Europe Theme Park Market Size, Share, Trends & Growth Forecast Report By Type, Ride, Age Group, Revenue Source, and By Country (France, Spain, United Kingdom, Germany, Italy & Rest of Europe) – Industry Analysis and Forecast, 2025 to 2033

Europe Theme Park Market Size

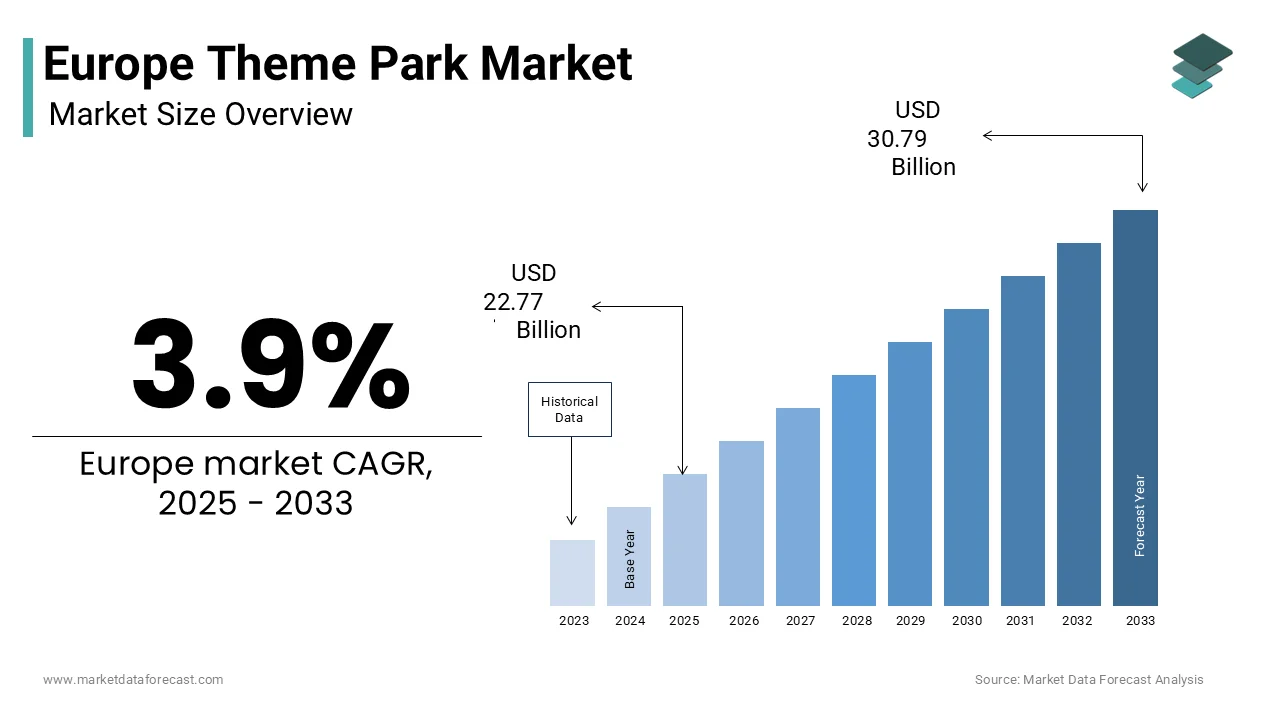

The europe theme park market was valued at USD 21.92 billion in 2024, is expected to reach USD 22.77 billion in 2025, and is growing at a CAGR of 3.9% from 2025 to 2033, and is projected to reach USD 30.79 billion by 2033.

The theme park is are fixed location entertainment complex offering immersive rides, themed environments, live performances, and interactive attractions designed to deliver narrative-driven guest experiences. As per the European Travel Commission, over 78% of international leisure visitors to Europe in 2024 included at least one paid attraction in their itinerary, reflecting the sector’s role in destination competitiveness. Regulatory frameworks such as the EU Accessibility Act mandate inclusive design, ensuring rides and facilities accommodate guests with disabilities, thereby broadening participation. Furthermore, climate resilience planning under the European Green Deal is influencing park infrastructure investments, particularly in Southern Europe, where heat stress mitigation has become integral to guest safety and operational continuity.

