Europe Industrial Air Filtration Market Size, Share, Trends, & Growth Forecast Report By Product Type (Dust collectors, Mist collectors, HEPA filters, CCF, and Baghouse filters), Application, Distribution Channel, Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Industrial Air Filtration Market Size

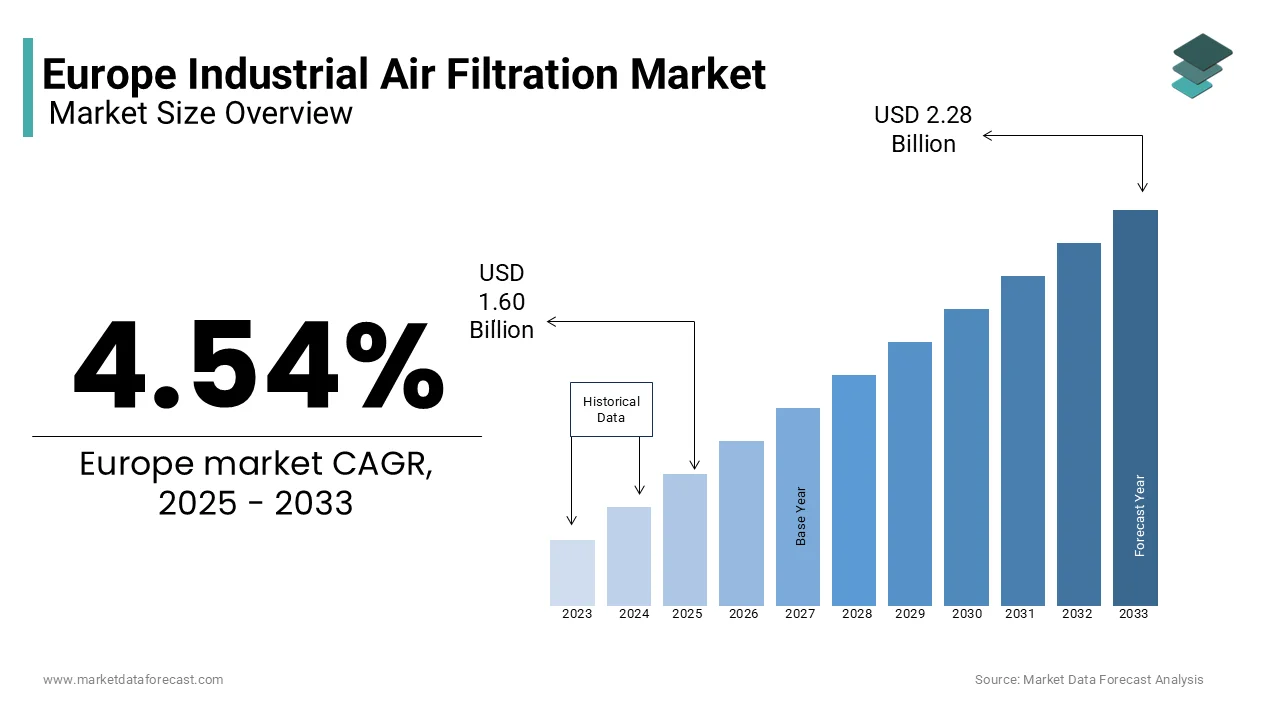

The Europe industrial air filtration market size was valued USD 1.60 billion in 2025 and is anticipated to reach USD 1.67 billion in 2026 to reach from 2.39 billion by 2034, growing at a CAGR of 4.54% from 2026 to 2034.

