Europe Rye Market Size, Share, Trends, & Growth Forecast Report By Type (Whole, Processed), Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Rye Market Report Summary

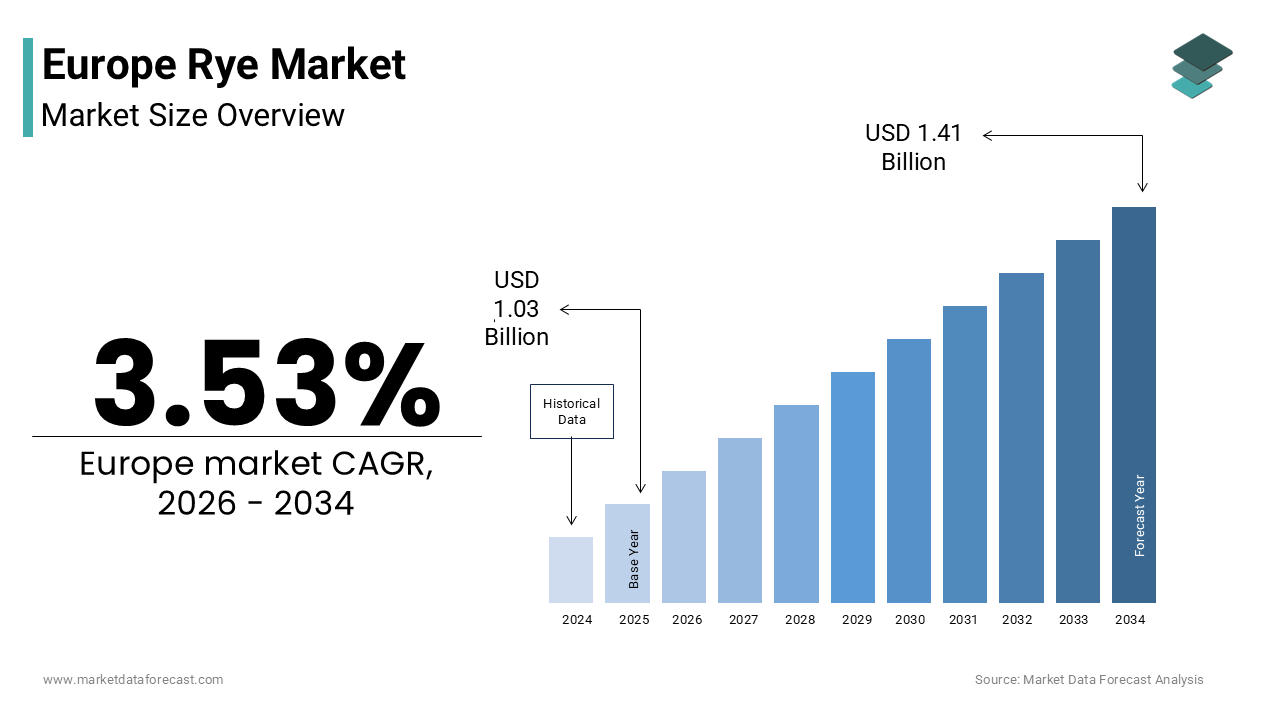

The Europe rye market was valued at USD 1.03 billion in 2025, is estimated to reach USD 1.07 billion in 2026, and is projected to reach USD 1.41 billion by 2034, growing at a CAGR of 3.53% during the forecast period from 2026 to 2034. The growth of the Europe rye market is driven by increasing demand for functional and whole-grain foods, rising awareness of rye’s nutritional benefits, and supportive agricultural policies promoting crop diversification. Rye is widely used in bread, flour, animal feed, and alcoholic beverages, and is gaining renewed importance due to its resilience in poor soil conditions and alignment with sustainable farming practices. Additionally, the European Green Deal and Farm to Fork Strategy are encouraging the cultivation of climate-resilient crops like rye, further supporting market growth.

