Europe Maize Market Size, Share, Trends, & Growth Forecast Report – Segmented By End-User, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034.

Europe Maize Market Report Summary

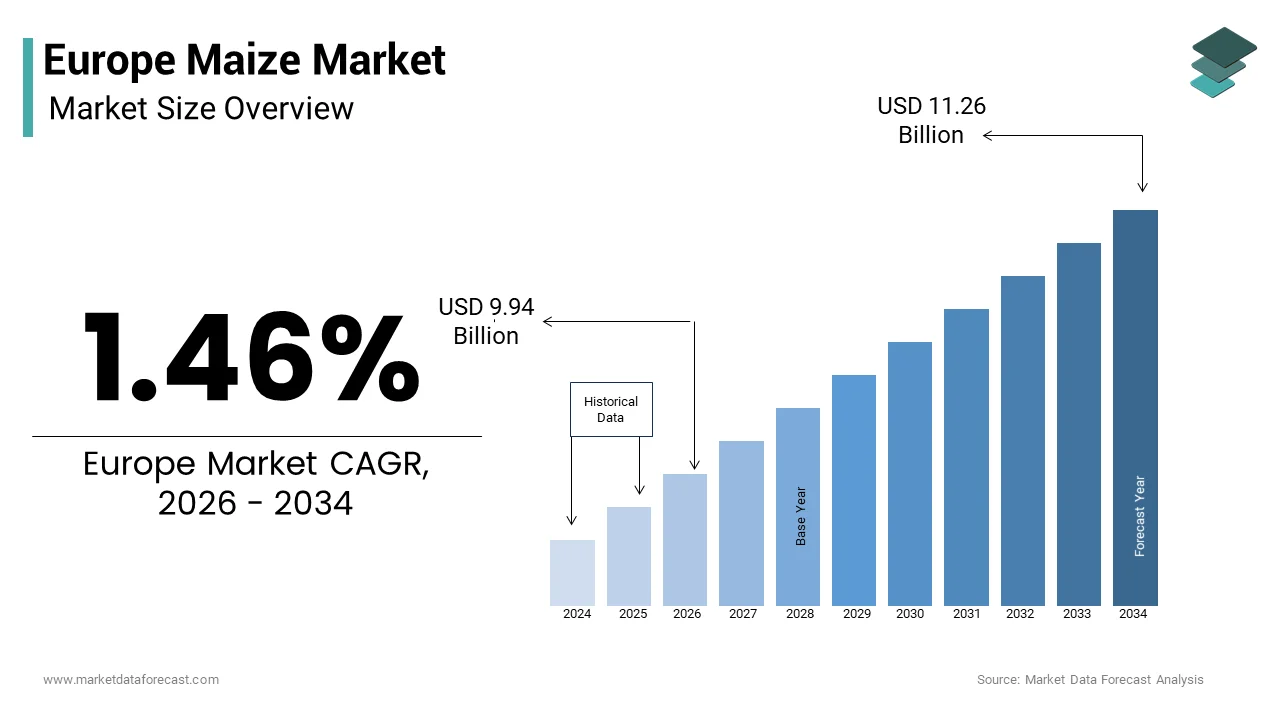

The Europe maize market was valued at USD 9.79 billion in 2025, is estimated to reach USD 9.94 billion in 2026, and is projected to reach USD 11.26 billion by 2034, growing at a CAGR of 1.46% during the forecast period from 2026 to 2034. The growth of the Europe maize market is driven by its extensive use across industrial applications, animal feed production, and food processing industries. Increasing demand for maize-based biofuels, starch derivatives, and sweeteners, along with its critical role in livestock nutrition, is supporting market stability. However, the relatively moderate growth rate reflects market maturity, fluctuating climatic conditions, and evolving agricultural policies across the region.

Key Market Trends

- Increasing utilization of maize in industrial applications such as bioethanol, starch processing, and sweetener production.

- Stable demand from the animal feed industry, particularly in poultry and livestock sectors.

- Growing emphasis on sustainable farming practices and yield optimization through advanced agricultural technologies.

- Expansion of export-oriented production in Eastern European countries.

- Impact of climate variability and regulatory frameworks on maize cultivation and supply dynamics.

