Global Generic Injectables Market Size, Share, Trends & Growth Forecast Report By Therapeutic Area (Oncology, Anesthesia, Anti-Infectives, Parenteral Nutrition and Cardiovascular Diseases), Containers (Vials, Ampoules, Premix and Prefilled Syringes), Distribution Channel and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Global Generic Injectables Market Report Summary

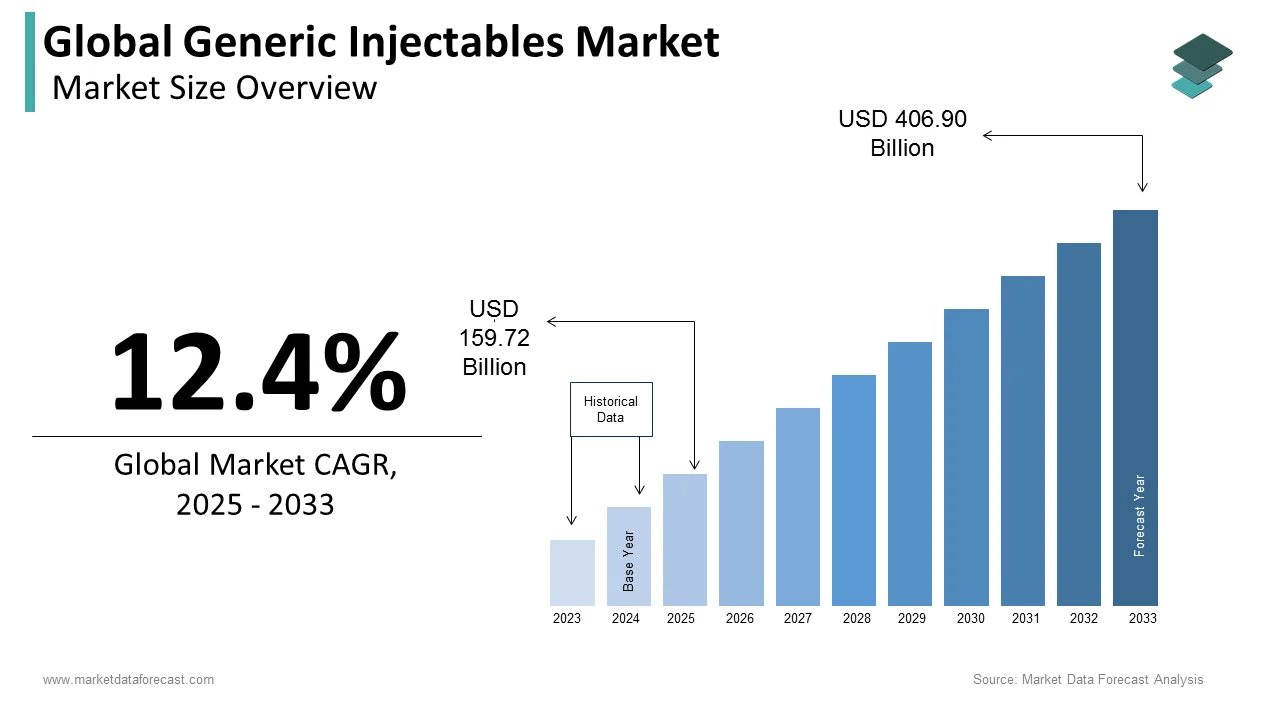

The global generic injectables market was valued at USD 159.72 billion in 2025, is estimated to reach USD 179.53 billion in 2026, and is projected to reach USD 457.36 billion by 2034, growing at a CAGR of 12.4% from 2026 to 2034. Market growth is driven by the rising prevalence of chronic diseases such as cancer and cardiovascular conditions, increasing demand for cost-effective treatment options, and the expiration of patents for branded injectable drugs. The growing focus on biosimilars and complex generics, along with expanding healthcare access in emerging markets, is further accelerating market expansion. Additionally, hospital demand for sterile and ready-to-use injectable formulations is strengthening market growth.

Key Market Trends

- Rising demand for cost-effective generic injectable drugs.

- Increasing prevalence of chronic diseases, especially cancer.

- Expiry of patents for major branded biologics and injectables.

