Europe Orthodontics Market Size, Share, Growth, Trends Research Report, Segmented By Product, Age Group, End-user, And By Region (U.K France, Germany, Spain, Italy, Sweden, Russia and Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis Forecasts (2026 to 2034)

Europe Orthodontics Market Report Summary

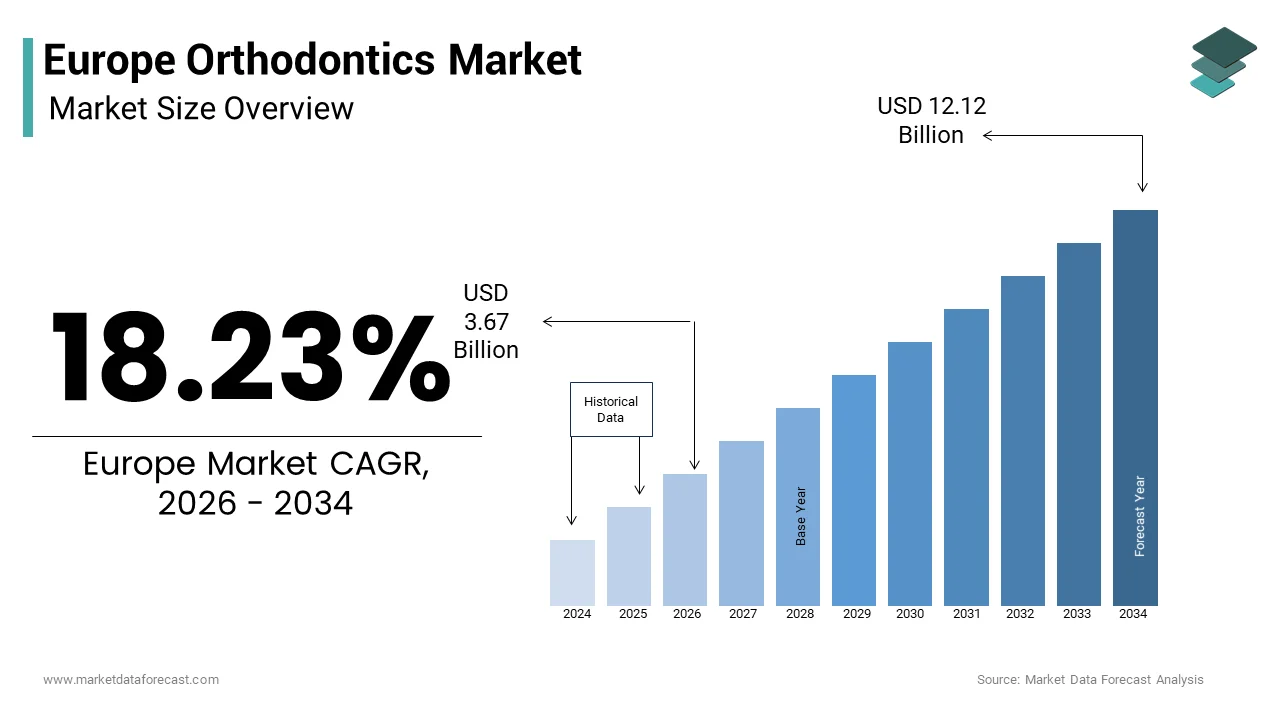

The Europe orthodontics market was valued at USD 3.10 billion in 2025, is estimated to reach USD 3.67 billion in 2026, and is projected to reach USD 12.12 billion by 2034, growing at a CAGR of 18.23% during the forecast period from 2026 to 2034. The growth of the Europe orthodontics market is driven by increasing awareness of dental aesthetics, rising demand for corrective dental procedures, and advancements in orthodontic technologies such as clear aligners and digital treatment planning. The growing focus on cosmetic dentistry, coupled with increasing disposable incomes and improved access to dental care, is further accelerating market expansion across Europe.

Key Market Trends

- Rising demand for aesthetic orthodontic solutions such as clear aligners and invisible braces is transforming treatment preferences.

- Increasing adoption of digital orthodontics, including 3D imaging and computer-aided treatment planning, is improving precision and patient outcomes.

- Growing awareness of dental health and early orthodontic intervention among younger populations is boosting market demand.

- Expansion of private dental clinics and specialized orthodontic practices across Europe is enhancing accessibility to advanced treatments.

- Technological innovations in materials and appliance design are improving comfort, efficiency, and treatment duration.

Segmental Insights

- Based on product, the fixed appliances segment dominated the Europe orthodontics market by holding a share of 58.9% in 2025. The segment’s leadership is attributed to its effectiveness in treating complex dental conditions and its widespread adoption among orthodontic professionals.

- Based on age group, the teens segment accounted for 62.6% of the Europe orthodontics market share in 2025. The dominance of this segment is driven by increasing orthodontic awareness among adolescents and early intervention practices recommended by dental professionals.

- Based on end user, the dentist and orthodontist-owned practices segment was the largest in the Europe orthodontics market in 2025. This is due to the high trust, personalized care, and specialized treatment offered by professional dental practices.

Regional Insights

The Europe orthodontics market exhibits strong growth across major countries.