Segmental Insights

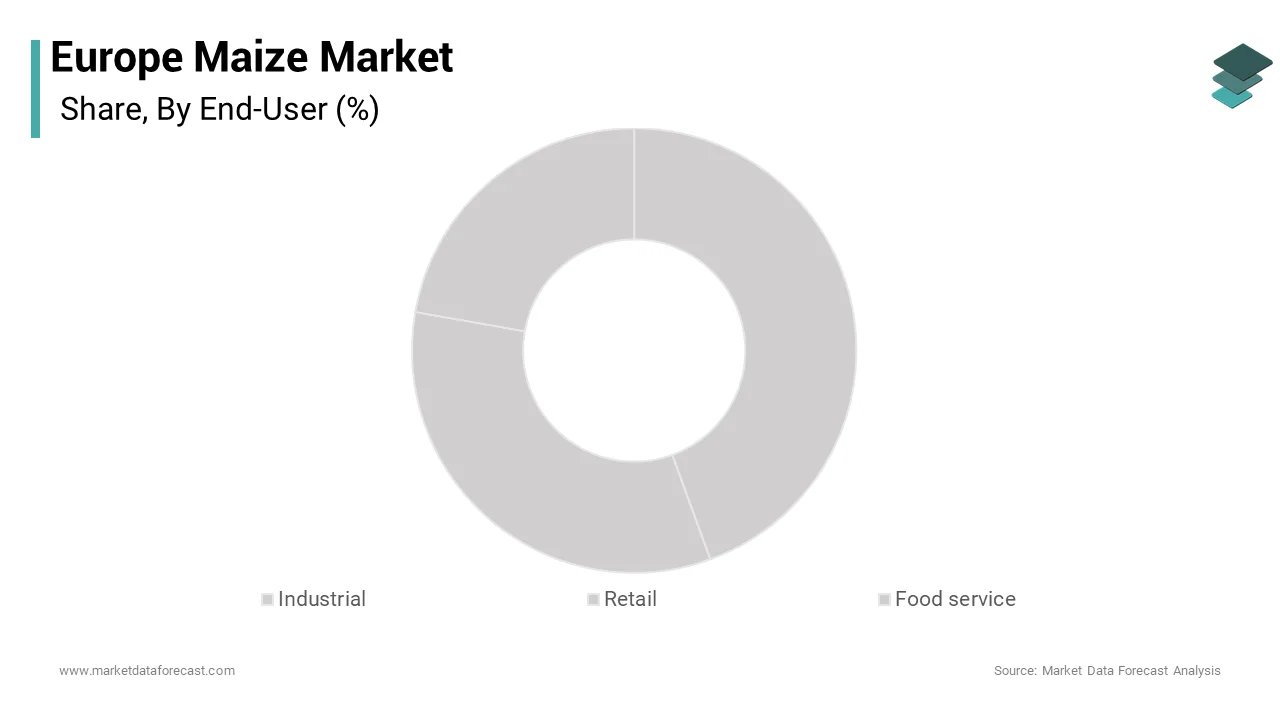

Based on end user, the industrial segment dominated the Europe maize market in 2025, accounting for 65.1% of the total market share. The segment’s dominance is attributed to the widespread use of maize in producing biofuels, processed food ingredients, and industrial starch products, making it a key raw material for multiple downstream industries.

Regional Insights

The Europe maize market exhibits diverse regional dynamics supported by agricultural capabilities and export potential.

- France led the market in 2025, driven by its strong agricultural infrastructure, high production capacity, and well-established supply chains.

- Romania followed closely, supported by its vast arable land and significant role as a major exporter of raw maize to global markets.

- Germany remains a key contributor due to its advanced industrial processing capabilities and strong domestic consumption demand.

- Hungary continues to experience steady growth, benefiting from high yield efficiency and its strategic position as a transit hub for grain exports in Eastern Europe.

- Italy is expected to witness notable growth during the forecast period, supported by increasing demand from food processing and feed industries.

Competitive Landscape

The Europe maize market is characterized by the presence of global agribusiness giants and regional players competing on production efficiency, supply chain integration, and product innovation. Companies are focusing on expanding their processing capabilities, enhancing seed technologies, and strengthening global trade networks to maintain a competitive edge.

Prominent players in the Europe maize market include Alianz Global Groups Pty Ltd., Archer Daniels Midland Co., Limagrain, Corteva Agriscience, KWS Saat, Associated British Foods Plc, Balaji Exim, Bayer AG, Bunge Ltd., Cargill Inc., CGB Enterprises Inc., COFCO Corp., Exotic Exim, Fazaz Global Concepts LLC, Gombella Integrated Services Ltd., Greenfield Global Inc., Groupe Limagrain, Ingredion Inc., Ista International General Trading LLC, Louis Dreyfus Holding BV, Maeddy Impex Pvt. Ltd., Roquette Freres SA, Tate and Lyle PLC, and Tereos Participations.

Europe Maize Market Size

The Europe maize market size was valued at USD 9.79 billion in 2025 and is anticipated to reach USD 9.94 billion in 2026 to reach USD 11.26 billion by 2034, growing at a CAGR of 1.46% during the forecast period from 2026 to 2034.