Key Market Trends

- Rising demand for traditional and artisanal rye bread across Europe.

- Increasing use of rye in functional foods due to its high fiber and low glycemic index properties.

- Growing adoption of rye in plant-based and clean-label food products.

- Expansion of rye applications in biofuels and bioeconomy value chains.

- Strong policy support for crop diversification and sustainable agriculture practices.

Segmental Insights

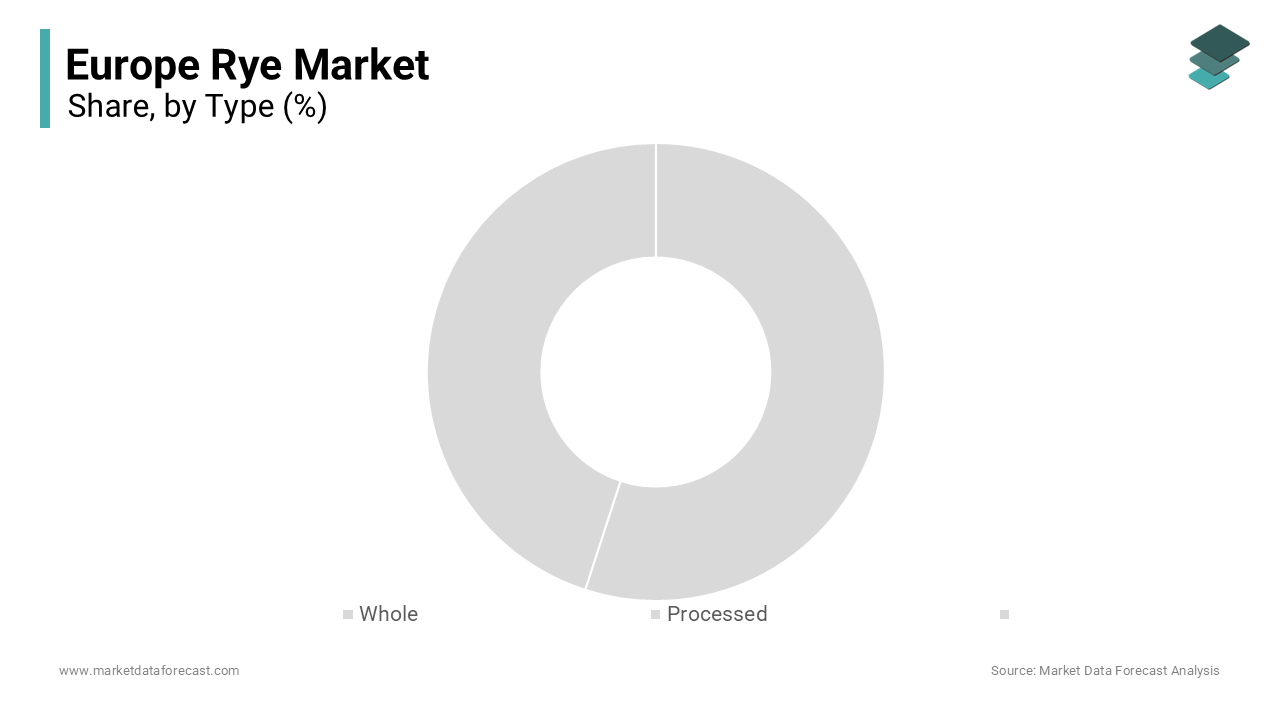

- By type, the processed rye segment held the largest share of the Europe rye market in 2025. This dominance is attributed to its widespread use in flour production and bakery applications, particularly in countries with strong rye bread consumption traditions.

- The whole rye grain segment is expected to grow at the fastest CAGR of 7.4% during the forecast period, driven by increasing demand for minimally processed, high-fiber, and nutrient-rich ingredients in functional foods and plant-based diets.

