Europe Semiconductor Market Size, Share, Trends & Growth Forecast Report By Components, By Material Used, By End User, and By Country (Germany, France, Netherlands, Italy, Sweden & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Semiconductor Market Size

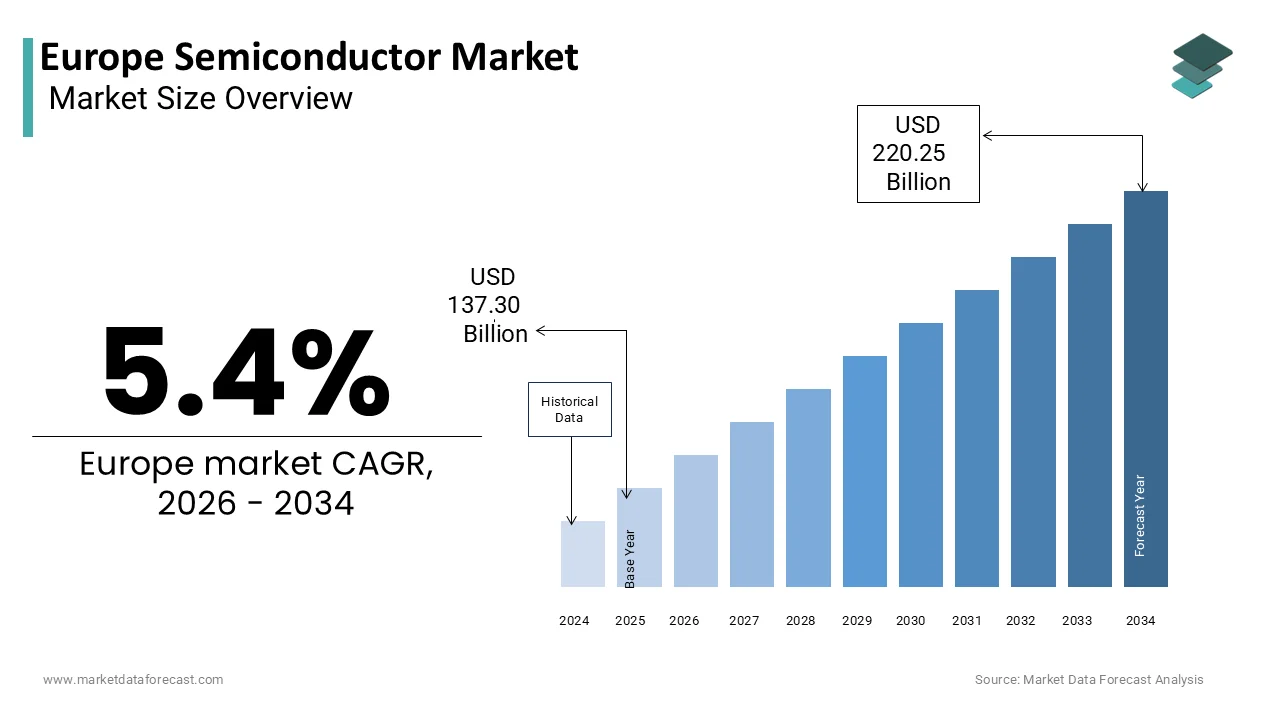

The Europe semiconductor market was valued at USD 137.30 billion in 2025, is estimated to reach USD 144.61 billion in 2026, and is projected to reach USD 220.25 billion by 2034, growing at a CAGR of 5.4% from 2026 to 2034.

