Europe Potentiometer Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Linear, Rotary, Digital), Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Potentiometer Market Report Summary

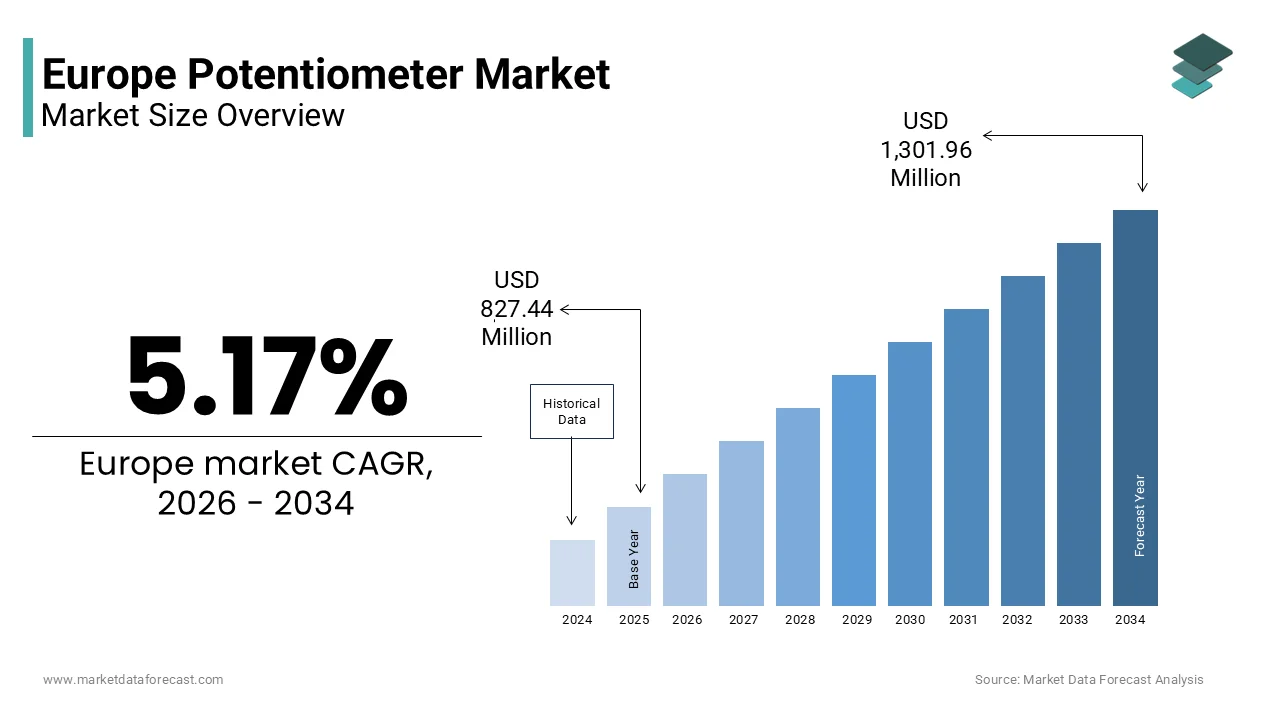

The Europe potentiometer market was valued at USD 827.44 million in 2025 and is projected to reach USD 1,301.96 million by 2034 from USD 870.21 million in 2026, growing at a CAGR of 5.17% during the forecast period. Market growth is primarily driven by increasing adoption of precision control components in medical equipment, industrial automation systems, and consumer electronics. Rising demand for accurate position sensing, voltage regulation, and motion control solutions across manufacturing and healthcare sectors is supporting steady expansion. Technological advancements in rotary and linear potentiometers, along with integration in advanced diagnostic and monitoring devices, are further contributing to market growth across Europe.

Key Market Trends

- Growing integration of potentiometers in medical equipment such as imaging systems, infusion pumps, and patient monitoring devices to ensure precision control and reliability.

- Rising demand from industrial automation and robotics sectors requiring accurate position feedback and motion control components.

- Increasing focus on miniaturization and high durability designs to meet evolving requirements in compact electronic devices.

- Adoption of advanced materials and improved resistive technologies to enhance performance, lifespan, and environmental resistance.

- Expansion of manufacturing activities across Germany and other major European economies supporting steady component demand.

