Europe Mobile Display Market Size, Share, Trends & Growth Forecast Report By Type, By Display Technology, and By Country (Germany, United Kingdom, France, Italy, Spain & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Mobile Display Market Size

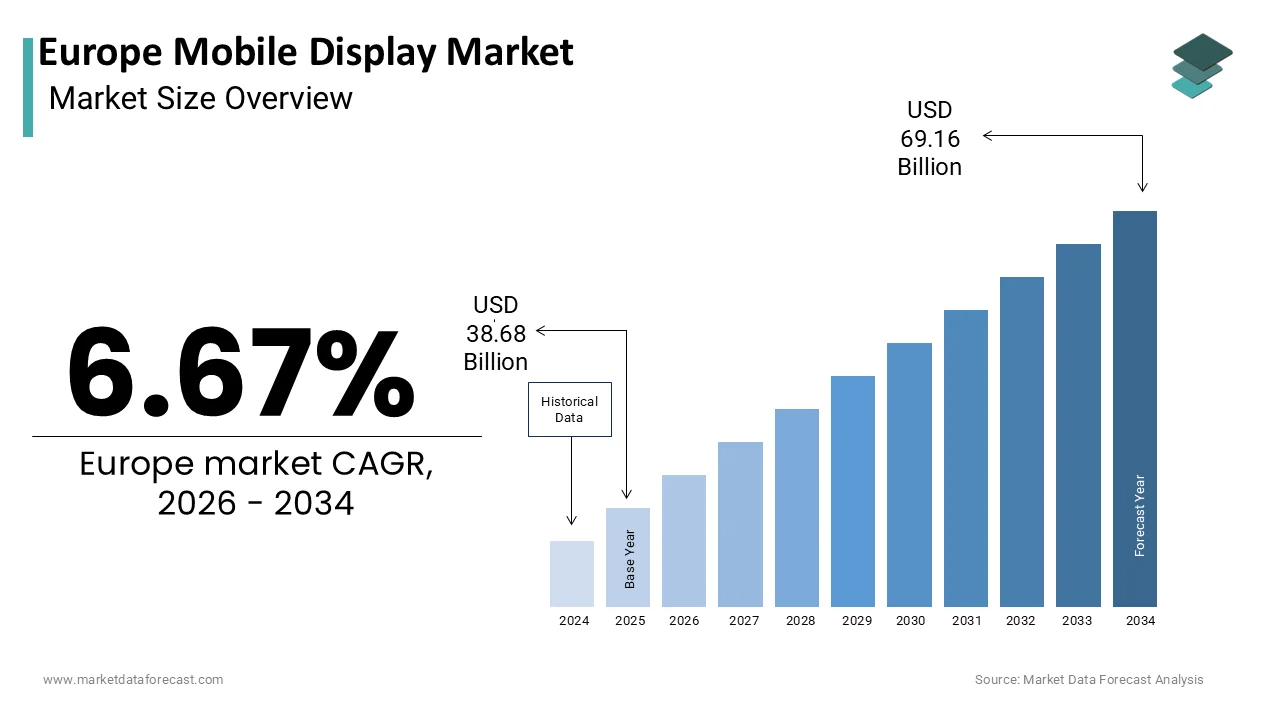

The Europe mobile display market was valued at USD 38.68 billion in 2025, is estimated to reach USD 41.26 billion in 2026, and is projected to reach USD 69.16 billion by 2034, growing at a CAGR of 6.67% from 2026 to 2034.