A semiconductor is a material with electrical conductivity that falls between that of a conductor (like copper) and an insulator (like glass). Its unique ability to conduct electricity only under specific conditions, such as certain temperatures or light exposure, makes it the fundamental building block of all modern electronics. Unlike regions dominated by consumer electronics-driven demand, Europe’s semiconductor ecosystem is anchored in high-reliability applications requiring robust performance under extreme conditions. As of 2025, the European Semiconductor Industry Association (ESIA) represents a broad alliance of numerous semiconductor companies and research organizations, though the continent hosts approximately 92 fabrication facilities. Major hubs remain concentrated in Germany (Silicon Saxony), France, and the Netherlands, supporting over 200,000 direct jobs. The European Commission emphasizes that the European Union's share of global semiconductor production remains relatively low compared to international competitors. Also, the region maintains a strong position in specialized areas such as sensors and power electronics. The European Chips Act is designed to mobilize significant public and private investment to boost the semiconductor sector. In addition, the initiative aims to significantly increase the European Union's global share of semiconductor production by the end of the decade. Notably, Europe accounts for approximately 30% of global automotive semiconductor demand. Within the region, the automotive sector is the single largest end-user, representing 39% of total European semiconductor device sales in 2023, driven by the rapid adoption of EVs and ADAS technologies.

MARKET DRIVERS

Expansion of Electric Vehicle Production in Europe

The rapid scaling of electric vehicle (EV) manufacturing across the region is boosting demand and driving growth in the European semiconductor market. This demand is particularly strong in power management and control systems. Data from the European Automobile Manufacturers’ Association indicates significant growth in electric vehicle registrations in the EU during 2023, with hybrid-electric vehicles forming a substantial portion of this market. Each EV requires more semiconductor content than a conventional internal combustion engine vehicle, with wide-bandgap devices like silicon carbide (SiC) playing a crucial role in inverters and onboard chargers. Furthermore, Infineon Technologies is expanding the adoption of its Silicon Carbide power modules across numerous electric vehicle models from major European manufacturers. Projections from the International Energy Agency suggest that global electric vehicle adoption will necessitate increased semiconductor production to meet rising demand by 2030. This transition is driving investment in domestic wafer fabrication and strategic partnerships between chipmakers and automakers to secure supply chains.

Growth in Industrial Automation and Smart Manufacturing

The region’s command in advanced manufacturing is fueling the expansion of the Europe semiconductor market. This is being driven by the proliferation of smart factories and Industry 4.0 technologies. Industrial robot installations in the European Union reached a new peak recently, with the majority of deployments concentrated in major manufacturing hubs like Germany and Italy. These systems rely heavily on microcontrollers, sensors, and field-programmable gate arrays (FPGAs) to enable real-time process control, predictive maintenance, and machine vision. Modern automated manufacturing systems are increasingly reliant on a high density of semiconductor components to enable real-time data processing and precision. Additionally, the European Union's Digital Europe Programme provides significant funding to accelerate the deployment of artificial intelligence and advanced computing to enhance industrial competitiveness. STMicroelectronics has expanded its 200mm wafer production in France to meet rising demand for industrial-grade microelectronics. This convergence of policy support and technological adoption is cementing semiconductors as foundational components in Europe’s next-generation manufacturing infrastructure.

MARKET RESTRAINTS

Limited Domestic Semiconductor Fabrication Capacity

The scarcity of advanced front-end fabrication facilities is a critical limitation in the Europe semiconductor market. Specifically, there is a shortage of facilities capable of producing sub-10nm logic chips. The European Union currently holds a minority share of global semiconductor production capacity and is actively investing to establish more advanced manufacturing facilities to reduce its reliance on foreign technology. This dependency forces European industries to rely on imports from Asia and the United States for cutting-edge processors used in AI, data centers, and high-performance computing. The lack of domestic foundry capabilities also exposes supply chains to geopolitical disruptions, as evidenced during the 2022–2023 chip shortages that halted automotive production in several countries. Procurement timelines for high-performance processors from overseas foundries have experienced significant fluctuations, prompting European industries to seek more resilient and predictable supply chains. Europe will struggle to compete in next-generation electronics unless it invests heavily and innovates its processes.

