Europe LED Display Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Conventional LED displays, Surface mounted LED displays), Application, Technology, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2026 To 2034

Europe LED Display Market Size

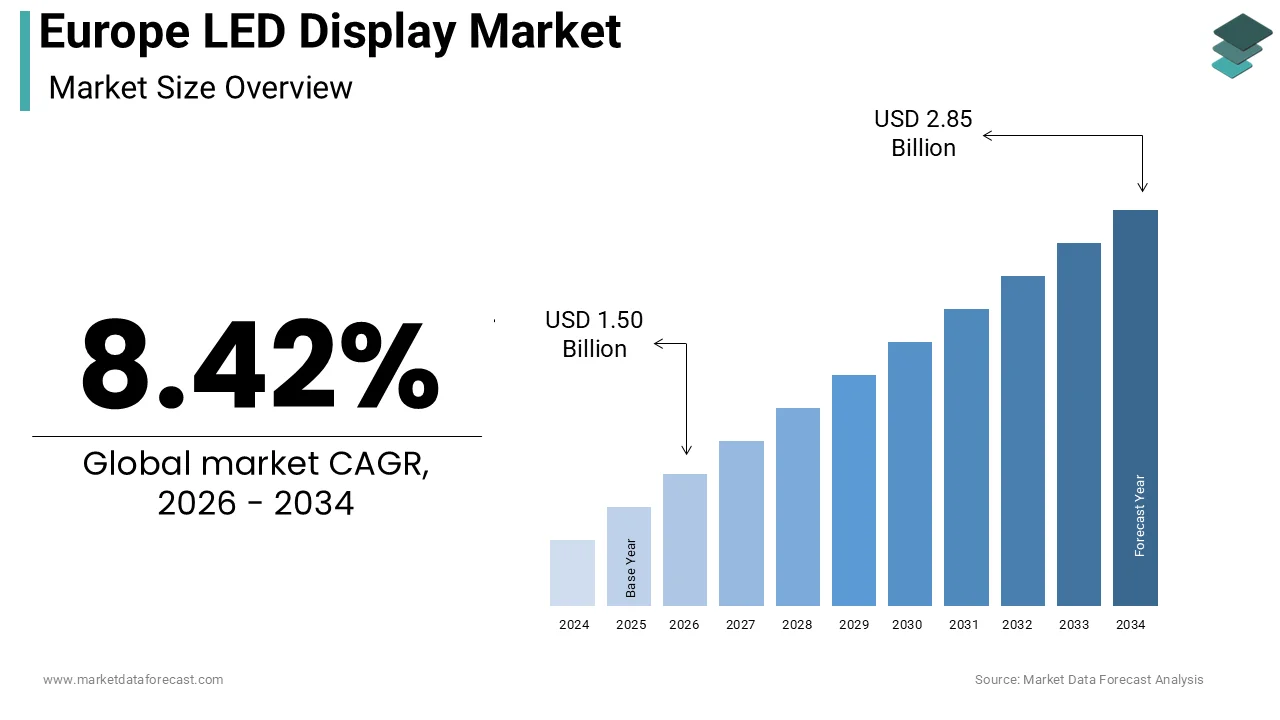

The Europe-led display market size was calculated to be USD 1.38 billion in 2025 and is anticipated to be worth USD 2.85 billion by 2034, from USD 1.50 billion in 2026, growing at a CAGR of 8.42% during the forecast period.

An LED Display (Light Emitting Diode display) is a flat panel display that uses a grid of tiny light-emitting diodes as pixels for a video display. This market is currently undergoing a transformative shift driven by the continent's aggressive digitalization mandates and the proliferation of smart city initiatives that prioritize energy-efficient and high-visibility information systems. Unlike other regions where consumer electronics dominate, the European landscape is uniquely characterized by a strong emphasis on public infrastructure, retail experiential marketing, and strict environmental compliance. According to the European Commission's Digital Economy and Society Index (DESI) 2022, the EU average score reached 52.3, driven primarily by improvements in digital public services, connectivity (such as 5G and fiber coverage), and the integration of digital technologies like Cloud and AI by businesses, rather than display hardware. Furthermore, the European Commission's Green Deal has imposed rigorous energy efficiency standards, compelling a migration from legacy liquid crystal display and projection systems to modern micro LED and mini LED solutions that consume significantly less power. Data from the European Commission and International Energy Agency indicate that the combined building sector (residential and commercial) accounts for approximately 40 percent of total energy consumption in Europe. This creates an urgent imperative for operators to implement comprehensive efficiency measures, including improved insulation and HVAC systems, alongside upgrades to low-power LED lighting. This convergence of regulatory pressure, technological advancement, and the strategic need for dynamic content delivery positions the region as a critical hub for next-generation visual display technologies.

