Europe Sonar Market Size, Share, Trends & Growth Forecast Report By Product Type, By Application, By Solution, By End User, and By Country (United Kingdom, France, Germany, Italy, Spain, Netherlands, Sweden & Rest of Europe) – Industry Analysis and Forecast, 2026 to 2034

Europe Sonar Market Size

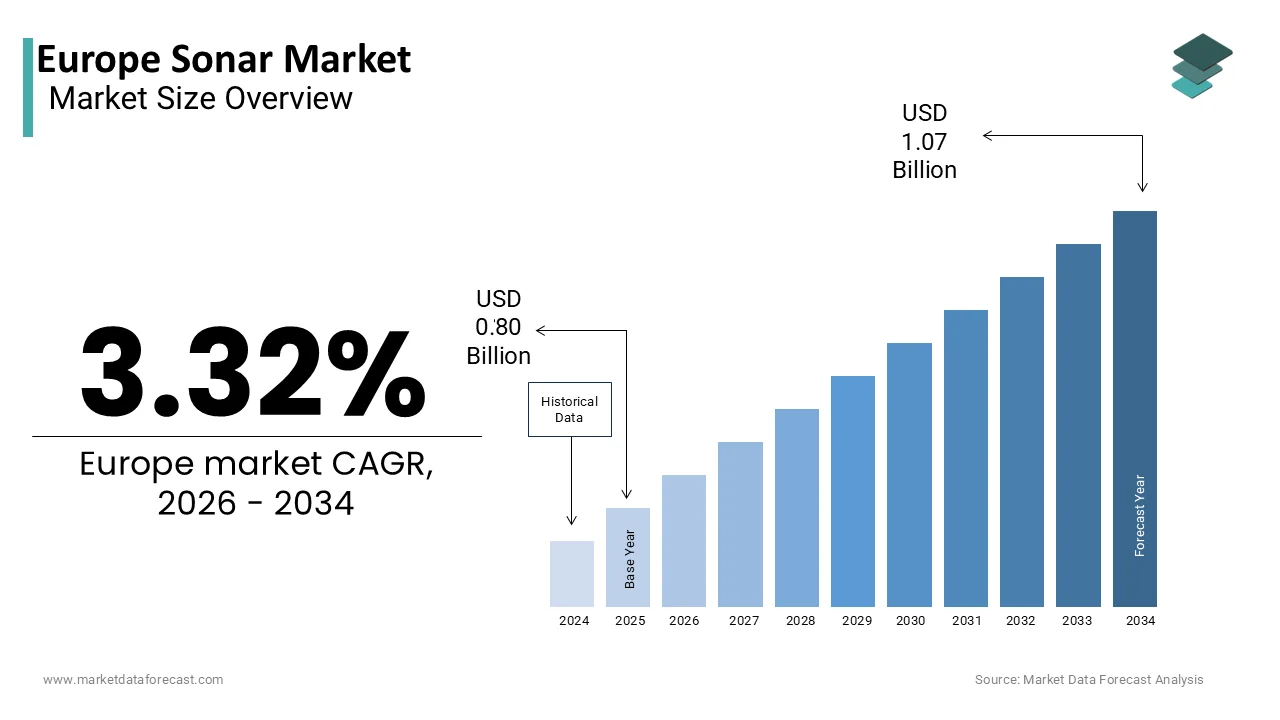

The Europe sonar market was valued at USD 0.80 billion in 2025, is estimated to reach USD 0.82 billion in 2026, and is projected to reach USD 1.07 billion by 2034, growing at a CAGR of 3.32% from 2026 to 2034.