Shortage of Skilled Semiconductor Engineers and Technicians

A growing human capital deficit, with a widening gap between industry demand and the availability of qualified engineers and process technicians, is further degrading the expansion of theEuropeane semiconductor market. The European semiconductor sector is facing a severe shortage of skilled professionals due to an aging workforce and ambitious growth targets, making the recruitment of new talent essential for meeting industry goals. Germany is experiencing a critical, growing shortage of microelectronics specialists, threatening the nation's ability to maintain its leading position in the European semiconductor industry. The complexity of modern fabrication processes, including extreme ultraviolet (EUV) lithography and 3D stacking, demands highly specialized training, yet academic programs in microelectronics have not scaled proportionally. Additionally, competition from the software and AI sectors diverts talent away from hardware disciplines. This shortage delays ramp-up timelines for new fabs and limits innovation velocity, posing a systemic risk to Europe’s ambition of achieving semiconductor sovereignty.

MARKET OPPORTUNITIES

EU Chips Act and Public-Private Investment in Semiconductor Sovereignty

The EU Chips Act, adopted in 2023, signifies a transformative opportunity for the European semiconductor market. It mobilizes over €43 billion in public and private investment to strengthen domestic production and research. The European Commission is implementing the Chips Act to significantly increase Europe's share of global semiconductor production by 2030, with a focus on fostering advanced, sub-5nm manufacturing capabilities within the region. Intel previously negotiated a significant investment in a new semiconductor campus in Germany, backed by government incentives to bolster European production, though the project has since been paused amid the company's broader financial restructuring. Similarly, STMicroelectronics and GlobalFoundries planned a major joint, high-volume chip manufacturing facility in France to support the automotive and industrial sectors. However, this project has faced significant delays and, according to recent reports, has been shelved. These developments, backed by streamlined regulatory pathways and R&D grants, are positioning Europe to reduce dependency on external suppliers and reclaim strategic autonomy in critical microelectronics.

MARKET OPPORTUNITIES

Rising Demand for Energy-Efficient and Sustainable Semiconductors

The region’s stringent environmental regulations and decarbonization goals are creating a robust landscape for energy-efficient semiconductor technologies, which is likely to promote the growth of the European semiconductor market. This demand is particularly strong in the fields of power conversion and renewable energy systems. The European Environment Agency emphasizes that advanced power electronics are essential for maximizing the efficiency of solar, wind, and electric vehicle charging infrastructure to support the transition to a cleaner energy system. Wide-bandgap semiconductors, specifically silicon carbide and gallium nitride, are critical for achieving EU climate goals because they significantly reduce energy losses, improve efficiency, and enable smaller, more robust systems compared to traditional silicon-based components. Additionally, the European Green Deal mandates a major increase in the share of renewables in the total EU energy mix by 2030, which necessitates the deployment of advanced, semiconductor-enabled smart grid technologies to handle increased variability. Companies like Infineon and Nexperia have scaled production of GaN transistors for data centers and industrial power supplies, aligning with the EU’s Ecodesign Directive. This regulatory and technological synergy is fostering innovation in sustainable microelectronics, establishing Europe as a leader in green semiconductor applications.

MARKET CHALLENGES

Geopolitical Fragmentation of Global Semiconductor Supply Chains

Increased vulnerability to geopolitical tensions disrupts the global flow of materials, equipment, and intellectual property, which is hampering the growth of the European semiconductor market. ASML is the sole supplier of extreme ultraviolet (EUV) lithography machines and controls the overwhelming majority of advanced photolithography systems used in European fabs, with its export capabilities restricted by both Dutch and U.S. government regulations. Additionally, Europe is heavily reliant on foreign, concentrated, and politically sensitive sources, particularly China, for the majority of its refined rare earth elements and specialized gases, according to reports on critical raw materials and the European Raw Materials Alliance. The 2023 export controls on advanced computing chips to certain countries have triggered retaliatory measures, affecting European firms’ access to key markets in Asia. This fragmentation complicates long-term planning and forces companies to diversify sourcing at substantial cost. Europe’s chip ambitions are exposed to external shocks absent international agreements and resilient supply architectures.