A mobile display is the visual output screen of a handheld device, such as a smartphone or tablet. This market is currently defined by a rapid transition from standard liquid crystal displays to advanced organic light-emitting diode and micro light-emitting diode panels that offer superior contrast, energy efficiency, and form factor flexibility. The European landscape is uniquely shaped by stringent environmental regulations and a high consumer emphasis on data privacy and digital well-being, which influence display specifications such as blue light reduction and power consumption. According to Eurostat, 91 percent of individuals in the European Union aged 16 to 74 used the internet in 2023, with 89 percent of urban residents specifically using a mobile phone or smartphone to access it, creating a massive installed base that drives continuous demand for replacement screens and upgraded visual experiences. Furthermore, the European Commission’s Delegated Regulation (EU) 2023/1669 (supplementing the Energy Labelling Regulation) now mandates repairability scores for smartphones and tablets alongside energy efficiency labels, effective June 2025. This, combined with the broader Ecodesign for Sustainable Products Regulation (ESPR) framework, compels manufacturers to adopt display technologies that are durable, repairable, and recyclable. Data from the International Telecommunication Union (ITU) indicates that mobile broadband subscriptions in Europe reached approximately 111 per 100 inhabitants in 2024 (totaling over 770 million subscriptions), fueling the need for high-resolution displays capable of rendering complex multimedia content and augmented reality applications. This convergence of ubiquitous connectivity, regulatory pressure for sustainability, and the demand for immersive visual interfaces positions the region as a critical market for next-generation mobile display innovations.

MARKET DRIVERS

Surging Demand for High Refresh Rate and Foldable Form Factors

Escalating consumer expectations for premium visual experiences are the main reasons for the growth of the Europe mobile display market. These expectations center on high refresh rates and novel form factors like foldable and rollable screens. European consumers, particularly in key markets like Germany and the United Kingdom, increasingly view high refresh rate displays exceeding 120 hertz as a standard requirement for fluid gaming and seamless multitasking, pushing original equipment manufacturers to integrate Low Temperature Polycrystalline Oxide backplanes. According to the International Data Corporation, there is a strong "premiumization" trend in Western Europe, where consumers are increasingly opting for high-end smartphones that feature advanced display technologies, including higher refresh rates and improved visual fluidity. Simultaneously, the emergence of foldable devices has opened a new segment where flexible organic light-emitting diode displays are indispensable, allowing for tablet-sized screens in pocketable formats. Research reveals that the European gaming industry continues to grow, with mobile and console gaming acting as the primary revenue drivers and pushing consumers toward hardware that can support increasingly demanding digital experiences. This demand for visual fluidity and physical versatility forces supply chains to prioritize advanced manufacturing processes capable of producing thin, bendable, and high-performance panels, thereby expanding the market value and technological complexity of mobile displays across the region.

Expansion of Mobile Gaming and Augmented Reality Applications

The explosive growth of the mobile gaming industry and the increasing integration of augmented reality applications further boost the expansion of the Europe mobile display market. These trends place immense demands on display resolution, peak brightness, and color gamut. Europe hosts a vibrant gaming community, with millions of users engaging in graphically intensive titles that require displays capable of rendering high dynamic range content without motion blur or color distortion. The annual report from Video Games Europe confirms that the European gaming industry continues to grow, with mobile and console gaming acting as the primary revenue drivers and pushing consumers toward hardware that can support increasingly demanding digital experiences. Furthermore, the proliferation of augmented reality tools for navigation, retail, and education relies on displays with exceptional pixel density and low latency to overlay digital information seamlessly onto the real world. The European Augmented Reality market indicates that widespread smartphone penetration and better mobile hardware are making immersive applications more accessible, leading manufacturers to incorporate higher-peak-brightness displays to ensure clear visibility in various lighting conditions. This synergy between content consumption habits and hardware capabilities ensures a sustained push for higher specification displays, making visual performance a key differentiator in the competitive European smartphone landscape.

MARKET RESTRAINTS

Stringent Environmental Regulations and Right to Repair Mandates

The increasingly stringent regulatory framework imposed by the European Union restricts the growth of the Europe mobile display market. This framework, specifically the Ecodesign for Sustainable Products Regulation and the Right to Repair directive, mandates higher recyclability and easier disassembly of electronic components. These regulations require manufacturers to design devices where displays can be replaced without destroying the unit, often conflicting with the industry trend towards glued, edge-to-edge, and curved screen designs that maximize aesthetics but hinder repairability. New European Commission regulations require manufacturers to provide long-term software support and maintain a supply of spare parts for several years, a mandate that encourages companies to develop more modular and durable display assemblies to simplify repair and maintenance. Data from the European Environmental Bureau emphasizes that the complexity of recycling organic light-emitting diode panels remains high due to the mixture of rare earth materials and plastics, leading to potential penalties for non-compliant designs. Manufacturers must now balance the demand for sleek, immersive displays with the legal necessity of creating bulky, easily separable components, slowing down the introduction of cutting-edge form factors. This regulatory pressure creates a compliance burden that acts as a brake on rapid innovation and increases the time to market for new display technologies.