- Growth in biosimilars and complex generics development.

- Expanding healthcare infrastructure in emerging markets.

Segmental Insights

- Based on therapeutic area, the oncology segment dominated the global generic injectables market by capturing 32.6% share in 2025, driven by high demand for cancer treatments.

- Based on container type, the vials segment held the largest share of 48.1% in 2025, supported by their widespread use in hospital settings and ease of storage.

Regional Insights

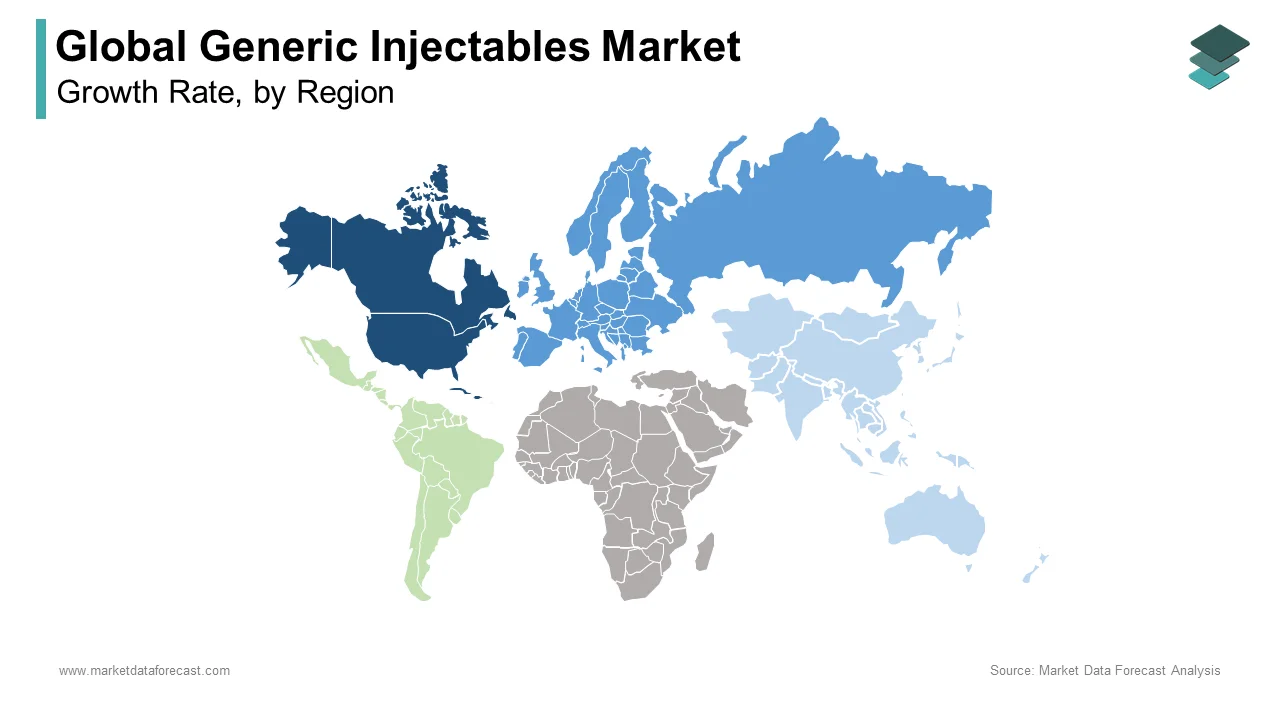

The global generic injectables market is witnessing strong growth across major regions due to increasing healthcare demand and cost pressures.

- North America led the market in 2025 with 38.5% share, driven by high healthcare spending and strong generic drug adoption.

- Europe followed with 27.6% share, supported by favorable regulatory policies and growing demand for affordable treatments.

- Asia-Pacific is the fastest-growing region due to expanding healthcare access, increasing manufacturing capabilities, and rising disease burden.

Competitive Landscape

The global generic injectables market is highly competitive, with key players focusing on expanding product portfolios, investing in biosimilars, and strengthening manufacturing capabilities. Strategic collaborations, mergers, and acquisitions are common as companies aim to enhance their market position.