- By application, the food segment accounted for the largest share of the Europe rye market in 2025 due to its extensive use in bread, bakery products, and traditional European diets.

- The beverage segment is projected to grow at the fastest CAGR of 12.2%, supported by rising demand for rye-based spirits and functional beverages, including fermented drinks and craft alcohol products.

Regional Insights

The Europe rye market is strongly concentrated in Northern and Eastern Europe, where rye has deep cultural and agricultural significance.

-

Poland held the largest share of the Europe rye market in 2025 due to its position as the leading producer and strong consumption of rye-based foods and beverages.

-

Germany is a key market driven by its advanced milling industry, high demand for rye bread, and strong regulatory framework supporting quality standards.

-

Denmark plays a strategic role with its focus on sustainable agriculture and high adoption of rye in daily diets and public nutrition programs.

-

Sweden is witnessing growth through both traditional consumption and innovative applications such as bioethanol and functional food ingredients.

-

Finland represents a unique market where rye is deeply integrated into daily nutrition, supported by public health policies promoting whole-grain consumption.

Competitive Landscape

The Europe rye market is moderately fragmented, with competition across agricultural cooperatives, seed developers, and food processing companies. Market players focus on genetic innovation, sustainable sourcing, and functional food development to strengthen their market position. Major companies operating in the Europe rye market include Lantmännen, The Soufflet Group, Tereos Group, BayWa AG, Agravis Raiffeisen AG, DLG Group, Tartu Mill AS, Verbio SE, Kärntnermilch Agrar, and Polskie Młyny S.A.

Europe Rye Market Size

The Europe rye market size was valued at USD 1.03 billion in 2025 and is anticipated to reach USD 1.07 billion in 2026 from USD 1.41 billion by 2034, growing at a CAGR of 3.53% during the forecast period from 2026 to 2034.

Rye encompasses the cultivation, processing, and utilization of Secale cereale, which is a cold tolerant cereal grain historically central to the dietary and agricultural systems of Northern and Eastern Europe. Unlike wheat, rye thrives in sandy, acidic, and low fertility soils, which is making it a resilient crop for marginal lands in countries such as Poland, Germany, and the Baltic states. Primarily used for flour, bread, animal feed, and increasingly for distilled spirits and functional food ingredients, rye holds cultural and nutritional significance across the continent. According to Eurostat, the European Union harvested rye in 2023, with Poland, Germany, and Denmark contributing the majority share. The crop’s deep root system contributes to soil health and carbon sequestration, which is aligning with the European Green Deal’s objectives for sustainable agriculture. As per the European Environment Agency, rye-based crop rotations help reduce nitrogen leaching compared to continuous maize systems. Furthermore, the European Commission’s Farm to Fork Strategy promotes diversification of cereal crops to enhance agro biodiversity and reduce input dependency. These agronomic and policy dynamics position rye not merely as a commodity but as a strategic component of Europe’s climate smart food system.

MARKET DRIVERS

Revival of Traditional Rye Bread in Culinary and Health-Conscious Diets

Consumer rediscovery of heritage grains has reignited demand for rye, particularly in the form of traditional sourdough rye bread valued for its dense texture, low glycemic index, and high fiber content, which is one of the major factors propelling the growth of the European rye market. As per the European Food Information Council, consumers in Germany, Poland, and Finland associate rye bread with digestive health and sustained energy release. Scientific validation further fuels this trend, as per the European Journal of Clinical Nutrition, daily consumption of whole grain rye has been shown to improve metabolic responses in adults with risk factors. In response, major retailers like Edeka in Germany and Kesko in Finland have expanded their artisanal rye bread sections with clear labeling of fiber content and origin. Additionally, the Nordic Nutrition Recommendations 2023 endorse whole grain rye as a staple for cardiovascular prevention, influencing national dietary guidelines in Sweden and Denmark. This convergence of cultural identity, scientific endorsement, and retail visibility transforms rye from a regional staple into a pan European functional food driving consistent demand beyond seasonal or ceremonial use.

