Europe Planters Market Size, Share, Trends, & Growth Forecast Report By End-User (Residential, Commercial), Distribution Channel and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Planters Market Report Summary

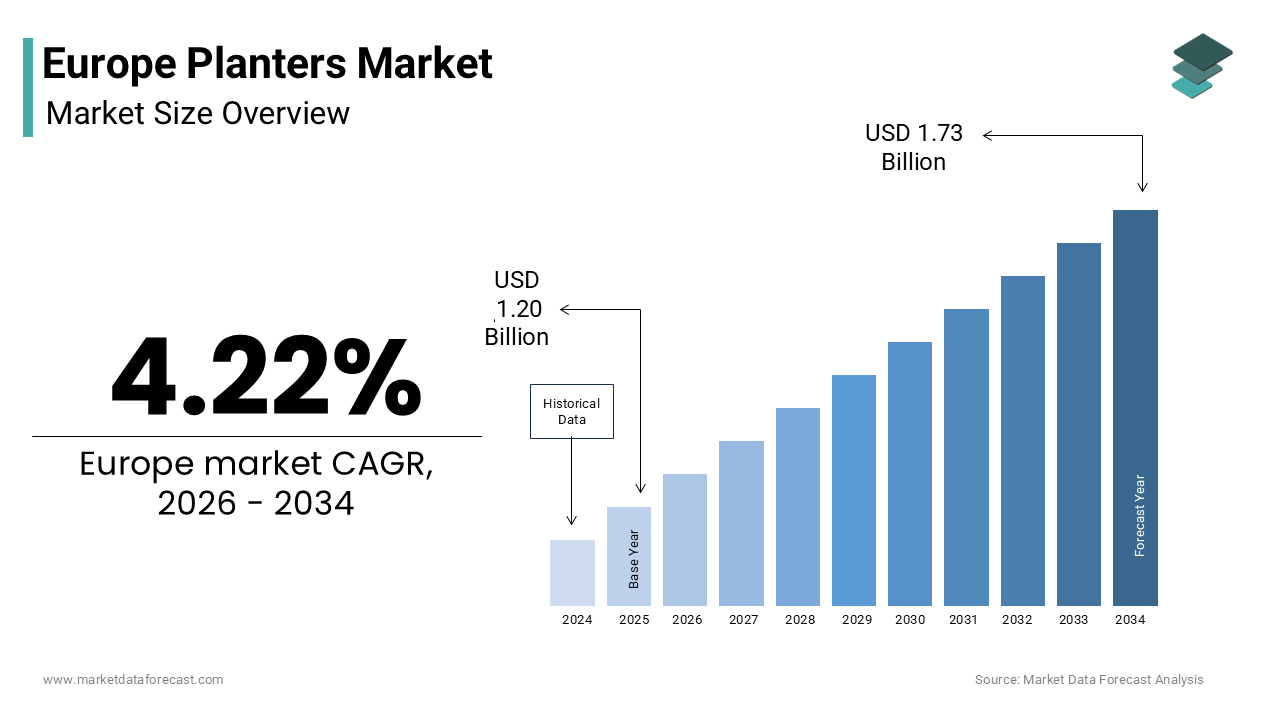

The Europe planters market was valued at USD 1.20 billion in 2025, is estimated to reach USD 1.25 billion in 2026, and is projected to reach USD 1.73 billion by 2034, growing at a CAGR of 4.22% during the forecast period from 2026 to 2034. The growth of the Europe planters market is driven by increasing urbanization, rising interest in home gardening, and growing investments in urban green infrastructure across European cities. In addition, the demand for decorative gardening solutions for balconies, terraces, and indoor spaces is expanding rapidly. Sustainability initiatives encouraging the use of recycled materials and biodegradable products are also shaping the market landscape. Furthermore, the growing popularity of smart planters integrated with moisture sensors and automated irrigation systems is transforming traditional gardening practices and creating new growth opportunities.

Key Market Trends

-

Increasing adoption of vertical gardening systems in urban environments due to limited gardening space.

-

Rising consumer preference for eco-friendly planters made from recycled plastics, biodegradable materials, and reclaimed wood.

-

Growing popularity of smart planters with automated watering and sensor-based monitoring systems.

-

Expanding investments in urban green infrastructure projects including rooftop gardens and public landscaping initiatives.