Prominent companies operating in the global generic injectables market include Hospira (Pfizer), Fresenius Kabi, Teva Pharmaceutical Industries, Hikma Pharmaceuticals, Sandoz (Novartis), Sagent Pharmaceuticals, Sanofi, and Baxter International.

Global Generic Injectables Market Size

The size of the global generic injectables market was worth USD 159.72 billion in 2025. The global market is anticipated to grow at a CAGR of 12.4% from 2026 to 2034 and be worth USD 457.36 billion by 2034 from USD 179.53 billion in 2026.

Generic injectables are sterile, pharmaceutical drugs designed to be injected into the body (intravenously, intramuscularly, etc.) that are therapeutically equivalent to an original brand-name drug, but are marketed after the original patent has expired. This market is fundamental to global healthcare infrastructure, delivering critical therapies for anesthesia, oncology, infectious diseases, and chronic conditions in hospital and ambulatory settings. The strategic importance of this market lies in its ability to provide life-saving treatments at a fraction of the cost of originator products, thereby ensuring accessibility for public health systems worldwide. The WHO Model List of Essential Medicines (24th Edition, 2025) includes over 520 medicines vital for global health systems. Injectable formulations are critical across almost every therapeutic category, particularly for emergency care, where they are often the only viable route for life-saving administration. Furthermore, Research published in the Bulletin of the World Health Organization indicates that approximately 313 million major surgical procedures are performed each year globally. The vast majority of these operations, especially in low- and middle-income countries, rely on a core set of generic injectable anesthetics (like ketamine and lidocaine) and analgesics listed as essential for safe patient management. The shift toward outpatient care has also intensified demand. According to OECD Health Statistics, the proportion of surgical procedures performed as "day cases" or in ambulatory settings has increased substantially across member nations. For instance, in many developed economies, ambulatory surgery now accounts for the majority of specific high-volume procedures, driving a significant demand for cost-effective, ready-to-use sterile injectable solutions. The reliance on generic injectables is a primary mechanism for sustaining clinical operations under increasing budget pressures. Furthermore, this strategy allows providers to maintain high patient outcomes and safety standards.

MARKET DRIVERS

Escalating Global Prevalence of Chronic Diseases Requiring Parenteral Therapy

The surging incidence of chronic conditions such as cancer, diabetes, and cardiovascular diseases is a major booster of the global generic injectables market. This drives the robust demand for generic injectable medications. These ailments often necessitate long-term administration of biologics or small-molecule drugs that cannot be delivered orally due to poor bioavailability or degradation in the gastrointestinal tract. According to the International Agency for Research on Cancer, there were an estimated 20 million new cancer cases globally in 2022, with a vast majority of patients requiring chemotherapy regimens composed largely of off-patent injectable agents like cisplatin and doxorubicin. Similarly, the International Diabetes Federation reports that 537 million adults live with diabetes, many of whom depend on affordable generic insulin injections for daily survival. The aging population further exacerbates this trend, as elderly patients frequently suffer from multiple comorbidities requiring complex injection protocols. Data from the United Nations Department of Economic and Social Affairs projects that the number of people aged 65 years or older will double by 2050, directly correlating with increased consumption of parenteral therapies for heart failure and stroke management. Hospitals and clinics prioritize generic versions to manage these high volumes sustainably, ensuring that cost does not become a barrier to essential life-extending treatments for the growing burden of chronic illness worldwide.

Cost Containment Pressures on Public and Private Healthcare Systems

Intense financial pressure on healthcare payers and providers to reduce expenditure while maintaining quality of care is surging, which further propels the growth of the generic injectables market. As a result, the widespread adoption of generic injectables over expensive branded counterparts is increasing. Governments and insurance companies globally are implementing stringent policies to encourage the substitution of originator drugs with generics to alleviate budget deficits. According to the Organisation for Economic Co-operation and Development, pharmaceutical spending accounts for approximately 15% to 17% of total health expenditure in many member countries, prompting aggressive procurement strategies favoring lower-cost alternatives. In the United States, data from the Association for Accessible Medicines highlights that the healthcare system achieves massive cost reductions, amounting to trillions of dollars over a decade, through the utilization of generic drugs. Sterile injectables account for a significant share of this value due to the high price of their branded counterparts. Across Europe, national health authorities have implemented strict protocols mandating the use of generic medicines in public hospitals. These measures are designed to optimize resource allocation and maintain service levels despite rising operational costs. A study suggests that health systems that successfully maximize generic penetration rates are better positioned to maintain financial sustainability and ensure broader patient access to essential life-saving therapies. This economic imperative forces hospital formularies to prioritize generic injectables, making them the default choice for standard treatments and fueling market expansion as stakeholders seek viable solutions to sustain healthcare delivery in an era of fiscal constraint.