Supply Chain Vulnerability for Critical Raw Materials

The region's heavy dependence on imported critical raw materials essential for mobile display manufacturing impedes the expansion of the Europe mobile display market. These materials, such as indium, gallium, and rare earth phosphors, are predominantly sourced from outside the continent. The geopolitical concentration of these supply chains exposes European original equipment manufacturers to export restrictions, trade disputes, and logistical bottlenecks that can abruptly disrupt production schedules and inflate costs. Strategic assessments by European critical raw material agencies highlight the region's total reliance on imports for key materials used in touchscreen layers, underscoring a significant vulnerability to global supply shocks and trade fluctuations. Multiple studies indicate that while the global supply of display drivers and glass substrates has stabilized since the major shortages, specific allocation issues still occasionally affect production timelines for high-end mobile hardware. This scarcity forces manufacturers to secure long-term contracts at premium prices or face production delays, ultimately passing costs onto consumers and dampening demand for mid-range devices. The lack of domestic refining and processing capabilities for these materials means that even with local assembly, the upstream supply chain remains a fragile link that constrains the scalability and cost competitiveness of the European mobile display market.

MARKET OPPORTUNITIES

Adoption of Micro LED and Quantum Dot Enhancement Films

The commercialization of Micro LED technology and the integration of quantum dot enhancement films offer strong potential for the Europe mobile display market. These technologies promise to overcome the limitations of current organic light-emitting diode panels regarding burn-in and lifespan. Micro LED displays offer self-emissive pixels with inorganic materials that provide superior brightness, energy efficiency, and durability, making them ideal for always-on displays and outdoor visibility in varying European weather conditions. According to the European Patent Office, patent filings related to electrical machinery, apparatus, and energy (driven largely by battery innovation) surged significantly in 2023, signaling strong industrial momentum in the clean energy and digital transition sectors. These technologies enable displays that consume significantly less power while delivering wider color gamuts, aligning perfectly with the EU's strict energy efficiency targets. A study projects that the penetration of OLED displays (specifically rigid and flexible OLEDs) in mid-range smartphones in Europe will continue to increase, bridging the gap between cost and performance as they replace traditional LCDs. Improved manufacturing yields for Micro LED create the potential to integrate these panels into flagship devices, opening a high-value segment that could redefine the premium mobile experience. These panels offer European consumers screens that are brighter, more efficient, and more durable than those currently available.

Integration of Under-Display Sensors and Biometric Technologies

The rapid advancement of under-display sensor technology provides a substantial opportunity for the European mobile display market. It enables truly bezel-less designs and integrates biometric security directly into the screen area. Consumers and enterprises in Europe increasingly demand devices with maximum screen-to-body ratios for immersive media consumption and robust security features like under-display fingerprint scanning for mobile banking and identity verification. Research emphasizes that mobile fraud and security threats in Europe remain a critical challenge, driving a surge in demand for secure, hardware-based biometric authentication methods embedded within the display itself. The development of transparent pixel architectures allows cameras and sensors to sit beneath the screen without compromising image quality, eliminating the need for notches or punch holes. Sources indicate that the adoption of under-display fingerprint sensors in smartphones continues to expand, becoming a standard feature even in mid-tier devices as manufacturers move away from capacitive sensors. This trend towards seamless integration not only enhances aesthetic appeal but also improves device durability by removing mechanical buttons and external sensor housing. Technology is maturing to support under-display front-facing cameras. This development will drive a new wave of premium device upgrades across the region by enabling fully uninterrupted visual surfaces.

