Europe Harrow Market Size, Share, Trends, & Growth Forecast Report By Type (Spring Harrows, Roller Harrow, Chain Harrow, Disc Harrows, Others), Type, Technology, Product, Tractor Power, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Harrow Market Report Summary

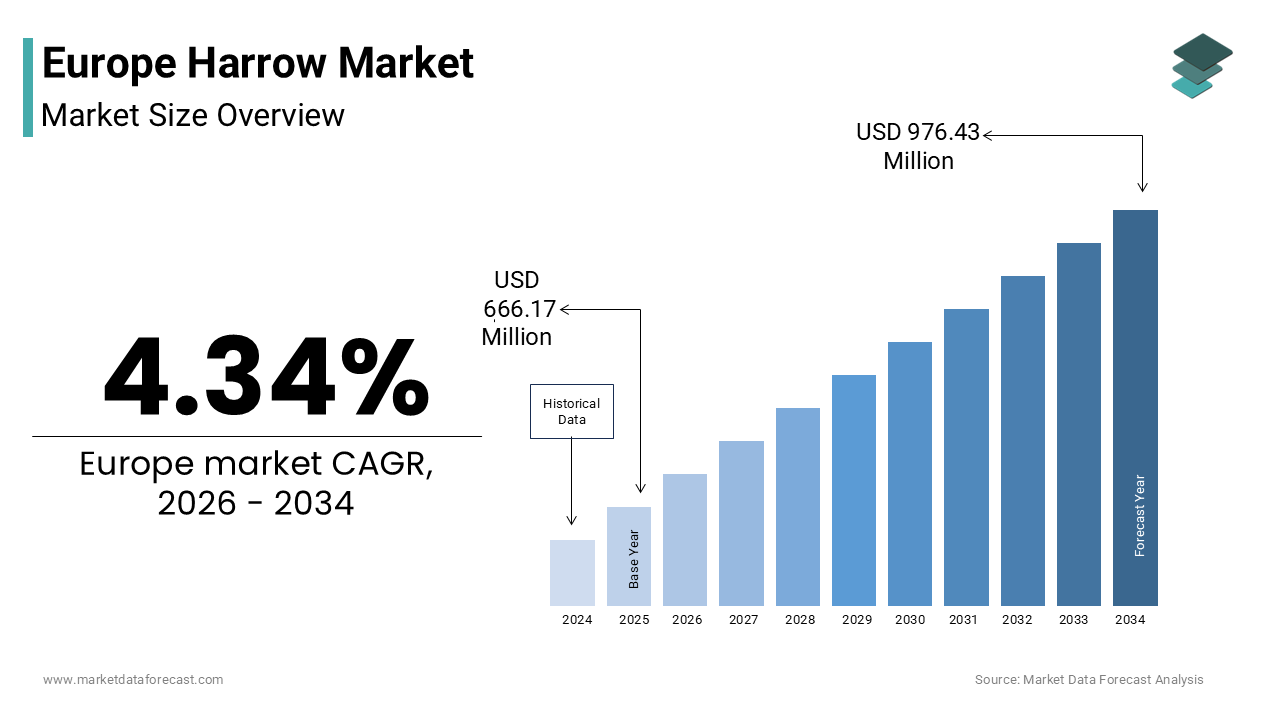

The Europe harrow market was valued at USD 666.17 million in 2025, is estimated to reach USD 695.08 million in 2026, and is projected to reach USD 976.43 million by 2034, growing at a CAGR of 4.34% during the forecast period from 2026 to 2034. The growth of the Europe harrow market is driven by increasing adoption of precision tillage practices, expanding cover cropping activities, and policy support under EU agri-environmental schemes promoting soil conservation and reduced tillage intensity. Rising demand for modern harrows capable of residue management, fertilizer incorporation, and shallow soil preparation is further fueling market growth. Moreover, integration of sensor-enabled implements, the expansion of organic farming requiring mechanical weed control, and the region’s transition toward climate-smart agriculture are strengthening the role of harrows as essential soil management tools across European farming systems.