MARKET RESTRAINTS

Complex Manufacturing Requirements and Sterility Assurance Challenges

The intricate nature of manufacturing sterile injectable products and the rigorous necessity for absolute sterility are complex, which negatively impacts the expansion of the generic injectables market. Together, they act as a formidable barrier to market entry and consistent supply. Unlike oral solids, injectables require aseptic processing or terminal sterilization within highly controlled environments to prevent microbial contamination, which can lead to fatal sepsis in patients. According to the Food and Drug Administration, sterile product facilities face significantly higher inspection scrutiny, with approximately 33% to 40% of warning letters issued to pharmaceutical manufacturers related to sterility assurance failures or data integrity issues in injectable lines. The complexity of lyophilization (freeze-drying) and the need for specialized isolator technology increase capital expenditure substantially, deterring smaller players from entering the market. Data from the International Society for Pharmaceutical Engineering highlights that building a compliant sterile fill-finish facility can cost upwards of 100 million dollars, creating a high threshold for production capacity expansion. Furthermore, any deviation in particulate matter limits or endotoxin levels results in immediate batch rejection, leading to supply shortages. The technical difficulty in maintaining consistent quality across large batches restricts the number of qualified suppliers, limiting market competition and creating vulnerabilities in the supply chain that hinder the reliable availability of generic injectables globally.

Frequent Supply Chain Disruptions and Raw Material Volatility

Continuing vulnerabilities in the global supply chain and the volatility of key raw material prices are limiting factors for the generic injectables market. These factors destabilize the production and distribution of generic injectables. The manufacturing of these drugs relies heavily on active pharmaceutical ingredients (APIs) and specialized components like glass vials and rubber stoppers, often sourced from a limited number of geographic regions. According to the World Bank, global supply chain disruptions caused by geopolitical tensions and logistical barriers led to an increase in freight costs and significant delays in API shipments during recent years. The dependence on single-source suppliers for critical sterile packaging materials has resulted in recurrent shortages, as per the American Society of Health-System Pharmacists, which reported over 300 drug shortages in the United States in 2023, with injectables comprising the largest category. Fluctuations in the price of petroleum-based plastics and glass further squeeze profit margins for generic manufacturers who operate on thin pricing models. Data from the International Monetary Fund indicates that producer price indices for chemical inputs rose sharply, forcing some manufacturers to halt production lines due to unprofitability. These supply-side constraints create unpredictability in market availability, eroding trust among healthcare providers and limiting the ability of the market to meet consistent global demand reliably.

MARKET OPPORTUNITIES

Expansion of Biosimilars and Complex Generic Formulations

The emerging landscape of biosimilars and complex generic injectables offers strong potential for the generic injectables market. Market participants can use this shift to capture high-value segments previously dominated by branded biologics. Manufacturers can develop biosimilars that offer similar efficacy at reduced costs as patents for major biologic drugs expire. Consequently, this opens new revenue streams beyond traditional small-molecule generics. According to the European Medicines Agency and industry economic reports, the approval and adoption of biosimilars in Europe have generated massive cumulative savings for healthcare systems. This demonstrates the immense potential for these products to increase the affordability of critical biological therapies. The development of complex injectables such as liposomal formulations, long-acting depots, and peptide-based drugs requires advanced technological capabilities that create higher barriers to entry and improved profit margins. Research suggests that the expanded use of biosimilars could save the global healthcare system hundreds of billions of dollars over the coming decade. These projected savings are a primary driver for significant investment in the development of off-patent biological medicines. Companies investing in specialized delivery platforms and novel excipient systems can differentiate their portfolios and secure long-term contracts with large health systems. This shift toward high-complexity products allows manufacturers to move up the value chain, addressing unmet medical needs while capitalizing on the growing demand for affordable advanced therapies in oncology and immunology.