MARKET DRIVERS

Proliferation of Smart City Initiatives and Digital Out-of-Home Advertising

The widespread implementation of smart city frameworks and the resurgence of digital out-of-home advertising drive unprecedented demand for large-format outdoor LED installations. The extensive rollout of smart city projects across major metropolitan areas is the primary growth enabler for the Europe LED display market. These projects integrate high-resolution LED screens as essential nodes for real-time information dissemination, traffic management, and public safety alerts. Municipalities are increasingly replacing static billboards with dynamic digital canvases that can update instantly during emergencies or display contextual advertisements, thereby maximizing revenue potential and civic utility. According to the European Commission, the Smart Cities Marketplace is a vital hub for over a hundred cities to share scalable urban solutions. These cities are increasingly investing in connected digital infrastructure that utilizes durable outdoor display technology to enhance citizen communication and public safety. The digital out-of-home advertising sector has seen a remarkable recovery and growth, with data from the European Outdoor Advertising Association indicating that digital screen networks grew by 18 percent in 2023, capturing a larger share of advertising budgets due to their ability to target audiences with time-sensitive content. Furthermore, the integration of these displays with Internet of Things sensors allows for adaptive brightness and content modulation based on weather and pedestrian flow, enhancing energy efficiency and viewer engagement. This strategic alignment of urban planning goals with commercial advertising needs ensures a sustained and robust pipeline for outdoor LED display deployments across the continent.

Surge in Experiential Retail and Corporate Collaboration Spaces

The transformation of physical retail into experiential destinations and the evolution of hybrid work models fuel demand for fine-pitch indoor LED video walls. The radical reimagining of physical retail spaces and corporate environments further boosts the expansion of the Europe LED display market. Businesses are deploying fine-pitch LED video walls to create immersive brand experiences and facilitate seamless hybrid collaboration. As e-commerce continues to grow, brick and mortar stores in Europe are pivoting towards experiential concepts that rely on stunning visual storytelling to attract foot traffic, making high-definition LED displays a central element of store design. Studies indicate that large-format LED installations are becoming standard features in new flagship stores across major European capitals. These displays are used as powerful experiential tools to create brand-specific atmospheres and drive customer footfall in competitive high-street environments. Simultaneously, the shift to hybrid work has rendered traditional projectors obsolete in favor of ultra-high resolution LED panels that offer superior clarity for video conferencing and data visualization in executive boardrooms and control centers. Data from the International Data Corporation shows a significant increase in enterprise spending on high-performance digital hardware. In Western Europe, businesses are prioritizing investments in technologies that offer long-term reliability and lower maintenance requirements to support their ongoing digital transformation projects. The ability of modern LED modules to be configured into arbitrary shapes and sizes allows architects to integrate them seamlessly into interior designs, further accelerating adoption in luxury hospitality and high-end corporate sectors.

MARKET RESTRAINTS

High Initial Capital Expenditure and Installation Complexity

The substantial upfront investment required for premium LED systems and the technical intricacies of installation act as significant barriers for small and medium enterprises. Upgrading visual infrastructure is a challenge for many small and medium-sized enterprises in the region due to the high cost and complex installation of fine-pitch LED panels, which restrains the growth of the Europe LED display market. This substantial initial investment acts as a significant restraint to the Europe LED display market. Unlike conventional display technologies, professional-grade LED video walls involve not only the cost of the modules but also expensive supporting structures, powerful processing units, and specialized cooling systems to ensure optimal performance and longevity. According to sources, nearly 70 percent of potential adopters cite high upfront costs as the primary obstacle to digital signage implementation, particularly in a climate of economic uncertainty and rising interest rates. Furthermore, the installation process frequently requires structural assessments, custom cabling, and certified technicians, adding layers of logistical complexity and expense that extend project timelines. Data from the Construction Products Regulation compliance bodies indicates that retrofitting older buildings with heavy LED facades often necessitates costly reinforcement works to meet safety standards. These financial and technical hurdles limit the market penetration to large corporations and public sector entities with deep pockets, slowing down the democratization of LED technology across the broader commercial landscape.

