Europe Rocket and Missile Market Size, Share, Trends & Growth Forecast Report By Type, By Platform, By Launch Mode, By Propulsion, and By Country (Germany, France, United Kingdom, Italy, Sweden & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034.

Europe Rocket and Missile Market Size

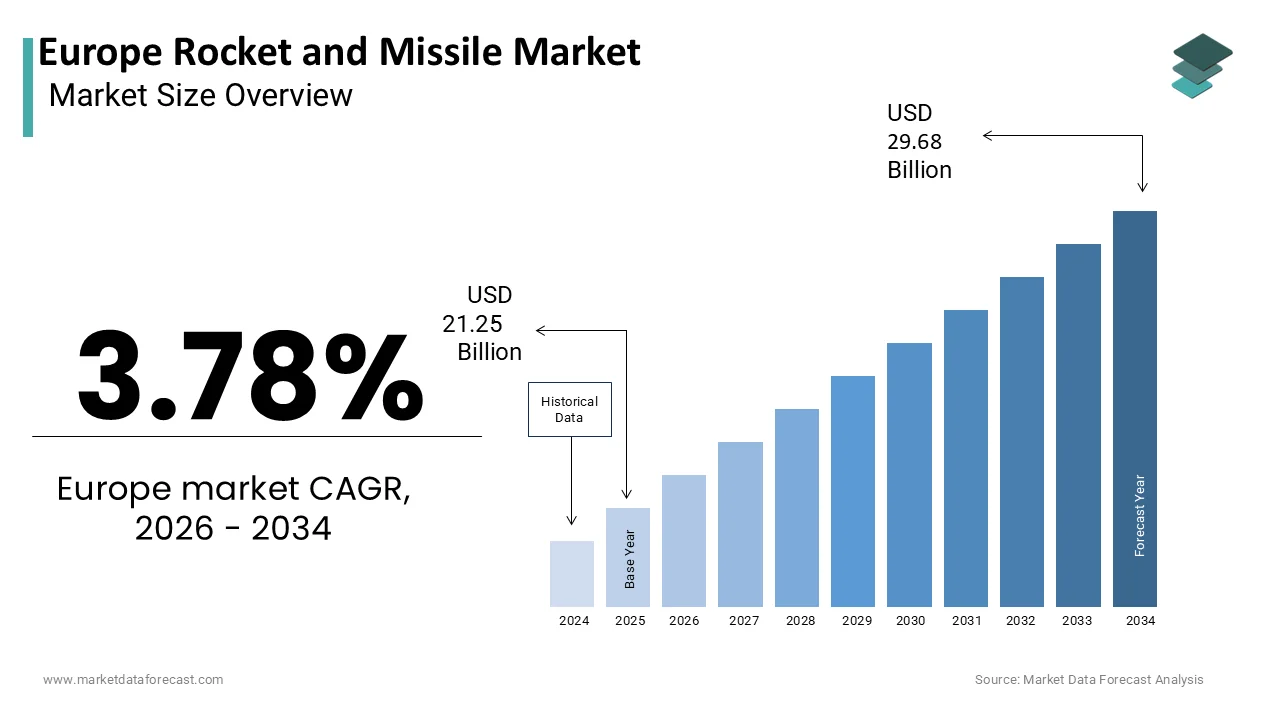

The Europe Rocket and Missile Market was valued at USD 21.25 billion in 2025, is estimated to reach USD 22.06 billion in 2026, and is projected to reach USD 29.68 billion by 2034, growing at a CAGR of 3.78% from 2026 to 2034.

A rocket is a vehicle or device propelled by an engine that carries its own fuel and oxidizer, allowing it to function outside the atmosphere. A missile is fundamentally a rocket or jet-propelled weapon designed for precision, featuring a guidance system to alter its trajectory to hit a target. This market includes ballistic missiles, cruise missiles, air-to-air missiles, surface-to-air missiles, and tactical rockets that serve critical roles in national security and deterrence strategies. The region is witnessing a paradigm shift in defense posture driven by evolving geopolitical threats and the need for sovereign capabilities. According to the Stockholm International Peace Research Institute (SIPRI), total military expenditure in Europe rose by 17% to $693 billion in 2024, marking the sharpest regional increase and the highest level since the end of the Cold War. This financial commitment reflects a broader strategic imperative to modernize armed forces and replenish depleted stockpiles. According to the North Atlantic Treaty Organization, 23 out of 32 member states met the target of spending at least 2 percent of their gross domestic product on defense in 2024. The conflict in Eastern Europe has further accelerated the demand for long-range precision strike capabilities and air defense systems. The European Defence Agency emphasizes the importance of collaborative projects to reduce fragmentation and enhance interoperability among member states. Furthermore, the rise of hypersonic technologies and autonomous systems is reshaping the technological landscape of missile development. As per the European Commission, the European Defence Fund has allocated substantial resources for research and innovation in disruptive technologies, including next-generation missile systems. Consequently, the convergence of heightened security concerns, increased funding, and technological advancement defines the current trajectory of the rocket and missile market in Europe.