Sonar encompasses a sophisticated ecosystem of acoustic technologies designed for underwater detection, navigation, and mapping, i ng serving both defense and commercial sectors. This industry includes active and passive systems deployed on surface vessels, submarines,s unmanned underwater vehicles,, es and fixed seabed installations to monitor maritime domains. The definition has evolved from simple echo sounding to complex networked arrays capable of real-time threat classification and environmental analysis. According to the European Maritime Safety Agency, global trade by volume moves through European waters, which necessitates advanced hydrographic surveying and obstacle avoidance systems to ensure safe passage. As per the European Environment Agency, the monitoring of marine biodiversity and noise pollution has become a regulatory priority,y which is driving the adoption of passive acoustic sensors for scientific research. According to the North Atlantic Treaty Organization, the alliance has identified undersea domain awareness as a critical capability g,, ap which is prompting member states to investnext-generationtion sonar suites to counter emerging submarine threats. The market is characterized by a shift toward digital beamforming and artificial intelligence integration, which enhances target resolution in cluttered shallow water environments. Regulatory frameworks regarding underwater noise emissions further shape product design, requiring manufacturers to develop quieter and more efficient transducers. This technological maturation transforms sonar from a standalone tool into an integral component of broader maritime security and oceanographic observation networks.

MARKET DRIVERS

Escalating Geopolitical Tensions and Undersea Domain Awareness Requirements

The resurgence of great power competition and increased security concerns in the North Atlantic and Arctic regions are majorly driving the growth of the European sonar market. Nations are urgently upgrading their anti-submarine warfare capabilities to detect increasingly quiet diesel electric and nuclear-powered submarines operating near critical infrastructure. As per the Stockholm International Peace Research Institute, European defense spending on naval platforms has increased, ed with a significant portion allocated to integrated sonar suites and towed array systems. The strategic importance of protecting undersea data cables and energy pipelines has further amplified demand for fixed seabed surveillance networks capable of continuous monitoring. According to the European Defence Agency, collaborative maritime projects now focus on enhancing undersea situational awareness through sensor fusion and networked acoustics. Navies across the continent are retrofitting legacy frigates with modern hull-mounted sonars to extend their operational lifespan and effectiveness against contemporary threats. The imperative to maintain control of sea lanes and deter hostile underwater activities drives sustained investment in high-frequency mine hunting and low-frequency detection systems. This strategic shift ensures that defense budgets remain robustly directed toward technologies that guarantee maritime superiority and asset protection in contested waters.

Expansion of Offshore Renewable Energy and Marine Infrastructure Projects

The aggressive pursuit of carbon neutrality and the massive rollout of offshore wind farms across Europe create substantial demand for specialized sonar technologies used in site surveying, installation,n and maintenance, which is further contributing to the expansion of the European sonar market. Developers rely on high-resolution multibeam echosounders and side scan sonars to map seabed topography, identify geological hazards,, ds and monitor scour around turbine foundations. According to WindEu, the continent has added new offshore wind capacity requiring extensive pre-construction surveys and ongoing integrity checks of subsea assets. As per the International Renewable Energy Agency, the lifecycle management of offshore installations necessitates regular underwater inspections to prevent structural failures and optimize energy output. The complexity of installing floating wind turbines in deeper waters further drives the need for advanced dynamic positioning sonars and underwater communication systems. Furthermore, the decommissioning of old oil and gas platforms requires precise acoustic imaging to ensure the complete removal of subsea infrastructure without environmental damage. Government mandates for marine spatial planning also utilize sonar data to designate protected areas and manage conflicting uses of the ocean. The convergence of green energy goals and the technical requirements of offshore engineering propels the commercial sector of the sonar market forward.

MARKET RESTRAINTS

Stringent Environmental Regulations Regarding Underwater Noise Pollution

The implementation of rigorous laws limiting anthropogenic noise in marine environments is impeding the growth of the European sonar market. Active sonar emits high-intensity sound pulses that can disrupt marine mammal communication, navigation,n and feeding patterns, ns leading to strict operational restrictions and permitting hurdles. As per the European Union Marine Strategy Framework Directive, member states are required to achieve good environmental st,atus, which includes keeping underwater noise levels below thresholds that cause harm to aquatic life. According to the European Environment Agency, several naval exercises and commercial survey projects have been delayed or cancelled due to objections from environmental groups and regulatory bodies concerned about cetacean safety. The requirement to implement mitigation measures such as soft start procedures and marine mammal observers increases operational costs and reduces the efficiency of sonar deployments. Manufacturers face pressure to develop low-impact alternatives or highly directional systems that minimize collateral noise exposure, which often involves complex and expensive engineering solutions. The varying interpretation of noise regulations across different national jurisdictions creates a fragmented operational landscape that complicatescross-borderr missions. These environmental constraints limit the frequency and intensity of active sonar use, thereby restraining market growth for traditional high-power systems.