MAREKT DRIVERS

Rising Domestic and Inbound Leisure Tourism Post-Pandemic Recovery

Europe’s theme park sector benefits from a sustained rebound in both domestic and international leisure travel, driven by pent-up demand and flexible work arrangements. The rising domestic and inbound leisure tourism post-pandemic recovery is prompting the growth of the European theme park market. As per Eurostat, overnight stays in tourist accommodation across the EU reached 3 8 billion in 2024, surpassing 2019 levels by 12% with family-oriented destinations showing the strongest recovery. Theme parks located near major urban centres such as Disneyland Paris, PortAventura in Spain and Europa Park in Germany recorded visitor numbers exceeding pre-pandemic peaks by 8 to 15%, according to national tourism observatories. The rise of “workation” culture, where employees combine remote work with extended leisure, has extended average stay durations, with families spending 42 days on average at park adjacent resorts compared to 28 days in 2019, as per sources.

Integration of Intellectual Property and Immersive Storytelling

European theme parks are increasingly leveraging globally recognised intellectual property and localised cultural narratives to create emotionally resonant experiences that command premium pricing and drive repeat visitation. The integration of intellectual property and immersive storytelling is additionally fuelling the growth of the European theme park market. As per the International Association of Amusement Parks and Attractions, parks featuring licensed cinematic or animated franchises are spending more than non-themed counterparts due to merchandise and food and beverage synergies. Simultaneously, regional parks are drawing on folklore and historical epics, such as Puy du Fou in France, which stages nightly historical spectacles based on Gallic and medieval narratives, attracting over 2 million visitors annually, as per a recent study. This shift from mechanical thrill to story-driven engagement aligns with European consumer preferences for experiential authenticity over pure adrenaline.

MARKET RESTRAINTS

Stringent Environmental and Land Use Regulations

The growing concern from environmental protection laws and restrictive land zoning policies that limit development in ecologically sensitive or peri-urban areas is one of the major factors restraining the growth of the European theme park. As per the European Environment Agency, proposed park expansions encountered delays or rejections due to non-compliance with the EU Habitats Directive, which protects species and Natura 2000 sites. In Germany, for instance, the 2022 rejection of a major roller coaster project near Leipzig was based on potential disturbance to the endangered Bechstein’s bat population. Additionally, the EU Energy Efficiency Directive mandates that all new large leisure facilities achieve nearly zero energy building standard, requiring costly investments in geothermal heating, photovoltaic canopies and rainwater harvesting. The cost of environmental impact assessments alone extends planning timelines by 18 to 30 months. These regulatory hurdles disproportionately affect independent parks lacking the legal and financial resources of multinational operators, thereby stifling innovation and market diversification.

High Operational Costs and Seasonal Revenue Volatility

The park with elevated fixed costs and pronounced seasonality that pressure profitability, particularly outside peak summer months, is restricting the growth of the European theme park market. As per the European Central Bank, average commercial electricity prices for large leisure venues in the EU exceeded 230 euros per megawatt hour in 2024, up 40% from 2021 levels due to energy market volatility. Labour costs further compound this burden, with the European Foundation for the Improvement of Living and Working Conditions reporting that theme parks employ over 60% of staff on seasonal contracts yet remain liable for health and safety training and social security contributions year-round. Attendance concentration is extreme, over 65% of annual visitors arrive between June and August, according to national tourism boards by forcing parks to maintain full staffing and maintenance readiness during low demand periods. Smaller operators like Belgium’s Bellewaerde report that off-season revenue covers operational expenses, necessitating aggressive discounting or closure.

MARKET OPPORTUNITIES

Development of Year-Round Indoor and Themed Entertainment Districts

Europe is witnessing a strategic pivot toward climate-controlled indoor attractions and mixed-use entertainment districts that mitigate seasonal fluctuations and urban space constraints. The development of year-round indoor and themed entertainment districts is creating new opportunities for the growth of the European theme park market. As per the European Construction Sector Observatory, over major indoor theme parks or family entertainment centres opened across Europe in 2024 alone, including Legoland Discovery Centre expansions in Milan and Stockholm. These venues leverage existing retail and transport infrastructure, occupying repurposed warehouses or mall spaces with footprints under 10,000 square meters. The new retail developments now allocate space for experiential tenants with minimum 10-year lease commitments, providing stable occupancy for operators. Furthermore, cities like Lyon and Rotterdam have adopted “leisure zoning” policies offering tax incentives for developments that combine hotels, dining, and attractions within walkable districts. This urban integration model transforms theme parks from standalone destinations into embedded lifestyle components supporting consistent visitation regardless of weather or season.