Maize, scientifically classified as Zea mays, functions as a foundational pillar within the European agricultural ecosystem, serving dual critical roles as the primary energy source for livestock nutrition and a vital raw material for industrial starch and bioenergy sectors. In the European Union, common wheat remains the dominant cereal crop, though grain maize is a key sector with production volumes reaching 58.9 million tonnes in 2024 according to data from Eurostat. The cultivation footprint spans approximately 8.7 million hectares, reflecting a 4.5 percent increase in planted area despite fluctuating climatic conditions as per statistics from Eurostat. France and Romania traditionally lead production outputs, although recent data indicates a divergence where Germany contributed significantly to volume increases while other nations faced yield contractions due to environmental stressors according to reports by the European Commission. Beyond its role in animal feed, which consumes the majority of the harvest, maize supports a robust bioenergy sector and provides essential starch for food manufacturing industries. The market dynamics are heavily influenced by the interplay between domestic harvest capabilities and import dependencies, particularly as the bloc seeks to balance food security with renewable energy mandates. Recent forecasts by the United States Department of Agriculture project production to stabilize at approximately 58.0 million tonnes in 2025, contradicting earlier optimistic outlooks of a sharp rebound. This commodity remains integral to the rural economy, supporting millions of farming households and underpinning the supply chains of meat, dairy, and biofuel sectors throughout the region.

MARKET DRIVERS

Expanding Livestock Feed Consumption Drives Core Demand

Structural Dependency of Animal Agriculture

The insatiable demand from the livestock sector is the primary factor propelling the growth of the Europe maize market. This sector utilizes maize as the fundamental energy component in compound feed formulations. Approximately 61 percent of total cereal production in the region is dedicated to animal feed, with maize specifically seeing an even higher utilization rate (estimated at over two-thirds) for this purpose, underlining its indispensable role in sustaining the European meat and dairy industries according to findings from the European Feed Manufacturers Federation (FEFAC). In major producing nations like France, the distribution of compound feed reveals that the poultry sector is the primary consumer, followed by the pig farming sector, which has seen a decline in share. Recent data from FranceAgriMer indicates that poultry feed production significantly outpaces pig feed, demonstrating the crop's critical link to the growing poultry protein supply chain. As the European Union maintains its status as one of the world's largest livestock producers, the requirement for high-energy feed ingredients remains steadfast despite minor fluctuations in herd sizes. The efficiency of maize in converting to animal biomass makes it the preferred choice over other cereals for fattening pigs and poultry, a practice deeply entrenched in agricultural traditions across Germany and Belgium according to sources. Furthermore, the rebound in feed consumption forecasts for the 2025/26 marketing year indicates a resilient demand trajectory, even as the industry navigates economic pressures and shifting consumer preferences toward plant-based alternatives as per research. This sustained utilization ensures that maize retains its market dominance, as producers continuously seek reliable grain sources to maintain optimal livestock growth rates and milk yields. The structural dependency of the European animal agriculture sector on maize creates a stable demand floor that shields the market from severe volume contractions, even during periods of price volatility or reduced export opportunities.

Rising Bioethanol Production Fuels Industrial Utilization

Renewable Energy Mandates and Feedstock Shifts

The burgeoning bioethanol industry is also a significant driver for the Europe maize market. It increasingly relies on maize starch as a primary feedstock for renewable fuel production. Within the European Union, maize accounts for nearly half of the raw materials used in ethanol manufacturing, establishing it as the leading feedstock in the region's strategy to meet renewable energy targets according to 2023 statistics from ePURE, the European Renewable Ethanol Association. The demand for fuel ethanol continues to grow, propelled by the widespread adoption of E10 and E85 fuel blends in countries such as France, where government policies actively promote lower carbon emission transportation solutions as per reports from the French Ministry of Ecological Transition. In 2022, bioethanol production in the EU-27 reached around 5.6 million cubic meters, with maize serving as a key input alongside wheat and sugar beet to satisfy these volumetric requirements according to data published by Eurostat. The strategic shift toward decarbonization under the European Green Deal has intensified the competition for maize between the feed and fuel sectors, thereby bolstering overall market demand. This industrial application diversifies the demand base, ensuring that maize growers have alternative off-take channels beyond traditional agricultural uses. Consequently, the synergy between energy security mandates and agricultural output creates a robust market environment where maize serves as a dual-purpose commodity essential for both food security and climate action goals.

MARKET RESTRAINTS

Climate Change Induced Yield Volatility Limits Supply Stability

Environmental Stressors and Production Risks

The escalating impact of climate change is a major barrier for the Europe maize market. This introduces severe unpredictability into crop yields and production planning. Scientific projections indicate that climate change is expected to significantly lower maize yields across Europe by the middle of the century, primarily due to an increased frequency of extreme heat and drought during sensitive growing periods according to research from the Joint Research Centre. The severe drought conditions experienced in recent years serve as a clear example of this vulnerability, leading to major yield losses for summer crops like maize, soybean, and sunflower while causing widespread disruption to regional supply chains as documented by the Copernicus Emergency Management Service. Southern and eastern European regions are particularly vulnerable, where hot and dry weather conditions have already begun to severely affect maize productivity and threaten future harvest volumes according to sources. Higher temperatures accelerate plant development, shortening the grain-filling period and ultimately resulting in lower biomass accumulation and reduced grain weight. In the absence of expanded irrigation infrastructure, many European maize systems remain highly susceptible to water scarcity, which can drastically reduce grain output compared to fields with consistent water access according to agricultural field trials. This environmental instability forces farmers to contend with erratic production outcomes, making it difficult to guarantee consistent supply volumes for downstream industries. The recurring nature of these climatic shocks undermines investor confidence and complicates long-term contracting between growers and processors, thereby acting as a persistent brake on market expansion and reliability.