Mandatory Crop Diversification Under the Common Agricultural Policy

The European Union’s Common Agricultural Policy reform for 2023 to 2027 enforces compulsory crop diversification on farms larger than 10 hectares requiring at least two crops with no single crop covering more than 75% of arable land, which is further boosting the rye market expansion in Europe. As per the European Commission, this measure incentivizes the inclusion of rye in rotation systems, particularly in monoculture dominated regions like Northern France and the Netherlands. Rye’s agronomic benefits such as weed suppression through allelopathy and improved soil structure via extensive rooting make it an ideal rotational partner for maize and oilseed rape. As per the Federal Ministry of Food and Agriculture in Germany, rye area increased among farms participating in eco schemes tied to CAP payments. Similarly, Denmark’s Green Development and Demonstration Programme allocated funding to support rye cover cropping for erosion control on sandy soils. These policy levers stabilize rye cultivation and enhance its ecosystem services, which is positioning it as a compliance tool and environmental asset rather than solely a cash crop.

MARKET RESTRAINTS

Declining Arable Land Allocation Due to Economic Marginality

Rye faces persistent pressure from more profitable cereals such as wheat and barley which offer higher yields and stronger market pricing, particularly in Western Europe, which is impeding the regional market growth. According to Eurostat, the area under rye cultivation in the European Union has declined, with France and the United Kingdom recording the steepest reductions. This contraction stems from rye’s lower average yield compared to wheat, as per the Joint Research Centre of the European Commission. Farmers in high input cost regions often view rye as economically nonviable despite its low fertilizer requirements. In Italy and Spain, rye is now largely restricted to mountainous zones with minimal mechanization potential, limiting scalability. Moreover, the absence of dedicated premium markets for feed grade rye reduces incentive for consistent production. Without targeted income support or value-added processing channels, rye remains vulnerable to displacement by higher return crops, especially as land consolidation accelerates across the EU.

Limited Industrial Processing Infrastructure and Market Fragmentation

The Europe rye market suffers from underdeveloped and fragmented processing infrastructure which constrains value addition and product consistency. Unlike wheat, which benefits from integrated milling, baking, and export networks, rye milling capacity is concentrated in a few Nordic and Baltic facilities with limited throughput. As per the German Agricultural Society, only a small number of specialized rye mills operate in the EU capable of producing high extraction flour suitable for premium bread. This scarcity forces bakers in Southern Europe to import flour at significant cost or substitute with wheat rye blends that compromise authenticity. Furthermore, the lack of standardized grading systems for rye grain leads to quality variability, deterring large scale food manufacturers. As per the European Bakery Association, many artisanal bakers cite inconsistent rye flour protein content as a major production challenge. Without coordinated investment in milling technology, quality protocols, and logistics, the market remains segmented between localized traditional use and underpenetrated industrial potential.

MARKET OPPORTUNITIES

Expansion of Rye in Plant Based and High Fiber Functional Foods

Food manufacturers are increasingly incorporating rye into plant based and high fiber product portfolios to meet evolving consumer demand for clean label functional ingredients, which is a prominent opportunity in the European rye market. Rye bran and whole grain flour are rich in arabinoxylan, beta glucan, and resistant starch, all recognized for prebiotic and cholesterol lowering effects. For instance, product launches featuring rye in European breakfast cereals, snack bars, and meat analogues have increased, with Germany and Sweden leading innovation. Companies like Oatly and Alpro have begun blending rye fiber into oat based dairy alternatives to enhance satiety and texture without artificial additives. The European Commission’s 2023 update to nutrition and health claims regulation permits the use of “high in fiber” labeling for products containing rye fiber, facilitating marketing. Additionally, Finland’s VTT Technical Research Centre developed a rye protein isolate with emulsifying properties now licensed to vegan cheese startups in the Netherlands. These developments unlock new revenue streams beyond traditional bread and feed, creating scalable demand for fractionated rye components.

