Global Fast Food Market Size, Share, Trends & Growth Forecast Report By Type (Burger/Sandwich, Pizza/Pasta, Chicken & Seafood, Asian/Latin American Food and Others), Distribution Platform (Quick Service Restaurant (QSR), Street Vendors, Food Delivery Services, Online Food Delivery, Others) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis from 2026 to 2034

Global Fast Food Market Summary

The global fast food market size was valued at USD 741.25 billion in 2025 and is projected to reach USD 1,111.10 billion by 2034, growing at a CAGR of 4.6% from 2026 to 2034.

The global fast food market is experiencing steady growth, driven by evolving consumer lifestyles, higher disposable incomes, and the demand for quick, affordable, and accessible food options. With the rise of dine-in, drive-thru, and delivery formats, international chains are expanding their reach, supported by strong franchise networks and innovative menu diversification.

Key Market Trends

- Expansion of online food delivery apps and aggregator platforms.

- Healthier fast food offerings to align with wellness-driven consumer preferences.

- Growth of digital ordering, AI-powered drive-thrus, and automation in QSRs.

- Increasing adoption of plant-based and sustainable menu options.

Segmental Insights

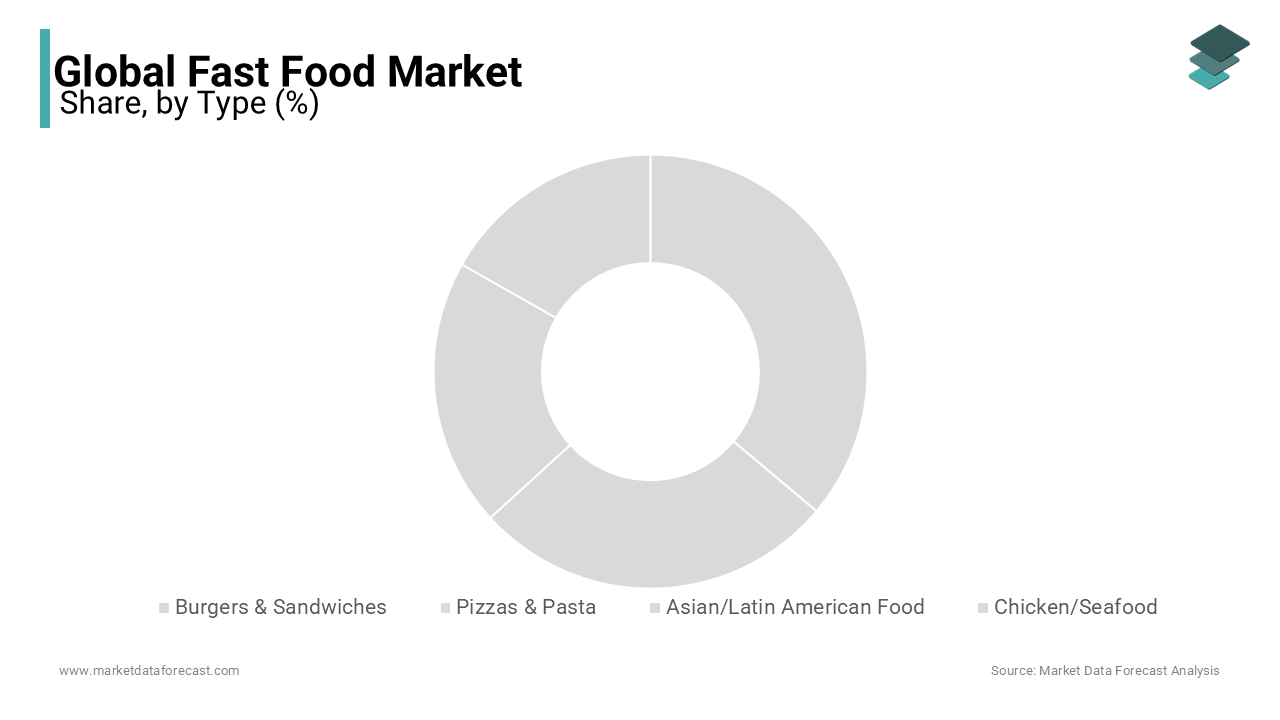

- By Product Type, the burgers and sandwiches segment led the market with 38.1% share in 2025, reflecting their dominance as a global fast food market.