- Germany led the market by accounting for 22.7% of the share in 2025, supported by advanced healthcare infrastructure and high adoption of orthodontic treatments.

- The United Kingdom followed with 16.4% of the market share, driven by increasing demand for cosmetic dentistry.

- France holds a significant position due to supportive regulatory frameworks and structured dental care systems.

- Italy remains a key market driven by a strong culture of aesthetic awareness and a high prevalence of private practices.

- Spain is expected to witness notable growth during the forecast period due to improving access to dental care and rising consumer awareness.

Competitive Landscape

The Europe orthodontics market is highly competitive, with key players focusing on innovation, product development, and strategic partnerships to strengthen their market presence. Companies are investing in advanced orthodontic solutions, expanding their digital capabilities, and enhancing treatment offerings to meet evolving consumer demands. Prominent players in the Europe orthodontics market include Dentsply Sirona, American Orthodontics, Institut Straumann AG, Align Technology, Inc., Solventum, Henry Schein, Inc., DB Orthodontics, Envista Holdings Corporation, Angelalign Technology Inc., TP Orthodontics, Inc., Braces on Demand, LightForce, Candid Care Co., and KLOwen.

Europe Orthodontics Market Size

The Europe Orthodontics market size was valued at USD 3.10 billion in 2025 and is anticipated to reach USD 3.67 billion in 2026 to reach USD 12.12 billion by 2034, growing at a CAGR of 18.23% during the forecast period from 2026 to 2034.

Current Introduction of the Europe Orthodontics Market

Orthodontics is a specialized branch of dentistry focused on diagnosing, preventing, and treating misaligned teeth and jaws. This market operates within a complex healthcare landscape where aesthetic concerns increasingly intersect with functional dental health requirements. The region hosts a significant burden of malocclusion. Epidemiological studies indicate that approximately 60% to 75% of the European population exhibits some form of tooth misalignment requiring professional intervention. As per data from the World Health Organization, oral diseases affect nearly 3.5 billion people globally, with dental caries and severe periodontal disease being primary contributors to tooth loss and subsequent alignment issues in Europe. The demographic shift toward an aging population further complicates the scenario, as adults now seek corrective treatments at higher rates than in previous decades. National health surveys in countries like Germany and France reveal that approximately 35% to 45% of adults express dissatisfaction with their smile aesthetics, driving a cultural shift toward accepting orthodontic care beyond adolescence. Furthermore, the integration of digital scanning technologies has transformed patient intake processes, reducing the reliance on physical impressions and enhancing diagnostic precision across clinics in the United Kingdom and Italy. These foundational elements create a robust environment for specialized dental interventions, supported by a strong network of orthodontic specialists and evolving reimbursement frameworks that gradually acknowledge the necessity of comprehensive occlusal management.

MARKET DRIVERS

Rising Prevalence of Malocclusion and Increasing Adult Acceptance

The escalating incidence of malocclusion is one of the major drivers of the Europe orthodontics market. Clinical assessments suggest that roughly 60% to 70% of children and adolescents in Western Europe present with varying degrees of dental irregularities that benefit from early intervention. This high prevalence rate creates a consistent pipeline of patients entering the treatment ecosystem annually. Beyond the pediatric demographic, there is a profound surge in adult participation driven by heightened aesthetic awareness and social pressures. The European Society of Orthodontists indicates that adult patients now constitute 30% to 40% of all new orthodontic cases in major markets such as Spain and the Netherlands. This shift stems from a growing understanding that straight teeth contribute significantly to psychological well being and professional confidence. Surveys conducted by national dental associations reveal that 8 out of 10 adults believe a perfect smile enhances career prospects and social interactions. The demand is further amplified by the availability of discreet treatment options that cater specifically to working professionals who wish to avoid the visual impact of traditional metal brackets. Technological advancements have reduced treatment durations, making the commitment more manageable for busy adults. Consequently, the convergence of widespread dental misalignment and a cultural pivot toward aesthetic perfectionism ensures a steady and expanding volume of patients seeking corrective solutions throughout the continent.

Technological Integration and Digital Workflow Adoption

The rapid assimilation of digital technologies into orthodontic practices fundamentally alters patient access and treatment efficiency across the region, which also contributes to the expansion of the Europe orthodontics market. The transition from conventional impression materials to intraoral scanners has revolutionized the initial consultation phase, reducing chair time. This digital transformation enables precise three dimensional modeling of dentition, allowing clinicians to simulate treatment outcomes with greater accuracy before any appliance is fabricated. Orthodontic technology reviews shows that clinics using 3D simulations and fully digital workflows see a significant boost, often cited at 40%, in case acceptance, as patients can visualize their final results before starting. The proliferation of tele dentistry platforms further extends reach, permitting remote monitoring of progress and reducing the frequency of in person visits which is particularly beneficial for patients in rural areas of Poland and Romania. Moreover, the automation of aligner manufacturing through computer aided design and computer aided manufacturing systems has slashed production turnaround times from weeks to mere days. This efficiency allows providers to manage larger patient volumes without compromising care quality. The seamless integration of artificial intelligence in treatment planning also minimizes human error and optimizes force application on teeth. These technological strides collectively lower barriers to entry for both providers and patients, fostering a more dynamic and accessible market environment that encourages broader adoption of orthodontic services.