Current Market Introduction and Definition

The industrial air filtration is to the removal of particulate matter, gases, and vapors from air streams within manufacturing and processing environments to ensure operational safety and regulatory compliance. This industry provides essential technologies including bag filters, cartridge collectors, electrostatic precipitators, and scrubbers that protect both human health and sensitive industrial equipment from contamination. The region faces intense pressure to maintain air quality standards as industrial activities remain a primary source of emissions. According to the European Environment Agency industrial combustion and manufacturing processes accounted for approximately 42% of total fine particulate matter emissions in the European Union during 2022. Furthermore, the European Green Deal mandates a reduction in net greenhouse gas emissions by at least 55% by 2030 compared to 1990 levels which directly influences filtration requirements. Facilities, must now integrate high efficiency solutions that not only capture pollutants but also enable energy recovery and process optimization. As nations strive to meet the Zero Pollution Action Plan targets the deployment of sophisticated air purification technologies becomes indispensable for the continuity of industrial operations across the continent.

MARKET DRIVERS

Stringent Regulatory Frameworks Mandating Emission Reductions

The rigorous enforcement of environmental legislation that sets increasingly lower limits on industrial emissions is majorly propelling the growth of Europe industrial air filtration market. The European Union Industrial Emissions Directive serves as the cornerstone policy requiring large industrial installations to operate using the best available techniques to prevent or minimize releases into the air. According to the European Commission, over 52000 industrial installations across the member states are subject to these strict permitting conditions which mandate continuous monitoring and upgrading of filtration infrastructure. Non-compliance results in severe financial penalties and potential operational shutdowns which forces facility managers to invest heavily in high performance filtration systems. The directive specifically targets pollutants such as sulfur dioxide nitrogen oxides and dust which necessitates the installation of advanced baghouses and electrostatic precipitators. Additionally, the National Emission Ceilings Directive imposes binding national limits on key air pollutants driving member states to enforce stricter local regulations on factories. Data from the European Environment Agency indicates that sectors like power generation and metal production must reduce their particulate emissions by up to 30% by 2030 to meet national targets. This regulatory pressure creates an inelastic demand for filtration upgrades as companies cannot legally operate without compliant systems. The constant tightening of these laws ensures a steady stream of projects focused on replacing outdated technology with next generation solutions capable of meeting ultra-low emission standards.

Rising Incidence of Occupational Respiratory Diseases and Safety Standards

The growing awareness of occupational health risks associated with industrial dust and the subsequent implementation of stringent workplace safety standards is additionally escalating the growth of Europe industrial air filtration market. Exposure to hazardous airborne particles, such as silica coal dust and metal fumes remains a leading cause of chronic respiratory diseases among industrial workers in Europe. As per Eurostat, statistics work related health problems including respiratory disorders affected over 2.3 million individuals in the European Union in 2022 prompting stronger enforcement of worker protection laws. The European Agency for Safety and Health at Work emphasizes that effective engineering controls including robust air filtration systems are the primary method for mitigating these risks at the source. Industries, such as woodworking pharmaceuticals and food processing are increasingly adopting high efficiency particulate air filtration to protect employees and avoid liability claims. The economic burden of occupational illnesses which includes healthcare costs and lost productivity acts as a powerful incentive for companies to upgrade their ventilation and filtration infrastructure. Furthermore, insurance providers are beginning to link premium rates to the quality of air quality management systems within facilities. This shift transforms air filtration from a regulatory checkbox into a critical component of risk management strategies. Companies are investing in real time monitoring sensors integrated with filtration units to ensure continuous compliance with occupational exposure limits. This focus on human capital preservation drives sustained demand for advanced filtration solutions across diverse industrial sectors.

MARKET RESTRAINTS

High Operational Costs and Energy Consumption of Advanced Systems

The substantial operational expenditure associated with running high efficiency filtration systems, particularly regarding energy consumption is limiting the growth of Europe industrial air filtration market. Advanced filtration technologies, such as high temperature bag filters and activated carbon adsorbers require significant power to maintain the necessary air flow and pressure differentials across the filter media. According to Eurostat, the industrial sector in the European Union faced an average electricity price increase of 45% in 2023 compared to the previous year due to energy market volatility. This surge in energy costs forces many small and medium sized enterprises to delay upgrades or operate existing less efficient systems to control expenses. The total cost of ownership for modern filtration units includes not only the initial capital outlay but also ongoing costs for filter replacement maintenance and energy usage which can strain operating budgets. Facilities operating on thin margins often struggle to justify the return on investment for premium filtration solutions. Additionally, the complexity of integrating energy recovery systems to offset these costs requires specialized engineering expertise that is not always readily available. The financial burden is exacerbated by the need for frequent monitoring and reporting to demonstrate compliance which adds administrative overhead.

