Europe Small Arms Market Size, Share, Trends & Growth Forecast Report By Type, By Application, and By Country (Germany, France, United Kingdom, Italy, Spain, Poland, Sweden & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Small Arms Market Size

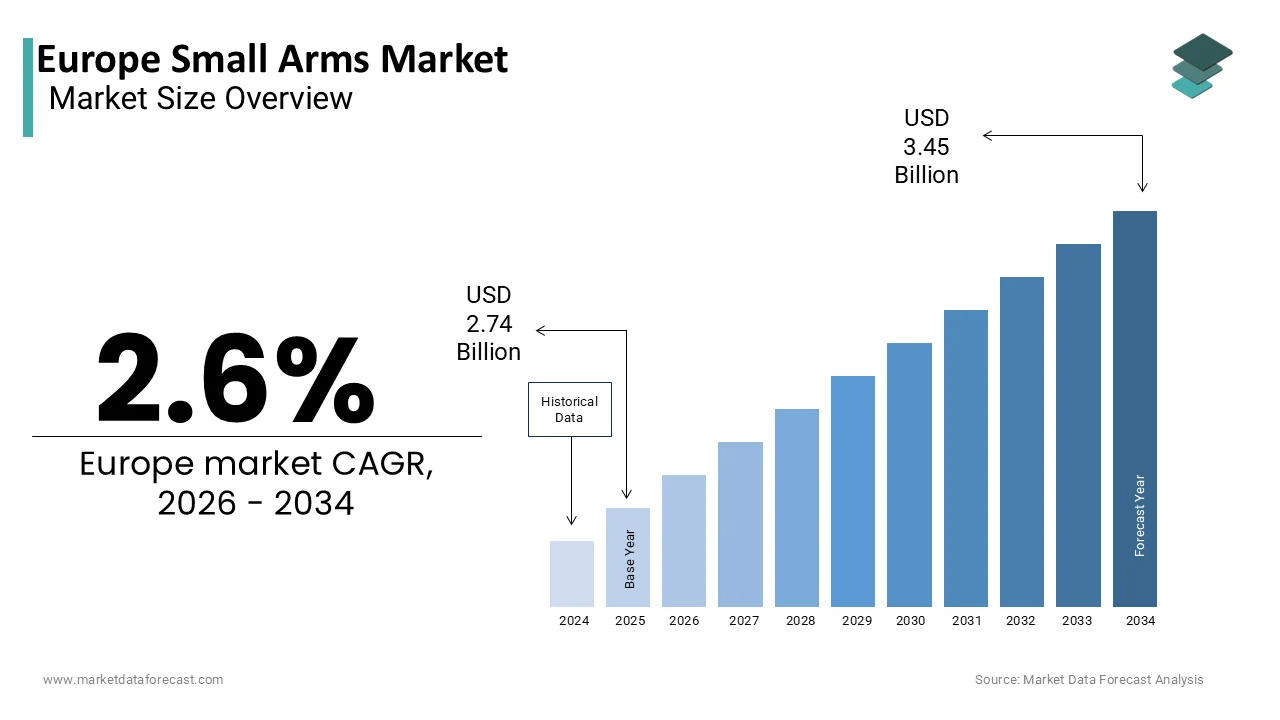

The Europe small arms market was valued at USD 2.74 billion in 2025, is estimated to reach USD 2.81 billion in 2026, and is projected to reach USD 3.45 billion by 2034, growing at a CAGR of 2.6% from 2026 to 2034.

Small arms are firearms designed for use by a single individual. Broadly defined by their portability, they are typically weapons that can be carried and operated by one person without a crew or vehicle. Unlike civilian firearms, which are heavily restricted, military and police small arms are procured under strict national and EU regulatory frameworks that prioritize interoperability, reliability, and compliance with international humanitarian law. The market is shaped by evolving security threats, NATO standardization mandates, and urgent replenishment needs following large-scale deployments. According to the European Defence Agency, total defence expenditure for its 27 member states reached €343 billion in 2024, rising for the 10th consecutive year. While specific inventory counts for small arms are classified by nation, the EU as a bloc remains a dominant player in the global arms trade, with its member states accounting for approximately one-quarter of global international arms exports. As per the NATO Defence Planning Capability Review (2023/2024), Allies have agreed to accelerate investments in defence following Russia's invasion of Ukraine, shifting priority toward collective defence requirements. To harness battlefield lessons, NATO and Ukraine established the Joint Analysis Training and Education Centre (JATEC) in early 2025 to integrate combat experiences into future capability targets and modernization efforts. This strategic recalibration positions small arms not as static inventory but as dynamic, network-ready tools essential for force readiness and tactical superiority in complex operational environments.