- By Distribution Channel, the Quick Service Restaurants (QSRs) segment dominated with a 49.8% share in 2025, supported by efficiency, affordability, and global accessibility.

Regional Insights

- North America: Remained the largest market, benefiting from established fast food culture and strong franchise operations.

- Europe: Held a substantial share alongside North America, with a high penetration of international brands.

- Asia-Pacific: Poised for promising growth due to rapid urbanization, young demographics, and rising middle-class demand.

- Latin America & Middle East: Expected to witness steady growth with the increasing entry of global QSR chains and expanding delivery platforms.

Competitive Landscape

The global fast food market is highly competitive, with major players including McDonald’s, Burger King, Domino’s Pizza, Yum! Brands, KFC, Wendy’s, Jack in the Box, and Doctor’s Association Inc. These companies are leveraging digital ordering, menu diversification, and international expansion strategies to sustain growth in a competitive environment.

Global Fast Food Market Size

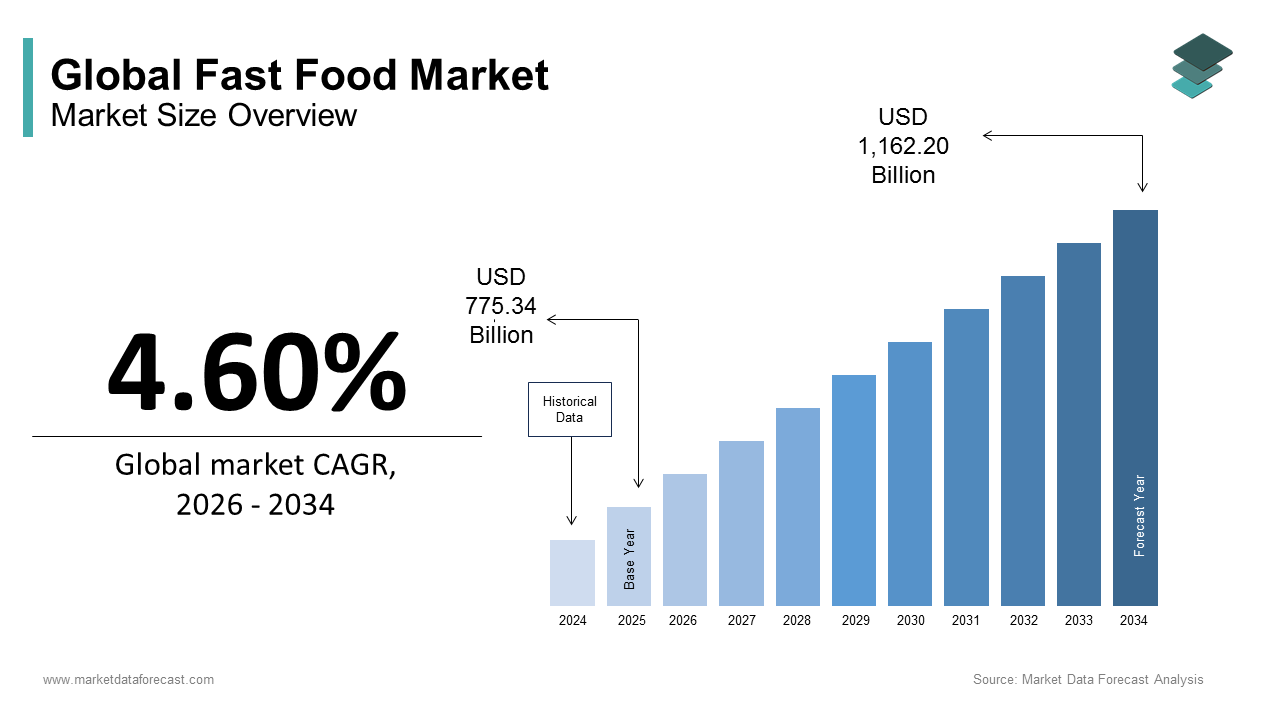

The global fast food market size was calculated to be USD 775.34 billion in 2025 and is anticipated to be worth USD 1,162.20 billion by 2034, from USD 811.01 billion in 2026, growing at a CAGR of 4.60% during the forecast period

The fast food is a rapidly cooked meals under time-efficient service models. Characterized by high turnover, limited table service, and emphasis on convenience, this sector has evolved beyond traditional burgers and fries to include globally inspired cuisines, plant-based alternatives, and digitally integrated ordering systems. As per the U.S. Bureau of Labor Statistics, the average American spends 37 minutes per day on meal preparation at home, a decline of nearly 25% since 2000, reflecting a structural shift toward outsourced eating. According to the World Health Organization, urban populations now constitute 56% of the global total, with city dwellers exhibiting a 40% higher frequency of fast food consumption compared to rural counterparts due to compressed schedules and proximity to outlets.

