Europe Heat Pump Water Heater Market Size, Share, Trends & Growth Forecast Report By Type (Air-to-Air heat pump water heater, Air-to-Water heat pump water, heater Water source heat pump water heater, Ground source (geothermal) heat pump water heater, Hybrid heat pump water heater), Storage Tank, Refrigerant Type and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Heat Pump Water Heater Market Size

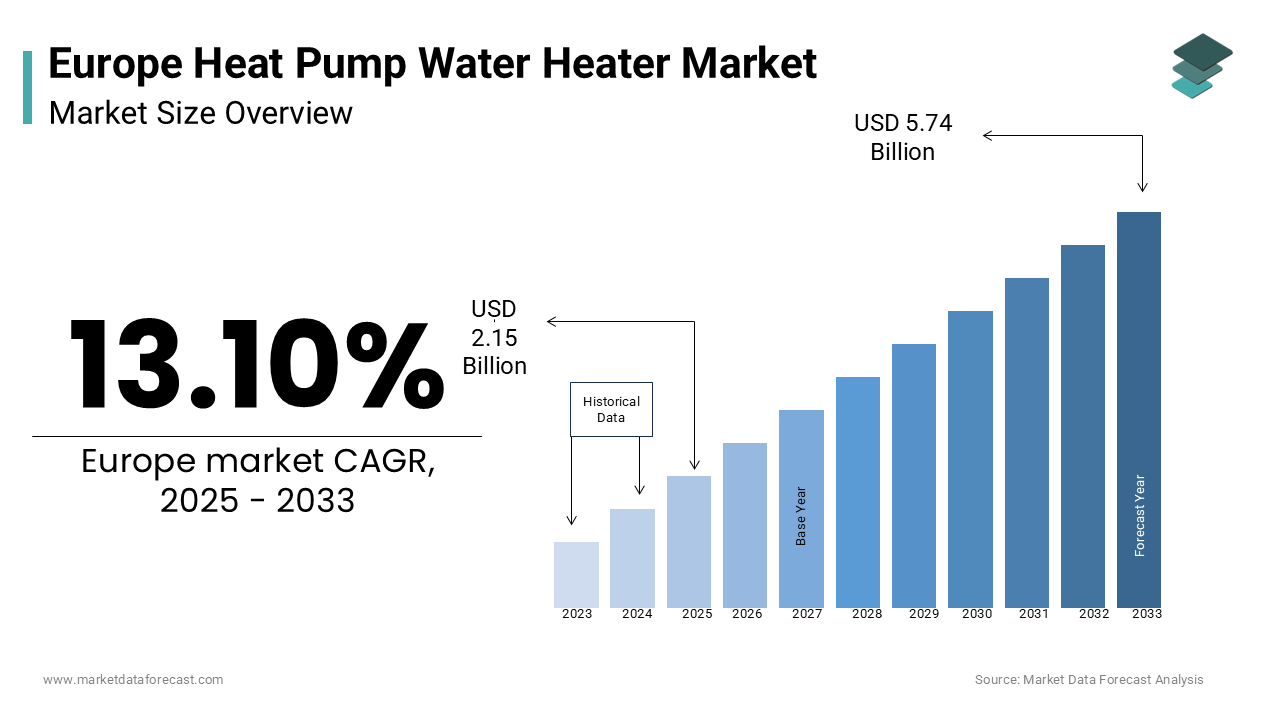

The europe heat pump water heater market was worth USD 1.90 billion in 2024. The European market is estimated to grow at a CAGR of 13.10% from 2025 to 2033 and be valued at USD 5.74 billion by the end of 2033 from USD 2.15 billion in 2025.

The Europe heat pump water heater market is experiencing robust growth, driven by stringent energy efficiency regulations and growing environmental awareness. This has led to a shift toward sustainable solutions, with heat pump water heaters gaining prominence. The International Energy Agency (IEA) notes that heat pumps can reduce household energy use, making them an attractive choice for European consumers. As per a report by the European Heat Pump Association (EHPA), the market witnessed a key year-on-year increase in installations in 2022, reaching approximately 3 million units.

MARKET DRIVERS

Stringent Environmental Regulations

Europe’s commitment to reducing greenhouse gas emissions under frameworks like the European Green Deal is a key driver of the heat pump water heater market. According to the European Environment Agency, buildings account for 36% of CO2 emissions in the EU, prompting governments to mandate energy-efficient heating solutions. For instance, the UK’s Future Homes Standard mandates that new homes must have low-carbon heating systems by 2025. This regulatory push has resulted in a major annual growth in heat pump water heater installations across Europe, as stated by the EHPA. Additionally, countries like Norway offer tax exemptions for eco-friendly appliances, boosting demand. The IEA highlights that replacing conventional water heaters with heat pumps could reduce residential emissions. These policies are creating a conducive environment for manufacturers and installers, fostering rapid market expansion.