Segmental Insights

- Based on type, the rotary potentiometer segment held the dominant position in 2025, accounting for 56.5% of the Europe potentiometer market share. The segment’s leadership is attributed to its widespread use in volume control systems, industrial machinery, automotive electronics, and medical devices due to ease of installation, reliability, and precise rotational control capabilities.

- Based on application, the medical equipment segment led the market by commanding 40.6% of the Europe potentiometer market share in 2025. Growth in this segment is driven by the increasing deployment of potentiometers in diagnostic devices, surgical equipment, and therapeutic systems that require accurate adjustment and feedback mechanisms.

Regional Insights

- Germany was the largest contributor to the Europe potentiometer market in 2025, holding 23.5% of the regional market share. The country’s dominance is supported by its strong industrial automation base, advanced manufacturing ecosystem, and significant presence of automotive and medical device industries that require high precision electronic components.

- Other Western European countries continue to contribute significantly due to rising investments in automation, healthcare infrastructure, and advanced electronics manufacturing.

Competitive Landscape

The Europe potentiometer market is moderately consolidated, with global and regional manufacturers focusing on product innovation, precision engineering, and long term reliability. Companies are investing in research and development to enhance performance characteristics such as temperature stability, wear resistance, and signal accuracy. Strategic collaborations with OEMs in medical, industrial, and automotive sectors are strengthening competitive positioning. Prominent players operating in the Europe potentiometer market include Bourns, Inc., TE Connectivity, Honeywell International Inc., Panasonic Corporation, Vishay Intertechnology, Inc., CTS Corporation, TT Electronics plc, ALPS, BEI Sensors, Positek Limited, Novotechnik, and SIKO.

Europe Potentiometer Market Size

The Europe potentiometer market size was valued at USD 827.44 million in 2025 and is projected to reach USD 1,301.96 million by 2034 from USD 870.21 million in 2026, growing at a CAGR of 5.17%.

Potentiometers are variable resistors that are used to control electrical signals by adjusting voltage or current levels within a circuit. These passive electronic components are fundamental building blocks in a vast array of industrial, automotive, and consumer applications, from precision instrumentation and audio equipment to motor speed controls and position sensors. In the European context, the market is defined by its integration into high value, engineering intensive sectors that demand exceptional reliability and precision. A critical non-market statistic shaping this landscape is the continent’s robust industrial base. As per Eurostat, the manufacturing sector contributes significantly to the European Union’s gross value added, which is indicating the immense scale of industrial activity that relies on such components. Furthermore, according to the European Automobile Manufacturers Association, motor vehicle production in the EU highlights the massive embedded demand for potentiometers in automotive systems for functions like throttle control, seat adjustment, and climate management, where mechanical feedback and analog control remain essential.

MARKET DRIVERS

Robust Industrial Automation and Machinery Sector Drives Component Demand

The deeply entrenched and technologically advanced industrial automation sector of Europe is majorly propelling the expansion of the Europe potentiometer market. European manufacturers, particularly in Germany, Italy, and Sweden, are global leaders in producing high precision machine tools, robotics, and process control systems. These complex machines rely heavily on potentiometers for critical functions such as position sensing, speed regulation, and manual calibration. The need for rugged, long lasting, and highly accurate components in these environments is non-negotiable. As per the German Engineering Federation (VDMA), order intake for German machinery and plant engineering has been above the long-term average, which is directly translating into a steady stream of demand for high quality electronic components like industrial grade potentiometers.

Prolonged Lifecycle of Legacy Industrial and Automotive Systems Ensures Sustained Demand

A powerful and often overlooked driver of the market is the extensive installed base of legacy industrial equipment and vehicles across Europe that continue to operate for decades, which is further fuelling the Europe potentiometer market growth. Unlike consumer electronics, industrial machinery and commercial vehicles are engineered for longevity, with operational lifespans often exceeding 20 or even 30 years. These systems were designed and built at a time when analog control via potentiometers was the standard, and their ongoing maintenance and repair create a persistent and reliable demand for replacement components. This is particularly evident in the rail and heavy machinery sectors, where entire fleets of equipment are maintained far beyond their original design life. As per the International Union of Railways, locomotive fleets in several Eastern European countries remain in operation well beyond their intended lifespan. This reality ensures that even as new digital systems emerge, there remains a vast and stable aftermarket for traditional potentiometers, providing a crucial revenue stream that buffers the market against cyclical downturns in new equipment production.