MARKET CHALLENGES

Complexity of Recycling Multi-Layered Display Architectures

The extreme technical difficulty associated with recycling modern multi-layered display architectures negatively impacts the growth of the Europe mobile display market. This issue conflicts with the European Union's ambitious circular economy and zero-waste targets. Contemporary mobile displays consist of complex stacks of chemically strengthened glass, polarizers, organic emissive layers, touch sensors, and adhesive bonding agents that are fused, making separation and material recovery economically unviable with current technologies. According to the European Electronics Recyclers Association (EERA) and data from global e-waste monitors, the recovery rate for valuable rare earth elements and indium from discarded smartphone screens is currently negligible (often cited as near zero), with the vast majority being lost during standard recycling processes due to the technical complexity and economic challenges of extracting widely dispersed materials. The new Ecodesign regulations mandate higher recycling rates, yet the industry lacks scalable industrial processes to efficiently separate these bonded layers without damaging the materials. Research by the Joint Research Centre (JRC) of the European Commission highlights that the recovery of critical raw materials from modern displays, such as organic light-emitting diodes, is significantly hindered by thermodynamic limits and economic barriers, meaning these materials are frequently lost in current recycling infrastructures rather than being effectively recovered for reuse. The inability to effectively close the loop on display materials remains a persistent regulatory and reputational risk for manufacturers in the European market. This challenge will persist until breakthroughs in chemical recycling or design for disassembly are achieved.

Balancing Energy Efficiency with High Performance Visuals

Reconciling the consumer desire for premium displays (high resolution, brightness, and refresh rate) with strict battery life requirements is a major challenge in the Europe mobile display market. This situation is driven by both user demand and regulatory mandates. Rising display resolutions (4K) and refresh rates (>144Hz) cause power consumption to increase exponentially, straining battery capacity and generating performance-throttling heat. Such high energy usage contradicts the European Union's Ecodesign directives, which aim to reduce overall device energy consumption. According to the European Commission's Joint Research Centre, the display unit (along with integrated circuits) is identified as one of the most significant contributors to a smartphone's embodied carbon footprint and resource depletion potential, particularly during the manufacturing phase, making it a critical priority for material efficiency and circular economy strategies. However, reducing brightness or lowering refresh rates to save power often compromises the user experience, leading to consumer dissatisfaction. Display industry market analysis indicates that despite advancements in power-saving technologies like Low-Temperature Polycrystalline Oxide (LTPO), the net power consumption of flagship mobile displays has continued to increase in recent years, driven by the industry's pursuit of higher peak brightness and superior refresh rates, which offset the efficiency gains. Engineers face the difficult task of developing new materials and driving schemes that can deliver cinema-grade visuals while adhering to tightening power budgets, a balancing act that slows down the deployment of next-generation display features and increases research and development costs.

SEGMENTAL ANALYSIS

By Type Insights

In 2025, the capacitive display screens segment led the Europe mobile display market and captured a substantial share. Superior touch sensitivity, multi-touch capabilities, and optical clarity drive the dominance of this segment. These features have become the non-negotiable standard for modern smartphones and tablets across the continent. A main reason for the absolute dominance of capacitive technology is its ability to support precise multi-touch gestures and offer a glass-like surface that provides an intuitive and fluid user experience essential for modern mobile operating systems. Unlike resistive screens that require pressure and typically support only single-point input, capacitive screens detect the electrical charge of the human finger, allowing for complex interactions like pinch-to-zoom, swipe navigation, and rapid typing that define the European consumer expectation for smartphones. According to sources, a large share of smartphones shipped in Western Europe in 2023 featured capacitive touch interfaces, as users reject the laggy and imprecise nature of older technologies. Furthermore, the integration of projective capacitive technology allows for operation with light touches, reducing finger fatigue during extended use. This alignment with user behavior and software requirements ensures capacitive screens remain the undisputed leader. Following this, the segment is backed by its superior optical transmission and compatibility with durable chemically strengthened glass, which are vital for the premium aesthetics and longevity demanded by the European market. Capacitive sensors can be embedded beneath a single layer of thick glass, eliminating the air gaps found in resistive screens that cause light refraction and reduce brightness, thereby delivering the vibrant colors and deep blacks required for high-definition content consumption. Additionally, the robust glass surface of capacitive screens resists scratches and wear far better than the flexible plastic layers of resistive screens, aligning with the European Commission's push for longer device lifespans under the Right to Repair framework. This combination of visual excellence and physical resilience cements capacitive technology as the only viable option for modern mobile devices.