Escalating R&D and Capital Expenditure Requirements

The escalating cost of semiconductor innovation poses a significant challenge to the European semiconductor market. This issue also threatens the region’s ability to compete in advanced technology nodes. The cost of building advanced, leading-edge semiconductor fabrication facilities is rising significantly, requiring substantial investments, while R&D expenses for developing cutting-edge, sub-5nm process technologies continue to escalate for industry leaders. This financial burden is compounded by the rapid obsolescence of equipment, as EUV lithography tools require replacement every five to seven years. Furthermore, small and medium-sized enterprises make up a substantial portion of the European semiconductor design community and often experience difficulties securing sufficient capital to engage in next-generation technology development, as emphasized by EARTO. Even large firms like STMicroelectronics and NXP rely heavily on public co-funding to sustain innovation. The mismatch between private investment capacity and technological ambition threatens to widen the performance gap between European and global leaders, undermining long-term competitiveness in high-stakes semiconductor domains.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Components, Material Used, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Ethicon (Johnson & Johnson Services, Inc.), Medtronic plc, B. Braun Melsungen AG, Teleflex Incorporated, Braun Surgical Suture Solutions, Smith & Nephew plc, Surgical Specialties Corporation, KLS Martin Group, ConMed Corporation, Lone Star Medical Products, Inc., BD (Becton, Dickinson and Company), Zimmer Biomet Holdings, Inc., Delta Med, Fallbrook Medical, Aspen Surgical Products, Teleflex Medical OEM, Serag-Wiessner GmbH & Co. KG, Sutures India Pvt. Ltd., Medical & Biological Laboratories Co., Ltd., Meril Life Sciences Pvt. Ltd. |