Supply Chain Disruptions and Raw Material Price Volatility

The persistent instability in the global supply chain for raw materials used in manufacturing filtration media and components is impeding the growth of Europe industrial air filtration market. The production of high-performance filter bags and cartridges relies heavily on specialized synthetic fibers, such as polytetrafluoroethylene and fiberglass, whose prices are subject to extreme fluctuations due to geopolitical tensions and logistics. As per data from the European Chemical Industry Council, the producer prices for basic chemical products which include polymer precursors rose by 22% in 2023, creating significant cost pressures for filtration manufacturers. Dependence on imported raw materials from outside Europe exposes the supply chain to trade barriers shipping delays and currency exchange risks which complicate production planning. The shortage of semiconductor components required for smart filtration control systems further exacerbates delivery lead times causing project postponements for industrial clients. Manufacturers find it difficult to pass these increased costs onto customers who often operate under fixed long-term contracts or regulated tariff structures. The inability to secure consistent supplies of high-quality materials forces some producers to ration output or compromise on specifications, which undermines market confidence. This volatility creates an unpredictable business environment where capacity expansion plans are frequently put on hold. The lack of localized sourcing options for specialized filtration materials means that the European market remains vulnerable to external shocks that disrupt the steady flow of essential equipment.

MARKET OPPORTUNITIES

Integration of Internet of Things and Predictive Maintenance Technologies

The widespread adoption of Internet of Things sensors and artificial intelligence to enable predictive maintenance and real time performance optimization is certainly to set up opportunities for the growth of Europe industrial air filtration market. Traditional filtration systems often rely on scheduled maintenance, which can lead to unnecessary downtime or unexpected failures if filter bags rupture prematurely. According to a study by the Fraunhofer Institute, the implementation of smart monitoring systems in European industrial plants could reduce maintenance costs by up to 35% while improving overall equipment effectiveness. Manufacturers have the chance to evolve from selling static hardware to providing intelligent connected solutions that transmit data on pressure drop temperature and particle counts to central control rooms. This shift allows facility managers to replace filters exactly when needed rather than based on arbitrary timelines drastically reducing waste and operational interruptions. The European Union funding for digital innovation under the Digital Europe Programme supports pilot projects that test these advanced monitoring capabilities in heavy industry settings. Startups and established players alike are developing filtration units with embedded connectivity that can automatically adjust fan speeds to optimize energy usage based on real time load conditions. The value proposition extends beyond the hardware itself to include data analytics services that provide actionable insights into process efficiency. As Industry 4.0 principles become standard practice the demand for these intelligent filtration solutions will surge offering a lucrative avenue for differentiation and recurring revenue growth.

Expansion of Carbon Capture and Storage Infrastructure

The accelerating deployment of carbon capture and storage technologies across heavy industries which rely heavily on specialized air filtration systems for gas separation and purification. The expansion of the advanced infrastructure for the storage facilities is additionally to elevate new opportunities for the growth of Europe industrial air filtration market. The European Green Deal and the Net Zero Industry Act have spurred massive investments in CCS projects aimed at decarbonizing sectors like cement steel and chemicals that are hard to abate through electrification alone. As per the European Commission, the EU aims to achieve an annual carbon capture capacity of 50 million tons by 2030 requiring the construction of numerous new capture facilities. Each CCS plant requires extensive pre combustion and post combustion filtration systems to remove particulates and contaminants that could poison solvents or damage compression equipment. The unique operating conditions of CCS processes involving high temperatures and corrosive gases create a demand for advanced ceramic and metal filters that can withstand harsh environments. Governments across Europe are providing substantial grants and tax incentives to accelerate CCS deployment, which directly boosts the market for specialized filtration components. The integration of filtration into the carbon value chain positions suppliers as critical enablers of climate goals rather than just compliance vendors. This alignment with the continent decarbonization strategy ensures sustained long-term growth for manufacturers capable of delivering robust solutions for carbon management applications.

