Europe Propane Market Size, Share, Trends & Growth Forecast Report, Segmented By Grade, End-User, And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2026 to 2034)

Europe Propane Market Size

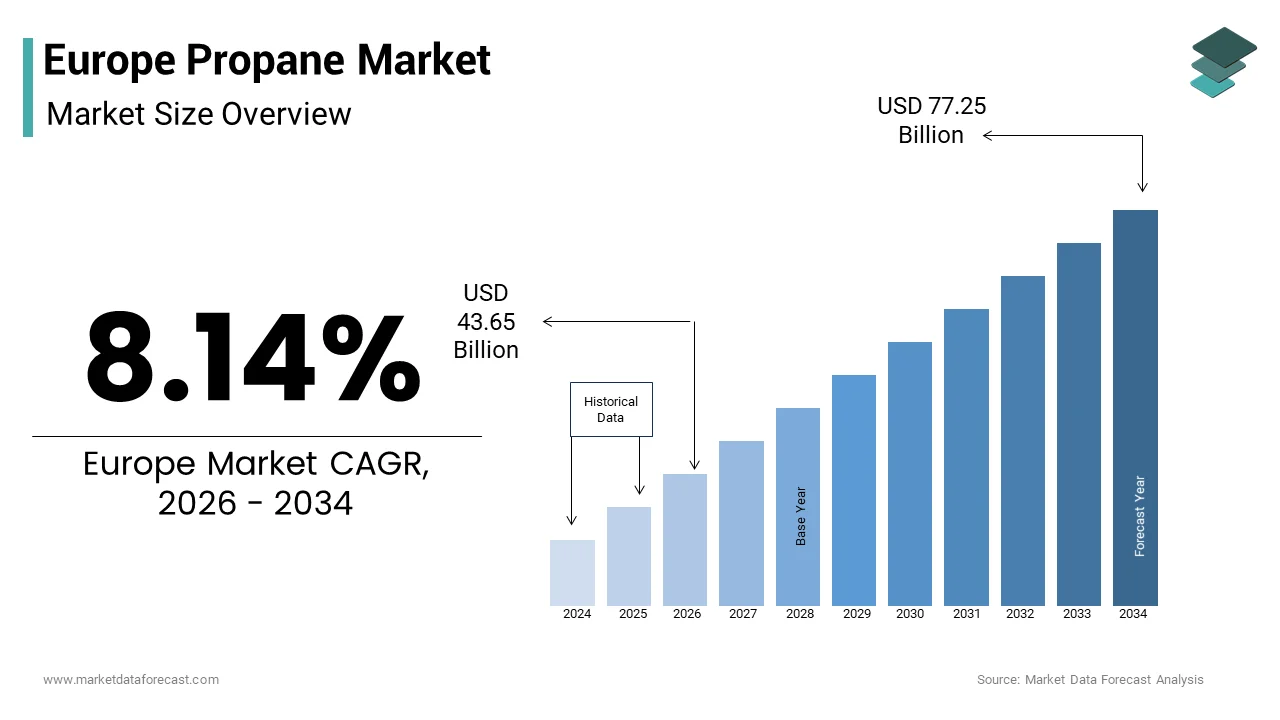

The Europe propane market size was valued at USD 40.35 billion in 2025 and is anticipated to reach USD 43.65 billion in 2026 to reach USD 77.25 billion by 2034, growing at a CAGR of 8.14% during the forecast period from 2026 to 2034.

The propane is a versatile liquefied petroleum gas derived from natural gas processing and crude oil refining. This hydrocarbon fuel is indispensable for residential heating commercial cooking and industrial processes in regions lacking access to centralized natural gas grids. The market dynamics are heavily influenced by the transitional energy policies of the European Union, which seek to balance immediate energy security needs with long term decarbonization goals. As per recent data, the total consumption of liquefied petroleum gases across all sectors in Europe was recorded at 33.18 million metric tons in 2024 before experiencing a slight decline . This volume underscores the entrenched role of propane in maintaining energy stability for millions of households and businesses. The fuel's portability allows it to serve off grid communities effectively thereby ensuring energy equity in rural and remote areas. Furthermore propane is increasingly recognized for its lower carbon intensity compared to coal and oil which positions it as a bridge fuel in the shift toward renewable energy sources.