SEGMENTAL ANALYSIS

By Components Insights

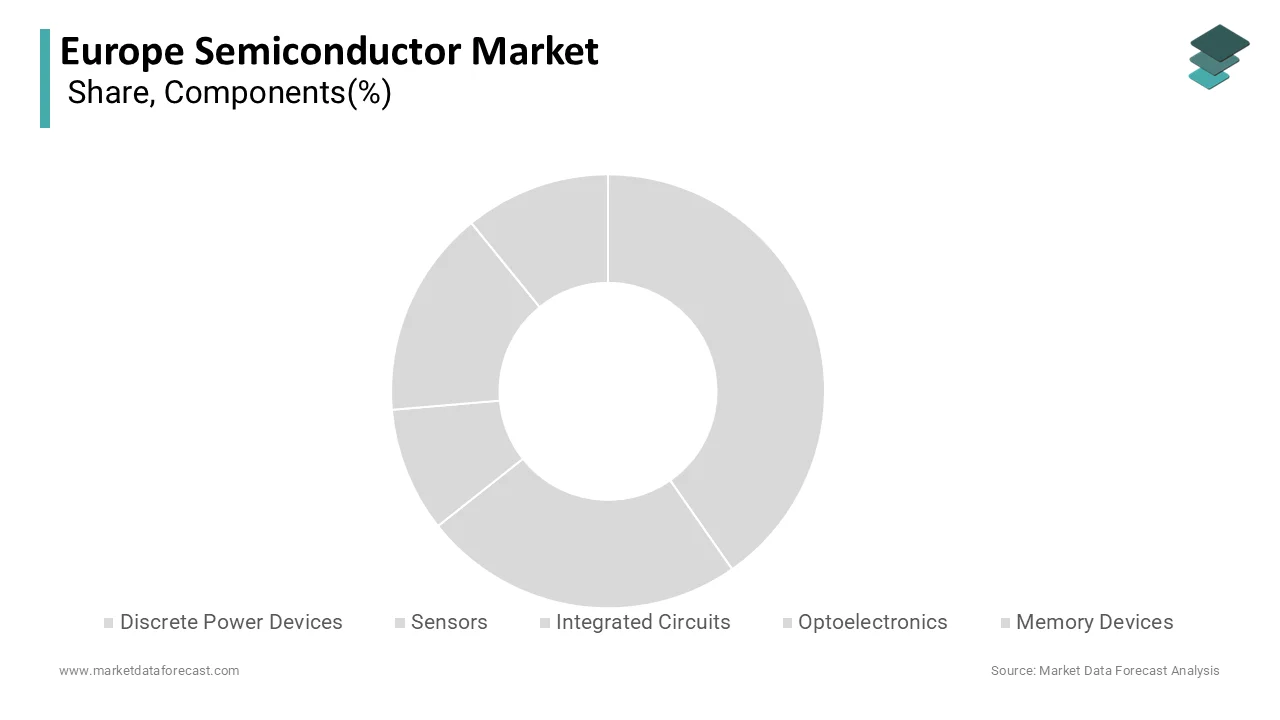

The discrete power devices segment maintained the majority share of 22.7% of the European semiconductor market in 2025. This supremacy of the segment is primarily driven by Europe’s leadership in automotive electrification and industrial power systems. Electric vehicles require a high volume of power semiconductors, particularly IGBTs and rapidly growing silicon carbide technology for motor inverters and battery management systems, to improve efficiency and power density, according to VDMA and other automotive suppliers. The shift toward renewable energy integration further amplifies demand, with power devices enabling efficient conversion in solar inverters and wind turbine systems. The rapid expansion of solar photovoltaic capacity in the European Union, driven by high demand for renewable energy, necessitates advanced inverters and power electronics to enhance efficiency, according to multiple studies. Additionally, industrial automation and rail transport systems, especially in Germany and France, rely heavily on high-voltage power semiconductors, ensuring sustained demand across mission-critical sectors.

The sensors segment is predicted to witness the highest CAGR 13.4% from 2026 to 2034 due to the proliferation of intelligent systems in automotive, healthcare, and smart cities. Modern vehicles in Europe increasingly incorporate a high density of environmental, safety, and monitoring sensors to support advanced driver-assistance systems (ADAS) and electrification, with luxury vehicles and higher-level automation driving the highest sensor counts. In healthcare, wearable medical devices incorporating biosensors are gaining regulatory approval and market traction, with the EU’s Medical Device Regulation (MDR) facilitating faster commercialization. Furthermore, the adoption of IoT-enabled sensors for predictive maintenance is growing within European smart manufacturing, as companies seek to monitor equipment performance and prevent downtime. The integration of AI at the edge is also increasing demand for sensor fusion technologies, positioning this segment at the forefront of Europe’s digital transformation.

By Material Used Insights

In 2025, the Silicon Carbide (SiC) segment dominated the European semiconductor market and captured a substantial share. The dominance of the SiC is attributed to its superior thermal conductivity, higher breakdown voltage, and energy efficiency compared to conventional silicon, making it ideal for high-power applications. The automotive sector is the primary adopter, with SiC-based power modules used in a portion of new electric vehicle inverters in Europe. Major European automakers, including BMW, Mercedes-Benz, and the Renault-Nissan-Mitsubishi alliance, are adopting silicon carbide (SiC) technology to improve power efficiency in electric vehicles. Additionally, the EU’s Green Deal targets a 55% reduction in CO₂ emissions by 2030, accelerating the deployment of SiC in solar inverters and fast-charging stations. The solar industry is increasingly utilizing SiC-based converters to reduce energy losses in high-capacity farms. These performance and regulatory advantages solidify SiC’s position as the cornerstone of next-generation power electronics.

The Molybdenum Disulfide (MoS₂) segment is estimated to register the fastest CAGR of 18.9% during the forecast period, owing to its potential in ultra-thin, flexible, and low-power electronic devices, particularly in emerging fields like neuromorphic computing and wearable sensors. MoS₂, a two-dimensional (2D) transition metal dichalcogenide, exhibits excellent electron mobility at atomic-scale thicknesses, enabling sub-5nm transistor designs. Research into two-dimensional molybdenum disulfide (MoS₂) transistors demonstrates their ability to operate at low voltages with improved efficiency compared to traditional silicon, emphasizing their potential for next-generation electronics. The European Graphene Flagship initiative has extended its scope to include MoS₂ for hybrid 2D material systems, with pilot fabrication lines established in Belgium and Sweden. Although commercial deployment remains limited, the material’s compatibility with EU-driven innovation in sustainable and miniaturized electronics positions it as a high-potential candidate for future semiconductor breakthroughs.