-

Increasing demand for decorative and designer planters is driven by home improvement and interior decoration trends.

Segmental Insights

Based on end user, the residential segment was the largest and held a significant share of the Europe planters market in 2025. The segment’s dominance is attributed to the strong gardening culture across Europe, increasing interest in balcony gardening in urban apartments, and the growing trend of home landscaping and decoration.

Based on distribution channel, the offline segment accounted for the largest share of the Europe planters market in 2025. The growth of this segment is driven by the presence of extensive networks of garden centers, nurseries, and home improvement stores where customers prefer to physically inspect planters before purchasing.

The online segment is expected to register the fastest CAGR during the forecast period due to increasing digitalization of retail, growing e-commerce platforms for home and garden products, and the convenience of home delivery for bulky gardening equipment.

Regional Insights

The Europe planters market is witnessing steady growth across several countries supported by rising gardening activities, urban greening initiatives, and increasing consumer spending on home improvement.

-

Germany was the largest contributor, accounting for 23.6% of the Europe planters market share in 2025, driven by its strong gardening culture, widespread use of allotment gardens, and increasing adoption of sustainable gardening products.

-

The United Kingdom holds a significant share due to the country’s rich gardening tradition and high demand for decorative outdoor products for residential gardens.

-

France is witnessing strong demand for planters due to increasing urban balcony gardening and government initiatives promoting green cities and rooftop gardens.

-

Italy continues to maintain steady demand supported by its outdoor lifestyle culture and the widespread use of traditional terracotta planters in residential and hospitality settings.

-

The Netherlands is emerging as a fast-growing market driven by its advanced horticulture industry and adoption of innovative smart gardening technologies.

Competitive Landscape

The Europe planters market is highly competitive with the presence of both large manufacturers and specialized design-oriented brands competing through innovation, sustainability initiatives, and product aesthetics. Companies are focusing on developing eco-friendly materials, self-watering planter systems, and smart gardening technologies to attract modern urban consumers. Strategic partnerships with retailers, garden centers, and e-commerce platforms are helping companies expand their distribution networks across the region. In addition, product differentiation through innovative designs, durability, and customization is becoming a key competitive factor in the market. Prominent players in the Europe planters market include Lechuza, Elho, Scheurich, Teraplast, Ecopots, Crescent Garden, Deroma, Lechuza by United Pet Group, Bloem Living, and Keter Group.

Europe Planters Market Size

The Europe planters market size was valued at USD 1.20 billion in 2025 and is anticipated to reach USD 1.25 billion in 2026 from USD 1.73 billion by 2034, growing at a CAGR of 4.22% during the forecast period from 2026 to 2034.

Planters encompasses a diverse array of containers designed for cultivating ornamental plants, vegetables, and herbs across residential, commercial, and public sectors within the continent. This industry includes products ranging from traditional terracotta pots and wooden boxes to modern self-watering systems and vertical gardening structures made from recycled polymers or composite materials. The definition extends beyond simple vessels to include smart planters integrated with sensors for moisture and nutrient monitoring, which is reflecting a shift towards technology-enabled urban agriculture. According to Eurostat, a large majority of the European population resides in urban areas, creating a profound need for green spaces that improve air quality and mental well-being in densely populated cities. Furthermore, as per the European Environment Agency, urban vegetation plays an important role in mitigating heat island effects, prompting municipal authorities to invest in street planters and green infrastructure projects. Unlike generic gardening supplies, this market is increasingly driven by sustainability mandates, with the European Commission encouraging the use of circular economy principles in product design. Consequently, manufacturers are prioritizing biodegradable materials and recycled plastics to align with the Green Deal objectives. The market serves not only individual homeowners seeking aesthetic enhancement but also landscape architects and city planners dedicated to transforming concrete jungles into vibrant ecological hubs through strategic deployment of functional and durable planting solutions.