MARKET DRIVERS

Urbanization and the Rise of Time-Constrained Consumer Lifestyles

The accelerating pace of urban life with dietary behaviors is driving the growth of the fast food market. As per the United Nations Department of Economic and Social Affairs, over 2.5 billion people are projected to be added to urban populations by 2050, primarily in Asia and Africa, where infrastructure and long commutes amplify time poverty. In cities like Jakarta and Lagos, average daily commute times exceed 90 minutes, as reported by the International Transport Forum, leaving minimal bandwidth for meal preparation. This temporal pressure drives reliance on rapid dining solutions, with fast food outlets strategically located near transit hubs and business districts.

Digital Transformation and the Expansion of Delivery Ecosystems

The proliferation of digital platforms has redefined fast food accessibility, transforming it from a location-bound service to an on-demand utility is additionally enhancing the growth of fast food market. Advanced logistics, including AI-driven route optimization and dark kitchen networks, have reduced delivery times to under 30 minutes in major metropolitan areas. In Dubai, the government’s Smart City initiative has facilitated drone-based food delivery trials, further accelerating service efficiency. These technological advancements have expanded the consumer base to include elderly populations and stay-at-home individuals who previously relied on home-cooked meals.

MAJOR RESTRAINTS

Escalating Regulatory Pressure on Nutritional Transparency and Health Impacts

The rising public health crises, particularly obesity and type 2 diabetes and growing awareness over the nutritional health is ascribed to restrain the growth of fast food market. According to the World Health Organization, global obesity rates have nearly tripled since 1975, with over 650 million adults classified as obese in 2022. Similarly, the UK’s sugar levy led to a 22% reduction in sugar content across soft drinks served in fast food outlets between 2018 and 2022, according to Public Health England. These regulations increase operational complexity and constrain menu innovation, compelling chains to reformulate recipes a process that risks altering taste profiles and alienating core customer segments.

Volatility in Supply Chain and Ingredient Sourcing Due to Climate and Geopolitical Factors

The fast food industry’s reliance on a narrow set of agricultural commodities makes it highly susceptible to disruptions in global supply chains. As per the Food and Agriculture Organization of the United Nations, extreme weather events linked to climate change reduced global wheat yields by 5.7% in 2022, directly impacting bun and pastry costs for major chains. McDonald’s disclosed in its 2023 sustainability report that ingredient price volatility contributed to a 12% increase in food procurement expenses year-on-year. These fluctuations strain profit margins and limit pricing flexibility, particularly in price-sensitive markets where consumers resist menu inflation.

MARKET OPPORTUNITIES

Integration of Plant-Based and Alternative Protein Offerings

The launch of plant-based and lab-grown alternatives is gaining traction among environmentally and health-conscious consumers, which is boosting the growth of fast food market. According to the Good Food Institute, global sales of plant-based meat reached $9.7 billion in 2023, with fast food chains serving as primary distribution channels. The environmental imperative is also driving adoption: a University of Oxford study found that producing a plant-based burger generates 90% less greenhouse gas than its beef counterpart.

Expansion into Emerging Markets with Rising Middle-Class Consumption

The operators are targeting emerging economies such as urbanization, income growth, and youth demographics, which is to incline the growth of fast food market. According to the World Bank, the global middle class is projected to reach 3.2 billion by 2030, with 88% of growth originating in Asia, Africa, and Latin America. Indonesia’s fast food market grew by 11% annually between 2020 and 2023, driven by rising disposable incomes and the proliferation of food courts in shopping malls, according to the Central Bureau of Statistics of Indonesia. McDonald’s opened its first store in Ghana in 2023, signaling strategic entry into West Africa.