Stringent Regulatory Frameworks Constrain Agricultural Practices

Pesticide Reduction and GMO Restrictions

The rigorous regulatory environment governing pesticide use and genetically modified organism cultivation further impedes the expansion of the Europe maize market. The European Union’s long-term agricultural strategies aim for a substantial reduction in the use and risk of chemical pesticides, presenting a significant challenge to the traditional weed and pest management techniques used by maize growers according to European Commission policy frameworks. Glyphosate, the most widely used herbicide in European agriculture, faces intense scrutiny and restricted application conditions, limiting the tools available for effective weed control in maize fields as per research. While the approval for glyphosate has been extended for a multi-year period, its application is now governed by stricter regulations, including bans on specific uses like pre-harvest desiccation, which adds complexity to harvest operations and potentially raises production costs for farmers. Furthermore, the European Union maintains a highly restrictive stance on genetically modified maize varieties, preventing the adoption of drought-resistant or pest-resistant traits that could mitigate climate and biological risks. This regulatory rigidity forces producers to rely on less efficient or more expensive alternative crop protection methods, potentially lowering overall productivity and increasing the cost of production. The cumulative effect of these regulations is a compression of profit margins for farmers and a limitation on the technological advancements that could otherwise enhance yield potential. Consequently, the policy landscape acts as a structural barrier, slowing the modernization of maize cultivation and restraining the market's ability to respond flexibly to emerging agricultural challenges.

MARKET OPPORTUNITIES

Development of Drought-Resistant Varieties Enhances Resilience

Genetic Innovation and Climate Adaptation

Developing and adopting drought-resistant varieties to combat changing climates opens major possibilities for the growth of the Europe maize market. This strategic shift addresses immediate environmental challenges while ensuring long-term sustainability. Water scarcity is becoming a defining challenge for European agriculture. Therefore, breeding programs focused on enhancing water-use efficiency offer a viable pathway to stabilize yields in rainfed systems. Research indicates that the adoption of modern agricultural technologies and the deployment of drought-tolerant germplasm are key strategies to counteract the projected yield declines in Central and Eastern Europe according to studies. By integrating advanced genomic selection techniques, seed companies can deliver hybrids that maintain productivity under heat stress and limited precipitation, thereby securing supply chains against climate volatility. The potential to recover lost yield potential through genetic improvement represents a significant untapped value pool for the market, encouraging investment in research and development. Farmers who transition to these resilient varieties can mitigate the risks associated with extreme weather events, ensuring more consistent income streams and reducing the need for costly irrigation infrastructure. This technological evolution not only addresses immediate production constraints but also aligns with broader sustainability goals by optimizing resource utilization. Climate models predict increasing aridity in key growing regions. Consequently, the commercialization of these specialized seeds presents a transformative opportunity to redefine the productivity ceiling of the European maize sector.

Expansion of Sustainable Crop Rotation Systems Improves Soil Health

Agroecological Integration and Biodiversity

The transition toward sustainable maize-based cropping systems offers a substantial opportunity to enhance long-term soil health and operational efficiency across the region, which is expected to boost the expansion of the Europe maize market. Implementing diverse crop rotations that include maize can significantly improve soil structure, reduce pest pressures, and minimize the reliance on synthetic fertilizers and pesticides. Studies suggest that rotated maize systems in northern and south-western Europe demonstrate higher sustainability scores compared to continuous monoculture practices, offering a blueprint for wider adoption. These integrated systems support the European Union's objectives for biodiversity conservation and nutrient management, potentially unlocking access to green financing and premium market segments. By breaking pest and disease cycles, farmers can lower input costs and improve the overall resilience of their agricultural enterprises against biological threats. Furthermore, sustainable rotation practices contribute to carbon sequestration in soils, aligning maize production with the carbon farming initiatives gaining traction across the continent. The economic benefits of such systems are becoming increasingly evident, as they promise to deliver profitable and resource-saving outcomes for growers willing to adapt their methodologies. Embracing these agroecological approaches positions the maize market to thrive in a regulatory environment that increasingly rewards environmental stewardship, creating a competitive advantage for early adopters of sustainable intensification strategies.