Growth of Ambulatory Surgical Centers and Home Infusion Therapies

The decisive shift of healthcare delivery from inpatient hospitals to ambulatory surgical centers (ASCs) and home care settings provides a substantial opportunity to expand the use of these injectables within the global generic injectables market. Patients increasingly prefer receiving treatments such as chemotherapy, antibiotics, and pain management in comfortable, cost-effective environments outside traditional hospitals. Projections from the Centers for Medicare and Medicaid Services indicate that spending on ambulatory health services is expected to outpace hospital care growth. This reflects a broad trend toward decentralizing medical services to more cost-effective outpatient and community settings. This transition demands reliable supplies of portable, easy-to-administer generic injectables that ensure safety and efficacy in non-clinical settings. The National Association for Home Care & Hospice reports a steady rise in the number of patients receiving complex infusion therapy in their own homes. This shift is creating a large and growing market for manufacturers of generic and biosimilar injectable medications. Furthermore, ASCs operate on tighter budgets than hospitals, making them highly receptive to cost-saving generic options without compromising quality. Generic injectable producers can tailor their packaging and distribution channels to support decentralized care environments. By doing so, they can tap into rapidly growing market segments.

MARKET CHALLENGES

Stringent Regulatory Scrutiny and Bioequivalence Demonstration Hurdles

Navigating the increasingly rigorous regulatory landscapes and the complex requirements for demonstrating bioequivalence in injectable products poses a significant challenge for participants in the generic injectables market. Regulatory agencies demand extensive clinical and analytical data to prove that generic injectables match the safety and efficacy profiles of reference-listed drugs, a process that is both time-consuming and costly. According to sources, the approval pathway for complex injectables often requires additional pharmacokinetic studies and sometimes clinical endpoint trials, extending development timelines by several years compared to oral generics. The European Medicines Agency has similarly tightened guidelines regarding impurity profiles and leachables from container closure systems, requiring sophisticated testing methodologies. Frequent changes in regulatory expectations regarding sterility testing and particulate matter further complicate compliance efforts. Manufacturers must constantly adapt to evolving global standards, which vary by region, creating a fragmented regulatory environment that hampers efficient global product launches and increases the risk of rejection or delayed market entry for new generic candidates.

Intense Price Erosion and Margin Compression in Competitive Tenders

The pervasive issue of aggressive price erosion driven by competitive bidding processes and group purchasing organizations severely impacts the profitability and sustainability of the generic injectables market. In many healthcare systems, procurement is determined through tender mechanisms where the lowest bidder wins the entire supply contract, forcing manufacturers to slash prices to unsustainable levels. This race to the bottom often compromises supply security, as manufacturers may exit the market if production becomes unprofitable. The pressure is exacerbated by the consolidation of hospital networks and buying groups that leverage massive volume to negotiate deeper discounts. This economic environment discourages innovation and threatens the long-term viability of suppliers, potentially leading to reduced competition and increased vulnerability to shortages when low-margin producers cease operations, thereby challenging the stability of the entire market ecosystem.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Therapeutic Area, Containers, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Hospira (Pfizer), Fresenius Kabi, Hikma, Sandoz (Novartis), Sagent, Sanofi, and Baxter. |