Stringent Environmental Regulations and Light Pollution Concerns

Rigorous European Union directives on energy consumption and light pollution impose strict operational constraints on outdoor LED deployment. Stringent regulations on light pollution and energy usage are severely hampering the Europe LED display market expansion. These complex, localized, and national restrictions force operators to strictly manage outdoor LED brightness and operating hours. The European Union's Energy Efficiency Directive and various national laws aimed at preserving the night sky and reducing ecological disruption have led to bans or severe limitations on brightly lit displays in residential zones and protected natural areas. Data from the International Dark Sky Association highlights that several European cities have halted new permits for outdoor LED installations until stricter impact assessments are conducted. Compliance with these regulations often requires the integration of advanced dimming sensors and software controls, increasing system costs and operational overhead. The fear of non-compliance penalties and the potential for future retroactive bans creates a cautious investment environment, causing some advertisers and municipalities to delay or cancel planned LED projects despite the technology's visual appeal.

MARKET OPPORTUNITIES

Integration of Micro LED and Transparent Display Technologies

The advent of micro LED and transparent LED solutions offers a transformative opportunity to penetrate high-end architectural and automotive applications. The rapid maturation of micro LED and transparent LED technologies is a paramount opportunity for the Europe LED display market. These advancements enable the creation of invisible, seamless, and ultra-high-resolution displays for integration into glass facades, retail windows, and vehicle windshields. These innovations overcome the aesthetic and spatial limitations of traditional opaque LED cabinets, opening up entirely new application verticals in luxury architecture and automotive heads-up displays. The ability of transparent LEDs to maintain visibility while displaying dynamic content makes them ideal for museum exhibits, airport terminals, and high-end retail storefronts where preserving the view is critical. Advanced form factors are set to make LED technology more accessible as production costs fall and yields improve. This breakthrough allows LEDs to penetrate new markets previously restricted by bulky display technologies. The result is substantial market differentiation and increased value creation.

Expansion of Virtual Production Studios in the Media Sector

The booming film and broadcast industry's shift towards virtual production sets creates a lucrative niche for high refresh rate and color-accurate LED volumes. The explosive growth of virtual production studios across Europe provides a potential prospect for the expansion of the Europe LED display market. Filmmakers and broadcasters are increasingly replacing green screens with massive, high-fidelity LED volumes that render real-time backgrounds. This technology, popularized by major productions, offers superior lighting realism and immediate visual feedback, drastically reducing post production time and costs for European content creators. According to sources, the number of dedicated virtual production facilities in Europe increased in 2023, with major hubs emerging in the United Kingdom, Germany, and Spain to serve the growing demand for high-quality local and international content. Each of these studios requires hundreds of square meters of fine-pitch LED panels with extremely high refresh rates and wide color gamuts to prevent flickering and ensure accurate color reproduction under camera capture. The demand for bespoke, high-performance LED solutions is set to rise as production houses adopt this workflow for global competition. Consequently, a high-margin segment is emerging within the broader market.

MARKET CHALLENGES

Supply Chain Volatility for Rare Earth Elements and Semiconductors

The reliance on imported rare earth materials and semiconductor components creates persistent supply chain vulnerabilities and price instability. Acute import dependency for specialized components and rare earth materials is a major hurdle for the European LED display market. The supply of these materials is subject to geopolitical tensions and global logistics bottlenecks. The manufacturing of high-brightness LEDs requires materials such as gallium, indium, and yttrium, the majority of which are sourced from outside Europe, leaving the regional supply chain exposed to export controls and trade disputes. According to research, the European Union imports most of its heavy rare earths, creating a strategic vulnerability that can lead to sudden price spikes and allocation shortages. Also, the volatility complicates long-term planning and pricing strategies for system integrators, who often struggle to honor fixed price contracts amidst fluctuating raw material costs. The region must develop more resilient domestic sourcing or recycling capabilities for these critical inputs. Until then, supply chain instability will remain a persistent threat to market growth and profitability.