MARKET CHALLENGES

Labor Shortages and Rising Wage Pressures in Key Operating Regions

The rising labor constraints in developed economies where workforce participation remains below pre-pandemic levels is impacting negatively on the growth of fast food market. According to the U.S. Bureau of Labor Statistics, the leisure and hospitality sector, which includes fast food, had 780,000 unfilled positions in 2023, despite offering average hourly wages of $15.80—a 23% increase since 2019. These pressures are prompting automation investments, such as self-order kiosks and robotic fry stations, but implementation is uneven and often met with resistance in regions where human interaction remains a service expectation, complicating operational scalability.

Consumer interest toward sustainability claims and greenwashing allegations

The trend towards eco-friendly initiatives, where there are lack of greenwashing systems and other sustainability claims are likely to degrade the growth of the fast food market. McDonald’s faced regulatory scrutiny in France for labeling packaging as “eco-designed” without substantiating lifecycle reductions, as reported by the Directorate General for Competition, Consumer Affairs, and Fraud Control. The production of paper straws and biodegradable containers that often marketed as sustainable, has been found to require 30% more energy and water than plastic alternatives, according to a University of Plymouth study.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.60% |

| Segments Covered | By Type, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | McDonald’s Corporation (U.S.), Burger King Worldwide, Inc. (U.S.), Domino’s Pizza Inc. (U.S.), Wendy’s, Yum! Brands Inc. (U.S.), Jack in the Box Inc. (U.S.), KFC, Wendy’s International Inc. (U.S.) and Doctor’s Association Inc. (U.S.). |

SEGMENTAL INSIGHTS

By Type Insights

The Burger/Sandwich segment dominated the global fast food market by capturing 38.3% of share in 2025 with the entrenched cultural presence of hamburger chains and the universal appeal of customizable, portable meals.

McDonald’s alone operates over 40,000 outlets globally, serving an estimated 68 million customers daily, according to the company’s 2023 Global Impact Report. Furthermore, as per the U.S. Department of Agriculture, beef consumption in the U.S. reached 62 pounds per capita in 2023, supporting sustained demand for burger-centric offerings. The sandwich sub-segment also benefits from health-conscious innovation, with Subway and similar chains introducing whole-grain bread and lean protein options, appealing to fitness-oriented consumers.

The Asian/Latin American Food segment is likely to register a CAGR of 10.6% in the coming years with the rising consumer demand for authentic, diverse, and spice-forward cuisines, particularly among younger demographics. As per the Pew Research Center, Millennials and Gen Z constitute over 50% of fast food consumers in North America and Western Europe, with 68% expressing a preference for ethnic flavors in their meals. Chains like Cava, Chipotle, and Panda Express have successfully scaled regionally inspired menus while maintaining operational efficiency. Additionally, the popularity of Korean, Thai, and Peruvian street food has surged, with Google Trends data showing a 200% increase in searches for “Korean BBQ burrito” and “Peruvian chicken bowl” since 2021.

By Distribution Platform Insights

The Quick Service Restaurant (QSR) segment held 42.3% of the fast food market share in 2025 with the standardized, scalable, and brand-driven nature of QSRs, which offer consistent quality, recognizable menus, and integrated service models.

McDonald’s, Starbucks, and KFC collectively operate over 150,000 locations worldwide, as reported by QSR Magazine, enabling unparalleled geographic penetration. The integration of digital kiosks, loyalty apps, and mobile ordering has enhanced customer retention, with 58% of U.S. consumers using branded apps for faster service, as per the National Restaurant Association. Moreover, QSRs benefit from economies of scale in procurement and marketing by allowing them to sustain aggressive pricing strategies and promotional campaigns that smaller vendors cannot match.

The Online Food Delivery segment is likely to register a CAGR of 13.8% from 2025 to 2033 with the emergence of smartphone ubiquity, digital payment adoption, and evolving urban lifestyles. As per the International Telecommunication Union, over 6.8 billion people now use mobile internet, enabling seamless access to delivery platforms. Additionally, AI-powered logistics, such as dynamic pricing and route optimization, have reduced delivery times to under 25 minutes in cities like Seoul and Dubai. These efficiencies, combined with subscription models like Uber Eats Pass, are transforming online delivery into a habitual, rather than occasional, dining mode.