High Development Costs and Complexity of Integration

The exorbitant financial investment required to research deve, develop, and certify advanced sonar systems is hampering the expansion of the European sonar market. Creating effective acoustic sensors capable of operating in diverse and challenging underwater conditions demands cutting-edge materials, sophisticated signal processing algorithms, and extensive sea trials. As per the European Defence Agency, the average cost of developing a new integrated sonar suite for a frigate has risen due to the increasing complexity of digital beamforming and artificial intelligence integration. For instance, certification processes involving rigorous testing against military standards can extend project timelines, thereby delaying revenue realization. The need to integrate sonar systems with existing combat management systems and other sensors on legacy platforms often requires custom engineering solutions that drive up costs significantly. Small medium-sizedized enterprises struggle to secure the necessary capital to fund these lengthy development cycles, leading to market consolidation where only a few large primes dominate. The risk of technical obsolescence before a system reaches full operational capability further deters investment in groundbreaking but unproven technologies. These economic and temporal constraints limit the pace of innovation and restrict the diversity of solutions available to end users.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Autonomous Target Recognition

The incorporation of artificial intelligence and machine learning into sonar processing is a prominent opportunity in the European sonar market. AI-driven algorithms can analyse vast amounts of acoustic data to distinguish between biological noise, mechanical interference,e and genuine targets with far greater accuracy than traditional rule-based systems. As per the NATO Science and Technology Organization, the adoption of cognitive sonar technologies is expected to improve detection ranges and reduce false alarm rates in cluttered environments. According to the European Commission Horizon Europe program, there is increased funding for projects focusing on autonomous underwater vehicles equipped with intelligent sonar payloads for mine countermeasures. This technological leap allows for the automatic identification of specific vessel types or mine signatures without human intervention, enabling faster decision-making in critical scenarios. Manufacturers who pioneer self-learning classification software will gain a decisive competitive advantage by offering superior situational awareness in dense acoustic landscapes. The ability to update threat libraries over the air ensures that sonar systems remain effective against emerging stealth technologies throughout their operational lifespan. Embracing these intelligent technologies positions the market to address the escalating complexity of undersea warfare and exploration effectively.

Deployment of Distributed and Networked Underwater Sensor Systems

The shift toward distributed architectures where multiple small, inexpensive sonar nodes operate as a coordinated network offers a lucrative opportunity for the European sonar market. Unlike traditional single-platform systems, networked sensors can provide wide-area monitoring, persistent tracking, and triangulation of targets with greater precision and redundancy. As per the European Defence Fund,d collaborative initiatives are underway to develop smart seabed infrastructures that integrate passive and active sonar nodes for continuous domain awareness. According to the Centre for European Policy Studies, es networked systems are expected to reduce the operational cost of patrolling vast maritime zones compared to relying solely on manned vessels. The modularity of these systems allows for rapid deployment and reconfiguration based on evolving threat scenarios or mission requirements. Advances in underwater acoustic communication and energy harvesting technologies are making long-endurance autonomous sensor networks technically feasible and economically viable. The strategic advantage of having a persistent invisible fence around critical assets appeals strongly to naval planners and port authorities. Capitalizing on this shift toward connected undersea ecosystems opens new revenue streams for companies specializing in miniaturized transducers and mesh networking protocols.

MARKET CHALLENGES

Complexity of Operating in Shallow and Littoral Waters

Operating sonar systems in shallow coastal and littoral environments presents a formidable technical challenge due to complex acoustic propagation effects caused by seabed interactions, surface reverberation, and thermal layers. These conditions create high levels of clutter and multipath interference that severely degrade detection performance and target classification accuracy for conventional systems. As per the Royal Netherlands Navy, its operations in the shallow waters of the North Sea and Baltic Sea frequently encounter difficulties in distinguishing small mines from natural debris due to intense bottom bounce. According to naval exercise reports, false alarm rates in littoral zones are often high,h forcing operators to rely on slower and more dangerous manual verification methods. The variability of sound speed profiles in coastal areas requires constant recalibration of sonar parameters, rs which demands highly skilled operators and adaptive software. Developing systems capable of automatically compensating for these dynamic environmental factors remains a significant engineering hurdle that limits operational effectiveness. The increasing focus on coastal defense and port security amplifies the need for reliable shallow water solutions, yet current technology often falls short of expectations. Until these acoustic challenges are fully overcome, the reliability of sonar in critical near-shore scenarios will remain a persistent concern for maritime forces.