MARKET DRIVERS

Rapid Urbanization and the Expansion of Vertical Gardening Initiatives

The accelerating pace of urbanization across Europe is majorly propelling the growth of the European planters market, which is driving demand for space efficient solutions like vertical gardens and rooftop containers. As cities become denser, the availability of horizontal ground space for traditional gardening diminishes, forcing residents and developers to look upwards for greenery integration. According to the United Nations Economic Commission for Europe, the urban population in the region is projected to increase significantly by 2050, intensifying the pressure on city planners to incorporate nature into built environments. This demographic shift has spurred the popularity of vertical planter systems that allow for high density planting on balconies, walls, and facades without consuming valuable floor area. Municipalities are increasingly mandating green roofs and living walls in new construction projects to comply with environmental regulations and improve biodiversity. As per the European Green Building Council, buildings equipped with vertical greening systems demonstrate improvements in thermal insulation and stormwater management, providing economic incentives alongside ecological benefits. The rise of urban farming movements further fuels this trend, with communities utilizing modular planters to grow food locally in shared spaces. This convergence of spatial constraints, regulatory support, and environmental awareness ensures a robust and growing demand for innovative planter designs tailored to vertical applications.

Growing Consumer Preference for Sustainable and Eco-Friendly Materials

The shifting consumer consciousness towards sustainability and the preference for products made from eco-friendly or recycled materials is further boosting the Europe planters market expansion. European consumers are increasingly scrutinizing the lifecycle of gardening products, favoring planters constructed from bioplastics, reclaimed wood, or recycled ocean plastics over traditional virgin petroleum based polymers. According to the European Commission, the Circular Economy Action Plan aims to make sustainable products the norm in the EU, influencing purchasing decisions across all sectors including home and garden. This regulatory and cultural push has led manufacturers to innovate with biodegradable pots that decompose naturally and reduce waste accumulation in landfills. As per the European Consumer Organisation, many shoppers are willing to pay a premium for goods that demonstrably reduce environmental impact, driving brands to highlight their green credentials. The adoption of the Single Use Plastics Directive has further accelerated the transition away from non-recyclable materials, forcing companies to reengineer their product lines. Additionally, the rise of organic gardening practices aligns perfectly with the use of natural fiber planters that do not leach harmful chemicals into the soil. This deep-seated commitment to environmental stewardship transforms sustainability from a niche feature into a core market requirement, sustaining long term growth for eco conscious manufacturers.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

The Europe planters market faces a significant restraint due to the volatility of raw material prices, particularly for plastics, metals, and ceramics, which constitute the bulk of manufacturing costs. Fluctuations in global energy prices directly impact the cost of producing polymer-based planters, while supply chain bottlenecks delay the availability of essential inputs like resin and clay. According to the European Chemical Industry Council, energy costs for chemical production have increased in recent years, forcing manufacturers to either absorb margins or pass increased costs onto consumers, thereby dampening demand. The reliance on imported raw materials from outside the continent exposes the industry to geopolitical tensions and logistical challenges that can disrupt production schedules. As per the European Central Bank, inflationary pressures on industrial producer prices have made it difficult for small and medium sized enterprises to maintain competitive pricing while ensuring quality. Furthermore, the scarcity of recycled plastic feedstock, despite high collection rates, creates a bottleneck for companies committed to circular economy goals, limiting their ability to scale sustainable product lines. These economic uncertainties lead to hesitation among retailers and consumers alike, who may delay purchases or opt for cheaper, lower quality alternatives. The instability in input costs thus acts as a persistent brake on market expansion, complicating long term planning and investment in new capacity.

Stringent Regulatory Compliance and Waste Management Standards

The implementation of rigorous environmental regulations and waste management standards acts as a complex restraint on the Europe planters market by increasing compliance burdens and operational costs for manufacturers. Producers must navigate a labyrinth of directives concerning material safety, recyclability, and end of life disposal, which often vary between member states, creating fragmentation in the single market. According to the European Environment Agency, the Extended Producer Responsibility schemes require companies to finance the collection and recycling of their products, adding a significant financial layer to the business model. Non compliance with these regulations can result in hefty fines and reputational damage, deterring smaller players from entering or expanding in the market. As per the European Committee for Standardization, meeting specific norms for durability and chemical leaching requires extensive testing and certification processes that prolong time to market. The ban on certain single use plastics and the push for fully biodegradable options force companies to invest heavily in research and development to reformulate existing products. While these measures are environmentally beneficial, they create high barriers to entry and increase the total cost of ownership for producers. This regulatory complexity slows down innovation cycles and limits the variety of products available, as companies prioritize compliance over experimentation with new designs or materials.