REGIONAL ANALYSIS

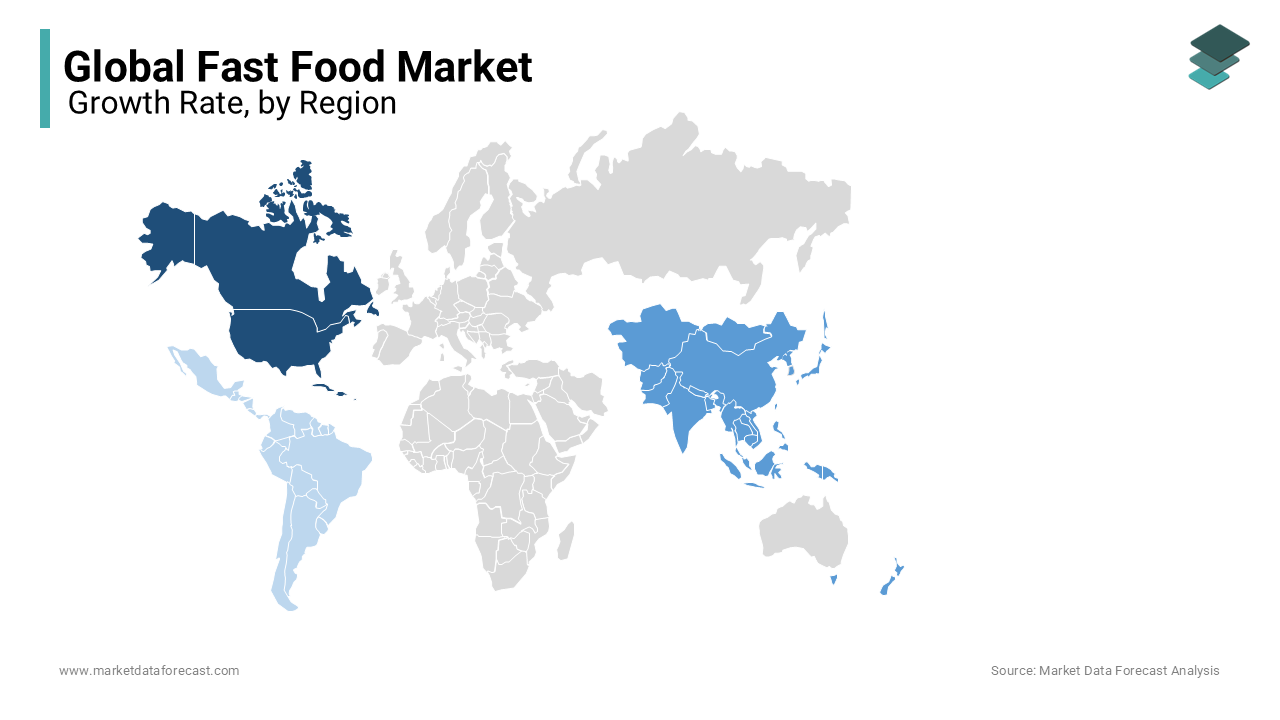

North America was the top performer in the global fast food market with 35.3% of share in 2025, where fast food is deeply embedded in consumer culture and daily routines.

Americans spend an average of $1,200 annually on fast food, as per the U.S. Bureau of Labor Statistics. The country hosts the world’s largest QSR chains, including McDonald’s, Subway, and Chick-fil-A, which collectively operate over 200,000 outlets. Canada complements this landscape with strong penetration of global brands and a growing preference for premium fast-casual dining. The integration of digital drive-thrus, AI-based menu boards, and voice ordering pioneered by companies like Domino’s and Starbucks has set technological benchmarks globally

Europe was the second largest by holding 27.3% of fast food market share in 2025.

Western European countries like the UK, Germany, and France exhibit high fast food penetration, with the average consumer visiting a QSR 18 times per year, as per the European Food Service Report by IRI. However, consumer behavior is increasingly shaped by regulatory and sustainability concerns. The UK’s sugar tax led to a 22% reduction in sugar content in soft drinks served by major chains between 2018 and 2022, according to Public Health England. Eastern Europe, particularly Poland and Romania, is witnessing rapid expansion due to rising disposable incomes and urbanization.

Asia Pacific fast food market growth is swiftly growing with a significant CAGR during the forecast period.