Key Market Trends

-

A growing shift toward shallow and conservation tillage practices supported by EU agri-environmental subsidies and soil health initiatives.

-

Increasing adoption of cover cropping systems is driving demand for high-capacity residue management and incorporation harrows.

-

Rising integration of GPS, soil sensors, and ISOBUS connectivity enables precision harrowing and compatibility with autonomous tractors.

-

Expanding organic farming acreage ais ccelerating demand for mechanical weed control solutions using specialized harrow systems.

-

Continuous innovation in modular and adjustable harrow designs allowing customization for diverse soil conditions and farm sizes.

Segmental Insights

- Based on type, the disc harrows segment was the largest and held a significant share of the Europe harrow market in 2025. The segment’s dominance is attributed to superior versatility across soil types, effective residue incorporation following cover cropping, and high-speed operational capability suitable for large-scale arable farming.

- Based on technology, the manual harrows segment accounted for 56.5% of the Europe harrow market share in 2025. Manual systems remain widely adopted due to fragmented farm structures across Southern and Eastern Europe, low acquisition cost, ease of maintenance, and suitability for small and irregular field geometries.

- Based on product, the horizontal rotation power harrows segment was the largest, occupying a prominent share of the Europe harrow market in 2025. Their ability to create fine seedbeds in a single pass while supporting conservation tillage practices and efficient fertilizer mixing continues to support segment leadership.

Regional Insights

The Europe harrow market is experiencing stable growth across major agricultural economies, supported by the modernization of farm equipment, sustainability-focused tillage practices, and expanding precision agriculture adoption.

-

Germany was the largest contributor, accounting for 20.2% of the Europe harrow market share in 2025, driven by large-scale mechanized farms, strong agricultural machinery manufacturing presence, and widespread adoption of precision tillage technologies.

-

France continues to perform strongly, supported by extensive cereal production areas and policy initiatives encouraging soil carbon sequestration and residue management practices.

-

The United Kingdom demonstrates steady demand, fueled by grassland management needs, pasture renovation activities, and investments in soil health improvement programs.

-

Italy is emerging as a diversified market, characterized by demand for specialized harrow solutions across vineyards, arable fields, and horticultural landscapes.

Competitive Landscape

The Europe harrow market is characterized by the presence of established agricultural machinery manufacturers and regional equipment specialists competing on durability, technological integration, and adaptability to diverse soil and farm structures. Leading companies are focusing on precision-enabled harrows, modular designs, lightweight high-strength materials, and compatibility with digital farm management platforms to enhance operational efficiency and sustainability compliance. Strategic investments in automation readiness, expanded service networks, and product customization capabilities are strengthening competitive positioning across Europe. Prominent players in the Europe harrow market include Lemken GmbH & Co. KG, Amazone H. Dreyer GmbH & Co. KG, KUHN Group, Kverneland Group, Maschio Gaspardo S.p.A., Bednar FMT, Horsch Maschinen GmbH, Pottinger Landtechnik GmbH, Vaderstad AB, and Gregoire Besson

Europe Harrow Market Size

The Europe harrow market size was valued at USD 666.17 million in 2025 and is anticipated to reach USD 695.08 million in 2026 from USD 976.43 million by 2034, growing at a CAGR of 4.34% during the forecast period from 2026 to 2034.

Harrow are agricultural implements used to refine seedbeds, incorporate fertilizers, control weeds, and manage crop residues across arable farmland. These tools range from traditional tine and disc harrows to modern power harrows and combination tillage systems and are integral to soil preparation protocols that balance productivity with environmental stewardship. The market’s evolution is deeply intertwined with Europe’s agrarian policies and ecological imperatives. As per Eurostat, the European Union dedicated extensive hectares to agricultural use in 2025, with a majority classified as arable land requiring regular tillage. Concurrently, according to the European Commission, a significant portion of EU farms now practice some form of conservation agriculture, which emphasizes minimal soil disturbance. This trend sustains demand for precision harrows that enable shallow, non-inversion tillage. This duality positions the harrow not as a relic of conventional farming but as a calibrated instrument in the continent’s transition toward climate smart agriculture, where mechanical soil management must reconcile yield stability with biodiversity preservation and carbon sequestration.