MARKET RESTRAINTS

Accelerated Shift Towards Digital and Contactless Sensing Technologies

The relentless technological shift towards digital and contactless alternatives in new product designs is primarily hampering the growth of the Europe potentiometer market. In many modern applications, especially in automotive and high-end industrial automation, potentiometers are being replaced by more reliable and durable technologies such as Hall effect sensors, optical encoders, and magneto resistive sensors. These solid-state solutions offer superior longevity, immunity to dust and moisture, and higher resolution, making them the preferred choice for next generation systems. As per a technical analysis by a leading European automotive supplier, the use of contactless position sensors in new vehicle platforms has been increasing significantly, directly displacing traditional potentiometers in critical applications like pedal position and steering angle detection. This trend confines the potentiometer market to legacy systems and costs sensitive applications, limiting its expansion into high growth, high technology segments.

Stringent Environmental and Material Compliance Regulations Increase Costs

The European potentiometer market faces significant pressure from the bloc’s comprehensive and ever evolving environmental regulations, which impose strict requirements on the materials used in electronic components. Directives like the Restriction of Hazardous Substances (RoHS) and Registration Evaluation Authorisation and Restriction of Chemicals (REACH) mandate the elimination of specific substances and require extensive documentation for all materials in the supply chain. Complying with these regulations necessitates costly reformulation of materials, rigorous testing, and complex supply chain audits. For manufacturers of potentiometers, which often rely on specialized conductive plastics and metal alloys, this can significantly increase production costs and complicate sourcing. As per a European electronics industry association, compliance with chemical regulations adds notable costs to the manufacturing of passive components. This financial burden is particularly challenging for smaller, specialized manufacturers, potentially forcing them out of the market and reducing the diversity of the supply base.

MARKET OPPORTUNITIES

Expansion into High Precision Medical and Laboratory Equipment Applications

The strategic expansion of Europe potentiometer market into the high precision medical and laboratory equipment sector is a notable opportunity for the market expansion. This segment demands components with exceptional accuracy, stability, and biocompatibility, areas where European manufacturers have a strong reputation for engineering excellence. Devices such as patient monitors, diagnostic imaging systems, and analytical laboratory instruments often require fine manual adjustments for calibration and control, a function where high quality multi turn or precision trimmer potentiometers are still irreplaceable. As per the European Commission, the European medical device market is one of the largest globally, accounting for a significant share of medical technology exports. As healthcare systems invest in advanced diagnostic and therapeutic technologies, the demand for these ultra reliable, niche potentiometers grow, offering a high margin, low volume opportunity that leverages Europe’s strengths in precision engineering and quality control.

Growth of Renewable Energy and Power Electronics Infrastructure

The aggressive push of Europe towards renewable energy and grid modernization is creating a new and substantial opportunity for the Europe potentiometer market. Inverters for solar and wind power systems, battery management systems for energy storage, and power conversion units for electric vehicle charging infrastructure all require robust components for manual setup, calibration, and system tuning during installation and maintenance. These applications operate in demanding electrical environments and require potentiometers that can handle high voltages and provide stable performance over time. As per the European Union’s REPowerEU plan, large scale solar photovoltaic capacity is targeted for installation by 2030. This massive deployment of power electronics hardware represents a significant new market for industrial grade potentiometers designed for high reliability in energy applications, allowing component suppliers to diversify their customer base beyond traditional industrial and automotive sectors.

MARKET CHALLENGES

Intense Price Competition from Low -Cost Asian Manufacturers

One of the most persistent challenges facing European potentiometer manufacturers is the intense price pressure from a flood of low-cost alternatives originating primarily from China and other Asian countries. These imports, often produced at a fraction of the cost due to lower labor and material expenses, have commoditized the market for standard, low precision potentiometers. This dynamic makes it extremely difficult for European firms, which must adhere to higher quality standards and bear the costs of stringent regulatory compliance, to compete on price in high volume, cost sensitive applications. The result is a market bifurcation where European producers are forced to retreat to high end, specialized niches, while the bulk of the volume market is captured by Asian suppliers. This erosion of the mid-tier segment undermines the economic viability of a broad-based European component manufacturing industry and threatens the long-term health of the domestic supply chain.

