Europe Paver Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Track Pavers, Wheel Pavers, Screeds), Pavement Width, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 To 2034

Europe Paver Market Report Summary

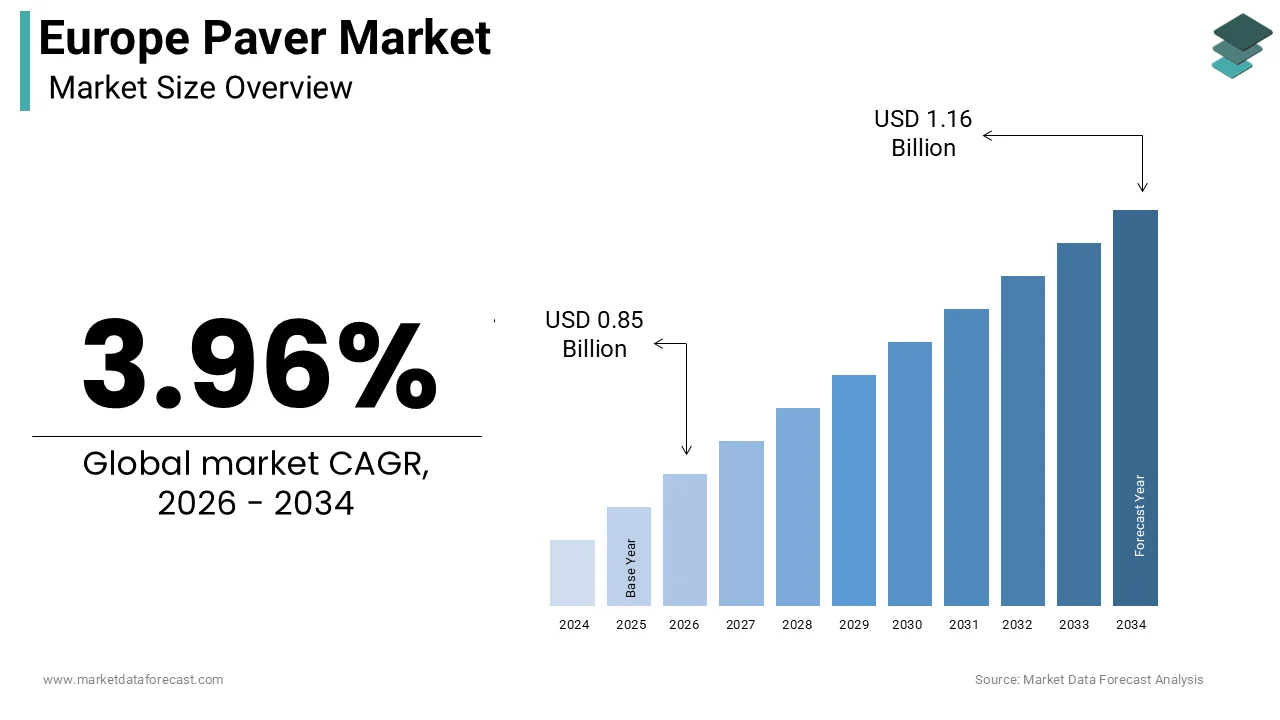

The Europe paver market was valued at USD 0.82 billion in 2025 and is projected to reach USD 1.16 billion by 2034, growing from USD 0.85 billion in 2026 at a CAGR of 3.96% during the forecast period. Market growth is driven by increasing investments in road infrastructure, urban development, and maintenance of existing transportation networks. The rising focus on smart cities, sustainable construction, and durable paving solutions is further supporting the growth of the Europe paver market.

Key Market Trends

- Increasing investment in road repair and maintenance projects

- Growth in urbanization and smart city initiatives

- Rising demand for efficient and high-performance paving equipment

- Expansion of tourism-driven infrastructure development

- Adoption of sustainable and durable paving materials

Segmental Insights

- Based on type, the track paver segment dominated the Europe paver market in 2025 by accounting for 58.4% of the regional market share, driven by better stability and performance on uneven terrain.

- Based on pavement width, the 2.5 to 5 meters segment led the market in 2025 by capturing 45.6% of the total market share, supported by its versatility in urban and highway construction.n

Regional Insights

- Germany led the Europe paver market in 2025 by holding 24.3% of the regional market share, supported by strong infrastructure investment and engineering capabilities.