MARKET DRIVERS

EU Agri-Environmental Schemes Are Promoting Precision Tillage Over Plowing

The European Union’s Common Agricultural Policy increasingly incentivizes reduced tillage intensity to protect soil health and reduce carbon emissions, which is driving the growth of the European harrow market. As per the European Environment Agency, these schemes have led to greater adoption of shallow tillage implements since 2022. Power harrows and rotary harrows are particularly favoured because they disturb only the top layer of soil, preserving organic matter and microbial ecosystems while still preparing a fine seedbed. In countries like France and Germany, where compliance with national eco-schemes is tied to subsidy eligibility, farmers are replacing deep plows with multi-functional harrow systems that integrate residue chopping and fertilizer incorporation. This policy-driven shift transforms the harrow from a secondary tool into a primary implement in sustainable field operations.

Rising Prevalence of Cover Cropping Is Driving Demand for Residue-Management Harrows

The EU’s Green Deal target of expanding organic farming by 2030 has accelerated the use of cover crops such as clover, vetch, and rye to fix nitrogen and prevent erosion, which is further contributing to the expansion of the European harrow market. As per the European Crop Protection Association, cover crop adoption increased notably across the EU between 2023 and 2025. Terminating these dense vegetative mats requires robust harrows capable of cutting, mixing, and incorporating biomass without clogging. Disc harrows with adjustable gang angles and heavy-duty tine harrows equipped with hydraulic depth control have become essential for this task. In Poland and Romania, where large-scale grain farms are integrating cover crops into rotation, demand for high-capacity trailed harrows has surged. These implements must operate efficiently within narrow spring planting windows. The convergence of ecological mandates and operational efficiency has elevated the harrow to a critical role in modern regenerative farming systems.

MARKET RESTRAINTS

Soil Compaction from Heavy Machinery Is Reducing the Efficacy of Traditional Harrowing

Despite their utility, conventional harrows struggle to address subsoil compaction caused by increasingly heavy tractors and harvesters, which is hindering the European harrow market growth. As per the Joint Research Centre of the European Commission, a significant portion of arable land in Western Europe exhibits severe compaction below 30 centimetres, which is a depth beyond the reach of most harrows. Surface tillage with tine or disc harrows may create a fine tilth on top but fails to alleviate deeper structural damage, leading to poor root penetration and waterlogging. Farmers often misinterpret this limitation as a flaw in the harrow itself, resulting in underutilization or premature replacement. In regions like the Netherlands and Denmark, where field traffic intensity is highest, many operators are bypassing harrows altogether in favor of deep subsoilers, reducing demand for mid-tier harrow models. This technical mismatch between tool capability and soil condition constrains market growth, particularly for standard equipment lacking depth versatility.

Fragmented Farm Sizes in Southern Europe Limit Investment in Advanced Harrow Systems

The economic viability of modern, wide-span harrows is undermined by the prevalence of small, fragmented holdings in Southern and Eastern Europe, which is further hampering the regional market expansion. As per Eurostat, a majority of farms in Italy, Greece, and Portugal are smaller than 10 hectares, with irregular field geometries that hinder efficient operation of large implements. A 6-meter power harrow, optimal for economies of scale, becomes impractical on small sloped plots. Consequently, demand remains skewed toward low-cost, manually adjustable tine harrows or second-hand equipment, stifling adoption of GPS-guided, hydraulically controlled models. As per the European Central Bank’s 2025 rural credit report, only a limited portion of smallholders in these regions accessed machinery financing, further limiting capital expenditure. This structural barrier creates a two-tier market where innovation thrives in the north but stalls in the south, fragmenting demand and complicating product standardization for manufacturers.