MARKET RESTRAINTS

High Treatment Costs and Limited Reimbursement Coverage

The substantial financial burden associated with orthodontic procedures remains a formidable barrier preventing widespread adoption across diverse socioeconomic groups in the region, and thereby negatively impacts the growth of the Europe orthodontics market. Comprehensive treatment plans often exceed 4000 euros depending on the complexity of the case and the type of appliance selected, placing them out of reach for many households without adequate insurance support. As per findings from the European Commission on health expenditure, out of pocket payments for dental care account for nearly 60 percent of total dental spending in several member states, highlighting the lack of universal coverage for corrective procedures. While some nations like Germany offer partial subsidies for children under specific medical necessity criteria, adult treatments are largely excluded from public health schemes. This disparity forces patients to rely on private financing or forego treatment entirely. Economic volatility in regions such as Southern Europe has further exacerbated affordability issues, with disposable income contraction leading to a decline in elective dental procedures during recent fiscal downturns. Private insurance policies frequently impose low annual caps on orthodontic benefits, often covering lesser share of the total cost. The absence of standardized reimbursement frameworks across the European Union creates a fragmented landscape where access depends heavily on geographic location and individual financial status. Consequently, despite the clear clinical need and desire for straighter teeth, the prohibitive cost structure acts as a significant dampener on market growth, limiting the patient pool to those with sufficient discretionary funds.

Shortage of Skilled Orthodontic Specialists

The acute scarcity of qualified orthodontic specialists relative to the growing patient demand continues to impede the full potential and the growth of the Europe orthodontics market. Training to become a certified orthodontist requires extensive postgraduate education spanning several years, resulting in a slow replenishment rate of the workforce. Data from the Federation of European Specialists in Orthodontics reveals that the ratio of orthodontists to the general population varies drastically, with some Eastern European countries having 5 – 10 or even fewer than 2 specialists per 100000 inhabitants compared to Western counterparts. This imbalance leads to prolonged waiting lists that can extend beyond 12 months in high demand urban centers like London and Paris. The barrier in human resources directly caps the number of cases a clinic can handle annually, regardless of technological advancements or marketing efforts. Furthermore, the aging workforce presents an additional challenge, as a significant portion of current practitioners approach retirement age without enough younger professionals to replace them. Recruitment difficulties are compounded by the high operational costs of establishing a specialized practice, deterring new graduates from entering independent practice. The shortage forces general dentists to attempt complex cases beyond their expertise, potentially compromising treatment quality and patient safety. The labor deficit will continue to stifle market expansion and limit timely access to essential care for millions of Europeans. This situation will persist until educational institutions expand their capacity and regulatory bodies streamline licensure mobility across borders.

MARKET OPPORTUNITIES

Expansion of Clear Aligner Therapy Among Teenage Demographics

The burgeoning acceptance of clear aligner systems among teenagers gives a lucrative opportunity for market stakeholders to capture a previously underserved segment, which is anticipated to boost the growth of the Europe orthodontics market. Historically, adolescents were predominantly treated with fixed metal braces due to compliance concerns regarding removable appliances. However, recent behavioral studies indicate that modern teenagers exhibit higher discipline levels and stronger aesthetic preferences than previous generations. Parents are increasingly willing to invest in these premium options due to the perceived social benefits and reduced stigma associated with invisible trays. Schools and peer groups have become more accepting of diverse orthodontic solutions, further normalizing the use of aligners among youth. Manufacturers are responding by developing products specifically engineered for teenage lifestyles, including compliance indicators and eruption tabs to accommodate developing dentition. The ability to remove trays for sports and musical instruments appeals strongly to active adolescents and their guardians. Additionally, the integration of gamified mobile applications helps monitor wear time and engages younger patients in their treatment journey. This demographic shift opens a vast avenue for revenue generation, allowing providers to diversify their portfolios beyond traditional braces and cater to a tech savvy generation that prioritizes discretion and convenience without compromising clinical efficacy.

Integration of Artificial Intelligence for Predictive Treatment Planning

The incorporation of artificial intelligence into orthodontic workflows paves the way to elevate treatment standards and operational efficiency across the region, which offers strong potential for the Europe orthodontics market. AI algorithms can analyze vast datasets of craniofacial images to predict tooth movement patterns with unprecedented accuracy, enabling clinicians to devise highly personalized treatment strategies. As per sources, AI assisted planning reduces the need for mid course corrections, thereby shortening overall treatment duration and improving patient satisfaction. This technology empowers practitioners to anticipate potential complications before they arise, ensuring smoother progression and more predictable outcomes. The capability to simulate thousands of virtual treatment scenarios allows for the selection of the optimal mechanical approach tailored to individual anatomical constraints. Furthermore, AI driven tools facilitate better communication between orthodontists and laboratory technicians, streamlining the fabrication of custom appliances and reducing material waste. The automation of routine diagnostic tasks frees up valuable clinical time, allowing specialists to focus on complex case management and patient interaction. As computational power increases and algorithms become more sophisticated, the scope of AI applications will expand to include real time adjustment recommendations based on remote monitoring data. Embracing these intelligent systems positions European clinics at the forefront of innovation, attracting discerning patients who seek cutting edge care and reinforcing the region reputation as a hub for advanced dental medicine.