MARKET OPPORTUNITIES

Integration of Smart Technology and IoT in Urban Gardening Solutions

The convergence of Internet of Things technology with traditional gardening presents a promising opportunity for the Europe planters market through the development of smart planters equipped with sensors and automated irrigation systems. These advanced containers can monitor soil moisture, light levels, and nutrient content in real time, transmitting data to smartphones to optimize plant health and reduce water wastage. According to the Fraunhofer Institute, the adoption of smart home technologies in Europe is accelerating, creating fertile ground for intelligent gardening products. This technological integration appeals to urban dwellers who lack gardening expertise but desire the benefits of home grown produce and greenery. As per the European Innovation Council, funding for agritech startups focusing on urban solutions has increased, driving innovation in autonomous care systems that adjust watering schedules based on weather forecasts. The opportunity extends to commercial applications where large-scale smart planter networks can manage urban green infrastructure efficiently, reducing maintenance costs for municipalities. Furthermore, the ability to collect data on plant growth patterns offers valuable insights for agricultural research and personalized gardening advice. By bridging the gap between technology and nature, manufacturers can create high value products that command premium pricing and foster brand loyalty among tech savvy consumers.

Expansion of Community Gardening and Public Green Infrastructure Projects

The growing emphasis on community well-being and social cohesion offers a lucrative avenue for the Europe planters market through the expansion of public gardening initiatives and shared green spaces. Governments and local authorities are increasingly investing in community gardens, pocket parks, and therapeutic landscapes to foster social interaction and improve mental health among citizens. According to the World Health Organization Regional Office for Europe, access to green spaces is linked to reduced stress levels and improved physical activity, prompting cities to allocate budgets for public planting installations. This trend creates a substantial demand for durable, large capacity, and vandal resistant planters suitable for high traffic public areas. As per the European Urban Initiative, many cities have launched programs to transform underutilized urban plots into vibrant community hubs, requiring modular and flexible planting units. The rise of edible landscaping in public zones further drives the need for food safe and aesthetically pleasing containers that encourage citizen participation in food production. Additionally, corporate social responsibility initiatives are leading businesses to sponsor green corners in urban centers, utilizing branded planters to enhance their image. This shift towards communal and public greening projects diversifies the customer base beyond individual consumers, opening up large volume contracts for manufacturers capable of delivering robust and scalable solutions.

MARKET CHALLENGES

Impact of Climate Change on Plant Viability and Product Durability

The increasing unpredictability of weather patterns due to climate change that affects both the viability of plants and the durability of the containers themselves is a significant challenge to the growth of the Europe planters market. Extreme weather events such as prolonged droughts, intense heatwaves, and heavy flooding place immense stress on outdoor planters, leading to higher rates of product failure and plant mortality. According to the European Environment Agency, the frequency of extreme weather phenomena has risen, causing materials like plastic to degrade faster under intense UV radiation and wooden planters to rot or warp due to excessive moisture. This environmental volatility forces manufacturers to engineer more resilient products capable of withstanding harsh conditions, which often increases production costs and complexity. As per meteorological services across the continent, shifting hardiness zones are altering the types of plants that can survive in specific regions, requiring consumers to frequently replace vegetation and adapt their gardening strategies. The risk of crop failure in edible planters may discourage potential buyers from investing in urban farming setups. Furthermore, the need for specialized features like enhanced drainage for flood prevention or insulation for heat protection adds to the design challenges. Adapting to these climatic realities requires continuous innovation and investment, posing a significant hurdle for companies striving to maintain product relevance and performance.

Logistical Complexities and High Transportation Costs for Bulky Items

The Europe planters market grapples with significant logistical challenges and elevated transportation costs inherent to shipping bulky, heavy, and often fragile items across diverse geographical regions. Planters, especially those made from ceramic, stone, or large volumes of soil filled composites, occupy substantial space and weight, leading to inefficient load utilization and higher freight expenses. According to the European Logistics Association, rising fuel prices and driver shortages have exacerbated transport costs, squeezing margins for manufacturers and retailers who rely on cross border distribution networks. The fragmentation of the European market with varying national regulations on road transport and emissions further complicates supply chain optimization. As per the International Road Transport Union, the cost of moving heavy goods within the EU has increased, making it difficult for producers to offer competitive pricing while maintaining profitability. Additionally, the risk of damage during transit for fragile materials like terracotta or glass necessitates expensive packaging and insurance, adding to the final consumer price. The push for localized production to reduce carbon footprints conflicts with the economies of scale achieved by centralized manufacturing, creating a strategic dilemma. These logistical hurdles limit market reach, particularly for smaller artisans and regional brands, and can deter online sales where shipping costs often outweigh the product value.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.22% |