By End User Insights

The automotive segment was the largest segment in theEuropeane semiconductor market and accounted for a 31.2% share in 2025. The leading position of the segment is supported by Europe’s status as a global hub for premium and electric vehicle manufacturing. Modern vehicles are increasingly reliant on numerous semiconductor devices, with electric vehicles requiring significantly higher chip content compared to traditional internal combustion engine vehicles to manage their power systems and advanced functionality. The shift toward electrification, connectivity, and autonomous driving has dramatically increased demand for microcontrollers, power modules, and sensors. The European Union experienced a substantial rise in the registration of new battery electric vehicles in 2023, representing a significant percentage increase in market adoption compared to the prior year. German OEMs like Volkswagen and BMW have mandated dual-sourcing strategies for semiconductors to mitigate supply risks. Additionally, the EU’s General Safety Regulation mandates advanced driver-assistance systems (ADAS) in all new vehicles, further accelerating semiconductor integration across the automotive value chain.

The Data Center segment is anticipated to witness the fastest CAGR of 15.2% over the forecast period. The swift growth of the segment is propelled by the exponential rise in cloud computing, artificial intelligence, and high-performance computing (HPC) infrastructure across Europe. European enterprises are increasingly adopting cloud services and AI technologies, driving demand for advanced computing hardware, as per Eurostat. The rollout of 5G and edge computing networks has further intensified demand for low-latency, high-bandwidth semiconductors. The European High-Performance Computing Joint Undertaking (EuroHPC JU) is deploying a network of world-class supercomputers, including exascale-level systems, across Europe, with significant investment in advanced computing infrastructure. Additionally, AI training clusters require thousands of GPUs and AI accelerators, with companies like Bosch and Siemens investing in on-premise AI data centers. Driven by a push for digital sovereignty, the EU is prioritizing the expansion of local data centers, which is, in turn, fueling sustained demand in the high-growth semiconductor sector.

COUNTRY-LEVEL ANALYSIS

Germany Semiconductor Market Analysis

Germany led the European semiconductor market and occupied a 26.4% share in 2025. The country serves as the technological and industrial nucleus of the regional semiconductor ecosystem, driven by its robust automotive, industrial automation, and engineering sectors. Germany, particularly via the Silicon Saxony region in Dresden, is a key European hub for semiconductor manufacturers like Infineon, Bosch, and GlobalFoundries, with a major contribution to the continental supply of power semiconductors. To bolster European technological sovereignty, Germany is heavily funding major semiconductor manufacturing projects in Dresden, including new capacity from TSMC and a significant "Smart Power Fab" from Infineon, with operations integrated into the wider European supply chain. Additionally, the country hosts the Leibniz Institute for High-Performance Microelectronics (IHP) and collaborates with TU Dresden on advanced chip design. Germany’s push for EVs and autonomous driving ensures a sustained demand for semiconductors. This momentum reinforces the country's leadership in both application and production as Europe’s largest car manufacturer.

France Semiconductor Market Analysis

France was the second-largest country in the European semiconductor market and captured a 17.8% share in 2025. The expansion of the French market is credited to its strong public-private synergy in semiconductor innovation and manufacturing. France hosts major STMicroelectronics manufacturing sites, including Crolles and Rousset, which are integral to the company's European production footprint for digital and analog technologies. France is a central node in the European Chips Initiative, supporting a major joint investment between STMicroelectronics and GlobalFoundries in Crolles to bolster European production of advanced FD-SOI technology, despite recent project delays. The country also leads in aerospace and defense electronics, supplying critical components to Airbus and Dassault. The French microelectronics sector, supported by institutions like CEA-Leti, maintains a substantial research and development workforce, with a high concentration of engineers focused on advanced technology development. This blend of industrial capability, state backing, and research excellence positions France as a pivotal force in Europe’s semiconductor sovereignty agenda.