Lack of Standardized Maintenance and Recycling Protocols

The absence of unified industry standards for maintenance and the complexity of recycling electronic waste hinder sustainable lifecycle management. Fragmented maintenance and a lack of standardized recycling for end-of-life modules pose an escalating challenge for the European LED display market. This situation directly conflicts with European Union circular economy objectives. Unlike simpler electronic devices, LED displays consist of complex assemblies of plastics, metals, and hazardous electronic components that are difficult to separate and recycle efficiently using current infrastructure. The absence of a unified standard for modular repair and component replacement leads to the premature disposal of entire panels when only a few modules fail, exacerbating electronic waste issues. Research highlights that the electronics sector is a priority area for improvement, with new regulations expected to mandate higher recyclability rates and right-to-repair provisions. Manufacturers face the dual burden of developing easily recyclable products while navigating a patchwork of national waste management laws, creating operational inefficiencies and reputational risks that could stifle market expansion if not addressed through industry-wide collaboration.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.42% |

| Segments Covered | By Type, Application, Technology, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Samsung Electronics, LG Electronics, Sony Corporation, Panasonic Corporation, Daktronics Inc., Barco NV, Leyard Optoelectronic Co., Ltd., Unilumin Group Co., Ltd., Absen Optoelectronic Co., Ltd., Sharp Corporation |

SEGMENTAL ANALYSIS

By Type Insights

The Surface Mounted LED Displays segment was the largest segment in the Europe LED display market and captured a significant share in 2025. This supremacy of the segment is attributed to its superior image quality, wider viewing angles, and versatility, which make it the preferred choice for both indoor fine pitch applications and high resolution outdoor advertising across the continent. A key driver for the dominance of surface-mounted device technology is its ability to deliver exceptional color consistency, higher brightness levels, and wide viewing angles that are critical for commercial signage and broadcast environments. Unlike conventional through-hole LEDs, surface-mounted devices allow for tighter pixel pitches, resulting in smoother images that are essential for close viewing distances in retail stores, control rooms, and corporate lobbies. The integration of red, green, and blue chips into a single package reduces the module thickness and weight, facilitating easier installation on fragile interior walls and glass facades. Also, the optical superiority makes them the standard for high-end applications where brand image and visual fidelity are paramount, securing their leading market position. An additional factor sustaining the leadership of surface-mounted displays is their remarkable versatility, allowing manufacturers to produce units that are robust enough for harsh outdoor weather yet refined enough for delicate indoor settings. Advances in encapsulation materials have enabled surface-mounted devices to achieve high ingress protection ratings against dust and water, making them suitable for everything from stadium scoreboards to bus shelter advertisements without compromising performance. The technology scales down effectively for indoor video walls, creating a unified supply chain and reducing costs for integrators who serve diverse sectors. This dual capability ensures that surface-mounted displays remain the go-to solution for a vast array of use cases, driving volume and revenue growth across the entire market spectrum.

The Conventional LED Displays segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 6.8% during the forecast period due to its unmatched durability and cost effectiveness for large-scale outdoor infrastructure projects where extreme weather resistance and long operational life are non-negotiable requirements. The primary catalyst for the rapid expansion of conventional LED displays, specifically those using through-hole technology, is their proven resilience in the face of Europe's increasingly volatile weather patterns, including heavy snow loads, hail, and extreme temperature fluctuations. The individual LED lamps in conventional displays are encased in robust epoxy shells and mounted with leads that penetrate the circuit board, providing superior mechanical stability compared to surface-mounted alternatives. The longevity of these units, often exceeding 100000 hours even under stress, reduces the total cost of ownership for public sector clients who require reliable infrastructure with minimal maintenance intervals. This reputation for indestructibility ensures steady demand in specific high-risk outdoor niches. A key driver for the robust growth of the conventional LED segment is its significant cost advantage when deploying massive display areas required for highways, airports, and large sports venues. For applications where viewing distances are substantial and ultra-fine pixel resolution is unnecessary, conventional through-hole LEDs offer a much lower price point per square meter while delivering sufficient brightness to compete with direct sunlight. The simplicity of the technology allows for localized repair and component swapping, further reducing operational expenses for facility managers. European governments continue to invest in expanding digital information networks across vast geographical areas. Consequently, the economic efficiency of conventional LED displays ensures they remain a vital and growing segment despite the rise of newer technologies.