MARKET CHALLENGES

Regulatory Complexities Regarding Device Approval

Navigating the intricate regulatory landscape for medical devices is a major obstacle for companies operating within the Europe orthodontics market. The implementation of the European Union Medical Device Regulation has intensified scrutiny on clinical evidence and post market surveillance requirements, extending approval timelines significantly. Also, the heightened regulatory burden disproportionately affects smaller enterprises and startups lacking the resources to conduct extensive trials and maintain rigorous documentation standards. The variability in interpretation among different notified bodies across member states further complicates the harmonization of market entry strategies. Companies often face conflicting feedback requiring multiple submission rounds, which inflates development costs and strains financial reserves. Additionally, the requirement for unique device identification and traceability adds layers of administrative complexity to supply chain management. The constant evolution of compliance standards demands continuous investment in legal expertise and quality assurance systems. These regulatory headwinds create an environment of uncertainty that can stifle innovation and slow the introduction of novel therapeutic solutions. Compliance obligations currently cause significant friction. Until a more streamlined oversight approach emerges, this will remain an obstacle to agility and competition.

Supply Chain Vulnerabilities and Material Availability

The fragility of global supply chains continues to threaten the stability of product availability throughout the region. This also inhibits the expansion of the Europe orthodontics market. The market relies heavily on specialized raw materials such as medical grade polymers and nickel titanium alloys, sourcing which often involves complex international logistics networks. Disruptions caused by geopolitical tensions or pandemics have exposed the susceptibility of these channels, leading to sporadic shortages and price volatility. The concentration of manufacturing capabilities in specific geographic regions creates single points of failure that can cascade into widespread delays. Fluctuations in energy costs within Europe further exacerbate production expenses, compelling manufacturers to pass on price increases to distributors and ultimately to patients. Inventory management becomes increasingly difficult when demand forecasts are rendered unreliable by external shocks. The lack of localized production facilities for certain high tech appliances means that European providers remain dependent on imports subject to customs bottlenecks and transportation delays. Building resilient supply networks requires substantial capital investment in diversification and stockpiling, which many small to medium sized entities cannot afford. These systemic vulnerabilities undermine the reliability of service delivery and erode trust among stakeholders who depend on consistent access to high quality orthodontic materials.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 18.23% |

| Segments Covered | By Product, Age Group, End-user, By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

| Market Leaders Profiled | Dentsply Sirona (U.S.), AMERICAN ORTHODONTICS (U.S.), Institut Straumann AG (Switzerland), Align Technology, Inc. (U.S.), Solventum (U.S.), Henry Schein, Inc. (U.S.), DB Orthodontics (U.S.), ENVISTA HOLDINGS CORPORATION (U.S.), Angelalign Technology Inc. (China), TP Orthodontics, Inc. (U.S.), BRACES ON DEMAND (U.S.), LightForce (U.S.), Candid Care Co. (U.S.), KLOwen (U.S.) |

SEGMENTAL ANALYSIS

By Product Insights

The fixed appliances segment dominated the Europe orthodontics market and accounted for a 58.9% share in 2025. This dominance of the segment is attributed to the clinical necessity of fixed systems for correcting complex malocclusions that removable options cannot address effectively. The segment includes brackets, bands, buccal tubes, and archwires, which remain the gold standard for comprehensive tooth movement control. Fixed appliances offer unparalleled precision in managing severe dental irregularities, making them the preferred choice for orthodontists treating intricate cases. As per clinical guidelines, fixed systems allow for three dimensional control of tooth position that removable aligners often struggle to achieve, particularly in cases requiring significant rotation or vertical movement. The ability to apply continuous force regardless of patient compliance ensures predictable outcomes, a critical factor for practitioners managing adolescent patients who may lack discipline with removable devices. Furthermore, the versatility of customizing wire sequences and bracket prescriptions allows clinicians to tailor mechanics to individual biological responses. This clinical reliability sustains high demand across public and private healthcare settings, ensuring that fixed appliances remain the backbone of orthodontic therapy despite the rising popularity of aesthetic alternatives. Economic factors heavily favor fixed appliances, as they generally present a lower overall cost profile compared to premium clear aligner systems, aligning better with existing reimbursement structures in many European nations. In countries like Germany and France, statutory health insurance schemes provide partial coverage for fixed braces for children under 18, whereas coverage for aligners is often restricted or entirely excluded. This financial disparity drives volume, as price sensitive patients and parents opt for the subsidized fixed option. Additionally, the durability of metal and ceramic brackets reduces the need for frequent replacements, lowering long term maintenance costs for patients. The established supply chain for fixed components also ensures competitive pricing among manufacturers, preventing cost inflation. Consequently, the alignment of fixed appliances with favorable insurance policies and their inherent affordability secures their position as the volume leader in the European market landscape.

