Europe Small Satellite Market Size, Share, Trends & Growth Forecast Report – Segmented By Application, Orbit Class, End User, Propulsion Tech, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2026 to 2034

Europe Small Satellite Market Report Summary

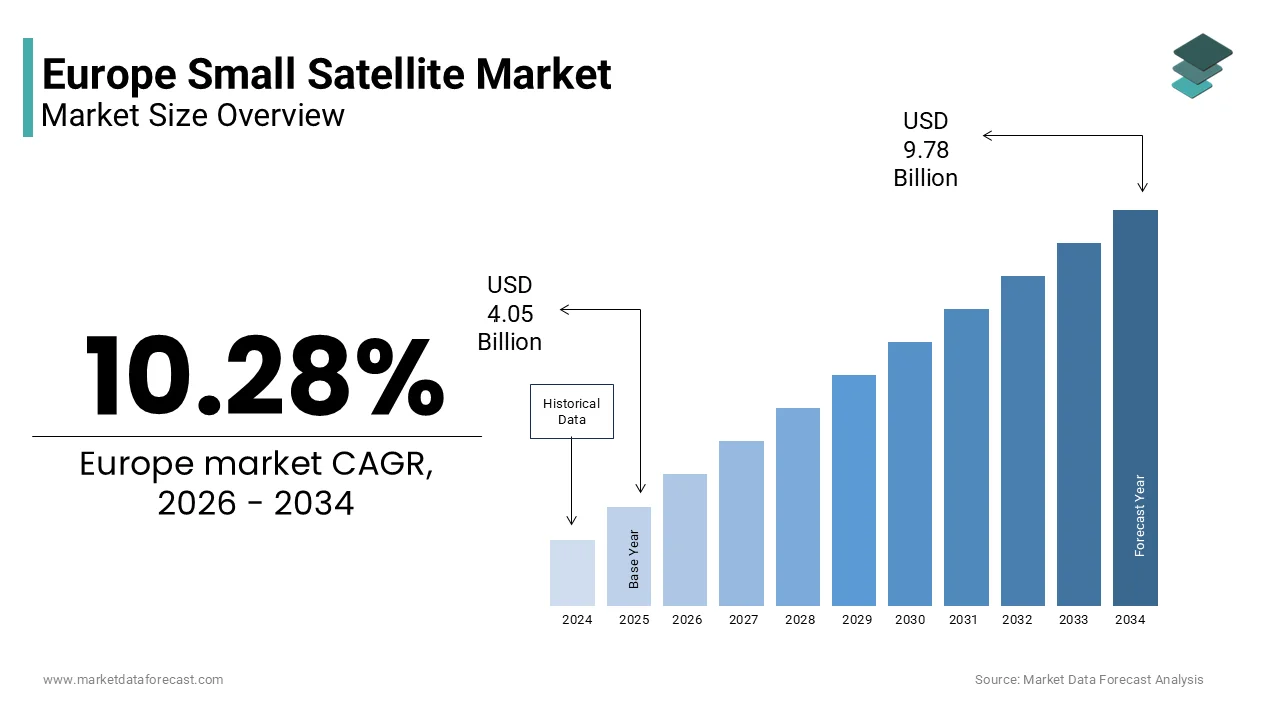

The Europe small satellite market was valued at USD 4.05 billion in 2025, is estimated to reach USD 4.47 billion in 2026, and is projected to reach USD 9.78 billion by 2034, growing at a CAGR of 10.28% during the forecast period from 2026 to 2034. The growth of the Europe small satellite market is driven by the increasing demand for earth observation services, expansion of satellite communication networks, and rising adoption of satellite based data for environmental monitoring, defense intelligence, and disaster management. Governments and private space companies across Europe are investing heavily in small satellite development, satellite constellations, and cost efficient launch technologies. In addition, advancements in miniaturized components, electric propulsion systems, and commercial space programs are accelerating satellite deployment and strengthening the regional space ecosystem.

Key Market Trends

- Growing deployment of satellite constellations to support earth observation, communication services, and data analytics applications across Europe.

- Increasing participation of private space companies and startups in satellite manufacturing, launch services, and satellite data solutions.

- Rising demand for high resolution earth observation data for climate monitoring, environmental assessment, agriculture management, and disaster response.

- Technological advancements in electric propulsion systems that improve satellite efficiency, maneuverability, and operational lifespan.