By Application Insights

The Indoor application segment dominated the Europe LED display market and accounted for a 58.7% share in 2025. This dominance of the segment is credited to the explosive growth of digital signage in retail, corporate offices, and entertainment venues, where high-resolution visual communication is essential for engagement and operational efficiency. The preeminence of the indoor segment is fundamentally driven by the strategic shift in the European retail sector towards experiential shopping, where brands utilize immersive LED video walls to differentiate themselves from online competitors and attract foot traffic. Physical stores are increasingly becoming showrooms that rely on dynamic content to tell brand stories, showcase products in action, and create Instagram-worthy moments that drive social media engagement. The ability of modern indoor LED panels to curve, fold, and integrate seamlessly into architectural designs allows retailers to create unique visual environments that static posters cannot match. As retailers continue to reinvest in physical locations to combat e-commerce pressure, the demand for high-quality indoor LED solutions remains robust, securing the segment's leading position. Also supporting this segment is the widespread adoption of hybrid work models, which has necessitated the upgrade of conference rooms, boardrooms, and collaboration hubs with superior visual presentation tools. Traditional projectors are being rapidly replaced by flat panel LED displays that offer better visibility in well-lit rooms, higher resolution for detailed data analysis, and seamless connectivity for video conferencing platforms. The clarity and brightness of indoor LED screens ensure that remote participants can see whiteboard sessions and presentations clearly, fostering better communication across distributed teams. This structural change in work culture creates a sustained and recurring demand for indoor LED installations across all industry verticals, from finance to education.

The outdoor application segment is expected to exhibit a noteworthy CAGR of 9.2% from 2026 to 2034, owing to the resurgence of the digital out-of-home advertising industry, the rollout of smart city infrastructure, and the modernization of public transport information systems. One of the major drivers of the rapid expansion of the outdoor segment is the aggressive digitization of advertising networks across European cities, as brands seek to leverage real-time, location-based marketing capabilities that static billboards cannot provide. Digital out-of-home screens allow advertisers to change content instantly based on time of day, weather conditions, or live events, maximizing relevance and return on investment. The ability to program multiple ads on a single screen increases inventory yield for site owners, accelerating the ROI for new installations. As urban centers become more crowded and competitive for consumer attention, the dynamic nature of outdoor LED displays ensures they remain the most effective medium for mass reach, driving rapid market expansion. Further boosting this segment is the extensive deployment of smart city initiatives that utilize outdoor LED displays as critical interfaces for public safety, traffic management, and civic engagement. Municipalities are installing networked LED screens in town squares, transit hubs, and along highways to disseminate emergency alerts, traffic updates, and community news in real time, enhancing urban resilience and livability. These public sector projects often involve large-scale deployments that significantly boost market volume. As European governments prioritize digital transformation to improve service delivery and safety, the demand for rugged, high-visibility outdoor LED solutions will continue to accelerate at a pace surpassing indoor applications.

By Technology Insights

The conventional LED technology segment held the majority share of 65.2% of the Europe LED display market in 2025 because of its maturity, cost efficiency, and proven reliability for large-format displays where ultra-fine pixel pitch is not the primary requirement. For large-scale projects such as highway signage, building facades, and stadium screens, traditional LED technology remains the most cost-efficient choice due to its well-established production infrastructure. The technology has benefited from decades of optimization, resulting in high yields and competitive pricing that make it accessible for municipal budgets and large venue operators who need to cover vast surface areas without prohibitive costs. The availability of standardized components and a wide pool of skilled technicians for installation and maintenance further reduces barriers to adoption. This economic advantage ensures that conventional LED remains the default choice for applications where viewing distances allow for slightly larger pixel pitches, securing its dominant market position. Following this, the segment is backed by its renowned durability and straightforward maintenance protocols, which are critical for installations in hard-to-reach or harsh environments. The modular design of conventional LED cabinets allows for easy replacement of individual units or power supplies without specialized tools, minimizing downtime for critical infrastructure like traffic control centers and sports arenas. The robustness of the technology against moisture, dust, and physical impact makes it ideal for outdoor applications where reliability is paramount. This track record of dependability gives facility managers confidence in long term performance, ensuring continued preference for conventional LED technology over newer, less proven alternatives in mission-critical scenarios.