MARKET OPPORTUNITIES

Integration with Autonomous Tractor Platforms Is Enabling Smart Harrowing Operations

The emergence of autonomous and semi-autonomous tractors in European agriculture is creating a new frontier for the European harrow market. Leading manufacturers are now equipping harrows with GPS, soil moisture sensors, and variable-rate actuators that adjust tine pressure or disc angle based on field conditions. As per the Fraunhofer Institute’s 2025 pilot, farms using sensor-fused harrows achieved notable reductions in fuel consumption and more uniform seedbed preparation compared to conventional setups. This data-driven approach aligns with the EU’s Digital Farming Strategy, which promotes precision input management. Companies offering ISOBUS-compatible harrows that communicate seamlessly with tractor telematics can capture premium value by transforming mechanical implements into decision-support nodes. This convergence of automation and agronomy opens recurring revenue streams through software updates and analytics services.

Demand for Organic Certification Is Boosting Mechanical Weed Control via Harrowing

With the EU targeting 25% of agricultural land under organic management by 2030, chemical herbicide use is declining sharply, which is elevating mechanical weeding as a core practice and acting as another notable opportunity in the regional market. Harrows are central to post-emergence weed control in cereals and row crops. As per IFOAM Organics Europe, certified organic arable area grew significantly in 2025, driving demand for high-precision harrows that can selectively uproot weeds without damaging crops. Innovations like camera-guided tine adjustment and intra-row harrowing units are gaining traction in Germany and Sweden, where organic premiums justify investment. These implements must operate at precise growth stages, requiring integration with agronomic calendars and weather data. This regulatory and consumer-driven shift positions the harrow not just as a tillage tool but as a frontline defense in chemical-free crop protection, unlocking a high-value niche aligned with Europe’s food sovereignty goals.

MARKET CHALLENGES

Raw Material Volatility Is Squeezing Margins on Steel-Intensive Implements

Harrow frames, tines and discs are predominantly fabricated from high-carbon steel, which is making manufacturers acutely vulnerable to commodity price swings and challenging the regional market growth. As per the European Steel Association, hot-rolled coil prices fluctuated sharply between 2024 and 2025 due to energy costs and global trade dynamics. This volatility compresses profit margins, especially for mid-sized fabricators lacking hedging capabilities. Unlike tractors or planters, harrows offer limited scope for electronic value addition, leaving price as a primary competitive lever. Producers face a dilemma: absorb cost increases and risk losses, or raise prices and lose price-sensitive customers in Eastern Europe. The absence of viable lightweight alternatives exacerbates dependency on steel, creating a persistent financial vulnerability that impedes R&D investment and long-term pricing stability.

Labor Shortages Are Reducing Timely Field Operations, Diminishing Harrow Utilization

Agricultural labor scarcity across Europe is disrupting critical tillage windows, which is indirectly undermining harrow demand and challenging the expansion of the European harrow market. As per the European Commission, seasonal farm worker deficits were significant in 2025, with aging demographics worsening the gap. When labor is unavailable during brief spring or autumn windows, farmers consolidate operations, often skipping secondary tillage passes that require harrowing. In regions like Bavaria and Normandy, delayed harrowing leads to rushed, suboptimal seedbed preparation or complete reliance on no-till drilling. This operational compression reduces the perceived necessity of owning dedicated harrows, encouraging rental or shared ownership models that lower overall equipment sales volume. Until automation or simplified workflows alleviate this timing pressure, the harrow market will remain susceptible to human capital constraints that lie beyond its direct control.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.34% |

| Segments Covered | By Type, Technology, Product, Tractor Power, Application and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Lemken GmbH & Co. KG, Amazone H. Dreyer GmbH & Co. KG, KUHN Group, Kverneland Group, Maschio Gaspardo S.p.A., Bednar FMT, Horsch Maschinen GmbH, Pottinger Landtechnik GmbH, Vaderstad AB, and Gregoire Besson. |