MARKET DRIVERS

Escalating Geopolitical Tensions Drive Urgent Procurement of Advanced Systems

The deteriorating security environment in Eastern Europe has served as a primary factor for the accelerated procurement of rocket and missile systems across the continent. This fuels the growth of the Europe rocket and missile market. Nations bordering conflict zones are increasingly prioritizing long-range precision strike capabilities and robust air defense networks to deter potential aggression. According to the Stockholm International Peace Research Institute (SIPRI), total global military expenditure reached $2443 billion in 2023, a 6.8 per cent increase from 2022, with European NATO members specifically boosting budgets by roughly 19 per cent to meet modernization and replenishment needs for ammunition and missile systems. This surge in investment is directly correlated with the need to replenish stockpiles depleted by aid to Ukraine and to enhance national deterrent capabilities. The Polish Ministry of National Defence announced plans to acquire multiple battery systems of high-altitude air defense missiles and long-range ballistic missiles to bolster its strategic posture. Similarly, the German Federal Ministry of Defence has initiated major procurement programs for advanced interceptor missiles to protect critical infrastructure and population centers. As per the European Defence Agency,cy the demand for joint procurement of missile systems has risen significantly among member states seeking to achieve economies of scale and standardization. These statistics illustrate a clear strategic shift towards enhancing missile capabilities in response to perceived threats. The integration of these systems into national defense architectures allows military forces to maintain credible deterrence and rapid response capabilities. Therefore, the imperative to safeguard national sovereignty amidst rising threats has become a dominant driver propelling the Europe rocket and missile market forward with sustained government funding ensuring long-term development and deployment cycles.

Increased Investment in Sovereign Space Launch Capabilities Fuels Demand

Nations in the region are increasingly recognizing the strategic importance of independent access to space, which drives significant investment in domestic rocket and launch vehicle technologies, and thereby propels the expansion of the European rocket and missile market. The reliance on non-European launch providers has raised concerns about strategic autonomy and security, prompting the European Space Agency and national governments to accelerate the development of sovereign launch capabilities. According to the European Space Agency, the budget for launchers and space transportation has seen consistent growth, with member states committing billions of Euros to ensure uninterrupted access to space. The development of next-generation launch vehicles, such as the Ariane 6 and Vega C, requires advanced rocket propulsion systems, guidance units, and structural components. As per the French Space Agency, CNES, France continues to lead efforts in maintaining European independence in space launch capabilities through substantial national funding and industrial partnerships. The rise of small satellite constellations for communication and earth observation further increases the demand for flexible and cost-effective launch solutions. Companies are investing in reusable rocket technologies and solid propellant motors to reduce launch costs and increase frequency. Additionally, the dual-use nature of rocket technology means that advancements in space launchers often benefit military missile programs. So, the strategic push for space sovereignty acts as a powerful driver, stimulating innovation and production in the rocket segment of the market, ensuring Europe maintains its competitive edge in global space operations.

MARKET RESTRAINTS

Stringent Export Control Regulations Restrict Market Expansion

The export of rocket and missile technologies from the region is heavily regulated under various international frameworks and national laws, which constrain the growth of the Europe rocket and missile market. The Missile Technology Control Regime and the Wassenaar Arrangement impose strict guidelines on the transfer of sensitive technologies, including propulsion systems, ms guidance electronics, and materials. According to the European External Action Service, compliance with these regimes requires extensive licensing procedures and end-user verification, which can delay transactions and increase administrative burdens. These regulatory hurdles often limit the ability of European manufacturers to compete in global markets where competitors from less-regulated regions may offer faster delivery times. As per the German Federal Office for Economic Affairs and Export Control (BAFA), Germany maintains a restrictive policy on dual-use and missile technology; however, actual license denials remain numerically low compared to approvals, though strict scrutiny during the application phase acts as a primary regulatory filter. Furthermore, the complexity of navigating different national export laws within the European Union creates fragmentation and inefficiencies for multinational consortia. The risk of technology diversion to unauthorized entities also leads to heightened scrutiny and restricted partnerships. Consequently, the stringent regulatory environment acts as a major restraint by limiting market access and increasing the cost and time associated with international sales. This constraint forces companies to focus primarily on domestic and allied markets, thereby restricting their global revenue potential and slowing down the pace of international collaboration.