Netherlands Semiconductor Market Analysis

Netherlands is a major part of the European semiconductor market and occupies a unique strategic position due to its role as the home of ASML, the sole global producer of extreme ultraviolet (EUV) lithography machines. These machines are indispensable for manufacturing chips below the 7nm node, placing the Netherlands at the heart of the global semiconductor supply chain. Major global chipmakers continue to rely on ASML's lithography systems for manufacturing, with the company experiencing substantial annual revenue growth driven largely by high demand in logic markets. The Dutch government collaborates closely with the semiconductor cluster in Eindhoven, known as the “Silicon Valley of Europe,” fostering innovation through PhotonDelta and Holst Centre. The semiconductor industry has become an increasingly vital pillar of the Dutch economy, demonstrating rapid growth in both total earnings and its specialized workforce. While the country does not mass-produce chips, its technological gatekeeper status grants it disproportionate influence in the European and global markets.

Italy Semiconductor Market Analysis

Italy showed consistent growth in the European semiconductor market owing to STMicroelectronics’ significant manufacturing presence and a growing ecosystem in embedded systems and industrial electronics. The company’s Agrate and Catania fabs are among Europe’s most advanced 200mm and 300mm facilities, producing MCUs, sensors, and power devices for automotive and industrial clients. STMicroelectronics is strengthening its position in the European semiconductor market by investing in a large-scale integrated silicon carbide (SiC) facility in Italy, supported by national and European funding, aimed at boosting the manufacturing of power chips for electric vehicles and industrial applications. Italy also excels in MEMS (micro-electromechanical systems) technology, supplying a portion of the world’s smartphone sensors, according to the Italian National Agency for New Technologies (ENEA). The country’s strong mechanical engineering base complements its semiconductor capabilities, particularly in robotics and automation. Italy is increasing public investment and integrating into pan-European R&D consortia like Key4Ever. In doing so, it is reinforcing its role as a critical node in Europe’s specialized semiconductor value chain.

Sweden Semiconductor Market Analysis

Sweden is predicted to expand in the European semiconductor market by punching above its weight through innovation in wireless communications and sustainable semiconductor technologies. The country is home to Ericsson, a global leader in 5G infrastructure, which drives demand for RF and analog semiconductors. Additionally, Northvolt, the Swedish battery manufacturer, is collaborating with semiconductor firms to develop smart battery management systems for EVs, creating new demand for integrated power electronics. The Kista Science City in Stockholm has emerged as a hub for semiconductor design, particularly in low-power and IoT chips. According to initiatives supported by Vinnova and findings from the European Patent Office, Sweden has shown a strong, consistent focus on patenting in advanced, sustainable technologies, particularly within the fields of energy-efficient solutions and circular, smart, and power-saving electronics. Academic institutions like KTH Royal Institute of Technology are pioneering research in compound semiconductors and chip recycling. This innovation-driven model positions Sweden as a key contributor to Europe’s sustainable and digital transition in microelectronics.

COMPETITIVE LANDSCAPE

The competition in the European semiconductor market is defined by a blend of technological specialization, strategic policy alignment, and fragmented manufacturing capabilities. Unlike global rivals focused on high-volume logic chips, European firms differentiate through leadership in power electronics, sensors, and automotive-grade semiconductors. The landscape is shaped by a few dominant players—Infineon, STMicroelectronics, and ASML—each commanding niche supremacy in critical domains. While ASML holds a monopoly in EUV lithography, others compete on application-specific integration and energy efficiency. Public funding under the EU Chips Act is reshaping competitive dynamics, enabling large-scale investments in domestic fabs and reducing reliance on external suppliers. However, the absence of a leading-edge logic foundry limits Europe’s ability to challenge Asia or the U.S. in computing chips. Competition is further intensified by rising innovation from research-driven SMEs and cross-border collaborations aimed at achieving semiconductor resilience and technological sovereignty.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global European suture market include

- Ethicon (Johnson & Johnson Services, Inc.)

- Medtronic plc

- B. Braun Melsungen AG

- Teleflex Incorporated

- Braun Surgical Suture Solutions

- Smith & Nephew plc

- Surgical Specialties Corporation

- KLS Martin Group

- ConMed Corporation

- Lone Star Medical Products, Inc.

- BD (Becton, Dickinson and Company)

- Zimmer Biomet Holdings, Inc.