MARKET DRIVERS

Escalating Hybrid Threats and Counter Terrorism Imperatives

The proliferation of asymmetric warfare and domestic terrorism has amplified the growth of the European small arms market. This has intensified demand for advanced, reliable small arms across European security forces. According to Europol's 2024 Terrorism Situation and Trend Report, the European Union experienced a rise in reported terrorist attacks, with separatists committing the highest number of completed attacks, while jihadist terrorism was the most lethal. In response, specialized units such as France’s RAID and Germany’s GSG 9 have upgraded to modular assault rifles like the HK416 and FN SCAR, which offer enhanced accuracy, suppressor compatibility, and rail integration for optics and lasers. The war in Ukraine further exposed vulnerabilities in legacy inventories. Western allies have transferred a significant number of small arms to Ukrainian forces between 2022 and 2024 to support their defense, resulting in a notable reduction of national stockpiles among contributing nations. Countries like Poland and the Baltic states have since launched emergency procurement programs. Poland continues to modernize its military and Territorial Defence Forces by acquiring new, domestically produced, and modernized small arms, including large-scale orders for the MSBS Grot rifle system and additional quantities of the Beryl platform. This dual pressure from external conflict and internal security threats transforms small arms from routine equipment into critical national security assets requiring continuous investment and readiness.

NATO Standardization and Interoperability Requirements

Alliance-wide efforts to harmonize ammunition, accessories, and maintenance protocols are driving the adoption of standardized small arms platforms across the region, which is one of the major factors boosting the expansion of the European small arms market. NATO STANAG standards 4172 and 2310 ensure that ammunition, rather than rifle ergonomic or rail design, is interchangeable across NATO member weapon systems. Modern NATO procurement, supported by NSPA, continues to show a strong preference for modularity and ambidextrous operating controls in new small arms acquisition. This standardization reduces logistical complexity during joint operations, such as those under the EU Rapid Deployment Capacity, and enables shared training and spare parts pools. The Belgian FN Herstal SCAR and German Heckler & Koch HK416 have become de facto standards due to their modularity and NATO compliance. These interoperability imperatives create economies of scale, incentivize collaborative procurement, and marginalize non-compliant legacy systems, consolidating the market around a few high-performance, alliance-certified platforms.

MARKET RESTRAINTS

Stringent National Firearm Control Legislation

Broader EU firearm regulations, despite military and police exemptions, indirectly constrain the growth of the European small arms market. These regulations also impact small arms development and export. The EU Firearms Directive, as amended, mandates strict control over semi-automatic firearms, high-capacity magazines, and the conversion or deactivation of firearms, requiring enhanced standards for weapons used for training or marking. The European Commission frequently identifies that Member States apply varying national restrictions beyond minimum EU standards, creating challenges in the cross-border movement of, and trade in, specialized, deactivated, or training weapons. Germany’s War Weapons Control Act requires stringent, specialized licensing for the export of war weapons, which involves complex, multi-agency scrutiny that can result in significant delays in deliveries to partner nations. These legal barriers increase administrative overhead, deter private investment in dual-use technologies, and fragment the European industrial base. Regulatory uncertainty is hindering innovation in smart optics and training simulators, slowing the industry’s ability to meet new, urgent operational needs, even though combat firearms remain exempt.

Ethical and Political Opposition to Arms Exports

Public and parliamentary scrutiny over arms sales to conflict zones or authoritarian regimes creates reputational and operational risks for manufacturers in the region, which negatively impacts the expansion of the European small arms market. According to the Stockholm International Peace Research Institute, Germany and Sweden saw a decrease in their share of global major arms exports between the 2015–19 and 2020–24 periods. Campaigns by NGOs like Amnesty International have pressured governments to revoke licenses for sales to countries involved in Yemen or human rights violations. The Dutch parliament has previously moved to restrict arms component exports to countries involved in Middle Eastern conflicts due to concerns over human rights violations. These interventions disrupt long term production planning, inflate compliance costs, and push manufacturers toward domestic-only contracts with lower margins. The resulting caution undermines Europe’s ambition for defence industrial autonomy, as companies avoid international partnerships that could enhance scale and innovation but carry political risk.