The removable aligners segment is predicted to witness the highest CAGR of 14.2% during the forecast period owing to shifting patient preferences toward invisible solutions and technological advancements that have expanded the treatable case scope for aligners. The main growth factor for the rapid expansion of removable aligners is the intense consumer demand for discreet treatment options that do not compromise personal appearance during social or professional interactions. The stigma associated with metal braces has driven a mass migration toward clear trays, particularly among working professionals and public figures who cannot afford the visual impact of traditional hardware. Social media influence has further normalized invisible aligners, with celebrities and influencers frequently showcasing their treatment journeys, thereby reducing psychological barriers for potential patients. The perception of aligners as a modern, lifestyle compatible solution appeals strongly to the growing adult demographic, which now represents a significant portion of new case starts. Manufacturers have capitalized on this sentiment by marketing aligners not just as medical devices but as wellness accessories, enhancing their appeal. This cultural shift toward valuing invisibility ensures that demand for removable systems will outpace traditional options as awareness penetrates deeper into conservative demographics across Southern and Eastern Europe. Advancements in digital planning software and material science have dramatically widened the range of malocclusions that removable aligners can successfully correct, removing previous clinical limitations. As per technical reports from leading aligner manufacturers, recent iterations of smart polymer materials exert more consistent and biologically optimal forces, enabling the correction of complex movements such as extrusions and significant rotations that were once exclusive to fixed braces. The integration of artificial intelligence in treatment simulation allows clinicians to predict outcomes with greater accuracy, boosting confidence in prescribing aligners for moderate to severe cases. Attachments and precision cuts have evolved to provide the necessary anchorage and force vectors, bridging the efficacy gap with fixed appliances. Furthermore, the speed of digital workflow from scanning to delivery has reduced turnaround times to under one week, enhancing patient satisfaction and clinic throughput. These technological leaps have transformed aligners from a niche cosmetic product into a comprehensive therapeutic modality, driving their explosive growth across the European market.

By Age Group Insights

The teens segment led the Europe orthodontics market and occupied a 62.6% share in 2025. This supremacy of the segment is credited to the biological advantages of treating malocclusion during adolescence and the strong support of school based screening programs and parental investment in early intervention. Treating orthodontic issues during the teenage years offers distinct biological advantages that make it the clinically preferred timing for intervention, thereby driving high volume in this demographic. During adolescence, the jawbones are still growing and more malleable, allowing for faster tooth movement and the possibility of guiding skeletal development without surgical intervention. As per research, treatment duration for teens is shorter than for adults due to higher cellular turnover rates and more responsive periodontal ligaments. This efficiency reduces the overall burden on patients and lowers the risk of root resorption or other complications associated with prolonged force application. Early correction also prevents the worsening of malocclusion, reducing the need for complex procedures like extractions or orthognathic surgery later in life. Pediatric dentists play a crucial role by identifying issues early through routine checkups. The consensus among clinicians that adolescence is the optimal window for treatment ensures a steady influx of teenage patients, solidifying this segment as the market leader in terms of case numbers and procedural volume. A strong cultural emphasis on preventive dental care and the willingness of parents to invest in their children long term health underpins the dominance of the teen segment. In Europe, parents increasingly view orthodontic treatment not as a luxury but as a essential component of overall health and future success. Many national health systems reinforce this behavior by offering subsidies or full coverage for orthodontic treatment for minors, significantly lowering the financial barrier for families. For instance, in countries like Sweden and Denmark, public healthcare covers a substantial portion of orthodontic costs for individuals under 20, encouraging universal uptake. School based dental screening programs further identify candidates early, creating a structured pipeline into the treatment system. The perception that correcting teeth early prevents costly dental problems in adulthood motivates parents to act promptly. This combination of biological timing, financial support, and parental dedication creates a robust and consistent demand base that keeps the teen segment at the forefront of the market.

The adults segment is estimated to register the fastest CAGR of 11.8% between 2026 and 2034 due to the normalization of adult orthodontics, increased disposable income among the working population, and the availability of discreet treatment modalities tailored specifically for mature patients. Moreover, the swift growth in adult orthodontics is largely propelled by a heightened awareness of the link between dental aesthetics and professional success in a competitive European job market. As per studies, individuals with confident smiles are perceived as more competent and approachable, leading to a higher likelihood of promotion in client facing roles. This realization has motivated a large cohort of professionals in their 30s and 40s to seek corrective treatment they may have missed during childhood. The stigma of wearing braces as an adult has diminished significantly, replaced by a view of orthodontics as a worthwhile investment in personal branding. Corporate wellness trends have also begun to include dental aesthetics, with some employers offering flexible spending accounts that can be utilized for such procedures. The rise of remote work and video conferencing has further intensified focus on facial appearance, accelerating the decision to undergo treatment. With the adult population in Europe expected to grow due to aging demographics, this pool of aesthetically conscious consumers continues to expand, fueling the double digit growth rates observed in this segment across major economies like Germany and the United Kingdom. The development of highly discreet and comfortable orthodontic solutions specifically designed for adult lifestyles has removed key barriers to entry, catalyzing rapid market expansion. Traditional metal braces were often a deterrent for adults due to visibility and discomfort, but the advent of lingual braces and advanced clear aligners has changed this dynamic. Moreover, improvements in aligner material comfort have reduced irritation, making them suitable for adults with sensitive gums or existing restorative work like crowns and bridges. The ability to remove aligners for business meals and social events aligns perfectly with the active social lives of European adults. Furthermore, shorter treatment protocols utilizing accelerated orthodontic techniques appeal to time constrained professionals who cannot commit to multi year therapies. Marketing campaigns targeting adults have effectively communicated these benefits, shifting the narrative from pediatric correction to adult enhancement. Technology continues to refine these invisible options. As a result, the addressable market for adult orthodontics will widen, sustaining its status as the highest growth segment.