SEGMENTAL ANALYSIS

By Type Insights

The disc harrows segment accounted for the leading share of 35.5% of the regional market in 2025. The growth of the disc harrows segment in the European market is driven by their unmatched versatility in primary and secondary tillage across diverse soil types and the effectiveness of disc harrows in residue management following the EU’s surge in cover cropping. As per the European Commission’s 2025 Farm Sustainability Report, millions of hectares of EU farmland now use cover crops, generating dense biomass that requires aggressive cutting and incorporation precisely what heavy-duty disc harrows deliver. Their angled concave discs slice through stalks and roots while mixing organic matter into the topsoil, preparing a uniform seedbed without full inversion. Another factor is compatibility with high-speed operations. Modern trailed disc harrows can operate efficiently at 10 to 12 kilometers per hour, enabling large farms in Germany and France to cover extensive areas within narrow spring windows. This speed-to-quality balance makes disc harrows indispensable for time-constrained, large-scale arable operations.

The spring harrows segment is estimated to grow at a CAGR of 6.12% over the forecast period owing to the continent’s rapid shift toward chemical-free weed control. With the EU targeting 25% organic farmland by 2030, mechanical weeding has become essential, and spring harrows excel at uprooting small broadleaf weeds in cereals and row crops during early growth stages. Another driver is their role in pasture renovation. In Ireland and Denmark, where permanent grassland accounts for a majority of agricultural land as per Eurostat, farmers use spring harrows in early spring to remove dead thatch, level molehills, and stimulate new grass growth without damaging root systems. Their lightweight design and low draft requirement also make them ideal for use on rented or sloped fields where heavy machinery is impractical. This dual utility in both arable and pastoral systems—amplified by policy support for biodiversity-friendly practices—is propelling spring harrows into a high-growth niche.

By Technology Insights

The manual harrows segment led the market by capturing 56.5% of the regional market share in 2025. The growth of the manual harrows segment in the European market is attributed to the structural realities across much of the continent and farm size distribution. As per Eurostat, a majority of EU farms are smaller than 10 hectares, particularly in Southern and Eastern Europe, where narrow plots and irregular terrain render automated systems inefficient. A simple tine or chain harrow pulled by a small tractor remains the most cost-effective solution for these holdings. Another factor is repairability and simplicity. Manual harrows have no electronics or hydraulic actuators, making them easy to maintain with basic tools—a critical advantage in regions like Romania and Greece, where access to specialized service technicians is limited. This robustness, combined with low acquisition costs, ensures manual harrows remain the pragmatic choice for the majority of Europe’s fragmented agricultural landscape.

The automatic harrows segment is estimated to grow at a CAGR of 8.4% over the forecast period owing to the convergence of labor scarcity and precision farming mandates and integration with autonomous and GPS-guided tractors. Leading manufacturers now offer harrows with real-time kinematic positioning and automatic depth control that adjust tine pressure based on soil moisture maps, ensuring consistent seedbed quality across variable fields. In Sweden and the Netherlands, where labor shortages are significant as per the European Commission, such systems enable single operators to manage multiple implements simultaneously. Another factor is compliance with the EU’s Digital Farming Strategy, which promotes data-driven input optimization. Automatic harrows generate field-level tillage records that feed into farm management software, supporting subsidy claims under eco-schemes. This transformation from mechanical tool to digital node is redefining value in high-tech agricultural regions.