- Increasing collaboration between European governments, defense organizations, and commercial space technology companies to expand satellite infrastructure.

Segmental Insights

- Based on application, the earth observation segment dominated the Europe small satellite market in 2025. The growth of this segment is driven by the increasing use of satellite imagery and geospatial data for environmental monitoring, agriculture analysis, urban planning, and national security operations.

- Based on end user, the commercial segment held the dominant position in the Europe small satellite market in 2025. The expansion of private satellite operators, satellite data providers, and telecommunication companies deploying satellite constellations is supporting the growth of this segment.

- Based on propulsion technology, the electric propulsion segment led the market by capturing the highest share of the Europe small satellite market in 2025. Electric propulsion systems are increasingly preferred due to their fuel efficiency, longer mission durations, and ability to support precise orbital maneuvers.

Regional Insights

- The Europe small satellite market is witnessing strong development across several countries, supported by expanding space programs, rising private sector investments, and increasing demand for satellite based services.

- Germany was the largest contributor, accounting for 26.5% of the Europe small satellite market share in 2025. The country’s strong aerospace manufacturing capabilities, active participation in European space initiatives, and growing number of satellite technology companies are supporting market growth.

Competitive Landscape

The Europe small satellite market is characterized by the presence of major aerospace companies and emerging space technology startups focusing on satellite manufacturing, launch services, and satellite data applications. Companies are investing in advanced propulsion systems, satellite constellations, and strategic collaborations with government space agencies to strengthen their market presence. Prominent players in the Europe small satellite market include Airbus Defence and Space, Thales Alenia Space, OHB SE, Surrey Satellite Technology Ltd, AAC Clyde Space, GomSpace, Exotrail, Spire Global, ICEYE, Planet Labs, Isar Aerospace, Rocket Factory Augsburg, Skyrora, PLD Space, and D Orbit.

Europe Small Satellite Market Size

The Europe small satellite market size was valued at USD 4.05 billion in 2025 and is projected to reach USD 9.78 billion by 2034 from USD 4.47 billion in 2026, growing at a CAGR of 10.28%.

Small satellite represents a dynamic and rapidly evolving sector dedicated to the design, manufacturing, and operation of spacecraft with a mass typically under five hundred kilograms, encompassing mini, micro, nano, and cube sat classes. This ecosystem is distinctively characterized by a shift from traditional bespoke engineering to serial production lines, enabling cost effective deployment of constellations for Earth observation, communications, and scientific research. The region leverages its robust institutional framework, primarily through the European Space Agency and the European Union, to foster sovereignty in space assets while nurturing a vibrant NewSpace startup culture. As per Eurostat, the digital economy relies increasingly on low latency data streams, which small satellites in low Earth orbit are positioned to provide for remote sensing and Internet of Things connectivity across the continent. Furthermore, as per the European Environment Agency, high revisit rate imagery from small satellite fleets is utilized to monitor climate change indicators, track biodiversity, and enforce agricultural policies with improved temporal resolution. Unlike the historical focus on large geostationary platforms, this market prioritizes agility, rapid iteration, and distributed risk, allowing for frequent technology updates and mission specific customization. The definition now extends to include integrated ground segment solutions and data analytics services, reflecting a holistic approach where the satellite is one node in a comprehensive information value chain driving the digital transformation of European industries.

MARKET DRIVERS

Strategic Imperative for Sovereign Low Earth Orbit Constellations

The urgent geopolitical necessity to establish sovereign, resilient and independent communication and observation capabilities in low Earth orbit is primarily driving the growth of the Europe small satellite market. Recent global conflicts have illustrated the vulnerabilities of relying on foreign commercial or state-owned assets for critical government functions, prompting the European Union to accelerate initiatives like the IRIS² secure connectivity program. As per the European Commission, this project aims to deploy a multi-orbital constellation including small satellites to ensure secure communications for member states and bridge the digital divide in rural areas. This strategic shift is reinforced by NATO, which has recognized space as an operational domain, driving European nations to invest in redundant small satellite networks that can withstand jamming and physical threats. As per the European Defence Agency, defense spending on space-based assets has increased, with a specific focus on distributed architectures where the loss of a single small unit does not compromise the entire mission. The drive for digital sovereignty extends beyond security to include economic independence, ensuring that European industries have guaranteed access to bandwidth and data without external interference.