Integration of Rye into Bioeconomy and Renewable Energy Value Chains

Rye is emerging as a feedstock for advanced biofuels and biobased chemicals, which is aligning with the EU’s Renewable Energy Directive II targets and is another major opportunity in the European market. Its high starch and lignocellulosic content make it suitable for second generation ethanol and biogas production, particularly when grown on marginal lands unsuitable for food crops. As per the European Bioeconomy Coalition, rye has been diverted to biorefineries in Germany and Poland under national biofuel blending mandates. In Sweden, Lantmännen Agro Eco operates a biorefinery that converts rye straw and grain into bioethanol and animal feed in a circular model certified under ISCC sustainability standards. The European Investment Bank approved funding to expand this facility’s capacity. Furthermore, rye’s winter growth cycle allows it to serve as a cover crop that prevents soil erosion while producing biomass, benefits recognized under the EU Soil Health Law proposal. This diversification into energy and chemical applications provides price stability and reduces reliance on volatile food markets.

MARKET CHALLENGES

Climate Induced Yield Volatility and Fusarium Head Blight Outbreaks

Rye production in Europe is increasingly undermined by climate driven disease pressure, particularly Fusarium head blight which thrives in warm humid conditions during flowering and is one of the major challenges to the European rye market growth. According to the Julius Kühn Institute in Germany, Fusarium incidence in rye fields has risen due to more frequent late spring rainfall events linked to climate change. This fungal infection not only reduces yield but also contaminates grain with mycotoxins such as deoxynivalenol, which are strictly regulated under EU Commission Regulation 1881 2006. In Poland, rye has been rejected from human consumption due to mycotoxin levels exceeding thresholds, as reported by the Chief Sanitary Inspectorate. Breeding for resistance remains slow due to limited public investment compared to wheat. Without robust integrated pest management protocols and early warning systems, farmers face recurring losses that deter long term cultivation commitments, especially in Central Europe where weather patterns are becoming less predictable.

Lack of Coordinated Breeding Programs and Genetic Improvement

The Europe rye market is hindered by insufficient investment in modern varietal development compared to other cereals, resulting in stagnant yields and limited adaptation to contemporary agronomic challenges. As per the European Cooperative Programme for Plant Genetic Resources, only a few public rye breeding programs operate at scale in the EU, located in Germany, Poland, and Denmark, with relatively low annual R and D funding. In contrast, wheat breeding receives significantly higher public investment. This disparity means most rye varieties in commercial use were released before 2010 and lack traits such as lodging resistance, drought tolerance, and low pre harvest sprouting. As per the Nordic Genetic Resource Center, newer rye hybrids yield only modest improvements compared to older cultivars, while wheat has achieved far greater gains. Without accelerated genomic selection and public private partnerships, rye will struggle to compete in precision agriculture systems where input efficiency and uniformity are paramount. This genetic stagnation represents a structural bottleneck to the crop’s modernization and scalability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.53% |

| Segments Covered | By Type, Application and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe.. |

| Market Leaders Profiled | Lantmännen, The Soufflet Group, Tereos Group, BayWa AG, Agravis Raiffeisen AG, DLG Group, Tartu Mill AS, Verbio SE, Kärntnermilch Agrar, and Polskie Młyny S.A. |

SEGMENTAL ANALYSIS

By Type Insights

The processed rye segment led the market by holding 65.5% of the European market share in 2025. The dominance of processed rye segment in the European market is attributed to its direct integration into food manufacturing and retail supply chains and the widespread use of rye flour in traditional bread production, particularly in Northern and Eastern Europe where regulatory and cultural norms favor whole grain content. As per the German Federal Ministry of Food and Agriculture, most rye harvested in Germany is milled close to the farm, ensuring freshness and reducing transport emissions. The European Commission’s 2023 update to the EU School Scheme allocated funding for whole grain rye bread in school meals across multiple member states, reinforcing institutional demand. Additionally, processed rye enables standardized baking performance through controlled protein and enzyme levels, which is critical for industrial bakeries producing consistent loaves at scale. In Finland, the National Nutrition Council mandates that all public catering services include at least one whole grain rye product daily, a policy widely adopted as per the Finnish Institute for Health and Welfare. These structural and policy driven factors ensure processed rye remains the primary commercial form.