MARKET DRIVERS

Residential Heating Demand in Off Grid Areas

The persistent reliance on propane for residential heating in off grid locations is propelling the growth of Europe propane market. A significant portion of the European population resides in rural areas where connection to the natural gas grid is economically unfeasible or technically impractical. According to Eurostat, space heating accounted for 63.5% of the final energy consumption in the residential sector in 2022, where the immense energy demand for thermal comfort . Propane offers a reliable and efficient solution for these households providing consistent heat supply regardless of external weather conditions. The fuel's high energy density allows for storage in onsite tanks ensuring uninterrupted service during peak winter months. In countries, such as France and Poland where rural housing stock is substantial propane remains a preferred choice for primary heating systems. The European Heat Pump Association indicates that while heat pump installations are rising there remains a massive disparity in adoption rates across different regions leaving many homes dependent on traditional fuels. This dependency ensures a steady baseline demand for propane as homeowners prioritize immediate reliability over long term retrofitting costs. Additionally the aging infrastructure in many Eastern European nations means that transitions to electric heating are slower than anticipated. Consequently, propane suppliers continue to see robust demand from residential users who value the autonomy and control provided by individual tank systems.

Automotive Autogas Adoption and Environmental Compliance

The automotive sector through the widespread adoption of autogas or liquefied petroleum gas as a vehicle fuel is additionally escalating the growth of Europe propane market. Propane is increasingly utilized as a cleaner alternative to gasoline and diesel helping fleet operators and private vehicle owners comply with stringent European emission standards. The LPG passenger cars shows that Poland and Italy dominate the scene with significant shares of the total vehicle fleet running on this fuel. Propane combustion produces fewer particulate matters and nitrogen oxides compared to conventional fossil fuels making it an attractive option for urban areas striving to improve air quality. Furthermore, the cost advantage of autogas remains a compelling factor for drivers seeking to reduce operational expenses amidst fluctuating oil prices. The Renault Group led by its budget Dacia brand expanded its lineup of LPG vehicles contributing to this uptake.

MARKET RESTRAINTS

Regulatory Pressure and Electrification Mandates

The intensifying regulatory pressure aimed at phasing out fossil fuel based heating systems in favor of electrification is majorly restricting the growth of Europe propane market. The European Union has been steadily tightening its approach to decarbonize the building sector which accounts for a significant portion of total energy consumption. Since early 2025 member states have faced stricter guidelines that discourage the installation of new fossil fuel boilers including those powered by propane. This policy shift is part of a broader strategy to achieve climate neutrality by 2050 and reduces the long term viability of propane as a primary heating source. The average lifetime of domestic gas boilers exceeds 20 years meaning that current restrictions will gradually erode the customer base for propane heating solutions. Additionally, the EU’s Renewable Energy Directive mandates an increase in the share of renewables in heating and cooling further marginalizing fossil fuels. As per Ember the total EU gas consumption declined by 20% in the past five years partly due to these regulatory measures and the push for efficiency. This structural decline poses a significant challenge for propane suppliers who must navigate a shrinking addressable market in the residential sector. The financial incentives provided for heat pump installations and solar thermal systems also make alternatives more attractive to homeowners. The propane companies face the dual challenge of complying with evolving regulations while competing against subsidized green technologies that offer lower operating costs in the long run.