Democratization of Space Access through Cost Reduction and Standardization

The reduction in entry barriers achieved through the standardization of components and the advent of serial manufacturing techniques are further boosting the expansion of the Europe small satellite market. The widespread adoption of the CubeSat form factor has created a modular ecosystem where off-the-shelf parts for power, propulsion, and communication are readily available, reducing development costs and timelines. As per the European Space Agency, the cost to build and launch a small satellite has decreased considerably in recent years, enabling universities, startups, and small nations to participate in space activities previously reserved for superpowers. This democratization has spurred a surge in commercial applications, particularly in Earth observation, where companies can deploy swarms of small satellites to achieve revisit rates impossible for larger platforms. As per the European Small Satellite Alliance, many new missions are currently in development across the continent, leveraging automated assembly lines similar to those in the automotive industry to produce satellites at scale. The availability of dedicated small launch vehicles and rideshare opportunities from European spaceports further enhances accessibility.

MARKET RESTRAINTS

Fragmented Regulatory Landscape and Spectrum Allocation Delays

The implementation of a fragmented regulatory framework across European member states acts as a significant restraint on the small satellite market by creating bureaucratic hurdles that delay mission deployment and increase operational complexity. While the European Union strives for a single market, regulations regarding frequency allocation, launch licensing, and end-of-life disposal often vary between national authorities, forcing operators to navigate differing legal requirements. As per the European Parliament, the lack of a unified European space law means that companies must seek approvals from multiple jurisdictions to operate a constellation that crosses borders, leading to prolonged timelines before a mission becomes operational. This administrative inconsistency disproportionately affects agile NewSpace startups that lack the legal resources to manage multinational compliance efforts compared to established aerospace primes. As per the European Satellite Operators Association, the uncertainty surrounding liability regimes and the coordination of radio frequencies with the International Telecommunication Union further discourages private investment in innovative constellations. The absence of a streamlined licensing process stifles agility and prevents European companies from competing effectively with counterparts in the United States, where the regulatory pathway is more centralized and predictable.

Limited Domestic Launch Capacity and Dependency on Foreign Providers

The Europe small satellite market faces a critical bottleneck due to the insufficient availability of dedicated domestic launch services tailored specifically for small payloads, leading to reliance on foreign providers and unpredictable launch schedules. Historically, European launch infrastructure was designed for heavy-lift vehicles, which are economically unviable for launching single small satellites or small clusters, forcing operators to wait for rideshare opportunities that dictate their orbit and timeline. As per the European Space Transportation Association, the gap in dedicated small launch capabilities has resulted in backlogs, with many European small satellite manufacturers forced to launch their assets on rockets from the United States, India, or China, thereby compromising data sovereignty and supply chain security. The delayed development of European small launchers has exacerbated this issue, leaving the industry vulnerable to geopolitical tensions and global logistics disruptions. As per industry analysts, the cost and lead time associated with securing a slot on a foreign rideshare mission can negate the cost advantages gained through small satellite miniaturization. This dependency limits the frequency of launches required to maintain and refresh large constellations, hindering the ability of European operators to offer competitive real-time services. Until a robust and reliable domestic small launch ecosystem matures, the market will remain constrained by logistical limitations.

MARKET OPPORTUNITIES

Expansion of Hybrid Multi-Orbital Architectures for Seamless Connectivity

The convergence of geostationary and low Earth orbit technologies offers a notable opportunity for the Europe small satellite market by enabling hybrid architectures that deliver ubiquitous, low latency connectivity for diverse applications. As demand for bandwidth surges due to the Internet of Things and fifth generation backhaul requirements, single orbit systems struggle to meet diverse needs, creating a niche for integrated solutions that leverage the coverage of high orbits and the speed of low orbit small satellite swarms. As per the European Telecommunications Standards Institute, the future of mobile communications lies in non-terrestrial networks that integrate with terrestrial infrastructure, a vision that European manufacturers are positioned to realize through their expertise in both segments. This architectural shift allows service providers to offer uninterrupted coverage for maritime, aviation, and remote industrial applications, opening new revenue streams in sectors previously underserved by static networks. As per research from the University of Surrey, hybrid systems can optimize traffic routing dynamically, reducing congestion and improving quality of service for critical applications like telemedicine and autonomous driving. The opportunity extends to software-defined small satellites that can reconfigure their payloads in orbit to adapt to changing traffic patterns, maximizing asset utilization.