By Product Insights

The horizontal rotation power harrows segment commanded for the leading share of 41.4% of the regional market in 2025. The leading position of horizontal rotation power harrows segment in the European market is attributed to their superior ability to create fine, level seedbeds in a single pass, which is critical for direct drilling and precision sowing systems. The compatibility of horizontal rotation power harrows with conservation agriculture is further boosting the expansion of the regional market. Unlike vertical or reciprocating models, horizontal rotors work just below the surface, minimizing soil inversion while thoroughly mixing residues and fertilizers. This aligns with EU agri-environmental schemes that discourage deep tillage. Another factor is operational efficiency in medium-textured soils prevalent in France and Germany. These harrows can prepare multiple hectares per day at optimal moisture levels, reducing fuel consumption compared to multi-pass systems, as documented in a 2025 field trial by the German Agricultural Society. This blend of agronomic precision and economic efficiency solidifies their position as the standard for modern arable farms.

The vertical rotation power harrows segment is estimated to witness a CAGR of 7.12% over the forecast period. The unique suitability of vertical rotation power harrows for heavy clay and wet soils common in the UK and Ireland is propelling the growth of the segment in this regional market. The vertical rotor design aggressively breaks up compacted layers without creating a hard pan, improving drainage and root penetration, which is critical in regions receiving high annual rainfall as per the European Environment Agency. Another factor is their synergy with strip-till systems. As European farms adopt controlled traffic farming to reduce compaction, vertical power harrows are used to till only the planting zone, leaving inter-rows undisturbed. In Denmark, maize growers increasingly use this approach, requiring specialized vertical harrows that integrate with GPS-guided toolbars. This niche yet high-value application in challenging soil conditions is accelerating adoption beyond traditional markets.

REGIONAL ANALYSIS

Germany Harrow Market Analysis

Germany led the harrow market in Europe in 2025 by holding 20.2% of the regional market share. The growth of Germany in the European market is driven by large-scale farms averaging over 60 hectares that demand high-efficiency, technologically integrated implements and country’s strict adherence to the National Action Plan for Sustainable Agriculture, which incentivizes shallow tillage to protect soil carbon stocks. As a result, German farmers heavily invest in GPS-guided disc and power harrows that minimize passes and fuel use. Additionally, Germany’s leadership in agricultural machinery manufacturing ensures rapid access to next-generation prototypes and service networks. The combination of policy alignment, farm scale, and industrial proximity creates a high-specification market that sets technical benchmarks for the continent.

France Harrow Market Analysis

France is another promising regional segment in the European harrow market. The position of France in the European market is attributed to the EU’s largest cereal producer with extensive arable land as per Agreste. Its market status is characterized by a strong preference for robust, wide-span disc and tine harrows capable of covering vast fields quickly during narrow seasonal windows. The key driver is the national “4 per 1000” initiative, which promotes soil carbon sequestration through reduced tillage intensity, boosting demand for residue-managing harrows that avoid plowing. In the Paris Basin and Beauce regions, cooperatives often pool resources to purchase large trailed harrows, driving economies of scale. Furthermore, France’s extensive network of agricultural advisory services provides farmers with real-time soil moisture data, enabling optimal harrowing timing. This blend of scale, policy, and agronomic support sustains consistent, high-volume demand.

United Kingdom Harrow Market Analysis

The United Kingdom is likely to account for a prominent share of the European harrow market over the forecast period. The growth of the UK in the European market is likely to be driven by the focus of the UK on grassland management and heavy soil tillage and a livestock-dominated agricultural system where a majority of farmland is permanent pasture as per DEFRA. This drives strong demand for chain and spring harrows used in spring pasture renovation to control rushes and improve grazing quality. Simultaneously, in eastern England’s clay belts, vertical rotation power harrows are essential for breaking compaction after winter rains. The UK’s departure from the EU has intensified focus on domestic food security, prompting investment in efficient tillage to maximize yields. Recent DEFRA grants covering a portion of equipment costs for soil health improvements have further stimulated harrow purchases, creating a dual-demand profile that balances pastoral care with arable productivity.