| Segments Covered | By End User, Distribution Channel and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | AGCO Corporation, Deere & Company, CNH Industrial N.V., Kubota Corporation, Väderstad AB, AMAZONE (AMAZONEN-Werke H. Dreyer GmbH & Co. KG), LEMKEN GmbH & Co. KG, Pöttinger Landtechnik GmbH, Maschio Gaspardo S.p.A., Kuhn Group, HORSCH Maschinen GmbH, Monosem Inc., SLY Agri, and Kverneland Group. |

SEGMENTAL ANALYSIS

By End User Insights

The residential segment led the market by capturing the highest share of the Europe planters market in 2025. The dominance of residential segment in the European planters market is driven by the deeply ingrained culture of home gardening and the increasing desire for personal green sanctuaries among European households and the widespread ownership of private gardens, balconies, and terraces, particularly in nations like Germany and the United Kingdom, where outdoor living is a cherished lifestyle component. According to Eurostat, many households in the European Union have access to private outdoor spaces, creating a vast installed base for decorative and functional planters. The post-pandemic shift towards home improvement has further amplified this trend, with consumers investing heavily in beautifying their immediate surroundings to enhance mental well being and property value. As per the European Garden Industry Association, sales of gardening products for home use have seen sustained growth, with planters being a fundamental purchase for both novice and experienced gardeners. The rise of urban balcony gardening in densely populated cities also contributes significantly, as residents utilize compact and vertical planters to grow herbs and flowers in limited spaces. Furthermore, the seasonal tradition of replanting flower boxes and pots ensures a consistent replacement cycle, driving recurring revenue. This deep cultural connection to nature at the home level, combined with the tangible benefits of private greenery, solidifies the residential sector as the undisputed leader in market volume.

The commercial segment is a promising segment and is expected to witness the fastest CAGR of 10.6% over the forecast period owing to the aggressive adoption of biophilic design principles in corporate offices, retail spaces, hotels, and public infrastructure across the continent. The rising recognition by businesses and municipalities that integrating greenery improves employee productivity, customer satisfaction, and air quality that is leading to substantial investments in large scale interior and exterior landscaping is further contributing to the expansion of the commercial segment in the European market. According to the World Green Building Council, buildings incorporating biophilic elements report improvements in occupant health and cognitive function, prompting facility managers to prioritize extensive planter installations. The expansion of hospitality and tourism sectors in Southern Europe also drives demand for aesthetic, high durability planters that enhance the visual appeal of resorts and restaurants. As per the European Facility Management Network, spending on soft services including landscape maintenance has increased, with a specific focus on modular and smart planter systems that reduce long term upkeep costs. Additionally, municipal projects aimed at creating pedestrian friendly zones and urban parks are utilizing commercial grade planters as street furniture to define spaces and manage traffic flow. This convergence of health trends, corporate responsibility, and urban planning initiatives propels the commercial segment to outpace residential growth rates.

By Distribution Channel Insights

The offline segment dominated the market by holding the major share of the Europe planters market in 2025. The growth of the offline segment in the European market can be credited to the tactile nature of the product and the consumer preference for physically inspecting quality before purchase. Planters vary significantly in material texture, weight, color accuracy, and structural integrity, factors that are difficult to assess accurately through digital images alone. The primary driver for this dominance is the extensive network of specialized garden centers, nurseries, and home improvement stores across Europe that offer expert advice and immediate product availability. According to the European DIY Retail Association, physical stores remain the preferred shopping destination for gardening enthusiasts who value the ability to touch and feel materials like terracotta, wood, and stone. These retailers often provide value added services such as delivery, assembly, and planting advice, which enhances the customer experience and builds loyalty. As per national retail federations, the majority of high value and bulky planter transactions still occur in brick-and-mortar locations where logistics are managed locally. Furthermore, the impulse buying behavior associated with seasonal gardening displays in physical stores drives significant volume during spring and summer months. The trust established through face-to-face interactions with knowledgeable staff also plays a crucial role in guiding consumers towards premium and specialized products. This combination of sensory evaluation, service integration, and immediate gratification ensures that offline channels remain the backbone of planter distribution.