High Development Costs and Lengthy Procurement Cycles Constrain Innovation

The development and production of advanced rocket and missile systems involve substantial financial investments and extended timelines, which limit the agility of the Europe rocket and missile market. Research and development for hypersonic missiles or advanced interceptors require specialized facilities, skilled personnel, and extensive testing protocols that can span several years. According to the European Defence Agency,y the average development cycle for a new missile system can exceed ten years from initial concept to operational deployment. This lengthy process delays the introduction of new capabilities and increases the risk of technological obsolescence before the system enters service. As per the National Audit Office of the United Kingdom, d cost overruns in major defense procurement projects are common due to changing requirements and technical complexities. High upfront costs also limit the number of units that can be procured within a fixed defense budget,s leading to smaller fleet sizes. The fragmentation of defense markets across European countries further exacerbates these issues by preventing economies of scale. Small production runs result in higher unit costs, making it difficult for nations to afford large stockpiles. Additionally,y budgetary uncertainties and shifting political priorities can lead to program cancellations or delays, disrupting supply chains. Hence, the high economic and temporal barriers to entry restrict the pace of innovation and modernization, forcing manufacturers to balance advanced capabilities with affordability and efficiency.

MARKET OPPORTUNITIES

Collaborative Defense Initiatives Create Opportunities for Standardized Solutions

Increased defense collaboration among regional nations is creating new paths for the European rocket and missile market. This trend is driven by a focus on joint development programs and standardized procurement processes. Initiatives such as the Permanent Structured Cooperation under the European Union framework encourage member states to invest in shared defense capabilities, reducing duplication and enhancing interoperability. According to the European Defence Fund, approximately 8 billion Euros are available for the 2021 to 2027 period to finance research and development projects, including those focused on missile technologies. This financial support incentivizes consortia of companies from different countries to collaborate on the design and production of next-generation weapons. For example, the Future Cruise Anti-Ship Weapon project involves France, Germany, and other partners working together to develop a common missile system. Such collaborations not only share the financial burden but also pool technical expertise, leading to more robust and versatile platforms. As per the NATO Allied Command Transformation, joint exercises involving missile defense systems have increased, highlighting the importance of interoperable technologies. These exercises provide valuable feedback for manufacturers, allowing them to refine their products based on real-world operational requirements. Furthermore, standardization efforts ensure that missile systems from different manufacturers can operate seamlessly within coalition forces. This harmonization reduces logistical complexities and enhances overall mission effectiveness. Therefore, the push for European strategic autonomy in defense technology drives demand for collaborative missile solutions, ns creating a stable and predictable market environment for industry stakeholders.

Advancements in Hypersonic and Autonomous Technologies Open New Avenues

The rapid advancement of hypersonic and autonomous technologies unlocks potential for the expansion of the Europe rocket and missile market. This is achieved by enabling new classes of strategic weapons. Hypersonic missiles, which travel at speeds greater than Mach 5, present a significant challenge to existing air defense systems due to their speed and maneuverability. According to the European Commission and industry reports, several member states are collaborating on hypersonic defense interceptor programs (e.g., HYDIS², EU-HYDEF) to counter emerging threats, while France actively tests its own hypersonic glide vehicle demonstrator (V-MAX) to enhance national deterrent capabilities. These technologies allow for rapid strike capabilities against time-sensitive targets, enhancing deterrence posture. The integration of artificial intelligence and machine learning into missile guidance systems enables autonomous target recognition and decision-making in contested environments. As per the French Directorate General of Armaments, investments in AI-driven missile technologies are accelerating to improve accuracy and resilience against electronic warfare. The development of swarm missile technologies also presents opportunities for overwhelming adversary defenses through coordinated attacks. These innovations require advanced materials, propulsion systems, and sensors, driving demand for specialized components. Furthermore, the dual-use nature of these technologies allows for spin-off applications in civilian aerospace sectors. Therefore, the focus on next-generation missile capabilities creates a fertile ground for innovation, attracting both established defense primes and agile startups to develop cutting-edge solutions that meet the evolving needs of European armed forces.