Commercialization of In-Orbit Servicing and Active Debris Removal

The growing congestion in Earth’s orbit and the increasing value of space assets offer a lucrative opportunity for the Europe small satellite market through the emergence of in-orbit servicing and active debris removal industries. With thousands of defunct satellites and fragments posing collision risks, there is a need for missions that can extend the life of existing satellites through refueling and repair or remove hazardous debris to ensure the sustainability of space operations. As per the European Space Agency, the ClearSpace-1 mission represents a pioneering step in this direction, demonstrating the feasibility of capturing and deorbiting space junk using small satellite technologies. The economic potential lies in offering life extension services that allow operators to defer the costly replacement of assets, creating a new service-based revenue model for small satellite manufacturers. As per the European Commission’s space traffic management proposals, future regulations may mandate end-of-life disposal plans, effectively creating a regulated market for debris removal services. This sector also drives innovation in robotics and autonomous rendezvous technologies, which have spin-off applications in other industries.

MARKET CHALLENGES

Intensifying Global Competition and Price Pressure from Mega-Constellations

The aggressive competition from established global players, particularly those deploying massive low Earth orbit constellations that benefit from economies of scale and vertical integration is a significant challenge to the Europe small satellite market growth. Competitors in the United States have launched large numbers of small satellites, driving down the cost per bit of bandwidth and setting price expectations that European manufacturers, often operating with smaller production runs and higher labor costs, struggle to match. As per the Consultative Committee for Space Data Systems, the influx of low-cost capacity from these mega-constellations threatens to commoditize the broadband market, squeezing margins for European operators who rely on traditional business models. The ability of foreign rivals to reuse rocket boosters and mass-produce satellites in assembly-line fashion creates a significant cost disparity that undermines the competitiveness of European launch services and hardware suppliers. As per the International Astronautical Federation, the dominance of non-European constellations in the consumer broadband sector makes it difficult for European initiatives to gain market traction without substantial state subsidies.

Critical Shortage of Specialized Workforce and Technical Talent

The Europe small satellite market faces a bottleneck due to the shortage of skilled professionals possessing the specialized knowledge required for advanced spacecraft engineering, orbital mechanics, and space cybersecurity. As the sector expands and technologies become more complex, the demand for experts in fields such as electric propulsion, software-defined payloads, and autonomous navigation has surged beyond the available supply of qualified personnel. As per Eurofound, the European labor market experiences a mismatch in high-tech sectors, with universities struggling to update curricula fast enough to meet the rapid pace of innovation in the small satellite industry. This talent gap delays project timelines and increases the cost of labor, as companies compete for a limited pool of experienced engineers and scientists. As per the European Space Policy Institute, the aging workforce in traditional aerospace primes is not being replaced at a sufficient rate, while the NewSpace sector struggles to attract talent away from more established tech industries. The lack of standardized training programs across member states further exacerbates the issue, hindering labor mobility within the single market. Until this skills deficit is addressed through targeted education initiatives and immigration policies, the European small satellite industry risks being constrained by human capital limitations rather than technological capability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.28% |

| Segments Covered | By Application, Orbit Class, End User, Propulsion Tech, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Airbus Defence and Space, Thales Alenia Space, OHB SE, Surrey Satellite Technology Ltd, AAC Clyde Space, GomSpace, Exotrail, Spire Global, ICEYE, Planet Labs, Isar Aerospace, Rocket Factory Augsburg, Skyrora, PLD Space, and D Orbit |

SEGMENTAL ANALYSIS

By Application Insights

The earth observation segment dominated the market by holding the major share of the Europe small satellite market in 2025. The dominance of earth observation segment in the European market is driven by the critical need for high-frequency, high-resolution data to monitor climate change, manage agriculture, and ensure border security and the operational success and expansion of the Copernicus program, which increasingly relies on constellations of small satellites to provide revisit rates that large single platforms cannot achieve. As per the European Space Agency, the demand for Sentinel data has grown significantly, with widespread access to free imagery prompting commercial entities to fill gaps in temporal resolution with proprietary small satellite fleets. The European Green Deal further accelerates this demand, as policymakers require precise, real-time metrics on carbon emissions, deforestation, and water quality to enforce environmental regulations. As per the European Environment Agency, the ability of small satellite swarms to capture rapid changes in weather patterns and natural disasters makes them indispensable for emergency response and civil protection services. Furthermore, the agricultural sector utilizes this data for precision farming, optimizing crop yields and reducing fertilizer usage, which aligns with sustainability goals. The versatility of small sensors capable of operating in optical, radar, and hyperspectral modes ensures that Earth observation remains the foundational application for the European small satellite ecosystem.