MARKET CHALLENGES

Technical Complexities in Disposing of Hazardous Filter Waste

The increasing difficulty and cost associated with the disposal of spent filter media that has captured hazardous substances is likely to pose a challenge for the growth of Europe industrial air filtration market. Filters used in industries, such as waste incineration metal smelting and chemical processing often become classified as dangerous waste due to the accumulation of heavy metals toxic dust or volatile organic compounds. According to research published by the European Waste Management Association, the volume of hazardous industrial waste requiring specialized treatment has increased by 18% over the last five years straining existing disposal infrastructure. The European Landfill Directive imposes strict limits on the disposal of untreated waste forcing companies to seek expensive incineration or chemical stabilization services for spent filters. The lack of standardized recycling protocols for composite filter materials means that most used units end up in high security landfills or incinerators which contradicts circular economy principles. Developing cost effective methods to recover valuable materials or safely neutralize trapped contaminants remains a significant scientific and logistical hurdle. Companies face growing pressure from regulators and stakeholders to develop biodegradable filter media or design for disassembly which requires substantial research and development investment. The uncertainty regarding future disposal regulations creates hesitation in the widespread adoption of certain filtration technologies despite their performance advantages.

Shortage of Skilled Technicians for Installation and Maintenance

The acute shortage of skilled labor and specialized technicians required for the proper installation inspection and maintenance of complex industrial air filtration systems is also to decline the growth of Europe industrial air filtration market. The aging workforce in the industrial sector combined with a lack of young entrants into vocational training programs has created a significant gap in technical expertise. As per Eurofound, the European Foundation for the Improvement of Living and Working Conditions the manufacturing sector in Europe faces a deficit of over 400000 skilled workers needed to support modern industrial operations. Proper installation of high efficiency filtration units requires precise knowledge of airflow dynamics sealing techniques and safety protocols which if executed incorrectly can lead to system failures and emissions violations. The scarcity of qualified personnel leads to project delays increased labor costs and potential safety hazards during maintenance operations. Facilities are struggling to find contractors capable of handling the complexities of advanced systems especially those integrated with digital monitoring tools. This human capital constraint limits the speed at which new infrastructure can be commissioned and existing assets can be upgraded. Companies are forced to invest heavily in training programs and automation technologies to mitigate the reliance on manual labor.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.54% |

| Segments Covered | By Product Type, Application, Distribution Channel, and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

| Market Leaders Profiled | Abatement Technologies, Inc., Alfa Laval, AAF, Camfil Air Pollution Control (APC), Con-Air Industries, Daikin Industries Ltd., Electrocorp, FILCOM GmbH, Good Life, Inc., HealthWay Home Products, Inc., Honeywell International, Inc., MANN+HUMMEL, Philips Electronics N.V., Sentry Air Systems, Inc, and Sharp Corporation. |

SEGMENTAL ANALYSIS

By Product Insights

The baghouse filters segment was the largest by accounting for 38.2% of the Europe Industrial Air Filtration Market share in 2025 with the unparalleled efficiency of baghouse systems in capturing fine particulate matter from high volume air streams in heavy industries, such as cement, steel, and power generation. The growth is sgemnt is attributed to be driven by the strict regulatory compliance required under the European Union Industrial Emissions Directive, which mandates ultra-low emission levels that only advanced baghouse configurations can consistently achieve. According to the European Cement Association, over 90% of cement plants in Europe rely on baghouse filters to meet particulate matter limits of less than 10 milligrams per normal cubic meter due to their superior collection efficiency compared to electrostatic precipitators. Additionally, the versatility of baghouse filters in handling a wide range of dust types, including sticky hygroscopic and explosive powders, which are common in chemical and food processing sectors.