MARKET CHALLENGES

Supply Chain Vulnerabilities Pose Risks to Production Stability

Dependency on global supply chains is a significant challenge to the European rocket and missile market. Specifically, reliance on foreign providers for rare earth materials, specialized alloys, and microelectronics hinders progress. Disruptions in these supply chains can severely impact production schedules and compromise national security. According to the European Commission, the EU relies heavily on imports for certain critical raw materials essential for missile production, including lithium and titanium. Geopolitical tensions and trade restrictions can limit access to these materials, causing delays and price volatility. As emphasized by the IPC (Association Connecting Electronics Industries) and European defence analysts, the fragility of the semiconductor supply chain, where Europe produces only 6% of defence-related Printed Circuit Boards (PCBs), poses a direct risk to the production of advanced electronics, including guidance systems for missile programs. The concentration of supply sources in non-European countries creates vulnerabilities that adversaries could exploit. Additionally, the complexity of missile systems requires thousands of specialized parts, many of which are sourced from a limited number of suppliers. Any disruption at a single supplier can halt entire production lines. The lack of redundant supply sources further exacerbates this risk. Manufacturers are struggling to secure long-term contracts for critical components amidst global competition. Consequently, supply chain instability represents a major challenge compelling companies to diversify suppliers and invest in local manufacturing capabilities. However, er achieving self-sufficiency is a long-term objective requiring substantial investment and policy support.

Shortage of Skilled Workforce Hinders Innovation and Capacity

The requirement for a highly specialized workforce with expertise in aerospace engineering, propulsion systems, guidance algorithms, and materials science remains an impediment to the European rocket and missile market. However, Europe faces a growing shortage of qualified professionals in these fields, ds which constrains innovation and production capacity. According to Cedefop (European Centre for the Development of Vocational Training), the European market faces high demand for STEM professionals, with millions of future job openings projected in science and engineering sectors (e.g., 2.3 million openings for researchers and engineers), driven by replacement needs and growth. This talent shortage affects the ability of companies to execute complex development projects and maintain production rates. As per the Aerospace and Defence Industries Association of Europe (ASD), the defense sector is contending with a demographic "cliff" where the aging workforce is retiring at a rate that challenges the industry's ability to replace them with sufficient numbers of new graduates. Universities often struggle to provide practical training in specialized defense technologies due to security restrictions and limited resources. The competition for talent from the commercial space and technology sectors further intensifies the shortage. Companies must invest heavily in training programs and competitive compensation packages to attract and retain skilled engineers. The lack of experienced personnel can lead to project delays, ys quality issues, and increased costs. Additionally, security clearance requirements for working on classified missile programs limit the pool of eligible candidates. Consequently, the scarcity of skilled professionals acts as a critical bottleneck hindering the industry’s ability to meet growing demand and maintain technological leadership. Addressing this issue requires coordinated efforts between industry, academia, and government to promote STEM education and career pathways in defense.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Platform, Launch Mode, Propulsion, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | MBDA, BAE Systems plc, Airbus SE, Thales Group, Leonardo S.p.A., Saab AB, Rheinmetall AG, Diehl Defence GmbH & Co. KG, Safran S.A., Rolls-Royce Holdings plc, Kongsberg Gruppen ASA, Nammo AS |

SEGMENTAL ANALYSIS

By Type Insights

The missile segment was the largest in the Europe rocket and missile market and accounted for a substantial share in 2025. This prom,inence of the segment is mainly supported by the urgent operational requirements of European armed forces to replenish depleted stockpiles and modernize their precision strike capabilities in response to heightened regional security threats. Missiles, air-to-air, air-to-air, IR, and cruise missiles are essential components of national defense architecture, providing critical deterrence and engagement capabilities. According to the Stockholm International Peace Research Institute (SIPRI), European states increased their arms imports by 155% between 2015–19 and 2020–24, with a primary focus on acquiring air defense capabilities to address heightened security threats. The conflict in Eastern Europe has highlighted the critical importance of having sufficient inventories of tactical and strategic missiles to sustain prolonged operations. As per the German Federal Ministry of Defence,nce the country alone has committed billions of Euros to acquire advanced interceptor missiles such as the Patriot and IRIS-T SLM to protect its airspace. Furthermore, the North Atlantic Treaty Organization has emphasized the need for member states to maintain higher readiness levels, which directly translates into increased demand for air-to-surface missile systems. The versatility of missiles across various platforms, including land, sea, and air,r further cements their dominance. Thus, the immediate need for operational readiness and the strategic imperative to restore ammunition reserves drive the sustained leadership of the missile segment in the European market.