The Resistive Display Screen segment is likely to experience the fastest CAGR of 2.1% during the forecast period. This growth is fueled by persistent demand in ruggedized industrial handhelds, legacy healthcare devices, and cost-sensitive specialized applications where glove operation and stylus precision are paramount. The modest yet steady growth of the resistive segment is primarily sustained by its unique ability to function reliably in harsh industrial environments where operators must wear thick protective gloves or use non-conductive styluses, scenarios where capacitive screens fail. In sectors such as logistics, manufacturing, and chemical processing across Europe, workers rely on rugged mobile computers and scanners that require pressure-based input to register commands accurately without accidental touches from clothing or equipment. Furthermore, in hazardous areas with explosive risks, resistive screens allow for input using specialized insulated tools that do not generate static electricity, a safety feature that capacitive screens cannot easily replicate. As long as industrial automation and field services require reliable input regardless of handwear or environmental conditions, resistive technology will maintain a dedicated, albeit small, growth trajectory. Also helping this segment is its significant cost advantage and compatibility with legacy software systems in specialized medical and point-of-sale terminals that do not require multi-touch functionality. Many hospitals and clinics in Europe still operate older diagnostic equipment and patient monitoring systems designed around single-point pressure input, and upgrading these entire systems is often prohibitively expensive compared to replacing just the interface components. Additionally, in the budget segment of point-of-sale terminals for small retailers, resistive screens offer a durable and affordable solution that withstands constant poking and prodding without the fragility of glass capacitive panels. This economic reality ensures that for specific, function-over-form applications where advanced gestures are unnecessary, resistive screens continue to see incremental adoption and replacement, driving their limited but positive growth rate.

By Display Technology Insights

The In-Plane Switching Liquid Crystal Display (IPS-LCD) technology segment held the majority share of 52.1% of the Europe mobile display market in 2025. This prominence of the segment is credited to its optimal balance of color accuracy, wide viewing angles, and cost-effectiveness, making it the preferred choice for mid-range smartphones and tablets that constitute the bulk of sales volume in the region. Moreover, the preeminence of IPS-LCD technology is fundamentally fuelled by its ability to deliver excellent color reproduction and wide viewing angles at a significantly lower manufacturing cost compared to organic light-emitting diode alternatives, perfectly suiting the price-sensitive mass market in Europe. While flagship devices increasingly adopt OLED, the majority of Europeans purchase mid-range smartphones priced between 200 and 400 euros, where IPS-LCD offers the best value proposition without compromising visual quality. According to studies, mid-range devices accounted for a notable share of all smartphone shipments in Europe in 2023, with nearly all utilizing IPS-LCD panels to maintain competitive pricing while offering 1080p resolution and accurate sRGB color gamuts. The European Consumer Organisation highlights that battery life and screen readability are top priorities for this demographic, and IPS-LCD panels generally consume less power when displaying white backgrounds common in web browsing and productivity apps compared to early-generation OLEDs. This economic efficiency ensures that IPS-LCD remains the workhorse technology powering the digital lives of the majority of European consumers. This segment is also built up by its superior longevity and immunity to screen burn-in, a critical consideration for users who keep their devices for extended periods or use them for static content like navigation and enterprise applications. Unlike OLED panels, where organic pixels degrade over time,e leading to permanent image retention, IPS-LCD uses inorganic liquid crystals that maintain consistent brightness and color uniformity throughout the device's lifespan, aligning with the European trend of longer device retention cycles. Furthermore, the stability of IPS-LCD performance under high brightness levels makes it ideal for outdoor usage in various European climates without the accelerated degradation seen in organic materials. This reliability ensures that IPS-LCD remains the trusted choice for both consumers and businesses prioritizing long-term asset value.