The HEPA Filters segment is gaining traction at a fastest CAGR of 7.4% throughout the forecast period owing to the stringent hygiene requirements in the pharmaceutical biotechnology and semiconductor manufacturing sectors which demand absolute removal of submicron particles. The primary driver is the surge in construction of new cleanroom facilities and the upgrading of existing ones to meet the revised Good Manufacturing Practice guidelines enforced by the European Medicines Agency. According to industry analysis by the European Society of Pharmaceutical Engineers investment in cleanroom infrastructure in Europe increased by 25% in 2023 to support the production of advanced therapies and vaccines. These facilities require HEPA filtration to maintain ISO Class 5 or better environments where even a single particle can compromise product integrity. The second critical factor is the rising focus on indoor air quality in high tech manufacturing where microscopic contaminants can cause defects in microchip fabrication. Data from the European Semiconductor Industry Association reveals that yield losses due to airborne contamination cost the sector billions annually driving the adoption of ultra-high efficiency filtration solutions. Additionally, the post pandemic emphasis on sterilization and pathogen control has led to the integration of HEPA filters in HVAC systems for hospitals and laboratories.

By Distribution Channel Insights

The direct sales segment was the largest by accounting for a prominent share of the Europe industrial air filtration market in 2025 with the highly customized nature of industrial air filtration projects which require direct engineering collaboration between manufacturers and end users. The complexity of designing filtration systems that must integrate seamlessly with specific industrial processes, necessitating detailed technical consultations and site assessments that intermediaries cannot provide is majorly escalating the growth of the segment. The need for long term service agreements and maintenance contracts, which are more effectively managed through direct relationships is also propelling the growth of Europe industrial air filtration market. Industrial clients prefer dealing directly with manufacturers to ensure access to genuine spare parts specialized training for their staff and rapid response times during emergencies. Statistics from the European Confederation of Iron and Steel Industries indicate that downtime costs in steel plants can exceed 100000 euros per hour, making direct support channels critical for operational continuity. Furthermore, direct sales allow manufacturers to gather precise feedback on product performance which informs future research and development initiatives. The high value and technical specificity of these transactions make the direct channel the most efficient and trusted route for delivering complex filtration solutions to heavy industry.

The indirect sales segment is projected to witness a fastest CAGR of 6.2% from 2026 to 2033. This rapid expansion is propelled by the increasing demand for standardized filtration units among small and medium sized enterprises that lack the resources for direct procurement processes. The primary driving factor is the extensive network of local distributors and system integrators who provide value added services such as installation local inventory management and immediate technical support to smaller industrial clients. According to a report by the European Small Business Alliance, SMEs account for 99% of all businesses in the EU and increasingly rely on local distributors for cost effective and accessible filtration solutions. These intermediaries bundle filtration products with other HVAC components offering a one stop shop experience that simplifies purchasing for non specialist buyers. Data from the European Distributor Organization shows that distributor led sales in the industrial equipment sector grew by 18% in 2023 driven by the convenience of localized supply chains. Additionally, the rise of e commerce platforms operated by major industrial distributors has made it easier for smaller firms to compare and purchase filtration products online. As the base of small industrial operators expands the reliance on indirect channels for efficient and scalable distribution will continue to accelerate.