Shortage of Specialized Acoustic Engineers and Technical Talent

The acute scarcity of engineers with expertise in underwater acoustics, signal processing, and ocean physics poses a critical challenge to the sustainability and innovation capacity of the European sonar market. The specialized nature of this field requires a deep understanding of wave propagation, fluid dynami, cs, and advanced mathematics skills that are increasingly rare in the general labor pool. As per the European Centre for the Development of Vocational Training,g the deficit of qualified personnel in the maritime defense sector has widened, hindering the pace of research and development. According to industry surveys, many sonar manufacturers report difficulties in recruiting staff capable of designing next-generation array architectures and processing algorithms. This talent gap is exacerbated by an aging workforce where experienced acousticians are retiring without sufficient successors to transfer their tacit knowledge. The competition for skilled professionals from adjacent sectors like telecommunications and consumer electronics further drains the available talent pool. Addressing this human capital constraint requires significant investment in university partnerships and specialized training programs, which take years to yield results. Without resolving these foundational issues, the market faces bottlenecks that could impair its ability to meet urgent defense and commercial requirements.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Application, Device Solution, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Thales Group, Atlas Elektronik GmbH, Kongsberg Gruppen ASA, Ultra Electronics Holdings plc, Sonardyne International Ltd., Teledyne Technologies Incorporated, Navico Holding AS, L3Harris Technologies Inc., Lockheed Martin Corporation, Raytheon Technologies Corporation, Furuno Electric Co., Ltd., Japan Radio Co., Ltd. |

SEGMENTAL ANALYSIS

By Product Type Insights

The hull-mounted sonar segment dominated the market by commanding the highest share of the European sonar market in 2025. The growth of the hull-mounted sonar segment in the European market is driven by its status as the primary and indispensable sensor suite installed on virtually all active naval surface vessels and submarines. The fundamental requirement for ships to possess organic detection capabilities for navigation, obstacle avoidance, and anti-submarine warfare, without relying on external assets, is also contributing to the expansion of the hull-mounted sonar segment in the European market. As per the European Defence Agency, new frigate and destroyer construction programs have specified integrated hull-mounted sonars as a mandatory component of the combat system architecture. The second major driver is the continuous modernization of existing fleets, where legacy analog systems are being replaced with advanced digital arrays, capable of superior target classification in shallow waters. According to the Royal Navy, upgrade programs for its Type 23 frigates included the installation of next-generation hull-mounted sonars to extend their operational life until the arrival of new Type 26 vessels. The reliability and proven performance of these systems in diverse oceanographic conditions make them the preferred choice for navies across the continent. Furthermore, the integration of hull-mounted sonars with shipboard combat management systems allows for seamless data fusion, which is critical for rapid decdecision-makingring high intensity operations. These factors ensure that hull-mounted systems remain the cornerstone of underwater sensing infrastructure.

The deployable deep sonar and towed array segment is projected to register the highest CAGR of 13.3% over the forecast period in the European market, owing to the urgent need to detect ultra-quiet submarines in deep water environments, where hull-mounted sensors suffer from thermal layer limitations. As per the North Atlantic Treaty Organization, member states have identified a critical gap in low-frequency detection capabilities, which is prompting significant investment in variable-depth and long towed array systems. According to the French Navy, the deployment of towed arrays on FREMM frigates has increasedto enhance surveillance ranges beyond the horizon. The ability of these systems to operate below the thermocline allows them to bypass acoustic shadow zones, which often hide hostile submarines from surface ship sensors. Additionally, the modularity of deployable systems enables smaller vessels to gain deep water capabilities without permanent structural modifications. The rising threat of advanced diesel-electric submarines operating in deep waters further accelerates the procurement of these sophisticated sensors. The combination of tactical necessity and technological advancement positions this segment as the most rapidly expanding category in the product landscape.