The communication segment is anticipated to record a CAGR of 17.4% over the forecast period in the Europe small satellite market. The urgent strategic imperative to establish sovereign, low-latency broadband connectivity across the continent and its surrounding regions, independent of non-European infrastructure and the European Union's IRIS² initiative that plans to deploy a constellation of small satellites in low Earth orbit to provide secure government communications and bridge the digital divide in rural areas are propelling the communication segment in the European market. As per the European Commission, the project aims to deliver advanced connectivity across the EU, creating strong demand for mass-produced communication small satellites. The rise of the Internet of Things also propels this growth, as industries ranging from maritime logistics to energy grids require ubiquitous, low-power connectivity for asset tracking and remote monitoring that terrestrial networks cannot provide. As per the European Telecommunications Standards Institute, the integration of non-terrestrial networks with fifth generation mobile systems creates a hybrid architecture where small satellites play a pivotal role in ensuring seamless coverage. The shift towards software-defined payloads allows these satellites to be reconfigured in orbit, maximizing their utility and lifespan.

By End User Insights

The commercial segment held the dominant position in the Europe small satellite market by holding the major share of the Europe small satellite market in 2025. The growth of the commercial segment in the European market can be credited to the vibrant ecosystem of NewSpace startups and established telecommunications operators driving innovation and deployment. The democratization of space access that has enabled private companies to develop cost-effective business models for Earth observation data sales, broadband services, and IoT connectivity is further boosting the expansion of the commercial segment in the regional market. As per the European Small Satellite Alliance, many private ventures have emerged across the continent, leveraging venture capital to fund constellations that serve diverse industries such as finance, insurance, and agriculture. The ability of commercial entities to iterate quickly and adopt agile manufacturing techniques allows them to outpace traditional government programs in terms of launch frequency and technological adoption. As per industry analysts, the market for downstream data services has matured, with businesses willing to pay premiums for real-time insights into supply chains, commodity trading, and environmental compliance. Furthermore, the rise of ride-sharing launch opportunities has lowered the barrier to entry, allowing smaller commercial players to deploy assets without bearing the full cost of a dedicated launch.

The military and government segment is poised to register a CAGR of 16.2% over the forecast period in the European small satellite market. Factors such as a paradigm shift in defense strategy following recent geopolitical instabilities, the recognition that space is a contested domain that require resilient, distributed architectures that can withstand jamming, cyberattacks, and physical threats better than large and singular assets are propelling the military and government segment in the European market. As per the European Defence Agency, member states are actively collaborating on projects like the Secure Connectivity Programme to ensure sovereign control over critical data links, reducing reliance on commercial or foreign government assets. The need for tactical reconnaissance and real-time battlefield awareness drives the procurement of small satellites equipped with advanced sensors and encrypted communication payloads. As per national defense ministries, the concept of "space resilience" through constellations of small satellites has become a cornerstone of national security strategies, prompting long-term procurement contracts. Additionally, the dual-use nature of many small satellite technologies allows for efficient resource sharing between civil and military applications, further accelerating adoption.

By Propulsion Tech Insights

The electric propulsion segment led the market by capturing the highest share of the Europe small satellite market in 2025. The dominance of the electric propulsion segment in the European market can be credited to its superior fuel efficiency, extended operational lifespan, and precise orbital maneuvering capabilities which are critical for constellation maintenance. The necessity for small satellites to perform complex mission profiles such as station keeping, collision avoidance, and end-of-life deorbiting within strict mass and volume constraints is further boosting the growth of the electric propulsion segment in the European market. As per the European Space Agency, electric thrusters including Hall effect and ion thrusters provide significantly higher specific impulses compared to chemical alternatives, allowing small satellites to carry less propellant and more payload or operate for longer durations. This efficiency is paramount for commercial operators seeking to maximize the return on investment for each unit in a large constellation. As per European propulsion manufacturers, the miniaturization of electric propulsion systems has made them accessible even for CubeSats, enabling missions that were previously impossible due to delta-v limitations. The ability to perform gradual orbit raising from rideshare drop-off orbits to operational altitudes further enhances mission flexibility and reduces launch costs. Furthermore, the clean nature of electric propulsion reduces the risk of contamination for sensitive optical instruments, making it the preferred choice for Earth observation missions. The maturity of this technology in Europe, supported by robust supply chains and extensive flight heritage, secures its position as the standard for modern small satellite operations.