COUNTRY ANALYSIS

Germany Industrial Air Filtration Market Analysis

Germany was the largest contributor of the Europe industrial air filtration market in 2024 by capturing 26.3% of share, owing to its massive manufacturing base and rigorous environmental standards. According to the German Federal Environment Agency, industrial facilities in Germany invested over 4 billion euros in air pollution control technologies in 2023 to meet stringent particulate matter limits. The country serves as a hub for innovation where leading filtration manufacturers develop next generation technologies specifically designed for high temperature and corrosive applications. The strong emphasis on Industry 4.0 has also led to the rapid adoption of smart filtration systems equipped with IoT sensors for real time monitoring. Government incentives for energy efficient industrial processes further drive the replacement of outdated units with modern high efficiency collectors. The dense concentration of heavy industry in regions like North Rhine Westphalia creates a consistent demand for large scale baghouse and electrostatic precipitator installations. Furthermore, the skilled engineering workforce in Germany supports the complex installation and maintenance requirements of advanced filtration infrastructure. As the engine of European industry Germany continues to set the benchmark for filtration performance and regulatory compliance influencing market trends across the entire region.

United Kingdom Industrial Air Filtration Market Analysis

The United Kingdom Industrial Air Filtration Market growth is likely to be driven by the strong focus on waste to energy and pharmaceutical sectors. The UK Clean Air Strategy, which sets ambitious targets for reducing industrial emissions and protecting public health from fine particulates is eventually to promote new opportunities for the growth of Europe industrial air filtration market. As per reports from the Department for Environment Food and Rural Affairs, the UK government has allocated significant funding to upgrade filtration systems in waste incineration plants to reduce dioxin and furan emissions by 50% by 2030. The robust pharmaceutical industry in the UK drives demand for high grade HEPA filtration systems to maintain sterile manufacturing environments compliant with MHRA regulations. The exit from the European Union has led to the development of independent UK specific environmental standards which often mirror or exceed EU directives ensuring continued investment in filtration technology. The presence of major global filtration companies with headquarters in the UK fosters a competitive environment that accelerates technological advancements. Additionally, the push for net zero emissions has spurred interest in carbon capture ready filtration systems in power generation and heavy industry. The island nation strict planning permissions for industrial expansions also mandate the use of best available techniques for air quality management. These factors combine to create a resilient and high value market for industrial air filtration solutions.

France Industrial Air Filtration Market Analysis

France industrial air filtration market growth is anticipated to grow with its unique requirements in the nuclear aerospace and luxury goods sectors. The extensive nuclear power infrastructure, which demands specialized filtration systems for radioactive particle containment and ventilation. According to the French Nuclear Safety Authority, over 56 nuclear reactors require continuous upgrades to their filtration systems to ensure radiological safety and compliance with evolving security protocols. The French government commitment to reindustrialization through the France 2030 plan, includes billions of euros in investments for modernizing industrial facilities with a focus on environmental sustainability. The luxury perfume and cosmetics industry in Grasse relies on advanced odor control and particulate filtration to maintain product quality and neighborhood relations. Furthermore, the strict enforcement of the French Environmental Code compels industries to adopt the best available techniques for emission reduction.

Italy Industrial Air Filtration Market Analysis

Italy industrial air filtration market growth is driven by its dominant ceramic tile and food processing industries. The need for robust dust collection systems in the ceramic clusters of Sassuolo, which produce a large portion of the world tiles and generate substantial silica dust is additionally to escalate the growth of the market. As per data from Confindustria Ceramica, Italian ceramic manufacturers have invested heavily in dry desulfurization and baghouse filtration systems to meet regional air quality plans that limit PM10 and PM2.5 concentrations. The food and beverage sector another pillar of the Italian economy requires hygienic filtration solutions to prevent cross contamination and ensure product safety under HACCP guidelines. The geographical diversity of Italy means that industrial plants face varying climatic conditions requiring adaptable filtration technologies that can operate efficiently in both humid coastal and dry inland areas. Government incentives under the National Recovery and Resilience Plan support the transition to greener industrial processes including the installation of high efficiency air purification units. The strong tradition of mechanical engineering in Italy also supports a local supply chain for custom filtration components.