- France ranked second with 16.4% share in 2025, driven by extensive road networks and urban renewal initiatives.s

- United Kingdom is expected to witness significant growth, supported by aging infrastructure and increased road maintenance spending.

- Italy is projected to grow steadily due to transportation network upgrades and post-disaster reconstruction.n

- Spain is anticipated to expand, driven by urban development and tourism-related infrastructure

Competitive Landscape

- The Europe paver market is moderately competitive, with key players focusing on product innovation, durability, and efficiency. Companies are investing in advanced paving technologies and sustainable construction solutions to meet evolving infrastructure demands.

- Prominent players in the Europe paver market include CRH plc, Holcim Group, Heidelberg Materials, Wienerberger AG, Boral Limited, Marshalls plc, Brett Group, Tobermore, Semmelrock International GmbH, and Barleystone Paving.

Europe Paver Market Size

The Europe paver market size was calculated to be USD 0.82 billion in 2025 and is anticipated to be worth USD 1.16 billion by 2034, from USD 0.85 billion in 2026, growing at a CAGR of 3.96% during the forecast period.

The paver is a diverse range of construction equipment designed for the continuous laying and compaction of asphalt concrete on roadways, bridges, parking lots, and other paved surfaces. These machines are infrastructure assets that ensure the durability, smoothness, and safety of transportation networks across the continent. This substantial economic activity drives the need for advanced paving technologies that can meet stringent performance standards. According to the International Road Federation, Europe maintains one of the densest road networks globally, with over 5 million kilometers of roads requiring regular upkeep and expansion. The European Commission has emphasized the importance of sustainable mobility through its Trans European Transport Network policy, which aims to modernize existing infrastructure to support electric and autonomous vehicles. Furthermore, the shift towards digitalization in construction is evident as manufacturers integrate telematics and automation into pavers to enhance efficiency and reduce material waste. The regulatory landscape is also evolving with stricter emissions standards compelling manufacturers to develop cleaner and more energy-efficient machinery.

MARKET DRIVERS

Extensive Road Maintenance and Rehabilitation Programs

The extensive focus on road maintenance and rehabilitation programs across European nations is majorly propelling the growth of the paver market. Many existing road networks are aging and require significant upgrades to handle increasing traffic volumes and heavier loads. According to the European Court of Auditors, approximately 20% of the main road network in the European Union is in poor or very poor condition, necessitating immediate attention and investment. This assessment has prompted governments to allocate substantial budgets for resurfacing and reconstruction projects. These initiatives create a steady demand for asphalt pavers capable of delivering high quality finishes and efficient operations. Such large-scale projects require a fleet of modern pavers equipped with advanced leveling and compaction technologies to ensure longevity and safety. Additionally, the European Union’s Cohesion Policy provides funding for infrastructure improvements in less developed regions, further stimulating market growth. The emphasis on preventive maintenance rather than reactive repairs also contributes to consistent demand as authorities seek to extend the lifespan of existing assets.

Urbanization and Development of Smart City Infrastructure

The rapid urbanization and the development of smart city infrastructure are also propelling the growth of the Europe paver market. As cities expand and evolve, there is an increasing need for new roads, pedestrian zones, and cycling paths that integrate seamlessly with urban areas. According to the United Nations Department of Economic and Social Affairs, 75% of the European population is expected to live in urban areas by 2030, driving the demand for improved urban mobility solutions. This demographic shift necessitates the construction of high-quality paved surfaces that can accommodate diverse modes of transport, including electric buses and bicycles. Smart city initiatives often involve the integration of sensors and charging infrastructure into roadways, which requires precise paving techniques to ensure proper installation and functionality. The City of Amsterdam launched a comprehensive smart mobility plan in 2025 that includes the creation of 200 kilometers of new dedicated bike lanes and smart roads. These projects require specialized pavers that can handle complex geometries and tight spaces while maintaining high standards of surface quality. Furthermore, the aesthetic appeal of urban spaces is increasingly important, leading to the use of colored and textured asphalt, which demands advanced paving equipment.