The gas-based propulsion segment is anticipated to showcase a CAGR of 19.4% over the forecast period in the European small satellite market owing to the increasing demand for high-thrust, impulsive manoeuvres required for rapid deployment and collision avoidance and the development of green, non-toxic propellants such as nitrous oxide and krypton that offer safer and easier-to-handle alternatives to traditional hydrazine while providing higher thrust densities than electric systems. As per the European Space Transportation Association, new regulations regarding active debris removal and safe disposal are pushing operators to equip small satellites with hybrid or dedicated chemical systems capable of rapid deorbiting. The simplicity and reliability of cold gas and warm gas systems make them ideal for short-duration missions and technology demonstrators where cost and complexity must be minimized. As per emerging European propulsion startups, the adoption of additively manufactured thrusters has reduced production costs and lead times, making gas-based systems attractive for mass-produced constellations. The ability to provide immediate thrust for attitude control and orbit insertion appeals to operators launching into crowded or specific orbital shells. This combination of regulatory pressure, safety improvements, and performance needs fuels the rapid ascent of gas-based technologies.

REGIONAL ANALYSIS

Germany Small Satellite Market Analysis

Germany held the dominant share of 26.5% of the European market share in 2025. The dominance of Germany in the European market is majorly driven by its robust industrial base, strong engineering heritage, and significant government funding for space initiatives. The dense network of specialized SMEs and research institutes such as the German Aerospace Center that pioneer advancements in miniaturized components, propulsion, and payload technologies and the federal government's strategic commitment to space sovereignty, evidenced by substantial investments in national security satellites and participation in key European programs like Galileo and Copernicus are further boosting the German market expansion. As per the German Federal Ministry for Economic Affairs and Climate Action, the national space strategy prioritizes the development of resilient low Earth orbit infrastructures, fostering a fertile environment for NewSpace startups. Furthermore, Germany hosts major manufacturing hubs for satellite buses and sensors, supplying components to projects across the continent. As per the German Space Industry Association, the sector benefits from strong collaboration between academia and industry, accelerating the transfer of cutting-edge research into commercial products. The presence of leading launch service providers and ground station networks further strengthens the ecosystem.

France Small Satellite Market Analysis

France held a promising share of the Europe small satellite market in 2025. The growth of France in the European market is attributed to its strong state-led approach to space independence and a vibrant ecosystem of innovative startups. The Centre National d'Études Spatiales that actively drives the development of small satellite capabilities for defense, Earth observation, and technology demonstration and the French government's emphasis on "space power" status are contributing to the French market expansion. As per the French Space Agency, national funding mechanisms target the reduction of dependency on foreign launchers and components, stimulating domestic production of critical subsystems. The country is also home to a dynamic cluster of NewSpace companies in Toulouse and Paris, focusing on agile manufacturing and novel propulsion systems. As per the French Association of Aerospace Industries, the sector is seeing a rise in public-private partnerships aimed at developing dual-use technologies that serve both civil and defense needs. The availability of the Guiana Space Centre provides a strategic advantage for testing and potential future small launcher operations.

United Kingdom Small Satellite Market Analysis

The United Kingdom is predicted to showcase a prominent CAGR in the Europe small satellite market over the forecast period owing to its expertise in satellite communications, downstream data analytics, and a proactive regulatory environment. The thriving NewSpace sector that has attracted significant private investment and the government's National Space Strategy that aims to double the size of the UK space economy by 2030 through supportive policies and the development of domestic launch capabilities is contributing to the small satellite market expansion in the UK. As per the UK Space Agency, the establishment of spaceports in Scotland and Cornwall is designed to enable vertical and horizontal launches of small satellites, reducing reliance on foreign ranges and stimulating local industry growth. The nation's strength in telecommunications, anchored by operators like OneWeb, continues to drive demand for advanced small satellite buses and payloads. As per Tech Nation, the concentration of space tech clusters creates a collaborative environment where startups can rapidly prototype and deploy missions.