However, the rocket segment is anticipated to witness the fastest CAGR of 9.4% from 2026 to 2034. This swift expansion of the segment is propelled by the increasing emphasis on sovereign space access and the development of next-generation launch vehicles for both civilian and military applications. European nations are actively investing in domestic rocket technologies to reduce reliance on non-European launch providers and ensure strategic autonomy in space operations. According to the European Space Agency (ESA), member states have secured the future of European space transportation by committing substantial annual funding to subsidize and stabilize the exploitation models of the Ariane 6 (up to €340 million/year) and Vega C (up to €21 million/year) programs. These projects require advanced rocket propulsion systems and structural components, driving significant market activity. As per the French Space Agen,cy C,, NES France is leading initiatives to develop reusable launch technologies, which necessitate innovative rocket designs and materials. Additionally, the rise of small satellite constellations for communication and earth observation creates a demand for dedicated small lift launch vehicles. The dual-use nature of rocket technology means that advancements in space launchers often contribute to the development of long-range ballistic missiles. Governments are also supporting private sector involvement in the industry, fostering innovation and competition. Therefore, the strategic push for independent space capabilities and the expansion of the commercial space sector drive the rapid growth of the rocket segment.

By Platform Insights

The ground-based segment held the majority share of 45.7% of the Europe rocket and missile market in 2025. This supremacy of the segment is credited to the critical role of ground-launched missiles in national air defense and territorial protection strategies. Surface-to-air missile systems are the backbone of air defense networks, protecting critical infrastructure,e population centers, rs and military bases from aerial threats. According to the North Atlantic Treaty Organization, the enhancement of integrated air and missile defense is a top priority for European allies, leading to significant investment in ground-based interceptor systems. Countries such as Poland, Germany, and the Netherlands have announced major procurement plans for advanced surface-to-air missile batteries to strengthen their defensive posture. As per the European Defence Agency, joint procurement initiatives for ground-based air defense systems have gained momentum, allowing member states to achieve economies of scale and interoperability. The deployment of mobile ground-launched missile systems also provides flexibility and rapid response capabilities in dynamic combat scenarios. Furthermore, the modernization of existing ground-based arsenals with longer range and more accurate missiles contributes to market growth. The strategic importance of denying adversary air superiority ensures sustained demand for ground-based platforms. Hence, the focus on territorial defense and the integration of multi-layer air defense systems sustains the dominance of the ground-based segment in the European market.

But the naval segment is likely to experience the fastest CAGR of 8.8% during the forecast period due to the modernization of European navies and the increasing threat of maritime insecurity. Naval forces are upgrading their fleets with advanced anti-ship and surface-to-air missiles to protect carrier groups and secure sea lines of communication. According to the International Institute for Strategic Studies, several European nations have initiated naval expansion programs, including the construction of new frigates and destroyers equipped with state-of-the-art missile systems. The United Kingdom Royal Navy and the French Marine Nationale are integrating long-range cruise missiles and vertical launch systems into their new vessels to enhance strike capabilities. As per the European Union's Maritime Security Strategy (EUMSS), the rise in hybrid threats and asymmetric warfare in maritime domains necessitates enhanced naval security and power projection capabilities, driving demand for robust defensive and strike missile systems. The development of hypersonic anti-ship missiles also drives innovation in the naval segment as nations seek to maintain technological superiority. Additionally, collaborative projects such as the Future Cruise Anti-Ship Weapon program involve multiple European countries working together to develop common naval missile systems. The strategic importance of controlling maritime approaches and projecting power globally further supports this growth. Thus, the modernization of naval fleets and the emergence of new maritime threats drive the rapid expansion of the naval platform segment.

By Launch Mode Insights

The surface-to-air launch mode segment led the Europe rocket and missile market and captured a 32.3% share in 2025. This leading position of the segment is attributed to the urgent need to protect European airspace from increasingly sophisticated aerial threats, including drones, cruise missiles, and ballistic missiles. The proliferation of unmanned aerial systems in recent conflicts has underscored the vulnerability of static defenses and the need for layered air defense solutions. NATO Allied Air Command and defense assessments highlight a critical surge in demand for air defense, noting in May 2024 that Europe possessed only 5% of the necessary air defense capacity to protect its eastern flank. Germany’s decision to purchase additional IRIS T SLM and Patriot systems exemplifies this trend. According to the Stockholm International Peace Research Institute (SIPRI), global arms revenues for the Top 100 companies reached a record $679 billion in 2024, with European firms recording a 13% revenue increase driven largely by demand for air defense and ammunition due to the war in Ukraine. The integration of radar and command and control systems with surface-to-air missiles enhances their effectiveness in complex electromagnetic environments. Furthermore, the modular nature of modern surface-to-air systems allows for easy deployment and relocation, making them ideal for protecting mobile assets. Thus, the critical requirement for comprehensive air defense coverage ensures the continued leadership of the surface-to-air segment in the European market.