MARKET OPPORTUNITIES

Modernization of Legacy Inventories Through Modular Upgrade Kits

Rather than full replacement, many militaries in the region are extending the life of existing small arms through precision upgrade packages, which pave the way for new opportunities for the European small arms market. Companies like Heckler & Koch and FN Herstal offer conversion kits that retrofit Cold War-era rifles with free-floating barrels, adjustable stocks, and MIL STD 1913 rails. European nations are actively phasing out or upgrading aging, legacy assault rifle platforms, such as the G36 and FAMAS, to meet modern combat requirements, often by adopting new, modular weapon systems (e.g., HK416/G95) rather than undertaking large-scale mid-life upgrades. Upgrading existing military small arms can provide significant budgetary savings compared to procuring entirely new systems. However, the decision to upgrade must be balanced against the need for full modern capability and long-term sustainability, which often leads to new procurement to address the limitations of older platforms. Upgrades also preserve familiar maintenance ecosystems and operator muscle memory. This approach aligns with EU sustainability principles by reducing waste and maximizing existing asset value, creating a robust secondary market for subsystem integrators and sustaining industrial capacity during transition periods to next-generation platforms.

Integration of Smart Optics and Fire Control Systems

The convergence of small arms with digital battlefield networks offers key growth areas to enhance marksmanship and situational awareness, which is predicted to drive the expansion of the European small arms market. Next-generation rifles are increasingly paired with fire control systems like the TrackingPoint or Rheinmetall’s Argus, which integrate laser rangefinders, ballistic computers, and augmented reality reticles. According to studies by the French Directorate General for Armaments (DGA), the FÉLIN integrated infantry system significantly improves lethality and engagement accuracy during day and night operations compared to standard equipment, specifically by enhancing target acquisition through advanced weapon sights and thermal imaging. Similarly, the UK’s Future Integrated Soldier Technology programme embeds weapon data into helmet displays, enabling squad-level target sharing. AI-powered threat detection and wireless connectivity are maturing. Consequently, small arms are evolving from passive tools into active nodes in network-centric warfare. This digitization not only improves lethality but also generates valuable training data, enabling personalized skill development and predictive maintenance, positioning early adopters at a decisive tactical advantage.

MARKET CHALLENGES

Supply Chain Vulnerabilities in Critical Component Sourcing

A high dependency on non-EU suppliers for critical components threatens the autonomy of the region’s small arms manufacturing and the overall growth of the European small arms market. This exposes production to geopolitical and logistical risks. European Union assessments highlight a heavy reliance on a limited number of non-EU nations for critical materials and high-performance components, prompting initiatives to diversify supply chains. The ongoing conflict in Ukraine has created logistical challenges for the European defense industry, causing delays in the delivery of various weapon systems. Similarly, rare earth elements essential for smart optic sensors are overwhelmingly sourced from China, creating long-term strategic exposure. Initiatives like the European Raw Materials Alliance aim to build resilience. However, establishing certified alternative sources requires years of qualification. These barriers constrain production scalability, inflate costs, and jeopardize the timely delivery of urgently needed weapons, undermining Europe’s goal of defence industrial autonomy.

Rapid Obsolescence Due to Emerging Battlefield Technologies

The pace of asymmetric warfare innovation, particularly in drone swarms, electronic warfare, and urban combat, threatens to outpace small arms effectiveness within years of fielding, and thereby impedes the expansion of the European small arms market. Commercial drones now conduct reconnaissance and drop grenades on entrenched positions, forcing infantry to engage aerial targets with standard rifles, a tactically disadvantageous scenario. Current small arms lack integrated counter-drone capabilities, requiring soldiers to carry separate launchers or jammers. Additionally, GPS jamming in contested zones disables smart ammunition guidance systems, rendering them ineffective. Research indicates that modern defense systems require open architecture designs to integrate new sensors and tools efficiently, preventing premature obsolescence. This approach, widely discussed in military technology, ensures that equipment remains effective throughout its deployment cycle. This dynamic demands unprecedented agility in design, testing, and fielding, pressuring legacy defence contractors to adopt software-centric development models more akin to Silicon Valley than traditional military procurement.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Heckler & Koch GmbH, SIG Sauer GmbH & Co. KG, FN Herstal, Beretta Holding S.p.A., Rheinmetall AG, B&T AG, CZ Group, Glock Ges.m.b.H., Smith & Wesson Brands, Inc., Colt’s Manufacturing Company LLC, Weatherby, Inc., Tikka, Steyr Mannlicher GmbH & Co. KG, Blaser Jagdwaffen GmbH, Benelli Armi S.p.A., Franchi S.p.A., J. P. Sauer & Sohn GmbH, Taurus Armas, Century International Arms |