The AMOLED segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 14.8% from 2026 to 2034 due to the rapid trickle-down of OLED technology from flagship to mid-range devices, the surging demand for foldable smartphones, and the superior energy efficiency of always-on display features. A key reason for the rapid expansion of AMOLED technology is its aggressive migration from premium flagship models to the highly voluminous mid-range smartphone segment, driven by falling production costs and intense competition among brands to offer "premium" features at accessible prices. European consumers are increasingly demanding deep blacks, infinite contrast ratios, and vibrant colors previously exclusive to high-end devices, forcing manufacturers to equip sub-400 euro phones with AMOLED panels to remain competitive. The ability of AMOLED to enable slim bezels and under-display fingerprint sensors adds perceived value that appeals to style-conscious European buyers. As major brands like Samsung, Xiaomi, and Realme saturate the mid-market with AMOLED-equipped devices, the volume growth for this technology is outpacing all other display types, reshaping the overall market landscape. A further key driver for the robust growth of the AMOLED segment is its status as the only viable display technology for the burgeoning foldable and rollable smartphone market, which is gaining significant traction in Europe. The organic nature of AMOLED materials allows them to be fabricated on flexible plastic substrates that can bend and fold thousands of times without breaking, a physical impossibility for rigid LCD structures. According to research, foldable smartphone shipments in Europe increased significantly, with every single unit utilizing flexible AMOLED technology to enable its form factor. Furthermore, AMOLED's pixel-level dimming capability enables "Always-On Display" features that show time and notifications with minimal power consumption, a feature highly valued by European users for convenience and aesthetics. Foldable devices are becoming more durable and affordable. This reliance on AMOLED technology will drive disproportionate growth for this segment.

COUNTRY LEVEL ANALYSIS

Germany Mobile Display Market Analysis

Germany dominated the Europe mobile display market and accounted for a 24.2% share in 2025. The dominance of the German market is driven by its status as Europe's largest economy, hosting a massive consumer base with high purchasing power, a strong automotive sector integrating mobile-like displays, and a robust industrial demand for ruggedized mobile devices. Germany's dominance is also propelled by its sophisticated consumer electronics market, where users prioritize high-quality displays for productivity and entertainment, driving strong sales of premium smartphones and tablets featuring advanced AMOLED and IPS-LCD technologies. The country is home to major automotive manufacturers who are increasingly adopting mobile-grade display technologies for in-vehicle infotainment systems, creating a synergistic demand for high-resolution, durable panels. Furthermore, Germany's strong industrial base drives significant demand for rugged mobile computers with specialized displays for logistics and manufacturing, supporting diverse display types,s including resistive screens. The presence of key research institutions focusing on material science and displaying innovation further strengthens the market. This combination of affluent consumer demand, industrial application, and automotive cross-pollination ensures Germany remains the primary engine of the European mobile display market.

United Kingdom Mobile Display Market Analysis

The United Kingdom was the second largest country in the Europe mobile display market and captured a share of 18.3% in 2025 because of its early adoption of flagship technologies, a vibrant mobile gaming culture, and a strong retail sector that promotes premium devices with advanced display features. The UK's strong market standing is largely attributable to its consumers' willingness to invest in high-end smartphones with cutting-edge display technologies such as high refresh rate AMOLED and mini-LED, fueled by a deep engagement with mobile gaming and streaming services. The country hosts a thriving games industry that pushes hardware manufacturers to supply devices with superior color accuracy and motion handling to support graphically intensive titles. Additionally, the UK's competitive telecommunications market frequently bundles the latest flagship devices with aggressive contract plans, accelerating the turnover rate and adoption of new display technologies among the general population. The strong presence of major tech retailers and the influence of London as a trendsetting hub further amplify the demand for visually stunning mobile experiences. This convergence of gaming culture, retail dynamics, and early adoption behavior positions the UK as a critical and dynamic market for mobile displays.