Spain Industrial Air Filtration Market Analysis

Spain Industrial Air Filtration Market growth is esteemed to grow with the expanding renewable energy manufacturing and mining sectors. The rapid construction of solar panel and wind turbine factories, which require precise dust control during the production of photovoltaic cells and composite blades. The mining industry in Spain particularly for lithium and copper extraction also generates significant amounts of dust necessitating heavy duty dust collectors to protect worker health and surrounding communities. The Spanish Industrial Emissions Law transposes EU directives into national law enforcing strict limits on particulate emissions from metallurgical and mineral processing plants. The tourism dependent economy also pressures industries to minimize visual and olfactory pollution leading to wider adoption of odor control and mist filtration systems. Regional governments in industrial hubs like the Basque Country and Catalonia, offer grants for companies that upgrade to low emission technologies. The increasing focus on circular economy principles encourages the installation of filtration systems that allow for the recovery and reuse of valuable process materials.

COMPETITIVE LANDSCAPE

The competition within the Europe Industrial Air Filtration Market is characterized by a rivalry between established global conglomerates and specialized regional manufacturers vying for dominance in a technically demanding sector. Incumbent players leverage their vast engineering expertise and proven track records to secure contracts for critical large scale infrastructure projects while smaller firms focus on niche applications or localized service delivery. The market landscape is moderately consolidated at the top tier where a few major entities control significant production capacity and proprietary technology intellectual property. Price competition exists but is often secondary to technical specifications reliability credentials and energy efficiency metrics given the catastrophic consequences of system failure in industrial settings. Regulatory compliance acts as a formidable barrier to entry ensuring that only firms with rigorous quality assurance systems can participate in major tenders across the European Union. Innovation cycles are accelerating as companies race to develop smarter and more durable filtration solutions that integrate seamlessly with Industry 4.0 frameworks. The push for sustainability forces competitors to differentiate themselves through green manufacturing credentials and demonstrable reductions in client carbon footprints. Strategic collaborations with industrial end users for pilot projects have become common as firms seek to validate new technologies before widespread deployment.

KEY MARKET PLAYERS

The major players in the Europe industrial air filtration market include

- Abatement Technologies, Inc.

- Alfa Laval

- AAF

- Camfil Air Pollution Control (APC)

- Con-Air Industries

- Donaldson Company

- Daikin Industries Ltd.

- Electrocorp

- FILCOM GmbH

- Good Life, Inc

- HealthWay Home Products, Inc.

- Honeywell International, Inc

- MANN+HUMMEL

- Philips Electronics N.V.

- Sentry Air Systems, Inc

- Sharp Corporation.

Top Players In The Market

- Donaldson Company operates as a global leader in filtration technology with a profound impact on the Europe Industrial Air Filtration Market through its extensive portfolio of dust collectors and cartridge filters. The company serves diverse sectors including cement power generation and food processing by delivering high efficiency solutions that ensure regulatory compliance. Its global contribution involves setting industry standards for filter media performance and developing proprietary nanofiber technologies that capture ultrafine particles. Recently, Donaldson has strengthened its market position by launching advanced IoT enabled monitoring systems that allow European clients to track filter health in real time. The firm actively expands its manufacturing footprint in the region to reduce lead times and provide localized engineering support. These strategic initiatives reinforce its reputation as an innovator capable of solving complex air quality challenges across various heavy industries worldwide.

- AAF International stands as a premier provider of air filtration solutions with a strong presence in Europe serving critical industries such as pharmaceuticals automotive and chemical processing. The company contributes globally by offering comprehensive air pollution control systems that range from standard baghouses to custom engineered scrubbers for hazardous gas removal. AAF recently intensified its focus on sustainability by introducing product lines designed specifically for carbon capture applications and energy recovery processes. The firm has expanded its service network across major European industrial hubs to ensure rapid maintenance and parts availability for its clients. Strategic partnerships with local engineering firms enable AAF to deliver tailored solutions that address unique site-specific challenges in dense urban environments. These efforts demonstrate its commitment to enhancing industrial air quality while supporting the global transition toward cleaner manufacturing practices and circular economy principles.