MARKET RESTRAINTS

Stringent Environmental Regulations and Emission Standards

The stringent environmental regulations and emission standards, by increasing compliance costs and limiting the use of older machinery, are restricting the growth of Europe paver market. The European Union has implemented rigorous directives aimed at reducing greenhouse gas emissions and air pollution from construction equipment. According to the European Environment Agency, non-road mobile machinery, including pavers, accounts for approximately 5% of nitrogen oxide emissions in Europe prompting tighter controls. The Stage V emission standard, which came into full effect in 2020, requires manufacturers to incorporate advanced exhaust after-treatment systems such as diesel particulate filters and selective catalytic reduction. This financial burden discourages the replacement of older fleets, particularly in regions with limited access to financing. Additionally, the operational complexity of maintaining these advanced emission control systems requires specialized training and services, which may not be readily available in all areas. These regulatory pressures thus act as a barrier to market growth by slowing down the adoption of new technologies and increasing the total cost of ownership for end users.

Volatility in Raw Material Prices and Supply Chain Disruptions

The volatility in raw material prices and ongoing supply chain disruptions, which affect both manufacturers and end users, is another factor degrading the growth of Europe paver market. The production of pavers relies heavily on steel, electronics, and hydraulic components, which are subject to global price fluctuations and availability issues. According to the study, the price of steel increased by 25% in 2024 due to heightened demand and energy costs impacting the manufacturing sector significantly. This surge in input costs forces manufacturers to raise prices, which in turn reduces the purchasing power of construction companies. The supply chain disruptions continued to affect the delivery times of critical components, such as semiconductors and engines, with average delays extending to 8 weeks in 2025. These delays disrupt project schedules and increase inventory holding costs for contractors who rely on timely equipment availability. Furthermore, the geopolitical tensions in Eastern Europe have exacerbated supply chain uncertainties by disrupting trade routes and limiting access to certain raw materials.

MARKET OPPORTUNITIES

Adoption of Electric and Hybrid Paving Technologies

The growing adoption of electric and hybrid paving technologies, as the construction industry shifts towards sustainability, is creating new opportunities for the growth of Europe paver market. Governments and private sector entities are increasingly prioritizing low-carbon construction methods to meet climate goals. According to the European Commission, the Green Deal Industrial Plan aims to accelerate the transition to clean technologies, including the electrification of construction equipment. Electric pavers offer several advantages, such as zero emissions, reduced noise level,s and lower operating costs compared to traditional diesel models. These benefits make electric pavers ideal for urban construction projects where environmental and social impacts are closely monitored. The Norwegian Public Roads Administration mandated the use of zero-emission machinery for all inner-city road works starting in 2025, creating a guaranteed market for electric pavers. Manufacturers are responding by developing innovative battery-powered and hybrid models that offer comparable performance to conventional machines.

Integration of Digitalization and Automation in Paving Operations

The integration of digitalization and automation in paving operations for enhancing efficiency and quality is expected to elevate the growth of the Europe paver market. Advanced technologies such as GPS-guided leveling systems, telematics, and artificial intelligence are transforming how paving projects are executed. Automated pavers can achieve higher precision in layer thickness and slope, ensuring uniform surface quality and extending road lifespan. As per the Dutch Ministry of Infrastructure and Water Management, the use of automated paving systems in highway projects reduced rework rates by 25% in 2024. Telematics solutions enable real-time monitoring of machine performance, fuel consumption, and maintenance needs, allowing for proactive management and cost savings. Furthermore, the use of building information modeling allows for better planning and coordination between different stages of construction, minimizing delays and errors. The Austrian Chamber of Commerce noted that companies investing in digital paving technologies reported a 10% increase in profit margins due to improved operational efficiency.

MARKET CHALLENGES

Shortage of Skilled Labor and Technical Expertise

The shortage of skilled labor and technical expertise, as modern machines become increasingly complex and technology-driven, is one of the challenges for the growth of Europe paver market. Operating and maintaining advanced pavers requires specialized knowledge in hydraulics, electronics, and software systems, which is not widely available in the current workforce. According to the European Centre for the Development of Vocational Training, the construction sector faces a deficit of 1.5 million skilled workers across the European Union by 2025. This labor gap affects the ability of construction firms to operate new equipment efficiently and safely. As per the German Construction Confederation, 60% of companies reported difficulties in finding qualified machine operators in 20,24 leading to project delays and increased labor costs. The aging workforce exacerbates this issue as experienced operators retire without sufficient replacements entering the field. Furthermore, the rapid pace of technological change requires continuous upskilling, which many employers struggle to provide.