By Application Insights

The defense segment held the dominant position in the European sonar market in 2025, holding the major share of the European sonar market in 2025. The dominating position of the defense segment in the European market is fueled by escalating geopolitical tensions, the prioritization of national security, and maritime domain awareness by European governments. As per the Stockholm International Peace Research Institute, European military spending on naval platforms has reached record levels, with a substantial portion allocated to anti-submarine warfare suites, including sonar systems. The second critical driver is the mandate from NATO allies to enhance collective defense capabilities, which requires interoperable and advanced sonar networks across member navies. According to the European Defence Industrial Development Programme, funded maritime projects now focus on improving undersea situational awareness through new sensor technologies. The need to protect strategic assets, such as nuclear deterrent submarinesand aircraft carriers, necessitates the deployment of the most sophisticated passiveand active on-board systems available. Furthermore, the increasing frequency of naval exercises, a patrolsin contested waters, drives the demand for robust and reliable detection equipment. The existential nature of maritime defense ensures that budget allocations for sonar technology remain resilient, even during economic downturns. These strategic imperatives secure the top spot for the defense sector in the regional market.

The commercial segment is anticipated to witness the fastest CAGR of 15.5% over the forecast period in the European sonar market. Factors such as the explosive expansion of the offshore renewable energy sector, the stringent requirements for marine environmental monitoring, and the European Green Deal targets that mandate the installation of new offshore wind capacity are driving the expansion of the commercial segment in the European market. As per WindEurope, the continent has added offshore wind capacity, creating unprecedented demand for high-resolution multibeam echosounders and side scan sonars, used in site surveys. According to the International Hydrographic Organization, the need for updated nautical charts to support safe navigation for larger commercial vesselsand autonomous shipsis driving investments in hydrographic survey equipment. Additionally, the growing regulatory pressure to monitor underwater noise pollution and marine biodiversity forces oil and gas companies andshipping lines to adopt passive acoustic monitoring systems. The emergence of underwater robotics for pipeline inspectionand aquaculture management further broadens the addressable market for compact and cost-effectivesonar solutions. The convergence of green energy transitions nd digitalization in maritime logistics propels the commercial segment to the forefront of market growth.

By Solution Insights

The hardware segment led the market by capturing the leading share of the European sonar market in 2025. The growth of hardwthe are segment in the European market is driven by the physical necessity of transducers, transmitters, receivers, and display units to generate and process acoustic signals. As per the European Association of Maritime Industries, sonar project budgets have been largely allocated to hardware procurement, including array elements and processing cabinets. The second major driver is the ongoing replacement cycle of aging analog hardware, with modern digital systems that offer higher resolution and better reliability. According to naval procurement records, the refurbishment of submarine fleets across Europe involves the complete overhaul of sensor arraysand control consoles, to meet current operational standards. The complexity of manufacturing specialized piezoelectric materials and precision-machined housingscreates high barriers to entry, ensuring that established hardware manufacturers retain market control. Furthermore, the integration of hardware with platform-specific interfaces requires custom engineering, which adds value and stickiness to physical supplies. The tangible nature of these assets and their critical role in mission successsolidify the leading position of the hardware solution in the market structure.

The software segment is anticipated to experience a CAGR of 16.5% over the forecast period in the European sonar market. The growing reliance on artificial intelligence and machine learning algorithmsfor autonomous target recognition, nd signal processing, and the realization that hardware alone cannot cope with the complexity of modern acoustic environments, filled with biological noise, nd clutter ar, are propelling the growth of the software segment in the European market. As per the NATO Science and Technology Organization, the adoption of cognitive sonar software has improved detection ranges and reduced false alarm rates, in recent trials, y enabling adaptive beamforming and real-time classification. According to the European Commission Horizon Europe program, there is significant funding for projects developing open architecture software frameworksthat allow for rapid updates to threat libraries, without hardware changes. The ability to simulate complex underwater scenariosand train algorithms virtually before deploymentreduces development costs nd time to market. Additionally, the shift toward networked sonar systems requires sophisticated middleware to manage data fusion and communicationbetween distributed nodes. The recurring revenue model of software licensesand maintenance contracts also attracts vendors to this high-margin. The convergence of big data analyticsand acoustic science positions software as the most dynamically growing component of the sonar ecosystem.