Poland Harrow Market Analysis

Poland is estimated to witness a healthy CAGR in the European harrow market over the forecast period. Poland is emerging as a key growth frontier due to farm consolidation and EU funding. The transition from fragmented smallholdings to larger commercial units supported by CAP convergence payments and rising need for efficient primary tillage across the country’s vast loess plains, where disc harrows are used extensively after sugar beet and potato harvests to incorporate residues are further propelling the polish market growth. As per Poland’s Central Statistical Office, significant land consolidation occurred between 2020 and 2025, enabling mechanization at scale. Additionally, Poland’s National Recovery Plan allocates funds for modernizing agricultural machinery, with harrows among the eligible categories. This policy-fueled modernization, combined with expanding export-oriented grain production, positions Poland as a high-volume, value-conscious market with rising technical sophistication.

Italy Harrow Market Analysis

Italy is projected to grow at a steady CAGR in the European harrow market over the forecast period. Italy is notable for its adaptation to extreme topographical diversity. The highly specialized demand and lightweight spring harrows for terraced vineyards in Piedmont, heavy disc harrows for Po Valley rice stubble, and compact power harrows for olive groves in Puglia are propelling the Italian market growth. The key driver is the EU’s Common Agricultural Policy, which provides higher subsidies for soil conservation in erosion-prone areas, encouraging minimal-tillage harrowing on slopes. Italy’s 2024 National Rural Development Program also offers tax credits for purchasing equipment that reduces soil disturbance. With millions of farms, as per ISTAT, the market favors versatile, narrow-frame harrows that can navigate tight spaces. This fragmentation fosters innovation in modular designs, making Italy a laboratory for adaptable, terrain-specific tillage solutions.

COMPETITIVE LANDSCAPE

The competition in the Europe harrow market is characterized by a blend of established engineering-focused manufacturers and agile regional specialists. Leading firms compete on technological sophistication, offering harrows with hydraulic adjustment, sensor integration, and compatibility with digital farm management systems, primarily targeting large-scale arable operations in Western and Central Europe. Simultaneously, smaller fabricators thrive in Southern and Eastern Europe by providing cost-effective, repairable manual harrows suited to fragmented landholdings. Differentiation hinges on adaptability to local soil conditions, compliance with evolving EU sustainability regulations, and after-sales support responsiveness. While price remains a factor for smallholders, larger farms prioritize long-term operational efficiency and data connectivity. This dual-market structure fosters continuous innovation at the high end while maintaining demand for simplicity and affordability elsewhere, creating a layered and resilient competitive landscape shaped by both policy and geography.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Harrow Market include

- Lemken GmbH & Co. KG

- Amazone H. Dreyer GmbH & Co. KG

- KUHN Group

- Kverneland Group

- Maschio Gaspardo S.p.A.

- Bednar FMT

- Horsch Maschinen GmbH

- Pottinger Landtechnik GmbH

- Vaderstad AB

- Gregoire Besson

Top Players in the Market

Amazone GmbH & Co. KG

Amazone is a leading German agricultural machinery manufacturer renowned for its high-precision harrows, including the Catros and DMC series, which are widely used across European arable farms. The company contributes globally by exporting its soil tillage expertise to over 100 countries, emphasizing durability, fuel efficiency, and integration with digital farming systems. Recently, Amazone enhanced its harrow lineup with ISOBUS compatibility and automatic depth control linked to real-time soil sensors. This innovation allows operators to adjust tillage intensity on the go, aligning with EU sustainability mandates. These advancements reinforce Amazone’s reputation as a pioneer in smart, conservation-focused tillage solutions on both European and global stages.

Kverneland Group ASA

Kverneland, a Norwegian headquartered but pan-European agricultural equipment specialist, plays a pivotal role in the harrow market through its Väderstad and Kverneland branded implements. The company serves diverse farming systems from Scandinavian pastures to Eastern European grain belts with tailored harrow solutions such as the Carrier and Spirit series. To strengthen its position, Kverneland has recently integrated telematics into its power harrows, enabling remote monitoring of operational hours, wear levels, and field coverage. This data-driven approach supports predictive maintenance and compliance with EU eco-scheme documentation requirements. Its commitment to modular design also allows farmers to adapt harrows to varying soil conditions, enhancing its relevance across global markets.