The air-to-surface launch mode segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 10.2% between 2026 and 2034, owing to the modernization of European air forces and the increasing demand for precision strike capabilities from airborne platforms. Air-to-surface missiles allow fighter jets and bombers to engage targets at stand-off distances, reducing exposure to enemy air defenses. European air forces are modernizing their fleets through a mix of procuring F-35 Lightning II stealth fighters (e.g., Germany, Italy, UK) and upgrading existing Eurofighter Typhoon aircraft. The integration of new-generation cruise missiles and tactical bombs into these aircraft drives demand for compatible air-to-surface systems. The French Directorate General of Armaments (DGA) and UK MoD are advancing the Future Cruise/Anti-Ship Weapon (FC/ASW) program. Also, the assessment phase concludes in 2025, with the air-launched variant expected to enter service around 2030. Concurrently, France is initiating the SCALP Mk2 cruise missile upgrade in 2026. The ability to strike high-value targets with precision minimizes collateral damage and enhances operational effectiveness. Additionally, the rise of unmanned combat aerial vehicles creates new opportunities for air-to-surface missiles as these platforms require lightweight and highly accurate weapons. Collaborative efforts among European nations to develop common air-launched weapons further accelerate market growth. Therefore, the evolution of air combat strategies and the adoption of advanced aircraft platforms drive the rapid expansion of the air-to-surface segment.

By Propulsion Insights

The solid propulsion segment dominated the Europe rocket and missile market, accounting for a 55.6% share in 2025. This dominance of the segment is driven by the operational advantages of solid propellant motors, including ease of storage, rapid readiness, ss and high reliability. Solid-fueled missiles can be kept in storage for extended periods and launched with minimal preparation, making them ideal for tactical and strategic defense applications. The majority of short-range and medium-range missile systems currently in service with European armed forces, such as the Meteor and Aster families produced by the MBDA consortium, utilize solid propulsion to ensure immediate readiness and logistical safety. The simplicity of solid motor design also reduces maintenance requirements and lifecycle costs. Avio S.p.A. establishes Italy as a key producer of solid rocket motors in Europe, supplying the P120C boosters for the Ariane 6 and Vega-C programs, as well as propulsion components for the Aster 30 missile defense system. The widespread use of solid propellants, air-to-air and surface-to-air missiles, further reinforces its market leadership. Additionally, advancements in composite materials have improved the energy density and performance of solid motors. The ability to scale solid motors for different missile sizes,s ranging from portable systems to large interceptors, rs ensures broad applicability. Consequently,tly the combination of operational readiness,iness cost effectiveness, and proven technology sustains the dominance of the solid propulsion segment in the European market.

The liquid propulsion segment is expected to exhibit a noteworthy CAGR of 7.6% over the forecast period because of the development of long-range ballistic missiles and space launch vehicles. Liquid propellant engines offer higher specific impulse and throttling capabilities, which are essential for heavy lift launchers and intercontinental range missiles. According to the European Space Agency (ESA), the Ariane 6 launcher relies on a hybrid propulsion architecture, combining cryogenic liquid engines (Vulcain 2.1 and Vinci) for the core and upper stages with high-thrust solid rocket boosters. The need for precise trajectory control and restart capabilities in space missions favors liquid engines over solid motors. As per the German Aerospace Center, research into reusable liquid rocket engines is accelerating as part of efforts to reduce launch costs and increase sustainability. The dual-use nature of liquid propulsion technology means that advancements in space launchers often benefit long-range missile programs. Furthermore, the development of hypersonic cruise missiles may utilize liquid-fueled scramjets or combined cycle engines, which fall under this category. The strategic imperative to maintain independent access to space and develop long-range deterrents drives investment in liquid propulsion. Consequently, the technological advantages of liquid engines for high-performance applications drive the rapid growth of this segment.

COUNTRY LEVEL ANALYSIS

Germany Rockets and Missiles Market Analysis

Germany was the top performer in the Europe rockets and missile market and occupied a share of 22.8% in 2025. Its position is propelled by its robust industrial base and recent commitment to significant defense spending increases. The German Federal Ministry of Defence has launched a special fund of 100 billion Euros to modernize the Bundeswe, hr, with a substantial portion allocated to air defense and missile systems. According to the Stockholm International Peace Research Institute, Germany has become one of the largest importers of defense equipment in Europe, ope particularly surface-to-air missiles. The country is home to major defense contractors such as MBDA Deutschland and Diehl Defence, which are key suppliers of missile technologies. As per the German Aerospace Center, er the nation is also investing heavily in space launch technologies,ies contributing to the rocket segment. The political shift towards greater military responsibility within NATO has accelerated procurement processes for systems like the Patriot and IRIS T. Furthermore, Germany participates in numerous collaborative European missile projects, enhancing its technological capabilities. The strong engineering sector supports the development of advanced guidance and propulsion systems. Consequently, Germany’s financial commitment and industrial capacity sustain its leadership in the European rocket and missile market.