SEGMENTAL ANALYSIS

By Type Insights

The rifles segment led the European small arms market and captured a 62.8% share in 2025. The leading position of the segment is attributed to its central role in military infantry operations, counter terrorism, and border security across NATO and EU forces. Rifles serve as the standard individual weapon for dismounted soldiers across all European armed forces, with platforms like the HK416, FN SCAR, and Beryl M762 forming the backbone of mechanized and rapid reaction units. NATO is focusing on the modernization of small arms, emphasizing interoperability and the adoption of NATO-standard calibers for infantry weapons across member forces. The war in Ukraine has intensified this requirement. Following the 2022 invasion of Ukraine, Western nations accelerated the transfer of varied small arms to Ukraine, resulting in significant, rapid procurement of new, modernized rifles by contributing nations to restock their arsenals. To modernize its forces and replace older weapons, Poland has significantly increased domestic procurement of Grot assault rifles and authorized major acquisitions of varied military equipment to bolster its capabilities. Unlike handguns or shotguns, rifles offer the optimal balance of range, accuracy, stopping power, and accessory integration, making them irreplaceable in both conventional and hybrid warfare scenarios. Modern military rifles are designed around NATO STANAG specifications, ensuring compatibility with standardized ammunition (5.56×45mm and 7.62×51mm), magazines, and rail systems. New rifle procurement contracts across the Alliance are increasingly mandating modern modular interfaces, specifically Picatinny rails, to support enhanced optic, laser, and grip compatibility. This interoperability reduces logistical complexity during joint operations and enables shared training protocols across allied forces. The Belgian FN Herstal SCAR and German Heckler & Koch HK416 have become de facto standards due to their adaptability, allowing quick barrel changes for close quarters or long-range roles. This standardization creates economies of scale, incentivizes collaborative procurement, and marginalizes non-compliant legacy systems, consolidating the rifle segment as the strategic core of Europe’s small arms ecosystem.

The handgun segment is estimated to register the fastest CAGR of 7.4% between 2026 and 2034 due to specialized law enforcement and personal defense needs. Handguns are increasingly issued as primary or secondary weapons to urban police, border guards, and counter terrorism teams operating in confined environments where rifles are impractical. European special intervention units are increasingly adopting modern, modular semi-automatic pistols that offer high capacity and compact frames for specialized operations. These models feature enhanced ergonomics, red dot sight compatibility, and improved trigger safety, critical for precision in high stress scenarios. France’s RAID and Germany’s GSG 9 have fully transitioned to modular handgun platforms since 2023, enabling rapid customization for mission profiles. The rise in lone actor terrorist attacks in public spaces further justifies concealed carry authorization for plainclothes officers, driving institutional demand beyond traditional military channels. While civilian firearm ownership remains tightly restricted, select EU countries have introduced limited handgun licensing for high-risk professionals such as armored transport guards, diplomats, and critical infrastructure personnel. Swedish authorities have revised national firearms legislation to tighten controls on high-risk weapons while streamlining administrative requirements for hunters and sport shooters. The Swedish Police Authority continues to maintain a rigorous licensing process, ensuring all new handgun permits for professional or private use meet strict national security standards. Manufacturers like Walther and CZ respond with compact, low-recoil models featuring biometric safeties and micro red dot mounts. Though small in volume compared to military sales, this segment offers high margin, premium pricing opportunities, and fosters brand loyalty among professional users who later influence institutional procurement decisions.