The online segment is estimated to register a CAGR of 11.4% over the forecast period in the European planters market due to the rapid digitalization of retail and the convenience of home delivery for heavy items and the improving logistics infrastructure and the emergence of specialized e-commerce platforms dedicated to home and garden products that offer wide varieties and competitive pricing. A major factor is the changing consumer behavior, particularly among younger demographics who prefer researching and purchasing goods digitally without the need to visit physical stores. According to Eurostat, the proportion of individuals in the European Union ordering goods online has reached record highs, with gardening supplies becoming an increasingly popular category. The development of advanced packaging solutions that ensure the safe transit of fragile and bulky planters has mitigated previous concerns about damage during shipping. As per the European E commerce Association, the availability of detailed product descriptions, customer reviews, and augmented reality tools that allow users to visualize planters in their spaces has enhanced confidence in online purchases. Furthermore, the rise of direct-to-consumer brands bypassing traditional retailers offers unique and customizable designs that attract niche markets. The convenience of doorstep delivery, especially for heavy soil filled units, appeals to urban dwellers lacking transport, accelerating the shift towards digital procurement.

REGIONAL ANALYSIS

Germany Planters Market Analysis

Germany dominated the planters market in Europe in 2025 by accounting for 23.6% of the regional market share. The dominating position of Germany in the European market is driven by its robust gardening culture, high disposable income, and strong emphasis on environmental sustainability. The country's market status is defined by the concept of "Schrebergarten" or allotment gardens, which are immensely popular and create a perpetual demand for high quality planting containers. The primary driver for this dominance is the deep rooted tradition of horticulture, where millions of Germans actively engage in gardening as a leisure activity, supported by a dense network of specialized nurseries and garden centers. According to the Federal Statistical Office of Germany, expenditure on home and garden products remains consistently high, with planters being a staple purchase for maintaining these extensive green spaces. Furthermore, the German commitment to the Circular Economy has spurred demand for planters made from recycled materials and sustainable sources, pushing manufacturers to innovate. As per the German Horticultural Society, the number of active gardeners has grown, including a surge in young urbanites practicing balcony gardening. The presence of leading European planter manufacturers within Germany also strengthens the supply chain, ensuring availability of diverse and durable products. This synergy of cultural passion, economic strength, and ecological awareness secures Germany's position as the most influential market in the region.

United Kingdom Planters Market Analysis

The United Kingdom was another regional segment in the Europe planters market in 2025 and held a promising share of the European market. The growth of the UK in the European market is attributed to a vibrant gardening heritage, a thriving housing market that prioritizes outdoor aesthetics and the iconic British love for flowers and gardens, evident in events like the Chelsea Flower Show which sets global trends for planter designs and planting schemes. A key factor driving demand is the high rate of home ownership and the cultural significance of the private garden as an extension of the living space. According to the Office for National Statistics, many UK households have access to a garden, fostering a consistent market for decorative and functional planters. The rise of "grow your own" movements, accelerated by recent economic pressures, has led to increased sales of vegetable planters and grow bags for domestic food production. As per the Horticultural Trades Association, gardening remains the most popular hobby in the nation, driving steady retail sales throughout the year. Additionally, the trend towards urbanization has boosted the market for compact and vertical planters suitable for city apartments and small courtyards. The combination of traditional gardening values and modern urban adaptations ensures the UK remains a critical and dynamic market for planter manufacturers.

France Planters Market Analysis

France is anticipated to secure a prominent share of the Europe planters market in 2025. The growth of France in the European market can be credited to its rich agricultural history, strong landscape architecture sector, the cultural importance of outdoor living and a blend of traditional rustic styles and modern contemporary designs, reflecting the diverse aesthetic preferences of its population. The principal driver for this market position is the prevalence of balconies and terraces in French urban architecture, particularly in cities like Paris, where ground level gardening space is scarce. According to the National Institute of Statistics and Economic Studies, a large portion of the urban population resides in apartments, creating a massive demand for container gardening solutions. The French government's initiatives to green cities, such as the "Parisculteurs" project, encourage the installation of planters on rooftops and facades, stimulating the commercial segment. As per the French Federation of Landscape Professionals, there is growing investment in public green spaces and private garden renovations, driving sales of high end and designer planters. The influence of French design and luxury brands also elevates the market, with consumers willing to invest in aesthetically superior products. This fusion of urban necessity, governmental support, and design consciousness reinforces France's standing as a key market player.