By End-User Insights

The line fit segment captured the major share of the European sonar market in 2025. The leading position of the line fit segment can be credited to the robust pipeline of new naval vessel constructionand the increasing production of specialized commercial offshore support vessels. As per the European Shipbuilding Strategy, new major combatants, including frigates nd submarines, have been under construction or planned inEuropean shipyards, all requiring factory-installed systems. The second critical driver is the efficiency and cost-effectiveness of installing sonar equipment during the build phase, which avoids the complex and expensiveretrofitting processes required later. According to major shipbuilders like Fincantieri nd Navantia, original equipment manufacturer contracts for integrated sonar suites constitute the bulk of their sensor procurement budgets. New vessels are designed with optimized hull forms and internal layouts, specifically to accommodate large towed arrays and dome-mounted sonars, for maximum performance. Furthermore, the requirement for seamless integration with new combat management systems favors line fit installations, where software and hardware can be tested together before delivery. The long lead times of shipbuilding programs ensure a steady and predictable demand stream for line-fit sonar solutions, securing its market dominance.

The retrofit segment is anticipated to exhibit a CAGR of 14.4% over the forecast period in the European market due to the urgent need to extend the service life of existing naval assetsand upgrade their capabilities to counter modern threats. As per the UK Ministry of Defence, the Life Extension Program for its Type 23 frigates includes comprehensive upgrades to sonar systems, to ensure they remain effective against next-generation submarines, until the Type 26 enters service. According to the German Navy, similar mid-life update programs for its U212A submarines involve the replacement of legacy sonar arrays with digital equivalents to improve detection ranges. The rapid evolution of submarine stealth technology renders older sonar systems obsolete faster than platform lifecycles, necessitating frequent technological refreshes. Additionally, the modular design of modern sonar systems facilitates easier installation on older vessels, reducing downtimeand costs. The rising threat landscape in the North Atlantic nd Mediterraneancompels operators to enhance the sensory perception of their existing ships immediately. The combination of fiscal prudence and operational necessity propels the retrofit segment to the forefront of market growth.

COUNTRY LEVEL ANALYSIS

United Kingdom Sonar Market Analysis

The United Kingdom led the sonar market in Europe in 2025 with 25.5% of the regional market share. The dominance of the UK in the European market is driven by its world-class naval industrial baseand aggressive maritime defense strategy. The nation serves as the primary hub for developing advanced sonar technologies, with major contractors delivering cutting-edge systems for global export and domestic use. As per the UK Ministry of Defence, the AUKUS partnership and the Future Combat Air System initiatives drive investment toward next-generation sea sensing capabilities. The Royal Navy's continuous modernization of its Astute class submarinesand Type 26 frigates ensures sustained demand for high-performance hull-mounted and towed array sonars. According to the Society of Underwater Technology, UK-based research institutions lead Europe in acoustic modelingand signal processing algorithms, fostering a vibrant innovation ecosystem. The strong collaboration between government defense labs and private industry accelerates the transition of conceptual technologies into operational systems. Furthermore, the UKUK'sommitment to protecting its exclusive economic zone and undersea cables drives the deployment of fixed seabed surveillance networks. The presence of premier testing facilities in Loch Ness and Portland allows for rigorous validation of systems under realistic conditions. The combination of technological prowess, strategic foresight, and industrial capacity solidifies the UK's position as the dominant force in the regional sonar market.

France Sonar Market Analysis

France was a promising regional segment in the European sonar market in 2025. The growth of France in the European market is attributed to its policy of strategic autonomy and robust nuclear deterrent program. The country leverages its independent industrial base to produce comprehensive sonar suites that equip its Barracuda-class submarines and FREMM frigates, while attracting international buyers. As per the French Directorate General of Armaments, investment in sovereign underwater detection technologies has increased to ensure immunity from foreign supply chain disruptions. The successful deployment of FreFrench-madenar systems in various global operations has enhanced their reputation for reliability, driving further sales to allied nations. According to the French Naval Group, exports of integrated sonar packages have grown, fueled by demand from countries seeking non-aligned defense solutions. The French approach emphasizes fully integrated mission systems, where sonar works seamlessly with torpedoesand command systems, maximizing combat efficiency. Government support for research into quantum sensing and low-frequency acoustics positions France at the forefront of future detection methods. The emphasis on maintaining a full spectrum of capabilities, from shallow water mine huntingto deep ocean tracking, ensures a diverse and resilient product portfolio. These strategic priorities ensure France remains a key growth engine for the European sonar industry.