Rising Energy Costs

Escalating energy prices in Europe are compelling households to adopt energy-efficient alternatives. Heat pump water heaters, which consume less energy than traditional electric heaters, are becoming a cost-effective solution. In Germany, where energy costs are among the highest in Europe, sales surged in 2022. Furthermore, the EHPA estimates that households can significantly save amount annually on energy bills by switching to heat pumps. Consumer awareness campaigns, such as those by the EU Energy Efficiency Directive, are amplifying this trend.

MARKET RESTRAINTS

High Initial Investment

Despite their long-term benefits, the high upfront costs of heat pump water heaters remain a significant barrier. This disparity discourages price-sensitive consumers, particularly in southern European countries like Spain and Italy, where disposable incomes are lower. A survey by the EHPA revealed that 40% of potential buyers cited cost as the primary reason for not adopting heat pumps. Although subsidies exist, they often fail to cover the entire expense, leaving consumers hesitant. For example, in Poland, where government incentives are limited, adoption rates lag behind Western Europe. Unless financing options improve, this factor will continue to hinder widespread adoption.

Limited Awareness and Technical Expertise

A lack of consumer awareness and skilled technicians poses another challenge. According to the IEA, only 30% of European households are familiar with heat pump technology with misconceptions about installation complexity and maintenance persisting. In rural areas, where access to information is limited, adoption rates are significantly lower. Moreover, the EHPA reports a shortage of trained professionals, with only 150,000 certified installers across Europe as of 2022. This shortage delays installations and increases costs, further deterring adoption. Countries like Romania and Bulgaria face acute shortages, exacerbating regional disparities. Addressing these gaps requires concerted efforts from governments and industry players to educate consumers and expand training programs.

MARKET OPPORTUNITIES

Retrofitting Existing Buildings

Retrofitting older buildings with heat pump water heaters presents a lucrative opportunity. According to the European Commission, 75% of Europe’s building stock is energy-inefficient, offering immense potential for upgrades. The Renovation Wave initiative aims to renovate 35 million buildings by 2030, creating a surge in demand for sustainable heating solutions. A study by the EHPA estimates that retrofitting projects could generate €1 trillion in economic activity while reducing emissions by 55%. In France, the MaPrimeRénov’ scheme subsidizes retrofits, driving increase in heat pump installations in 2022. Manufacturers focusing on compact, easy-to-install models are well-positioned to capitalize on this trend, especially in densely populated urban areas.

Integration with Renewable Energy Systems

The integration of heat pump water heaters with renewable energy sources is another promising avenue. According to the IEA, solar PV installations in Europe grew by 40% in 2022, creating synergies with heat pumps. Hybrid systems combining solar panels and heat pumps can reduce energy consumption. Germany, a leader in solar adoption, saw a notable rise in hybrid system installations in 2022. The EU’s Solar Strategy aims to quadruple solar capacity by 2030, further boosting demand. Companies investing in smart technologies that optimize energy usage stand to gain a competitive edge in this emerging segment.

MARKET CHALLENGES

Infrastructure Limitations

Infrastructure limitations, particularly in older buildings, pose a significant challenge. According to the European Commission, 40% of Europe’s housing stock was built before 1970, lacking the necessary insulation and electrical systems for efficient heat pump operation. In countries like Italy, where historical preservation laws restrict renovations, upgrading infrastructure is complex and costly. The EHPA notes that inadequate grid capacity in rural areas further complicates installations, limiting market penetration. For instance, in Greece, outdated electrical grids hinder the adoption of high-capacity heat pumps.

Competition from Alternative Technologies

Competition from alternative heating technologies, such as gas boilers and district heating, remains a hurdle. In Eastern Europe, where gas infrastructure is prevalent, adoption rates for heat pumps remain low. Additionally, district heating systems in Scandinavia serve over 60% of households, as per the IEA, leaving little room for individual heat pump installations. While heat pumps offer long-term savings, overcoming entrenched preferences for traditional systems requires targeted marketing and education campaigns.

SEGMENTAL ANALYSIS

By Type Insights

The air-to-water heat pumps dominated the Europe heat pump water heater market by holding a 60% market share as of 2024. Their popularity is due to the versatility and compatibility with existing radiators and underfloor heating systems. In Germany, air-to-water systems accounted for a major share of installations, driven by government incentives like the Market Rebate Program. The IEA highlights that these systems achieve a Coefficient of Performance (COP) of 3–4, making them highly efficient. Urban areas benefit most, as compact designs suit space-constrained properties. With urbanization trends accelerating, demand is expected to grow steadily.

