company is a US-based multinational with a robust European footprint in industrial air and liquid filtration, serving automotive, power generation, and off-highway equipment markets. The company’s PTFE membrane-based filter cartridges and Synteq XP media are standard in diesel particulate and crankcase ventilation systems across German and French automotiv e OEMs. Donaldson o,,peroff-highwaycturing facilities in Belgium, Germany, nd the UK producing over 150 million filter elements annually for the European market. In early 2025, the company introduced a new generation of hydrophobic air filters for hydrogen compressor stations in the Netherlands and Spain, aligned with the European Hydrogen Backbone requirements. It also enhanced its filter monitoring IoT platform to support predictive maintenance in industrial settings. These actions demonstrate Donaldson’s commitment to sustainability and digital integration in core European industrial applications.

- MANN+HUMMEL is a Germany-headquartered filtration specialist with global leadership in automotive cabin air and industrial process filtration. The company supplies cabin filters with activated carbon and bio-based media to virtually every major European carmaker, including Volkswagen, BMW, and Stellantis. Beyond mobility, it provideshigh-efficiencyy air filtration solutions for hospitals, data centers, and microelectronics cleanrooms across the EU. In 2025, MANN+HUMMEL launched its “Pure Air for Europe” initiative, integrating real-time air quality sensors into HVAC filter housings for smart buildings in France and Sweden. It als,o scaled production of its EUV cleanroom filters at its Ludwigsburg facility to support semiconductor investments under the European Chips Act. These strategic moves position the company at the convergence of mobility, sustainability, and digital infrastructure.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European filters market focus on vertical integration of membrane media development and filter element manufacturing to ensure performance consistency and supply security. They invest heavily in digitalization through IoT-enabled condition monitoring and remote integrity verification to enhance service offerings. Companies align product portfolios with EU regulatory milestones, including the Industrial Emissions Directive, the Drinking Water Directive, and GMP Annex 1. Strategic expansion of single-use and bio-based filtration solutions supports pharmaceutical and food industry sustainability goals. Additionally, firms establish local manufacturing and validation centers to shorten lead times and comply with data sovereignty and quality documentation requirements across member states.

MARKET SEGMENTATION

This research report on the europe filters market is segmented and sub-segmented into the following categories.

By Product Type

- Air Filters

- Water Filters

By Application

- Pharmaceuticals & Medical

- Food & Beverage

- Industrial

- Residential

- Commercial

By Country

- Germany

- France

- United Kingdom

- Italy

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. What drives growth in the Europe Filters Market?

Growth in the Europe Filters Market is primarily driven by strict EU environmental regulations, such as Euro 7 emission norms, and increasing industrialization in sectors like automotive and manufacturing. Urban pollution concerns and health-focused filtration in vehicles boost demand, especially for air and cabin filters.

2. Who are the top players in the Europe Filters Market?

Leading companies in the Europe Filters Market include Mann+Hummel, Donaldson, MAHLE, Freudenberg Filtration Technologies, and Sogefi Group. These firms dominate automotive air filters and industrial filtration, with strong manufacturing bases in Germany.

3. What is the role of Germany in the Europe Filters Market?

Germany holds the largest share in the Europe Filters Market, particularly in industrial air filtration and automotive segments, valued at billions with high CAGRs. Its dominance stems from major manufacturers like Mann+Hummel and robust construction and automotive sectors.

4. How do EU regulations impact the Europe Filters Market?

EU regulations like Euro 7 and Euro VI-D standards significantly propel the Europe Filters Market by mandating advanced filtration to reduce emissions. This drives innovation in nanofiber and high-efficiency filters across automotive and industrial applications.

5. What are key segments in the Europe Filters Market?

The Europe Filters Market segments include air filters (largest share), water filters, industrial filtration, and automotive cabin/intake filters. Air filters lead due to pollution control needs in urban and industrial settings.

6. Which trends shape the Europe Filters Market?

Key trends in the Europe Filters Market include sustainable, energy-efficient filters, modular designs for customization, and AI-enhanced filtration. Post-pandemic health focus boosts cabin and purifier filters.

7. What challenges face the Europe Filters Market?

Challenges in the Europe Filters Market involve competition from unorganized players, high R&D costs for compliance, and water scarcity issues. Balancing eco-friendly innovation with affordability remains key.

8. Are water filters growing in the Europe Filters Market?

Yes, the Europe Water Filters Market hit USD 5.28 billion in 2024, with 7.7% CAGR forecast, driven by RO systems and contaminant concerns in countries like Germany and France.

9. What opportunities exist in the Europe Filters Market?

Opportunities in the Europe Filters Market lie in EV-compatible filters, smart IoT filtration, and exports from hubs like Germany. Sustainability policies favor advanced, low-energy solutions.

10. How does pollution affect the Europe Filters Market?

Urban smog and industrial emissions heighten demand in the Europe Filters Market, especially for high-MERV air filters and cabin types, with passenger cars driving 52% of automotive segment growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com