The Micro-LED segment is predicted to witness the highest CAGR of 28.5% between 2026 and 2034. This swift expansion of the segment is fueled by breakthroughs in manufacturing scalability, the demand for ultra-high resolution transparent displays, and the proliferation of augmented reality applications in automotive and consumer electronics. A strong force behind the explosive growth of Micro-LED technology is the recent resolution of key manufacturing bottlenecks, particularly in mass transfer techniques and defect repair processes, which have significantly improved yield rates and reduced production costs. Historically, the complexity of placing millions of microscopic LEDs onto a substrate hindered commercial viability, but advancements in laser transfer and self-assembly methods have enabled mass production capabilities. These improvements are making Micro-LED displays competitive for smaller form factors such as smartwatches and heads-up displays, expanding the addressable market beyond large video walls. As economies of scale kick in, the price premium for Micro-LED is expected to decrease rapidly, driving widespread adoption in premium consumer electronics and automotive sectors. This segment is also built up by the unique ability of the technology to deliver unparalleled brightness, contrast, and transparency, enabling novel applications that are impossible with LCD or OLED technologies. Micro-LEDs can be fabricated on transparent substrates, creating invisible displays that can be integrated into shop windows, museum exhibits, and vehicle windshields without obstructing the view, a feature highly valued in luxury retail and automotive design. The technology's self-emissive nature also ensures perfect blacks and infinite contrast ratios, making it the ultimate choice for high-end home theater and professional monitoring. This combination of aesthetic versatility and optical superiority positions Micro-LED as the fastest-growing technology segment.

REGIONAL ANALYSIS

Germany LED Display Market Analysis

Germany led the Europe LED display market and occupied a 26.8% share in 2025. Robust manufacturing, a strong automotive sector, and top-tier trade fairs drive the nation's preeminence and demand for premium visual technology. Germany's massive manufacturing and exhibition sectors, powered by the nation's top-tier economy, drive the market for advanced, multifunctional LED displays. The country hosts world-renowned trade fairs like Hanover Messe and IFA, which serve as global launchpads for new LED technologies and generate significant domestic sales. Furthermore, Germany's strict energy efficiency regulations have accelerated the replacement of legacy lighting and display systems with next-generation low-power LED solutions in public buildings and commercial spaces. The presence of major LED component manufacturers and system integrators within the country fosters a vibrant ecosystem of innovation and application, ensuring Germany remains the primary engine of the European LED display market.

United Kingdom LED Display Market Analysis

The United Kingdom was the next prominent country in the European market and accounted for a share of 18.4% because of its thriving media and entertainment industry, extensive retail sector, and significant investments in smart city infrastructure across major urban centers. The UK's strong market standing is largely attributable to London's status as a global advertising capital, where digital out of home screens in locations like Piccadilly Circus and Times Square equivalent sites command premium rates and drive continuous upgrades to high-resolution LED arrays. The country's vibrant film and television production sector has also embraced virtual production techniques, leading to a surge in demand for fine-pitch LED volumes in studios across England and Scotland. Additionally, the UK government's levelling up agenda has funded digital signage projects in transport hubs and public spaces in secondary cities to improve connectivity and information access. The combination of a strong creative economy, aggressive retail digitization, and public sector modernization ensures the UK remains a critical and dynamic market for LED displays.

France LED Display Market Analysis

France is another key player in the Europe LED display market due to its ambitious smart city initiatives, a strong tourism sector requiring multilingual digital signage, and a robust public transportation network undergoing digital transformation. Also, France's market strength is underpinned by extensive government programs aimed at modernizing urban infrastructure, with cities like Paris, Lyon, and Marseille deploying vast networks of LED displays for traffic management, public safety alerts, and cultural promotion. The country's status as the world's top tourist destination necessitates dynamic, multilingual information systems in airports, train stations, and attractions, driving consistent demand for durable outdoor and indoor LED solutions. The upcoming Olympic Games legacy has also spurred long-term investments in digital infrastructure that will continue to benefit the market post-event. Furthermore, the French retail sector is rapidly adopting experiential technologies to compete with e-commerce, fueling growth in indoor commercial displays. This blend of public sector leadership and private sector innovation positions France as a pivotal market in Western Europe.