Critical Shortage of Skilled Labor for Precision Component Manufacturing

The Europe potentiometer market is grappling with a severe shortage of skilled technicians and engineers proficient in the specialized crafts of precision component manufacturing and assembly. The production of high-quality potentiometers, especially for military, aerospace, and medical applications, requires a deep understanding of materials science, meticulous manual dexterity, and expertise in fine calibration as these are the skills that are increasingly rare in a labor market focused on software and digital technologies. As per a survey by a German association of electronic component manufacturers, a majority of its members reported significant difficulties in recruiting and retaining qualified production staff for their precision assembly lines. This human capital gap not only constrains production capacity but also increases the risk of quality inconsistencies and longer lead times, which can erode customer confidence and make it harder for European manufacturers to justify their premium pricing against automated, high-volume competitors from Asia.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.17% |

| Segments Covered | By Type, Application, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Bourns Inc., TE Connectivity, Honeywell International Inc., Panasonic Corporation, Vishay Intertechnology Inc., CTS Corporation, TT Electronics plc, Alps Alpine Co. Ltd., BEI Sensors, Positek Limited, Novotechnik, and SIKO |

SEGMENTAL ANALYSIS

By Type Insights

The rotary segment held the dominant position in the regional market in 2025 by holding 56.5% of the regional market share. The dominance of rotary segment in the European market is driven by its widespread utility and mechanical simplicity across a vast array of industrial and consumer applications. Rotary potentiometers play a fundamental role in human machine interfaces where intuitive manual control is required. Their circular motion provides a natural and ergonomic method for adjusting volume, brightness, speed, or position, making them the preferred choice in audio equipment, industrial control panels, and automotive dashboards. In the industrial sector, rotary potentiometers are indispensable for calibrating machinery and providing feedback on rotational position. As per the German Electrical and Electronic Manufacturers’ Association (ZVEI), rotary types remain the majority among variable resistors used in European industrial control systems, underscoring their entrenched position as reliable and cost-effective solutions for analogue control.

The digital segment is anticipated to witness the fastest CAGR of 9.4% over the forecast period owing to the new applications requiring programmable, non-mechanical resistance adjustment. Digital potentiometers are integrated into sophisticated power management and signal conditioning circuits within modern electronics. Controlled via communication protocols like I2C or SPI, they allow microcontrollers to automatically calibrate sensors, adjust gain in amplifiers, or fine tune voltage references without moving parts. This is critical in compact, sealed, or high reliability systems such as medical implants, aerospace avionics, and advanced battery management systems for electric vehicles. As per a European semiconductor industry group, adoption of digital potentiometers in automotive electronic control units has been rising significantly, driven by the need for greater system intelligence and self-diagnostics.

By Application Insights

The medical equipment segment led the market by commanding for 40.6% of the regional market share in 2025. The growth of the medical equipment segment in the European market can be credited to the stringent performance and reliability requirements of the healthcare sector, where precision and safety are paramount. Medical equipment such as patient monitors, dialysis machines, and imaging systems often requires manual calibration and fine-tuning during setup and maintenance. Multi turn precision potentiometers are uniquely suited for these tasks, offering the resolution and repeatability necessary for life critical applications. European manufacturers, renowned for their engineering quality, are major suppliers to this sector. As per the European Coordination Committee of the Radiological Electromedical and Healthcare IT Industry (COCIR), most high-end medical devices produced in Western Europe specify components from local or regional suppliers to ensure traceability and compliance with EU Medical Device Regulation, creating a stable and high value demand stream for specialized potentiometers.

Conversely, the computation segment is the fastest growing and is anticipated to register a CAGR of 8.86% over the forecast period due to the increasing complexity of data center and server infrastructure, which requires sophisticated power management and signal integrity solutions. Digital potentiometers are used for remote calibration and voltage margining in server motherboards and power supplies. As data centers strive for greater energy efficiency and operational reliability, the ability to remotely fine tune voltage levels to individual processor cores or memory banks becomes essential. Digital potentiometers provide this capability without physical access, enabling predictive maintenance and performance optimization. As per a European data center alliance, the average number of digital potentiometers per high performance server has been increasing steadily, reflecting their growing importance in managing the power demands of next generation computing hardware.