By End User Insights

In 2025, dentist and orthodontist owned practices segment was the largest segment in the Europe orthodontics market and occupied a substantial share because of the specialized nature of orthodontic care, the trust patients place in direct provider relationships, and the comprehensive service model these practices offer. Apart from these, a key growth enabler of this segment is the high level of expertise required for complex orthodontic diagnoses and treatments, which fosters deep patient trust. Orthodontics is a recognized specialty requiring additional years of postgraduate training, and patients overwhelmingly prefer seeking care from certified specialists rather than general dentists or corporate chains. These independent practices often boast long standing relationships with local communities, creating a loyal patient base that values personalized care plans over standardized corporate protocols. The ability of specialist owners to tailor every aspect of treatment, from appliance selection to retention strategies, ensures higher satisfaction and referral rates. Furthermore, these practices are typically at the forefront of adopting new technologies, as owners have a direct incentive to invest in tools that enhance clinical efficiency and results. This reputation for excellence and the perception of unbiased, patient centric care solidify the position of independent specialist practices as the primary channel for orthodontic services across the continent. Independent dentist and orthodontist practices offer a continuum of care that integrated corporate models often struggle to replicate, ensuring better long term outcomes and patient retention. In a specialist owned setting, the same clinician oversees the patient from initial diagnosis through active treatment and into the retention phase, minimizing communication gaps and ensuring consistent mechanical application. The continuity allows for nuanced adjustments based on the patient unique biological response, which is critical for achieving stable results. Additionally, these practices often provide holistic oral health advice, coordinating with general dentists and other specialists to address broader dental needs simultaneously. The flexibility of independent practices enables them to offer extended appointment hours and emergency support, catering to the specific schedules of students and working adults. This personalized, end to end service model builds strong patient loyalty and generates a steady stream of word of mouth referrals, which remains the most powerful marketing tool in the dental sector, thereby maintaining the segment market leadership.

The corporate chains and hospital based clinics segment is anticipated to witness the fastest CAGR of 9.5% during the forecast period. This acceleration is fueled by consolidation trends in the healthcare sector and the increasing integration of orthodontics into broader multidisciplinary hospital services. The rapid expansion of corporate chains is driven by aggressive consolidation strategies that leverage economies of scale to offer competitive pricing and standardized high quality care. Large dental groups are acquiring independent practices across Europe to create extensive networks that can negotiate better rates for supplies and insurance contracts, passing savings to patients. The financial efficiency allows them to invest heavily in state of the art digital infrastructure, such as in house 3D printing and AI diagnostics, which attracts tech savvy patients. Furthermore, corporate entities have the capital to execute large scale marketing campaigns that build brand recognition quickly, drawing patients who value consistency and convenience across multiple locations. The ability to offer flexible financing plans and membership models also broadens access for middle income families who might find independent practice fees prohibitive. As the healthcare landscape in Europe shifts towards larger integrated providers, the momentum behind corporate chains is expected to continue, reshaping the delivery model of orthodontic care. Hospital based clinics are witnessing accelerated growth due to the increasing recognition of orthodontics as a critical component of multidisciplinary care for patients with craniofacial anomalies and severe skeletal discrepancies. Modern hospitals are expanding their dental departments to include specialized orthodontic units that collaborate closely with oral surgeons, speech therapists, and geneticists. The collaborative approach is essential for treating conditions like cleft lip and palate, where timing and precision are paramount. Public funding often supports these hospital based services, making them accessible to patients with severe needs regardless of their financial status. The presence of advanced imaging facilities and surgical theaters within hospitals facilitates seamless transitions from diagnosis to operative care, reducing patient stress and treatment time. Awareness of the benefits of multidisciplinary care is growing, leading to an increase in patients referred to hospital clinics for comprehensive management. Consequently, this trend is driving the upward trajectory of this segment within the broader market.

COUNTRY LEVEL ANALYSIS

Germany Orthodontics Market Analysis

Germany outperformed other countries in the Europe orthodontics market and accounted for a 22.7% share in 2025. The driving force behind this dominance is the widespread coverage provided by the German statutory health insurance, which fully reimburses orthodontic treatment for children and adolescents with diagnosed medical necessity, ensuring near universal access for the younger demographic. Also, the German market has a highly developed healthcare infrastructure, a dense network of specialized orthodontic practices, and a robust statutory insurance system that supports early intervention. Furthermore, Germany boasts one of the highest densities of orthodontic specialists in the world, with rigorous training standards that maintain exceptional clinical quality. The German population exhibits a strong cultural appreciation for dental perfection, viewing straight teeth as a marker of health and social standing. High disposable income levels also enable adults to pursue premium elective treatments like lingual braces and clear aligners, which are increasingly popular in urban centers like Munich and Berlin. The convergence of comprehensive insurance support, specialist availability, and aesthetic consciousness ensures Germany retains its top position, setting the benchmark for clinical standards and market volume across the continent.