High Initial Investment and Maintenance Costs

The high initial investment and maintenance costs associated with advanced pavers for many construction companies, particularly small and medium-sized enterprises, are also acting as a barrier for the growth of Europe paver market. Modern pavers equipped with digital and emission control technologies are substantially more expensive than their predecessors. This price escalation makes it difficult for smaller firms to upgrade their fleets or enter the market. Additionally, the maintenance of sophisticated systems such as electronic leveling and exhaust after treatment requires specialized services and genuine parts, which are costly and sometimes scarce. These financial burdens force many companies to extend the life of outdated equipment, which may not meet current environmental or performance standards. The lack of accessible financing options further compounds the problem, limiting the ability of firms to invest in modern technology.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.96% |

| Segments Covered | By Type, Pavement Width, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | CRH plc, Holcim Group, Heidelberg Materials, Wienerberger AG, Boral Limited, Marshalls plc, Brett Group, Tobermore, Semmelrock International GmbH, Barleystone Paving |

SEGMENTAL ANALYSIS

By Type Insights

The track paver segment accounted in holding 58.4% of the Europe paver market share in 2025. The track pavers are preferred for major highway and arterial road construction due to their ability to distribute weight evenly and maintain stability on uneven or soft substrates. According to the study, over 70% of highway rehabilitation projects in Europe utilize track pavers to ensure consistent mat quality and density. The continuous contact area of tracks minimizes ground pressure, preventing sinkage and ensuring a smooth paving surface even in challenging soil conditions. These machines can handle wider paving widths and thicker lifts required for high traffic volumes, making them indispensable for national road networks. Furthermore, the robust design of track pavers allows them to operate effectively in adverse weather conditions, which are common in Northern and Central Europe. The Swedish Transport Administration noted that track pavers maintained operational efficiency during winter maintenance projects where ground stability was compromised. This reliability ensures project timelines are met, reducing costly delays and reinforcing the dominance of track pavers in the heavy construction sector.

The wheel paver segment is expected to grow at an anticipated CAGR of 6.5% from 2026 to 2034. Wheel pavers are gaining popularity in urban construction due to their superior mobility and ease of transport between job sites. According to the United Nations Department of Economic and Social Affairs, 75% of Europeans will live in urban areas by 2030, driving the need for efficient city infrastructure maintenance. Wheel pavers allow contractors to quickly move between multiple small-scale projects such as parking lots, residential streets, and bike paths. The compact size and lighter weight reduce the need for extensive site preparation and logistical support. This efficiency translates to lower labor costs and faster project completion times. Furthermore, wheel pavers cause less vibration and noise, which is crucial for working in densely populated areas with strict environmental regulations.

By Pavement Width Insights

The pavement width segment of 2.5 to 5 meters was the largest, holding 45.6% of the Europe paver market share in 2025. The extensive network of urban and suburban roads in Europe drives the dominance of the 2.5 to 5 meter pavement width segment. Most city streets, residential avenues, and secondary roads fall within this width category, requiring pavers that can efficiently handle these dimensions. The vast infrastructure base requires regular maintenance, resurfacing, and occasional widening to accommodate growing traffic. This consistency in road design standards ensures steady demand for pavers in this category. Furthermore, the modular nature of many pavers allows them to adjust within this range, providing flexibility for varying lane widths without requiring multiple machines.

The pavement width segment of more than 5 meters is likely to witness the fastest CAGR of 7.2% from 2026 to 2034. The expansion of multi-lane highway infrastructure is a primary driver for the rapid growth of the more than 5-meter pavement width segment. Governments are investing heavily in widening existing highways and constructing new multi-lane corridors to alleviate congestion and improve connectivity. Large-width pavers enable the simultaneous laying of multiple lanes, reducing construction time and minimizing traffic disruptions. Furthermore, the ability to pave wide sections without longitudinal joints improves road durability and ride quality.

REGIONAL ANALYSIS

Germany Paver Market Analysis

Germany was the largest contributor in the Europe paver market by holding 24.3% of the share in 2025. The country’s robust automotive industry and extensive highway network drive the demand for high quality paving equipment. According to the German Federal Ministry for Digital and Transport, the federal government has allocated 10 billion euros annually for road infrastructure maintenance and expansion through 2030. This substantial investment supports the procurement of advanced track and wheel pavers for nationwide projects. The presence of major construction machinery manufacturers, such as Wirtgen Group and Hamm AG, fosters innovation and local supply chain strength. The country’s focus on sustainable construction practices encourages the adoption of energy-efficient and low-emission pavers. The German Environment Agency reported that the use of warm mix asphalt technologies facilitated by modern pavers reduced energy consumption by 20% in 2024. Furthermore, the rigorous quality standards imposed by German authorities ensure that only high-performance equipment is used in public projects. The strong vocational training system provides a skilled workforce capable of operating and maintaining sophisticated paving machinery.