Adoption of Advanced Digital Ticketing and Dynamic Pricing Models

Harnessing data analytics and digital platforms to optimise revenue management and enhance guest flow through personalised pricing and contactless access also promotes new opportunities for the growth of the European theme park market. Disneyland Paris implemented school calendars, weather forecasts, and hotel occupancy, achieving a 12% increase in off-peak attendance. Similarly, PortAventura’s loyalty app offers personalised discounts on fast passes and dining based on past behaviour, lifting secondary spend by 19%. The General Data Protection Regulation-compliant data frameworks developed with local supervisory authorities ensure transparency while enabling granular segmentation.

MARKET CHALLENGES

Labour Shortages in Skilled Technical and Hospitality Roles

The acute staffing gaps in specialised roles essential for safety, guest service, and ride maintenance are due to demographic shifts and competition from other sectors. As per the European Labour Authority, over 40% of technical positions, such as ride mechanics, automation technicians and pyrotechnic operators, remain unfilled across Southern and Central Europe owing to a lack of vocational training pipelines. The hospitality segment is equally strained, with Eurofound reporting that 68% of seasonal park staff in France, Spain and Italy are recruited from non-EU countries, facing visa processing delays and housing shortages. Turnover rates exceed 50% annually in entry-level roles according to the European Federation of Trade Unions in Tourism, reducing service consistency and increasing training costs. The problem is exacerbated by the EU Blue Card Directive’s exclusion of seasonal entertainment work from skilled migration categories.

Geopolitical and Macroeconomic Sensitivity to Discretionary Spending

The highly vulnerable to economic downturns, energy price spikes,s, and geopolitical instability that suppress discretionary leisure expenditure is another factor hampering the growth of the European theme park market. Theme park visitation is among the first leisure categories families cut with a decline in out-of-home entertainment spending during periods of real wage contraction. Additionally, geopolitical tensions such as the Red Sea shipping disruptions in 2024 reduced long-haul tourism from Asia, directly impacting parks reliant on international guests like Disneyland Paris. Unlike essential services, theme parks lack pricing power during downturns and cannot easily defer maintenance without compromising safety.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Type, Ride, Age Group, Revenue Source and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Walt Disney Company, Merlin Entertainments Ltd., Europa-Park GmbH & Co., Mack KG, Parques Reunidos, Compagnie des Alpes, LEGOLAND Parks (Merlin Entertainments), Gardaland Resort, Puy du Fou, PortAventura World, Phantasialand, Efteling B.V., Alton Towers Resort (Merlin Entertainments), Tivoli Gardens, Warner Bros. Discovery (Parque Warner Madrid), Gröna Lund Tivoli, Movieland Park, Futuroscope, Liseberg AB, Tripsdrill Theme Park, Dreamland Margate |

SEGMENTAL ANALYSIS

By Type Insights

The theme parks segment accounted in holding 46.3% of the European theme park market share in 2024 due to their ability to function as multi-day destination resorts combining immersive storytelling with high-capacity infrastructure. The integration of cinematic intellectual property enables premium pricing, with average ticket revenue per guest exceeding 85 euros compared to 42 euros at non-themed parks. Furthermore, EU consumer protection laws governing package travel ensure bundled ticket and hotel offerings are transparently marketed, enhancing trust and conversion. This combination of narrativh, commercial scalability, and regulatory support solidifies theme parks as the cornerstone of Europe’s paid attraction ecosystem.

The adventure parks segment is growing at a fast CAGR of 9.3% from 2025 to 2033, owing to the rising demand for active outdoor experiences and alignment with public health initiatives. The European Commission’s HealthyLifestyle 2030 program has allocated funds to promote physical recreation in natural settings, with adventure parks qualifying for municipal grants when located in protected forest or mountain zones. These parks appeal to eco-conscious families seeking screen-free engagement with average dwell times of 35 hours compared to 21 hours at traditional amusement venues. France’s AccroBranch network alone added 28 new locations in 2024, leveraging partnerships with national park authorities.

By Ride Insights

The Mechanical Rides segment held a dominant share of the European theme park market in 2024. Mechanical rides are engineering advancements that reconcile high-intensity experiences with rigorous EU safety protocols. Companies like Mack Rides in Germany and Vekoma in the Netherlands deploy real-time sensor networks that monitor stress vibrations and wind loads, enabling predictive maintenance and minimising downtime. The European Agency for Safety and Health at Work reports that mechanical ride incident rates have declined due to standardised operator training and automated restraint verification. Additionally, the integration of virtual reality overlays on coasters, such as Europa Park’s VR Europa Jet, extends ride lifespans without major capital outlay. This fusion of safety, reliability, ty and experiential novelty ensures mechanical rides remain the core attraction in both legacy and new parks.