Italy LED Display Market Analysis

Italy expanded steadily in the regional market owing to its rich cultural heritage sites, utilizing discreet LED solutions, a strong design and fashion industry, and increasing adoption of LED technology in sports stadiums and public squares. Moreover, Italy's significant market presence is driven by the unique requirement to integrate modern display technology into historic environments without compromising aesthetic integrity, spurring demand for custom-shaped, transparent, and fine-pitch LED solutions that blend seamlessly with architecture. The country's passion for football and hosting of major sporting events has led to widespread renovations of stadiums with state-of-the-art LED perimeter boards and giant screens, adhering to international broadcasting standards. Additionally, Italy's renowned fashion and design sectors utilize LED displays extensively in Milan and other fashion capitals for runway shows and flagship store experiences, setting global trends in visual merchandising. The government's tourism recovery plan also includes funding for digital information points in heritage sites, further expanding the market. This fusion of tradition and modernity ensures Italy remains a key growth area for specialized LED applications.

Spain LED Display Market Analysis

Spain is anticipated to grow notably in the European market during the forecast due to its booming tourism industry, extensive coastal resort developments, and aggressive rollout of digital signage in transport hubs and commercial centers. In addition, Spain's market trajectory is influenced by its status as a premier holiday destination, which drives heavy investment in LED displays for hotels, resorts, and entertainment venues along the Costa del Sol and Balearic Islands to enhance guest experiences and promote activities. The country's major cities, including Madrid and Barcelona, are expanding their public transport networks with modern digital information systems featuring bright, weather-resistant LED screens to serve millions of commuters and tourists annually. The retail sector is also witnessing a revival, with shopping centers upgrading to interactive LED kiosks and video walls to attract visitors. Furthermore, Spain's commitment to becoming a leading tech hub in Southern Europe is fostering startups focused on LED content management and integration. This combination of tourism-driven demand and urban modernization ensures Spain remains a vital market for LED displays in the region.

COMPETITION OVERVIEW

The competition in the Europe LED display market is characterized by intense rivalry among established multinational corporations and agile regional specialists vying for dominance in specific application verticals. Large global players leverage their extensive manufacturing networks and deep technical expertise to secure long term contracts with major retailers and municipal authorities across the continent. This trend towards comprehensive solution providers creates high barriers to entry for smaller firms unless they possess highly differentiated, transparent, or flexible display technologies. The competitive landscape is further complicated by stringent energy efficiency regulations and varying safety standards across different European nations, which demand rigorous testing and certification before market approval. Companies must therefore invest significantly in research and development to demonstrate superior brightness and longevity while navigating complex procurement processes. Innovation speed and the ability to provide localized after-sales support are critical differentiators that determine market success. Furthermore, strategic alliances between display manufacturers and software developers have become essential for accessing cutting-edge content management systems to accelerate product adoption. The market remains dynamic with continuous entries of Micro LED and augmented reality solutions challenging traditional standards and reshaping competitive dynamics across the region.

KEY MARKET PLAYERS

A few major players of the Europe LED display market include

- Samsung Electronics

- LG Electronics

- Sony Corporation

- Panasonic Corporation

- Daktronics Inc

- Barco NV

- Leyard Optoelectronic Co., Ltd

- Unilumin Group Co., Ltd

- Absen Optoelectronic Co., Ltd

- Sharp Corporation

Top Strategies Used by Key Market Participants

Key players in the Europe LED display market predominantly employ strategic product innovation and vertical integration to expand their portfolios and enhance technological capabilities. Companies frequently launch next-generation Micro LED and transparent display panels embedded with artificial intelligence features to differentiate their offerings and meet evolving consumer expectations. Another major strategy involves forming extensive collaborations with system integrators and content creators to develop customized visual solutions for specific verticals like retail and sports. Market participants also focus heavily on expanding their service and maintenance networks within the European Union to ensure rapid response times and maximize uptime for critical installations. Investment in research and development remains a cornerstone strategy as firms strive to achieve breakthroughs in energy efficiency and pixel density. Additionally, companies pursue targeted acquisitions of software startups to rapidly incorporate advanced content management and analytics tools into their existing hardware platforms. These combined approaches allow industry leaders to navigate complex regulatory landscapes while maintaining a competitive edge in this rapidly evolving technological sector.