France Mobile Display Market Analysis

France plays a key role in the Europe mobile display market owing to its large population, government initiatives promoting digital inclusion, and a growing emphasis on sustainable and repairable devices influencing display choices. France's market strength is supported by its substantial consumer base and unique regulatory environment that encourages the purchase of refurbished and repairable smartphones, impacting the types of displays in circulation. The French Repairability Index has forced manufacturers to design devices with easier-to-replace screens, influencing the supply chain towards modular display assemblies that comply with local laws. According to research, sales of refurbished smartphones increased in 2023, creating a secondary market demand for durable and cost-effective display panels like IPS-LCD. Simultaneously, the French government's push for digital sovereignty and connectivity has expanded mobile access in rural areas, driving volume sales of mid-range devices equipped with reliable LCD technology. The country's strong cultural appreciation for design and multimedia also sustains demand for high-quality screens in flagship models. This blend of regulatory influence, digital inclusion efforts, and diverse consumer preferences ensures France remains a pivotal market for mobile display technologies in Western Europe.

Italy Mobile Display Market Analysis

Italy witnessed a consistent growth in the European market due to a strong preference for stylish and camera-centric smartphones, a booming mobile commerce sector, and increasing adoption of 5G devices requiring advanced display capabilities. In addition, Italy's significant market presence is driven by consumers who prioritize aesthetic design and multimedia capabilities, leading to strong sales of smartphones with vibrant AMOLED displays that enhance photo viewing and social media engagement. The country has seen a surge in mobile commerce, with Italians increasingly using smartphones for shopping and banking, necessitating secure and clear displays for transactions and biometric authentication. The rapid rollout of 5G networks across major Italian cities has also accelerated the upgrade cycle to newer devices equipped with high-efficiency displays to manage data speeds without draining batteries. Furthermore, the popularity of social media platforms like Instagram and TikTok among Italian youth fuels the demand for high-resolution front and rear-facing display experiences. This focus on lifestyle, commerce, and connectivity keeps Italy a key growth market for mobile displays in Southern Europe.

Spain Mobile Display Market Analysis

Spain is likely to expand notably in the European market during the forecast period owing to its high smartphone penetration rate, a tourism-driven economy requiring multilingual and robust mobile interfaces, and a competitive telecom sector driving device refreshes. Also, Spain's market trajectory is influenced by its status as a major tourist destination, which drives demand for durable, high-brightness mobile displays capable of functioning clearly in bright sunlight for navigation and translation apps used by millions of visitors annually. The domestic market also benefits from a highly competitive telecommunications landscape where operators frequently subsidize the latest smartphones, encouraging frequent upgrades to devices with advanced display technologies. The country's vibrant digital content creation scene, particularly in video and streaming, has increased consumer awareness of display quality, pushing brands to offer better visual specifications even in budget segments. Additionally, the growing adoption of mobile payments and digital wallets requires secure and responsive touch interfaces, further driving demand for modern capacitive display solutions. This combination of tourism needs, telecom competition, and high data usage ensures Spain remains a vital and evolving market for mobile displays.

COMPETITIVE LANDSCAPE

The competition in the Europe mobile display market is characterized by intense rivalry among established multinational corporations and emerging Asian giants vying for dominance in specific technology verticals like foldable and high refresh rate panels. Large global players leverage their extensive manufacturing networks and deep technical expertise to secure long-term supply agreements with major smartphone brands and automotive integrators across the continent. This trend towards comprehensive solution providers creates high barriers to entry for smaller firms unless they possess highly differentiated, flexible display technologies or proprietary low-power architectures. The competitive landscape is further complicated by stringent European Union environmental regulations and varying sustainability standards across different nations, which demand rigorous testing and certification before market approval. Companies must therefore invest significantly in research and development to demonstrate superior durability and energy efficiency while navigating complex procurement processes. Innovation speed and the ability to provide localized after-sales support are critical differentiators that determine market success. Furthermore, strategic alliances between display manufacturers and glass suppliers have become essential for accessing cutting-edge substrate materials to accelerate product adoption. The market remains dynamic with continuous entries of micro light-emitting diode solutions challenging traditional organic light-emitting diode standards and reshaping competitive dynamics across the region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Mobile Display Market include

- Samsung Display Co., Ltd.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- AU Optronics Corporation

- Innolux Corporation

- Japan Display Inc.