SEGMENTAL ANALYSIS

By Therapeutic Area Insights

The Oncology segment dominated the global generic injectables market and accounted for a 32.6% share in 2025. This dominance of the segment is driven by the critical reliance of cancer treatment protocols on off-patent intravenous chemotherapeutic agents and the sheer volume of patients requiring these life-saving therapies globally. The oncology segment is also driven by the growing global cancer burden and the high demand for off-patent, injectable chemotherapy. Unlike many oral medications, a significant proportion of cytotoxic drugs must be administered intravenously to ensure immediate bioavailability and precise dosing during complex treatment cycles. According to the International Agency for Research on Cancer, the number of new cancer diagnoses is significant and is projected to rise steadily due to global population growth and an aging society. This trend creates a long-term and increasing demand for accessible oncological care worldwide. The World Health Organization identifies systemic therapy as a critical component of cancer treatment. Injectable formulations of standard medicines remain the global benchmark for treating solid tumors, including those of the lungs, breasts, and colon. As these blockbuster drugs expire, healthcare systems aggressively switch to generic versions to manage the high costs of cancer care. Data from the American Society of Clinical Oncology shows that generic injectables form the backbone of chemotherapy administrations in community-based practices. These affordable options are vital for providing life-saving treatment to patients who would otherwise be unable to afford more expensive branded versions. This massive patient pool, combined with the mandatory parenteral route for many core therapies, ensures the oncology segment remains the financial cornerstone of the market. The intense financial pressure on healthcare systems to reduce the exorbitant costs associated with cancer treatment acts as a powerful driver for the dominance of generic oncology injectables. Cancer care is one of the most expensive areas of medicine, prompting governments and insurance providers to mandate the use of cost-effective alternatives wherever clinical equivalence is proven. Reports from the Organisation for Economic Co-operation and Development indicate that pharmaceutical spending in the oncology sector is growing faster than in other therapeutic areas. This financial pressure has led healthcare payers to adopt policies that prioritize the use of high-quality generic medications. The Centers for Medicare and Medicaid Services in the United States have documented substantial savings in federal health spending due to the adoption of generic injectable therapies. These savings allow for the redistribution of resources to other critical areas of patient care. In Europe, national health services utilize tendering processes that heavily favor low-cost generic suppliers for hospital-based cancer treatments. The European Society for Medical Oncology highlights that the availability of generic injectables has significantly expanded access to essential cancer treatments in developing regions. Lower costs enable healthcare systems to provide therapy to more patients, improving overall survival rates in these areas. Hospitals operating under fixed diagnosis-related group payments rely on the margin provided by cheaper generics to sustain their oncology departments. This economic necessity ensures that generic oncology injectables remain the preferred choice for providers globally, solidifying the segment's leading market position.

The anti-infectives segment is anticipated to witness the fastest CAGR of 9.8% over the forecast period. This rapid expansion of the segment is propelled by the rising prevalence of multidrug-resistant infections, the increasing frequency of surgical procedures requiring prophylaxis, and the urgent global need for affordable antibiotic solutions. The swift growth of the anti-infectives segment is mainly supported by the alarming rise in antimicrobial resistance and the consequent increase in hospital-acquired infections that require potent injectable therapies. Clinicians are increasingly forced to resort to intravenous administration of broader-spectrum or last-resort generic agents to ensure patient survival. This shift is occurring as bacteria evolve to resist oral antibiotics. According to the World Health Organization, antimicrobial resistance is a leading cause of death worldwide. This escalating health crisis creates a critical and urgent demand for advanced injectable treatments capable of combating resistant bacterial strains. The Centers for Disease Control and Prevention show that a notable portion of hospital patients contract infections during their stay. Treating these conditions often requires prolonged courses of potent intravenous antibiotics to ensure patient recovery. The complexity of treating resistant strains like MRSA and CRE often necessitates the use of older generic injectables that remain highly effective but require careful dosing managed in hospital settings. Research published in The Lancet Infectious Diseases indicates a steady increase in the consumption of parenteral antibiotics within intensive care units. This trend reflects the growing complexity of treating severely ill patients and the rising prevalence of difficult-to-treat infections. This clinical shift toward aggressive IV therapy for resistant pathogens drives a surge in volume for generic anti-infective injectables, making it the fastest-growing therapeutic category as the global community battles the superbug crisis. The growing number of surgical interventions worldwide and the strict adherence to prophylactic antibiotic protocols serve as a critical booster for the rapid growth of the anti-infectives segment. Preventing surgical site infections is a paramount quality metric, and guidelines universally recommend the administration of injectable antibiotics within one hour before incision. The Organisation for Economic Co-operation and Development confirms that major surgical procedures have returned to their full pre-pandemic capacity. This rebound sustains a high and consistent global demand for the sterile injectable medicines required for perioperative care. Moreover, the World Health Organization emphasizes that administering appropriate surgical prophylaxis can dramatically lower the rate of post-operative infections. These findings have led to the implementation of mandatory antibiotic protocols in hospitals across both developed and developing nations. Many of the recommended agents for prophylaxis, such as cefazolin and clindamycin, are available as low-cost generics, encouraging their ubiquitous use. Observations from the American College of Surgeons show that healthcare providers have become significantly more consistent in the timing and selection of prophylactic treatments. This improved adherence to safety standards drives a reliable demand for high-quality injectable products. Furthermore, the rise of ambulatory surgical centers has expanded the settings where these prophylactics are administered, broadening the market base beyond traditional hospitals. As surgical volumes continue to grow with aging populations and increased access to care, the requirement for reliable, affordable generic injectable antibiotics for prevention ensures this segment maintains its high growth trajectory.