On the other hand, the whole rye grain segment is the fastest growing type segment and is estimated to witness a promising CAGR of 7.4% over the forecast period in the European market owing to the rising demand for minimally processed ingredients in plant based and functional food innovation. Unlike milled products, whole rye retains its bran, germ, and endosperm, offering maximum fiber, polyphenols, and resistant starch as nutrients increasingly linked to gut health and metabolic regulation. As per the European Food Safety Authority, scientific opinion confirms that daily intake of whole grain rye contributes to normal bowel function, supporting authorized health claims. Food startups in Sweden and the Netherlands now use whole rye berries in ready to eat grain bowls, fermented beverages, and meat analogues, which is leveraging its chewy texture and nutty flavor. The European Organic Regulation permits whole rye to carry the EU organic logo without further processing, making it attractive for clean label positioning. Furthermore, farm to table restaurants in Berlin and Copenhagen feature whole rye in seasonal menus sourced directly from regenerative farms. This culinary and nutritional repositioning transforms whole rye from a feed or milling input into a premium consumer ingredient, which is fuelling rapid growth.

By Application Insights

The food segment led the market by capturing 51.8% of the European market share in 2025. The dominance of food segment in the European market can be credited to centuries old bread traditions and reinforced by modern nutritional science. As per the European Bakery Association, rye bread consumption remains high in countries like Poland, Germany, Finland, and Denmark. The dominance is further sustained by regulatory frameworks—Finland’s National Nutrition Policy requires that a significant portion of flour used in public sector bread be whole grain rye. In Germany, the “Roggenbrot” designation is protected under national food law mandating minimum rye content and sourdough fermentation. Retailers like Lidl and Aldi have expanded private label rye bread lines with clear fiber and origin labeling, responding to consumer demand for transparency. Additionally, the European Commission’s 2023 revision of front of pack nutrition labeling favors high fiber, low glycemic foods, giving rye bread a competitive edge over refined wheat alternatives. These cultural, institutional, and regulatory pillars ensure food remains the core application despite diversification into other sectors.

However, the beverage segment is the fastest growing application for rye in Europe and is predicted to witness a CAGR of 12.2% over the forecast period due to the craft spirits boom and functional drink innovation. Rye is a key grain in premium vodka and gin production, with EU geographical indications such as “Żubrówka” in Poland and “Koskenkorva” in Finland mandating specific rye varieties. As per the European Spirits Organisation, craft distilleries using rye have increased, with Germany and Sweden leading new registrations. Beyond alcohol, rye is gaining traction in non alcoholic fermented beverages—Swedish startup Oatly launched a rye water kefir marketed as a gut health tonic. As per the European Food Safety Authority, health claims linking rye arabinoxylan to reduced postprandial glucose response have spurred development of functional tonics and sports drinks. Moreover, rye’s low allergen profile compared to barley makes it suitable for gluten reduced beverage formulations under EU Regulation 828 2014. These converging trends in premiumization, health, and innovation position beverage as the highest growth frontier.