Leading Players in the Europe LED Display Market

- Samsung Electronics Co., Ltd. stands as a global pioneer in display technology with a profound impact on the European LED landscape through its innovative Micro LED and fine pitch solutions. The company contributes significantly to the global market by setting benchmarks for resolution, brightness, and energy efficiency in both commercial and consumer segments. Recently, Samsung has strengthened its position by launching next-generation transparent Micro LED displays tailored for high-end retail and architectural applications across major European cities. The firm actively collaborates with European system integrators to deploy massive video walls for sports stadiums and virtual production studios. These strategic initiatives ensure their technology remains at the forefront of visual excellence while addressing the growing demand for immersive and sustainable display solutions throughout the continent.

- LG Electronics Inc operates as a leading innovator in visual display systems with a dominant presence in the European market, particularly within digital signage and OLED hybrid technologies. The company contributes globally by delivering versatile LED panels that offer superior color accuracy and flexible form factors for diverse installation environments. Their recent actions to solidify market presence include introducing ultra-slim indoor LED tiles designed specifically for corporate collaboration spaces and luxury retail storefronts in Western Europe. LG Electronics has also invested heavily in expanding its service network to provide rapid maintenance and content management support for large-scale outdoor advertising networks. The firm frequently engages in partnerships with event organizers to supply state-of-the-art screens for major cultural and sporting events. By focusing on design aesthetics and operational reliability, LG Electronics enhances value for customers seeking premium visual experiences. These efforts demonstrate their commitment to driving technological advancement and maintaining leadership in the competitive European arena.

- Signify N.V. is a specialized lighting and display solutions provider that has established itself as a key player in the European market through its focus on connected LED systems and smart city infrastructure. The company makes a substantial global contribution by integrating LED displays with Internet of Things platforms to enable dynamic content delivery and energy optimization. Their recent strategy to strengthen their European position involves deploying intelligent outdoor LED networks that adapt to environmental conditions and traffic patterns in major metropolitan areas. Signify has also expanded its portfolio to include modular LED video walls for public transport hubs and emergency information systems. The firm continues to invest in research and development for sustainable manufacturing processes that align with strict European environmental regulations. By maintaining a dedicated focus on connectivity and sustainability, Signify addresses the evolving needs of municipal authorities and commercial operators. Their persistent innovation in smart display ecosystems ensures they remain a vital partner for cities and businesses seeking efficient and future-proof visual communication tools.

MARKET SEGMENTATION

This research report on the Europe LED display market has been segmented and sub-segmented based on type, application, technology & region.

By Type

- Conventional LED displays

- Surface-mounted LED displays

By Application

- Indoor

- Outdoor

By Technology

- Conventional LED

- OLED

- Micro-LED

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the Europe LED display market?

Growth is driven by increasing demand for digital signage, advertising displays, and advancements in display technologies.

2. What are the main types of LED displays?

Indoor LED displays, outdoor LED displays, and transparent LED displays are the key types.

3. Which applications dominate the market?

Advertising, retail, sports stadiums, transportation hubs, and corporate environments are major applications.

4. What is digital signage?

Digital signage refers to electronic displays used for advertising, information sharing, and branding in public spaces.

5. What are the advantages of LED displays?

They offer high brightness, energy efficiency, durability, and better visibility compared to traditional displays.

6. What challenges does the market face?

High initial costs and competition from alternative display technologies are major challenges.

7. Who are the key players in the market?

Leading companies include Samsung Electronics, LG Electronics, and Barco NV.

8. What is the role of outdoor advertising in market growth?

Outdoor advertising significantly boosts demand for large-scale LED displays.

9. What distribution channels are used?

Direct sales, system integrators, and distributors are commonly used channels.

10. What is the future outlook of the Europe LED display market?

The market is expected to grow steadily due to rising digitalization and increasing demand for visual communication solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com