Germany Sonar Market Analysis

Germany is anticipated to account for a significant share of the European sonar market during the forecast period owing to its renowned engineering sector nd significant investments in upgrading its U-boat and frigate fleets. The nation is undertaking extensive modernization programs to equip its Type 212CD submarines d BadeBaden-Württembergss frigates with state-of-the-art sonar arrays. As per the German Federal Ministry of Defence, the special fund for the Bundeswehr has allocated resources specifically for enhancing undersea warfare capabilities, including advanced passiveand active sonars. The German engineering sector excels in producing high precision transducers and digital signal processing units, which are integrated into both domestic nd collaborative European projects. According to the German Marine Industries Consortium, contracts for sonar equipment have risen, as part of the broader effort to achieve full operational readiness. The focus on developing common European standards for underwater sensors promotes interoperability and reduces costsfor partner nations. Furthermore, Germany's active participation in joint NATO initiatives drives innovation in networked sonar solutions. The strong regulatory framework ensures that all installed systems meet the highest safety and performance benchmarks. The synergy between substantial funding, industrial expertise, and collaborative spirit makes Germany a vital player in the market.

Italy Sonar Market Analysis

Italy is estimated to hold a notable share of the European sonar market during the forecast period due to its specialized expertise in designing sonar systems optimized for the complex acoustic environments of the Mediterranean Sea. The Italian aerospace nd defense industry has developed renowned sonar solutions tailored for littoral warfare, mine countermeasures, and submarine detection in shallow waters. As per the Italian Ministry of Defence, the renewal of the U212NFS submarine fleet and the construction of new PPA offshore patrol vesselsinclude the installation of advanced, domestically produced sonar suites. The country's strong naval tradition drives demand for versatile systems, capable of operating in congested and noisy coastal zones. According to Leonardo S.p.A., exports of IItalian-madesonar systems have increased, due to their proven performance in diverse climatic conditions. The collaboration with other European nations on joint frigate programs ensures that Italian companies contribute advanced components to multinational platforms. The focus on compact and lightweight systems allows for effective protection nd detectionof smaller vessels without compromising stability. Government incentives for research and developmentencourage the adoption of new materias, nd miniaturized electronics. Italy's specific strengths in littoral sonar technology ensure a distinct and vvaluable nichewithin the broader European landscape.

COMPETITIVE LANDSCAPE

The competition in the European sonar market is characterized by intense rivalry among established defense giants and specialized technology firms that vie for dominance through technological superiority and strategic alliances. Market leaders leverage their extensive experience and deep relationships with national governments to secure major contracts for flagship submarine and frigate programs. The landscape is highly dynamic, with companies constantly striving to integrate advanced artificial intelligence and machine learning capabilities into their acoustic suites to counter evolving underwater threats. Regulatory compliance regarding export controls and data security acts as a significant barrier to entry, ensuring that only well-capitalized entities with robust quality assurance systems can thrive. Price competition remains fierce, particularly in retrofit programs where budget constraints force manufacturers to optimize costs while maintaining performance standards. Strategic acquisitions and joint ventures are becoming increasingly common as firms seek to acquire niche acoustic technologies or expand their geographical reach rapidly. This competitive environment fosters rapid technological advancement and benefits end users through improved detection ranges and innovative solutions across the region.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global Europe Sonar Market include

- Thales Group

- Atlas Elektronik GmbH

- Kongsberg Gruppen ASA

- Ultra Electronics Holdings plc

- Sonardyne International Ltd.

- Teledyne Technologies Incorporated

- Navico Holding AS

- L3Harris Technologies Inc.

- Lockheed Martin Corporation

- Raytheon Technologies Corporation

- Furuno Electric Co., Ltd.