United Kingdom Orthodontics Market Analysis

The United Kingdom was the next prominent counrty in the regional market, and occupied a 16.4% share in 2025. A key driver for the UK market is the significant activity within the private sector, where waiting lists for NHS orthodontic treatment have pushed many patients toward private providers. The market status here is defined by a dual system of public provision through the National Health Service and a vibrant private sector that caters to aesthetic demands. The UK is also a hub for innovation, with London serving as a headquarters for several global aligner companies, fostering rapid adoption of new technologies. The growing trend of "smile makeovers" among the working population has further stimulated demand, with adults increasingly viewing orthodontics as a key element of personal grooming. Despite economic fluctuations, the resilience of the private dental market remains strong, supported by flexible finance options that make treatment affordable. The combination of public health mandates for children and a booming private adult market creates a balanced yet dynamic environment that sustains the UK status as a key growth engine in Europe.

France Orthodontics Market Analysis

France plays a major role in the European market. This position of the French market is fuelled by the "Convention Nationale des Chirurgiens-Dentistes," which regulates fees and ensures a baseline of affordability for patients. The French market has a strong tradition of dental care and a reimbursement framework that, while undergoing reforms, still provides significant support for orthodontic interventions. However, the most dynamic growth is occurring in the adult segment, fueled by a rising fashion consciousness in cities like Paris and Lyon where aesthetic perfection is highly valued. French consumers are increasingly opting for invisible aligners, with adoption rates climbing steeply as social stigma around adult braces dissipates. The presence of renowned dental schools and research institutions also fosters a culture of evidence based practice, encouraging the uptake of advanced digital workflows. Additionally, the French government initiatives to improve oral health awareness have led to earlier detection of malocclusion, expanding the treatable population. This blend of regulatory support, cultural emphasis on aesthetics, and clinical excellence propels France as a pivotal market in the region.

Italy Orthodontics Market Analysis

Italy maintains a key position in the regional market due to a high prevalence of private practice and a deep seated cultural emphasis on personal appearance. The market status in Italy is unique due to the limited public reimbursement for orthodontics, which has fostered a robust private sector where patients directly fund their treatments. The primary driver here is the intense aesthetic focus of the Italian population, where a perfect smile is considered integral to social identity and professional success. The demand for high end aesthetic solutions like ceramic brackets and custom lingual systems is particularly strong in northern regions such as Lombardy and Veneto. Italian dentists are known for their artistic approach to smile design, often integrating orthodontics with restorative and cosmetic procedures to achieve holistic results. This comprehensive approach appeals to discerning patients willing to invest in premium care. Furthermore, the growing medical tourism sector attracts patients from neighboring countries seeking high quality yet competitively priced treatments. The synergy of cultural values, private sector agility, and clinical artistry ensures Italy remains a critical and influential market within the European landscape.

Spain Orthodontics Market Analysis

Spain is likely to grow notably in the European market from 2026 to 2034, with a landscape marked by rapid modernization and increasing acceptance of orthodontic care across all age groups. The market status is evolving from a traditionally low utilization rate to a high growth trajectory, driven by improved economic conditions and greater health awareness. A key driver for the Spanish market is the expanding middle class which now views orthodontics as an attainable investment rather than a luxury. The proliferation of dental clinics offering flexible payment plans has democratized access, allowing families to manage costs over time. Spain is also seeing a boom in clear aligner adoption, particularly among the youth in metropolitan areas like Madrid and Barcelona, influenced by global trends and social media. The government recent efforts to enhance public oral health programs are beginning to yield results, with earlier screenings in schools identifying more candidates for intervention. Additionally, Spain emerging role as a destination for affordable high quality dental tourism bolsters clinic volumes. These factors combine to create a vibrant, fast expanding market that is quickly closing the gap with its northern European counterparts.

COMPETITIVE LANDSCAPE

The competitive landscape of the Europe orthodontics market is characterized by intense rivalry among established multinational corporations and agile niche innovators. Market leaders leverage their extensive distribution networks and broad product portfolios to maintain dominance while facing pressure from newer entrants specializing in clear aligner technology. The threat of new competitors remains high as digital manufacturing lowers barriers to entry for custom appliance providers. Competitive dynamics are further shaped by rapid technological advancements where companies vie to offer the most precise and efficient digital workflows. Price competition is evident in the fixed appliance segment whereas differentiation through aesthetics and comfort drives competition in the removable sector. Regulatory compliance acts as a significant moat protecting incumbents but also slows down the speed of innovation for smaller firms. Strategic collaborations between manufacturers and software developers are becoming common to create integrated solutions that lock in customers. The market sees frequent product launches aimed at capturing specific demographic segments such as adults or teenagers. Overall the environment fosters continuous improvement in clinical outcomes.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe orthodontics market are

- Dentsply Sirona (U.S.)

- AMERICAN ORTHODONTICS (U.S.)

- Institut Straumann AG (Switzerland)

- Align Technology, Inc. (U.S.)

- Solventum (U.S.)

- Henry Schein, Inc. (U.S.)