REGIONAL ANALYSIS

Germany Potentiometer Market Analysis

Germany was the undisputed leader in the European potentiometer market in 2025 and held 23.5% of the regional market share. The dominating position of Germany in the European market is driven by its world leading industrial machinery and automotive sectors, which are massive consumers of high-quality electronic components. The German economy’s focus on “Industrie 4.0” has further cemented the demand for reliable sensors and control elements, including precision potentiometers, in its advanced manufacturing base. As per Eurostat, Germany contributes a significant portion of the EU’s machinery production. This immense industrial output, combined with a dense network of highly specialized small and medium sized enterprises, creates a self-sustaining ecosystem that drives continuous demand for both standard and custom engineered potentiometers, which is making Germany the central hub of the continental market.

Italy Potentiometer Market Analysis

Italy secured the second largest share of the European potentiometer market in 2025. The growth of Italy in the European market is attributed to its diverse and innovative manufacturing landscape, particularly in industrial automation, robotics, and high-end consumer appliances. Italian manufacturers are known for their design excellence and integration of mechanical and electronic systems, which creates steady demand for robust and aesthetically integrated control components. As per the Italian Packaging Machinery Association (UCIMA), Italy is a global leader in packaging machinery exports, a sector that relies heavily on potentiometers for tension control and speed regulation. This export oriented industrial base ensures a constant flow of demand for reliable components that can perform in demanding, high speed production environments.

United Kingdom Potentiometer Market Analysis

The United Kingdom is estimated to hold a promising share of the European potentiometer market during the forecast period. The leadership of the UK in aerospace, defense, and medical technology is majorly supporting the growth of the UK potentiometer market. UK based companies develop complex systems where precision, reliability, and miniaturization are critical. The aerospace and defense industry requires components that can operate under extreme conditions with zero failure tolerance, driving demand for high reliability potentiometers. The UK is home to major players like BAE Systems and Rolls Royce, whose supply chains depend on specialized components. Strong university research in electronics and photonics fosters innovation in niche applications, ensuring consistent demand for cutting edge solutions that support its advanced engineering economy.

France Potentiometer Market Analysis

France is expected to showcase a prominent CAGR in the European potentiometer market during the forecast period. The strong state supported industrial policy and a focus on strategic sectors like nuclear energy, rail transport, and aerospace are driving the market growth in France. These capital-intensive industries require long lasting, highly reliable components for control and monitoring systems. A defining feature of the French market is the extensive use of potentiometers in its national rail network. As per the International Union of Railways, France has one of the largest electrified railway infrastructures in Europe, representing a vast installed base of equipment that necessitates ongoing maintenance and component replacement. This creates stable and predictable demand for industrial grade potentiometers.

Sweden Potentiometer Market Analysis

Sweden is estimated to register a healthy CAGR in the European potentiometer market over the forecast period. Its position is built on world class engineering in automotive, telecommunications, and clean tech sectors. Companies like Volvo Cars and Ericsson are known for innovation and high-quality standards, which translates into demand for premium electronic components. A crucial factor for Sweden’s potentiometer market is its leadership in electric and autonomous vehicle development. The transition to electric drivetrains and advanced driver assistance systems requires specialized potentiometers for battery management and manual override systems. Sweden’s commitment to sustainability and its advanced manufacturing base in renewable energy technologies further create demand for components used in power electronics and control systems for wind and solar installations, positioning the country as a key market for future oriented applications.

COMPETITIVE LANDSCAPE

The competitive landscape of the Europe potentiometer market is characterized by a clear division between a few global technology leaders and a fragmented base of regional and local manufacturers. The top tier, comprising companies like Vishay, Bourns, and TT Electronics, competes on the basis of engineering excellence, product reliability, and deep application expertise, particularly in high value sectors such as medical, aerospace, and industrial automation. These firms benefit from strong brand recognition and established relationships with major European OEMs. In contrast, the lower end of the market is crowded with smaller suppliers and Asian imports that compete almost exclusively on price for standard, low precision components. This bifurcation creates a stable environment for leaders in specialized niches but intense pressure in the commoditized segment. The overall market is not highly dynamic, with competition centred on maintaining quality and meeting regulatory standards rather than disruptive innovation.

KEY MARKET PLAYERS

Some of the notable key players in the Europe potentiometer market are

- Bourns, Inc.

- TE Connectivity

- Honeywell International Inc.

- Panasonic Corporation

- Vishay Intertechnology, Inc.