China and India are the major contributors with the presence of huge urban middle class, now exceeding 400 million people, drives demand for Western-style chains and localized adaptations like KFC’s congee and Peking duck. Street food remains a dominant force, with over 10 million vendors operating in India alone, according to the Ministry of Housing and Urban Affairs.

Latin America fast food market is likely to have steady growth opportunities in the next coming years with the local flavors and informal economies.

However, formal QSRs are gaining ground, with McDonald’s operating over 3,000 outlets across Latin America, according to company data. Mexico’s proximity to the U.S. has facilitated the adoption of drive-thru models and digital ordering, with 45% of fast food transactions now occurring via mobile apps, according to INEGI.

The Middle East & Africa fast food market growth is likely to grow steadily in the coming years.

The UAE and Saudi Arabia are at the forefront, with Dubai hosting over 5,000 fast food outlets, as per the Dubai Economy and Tourism Department. Vision 2030 initiatives in Saudi Arabia are driving investments in food service infrastructure, including smart kitchens and automated ordering systems. In Africa, Nigeria and South Africa are emerging as key markets, with Nigeria’s fast food sector growing at 10% annually, according to the Nigerian Bureau of Statistics. Urbanization is a key driver: as per the United Nations, Africa’s urban population is expected to double by 2050, increasing demand for convenient dining.

COMPETITION OVERVIEW

The fast food market is driven by intense and multifaceted competition, shaped by brand loyalty, technological innovation, and regional adaptability. Global chains like McDonald’s, KFC, and Domino’s compete not only with one another but also with fast-casual brands, local chains, and digital-native delivery concepts. Differentiation increasingly hinges on speed, digital experience, and cultural relevance rather than price alone. In Asia Pacific, localization of menus and integration with regional payment ecosystems are success factors. The rise of cloud kitchens and ghost brands has lowered entry barriers, enabling agile startups to challenge established players. At the same time, consumer demand for transparency, sustainability, and healthier options forces incumbents to reformulate products and enhance supply chain accountability. The competitive landscape is further complicated by regulatory pressures on nutrition labeling and packaging waste, which is requiring continuous adaptation.

LEADING PLAYERS IN THE FAST FOOD MARKET

McDonald’s Corporation

McDonald’s maintains a dominant presence in the Asia Pacific fast food landscape through a blend of global consistency and hyper-localized menu innovation. In China, it operates over 5,500 restaurants, offering region-specific items such as the Egg Tofu Burger and congee, tailored to local palates, as confirmed by the company’s 2023 Asia Pacific Business Review. The chain has accelerated digital transformation by integrating WeChat and Alipay for seamless ordering and launching delivery partnerships with Meituan and Alibaba’s Ele.me. In India, McDonald’s introduced an entirely vegetarian menu in non-beef regions, catering to religious and cultural preferences. Its commitment to sustainability includes opening LEED-certified outlets in Singapore and Tokyo.

KFC (Yum! Brands)

KFC holds a pioneering position in the Asia Pacific fast food sector, being one of the first Western QSRs to enter China in 1987, where it now operates over 9,000 outlets—the largest market for the brand globally. The company has localized its offerings extensively, introducing rice bowls, spicy Sichuan-style chicken, and mooncakes during festivals, as noted in Yum! Brands’ 2023 Annual Report. In Japan, KFC’s Christmas chicken meal has become a cultural phenomenon, generating 10% of annual sales in a single week. The brand has invested heavily in digital infrastructure, launching AI-driven drive-thrus in South Korea and mobile loyalty programs across Southeast Asia.

Domino’s Pizza

Domino’s has carved a distinct niche in the Asia Pacific market by positioning itself as a technology-driven delivery specialist. The company operates in over 15 countries across the region, with India alone hosting more than 1,800 stores, making it one of its fastest-growing markets, as reported in Domino’s 2023 Global Expansion Update. Its “30-minute delivery or free” promise, though adapted locally, remains a core brand differentiator. In Japan and Australia, Domino’s utilizes GPS tracking and real-time order updates to enhance customer experience. The company launched its proprietary AI-powered pizza quality checker in the Philippines, ensuring consistency across outlets. In 2023, it introduced electric delivery scooters in Vietnam and Indonesia to reduce emissions and navigate traffic efficiently.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the fast food market employ a multifaceted strategic approach to maintain competitive advantage, including digital integration, menu localization, supply chain optimization, sustainability initiatives, and expansion into emerging markets. Companies are investing in proprietary mobile apps, AI-driven drive-thrus, and cloud kitchens to enhance delivery efficiency and customer retention. Menu innovation focuses on regional flavors, plant-based proteins, and health-conscious options to align with evolving consumer preferences. Strategic franchising enables rapid geographic penetration with reduced capital risk. Sustainability efforts include eco-friendly packaging, carbon footprint reduction, and ethical sourcing, often aligned with regulatory demands. Additionally, partnerships with third-party delivery platforms and investment in automation technologies such as robotic kitchens and self-order kiosks are improving operational efficiency and scalability in high-labor-cost environments.