REGIONAL ANALYSIS

Poland Rye Market Analysis

Poland led the rye market in Europe in 2025 with 30.8% of the regional market share. Poland is the continent’s top producer and a cultural stronghold of rye consumption. As per Statistics Poland, the country harvested rye in 2023, with a majority used for traditional bread and spirits. The national diet includes rye in daily meals from chleb żytni to żurek soup, reinforcing intergenerational demand. Poland’s Ministry of Agriculture supports rye through the Rural Development Program, allocating funding for modernization of small mills and distilleries. The country also hosts numerous registered craft distilleries producing rye based spirits protected under EU geographical indications. Climate suitability, particularly in the Lublin and Masovia regions, enables high yielding cultivation with minimal irrigation. Additionally, Polish research institutes like IHAR Radzików have released new fusarium resistant varieties such as “Danko,” improving yield stability.

Germany Rye Market Analysis

Germany plays a pivotal role in the Europe rye market through its advanced milling infrastructure, strong regulatory standards, and high per capita consumption. As per the Federal Statistical Office, national production of rye in 2023 was largely processed into flour for bread. German food law defines “Roggenmischbrot” as containing at least 50% rye flour, ensuring market authenticity. The country hosts Europe’s largest concentration of industrial rye bakeries, including Kamps and Harry, that supply national and export markets. Germany’s Federal Ministry for Economic Affairs allocated funding in 2023 to support rye based bioeconomy projects, including biogas from straw. Furthermore, the “Bio Roggen” organic rye initiative certified tens of thousands of hectares in 2023, meeting rising demand for pesticide free grain. Urban consumers in cities like Berlin and Munich increasingly seek heritage grain bread from artisanal bakeries, driving premiumization.

Denmark Rye Market Analysis

Denmark maintains a strategic position in the Europe rye market through its leadership in sustainable agronomy and functional food science. As per Statistics Denmark, rye production in 2023 was predominantly grown under low input or organic systems. Danish research institutions like Aarhus University have pioneered rye varieties with enhanced fiber profiles for metabolic health applications. The national dietary guidelines recommend rye bread as a daily staple, a message reinforced through public health campaigns as per the Danish Health Authority. Companies like Lantmännen Danmark supply rye flour to major Nordic supermarkets under traceable sustainability labels. Additionally, Denmark’s Green Tripartite Agreement mandates that public institution bread must increasingly include whole grain rye.

Sweden Rye Market Analysis

Sweden occupies a distinctive niche in the Europe rye market by blending traditional consumption with cutting edge bioeconomy applications. As per Statistics Sweden, national rye output in 2023 was used both for bread and renewable ethanol. The state owned Lantmännen operates a biorefinery in Norrköping that converts rye grain and straw into bioethanol, animal feed, and lignin based chemicals certified under ISCC standards. Swedish consumers eat rye bread regularly, with knäckebröd being a dietary staple fortified with seeds and whole rye. The Swedish Board of Agriculture’s eco subsidy scheme rewarded farmers for rye cover cropping on sandy soils, reducing nitrogen leaching. Moreover, Stockholm’s public schools serve rye crispbread daily as part of the National School Meal Program.

Finland Rye Market Analysis

Finland holds a culturally embedded and scientifically advanced position in the Europe rye market, characterized by near universal consumption and public health integration. As per Natural Resources Institute Finland, rye production in 2023 was overwhelmingly used for food. Finnish adults consume rye daily, primarily as ruisleipä, a dense sourdough loaf protected under national food heritage laws. The National Nutrition Council mandates rye inclusion in all public catering and school meals, a policy implemented nationwide as per the Finnish Institute for Health and Welfare. Research from the University of Eastern Finland has linked rye consumption to reduced risk of type 2 diabetes, leading to its inclusion in clinical dietary recommendations. Companies like Fazer and Raisio export rye products across Europe under certified health claims. This fusion of tradition, science, and policy makes Finland a benchmark for rye’s role in preventive nutrition.