Volatility in Global Supply Chains and Import Dependencies

The volatility in global supply chains and Europe’s heavy dependence on imported propane, which exposes to geopolitical and logistical risks is also hindering the growth of Europe propane market. Europe does not produce sufficient propane to meet its domestic demand relying heavily on imports from regions, such as the United States and the Middle East. In 2025, the EU imported €336.7 billion worth of energy products reflecting the continent’s deep integration into global energy markets . However, this dependency makes the propane market susceptible to price fluctuations driven by international events such as conflicts in the Middle East or trade disputes. For instance, tensions in the Hormuz Strait can disrupt shipping routes leading to sudden spikes in propane prices and supply shortages . Additionally warm weather conditions in Europe can lead to weak demand causing inventory buildups and price instability as seen with record US propane shipments struggling to find buyers. The lack of diversified supply sources exacerbates this vulnerability limiting the ability of European buyers to negotiate favorable terms. Infrastructure limitations such as insufficient storage capacity and terminal bottlenecks further compound the issue preventing efficient management of supply shocks. As per Argus Media Northwest Europe’s propane market is undergoing major changes due to price volatility and oversupply issues.

MARKET OPPORTUNITIES

Expansion into Petrochemical Feedstock Applications

The expanding use as a feedstock for the petrochemical industry in the production of propylene and other derivatives is expected to showcase new opportunities for the growth of Europe propane market. Propane dehydrogenation plants are increasingly being developed across Europe to meet the growing demand for polypropylene and other plastic materials. Propane offers a cost effective and efficient route to producing propylene compared to traditional naphtha cracking especially when oil prices are high. This shift allows chemical manufacturers to diversify their raw material sources and reduce dependence on crude oil derivatives. Several major chemical companies in Europe are investing in new propane dehydrogenation facilities to capitalize on this trend. The flexibility of propane as a feedstock enables producers to adjust output based on market conditions enhancing operational efficiency. Furthermore, the availability of abundant propane supplies from global markets supports the scalability of these operations. As per industry analysis the demand for lightweight and durable plastics in automotive packaging and construction sectors continues to rise driving the need for reliable feedstock sources. This industrial application provides a stable and growing demand stream for propane that is less susceptible to the seasonal fluctuations seen in the residential heating sector.

Development of Renewable Propane and Bio LPG

The development of renewable propane and bio-LPG by aligning with the continent’s sustainability goals is additionally enhancing the growth of Europe propane market. Renewable propane is produced from biological sources such as vegetable oils animal fats and waste greases offering a significantly lower carbon footprint than conventional fossil propane. Liquid Gas Europe has highlighted the outlook for renewable liquid gas noting its potential to contribute to the EU’s climate objectives . This bio based alternative can be used in existing propane infrastructure without modifications making it a drop in solution for current users. The European Union’s focus on circular economy principles supports the production of bio LPG from waste materials reducing landfill usage and greenhouse gas emissions. As per Eurostat, renewable energy sources accounted for 25.2% of gross final energy consumption in the EU in 2024 creating a favorable policy environment for bio fuels . Propane suppliers are increasingly exploring partnerships with biofuel producers to integrate renewable propane into their product portfolios. This shift allows them to cater to environmentally conscious customers and comply with stricter emission regulations. The aviation and maritime sectors are also showing interest in sustainable liquid fuels opening new avenues for bio LPG applications.

MARKET CHALLENGES

Infrastructure Limitations and Storage Constraints

The existing infrastructure limitations and storage constraints that hinder efficient distribution and supply management is one of the major challenges for the growth of Europe propane market. The propane supply chain relies on a network of terminals storage facilities and transportation networks that are often aging or insufficient to handle fluctuating demand. In 2025, the propane supply chain crisis underscored the fragility of energy infrastructure and the urgency of modernization efforts . Many European countries lack adequate storage capacity to buffer against supply shocks leading to price volatility and potential shortages during peak demand periods. The reliance on imported propane requires specialized terminals for receiving liquefied gas shipments which are not evenly distributed across the continent. This geographical imbalance creates logistical bottlenecks and increases transportation costs for inland regions. Additionally, the maintenance and upgrading of existing infrastructure require significant capital investment which may be delayed due to regulatory uncertainty. As per S&P Global Europe struggles to absorb record inflows of propane due to these infrastructure challenges. The lack of interoperability between national gas networks further complicates the movement of propane across borders. These structural weaknesses make the market vulnerable to disruptions and limit its ability to respond swiftly to changing market conditions.