By Application Insights

The defense and homeland security applications segment was the largest in the European small arms market and occupied a significant share in 2025. The supremacy of the segment is credited to the prioritization of national and collective security in post invasion Europe. The full-scale Russian invasion of Ukraine triggered an unprecedented drawdown of European military small arms stocks. Following extensive military support transfers to Ukraine, European nations are rapidly procuring new service weapons to replenish stocks and enhance readiness. Countries like Poland, Romania, and the Baltic states launched emergency procurement programs. Poland is executing a major modernization of its military, which includes ordering large numbers of domestically produced rifles to replace older weapons. Simultaneously, NATO’s Enhanced Forward Presence in Eastern Europe requires fully equipped brigade combat teams, each needing thousands of rifles, machine guns, and sidearms. The European Commission’s Strategic Compass explicitly identifies small arms as “critical enablers of credible deterrence,” ensuring multi-year funding through national defence budgets and the European Peace Facility. Beyond conventional warfare, small arms are essential for countering hybrid threats such as sabotage, drone swarms, and paramilitary incursions. Border security forces in Finland and Estonia now conduct regular live fire drills against simulated infiltrator scenarios, requiring reliable, cold-weather-tested firearms. The EU’s Rapid Deployment Capacity mandates standardized small arms for all contributing nations to ensure interoperability. In response to increased security challenges at external borders, Frontex has highlighted the need for increased cooperation and enhanced equipment to counter emerging risks. This dual focus on high-intensity conflict and sub-threshold aggression cements Defense and Homeland Security as the structural core of small arms demand, insulated from economic cycles and driven by strategic necessity.

The law enforcement application segment is anticipated to witness the fastest CAGR of 8.1% from 2026 to 2034, owing to urban counter terrorism and active shooter preparedness, and standardization across municipal and national forces. European police forces are upgrading small arms in response to evolving urban threat landscapes. Recent Europol reports have indicated a significant rise in total terrorist incidents within the EU, resulting in police forces continuing to adopt specialized long guns for rapid response. Following a review of the 2019 Halle synagogue attack, multiple German state police forces accelerated the issuance of compact carbines to regular patrol officers. Similarly, France's National Police and Gendarmerie modernized their arsenal by selecting the HK UMP9 to replace older submachine guns, a process that has been ongoing since the late 2010s. These platforms offer superior stopping power and accuracy over traditional handguns in open or crowded environments. Fragmentation in police equipment historically hindered joint operations, but recent EU initiatives promote harmonization. The Prüm II Agreement facilitatescross-borderr pursuit, requiring compatible firearms and ammunition among participating states. In response, countries like Spain and Italy have aligned their service pistol calibers to the 9×19mm NATO standard, enabling mutual logistics support. This trend toward common platforms reduces training costs, simplifies spare parts management, and enhances interoperability during multinational crisis responses. As urban security becomes increasingly networked, law enforcement's small arms evolve from local tools to integrated components of continental public safety architecture.

COUNTRY LEVEL ANALYSIS

Russia Small Arms Market Analysis

Russia dominated the European small arms market and accounted for a 38.8% share in 2025. The demand for small arms in Russia is driven by its massive domestic military requirements and extensive export networks. The market position in this region reveals a total war economy orientation where state-owned enterprises like Kalashnikov Concern and Degtyarev Plant operate at maximum capacity to supply both regular forces and paramilitary units. The ongoing conflict in Ukraine has necessitated an unprecedented surge in production. According to the Stockholm International Peace Research Institute, Russian arms manufacturing has seen a substantial increase in revenue as the industry ramps up production to meet heightened domestic demand. The Russian government has allocated a significant portion of its gross domestic product to military expenditure, with a substantial part of these funds directed toward the procurement of essential infantry weaponry and specialized combat systems. Furthermore, the reliance on legacy designs such as the AK-74M and the newer AK-12 ensures standardized logistics while allowing for rapid scaling due to mature supply chains. As per research, Russia continues to provide military equipment to various partner nations in Africa and the Middle East, though its overall share of the global export market has decreased as it prioritizes its own operational needs. The integration of private military companies into state strategy has also created a new domestic demand vector for specialized compact weapons and suppressed variants, further solidifying the country's dominant volume position in the regional landscape.