Key Market Players

Companies playing a major role in the global fast food market include McDonald’s Corporation (U.S.), Burger King Worldwide, Inc. (U.S.), Domino’s Pizza Inc. (U.S.), Wendy’s, Yum! Brands Inc. (U.S.), Jack in the Box Inc. (U.S.), KFC, Wendy’s International Inc. (U.S.) and Doctor’s Association Inc. (U.S.).

Fast Food Market Recent News

- In January 2025, McDonald’s launched its first AI-powered drive-thru system in Shanghai, utilizing natural language processing to handle Mandarin dialects and process orders with 95% accuracy, which is significantly reducing wait times and enhancing customer experience in one of its most competitive markets.

- In March 2025, KFC partnered with Singapore-based Next Gen Foods to introduce TiNDLE chicken in select outlets across Singapore and Hong Kong, which is marking a strategic move into the alternative protein space and appealing to environmentally conscious consumers in the Asia Pacific region.

- In August 2023, Domino’s opened its 1,000th store in India, located in Guwahati, Assam by reinforcing its commitment to deep-tier expansion and capturing untapped demand in non-metro cities through localized marketing and delivery infrastructure.

- In May 2025, Starbucks, expanding its fast food adjacency, introduced a savory breakfast bowl menu in Japan and South Korea, developed in collaboration with local chefs, to increase daytime footfall and compete with traditional QSR breakfast offerings.

- In February 2023, Jollibee Foods Corporation acquired 60% stake in Tim Ho Wan, the Michelin-recommended dim sum chain, to diversify its portfolio and strengthen its premium fast-casual presence in China, Hong Kong, and Southeast Asia by leveraging cross-brand synergies and shared logistics.

MARKET SEGMENTATION

This research report on the global fast food market has been segmented and sub-segmented based on type, distribution channel, and region.

By Type

- Burgers & Sandwiches

- Pizzas & Pasta

- Asian/Latin American Food

- Chicken/Seafood

By Distribution Channel

- Quick Service Restaurant (QSR)

- Street Vendors

- Food Delivery Services

- Online Food Delivery

By Region

- North America

- Europe

- The Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What types of food are included in the fast food market?

The market includes b2urgers, pizzas, fried chicken, sandwiches, tacos, wraps, noodles, fries, and beverages offered by quick-service restaurants.

2. What are the main drivers of the fast food market?

Key drivers include busy lifestyles, urbanization, rising disposable incomes, growing preference for convenience foods, and expansion of quick-service restaurant chains.

3. How does digitalization impact the fast food market?

Digital ordering, mobile apps, self-service kiosks, and food delivery platforms improve customer convenience and boost sales for fast food operators.

4. Which regions dominate the global fast food market?

North America dominates the market, followed by Europe and the Asia Pacific, driven by strong brand presence and high consumer demand.

5. What role do delivery services play in the fast food market?

Food delivery services significantly expand market reach, increase order frequency, and support revenue growth for fast food brands.

6. How are consumer preferences changing in the fast food market?

Consumers are increasingly seeking healthier options, plant-based menus, low-calorie meals, and transparency in ingredients.

7. What challenges does the fast food market face?

Key challenges include rising raw material costs, labor shortages, health concerns, and increasing regulatory scrutiny.

8. How is sustainability influencing the fast food market?

Sustainability efforts focus on eco-friendly packaging, reducing food waste, ethical sourcing, and lowering carbon footprints

9. What are the key trends in the fast food market?

Major trends include plant-based fast food, ghost kitchens, menu customization, and technology-driven operations.

10. What is the future outlook for the fast food market?

The fast food market is expected to grow steadily, supported by urban expansion, digital transformation, and evolving consumer tastes.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com