MARKET CHALLENGES

Escalating Pest and Disease Pressures Threaten Crop Integrity

Biological Threats and Warming Climates

The increasing prevalence and severity of pests and diseases are slowing down the growth of the Europe maize market. These issues are exacerbated by warming temperatures and changing cultivation patterns. The European corn borer and other arthropod pests remain among the most destructive forces, causing significant economic losses and necessitating rigorous monitoring and control measures according to sources. Global warming is facilitating the northward expansion of pest populations and extending their active seasons, thereby exposing previously unaffected regions in north-western Europe to new biological threats as warned by climatologists. Fungal diseases also pose a critical risk, with warmer and humid conditions favoring the proliferation of pathogens that can devastate yields and compromise grain quality. The emergence of new quarantine pests adds another layer of complexity, requiring farmers to remain vigilant and adaptable in their protection strategies according to studies. Managing these biological adversaries without relying heavily on restricted chemical inputs demands sophisticated integrated pest management approaches, which can be knowledge-intensive and costly to implement. The constant evolutionary arms race between pests and control measures strains the resources of growers and threatens the stability of production volumes. The market must contend with the potential for sudden supply shocks and increased production costs as the intensity of biological challenges grows. This makes pest and disease management a pivotal hurdle for future growth.

Geopolitical Instability Disrupts Trade Flows and Input Costs

Global Tensions and Supply Chain Volatility

Geopolitical tensions and trade conflicts are serious obstacles to the Europe maize market. They do this by disrupting established supply chains and inflating input costs. The European Union's position as a significant importer and exporter of maize means that global instability can rapidly alter trade dynamics, leading to price volatility and supply uncertainties. Recent forecasts warn that trade conflicts could induce high price volatility in non-GMO crop outputs, affecting the competitiveness of European maize in both domestic and international markets according to research. Dependence on imported feed ingredients or the disruption of export routes to key partners can strain the balance between supply and demand, impacting the entire value chain from farm to fork. Additionally, geopolitical strife often leads to spikes in energy and fertilizer prices, which directly increase the cost of maize production and squeeze farmer margins. The uncertainty surrounding trade policies and international relations complicates long-term planning for market participants, forcing them to navigate a fragmented and unpredictable global landscape. This external volatility acts as a persistent drag on market confidence, hindering investment and expansion efforts within the sector. The global order remains fluid. Therefore, the Europe maize market must develop greater resilience to withstand external shocks and maintain stability amidst ongoing geopolitical turbulence.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 1.46% |

| Segments Covered | By End-User, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Alianz Global Groups Pty Ltd., Archer Daniels Midland Co., Limagrain, Corteva Agriscience, KWS Saat, Associated British Foods Plc, Balaji Exim, Bayer AG, Bunge Ltd., Cargill Inc., CGB Enterprises Inc., COFCO Corp., Exotic Exim, Fazaz Global Concepts LLC, Gombella Integrated Services Ltd., Greenfield Global Inc., Groupe Limagrain, Ingredion Inc., Ista International General Trading LLC, Louis Dreyfus Holding BV, Maeddy Impex Pvt. Ltd., Roquette Freres SA, Tate and Lyle PLC, Tereos Participations |

SEGMENTAL ANALYSIS

By End User Insights

In 2025, the Industrial segment was the largest segment in the Europe maize market and captured a 65.1% share. The leading position of this segment is credited to the sector's dual role as the primary consumer of maize for animal feed manufacturing and the leading user of maize starch for bioethanol and food processing applications. The sheer scale of the European livestock industry necessitates massive volumes of maize grain to sustain poultry, swine, and cattle populations, creating a structural demand that far outpaces direct human consumption or food service usage. Furthermore, the renewable energy mandates across the European Union have cemented the industrial sector's position by driving consistent demand for maize based biofuels. The main factor sustaining the industrial segment's dominance is the colossal requirement for compound feed to support the European meat and dairy industries. In countries like France and Germany, maize constitutes the backbone of energy dense rations for poultry and pigs, with the French poultry sector alone consuming a notable share of the national maize grain supply. The efficiency of maize in converting solar energy into digestible carbohydrates makes it irreplaceable for intensive farming operations that require rapid weight gain in livestock. As the European Union remains a global powerhouse in pork and poultry production, the industrial feed mills continue to absorb the vast majority of the harvest. This dependency ensures that even minor fluctuations in herd sizes result in significant volume shifts within the industrial segment, reinforcing its status as the market leader. The integration of maize into automated feed formulation systems further locks in this demand, as nutritional profiles for modern livestock breeds are optimized around maize availability. An additional driver of the industrial segment is the robust bioethanol industry, which relies heavily on maize starch to meet European renewable energy targets. Maize accounts for a considerable share of the total feedstock used in EU ethanol production, serving as a crucial input alongside wheat and sugar beet. The mandatory blending of biofuels into transportation fuels, such as the widespread E10 gasoline blend adopted across member states, creates a guaranteed offtake channel for millions of tonnes of maize annually. The strategic push toward decarbonization under the European Green Deal has intensified this demand, with projections indicating that bioethanol consumption will rise to support the transport sector's emission reduction goals. This industrial application provides a vital price floor and volume stability for maize growers, distinguishing the industrial segment from more volatile retail or food service sectors. The synergy between agricultural policy and energy security ensures that the industrial utilization of maize remains the central pillar of the European market structure.