COMPETITIVE LANDSCAPE

The Europe rye market features a dual competitive structure with large integrated agri food cooperatives coexisting alongside specialized seed companies and artisanal food producers. Competition in the upstream segment is driven by genetic innovation and agronomic support with breeders like RAGT and KWS Saat competing on yield stability and disease resistance. Downstream competition centers on brand authenticity nutritional science and sustainability storytelling with companies like Fazer and Barilla leveraging cultural heritage to command premium pricing. Unlike commoditized grains rye benefits from strong regional identities—German “Roggenbrot” Polish “chleb żytni” and Finnish “ruisleipä”—which create natural market segmentation. However fragmentation persists in processing with limited milling capacity outside Nordic and Baltic regions constraining scale. New entrants face high barriers including varietal adaptation regulatory compliance and consumer trust. Overall the market rewards those who combine agronomic excellence with compelling health and heritage narratives.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe transport management system market include

- Lantmännen

- The Soufflet Group

- Tereos Group

- BayWa AG

- Agravis Raiffeisen AG

- DLG Group

- Tartu Mill AS

- Verbio SE

- Kärntnermilch Agrar

- Polskie Młyny S.A.

Top Players in the Market

Lantmännen

Lantmännen is a leading Nordic agricultural cooperative and a major force in the Europe rye market with integrated operations spanning farming milling and food production. Headquartered in Sweden the group sources rye from over 8000 member farmers across Sweden Denmark and Finland ensuring traceable and sustainable supply. Lantmännen contributes globally by exporting rye flour and functional ingredients to Asia and North America while promoting Nordic dietary patterns rich in whole grains. The company operates one of Europe’s most advanced biorefineries in Norrköping converting rye into bioethanol animal feed and high fiber food components. In February 2024 Lantmännen launched a new line of climate certified rye flour with verified carbon footprint data enabling bakeries to meet EU Green Public Procurement criteria. This initiative reinforces its leadership in sustainable grain value chains.

RAGT Semences

RAGT Semences is a prominent French plant breeding company specializing in cereal genetics with a strong portfolio of high yielding disease resistant rye varieties adapted to diverse European climates. The company plays a critical role in the global rye market by developing hybrids that address key agronomic challenges such as Fusarium head blight and lodging. RAGT’s research station in Toulouse collaborates with public institutions across the EU to accelerate genomic selection for improved fiber and starch profiles. In November 2023 the company released “RGT Planet” a new rye variety with 15 percent higher yield potential and enhanced drought tolerance validated in trials across Germany Poland and France. This innovation supports farmers in marginal regions while aligning with the EU’s Farm to Fork objectives for input reduction and resilience.

Fazer Group

Fazer Group is a Finnish food and confectionery leader renowned for its heritage rye bread and baked goods that define Nordic culinary identity. The company sources 100 percent of its rye from Finnish farms under long term contracts ensuring quality and supply stability. Fazer contributes to the global market by exporting its rye crispbread and functional bakery products to over 40 countries while promoting whole grain health benefits through scientific partnerships. In March 2024 Fazer introduced a new range of rye based plant protein snacks fortified with lentils and seeds targeting health conscious consumers in Western Europe. The products carry the Keyhole nutrition label and are produced in a carbon neutral bakery powered by renewable energy. These actions position Fazer at the intersection of tradition innovation and sustainability in the European rye landscape.

Top Strategies Used by the Key Market Participants

Key players in the Europe rye market focus on vertical integration to control quality from seed to shelf ensuring traceability and sustainability credentials. They invest in varietal innovation through public private breeding programs to enhance yield disease resistance and nutritional profiles. Strategic partnerships with research institutions drive functional food development leveraging rye’s high fiber and prebiotic properties. Companies pursue climate certification and carbon footprint labeling to align with EU Green Public Procurement and consumer demand for transparency. Export development targets premium health food markets in North America and Asia with clean label positioning. Digital platforms provide farmers with agronomic support and market access strengthening supply chain resilience. These strategies collectively enhance value capture and long term market relevance.

MARKET SEGMENTATION

This research report on the Europe Burritos Market has been segmented and sub-segmented based on the following categories.

By Type

- Whole

- Processed

By Application

- Food

- Feed

- Beverage

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com