Geothermal heat pumps are the fastest-growing segment, with a CAGR of 15% projected through 2033. Their superior efficiency, with COPs exceeding 5, appeals to environmentally conscious consumers. In Sweden, geothermal systems account for 20% of new installations, supported by favorable geological conditions. The EU’s Horizon Europe program funds research into advanced drilling techniques, reducing costs. As technology improves, adoption is set to accelerate, particularly in regions with suitable geology.

By Storage Tank Insights

The tanks with capacities up to 500 liters segment commanded the market by holding a 55% market share, according to the EHPA. Their affordability and suitability for small households drive demand. In France, these systems account for 65% of installations supported by subsidies under the CITE scheme. The IEA notes that compact tanks integrate seamlessly with modern apartments appealing to urban dwellers. With urban populations rising, this segment is poised for sustained growth.

Above 1,000-liter tanks are the fastest-growing, with a CAGR of 12.2%. Their ability to meet high hot water demands makes them ideal for commercial applications. In Germany, industrial facilities are increasingly adopting these systems, driven by energy efficiency goals. Government incentives targeting large-scale installations further boost adoption, ensuring rapid expansion.

By Refrigerant Type Insights

R410A refrigerants led the market by holding a 45.3% share in 2024. Their widespread use stems from excellent thermodynamic properties and compatibility with existing systems. In Italy, R410A systems account for 50% of installations, supported by established supply chains. The IEA highlights their reliability, making them a preferred choice for residential applications.

R744 refrigerants are the fastest-growing, with a CAGR of 18.2%. Their low Global Warming Potential aligns with EU F-Gas regulations, driving adoption. In Norway, R744 systems account for a significant share of new installations, supported by strict environmental policies. Technological advancements are reducing costs, ensuring rapid market penetration.

REGIONAL ANALYSIS

Germany dominated the market by holding a 30.3% share in 2024. Robust government incentives and a strong manufacturing base drive adoption. The Federal Office for Economic Affairs and Export Control offers subsidies, boosting installations in 2022. Germany’s leadership underscores its commitment to sustainability.

France is the fastest-growing market. Programs like MaPrimeRénov’ drive demand, with installations increasing in 2022. France’s focus on decarbonization positions it as a key growth driver.

Italy and Spain show steady growth, supported by EU funding. The UK lags due to Brexit-related disruptions but is expected to recover post-2025.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Stiebel Eltron, Bosch Thermotechnik, Vaillant Group, Ariston Thermo, Viessmann, and Baxi (BDR Thermea Group) are some of the key market players in the europe heat pump water heater market.

The market is highly competitive, with players investing in R&D and digitalization. Consolidation through mergers and acquisitions is common, enhancing market presence.

Top Players and Their Contribution

Vaillant Group

A leader in Europe, Vaillant holds a 20% market share, as per the EHPA. Its ecoTEC line drives global innovation.

Viessmann

Viessmann commands a 15% share, focusing on integrated solutions.

Bosch Thermotechnology

Bosch contributes 10%, leveraging smart technologies.

Top Strategies Used by Key Players

Key strategies include product innovation, strategic partnerships, and expanding service networks. For instance, Viessmann collaborates with renewable energy firms to enhance hybrid systems.

RECENT MARKET DEVELOPMENTS

- In March 2023, Vaillant launched the ecoTEC exclusive heat pump, targeting energy-efficient homes.

- In June 2023, Viessmann partnered with SolarEdge to develop hybrid systems.

- In September 2023, Bosch acquired a software firm specializing in smart home integration.

- In December 2023, Daikin expanded its production facility in Poland to meet rising demand.

- In February 2024, Ariston introduced a new R744-based model, aligning with EU regulations

MARKET SEGMENTATION

This research report on the europe heat pump water heater market is segmented and sub-segmented based on categories.

By Type

- Air-to-Air heat pump water heater

- Air-to-Water heat pump water heater

- Water source heat pump water heater

- Ground source (geothermal) heat pump water heater

- Hybrid heat pump water heater

By Storage Tank

- Up to 500 liters

- 500–1,000 liters

- Above 1,000 liters

By Refrigerant Type

- R410A

- R407C

- R744

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What factors are driving the growth of the heat pump water heater market in Europe

The market is growing due to supportive EU regulations, rising energy prices, and the push toward carbon neutrality. Consumer interest in sustainable and cost-saving technologies is also rising

What are the key challenges affecting the heat pump water heater market in Europe?

High upfront costs and technical difficulties in retrofitting older buildings are major challenges. Additionally, awareness and availability still vary across regions.

What is the future outlook of the Europe Heat Pump Water Heater Market?

The Europe Heat Pump Water Heater Market is expected to experience significant growth in the coming years. This is driven by rising demand for energy-efficient solutions, supportive environmental policies, and increased consumer awareness about sustainable technologies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com