The water rides segment is likely to grow at the fastest CAGR of 8.7% from 2025 to 2033, driven by climate adaptation strategies and family-oriented signs. Furthermore, EU water reuse regulations under the Urban Wastewater Treatment Directive permit closed-loop filtration systems that recycle over 95% of water by addressing historical sustainability concerns. The modern wave pools and raft rides are controlled through smart flow control. This operational efficiency, combined with broad age appeal, positions water rides as a climate-resilient growth vector.

By Age Group Insights

The Up to 18 years segment accounted in holding 38.3% of the Europe theme park market share in 2024 due to Europe’s strong culture of family-centric leisure and school-linked excursion policies. As per the European Commission’s Education and Youth Portal, EU member states mandate at least two curriculum-aligned field trips per academic year, with theme parks featuring heavily in science and history programs. Additionally, EU parental leave policies in countries like Sweden and Germany enable extended summer stay, with 63% of families visiting parks during July and August. Parks design dedicated children’s land with sensory-inclusive certified under the European Accessibility Act, ensuring participation for neurodiverse guests. This institutional and cultural integration ensures sustained demand from the youngest demographic as both entertainment and pedagogical destinations.

The 19 to 35 age group segment is likely to grow the fastest CAGR of 10.1% from 2025 to 2033 du,e to experiential consumption trends and digital social validation. Many millennials and Gen Z respondents prioritise “unique experiences” over material purchases, with theme parks ranking third after concerts and travel. Parks respond with after-dark events like Thorpe Park’s Fright Nights and Efteling’s Night of Lights, which blend immersive storytelling with adult-oriented dining and music that attracts attendance. Social media integration is a new attraction designed for photo and video sharing, including augmented reality filters and interactive queue zones.

By Revenue Source Insights

The tickets segment was the largest by occupying 42.3% of the European theme park market share in 2024 due to its role in capacity control and guest segmentation. As per the European Consumer Organisation, major parks now use dynamic pricing algorithms that adjust daily rates based on weather, school holidays and competitor availability, increasing revenue. Advance online booking mandates undepost-pandemic health protocols have enabled precise forecasting with Disneyland Paris pre-booked attendance, allowing optimised staffing and inventory. Furthermore, EU consumer law requires transparent refund policies for weather cancellations, which builds trust and encourages early purchase. The integration of tickets with national rail passes, such as the Eurail Global Pas, further expands access while guaranteeing baseline visitation.

The food and beverage segment is growing at a CAGR of 9.6% from 2025 to 2033, driven by culinary storytelling, premiumization and local sourcing mandates. Themed dining experiences like the Three Broomsticks at Warner Bros Studio Tour London have higher check averages than generic fast food outlets. Additionally, EU nutrition labelling rules require clear allergen and calorie disclosure, enabling parks to offer tailored wellness menus that appeal to health-conscious families.

COUNTRY LEVEL ANALYSIS

France Theme Park Market Analysis

France was the top performer of the European theme park market, holding 28.3% of the share in 2024, with Disneyland Pari, which alone accounts for over 40% of the country’s paid attraction revenue. France’s “Pass Culture” initiative now includes theme park vouchers for minors, enhancing domestic accessibility. Stringent national safety standards under the Direction Générale de la Concurrence align with EU norms while allowing faster permit approvals for IIP-based attractions.

Spain Theme Park Market Analysis

Spain's theme park market growth is likely to grow with its year-round sunshine and coastal tourism infrastructure. PortAventura World near Barcelona welcomed 58 million guests in 202,4, includin12 2 million to its Ferrari Land and Caribe Aquatic Park zone, as per its sustainability report. Aggressive investment in water attractions addresses summer heat with over 90% of new rides since 20,22, incorporating misting shade or cooling tunnels compliant with the national Heatwave Action Plan. Regional governments offer tax credits for parks achieving ISO 14001 environmental certification, accelerating sustainability upgrades. Spain’s blend of cultural theming, Mediterranean climate, and transport connectivity solidifies its role as Southern Europe’s entertainment capital.