Italy Planters Market Analysis

Italy is estimated to showcase a healthy CAGR in the Europe planters market over the forecast period owing to its profound connection to landscape beauty, historical heritage, the centrality of outdoor dining and socializing and the architectural style of its cities and towns, where terracotta and stone planters are integral to the visual identity of streetscapes and private courtyards. According to the Italian National Institute of Statistics, the renovation and maintenance of historical sites and private villas drive steady demand for traditional and artisanal planters. The Mediterranean climate allows for year-round gardening, extending the selling season and encouraging continuous investment in outdoor decor. As per the Italian Association of Floristry and Landscaping, there is a strong preference for locally crafted ceramic and terracotta products, supporting a robust domestic manufacturing base. The cultural emphasis on "la dolce vita" and outdoor living ensures that planters are not merely functional but essential elements of Italian lifestyle. This deep cultural integration and the strength of the tourism sector sustain Italy's prominent position in the regional market.

Netherlands Planters Market Analysis

The Netherlands is projected to register a notable CAGR in the Europe planters market over the forecast period due to its status as a global hub for floriculture and its innovative approach to urban greening. The high levels of expertise in horticulture and a forward-thinking attitude towards sustainable and smart gardening solutions are further contributing to the planters market expansion in Netherlands. According to Statistics Netherlands, the density of green spaces per capita is among the highest in Europe, with extensive use of planters in urban planning to maximize limited land area. The Dutch concept of living labs and smart cities has led to the early adoption of self watering and sensor equipped planters for both residential and commercial use. As per Royal FloraHolland, the local availability of a vast array of plants drives complementary sales of high quality containers. The government's aggressive policies on climate adaptation, including the creation of rain gardens and green roofs, further stimulate demand for specialized planters. This combination of horticultural leadership, innovation, and proactive environmental policy ensures the Netherlands punches above its weight in the European market.

COMPETITIVE LANDSCAPE

The competition in the Europe planters market is characterized by a dynamic mix of established manufacturers and emerging artisanal brands who compete on design innovation, material sustainability, and functional technology. Major players differentiate themselves by obtaining eco-certifications and offering smart features that appeal to tech-savvy urban gardeners seeking convenience and efficiency. The market sees frequent launches of collections made from recycled plastics or biodegradable composites as companies strive to align with strict European environmental regulations and consumer values. Price competition varies significantly between mass-market producers offering affordable solutions and premium brands commanding higher prices for unique designs and superior durability. Regional specialists often compete by providing localized styles and rapid customization services for landscape architects and commercial clients. The barrier to entry remains moderate due to the availability of raw materials but high for brands seeking to establish strong recognition and distribution networks. Collaboration between manufacturers and sustainability organizations is increasing to promote best practices in recycling and resource efficiency. Overall the landscape is vibrant with companies vying to lead in eco-innovation and design excellence while adapting to shifting urban living trends and climate challenges across the continent.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Planters Market include

- AGCO Corporation

- Deere & Company

- CNH Industrial N.V.

- Kubota Corporation

- Väderstad AB

- AMAZONE (AMAZONEN-Werke H. Dreyer GmbH & Co. KG)

- LEMKEN GmbH & Co. KG

- Pöttinger Landtechnik GmbH

- Maschio Gaspardo S.p.A.

- KUHN Group

- HORSCH Maschinen GmbH

- Monosem Inc.

- Kverneland Group

- SLY Agri

Top Players in the Market

Lechuza by United Pet Group

Lechuza stands as a premier innovator in the Europe planters market, renowned for pioneering self-watering systems that revolutionize indoor and outdoor gardening efficiency. The company significantly contributes to the global landscape by setting high standards for functional design and water conservation technologies in horticultural containers. Lechuza recently strengthened its European position by expanding its product line with smart sensors that monitor soil moisture levels via smartphone applications. The firm actively collaborates with interior designers to integrate stylish planters into modern living spaces, blending aesthetics with advanced irrigation capabilities. By utilizing recycled plastics in manufacturing, Lechuza aligns with European sustainability goals while maintaining product durability. Their commitment to user-friendly gardening solutions empowers individuals with limited time or expertise to maintain healthy plants. This strategic focus on technology integration and eco-conscious production solidifies their reputation as a leader in the global premium planter sector.