- Sharp Corporation

- Visionox Company

- Tianma Microelectronics Co., Ltd.

- Sony Corporation

- Panasonic Holdings Corporation

- Corning Incorporated

TOP LEADING PLAYERS IN THE MARKET

- Samsung Display Co., Ltd. stands as a global pioneer in mobile visual technology with a profound impact on the European market through its leadership in flexible organic light-emitting diode panels. The company contributes significantly to the global supply chain by setting industry standards for resolution, brightness, and foldable form factors used in flagship smartphones. Recently, Samsung Display has strengthened its position by expanding production lines dedicated to ultra-thin glass substrates specifically for the growing European foldable device sector. The firm actively collaborates with major European smartphone manufacturers to co-develop custom display solutions that meet strict energy efficiency regulations. These strategic initiatives ensure their technology remains at the forefront of innovation while addressing the increasing demand for durable and immersive mobile screens across the continent.

- LG Display Co Ltd operates as a leading innovator in advanced panel technologies with a dominant presence in the European market, particularly within high-performance liquid crystal and organic light-emitting diode segments. The company contributes globally by delivering versatile displays that offer superior color accuracy and eye comfort features essential for modern mobile usage. Their recent actions to solidify market presence include launching new low-power oxide backplane technologies designed to extend battery life for devices sold in Western Europe. LG Display has also invested heavily in establishing technical support centers near key European original equipment manufacturer hubs to facilitate rapid integration. The firm frequently engages in partnerships with automotive companies to adapt mobile display tech for vehicle interfaces. By focusing on sustainability and operational efficiency, LG Display enhances value for customers seeking compliant and high-quality visual components. These efforts demonstrate their commitment to driving technological advancement and maintaining leadership in the competitive European arena.

- BOE Technology Group Co., Ltd. is a specialized display manufacturer that has established itself as a key player in the European market through its focus on cost-effective and high-volume mobile panel solutions. The company makes a substantial global contribution by supplying a wide range of liquid crystal and organic light-emitting diode screens to diverse smartphone brands targeting the mid-range segment. Their recent strategy to strengthen their European position involves opening new research facilities in Germany to develop localized display modules that comply with European Union repairability standards. BOE has also expanded its logistics network to ensure the timely delivery of panels to assembly plants across Eastern and Southern Europe. The firm continues to invest in next-generation micro light-emitting diode research to future-proof its product portfolio against evolving consumer demands. By maintaining a dedicated focus on scalability and technological accessibility, BOE addresses the needs of budget-conscious manufacturers. Their persistent innovation in mass production techniques ensures they remain a vital partner for industries seeking reliable and affordable mobile display solutions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe mobile display market predominantly employ strategic product differentiation and regulatory compliance to secure supply chains and meet escalating regional demand for sustainable visual technologies. Companies frequently invest billions in constructing new fabrication lines specifically for flexible organic light-emitting diode panels to support the burgeoning foldable smartphone sector. Another major strategy involves forming deep collaborative partnerships with European original equipment manufacturers to co-develop customized display solutions that address specific application requirements like high refresh rates and low power consumption. Market participants also focus heavily on expanding their recycling and repair programs to align with strict European Union right-to-repair directives and circular economy goals. Investment in research and development remains a cornerstone strategy as firms strive to achieve breakthroughs in pixel density and energy efficiency. Additionally, companies pursue targeted acquisitions of material science startups to rapidly incorporate novel substrate and encapsulation technologies into their existing production platforms. These combined approaches allow industry leaders to navigate complex environmental regulations while maintaining a competitive edge in this rapidly evolving technological sector.

MARKET SEGMENTATION

This research report on the europe mobile display market is segmented and sub-segmented into the following categories.

By Type

- Capacitive Display Screens

- Resistive Display Screens

By Display Technology

- IPS-LCD (In-Plane Switching Liquid Crystal Display)

- AMOLED

- OLED (Others)

By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com