Turkey Small Arms Market Analysis

Turkey was the next prominent country in the Europe small arms market and held a share of 19.2% share in 2025. The growth of the Turkish market is attributed to its transformation from a net importer to a leading indigenous manufacturer and exporter within the NATO alliance. The market status in Turkey is characterized by a robust public-private partnership model where state entities like MKEK collaborate with dynamic private firms such as Sarsılmaz and Canik to produce world-class handguns and rifles. Research indicates that defense exports have reached record levels, with small arms and light weapons making up an increasingly important part of the total, particularly in expanding markets across Asia and Africa. The country's strategic autonomy goals have driven massive investment in research and development, resulting in the widespread adoption of domestically designed platforms like the Mehmetçik-1 rifle by the Turkish armed forces. According to sources, Turkish small arms manufacturers have successfully secured contracts with dozens of countries, utilizing a combination of value and performance to compete effectively against established international suppliers. The internal security situation involving counter-terrorism operations has also sustained steady domestic demand for specialized urban warfare weaponry. As per studies, the percentage of locally produced components in small arms production has reached a very high level, significantly decreasing the need for foreign parts and allowing for greater freedom in exporting these products to global markets.

Germany Small Arms Market Analysis

Germany maintains a noteworthy share in the Europe small arms market and serves as the premier hub for high-precision engineering and premium tactical firearms in Western Europe. The market status in this region is defined by stringent quality standards and a strong focus on supplying elite military units and law enforcement agencies with technologically advanced weapon systems. The Federal Ministry of Defence has moved forward with its infantry modernization program, awarding a substantial contract to replace existing service rifles with a new platform produced by Heckler & Koch, marking a significant step in the renewal of domestic military equipment. Moreover, the German Federal Office for Economic Affairs and Export Control reveals that small arms exports reached a record high in 2024, with major portions of these deliveries destined for Ukraine and partner nations within the NATO alliance and the Indo-Pacific region. The German industry is also leading the integration of smart optics and modular accessory systems into standard infantry weapons, setting global trends for interoperability. According to Rheinmetall AG, the company has significantly expanded its manufacturing capacity to fulfill a surge in orders from European governments as they work to replenish their national defense stockpiles. The emphasis on dual-use technologies and strict end-user monitoring ensures that German small arms remain synonymous with reliability and precision, securing its pivotal role in the regional security architecture.

France Small Arms Market Analysis

France expanded steadily in the Europe small arms market due to its fully integrated national defense industrial base that prioritizes strategic autonomy and operational excellence. The market status in France is marked by the successful deployment of the FAMAS replacement program, where the HK416F manufactured under license by Nexter Systems has become the standard issue rifle for the French Army, driving significant domestic production volumes. The French government's multi-year military budget for the current decade allocates a significant sum to defense, with specific provisions for modernizing individual combat equipment and substantially increasing ammunition reserves. According to studies, France has intensified efforts to reconstitute its war stocks following extensive deployments in the Sahel and contributions to Eastern European deterrence missions. The country maintains a strong export presence in Francophone Africa and the Middle East, leveraging historical ties and diplomatic agreements to secure long-term supply contracts for pistols and submachine guns. As per reports from La Tribune, the French small arms sector is increasingly focusing on lightweight materials and ergonomic designs to enhance soldier mobility in diverse operational environments. The collaboration between state-owned giants and specialized subcontractors ensures a resilient supply chain capable of scaling up production during crises, reinforcing France's status as a key sovereign power in the European defense landscape.

Italy Small Arms Market Analysis

Italy is predicted to grow notably in the Europe small arms market during the forecast period by functioning as a historic and influential center for firearm craftsmanship and innovation that serves both civilian and military sectors globally. The market growth in Italy is unique due to the strength of its private manufacturing cluster in the Brescia region, home to legendary brands like Beretta, Benelli, and Franchi, which dominate the global market for semi-automatic pistols and shotguns. The Italian Ministry of Defence has continued to advance the procurement of modern battle rifles and grenade launchers to equip its specialist mountain and infantry units, effectively stimulating domestic industrial activity. According to sources, Italian defense exports reached significant multi-billion euro levels in 2024, with small arms continuing to be a highly profitable segment that leverages high product value relative to shipping volume. The country benefits from a robust civilian shooting sports culture which sustains a steady baseline of production and R&D investment that spills over into military applications. According to research, the use of advanced polymers and modular rail systems in modern Italian weapon designs has ensured their continued competitiveness against new international entrants. The ability to rapidly switch between commercial and military production lines provides Italian manufacturers with exceptional flexibility, allowing them to capitalize on sudden spikes in global demand while maintaining financial stability through diverse revenue streams.