- Delta Med (Sutures & Devices)

- Fallbrook Medical (Suture Innovations)

- Aspen Surgical Products

- Teleflex (Teleflex Medical OEM)

- Serag-Wiessner GmbH & Co. KG

- Sutures India Pvt. Ltd.

- Medical & Biological Laboratories Co., Ltd.

- Meril Life Sciences Pvt. Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Infineon Technologies is a cornerstone of the European semiconductor market, specializing in power semiconductors, sensor systems, and automotive ICs. The company plays a critical role in enabling electric mobility, industrial automation, and renewable energy conversion across the continent. Its 300mm fab in Villach, Austria, is one of Europe’s most advanced, focusing on silicon carbide (SiC) devices essential for high-efficiency EV powertrains. In the Asia Pacific region, Infineon has deepened its footprint through strategic collaborations with Chinese EV makers such as BYD and NIO, while expanding its Singapore R&D center to accelerate innovation in power management and AI-driven systems. Recent investments in expanding SiC capacity and partnerships with global foundries underscore its commitment to securing leadership in next-generation power electronics across both Europe and the Asia Pacific.

- STMicroelectronics is a dominant force in analog, microcontroller, and sensor technologies, with a strong presence in automotive, industrial, and IoT applications across Europe. Headquartered in Geneva and operating major fabrication plants in France, Italy, and Sweden, the company integrates design and manufacturing to deliver highly specialized semiconductor solutions. It is a leading supplier of MCUs and MEMS sensors used in vehicle safety systems and smart industrial devices. In the Asia Pacific market, STMicroelectronics has strengthened its position by establishing joint development programs with Indian and South Korean electronics manufacturers and expanding its distribution network in Southeast Asia. Its participation in the EU Chips Act and aggressive scaling of FD-SOI and SiC production highlight its strategy to enhance technological sovereignty in Europe while broadening its influence in high-growth Asian markets.

- ASML Holding occupies a unique and pivotal position in the European semiconductor market as the world’s sole manufacturer of extreme ultraviolet (EUV) lithography systems, essential for producing advanced logic chips below the 7nm node. Based in Veldhoven, the Netherlands, ASML’s technology enables foundries like TSMC, Samsung, and Intel to fabricate cutting-edge processors used in AI, data centers, and mobile computing. The company collaborates closely with European research institutions such as imec to push the boundaries of semiconductor patterning. In the Asia Pacific region, ASML has intensified its engagement with semiconductor clusters in Taiwan, South Korea, and China, despite export restrictions on certain advanced systems. Its relentless focus on innovation, including the development of high-NA EUV systems, ensures ASML remains indispensable to both European technological ambitions and global semiconductor manufacturing.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European semiconductor market deploy advanced strategies to maintain technological leadership and expand influence. A primary focus is on vertical integration, combining chip design with proprietary manufacturing processes to ensure performance and supply control. Companies invest heavily in wide-bandgap materials like silicon carbide and gallium nitride to serve high-growth sectors such as electric vehicles and renewable energy. Strategic alignment with the EU Chips Act enables access to public funding for greenfield fabrication projects and R&D consortia. Partnerships with automotive OEMs and industrial equipment manufacturers ensure application-specific optimization. Additionally, firms prioritize sustainability by reducing energy consumption in chip production and advancing circular economy models. Global expansion is pursued through localized innovation centers and supply chain diversification, particularly in the Asia Pacific, to meet regional demand while navigating geopolitical complexities in the global semiconductor ecosystem.

MARKET SEGMENTATION

This research report on the europe semiconductor market is segmented and sub-segmented into the following categories.

By Components

- Discrete Power Devices

- Sensors

- Integrated Circuits

- Optoelectronics

- Memory Devices

- Others

By Material Used

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Molybdenum Disulfide (MoS₂)

- Others

By End User

- Automotive

- Data Centers

- Industrial

- Consumer Electronics

- Healthcare

- Telecommunications

- Aerospace & Defense

- Others

By Country

- Germany

- France

- Netherlands

- Italy

- Sweden

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com