France Rockets And Missile Market Analysis

France was the next prominent country in the Europe rocket and missile market and accounted for a 18.6% share in 2025. This position of the French market is fuelled by its strong emphasis on strategic autonomy and its leading role in the European aerospace industry. France possesses a complete spectrum of missile capabilities from tactical to strategic levels, including nuclear deterrent forces. According to the French Ministry of Armed Forces, the national defense budget has increased consistently, supporting the development and production of next-generation weapons. The country is home to major prime contractors such as MBDA France and ArianeGroup, which drive innovation in missile and rocket technologies. As per the French Space Agency, CNES, France leads European efforts in space launch, ensuring independent access to space. The development of the Future Cruise Anti-Ship Weapon and the ASN4G nuclear cruise missile highlights France’s commitment to maintaining technological superiority. France also exports a significant volume of missile systems to allied nations, strengthening its industrial base. The government’s support for research and development in hypersonics and artificial intelligence further enhances its competitive edge. So, France’s comprehensive defense strategy and aerospace prowess maintain its prominent position in the regional market.

United Kingdom Rockets and Missiles Market Analysis

The United Kingdom holds a noteworthy share of the Europe rocket and missile market owing to its advanced defense technology sector and strong naval traditions. Moreover, the UK Ministry of Defence has prioritized the modernization of its nuclear deterrent and the enhancement of conventional strike capabilities. According to the ADS Group, the UK aerospace and defense sector continues to invest heavily in the research and development of precision-guided munitions. The country is a key partner in multinational missile programs and maintains a robust domestic industry led by companies such as MBDA UK. As per the UK Ministry of Defence, the UK is focusing on integrating advanced missiles into its new class of frigates and submarines to project power globally. The development of hypersonic technologies and autonomous systems is also a key area of investment. The UK’s exit from the European Union has led to adjustments in supply chains, ns but collaboration on security matters remains strong. The presence of world-class research institutions supports innovation in propulsion and guidance. Hence, the UK’s technological expertise and strategic priorities ensure its significant role in the European market.

Italy Rockets And Missile Market Analysis

Italy grew steadily in the Europe rocket and missile market due to its strong manufacturing capabilities in aerospace and defense, particularly in the production of solid rocket motors and tactical missiles. According to Avio S.p.A., Italy is a leading supplier of propulsion systems for European launch vehicles and missile programs. The country is home to Av, io a key player in the space launch sector,r and Leonardo, which produces a wide range of missile systems. As per the Italian Ministry of Defense, defense spending has increased to meet NATO targets, supporting the modernization of armed forces. Italy actively participates in European collaborative projects such as the Future Cruise Anti-Shippon, enhancing its technological base. The country also has a strong export orientation, selling missile systems to various international customers. The presence of specialized clusters for aerospace and defense in regions like Lazio and Piedmont fosters innovation and efficiency. Government incentives for research and development further support the industry. Thus, Italy’s industrial strength and active participation in European defense initiatives sustain its significant market presence.

Sweden Rockets And Missile Market Analysis

Sweden is likely to command a prominent share of the regional market over the forecast period owing to its recent accession to NATO and its historically strong defense industry. Also, Sweden has long maintained a policy of armed neutrality, which required the development of indigenous defense capabilities,s including advanced missile systems. According to the Swedish Ministry of Defence, the country is now integrating its systems with NATO standards while continuing to invest in domestic production. Saa, a major Swedish defense company,ny is a key producer of air-to-air and surface-to-air missiles. As per the Inspectorate of Strategic Products (ISP), the defense sector is experiencing growth due to increased government orders and export opportunities. The country is also investing in space technologies, including small satellite launchers, which contribute to the rocket segment. The strategic location of Sweden in the Baltic region has increased its importance in regional security architecture. Collaboration with neighboring Nordic countries and NATO allies is expanding. The focus on high-tech solutions and innovation ensures competitiveness. Consequently, Sweden’s strategic shift and industrial capabilities maintain its position as a key market participant.