- Camfil is a Swedish multinational corporation that leads the Europe Industrial Air Filtration Market with a specialized focus on clean air solutions for process industries and indoor environments. The company plays a vital role globally by supplying high efficiency particulate air filters and molecular contamination control systems to sensitive sectors like semiconductor manufacturing and biotechnology. Camfil, recently strengthened its position by acquiring niche technology firms to enhance its capabilities in removing volatile organic compounds and odors from industrial exhaust streams. The firm actively promotes the concept of total cost of ownership by designing filters that significantly reduce energy consumption in ventilation systems. Its European operations benefit from a robust supply chain and dedicated testing centers that validate product performance against the latest environmental regulations. Camfil also collaborates with industrial clients to develop custom filtration strategies that align with their sustainability goals and corporate social responsibility targets.

Top Strategies Used By Key Market Participants

Key players in the Europe Industrial Air Filtration Market primarily employ strategic acquisitions to expand their technological portfolios and gain immediate access to specialized filtration niches such as molecular contamination control. Companies frequently invest heavily in research and development to innovate new filter media materials that offer higher efficiency while reducing energy consumption and pressure drop. Another dominant strategy involves the integration of Internet of Things sensors and digital monitoring platforms to provide predictive maintenance services that enhance operational reliability for industrial clients. Manufacturers are increasingly focusing on localization by establishing regional production facilities and service centers to reduce supply chain risks and improve response times for customers. Sustainability serves as a critical approach where firms design products that support circular economy principles through recyclable materials and energy recovery capabilities. Furthermore, participants engage in strategic partnerships with engineering firms and original equipment manufacturers to bundle filtration solutions into larger industrial projects. These collective strategies aim to build resilience foster innovation and secure a competitive advantage in a market driven by stringent environmental regulations and the urgent need for industrial decarbonization.

MARKET SEGMENTATION

This research report on the Europe industrial air filtration market is segmented and sub-segmented into the following categories.

By Product Type

- Dust collectors

- Mist collectors

- HEPA filters

- CCF

- Baghouse filters

By Application

- Cement

- Food

- Cereal

- Spices

- Feed and raw grain agriculture

- Eggshell and dust

- Sugar dust

- Flour

- Corn starches

- Others

- Metal

- Grinding

- Sandblasting

- Welding fumes

- Fine powders

- Others

- Power

- Pharmaceuticals

- Other

By Distribution Channel

- Direct Sales

- Indirect Sales

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is industrial air filtration used for in manufacturing facilities?

Industrial air filtration systems remove dust, smoke, and airborne contaminants to maintain clean and safe working environments.

Why is the demand for industrial air filtration increasing in Europe?

Strict environmental regulations and workplace safety standards are driving the adoption of advanced air filtration systems.

Which industries commonly use industrial air filtration systems?

Industries such as manufacturing, pharmaceuticals, food processing, chemicals, and metal processing widely use these systems.

What types of industrial air filtration technologies are commonly used?

Dust collectors, HEPA filters, cartridge filters, and electrostatic precipitators are widely used filtration technologies.

How do industrial air filtration systems improve workplace safety?

They capture harmful airborne particles and pollutants, reducing worker exposure to hazardous substances.

What factors are driving growth in the Europe industrial air filtration market?

Increasing industrialization, environmental compliance requirements, and focus on air quality management are key drivers.

How do industrial air filtration systems support environmental sustainability?

They help industries reduce emissions and control particulate pollution released into the atmosphere.

What challenges affect the industrial air filtration market in Europe?

High installation costs and maintenance requirements can affect adoption among smaller industries.

Which countries play a major role in the Europe industrial air filtration market?

Germany, France, the United Kingdom, and Italy are key contributors due to their strong industrial sectors.

What future trend is expected in the Europe industrial air filtration market?

Growing investment in energy-efficient and smart filtration technologies is expected to drive market development.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com