United Kingdom Theme Park Market Analysis

The United Kingdom theme park market growth is likely to be driven by the intellectual property-based attractions. Alton Towers and Thorpe Park continuously refresh with IP-licensed dark rides and seasonal horror events targeting young adults. Post-Brexit regulatory autonomy enabled faster approval of new ride technologies such as motion simulators with haptic feedback.

Germany Theme Park Market Analysis

Germany's theme park market growth is likely to grow with the high density of mid-sized parks and engineering prowess. Over 300 regional parks operate across Bavaria and Baden-Württemberg, often integrated with holiday villages and wellness centres. The domestic leisure trips include a park visit with strong repeat rates due to annual pass models. German manufacturers like Mack Rides supply 60% of Europe’s high-end coasters by enabling rapid in-house innovation. Strict national noise and emissions regulations under the Bundesimmissionsschutzgesetz ensure parks coexist with rural communities. This ecosystem of local access engineering integration and regulatory compliance sustains consistent demand.

Italy Theme Park Market Analysis

Italy's theme park market growth is likely to grow with the blend of historical narratives with family recreation. Gardaland on Lake Garda welcomed 32 million guests in 2024 with expansions themed around Italian folklore and Roman mythology as per its annual report. The Italian National Institute of Statistics notes that 58% of Italian families take at least one park trip annually, often combining it with cultural heritage visits. Parks like Mirabilandia integrate rides with live shows featuring commedia dell’arte and opera excerpts appealing to multigenerational groups. The Ministry of Cultural Heritage supports “edutainment” models where attractions align with national identity.

COMPETITIVE LANDSCAPE

The European theme park market features a dual structure comprising a few global-scale destination resorts and a dense network of regional, family-owned parks. Competition among major players centres on intellectual property exclusivity, ride innovation and guest experience personalisation rather than price. Disneyland Paris, Europa Park, and PortAventura dominate through integrated resort models that capture spending across tickets, food, lodging and merchandise. Meanwhile, smaller parks differentiate via local culture adventure formats or educational content, often supported by municipal tourism funds. The entry barrier is high due to land use regulations, capital intensity and safety certification requirements, yet digitalisation enables niche operators to compete through targeted marketing and agile programming. Regulatory compliance with EU accessibility, environmental, and consumer protection laws is non-negotiable and shapes investment priorities.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global European theme park market include

- Walt Disney Company

- Merlin Entertainments Ltd.

- Europa-Park GmbH & Co Mack KG

- Parques Reunidos

- Compagnie des Alpes

- LEGOLAND Parks (part of Merlin Entertainments)

- Gardaland Resort

- Puy du Fou

- PortAventura World

- Phantasialand

- Efteling B.V.

- Alton Towers Resort (Merlin Entertainments)

- Tivoli Gardens

- Warner Bros. Discovery (Parque Warner Madrid)

- Gröna Lund Tivoli

- Movieland Park

- Futuroscope

- Liseberg AB

- Tripsdrill Theme Park

- Dreamland Margate

TOP LEADING PLAYERS IN THE MARKET

- Disneyland Paris is Europe’s premier themed entertainment destination operated by The Walt Disney Company through a European subsidiary. It serves as the continent’s flagship for immersive storytelling, combining globally recognised intellectual property with localised cultural elements. The resort includes two parks, seven themed hotels, and a shopping district, attracting guests from over 120 countries. Recently, Disneyland Paris completed its multi-year transformation plan with the opening of Avengers Campus and enhancements to sustainability infrastructure, including a 37,000 square meter solar canopy. The company also launched dynamic pricing and a mobile app with real-time queue updates to improve guest flow. Its investment in European talent through local casting and culinary partnerships reinforces its integration into the regional leisure ecosystem while maintaining global brand consistency.

- Europa Park is Germany’s largest theme park and a family-owned enterprise renowned for its innovative ride engineering and cultural theming representing 16 European countries. It operates over 100 attractions and 18 themed hotels, making it a year-round destination. Europa Park contributes to the global market through its Mack Rides division, which designs and exports roller coasters and dark rides to parks worldwide. The company recently expanded its Rulantica water park and introduced virtual reality enhancements on classic rides to extend appeal across age groups. It also launched a comprehensive carbon neutrality program targeting zero emissions by 2030 with investments in geothermal heating and electric shuttle fleets.