COMPETITIVE LANDSCAPE

The competition in the Europe rocket and missile market is characterized by a mix of large multinational consortia and specialized national defense contractors. Leading players compete based on technological innovation, system reliability, and the ability to deliver complex integrated solutions. The market sees intense rivalry in the development of next-generation weapons such as hypersonic missiles and advanced air defense systems. Established companies leverage their extensive experience and strong relationships with government entities to secure major procurement contracts. Collaboration is a defining feature of the competitive landscape as nations seek to pool resources for costly development projects. Intellectual property protection and export control compliance are critical factors influencing competitive dynamics. New entrants face high barriers to entry due to stringent regulatory requirements and the need for specialized expertise. Price competition is less significant than performance and strategic value, which are paramount in defense procurement. The push for European strategic autonomy encourages domestic production and reduces reliance on non-European suppliers. Consequently, the market is driven by continuous innovation,n strategic alliances, es and adherence to rigorous security standards.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Rocket and Missile Market include

- MBDA

- BAE Systems plc

- Airbus SE

- Thales Group

- Leonardo S.p.A.

- Saab AB

- Rheinmetall AG

- Diehl Defence GmbH & Co. KG

- Safran S.A.

- Rolls-Royce Holdings plc

- Kongsberg Gruppen ASA

- Nammo AS

TOP LEADING PLAYERS IN THE MARKET

- MBDA is a leading European missile systems company with significant operations in France, Germany, Italy, and the United Kingdom. The group designs, develops, and produces a comprehensive range of missile systems for air, land,, nd and sea domains. Its contribution to the global market includes advanced solutions such as the Meteor-to-air missile and the Storm Shadow cruise missile. Recent actions involve the acceleration of the Future Cruise Anti-Ship Weapon program in partnership with other European nations. MBDA actively invests in hypersonic technologies and artificial intelligence to enhance missile capabilities. The company strengthens its position through collaborative projects that promote interoperability among allied forces. By focusing on innovation and strategic partnerships, MBDA maintains its status as a key provider of sophisticated defense solutions. This approach ensures it meets the evolving security needs of European governments and international customers effectively.

- ArianeGroup is a major aerospace manufacturer specializing in launch vehicles and ballistic missiles with headquarters in France and Germany. The company plays a pivotal role in ensuring European sovereign access to space through the development of the Ariane and Vega launcher families. Its global contribution includes providing reliable and competitive launch services for institutional and commercial satellites. Recent actions focus on the operational readiness of the Ariane 6 launcher and the development of reusable rocket technologies. ArianeGroup also contributes to national defense programs by supplying solid rocket motors for strategic missiles. The company collaborates closely with the European Space Agency and national governments to advance space transportation capabilities. By integrating vertical production chains and fostering innovation, ArianeGroup strengthens its market position. This strategic focus on sustainability and autonomy supports Europe’s long-term goals in space and defense sectors.

- Diehl Defence is a prominent German defense contractor specializing in air defense systems and guided munitions. The company is widely recognized for its IRIS-T family of missiles, which serves as a critical component of modern air defense networks. Its contribution to the global market includes providing highly effective short- and medium-range surface-to-air missile systems. Recent actions involve scaling up production capacities to meet surging demand from European nations seeking to replenish stockpiles. Diehl Defence actively participates in multinational collaborations to enhance the interoperability of its systems within NATO frameworks. The company invests heavily in research and development to improve sensor fusion and target acquisition capabilities. By delivering proven and reliable defense solutions, Diehl Defence strengthens its reputation as a trusted partner. This commitment to quality and rapid delivery supports its growth in the competitive European rocket and missile market.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe rocket and missile market primarily focus on international collaborations and joint ventures to share development costs and enhance technological capabilities. Companies actively participate in multinational programs to create standardized systems that ensure interoperability among allied forces. Investment in research and development is a central strategy aimed at advancing hypersonic technologies,,artificial intelligence, and autonomous guidance systems. Manufacturers also prioritize expanding production capacities to address the urgent demand for replenishing depleted stockpiles. Strategic partnerships with government agencies facilitate secure funding and long-term contracts essential for sustained innovation. Firms emphasize supply chain resilience by diversifying sources for critical components such as semiconductors and raw materials. Additionally, companies focus on exporting advanced systems to allied nations to strengthen geopolitical ties and generate revenue. By combining technological leadership with robust industrial cooperation,n key participants maintain their competitive edge and support European strategic autonomy in defense capabilities.

MARKET SEGMENTATION

This research report on the europe rocket and missile market is segmented and sub-segmented into the following categories.

By Type

- Missiles

- Rockets

By Platform

- Ground-Based

- Naval

- Airborne

By Launch Mode

- Surface-to-Air

- Air-to-Surface

- Surface-to-Surface

- Air-to-Air

By Propulsion

- Solid Propulsion

- Liquid Propulsion

By Country

- Germany

- France

- United Kingdom

- Italy

- Sweden

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com