- Japan Radio Co., Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Thales Group stands as a preeminent global leader in naval defense systems,s delivering advanced sonar suites that protect surface vessels and submarines across diverse operational theaters. The company contributes significantly to the worldwide market by providing integrated underwater warfare solutions for major naval programs, ms including frigates and nuclear submarines. Recently,tly Thales has strengthened its position by investing heavily in artificial intelligence-driven sonar processing technologies that enhance target classification in complex shallow water environments. Their strategic focus involves developing next-generation towed array systems and variable-depth sonars to ensure dominance in deep water anti-submarine warfare. The firm actively collaborates with European governments and NATO allies to enhance interoperability and standardize underwater sensor architectures. Continuous innovation in digital beamforming and acoustic signal analysis allows Thales to maintain its leadership in safeguarding maritime assets. This commitment to cutting-edge research and robust manufacturing capabilities secures their role as a critical partner for modern navies seeking comprehensive undersea awareness.

- Leonardo S.p.A. operates as a leading European aerospace and defense giant specializing in sophisticated sonar systems for rotary wing platforms, surface ships,s and unmanned underwater vehicles. The company plays a vital role in the global market by supplying hull-mounted and dipping sonars that are renowned for their reliability and performance in harsh maritime conditions. Recent actions to strengthen its market position include the launch of new compact sonar suites designed specifically for next-generation corvettes and offshore patrol vessels. Leonardo has expanded its research facilities to accelerate the development of quantum sensing technologies and advanced acoustic countermeasures. Their focus on creating modular and scalable solutions allows customers to upgrade existing fleets with minimal downtime and cost. The firm prioritizes international partnerships to integrate its sonar equipment into multinational naval programs. By leveraging deep expertise in transducer materials and signal processing, Leonardo ensures its products remain at the forefront of underwater detection. This strategic emphasis on innovation and customer-tailored solutions solidifies their reputation as a top-tier provider in the industry.

- Kongsberg Gruppen serves as a powerhouse in the maritime technology sector, offering comprehensive sonar portfolios that encompass high-resolution mapping, mine hunting,g and anti-submarine warfare systems. The company contributes extensively to the global market by delivering state-of-the-art synthetic aperture sonars and multibeam echosounders for both military and commercial applications. To strengthen its market position, Kongsberg recently unveiled advanced autonomous underwater vehicles equipped with integrated sonar payloads for persistent seabed monitoring. They have secured major contracts to equip future naval fleets with next-generation flank array sonars and cyber-hardened communication links. The group actively invests in machine learning driven decision support tools that enhance operator situational awareness and reaction times during critical underwater engagements. Kongsberg focuses on fostering a resilient supply chain within Europe to ensure uninterrupted production of critical acoustic components. Their dedication to open system standards facilitates seamless integration with allied platforms and future upgrades. This holistic approach to maritime innovation and strategic autonomy enables Kongsberg to maintain its status as a key enabler of underwater security and exploration worldwide.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the European sonar market primarily focus on research and development investments to pioneer artificial intelligence-driven acoustic processing and cognitive sonar capabilities. Manufacturers actively pursue strategic partnerships with government agencies and prime contractors to secure long term supply contracts for next generation naval vessel programs. Companies are increasingly adopting modular open system architectures to allow for rapid software updates and hardware upgrades without extensive platform modifications. Another major strategy involves expanding production capacities and diversifying supply chains within Europe to mitigate geopolitical risks and ensure regulatory compliance. Firms also prioritize international collaborations to enhance interoperability among allied forces and access broader export markets for underwater warfare systems. Additionally, vendors are developing specialized solutions for unmanned underwater vehicles to address the growing demand for autonomous seabed mapping and mine countermeasures. These combined approaches enable market participants to navigate complex regulatory environments and capture growth opportunities in a rapidly evolving defense landscape.

MARKET SEGMENTATION

This research report on the European sonar market is segmented and sub-segmented into the following categories.

By Product Type

- Hull-Mounted Sonar

- Towed Array Sonar

- Variable Depth / Deployable Sonar

- Sonobuoys

By Application

- Defense

- Commercial

By Solution

- Hardware

- Software

By End User

- Line Fit (New Installations)

- Retrofit / Upgrade

By Country

- United Kingdom

- France

- Germany

- Italy

- Spain

- Netherlands

- Sweden

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com