Competition from Alternative Energy Sources

Intense competition from alternative energy sources particularly electricity and natural gas poses a significant challenge to the Europe propane market. The rapid advancement of heat pump technology and the expansion of the electrical grid are providing viable alternatives to propane heating in both residential and commercial sectors. As per the European Commission renewable energy represented 24.6% of EU energy consumption in 2023 reflecting the growing presence of clean energy options . Natural gas remains a dominant fuel for heating in many urban areas offering lower costs and greater convenience compared to propane. The electrification of transport is also reducing the demand for autogas as electric vehicles gain market share. Government subsidies for electric vehicles and charging infrastructure further accelerate this transition. The European Heat Pump Association notes that heat pump installations are increasing although unevenly across the region . This competitive landscape forces propane suppliers to continuously innovate and demonstrate the value proposition of their fuel. Price competitiveness is a key factor as fluctuations in electricity and natural gas prices can influence consumer choices. Additionally, the perception of propane as a fossil fuel may deter environmentally conscious consumers despite its lower carbon intensity compared to coal and oil. Propane marketers must therefore emphasize the fuel’s reliability and the potential for renewable blends to maintain their market position.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.14% |

| Segments Covered | By Grade, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis, DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled | BP Plc (U.K.), SHV Energy, TotalEnergies, Neste, Chevron Corporation (U.S.), Royal Dutch Shell Plc (U.K.), Exxon Mobil Corporation (U.S.), ConocoPhillips (U.S), Reliance Industries Ltd. (India), PetroChina Company Limited (China), Sinopec (China), Total S A (France), Ferrellgas Partners L.P. (U.S.) |

SEGMENTAL ANALYSIS

By Grade Insights

The HD 5 grade segment was accounted in holding a dominant share of the Europe propane market in 2025 due to its stringent purity standards and suitability for high performance applications. This grade contains a minimum of 90% propane with limited propylene content making it ideal for engine fuel and sensitive industrial processes. The automotive sector’s reliance on Autogas, which requires high purity to prevent engine damage and ensure efficient combustion is leveraging the growth of Europe propane market. As per the World Liquid Gas Association, over 13 million vehicles in Europe run on LPG with HD 5 being the standard specification for these engines. The strict regulatory framework in the European Union mandates low sulfur and olefin content in vehicle fuels to reduce emissions further cementing the position of HD 5. Additionally, the petrochemical industry prefers HD 5 for propane dehydrogenation units because impurities can poison catalysts and reduce yield efficiency. The growing number of propane dehydrogenation plants in Northern Europe has increased demand for this high purity grade. The consistency in supply quality also reduces maintenance costs for end users making it the preferred choice for commercial heating systems in premium sectors.

The commercial grade propane segment is likely to witness a fastest CAGR of 4.2% during the forecast period driven by its cost effectiveness and expanding use in less sensitive heating applications. This grade typically contains higher levels of propylene and other hydrocarbons which makes it unsuitable for engines but perfectly adequate for space heating and cooking in large commercial establishments. The rising demand for affordable heating solutions in the hospitality and retail sectors across Southern and Eastern Europe is additionally fuelling the growth of the segment. Many small and medium enterprises are opting for commercial grade propane due to its lower price point compared to HD 5 allowing them to manage operational costs effectively. Furthermore the expansion of outdoor dining areas and temporary event structures has created a niche market for portable commercial grade propane cylinders. The flexibility of supply chains for this grade allows distributors to offer competitive pricing and rapid delivery services. Industry reports indicate that the adoption of commercial grade propane in agricultural drying applications has also risen by 8% annually as farmers seek reliable alternatives to electric dryers.