The Retail segment is expected to exhibit a noteworthy CAGR of 4.9% during the forecast period due to shifting consumer preferences toward convenient, plant based, and gluten free food products derived from maize. The proliferation of maize-based snacks, ready to eat cereals, and alternative flour products in supermarket aisles reflects a broader trend of health consciousness and dietary diversification among European consumers. Unlike the mature and saturated industrial feed market, the retail space benefits from continuous product innovation and the introduction of premium maize derivatives that command higher value margins. A major factor that aids this segment is the surging consumer demand for gluten free products, where maize flour serves as a fundamental substitute for wheat. The prevalence of celiac disease and gluten sensitivity in Europe has driven a permanent shift in purchasing habits. Maize based pasta, bread mixes, and baking flours have become staple items in retail households, displacing traditional wheat products in millions of kitchens. The dietary transition is not limited to medical necessity but extends to lifestyle choices, as health conscious consumers perceive maize as a lighter and more natural grain option. Retailers have responded by expanding their shelf space dedicated to maize centric products, thereby accelerating the velocity of maize flow into the consumer direct channel. The versatility of maize flour in replicating textures of traditional baked goods without gluten ensures its sustained growth trajectory in the retail arena. A further reason for this growth is the explosive popularity of convenient maize based snack foods among younger demographics. The convenience factor aligns perfectly with modern urban lifestyles, where on the go consumption drives retail purchases of single serve and family pack maize snacks. Innovation in flavor profiles and the introduction of organic and non genetically modified organism labeled maize snacks have further stimulated retail turnover, appealing to discerning shoppers who prioritize clean label ingredients. The ability of manufacturers to introduce limited edition flavors and healthy variants, such as baked instead of fried maize chips, keeps the category dynamic and engaging for repeat purchases. This constant cycle of product refreshment and the deep penetration of maize snacks into discount and premium retail channels ensure that this segment maintains its status as the fastest growing avenue for maize consumption in Europe.

COUNTRY LEVEL ANALYSIS

France Maize Market Analysis

France dominated the European maize market in 2025. It is consistently securing the top position in both production volume and export capacity, thereby dictating the regional supply dynamics. The nation's agricultural landscape is uniquely suited for maize cultivation, benefiting from favorable climatic conditions in the southwest and extensive arable land dedicated to grain crops. France typically accounts for a notable share of the total maize production within the European Union, producing upwards of millions of tonnes annually depending on seasonal weather patterns. The country's dominance is not merely a function of volume but also of technological sophistication, with French farmers employing advanced breeding techniques and precision agriculture to maximize yields per hectare. A key driver of this status is the robust domestic demand from a large livestock sector, particularly the poultry and duck industries which are integral to the national gastronomy and export economy. Additionally, France serves as the primary supplier of maize to neighboring deficit regions, exporting millions of tonnes to Spain and other Mediterranean nations. The government's strong support for agricultural research and the presence of major seed companies further reinforce France's competitive edge. Despite facing periodic challenges from drought, the resilience of the French farming community and their ability to adapt crop varieties ensure that the nation maintains its stranglehold on the European maize supply chain, making it the critical anchor for regional food security.

Romania Maize Market Analysis

Romania followed closely behind in the Europe maize market in 2025 because of its vast arable land potential and its role as a major exporter of raw maize grain to global markets. The country frequently alternates with France for the top spot in total production volume, often harvesting substantial tonnes, which represents a portion of the European Union's total output. Romania's market status is characterized by a heavy reliance on rainfed agriculture, which makes its yields highly susceptible to climatic variability, yet its sheer scale of cultivation ensures it remains a powerhouse. The driving force behind Romania's prominence is the continuous expansion of planted areas, as farmers capitalize on high global prices and the suitability of the Danube plains for cereal cultivation. Unlike Western European nations where land is fragmented, Romania offers large contiguous fields that facilitate mechanized farming and economies of scale. A significant portion of Romanian maize is destined for export, feeding the demand in North Africa and the Middle East, which integrates the country deeply into global trade flows. The domestic livestock sector is also growing, gradually absorbing more maize for internal feed production, but the export orientation remains the defining feature of its market behavior. Investments in irrigation infrastructure, though still developing, promise to stabilize yields and unlock even greater production potential, solidifying Romania's status as the breadbasket of Eastern Europe and a pivotal player in the continental maize balance.