Elho

Elho leverages its Dutch heritage to maintain a dominant presence in the Europe planters market through a comprehensive range of sustainable and design-led plastic pots. The company contributes globally by championing the circular economy, producing items entirely from recycled materials and ensuring full recyclability at end of life. Elho recently enhanced its European footprint by launching collections specifically tailored for urban balconies and vertical gardening applications to address space constraints. The firm focuses on local production within Europe to minimize carbon emissions associated with transportation and logistics. Through strategic partnerships with retail chains, Elho ensures widespread availability of its colorful and durable products across the continent. Their dedication to sustainability drives the development of innovative manufacturing processes that reduce energy consumption and waste. This customer-centric approach combined with an unwavering commitment to environmental responsibility ensures the company remains a trusted partner for gardening enthusiasts and professionals alike.

Scheurich

Scheurich is a leading manufacturer in the Europe planters market, distinguished by its extensive portfolio of high-quality ceramic and terracotta containers that blend traditional craftsmanship with modern trends. The company plays a pivotal role globally by exporting distinctive European designs that cater to diverse aesthetic preferences in home and garden decor. Scheurich recently strengthened its market position by introducing new glazing techniques that enhance frost resistance and durability for outdoor use in varying climates. The firm actively invests in expanding its distribution network to reach independent garden centers and online platforms more effectively. By collaborating with landscape architects, Scheurich provides customized solutions for large-scale commercial projects and public spaces. Their focus on artistic expression and material quality ensures that each planter serves as both a functional vessel and a decorative statement. This holistic approach to combining heritage skills with contemporary design allows Scheurich to meet the evolving needs of discerning customers across the European and international markets.

Top Strategies Used by Key Market Participants

Key players in the Europe planters market primarily focus on product innovation and sustainability to differentiate their offerings and meet evolving consumer demands. Companies heavily invest in research and development to create self-watering systems and smart planters equipped with sensors for optimal plant care. Strategic partnerships with retailers and online platforms enable manufacturers to expand their reach and ensure broad product availability across diverse regions. Firms increasingly adopt circular economy principles by utilizing recycled materials and designing products for full recyclability at end of life. Expanding production facilities within Europe helps companies reduce logistics costs and carbon footprints while ensuring faster delivery times. Offering customizable designs and collaborative collections with famous designers attracts style-conscious consumers and enhances brand prestige. Providing educational content and gardening guides builds customer loyalty and encourages engagement with the brand community. Acquiring smaller niche brands allows major players to diversify their portfolios and enter specialized segments such as vertical gardening or luxury ceramics.

MARKET SEGMENTATION

This research report on the Europe Planters Market has been segmented and sub-segmented based on the following categories.

By End User

- Residential

- Commercial

By Distribution Channel

- Offline

- Online

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Planters Market?

The Europe planters market refers to the industry involved in the manufacturing, distribution, and sale of planters used for gardening, landscaping, and agricultural planting across European countries.

What are planters used for in Europe?

Planters are used for growing flowers, herbs, vegetables, and decorative plants in homes, gardens, commercial spaces, and urban landscaping projects.

What factors are driving the growth of the Europe Planters Market?

Growing interest in home gardening, urban landscaping projects, and increasing awareness of indoor plants are key factors driving market growth.

What materials are commonly used to manufacture planters in Europe?

Planters are commonly made from materials such as ceramic, plastic, metal, wood, fiberglass, and concrete.

Which sectors contribute most to the demand for planters in Europe?

Residential gardening, commercial landscaping, hospitality, and urban development projects are major sectors driving demand.

Which countries lead the Europe Planters Market?

Countries such as Germany, France, the United Kingdom, Italy, and the Netherlands are major contributors due to strong gardening culture and landscaping industries.

What types of planters are popular in Europe?

Popular types include indoor planters, outdoor planters, hanging planters, self-watering planters, and decorative planters.

What role does the landscaping industry play in the market?

The landscaping industry drives demand for large decorative and commercial planters used in parks, offices, hotels, and public spaces

What are self-watering planters and why are they gaining popularity?

Self-watering planters contain built-in water reservoirs that help maintain consistent moisture levels, reducing the need for frequent watering.

What are the challenges faced by the Europe Planters Market?

Challenges include fluctuating raw material costs, competition from low-cost imports, and environmental regulations regarding plastic usage

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com