By End User Insights

The residential end user segment was accounted in holding 55.4% of the Europe propane market share in 2025 with the extensive use of propane for heating and cooking in off grid households. This leadership is underpinned by the vast number of rural homes across Europe that lack access to the natural gas grid and rely on propane as their primary energy source. Propane offers a reliable and independent heating option that is not subject to the vulnerabilities of centralized power grids. The aging housing stock in countries like France and Poland requires consistent thermal energy which propane delivers efficiently through modern condensing boilers. The European Heat Pump Association notes that despite the rise of electrification millions of homes remain dependent on fossil fuels due to high retrofitting costs. This structural dependency ensures a stable baseline demand for residential propane. Additionally, the trend towards second homes and vacation properties in coastal and mountainous regions has boosted seasonal propane consumption. These properties often utilize propane for both heating and water heating due to its ease of storage and on demand availability. The emotional preference for gas cooking among European consumers also sustains demand in the kitchen appliance segment.

The industrial end user segment is swiftly emerging at the fastest CAGR of 5.1% from 2026 to 2034 with the expanding petrochemical and manufacturing sectors. This growth is primarily driven by the increasing use of propane as a feedstock for propane dehydrogenation plants which produce propylene a key ingredient in plastic production. As per the American Chemistry Council, European investments in propane dehydrogenation capacity have increased by 15% in the last three years reflecting this strategic shift. Propane offers a cleaner and more efficient route to propylene compared to naphtha cracking reducing carbon emissions and operational costs. Additionally, the metal fabrication and glass manufacturing industries are adopting propane for high temperature processes due to its precise flame control and lower sulfur content. The European Commission’s industrial strategy emphasizes the need for sustainable and efficient energy sources in manufacturing which aligns with propane’s characteristics. The rise of on site energy generation using propane fueled combined heat and power units in industrial parks is another contributing factor.

COUNTRY LEVEL ANALYSIS

Germany Propane Market Analysis

Germany was the largest contributor in the Europe propane market by capturing 23.7% of share in 2025 with its robust industrial base and significant residential heating demand in rural regions. The country’s market status is characterized by a dual focus on maintaining energy security for manufacturing while navigating the complexities of the Energiewende or energy transition. The industrial sector particularly chemicals and metals accounts for a substantial portion of propane consumption due to the presence of major production facilities. The residential sector remains a key driver with millions of homes in southern and eastern Germany relying on propane for heating due to limited natural gas infrastructure. According to the German Liquid Gas Association, the adoption of renewable propane in residential heating grew by 12% in 2025 supported by federal subsidies . Germany’s strategic location and advanced logistics network facilitate efficient distribution of propane across central Europe. The country is also a leader in propane powered fork lifts and industrial vehicles contributing to commercial demand.

Italy Propane Market Analysis

Italy propane market growth is likely to be driven by its world leading adoption of autogas for vehicular use. As per the Italian Ministry of Ecological Transition, there were over 1.1 million LPG vehicles registered in Italy in 2024 representing one of the highest penetration rates globally . This widespread adoption is driven by favorable tax policies that make autogas significantly cheaper than gasoline and diesel. The residential sector also contributes significantly particularly in rural areas and islands where natural gas pipelines are absent. Propane provides a reliable energy source for heating and cooking in these isolated communities. The Italian government has implemented incentives for converting older vehicles to LPG to reduce urban air pollution further boosting demand. The tourism sector also utilizes propane extensively for hospitality services in remote locations. Italy’s strong domestic refining capacity helps stabilize supply although imports remain necessary to meet peak demand. The country’s commitment to reducing carbon emissions in transport ensures that propane will remain a key fuel in the automotive sector.

Poland Propane Market Analysis

Poland propane market growth is likely to grow with heavy reliance on propane for residential heating as a substitute for coal. The stringent anti-smog regulations that are forcing households to switch from solid fuels to cleaner alternatives is impacting positively on the growth of Europe propane market. As per the Central Statistical Office of Poland, over 3 million households in rural areas use liquefied petroleum gases for heating purposes. This transition is supported by government programs such as the Clean Air Program which provides financial assistance for replacing old coal boilers with gas or propane systems. The automotive sector in Poland is also a major consumer with a large fleet of LPG vehicles benefiting from low fuel prices. The country’s strategic position as a gateway for energy imports from the east and west enhances its supply security. Industrial demand is also rising as manufacturers seek reliable energy sources amidst grid instability. Poland’s vast rural landscape ensures a long term demand for decentralized heating solutions. The government’s focus on energy independence and air quality improvement continues to drive policy support for propane.