- PortAventura World is a leading resort in Southern Europe located near Barcelona and jointly owned by Investindustrial and Chimelong Group. It encompasses PortAventura P, Ark Ferrari Land, and Caribe Aquatic Park alongside six themed hotels. The resort leverages Spain’s climate and tourism infrastructure to attract both European and international visitors. Recently, PortAventura introduced new intellectual property-based zones, including a Star Trek-themed area and expanded its sustainable practices by achieving 95% water recycling in its aquatic attractions. It also partnered with local universities to develop heat stress mitigation protocols for summer operations. The resort’s strategy focuses on premium experiential offerings such as VIP guided tours and gastronomic events, aligning with EU wellness and sustainability trends while strengthening its position as a Mediterranean entertainment hub.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European theme park market are investing in intellectual property-driven attractions to enhance emotional engagement and command premium pricing. They are adopting dynamic pricing and digital ticketing platforms to optimise attendance flow and maximise revenue per guest. Companies are expanding into year-round operations through indoor attractions, water parks, and themed hotels to mitigate seasonality. They are integrating sustainability measures such as renewable energy, water recycling, and local sourcing to comply with EU environmental regulations and appeal to conscious consumers. Additionally, they are developing after-dark and seasonal events to attract young adult demographics and extend dwell time beyond daytime visits.

MARKET SEGMENTATION

This research report on the europe theme park market is segmented and sub-segmented into the following categories.

By Type

- Theme Parks

- Adventure Parks

By Ride

- Mechanical Rides

- Water Rides

By Age Group

- Up to 18 Years

- 19 to 35 Years

By Revenue Source

- Tickets

- Food & Beverages

By Country

- France

- Spain

- United Kingdom

- Germany

- Italy

- Rest of Europe

Frequently Asked Questions

1. What are the main growth drivers for the Europe Theme Park Market?

The Europe Theme Park Market is driven by experiential tourism, rising disposable incomes, transport connectivity, and the integration of branded IP.

digital technologies, and resort facilities that increase visitor frequency, length of stay, and overall spending across the region.

2. Which countries lead the Europe Theme Park Market?

Germany, France, Spain, and the U.K. lead the Europe Theme Park Market due to established flagship parks, strong domestic and inbound tourism,

robust infrastructure, and sustained investment in new rides, themed lands, and accommodation that reinforce their regional dominance.

3. What are the key trends shaping the Europe Theme Park Market?

Key trends in the Europe Theme Park Market include resort-style multi-park destinations, eco-friendly concepts, VR-enhanced attractions, and indoor facilities,

along with IP-based storytelling, multi-day packages, and diversification into water parks and family entertainment centers

4. How is technology influencing the Europe Theme Park Market?

The Europe Theme Park Market is leveraging mobile apps, virtual and augmented reality, smart queuing, and advanced safety systems to personalize visits,

reduce friction, and deepen immersion, which helps operators differentiate and capture higher visitor satisfaction and spending.

5. What challenges and restraints affect the Europe Theme Park Market?

The Europe Theme Park Market faces restraints from high capital and operating costs, regulatory and environmental constraints, and competition from digital entertainment,

plus exposure to economic cycles and seasonality that can pressure attendance and returns on large-scale investments

6. Who are the major players in the Europe Theme Park Market?

Major operators in the Europe Theme Park Market include global groups such as Disney and Merlin, and regional leaders like Europa-Park’s operator,

alongside national brands that run theme, water, and adventure parks across Western and emerging Eastern European destinations.

7. How does tourism impact the Europe Theme Park Market?

Tourism is central to the Europe Theme Park Market, with intra-European travel, city breaks, and package holidays feeding park attendance,

while improved air and rail links and bundled resort stays help parks attract international visitors and extend length of stay.

8. What role do water parks and indoor parks play in the Europe Theme Park Market?

Water parks and indoor parks form a fast-growing segment of the Europe Theme Park Market, enabling year-round operation in colder climates,

supporting destination resorts, and diversifying offerings to attract families, short-break tourists, and local repeat visitors.

9. How is sustainability being integrated into the Europe Theme Park Market?

In the Europe Theme Park Market, operators are incorporating energy-efficient systems, waste reduction, and green design,

aligning with sustainable tourism expectations while also modernizing legacy infrastructure and promoting nature- and heritage-based themes.

10. Which visitor segments drive demand in the Europe Theme Park Market?

Families with children, teenagers, and young adults are core segments in the European Theme Park Market,

supported by rising focus on youth-oriented IP, thrill rides, and multi-generational experiences that appeal to both domestic and international tourists.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com