France Paver Market Analysis

France paver market held the second position by holding 16.4% of share in 2025, with the extensive road network and ongoing urban renewal initiatives fueling the demand for versatile paving solutions. According to the French Ministry of the Interior, local authorities invested 15 billion euros in road maintenance in 2024, prioritizing urban and suburban infrastructure. The presence of leading equipment distributors and service providers enhances market accessibility and support. The government’s commitment to sustainable mobility through the Climate and Resilience Law encourages the use of eco-friendly paving methods. Furthermore, the preparation for major international events such as the Olympics has accelerated infrastructure upgrades in key cities.

United Kingdom Paver Market Analysis

The United Kingdom paver market growth is likely to have prominent growth opportunities in the coming years, with the aging population and significant investment in road repairs driving the demand for reliable paving equipment. According to the Department for Transport, the UK government announced a 2 billion pound fund for pothole repairs and local road maintenance in 2024. This initiative creates substantial demand for wheel pavers suitable for urban and local road applications. The presence of established construction firms and equipment rental companies facilitates access to modern paving technologies. The Office for Zero Emission Vehicles reported that pilot projects for electric construction machinery received 50 million pounds in funding in 2024. Furthermore, the devolved administrations in Scotland, Wales, and Northern Ireland have their own infrastructure investment plans contributing to regional market growth.

Italy Paver Market Analysis

Italy's paving market growth is driven by its transport network, and the recovery from natural disasters drives the demand for paving equipment. According to the Italian Ministry of Infrastructure and Transport, the National Recovery and Resilience Plan includes 25 billion euros for infrastructure development, with a significant portion for road improvements. This funding supports the procurement of advanced pavers for highway and urban projects. The presence of domestic manufacturers and distributors strengthens the local supply chain. The country’s vulnerability to earthquakes and floods necessitates frequent road reconstruction, creating a steady demand for resilient paving solutions. Furthermore, the tourism sector’s reliance on accessible transport networks encourages the continuous maintenance of scenic and coastal roads.

Spain Paver Market Analysis

Spain's paving market growth is driven by expanding urban centers and tourism-driven infrastructure needs, which fuel the demand for paving equipment. According to the Spanish Ministry of Transport, Mobility and Urban Agenda, the Strategic Infrastructure Plan allocates 18 billion euros for road network improvements through 2026. This investment focuses on enhancing connectivity between major cities and tourist destinations. The presence of active construction sectors in Madrid, Barcelona, and Valencia drives local demand. The country’s climate conditions require durable road surfaces capable of withstanding high temperatures and heavy traffic. Furthermore, the expansion of high-speed rail networks often involves concurrent road upgrades to improve intermodal connectivity.

COMPETITION OVERVIEW

The competition in the Europe paver market is characterized by intense rivalry among established global manufacturers and specialized regional providers. Companies compete primarily on technological innovation, product reliability, and after-sales service capabilities. The presence of major players such as Wirtgen Group Volvo, and Dynapac creates a consolidated market structure where brand reputation and engineering excellence are critical success factors. New entrants face significant barriers due to high capital requirements and complex regulatory standards. Competitive dynamics are further influenced by the rapid adoption of digital technologies and automation, which require continuous investment in research and development. Price competition remains moderate as customers prioritize long-term value and performance over initial cost. Strategic alliances and mergers are frequently employed to expand market reach and enhance technological capabilities. The focus on sustainability and energy efficiency also differentiates competitors as manufacturers seek to comply with stringent environmental regulations.

KEY MARKET PLAYERS

A few major players of the Europe paver market include

- CRH plc

- Holcim Group

- Heidelberg Materials

- Wienerberger AG

- Boral Limited

- Marshalls plc

- Brett Group

- Tobermore

- Semmelrock International GmbH

- Barleystone Paving

Top Strategies Used by the Key Market Participants

Key players in the Europe paver market primarily focus on product innovation and technological advancement to maintain a competitive advantage. Companies invest heavily in research and development to create automated and digitalized paving solutions that enhance efficiency and precision. Strategic partnerships with technology firms are common to integrate artificial intelligence and Internet of Things capabilities into machinery. Expansion of service networks and after-sales support infrastructure helps firms enhance customer retention and satisfaction. Many participants pursue sustainability initiatives by developing electric and hybrid models that align with environmental regulations. Acquisitions of smaller specialized companies allow larger players to broaden their product portfolios and access new markets. Digitalization strategies, including remote monitoring and predictive maintenance, are increasingly adopted to optimize machine performance. These approaches enable manufacturers to meet evolving customer demands while improving operational efficiency and reducing the total cost of ownership for end users in diverse construction sectors.