- DB Orthodontics (U.S.)

- ENVISTA HOLDINGS CORPORATION (U.S.)

- Angelalign Technology Inc. (China)

- TP Orthodontics, Inc. (U.S.)

- BRACES ON DEMAND (U.S.)

- LightForce (U.S.)

- Candid Care Co. (U.S.)

- KLOwen (U.S.)

Top Players In The Market

- Align Technology stands as a global pioneer in digital orthodontics and is best known for its Invisalign clear aligner system. The company has revolutionized the industry by shifting treatment paradigms from fixed appliances to removable aesthetic solutions. In Europe, Align Technology continues to expand its footprint by partnering with local orthodontists and investing heavily in digital scanning infrastructure. Recent actions include the enhancement of its iTero intraoral scanner portfolio with artificial intelligence capabilities to improve treatment planning accuracy. The firm actively engages in educational initiatives across European dental schools to train the next generation of practitioners on digital workflows. By continuously refining its polymer materials and expanding treatment indications for complex cases, Align Technology solidifies its leadership position. Their commitment to direct to consumer models in select regions also broadens access while maintaining strong relationships with professional providers throughout the continent.

- Dentsply Sirona operates as a comprehensive dental technology giant with a profound impact on the global orthodontics landscape through its extensive product portfolio. The company integrates orthodontic instruments, brackets, and digital solutions into a cohesive ecosystem that serves practitioners worldwide. In Europe, Dentsply Sirona focuses on delivering end to end digital workflows that connect diagnostics with appliance fabrication. Recent strategic moves involve the launch of advanced self ligating bracket systems designed to reduce friction and treatment time. The corporation has also strengthened its European supply chain to ensure consistent availability of critical consumables despite global logistical challenges. By leveraging its vast distribution network, the company ensures that both large clinics and small practices have access to cutting edge technologies. Their ongoing investment in research and development drives innovation in biomaterials, ensuring their products meet the highest clinical standards required by European regulatory bodies.

- Envista Holdings Corporation has emerged as a formidable force in the orthodontics sector following its spin off and subsequent strategic acquisitions. The company houses several iconic orthodontic brands that provide a wide range of fixed and removable appliances to the global market. In Europe, Envista focuses on consolidating its presence by integrating acquired entities to offer a unified and robust product lineup. Recent actions include the introduction of customized bracket systems that utilize digital imaging for precise placement and improved patient comfort. The firm actively participates in major European dental conferences to showcase its latest innovations and build stronger ties with regional key opinion leaders. Envista is also committed to sustainability initiatives within its manufacturing processes, aligning with European environmental regulations. By streamlining operations and focusing on customer centric solutions, the company enhances its ability to respond rapidly to evolving market demands and clinician preferences across diverse European healthcare settings.

Top Strategies Used By Key Market Participants

Key players in the Europe orthodontics market primarily employ aggressive merger and acquisition strategies to consolidate their portfolios and eliminate competition. Companies frequently invest heavily in research and development to introduce innovative materials and digital tools that enhance treatment efficiency. Strategic partnerships with local distributors and dental associations help firms navigate complex regulatory landscapes and penetrate emerging markets effectively. Many participants focus on expanding their digital ecosystems by integrating artificial intelligence and cloud based platforms into their core offerings. Educational initiatives and continuous professional development programs are widely used to build brand loyalty among orthodontists and encourage the adoption of proprietary technologies. Pricing strategies often involve tiered product lines to cater to both premium private clinics and cost sensitive public health sectors. Furthermore, companies are increasingly adopting direct to consumer marketing approaches to raise awareness and drive patient demand for specific aesthetic treatments.

MARKET SEGMENTATION

This research report on the Europe orthodontics market is segmented and sub-segmented into the following categories.

By Product Type

- Instruments

- Supplies

- Fixed

- By Product

- Brackets

- Bands & Buccal Tubes

- Archwires

- Others

- By Type

- Conventional

- Custom

- Removable

- Aligners

- Retainers

- Others

By Age Group

- Teens

- Adults

By End-user

- Dentist & Orthodontist Owned Practices

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

Frequently Asked Questions

What does the orthodontics market include in Europe?

It covers devices and treatments used to correct teeth alignment and jaw positioning.

Why is orthodontic treatment demand increasing across Europe?

Growing awareness of dental aesthetics and oral health is driving more people to seek treatment.

How can orthodontics be explained in simple terms?

It is a branch of dentistry focused on straightening teeth and correcting bite issues.

Which age groups contribute most to this market?

Both teenagers and adults are increasingly opting for orthodontic treatments.

What types of products are commonly used in orthodontics?

Braces, clear aligners, retainers, and related accessories are widely used.

How are clear aligners influencing market growth?

They offer a discreet and comfortable alternative to traditional braces.

What role do dental clinics play in this market?

They are the primary providers of orthodontic consultations and treatments.

How is technology transforming orthodontic solutions?

Digital scanning and 3D printing are improving treatment accuracy and customization.

What challenges affect orthodontic treatment adoption?

High treatment costs and limited insurance coverage can restrict access.

How does cosmetic dentistry impact this market?

Aesthetic preferences are encouraging more adults to pursue orthodontic care.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com