Germany Maize Market Analysis

Germany is another key player in the Europe maize market due to its sophisticated domestic consumption and advanced industrial processing capabilities. While its production volumes are lower than France or Romania, Germany's market status is defined by its role as a net importer and a central hub for high value maize utilization. The country possesses one of the most intensive livestock sectors in Europe, particularly in pig and poultry farming, which creates an insatiable demand for high quality feed maize that often exceeds domestic supply. This structural deficit drives significant imports from France and Ukraine, making Germany a critical demand center that stabilizes prices for producers in neighboring regions. Furthermore, Germany is a leader in the bioenergy sector, with a vast network of biogas plants that utilize maize silage as a primary feedstock, adding a unique dimension to its maize consumption profile. The driving factors here include strict environmental regulations that promote renewable energy and a highly organized agricultural cooperative system that ensures efficient supply chain logistics. German farmers focus on optimizing yield stability and quality rather than just volume, employing cutting edge agronomic practices to maximize output on limited land. The integration of maize into the circular economy through biogas production underscores Germany's innovative approach, ensuring that the crop remains central to both its food security and energy transition strategies.

Hungary Maize Market Analysis

Hungary grew steadily in the European maize market. It is renowned for its high yield efficiency and its strategic importance as a transit corridor for grain exports from Eastern Europe. The country consistently produces between 4 and 5 million tonnes of maize, achieving some of the highest yields per hectare in the continent due to its favorable soil conditions and focused agronomic expertise according to the Hungarian Central Statistical Office. Hungary's market status is bolstered by its geographical location along the Danube River, which facilitates cost effective barge transport of maize to downstream markets in the Balkans and beyond. The driving force behind Hungary's strong performance is the deep cultural and economic embedding of maize in its agricultural tradition, supported by a dense network of local storage and trading facilities. The nation serves as a critical supplier for the Central European livestock industry, with a significant portion of its harvest dedicated to regional feed mills. Additionally, Hungary has developed a robust seed production sector, exporting high quality hybrid seeds to various parts of Europe and the world, which adds value beyond simple grain sales. The government's proactive stance on water management and flood control in the Great Hungarian Plain further mitigates climate risks, allowing for more predictable production cycles. This combination of logistical advantage, agronomic excellence, and value added seed production ensures Hungary remains a resilient and influential actor in the European maize landscape.

Italy Maize Market Analysis

Italy is predicted to expand notably in the Europe maize market during the forecast period due to its unique dual demand structure that balances significant livestock feed requirements with a specialized food processing sector. Producing millions of tonnes annually, Italy operates as a net importer to satisfy its total consumption needs, which are driven by a massive dairy industry and a traditional food culture reliant on maize products. The market status of Italy is heavily influenced by the demand for white maize varieties, which are essential for producing polenta and other traditional culinary staples, creating a niche market segment that commands premium prices. The driving factors for Italy's maize market include the intense concentration of dairy farming in the Po Valley, which requires high energy feed rations to sustain milk production for famous cheeses like Parmigiano Reggiano. Furthermore, the Italian poultry sector is a voracious consumer of maize, relying on it as the primary energy source for broiler and layer feeds. The country's dependence on imports from France and Eastern Europe highlights its role as a demand sink that supports the export economies of its neighbors. Recent trends show a growing interest in sustainable and locally sourced maize, prompting initiatives to increase domestic production efficiency and reduce the carbon footprint of feed supply chains. This blend of culinary tradition and industrial dairy demand makes Italy a distinctive and vital component of the overall European maize ecosystem.

COMPETITIVE LANDSCAPE

The competition in the Europe maize market is characterized by a high degree of innovation and strategic maneuvering among established seed companies and agricultural cooperatives. Major players compete intensely on the quality and performance of their hybrid varieties, striving to deliver superior yields and resilience against abiotic stresses like drought and heat. The landscape features a mix of large multinational corporations and strong regional cooperatives that leverage deep local knowledge to serve specific agronomic needs. Competitive dynamics are further shaped by the regulatory environment, which pushes companies to develop non genetically modified solutions that comply with strict European Union standards. Firms differentiate themselves through digital service offerings that enhance farmer decision making and operational efficiency. The race to secure intellectual property rights for advanced traits drives significant investment in research and development activities. Additionally, competition extends to supply chain reliability, where companies strive to ensure consistent seed availability and technical support for growers. This vibrant competitive ecosystem fosters continuous advancement in maize technology and sustainability practices across the continent.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe maize market are

- Alianz Global Groups Pty Ltd.

- Archer Daniels Midland Co.

- Limagrain

- Corteva Agriscience

- KWS Saat

- Associated British Foods Plc

- Balaji Exim

- Bayer AG

- Bunge Ltd.

- Cargill Inc.

- CGB Enterprises Inc.

- COFCO Corp.

- Exotic Exim

- Fazaz Global Concepts LLC

- Gombella Integrated Services Ltd.

- Greenfield Global Inc.

- Groupe Limagrain

- Ingredion Inc.

- Ista International General Trading LLC

- Louis Dreyfus Holding BV

- Maeddy Impex Pvt. Ltd.