- CTS Corporation

- TT Electronics plc

- ALPS

- BEI Sensors

- Positek Limited

- Novotechnik

- SIKO

Top Players in the Market

- Vishay Intertechnology is a global leader in discrete semiconductors and passive components with a formidable presence in the European potentiometer market. The company offers an extensive portfolio of precision rotary and linear potentiometers, including high reliability models for industrial, automotive, and medical applications. Vishay’s contribution to the global market lies in its vertically integrated manufacturing and its commitment to quality and long-term product availability. To strengthen its position in Europe, Vishay has focused on developing potentiometers that meet the stringent requirements of the EU’s automotive and medical device regulations. The company has also invested in expanding its European logistics network to ensure rapid delivery of its components to key industrial customers across the region.

- Bourns is a major international manufacturer of electronic components renowned for its innovative circuit protection and sensing solutions, including a wide range of precision potentiometers. In Europe, Bourns serves a diverse customer base in the industrial automation, test and measurement, and transportation sectors. The company’s global contribution is marked by its engineering expertise in creating highly durable and stable components for harsh environments. To enhance its European market standing, Bourns has recently intensified its focus on digital potentiometers and sensor integration, launching new product lines specifically designed for battery management systems in electric vehicles and for calibration in advanced power electronics used in renewable energy infrastructure.

- TT Electronics is a UK based global provider of engineered electronics with a strong heritage in high reliability components, including a comprehensive range of potentiometers under its BI Technologies brand. The company is a key supplier to the European aerospace, defense, and medical markets, where its products are valued for their precision and long-term stability. TT Electronics’ global contribution is its specialization in custom engineered solutions for mission critical applications. To solidify its European position, the company has been actively investing in its manufacturing facilities in the United Kingdom and Sweden, enhancing capabilities for producing high mix, low volume precision potentiometers and ensuring compliance with the latest European environmental and safety directives for its most demanding industrial clients.

Top Strategies Used by the Key Market Participants

Key players in the Europe potentiometer market are primarily focused on differentiating themselves through high reliability and application specific engineering rather than competing on price. They invest heavily in developing components that comply with stringent European regulations for automotive, medical, and industrial sectors. A core strategy involves expanding their portfolios of digital and hybrid potentiometers to address the needs of modern power electronics and smart systems. Companies also prioritize securing long term supply agreements with major industrial OEMs to ensure stability. Furthermore, they are strengthening their local European manufacturing and logistics capabilities to mitigate global supply chain risks and provide faster, more responsive service to their engineering-focused customer base.

MARKET SEGMENTATION

This research report on the European potentiometer market has been segmented and sub-segmented based on categories.

By Type

- Linear

- Rotary

- Digital

By Application

- Television

- Computation

- Medical Equipment

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1.What is driving the growth of the Europe potentiometer market?

Growth is primarily driven by increasing demand from the automotive sector, expansion of industrial automation, rising adoption of consumer electronics, and continuous advancements in electronic component technologies.

2.Which countries are leading the Europe potentiometer market?

Germany leads the market due to its strong automotive and manufacturing base, followed by countries such as France, Italy, and the United Kingdom that contribute significantly through industrial and electronics production.

3.Which types of potentiometers are widely used in Europe?

Rotary potentiometers are widely used in audio systems and automotive controls, while linear potentiometers are commonly adopted in industrial equipment and precision measurement applications.

4.What are the key applications of potentiometers in Europe?

Potentiometers are used in automotive control systems, industrial machinery, consumer electronics, aerospace systems, and medical devices for voltage regulation and position sensing.

5.How does the automotive industry impact the Europe potentiometer market?

The automotive industry drives demand through the integration of electronic control systems, throttle position sensing, climate control modules, and advanced driver assistance systems.

6.What role does industrial automation play in market growth?

Industrial automation significantly contributes to demand as potentiometers are essential for motion control, equipment calibration, robotics, and precision positioning systems.

7.How are digital potentiometers influencing the market?

Digital potentiometers are gaining adoption due to their improved reliability, compact design, programmability, and compatibility with modern electronic systems.

8.What technological trends are shaping the Europe potentiometer market?

Key trends include miniaturization, enhanced durability, higher precision components, integration with smart systems, and development of long life materials for demanding applications.

9.Who are the major companies operating in the Europe potentiometer market?

Leading companies include Bourns Inc., Vishay Intertechnology, TT Electronics, Alps Alpine Co. Ltd., and Panasonic Corporation, focusing on product innovation and strategic expansion.

10.What challenges are affecting the Europe potentiometer market?

The market faces challenges such as competition from non contact sensing technologies, price volatility of raw materials, and supply chain constraints.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com