France Propane Market Analysis

France propane market growth is likely to grow with a balanced demand profile spanning residential agricultural and automotive sectors. The well-established distribution network and a diverse user base that ensures steady consumption throughout the year is also enhancing the growth of Europe propane market. The residential sector is a major driver with many rural homes relying on propane for heating and hot water. The agricultural sector is another significant contributor with propane used for crop drying tobacco curing and poultry farming. This seasonal demand creates peaks in consumption that are managed through robust storage infrastructure. The automotive sector in France has seen a resurgence in LPG vehicle sales driven by environmental zones in major cities that restrict high emission vehicles. France is also exploring the potential of bio propane to meet its climate goals with several pilot projects underway. The country’s commitment to reducing greenhouse gas emissions while maintaining energy affordability supports the continued use of propane.

United Kingdom Propane Market Analysis

The United Kingdom propane market growth is driven with the needs of off grid residential properties and the commercial hospitality sector. The country’s market status is defined by a large number of rural homes that are not connected to the national gas grid and rely on propane for heating. The commercial sector including pubs hotels and restaurants also contributes substantially to demand particularly in rural tourist destinations. The automotive sector in the UK has a smaller but dedicated base of LPG users supported by a network of refueling stations. The government’s net zero strategy includes provisions for renewable gases which opens opportunities for bio propane in the UK market. The resilience of the propane supply during recent energy crises has reinforced its value as a secure energy source.

KEY MARKET PLAYERS

A few of the market players that are dominating the Europe propane market are

- BP Plc (U.K.)

- SHV Energy

- TotalEnergies

- Neste

- Chevron Corporation (U.S.)

- Royal Dutch Shell Plc (U.K.)

- Exxon Mobil Corporation (U.S.)

- ConocoPhillips (U.S)

- Reliance Industries Ltd. (India)

- PetroChina Company Limited (China)

- Sinopec (China)

- Total S A (France)

- Ferrellgas Partners L.P. (U.S.)

Top Players In The Market

- SHV Energy stands as a prominent global player with a substantial footprint across the European liquefied petroleum gas sector. The company operates through well known brands such as Calor and Primagaz delivering reliable energy solutions to residential commercial and industrial customers. SHV Energy focuses heavily on sustainability by investing in renewable propane and bio LPG initiatives to support the transition toward low carbon energy sources. Recent actions include expanding its digital customer platforms to enhance service efficiency and user experience. The company actively partners with local governments to promote safe and clean energy usage in off grid areas. Its strategic emphasis on innovation and customer centric services strengthens its competitive edge. SHV Energy continues to diversify its portfolio by integrating smart metering technologies that allow users to monitor consumption in real time. This approach not only improves operational efficiency but also aligns with broader environmental goals.

- TotalEnergies is a major integrated energy company that plays a critical role in the European propane market through its extensive refining and distribution networks. The company leverages its downstream capabilities to supply high quality liquefied petroleum gases to various sectors including automotive residential and industrial users. TotalEnergies is committed to reducing its carbon footprint by increasing the availability of bio propane and other renewable alternatives. Recent strategic moves involve strengthening partnerships with automotive manufacturers to promote autogas adoption across Europe. The company invests in modernizing its storage and logistics infrastructure to ensure consistent supply chain resilience. TotalEnergies also focuses on digital transformation to optimize distribution routes and improve customer engagement. Its robust research and development efforts aim to enhance the efficiency of propane usage in industrial applications.