- Roquette Freres SA

- Tate and Lyle PLC

- Tereos Participations

Top Players In The Market

- Limagrain stands as a premier international cooperative and a leading seed producer deeply embedded in the European maize landscape. The company focuses extensively on developing high yielding and climate resilient maize hybrids tailored specifically for European agronomic conditions. Limagrain contributes significantly to the global market by exporting its advanced genetic material to numerous countries while maintaining a strong domestic footprint in France and surrounding regions. Recent actions to strengthen its position include heavy investment in digital breeding technologies and the launch of new hybrid varieties designed to withstand drought stress and reduce pesticide dependency. The cooperative actively collaborates with farmers to promote sustainable agricultural practices and optimize crop performance. By prioritizing research and development in genomic selection, Limagrain ensures its portfolio remains at the forefront of innovation. This strategic focus allows the company to address the evolving needs of European growers facing climate change challenges while securing its role as a vital partner in global food security initiatives.

- KWS Saat operates as a major German seed company with a profound influence on the European maize sector through its specialized breeding programs. The firm is renowned for delivering high performance maize varieties that offer superior yield stability and disease resistance across diverse European climates. KWS contributes to the global market by leveraging its extensive international network to distribute its proprietary genetics worldwide while anchoring its operations in Central Europe. To strengthen its market position recently, KWS has accelerated its use of gene editing technologies and expanded its digital farming solutions to assist growers in precision agriculture. The company has also formed strategic partnerships with biotech firms to enhance trait development for abiotic stress tolerance. These initiatives enable KWS to provide tailored solutions that maximize farmer profitability and resource efficiency. KWS Saat reinforces its commitment to advancing maize cultivation and supporting the agricultural value chain throughout Europe and beyond. This is achieved by continuously innovating its product pipeline and focusing on sustainability goals.

- Corteva Agriscience functions as a global agriculture giant with a substantial presence in the European maize market through its comprehensive seed and crop protection portfolios. The company delivers advanced maize hybrids and integrated pest management solutions that help European farmers optimize productivity and protect crop health. Corteva contributes to the global market by deploying its vast research capabilities to introduce cutting edge traits and digital tools that enhance farming outcomes worldwide. Recent actions to bolster its position include the introduction of new herbicide tolerant maize varieties and the expansion of its Granular digital platform to support data driven decision making for growers. The firm actively invests in sustainable agriculture initiatives and collaborates with stakeholders to promote regenerative farming practices. By combining biological advancements with digital innovation, Corteva aims to solve complex agricultural challenges and improve supply chain resilience. This holistic approach ensures that Corteva remains a key driver of progress in the European maize sector while addressing global food system demands.

Top Strategies Used By The Key Market Participants

Key players in the Europe maize market primarily employ strategies focused on intensive research and development to create climate resilient hybrid varieties. Companies invest heavily in genomic selection and gene editing technologies to accelerate breeding cycles and enhance trait performance. Another major strategy involves the integration of digital agriculture tools that provide farmers with precise data for optimizing planting and input usage. Strategic partnerships and collaborations with biotechnology firms allow these entities to access novel traits and expand their technological capabilities. Market participants also focus on sustainability initiatives by promoting regenerative farming practices and reducing the environmental footprint of maize cultivation. Expansion into emerging markets within Eastern Europe helps companies diversify their revenue streams and capture growth opportunities. Additionally, firms engage in vertical integration by strengthening relationships with downstream processors and feed manufacturers to secure demand. These combined approaches enable key players to maintain competitive advantages and adapt to the dynamic regulatory and climatic landscape of the European agricultural sector.

MARKET SEGMENTATION

This research report on the Europe maize market is segmented and sub-segmented into the following categories.

By End-user

- Industrial

- Retail

- Food service

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

How is maize used across agricultural and industrial sectors in Europe?

Maize is widely used as animal feed, food ingredient, and raw material for biofuel and industrial products.

What factors are driving the demand for maize in Europe?

Growing livestock production and demand for feed grains are key drivers of maize consumption.

Which industries rely heavily on maize in the European market?

Livestock feed, food processing, and biofuel industries are major consumers of maize.

Why is maize considered an important crop in European agriculture?

It offers high yield potential and versatility across multiple applications.

How does maize contribute to the livestock sector in Europe?

It serves as a primary energy-rich feed ingredient for poultry, cattle, and swine.

What challenges affect maize production in Europe?

Weather variability, pest pressures, and fluctuating input costs can impact production levels.

Which countries are major producers of maize in Europe?

France, Romania, Hungary, and Italy are key maize-producing countries in the region.

How do trade dynamics influence the Europe maize market?

Imports and exports help balance supply and demand across different countries.

How is maize used in food applications in Europe?

It is processed into products such as cornmeal, starch, and sweeteners.

What future trend is expected in the Europe maize market?

Increasing demand for animal feed and bio-based products is expected to support market growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com