Leading Players in the Market

- Wirtgen Group stands as a global leader in road construction technology with a significant presence in the Europe paver market. The company offers a comprehensive portfolio of asphalt pavers known for their precision, durability, and advanced automation features. Wirtgen contributes to the global market by setting industry standards for paving quality and efficiency through continuous innovation. Recent actions include the launch of new generation pavers equipped with intelligent machine control systems that optimize material usage and surface evenness. The firm has also expanded its digital services platform, allowing customers to monitor fleet performance and schedule maintenance remotely. These initiatives strengthen its market position by enhancing customer value and operational efficiency. Wirtgen remains committed to sustainability by developing machines that support low-temperature asphalt applications, reducing energy consumption and emissions. This strategic focus ensures its continued leadership in the competitive European landscape.

- Volvo Construction Equipment is a major player in the Europe paver market, renowned for its robust and reliable paving solutions. The company provides a wide range of asphalt pavers designed to meet diverse project requirements from urban repairs to highway construction. Volvo contributes globally by leveraging its extensive distribution network and strong brand reputation for quality and safety. Recent efforts to strengthen its position include the introduction of electric compact pavers aimed at reducing carbon footprints in urban environments. The company has also integrated advanced telematics systems into its equipment, enabling real-time data analysis and predictive maintenance. These technological advancements improve uptime and reduce the total cost of ownership for clients. Volvo actively collaborates with contractors to develop customized solutions that address specific challenges in road construction. Its commitment to innovation and sustainability reinforces its status as a preferred partner in the European market.

- Dynapac is a key contributor to the Europe paver market, offering high-performance asphalt pavers and compaction equipment. The company focuses on delivering efficient and user-friendly solutions that enhance productivity and improve quality. Dynapac plays a vital role in the global market by providing specialized technologies for complex paving applications. Recent actions to bolster its market position include the development of modular paver concepts that allow for easy adaptation to various job site conditions. The firm has also invested in research and development to improve fuel efficiency and reduce noise levels in its machines. Dynapac emphasizes customer support through comprehensive training programs and responsive service networks. These initiatives ensure that operators can maximize the potential of their equipment.

MARKET SEGMENTATION

This research report on the Europe paver market has been segmented and sub-segmented based on type, pavement width & region.

By Type

- Track pavers

- Wheel pavers

- Screeds

By Pavement Width

- Less than 2.5 Meters

- 2.5 – 5 Meters

- More than 5 Meters

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What are the key drivers of the Europe paver market?

Major drivers include urbanization, rising infrastructure projects, increasing demand for aesthetically appealing outdoor spaces, and renovation activities.

2. Which materials are commonly used in pavers?

Common materials include concrete, natural stone, clay brick, and porcelain.

3. Which segment dominates the market by material type?

Concrete pavers dominate the market due to their cost-effectiveness, durability, and versatility.

4. What are the major applications of pavers in Europe?

Key applications include residential landscaping, commercial construction, public infrastructure, and industrial flooring.

5. What role does urbanization play in market growth?

Urbanization increases demand for roads, sidewalks, and public spaces, thereby boosting the use of pavers.

6. What are the key trends in the Europe paver market?

Trends include the adoption of eco-friendly permeable pavers, innovative designs, and digital manufacturing technologies.

7. What are permeable pavers and why are they important?

Permeable pavers allow water to pass through, reducing runoff and supporting sustainable urban drainage systems.

8. What challenges does the market face?

Challenges include high installation costs, fluctuating raw material prices, and environmental regulations.

9. How is sustainability influencing the market?

Sustainability is driving demand for recycled materials, low-carbon manufacturing processes, and water-permeable paving solutions.

10. What is the future outlook for the Europe paver market?

The market is expected to witness steady growth driven by infrastructure investments, smart city projects, and increasing demand for sustainable construction materials.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com