- Neste is a leading producer of renewable fuels and has emerged as a significant innovator in the European propane market through its development of renewable propane. The company utilizes its expertise in refining waste and residue materials to create sustainable liquid gas solutions that significantly reduce greenhouse gas emissions. Neste’s renewable propane serves as a drop in replacement for fossil based propane allowing existing infrastructure to be used without modifications. Recent actions include scaling up production capacities at its refineries in Finland and Singapore to meet growing European demand. The company collaborates with major energy distributors to integrate renewable propane into their product offerings. Neste actively promotes the benefits of circular economy principles by converting waste fats and oils into valuable energy resources. Its commitment to sustainability attracts environmentally conscious customers and supports regulatory compliance for businesses.

Top Strategies Used By Key Market Participants

Key players in the Europe propane market primarily focus on product diversification by integrating renewable propane and bio LPG into their portfolios to align with stringent environmental regulations. Companies are heavily investing in digital transformation initiatives such as smart metering and automated delivery systems to enhance operational efficiency and improve customer experience. Strategic partnerships with automotive manufacturers and government bodies are common tactics to promote autogas adoption and secure favorable policy frameworks. Infrastructure modernization is another strategy, where firms upgrade storage facilities and logistics networks to ensure supply chain resilience against geopolitical disruptions. These strategies collectively enable companies to maintain competitiveness while navigating the transition toward a low carbon energy landscape. By balancing traditional fossil fuel supplies with innovative green alternatives industry leaders aim to capture emerging opportunities in both residential and industrial segments. This multifaceted approach ensures long term sustainability and adaptability in a rapidly evolving regulatory environment.

COMPETITIVE LANDSCAPE

The competition in the Europe propane market is characterized by a mix of established energy giants and specialized regional distributors who vie for dominance through service quality and sustainability initiatives. Major players leverage their extensive infrastructure and brand recognition to maintain strong relationships with residential and commercial customers. The market sees intense rivalry in the automotive sector where price competitiveness and refueling network coverage determine consumer preference. Companies are increasingly differentiating themselves by offering renewable propane options which appeal to environmentally conscious buyers and comply with evolving EU regulations. Strategic acquisitions and partnerships are common as firms seek to expand their geographic reach and enhance supply chain efficiency. The entry of new biofuel producers adds further complexity to the competitive landscape by introducing alternative low carbon solutions. Price volatility and supply chain disruptions also influence competitive dynamics forcing companies to adopt flexible pricing models and robust risk management strategies. Innovation in digital services such as remote monitoring and automated billing provides a competitive edge by improving customer retention.

MARKET SEGMENTATION

This research report on the Europe propane market is segmented and sub-segmented into the following categories.

By Grade

- HD – 5

- HD – 10

- Commercial

By End-user

- Residential

- Commercial

- Industrial

- Others

By Country

- UK

- Russia

- Germany

- Italy

- France

- Spain

- Sweden

- Denmark

- Poland

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is currently driving demand in the Europe propane market?

Growing use of propane for heating, cooking, and industrial applications is driving demand.

Why is propane widely used across Europe as an energy source?

It is a versatile and cleaner-burning fuel compared to many traditional options.

How would you describe propane in simple terms?

It is a liquefied petroleum gas used for energy in residential, commercial, and industrial settings.

Where is propane most commonly utilized across Europe?

It is widely used in homes, industries, agriculture, and transportation sectors.

What makes propane a preferred fuel in off-grid areas?

It provides reliable energy where natural gas pipelines are not available.

From a cost perspective, is propane a practical energy option?

Yes, it offers efficient energy use and competitive pricing in many applications.

What challenges are affecting the Europe propane market?

Price volatility and transition toward renewable energy sources are key challenges.

How is the energy transition influencing propane demand in Europe?

Shifts toward cleaner energy are encouraging more efficient and low-emission propane usage.

Which sectors contribute the most to propane consumption?

Residential heating, industrial use, and agriculture are major contributors.

Is the Europe propane market growing steadily?

Yes, it is experiencing moderate growth with stable demand across sectors.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com