Pöttinger Landtechnik GmbH

Pöttinger is an Austrian manufacturer known for its robust and versatile harrows, particularly the Eurocat and Vitas series, which excel in both residue incorporation and seedbed preparation. The company’s global contribution lies in its focus on compact yet high-performance implements suited for hilly and fragmented landscapes common in Southern Europe and parts of Asia. In recent years, Pöttinger has invested in hydraulic adjustment systems that enable on-the-go tine angle and working depth changes without stopping the tractor. It also launched a lightweight disc harrow line using high-strength steel to reduce draft requirements. These innovations cater to labor-constrained and fuel-sensitive markets, reinforcing Pöttinger’s niche as a provider of efficient, terrain-adaptive tillage technology worldwide.

Top Strategies Used by the Key Market Participants

Key players in the Europe harrow market are increasingly integrating digital technologies such as GPS guidance, soil sensors, and telematics to enable precision tillage and compliance with agri-environmental schemes. They are developing modular and adjustable harrow designs that allow farmers to customize tine configuration, working width, and depth for varying soil types and crop rotations. Companies are also utilizing high-strength, lightweight steel alloys to reduce draft requirements and fuel consumption without compromising durability. Strategic partnerships with autonomous tractor developers are being formed to ensure compatibility with next-generation farming platforms. Additionally, manufacturers are expanding regional service networks to provide rapid spare parts delivery and technical support, enhancing customer retention in a competitive and seasonally driven market.

MARKET SEGMENTATION

This research report on the Europe harrow market has been segmented and sub-segmented based on the following categories.

By Type

- Spring Harrows

- Roller Harrow

- Chain Harrow

- Disc Harrows

- Others

By Technology

- Manual

- Semi-Automatic

- Automatic

By Product

- Reciprocating Power Harrow

- Horizontal Rotation Power Harrow

- Vertical Rotation Power Harrow

By Tractor Power

- Less than 60HP

- 60HP-120HP

- 120HP-160HP

- More than 160HP

By Application

- Farmland

- Pasture

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What factors are driving the growth of the Europe harrow market?

Growth is driven by increasing mechanization in agriculture, rising demand for efficient soil preparation equipment, and the need to improve crop productivity.

Which types of harrows are commonly used in Europe?

Disc harrows, tine harrows, chain harrows, and power harrows are widely used for different soil preparation and cultivation requirements.

Which countries lead the Europe harrow market?

Germany, France, the UK, Italy, and Spain are major markets due to their advanced agricultural practices and high adoption of farm machinery.

What role does harrow equipment play in modern farming?

Harrows help in soil leveling, weed control, seedbed preparation, and residue management, improving overall farm efficiency.

What challenges affect the Europe harrow market?

High equipment costs, fluctuating farm income, and seasonal demand variations are key challenges.

How is technology influencing the harrow market in Europe?

Integration with precision farming, GPS-enabled machinery, and durable material innovations are enhancing harrow performance and adoption.

What opportunities exist in the Europe harrow market?

Opportunities include demand for lightweight equipment, expansion of sustainable farming practices, and increasing use of combined tillage solutions.

What distribution channels are used for harrow equipment in Europe?

Agricultural machinery dealers, direct manufacturer sales, distributors, and online farm equipment platforms are key distribution channels.

How do government policies impact the Europe harrow market?

Subsidies for farm mechanization and sustainability initiatives encourage farmers to invest in modern soil preparation equipment.

What materials are commonly used in manufacturing harrows?

High-strength steel and corrosion-resistant alloys are commonly used to ensure durability and long service life.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com