Italy Small Satellite Market Analysis

Italy is projected to account for a notable share of the Europe small satellite market during the forecast period due to its capabilities in radar Earth observation, optical payloads, and system integration for scientific missions. The success of the COSMO SkyMed constellation, the collaboration between the Italian Space Agency and industrial primes like Leonardo and Thales Alenia Space Italy and nation's strategic focus on dual-use technologies that serve both national defense and civil protection are favouring the growth of the Italian market. As per the Italian National Institute of Statistics, the aerospace sector is a strategic asset receiving sustained government support to maintain technological sovereignty in observation and communication. The country's geographical position makes it a hub for ground stations and data downlink facilities, enhancing its role in the operational phase of small satellite missions. As per the Italian Association of Aerospace Industries, there is growing emphasis on developing green propulsion technologies and sustainable satellite designs, aligning with broader European environmental goals.

Spain Small Satellite Market Analysis

Spain is estimated to witness a healthy CAGR in the Europe small satellite market over the forecast period due to its growing capabilities in small satellite manufacturing, microelectronics, and ground segment infrastructure. As per the Spanish National Institute of Aerospace Technology, investments are being made in the development of nanosatellite constellations for Earth observation and IoT connectivity, leveraging the country's semiconductor design sector. The strategic location of Spanish territory, including the Canary Islands, provides ideal sites for ground stations and future launch complexes, attracting international operators seeking diverse geographic coverage. As per the Spanish Association of Companies in the Space Sector, the number of space-related startups has multiplied in recent years, injecting fresh innovation into the supply chain.

COMPETITIVE LANDSCAPE

The competition in the Europe small satellite market is characterized by intense rivalry among established aerospace primes and agile NewSpace entrants who constantly innovate to capture market share through technological superiority and cost efficiency. Major players differentiate themselves by securing exclusive contracts for sovereign European programs and offering comprehensive end-to-end solutions that span manufacturing, launch, and operations. The market sees frequent announcements of strategic alliances and joint ventures aimed at pooling resources for mega-constellation projects and reducing the financial burden of development. Price competition is moderating as the focus shifts towards value-added services such as data analytics, cybersecurity, and in-orbit servicing rather than hardware costs alone. Regional specialists compete by providing niche capabilities in optical communications, radar imaging, or small satellite buses that complement the offerings of larger integrators. The barrier to entry remains high due to significant capital requirements and stringent regulatory standards, yet the rise of venture capital in the space sector is lowering these hurdles for innovative startups. Collaboration between industry and academia is accelerating the development of breakthrough technologies like quantum encryption and autonomous navigation. Overall the landscape is dynamic with companies vying to establish leadership in the transition towards sustainable, software-defined, and highly connected space architectures across the continent.

KEY MARKET PLAYERS

Some of the notable key players in the Europe small satellite market are

- Airbus Defence and Space

- Thales Alenia Space

- OHB SE

- Surrey Satellite Technology Ltd

- AAC Clyde Space

- GomSpace

- Exotrail

- Spire Global

- ICEYE

- Planet Labs

- Isar Aerospace

- Rocket Factory Augsburg

- Skyrora

- PLD Space

- D-Orbit

Top Players in the Market

- OHB SE stands as a premier aerospace manufacturer in the Europe small satellite market, delivering advanced platforms for navigation, Earth observation, and secure communications globally. The company significantly contributes to the international space sector by serving as a key industrial partner for major European Union initiatives like Galileo and the upcoming IRIS squared constellation. OHB recently strengthened its market position by securing contracts to build multiple satellites for sovereign European security programs, highlighting its capability in dual-use technologies. The firm actively invests in developing modular small satellite buses that allow for rapid customization and cost-effective serial production. By expanding its network of specialized subsidiaries across Europe, OHB ensures robust supply chain resilience and localized expertise for international clients. Their focus on electric propulsion and optical communication technologies enables high-performance missions within strict mass constraints. This strategic commitment to innovation and sovereignty solidifies their reputation as a global leader in the small satellite industry.