COMPETITIVE LANDSCAPE

The European small arms market features intense rivalry among legacy defence primes, state-backed national champions, and emerging technology integrators. Established players like Heckler & Koch and FN Herstal leverage decades of operational validation and deep integration into NATO logistics networks. Meanwhile, national manufacturers such as Fabryka Broni benefit from sovereign procurement policies and emergency rearmament budgets. Competition is increasingly defined by modularity, digital integration, and supply chain resilience rather than price alone. Ethical export controls and public scrutiny constrain commercial flexibility, favoring companies with strong government ties and transparent compliance frameworks. Despite rising demand, the market remains highly regulated, with success dependent on balancing cutting-edge performance, political alignment, and industrial sovereignty within Europe’s evolving security architecture.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global europe small arms market include

- Heckler & Koch GmbH

- SIG Sauer GmbH & Co. KG

- Fabrique Nationale Herstal (FN Herstal)

- Beretta Holding S.p.A.

- Rheinmetall AG

- B&T AG (Brügger & Thomet)

- CZ Group (Česká Zbrojovka)

- Glock Ges.m.b.H.

- Smith & Wesson Brands, Inc.

- Colt’s Manufacturing Company LLC

- Weatherby, Inc.

- Tikka (part of Sako/Beretta Group)

- Steyr Mannlicher GmbH & Co. KG

- Blaser Jagdwaffen GmbH

- Benelli Armi S.p.A.

- Franchi S.p.A.

- Sauer & Sohn GmbH

- Taurus Armas

- Century International Arms

TOP LEADING PLAYERS IN THE MARKET

- Headquartered in Germany, Heckler & Koch is a globally recognized leader in military and law enforcement small arms, renowned for its G36, HK416, and P30 series. The company supplies NATO forces, special operations units, and police agencies across Europe and beyond with precision-engineered firearms that emphasize reliability, modularity, and ergonomic design. It also expanded its digital training ecosystem with virtual reality marksmanship simulators adopted by the German Bundeswehr and Dutch National Police. These innovations reinforce its reputation as a technology-forward partner in modern infantry modernization and tactical readiness.

- Based in Belgium, FN Herstal is a cornerstone of European small arms production, manufacturing the SCAR rifle family, FNX pistols, and Minimi light machine guns used by numerous armed forces worldwide. The company plays a critical role in NATO standardization through its STANAG-compliant platforms. It also established a joint sustainment hub in Estonia to support Eastern European allies with rapid spare parts logistics and field maintenance training. These actions strengthen its position as a strategic enabler of allied interoperability and rapid response capability.

- Operating under Poland’s state-owned Polish Armaments Group, Fabryka Broni is a key Central European manufacturer producing the Beryl and MSBS Grot rifle families for the Polish Armed Forces and export markets. The company has emerged as a vital supplier in Europe’s post-Ukraine war rearmament drive. It also inaugurated a new automated barrel forging line in Radom to increase annual output significantly by 2026. These investments position Fabryka Broni as a sovereign industrial pillar in Europe’s push for defence autonomy and resilient supply chains.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European small arms market are prioritizing modular weapon architectures to enable rapid customization for diverse mission profiles. They are integrating smart optics and digital fire control systems to enhance marksmanship and battlefield connectivity. Companies are establishing regional sustainment hubs to provide rapid spare parts and training support to allied forces. Strategic alignment with NATO standardization mandates ensures interoperability and access to multinational procurement programs. Additionally, manufacturers are investing in automated production lines to scale output while maintaining precision, addressing urgent replenishment needs driven by geopolitical instability and stockpile depletion.

MARKET SEGMENTATION

This research report on the europe small arms market is segmented and sub-segmented into the following categories.

By Type

- Rifles

- Handguns

- Shotguns

- Submachine Guns

- Light Machine Guns

By Application

- Defense & Homeland Security

- Law Enforcement

- Civilian / Sporting

- Private Security

By Country

- Germany

- France

- United Kingdom

- Italy

- Spain

- Poland

- Sweden

- Rest of Europe

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com