- Airbus Defence and Space leverages its extensive engineering heritage to maintain a dominant presence in the Europe small satellite market through comprehensive offerings in military, civil, and commercial segments. The company contributes globally by providing critical infrastructure for deep space exploration, planetary science, and secure government communication networks using small form factors. Airbus recently enhanced its European footprint by announcing significant investments in automated manufacturing lines specifically designed to accelerate the production of small satellite constellations. The firm focuses on integrating artificial intelligence into satellite operations to enable autonomous collision avoidance and dynamic resource management for swarms. Through strategic partnerships with emerging launch service providers, Airbus ensures reliable and frequent access to space for its diverse portfolio of small missions. Their dedication to developing next-generation high-throughput small satellites supports the growing demand for global broadband connectivity and real-time Earth monitoring. This customer-centric approach combined with continuous technological evolution ensures the company remains a trusted partner for space agencies worldwide.

- Surrey Satellite Technology Ltd is a leading innovator in the Europe small satellite market, distinguished by its pioneering role in the CubeSat and microsatellite revolution over the past four decades. The company plays a pivotal role globally by supplying complete small satellite systems and components for navigation, science, and security applications with a strong emphasis on cost efficiency. SSTL recently strengthened its market position by winning key contracts for the development of disaster monitoring constellations and technology demonstration missions for the European Space Agency. The firm actively invests in research and development to advance chemical and electric propulsion solutions tailored specifically for small platform maneuverability and deorbiting. By expanding its collaborative projects with universities and NewSpace startups, SSTL fosters a vibrant ecosystem of innovation and talent development across the continent. Their focus on modular architectures allows for rapid deployment of tailored solutions meeting the specific needs of diverse international customers. This dedication to versatility and technological excellence secures their status as a crucial enabler of European space autonomy and commercial growth.

Top Strategies Used by Key Market Participants

Key players in the Europe small satellite market primarily employ strategies focused on vertical integration and strategic partnerships to secure supply chains and enhance technological capabilities. Companies heavily invest in research and development to pioneer software-defined payloads and electric propulsion systems that extend satellite lifespans and operational flexibility. Strategic collaborations with national space agencies and the European Union enable firms to secure long-term contracts for flagship programs like Galileo and Copernicus. Expanding manufacturing capacities through automation and digital twins helps companies reduce production costs and accelerate delivery times for large constellations. Firms increasingly adopt sustainable practices by developing active debris removal technologies and eco-friendly propulsion methods to comply with emerging space traffic regulations. Offering end-to-end services from design to launch and ground segment management allows providers to capture greater value across the entire mission lifecycle. Acquisitions of specialized startups in areas such as quantum communications and artificial intelligence allow major players to rapidly integrate cutting-edge innovations. Diversifying revenue streams by targeting commercial broadband and Internet of Things markets reduces dependency on government funding and fosters resilient growth.

MARKET SEGMENTATION

This research report on the European small satellite market has been segmented and sub-segmented based on categories.

By Application

- Communication

- Earth Observation

- Navigation

- Space Observation

- Others

By Orbit Class

- GEO

- LEO

- MEO

- By End User

- Commercial

- Military & Government

- Other

By Propulsion Tech

- Electric

- Gas Based

- Liquid Fuel

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the Europe small satellite market?

It refers to the industry involved in the development, launch, and operation of satellites weighing below 500 kg for various applications.

2. What factors are driving the Europe small satellite market growth?

Key drivers include rising demand for low cost satellite missions, technological advancements, and increasing use of satellite data.

3. What are small satellites used for in Europe?

They are used for communication, Earth observation, navigation, scientific research, and remote sensing.

4. Which countries lead the small satellite market in Europe?

Germany, the United Kingdom, France, Italy, and Spain are major contributors to the market.

5. What types of small satellites are commonly used?

Common types include nanosatellites, microsatellites, and CubeSats.

6. Who are the key end users in the Europe small satellite market?

Major end users include commercial organizations, government agencies, and defense sectors.

7. How does miniaturization impact small satellites?

Miniaturization enables smaller, lighter, and more cost efficient satellites with improved capabilities.

8. What role do private companies play in this market?

Private companies support satellite manufacturing, launch services, and satellite data solutions.

9. What challenges affect the Europe small satellite market?

Challenges include regulatory complexities, space debris concerns, and limited launch availability.

10. What is the future outlook of the Europe small satellite market?

The market is expected to grow steadily due to increasing satellite launches and rising demand for satellite based services.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com