By Container Type Insights

The Vials segment held the majority share of 48.1% of the generic injectables market in 2025. This supremacy of the segment is attributed to its versatility in accommodating various drug volumes, their compatibility with lyophilized formulations, and their established role in hospital pharmacy compounding workflows. The main factor behind the dominance of vials is their unique ability to house lyophilized (freeze-dried) powders, which constitute a large portion of unstable generic injectables such as antibiotics, oncology drugs, and biologics. Many active pharmaceutical ingredients degrade rapidly in liquid form, necessitating a dry state that requires reconstitution with a solvent immediately before administration, a process perfectly suited for vial formats. Vials also offer the flexibility for multi-dose usage in certain clinical settings, allowing healthcare providers to draw multiple doses from a single container when preservatives are added, which reduces waste and cost for high-volume drugs. The ability of vials to accommodate volumes ranging from 2 milliliters to over 100 milliliters makes them indispensable for diverse therapies, including parenteral nutrition and large-volume infusions. This functional adaptability ensures that vials remain the default packaging choice for the widest array of generic injectable products, securing their leading market share. The entrenched infrastructure of hospital pharmacies and the widespread practice of extemporaneous compounding further cement the leading position of the vial segment. Hospital pharmacists routinely compound individual patient doses from bulk vials to tailor concentrations or mix multiple drugs into a single bag, a workflow that is optimized for vial access using standard needles and transfer devices. The global supply chain for glass and plastic vials is mature and robust, ensuring consistent availability and lower unit costs compared to more specialized containers. The familiarity of nursing staff with vial reconstitution techniques minimizes training requirements and reduces the risk of administration errors. This deep integration into clinical workflows and the economic efficiency of bulk vial purchasing create a high barrier for alternative formats to displace vials, ensuring their continued dominance in the market landscape.

The prefilled syringes segment is likely to experience the fastest CAGR of 11.5% from 2026 to 2034, owing to the critical need to minimize medication errors, the shift toward home-based care administration, and the superior convenience they offer to healthcare professionals and patients alike. In addition, the swift growth of the prefilled syringe segment is primarily fueled by the urgent global imperative to reduce medication errors associated with the manual drawing of drugs from vials, which can lead to dosage inaccuracies and contamination. Prefilled syringes eliminate the steps of reconstitution and withdrawal, thereby removing significant opportunities for human error and needlestick injuries among healthcare workers. According to research, medication errors involving injectables result in thousands of adverse events annually, with incorrect dosing during transfer from vials being a major contributor. In emergencies where seconds count, the ready-to-administer nature of prefilled syringes is invaluable. As regulatory bodies and accreditation organizations increasingly mandate safer delivery systems, the transition from vials to prefilled syringes accelerates. This safety-driven adoption, supported by strong clinical evidence, propels the segment to become the fastest-growing container type in the generic injectables market. The decisive shift of care delivery from hospitals to home settings and the rising trend of patient self-administration act as a potent catalyst for the rapid expansion of the prefilled syringe segment. Patients managing chronic conditions at home require delivery systems that are intuitive, portable, and safe to use without professional supervision, characteristics inherent to prefilled syringes. According to a study, the number of patients receiving infusion therapy and injectable medications at home has grown in the last five years, driven by cost containment and patient preference. Research notes that prefilled syringes improve adherence to treatment regimens by simplifying the injection process, which is crucial for therapies like insulin, anticoagulants, and fertility drugs. Various sources suggest that the convenience of prefilled formats increases patient satisfaction scores significantly compared to traditional vial and syringe combinations. Furthermore, the aging population prefers devices that require less dexterity and technical skill, making prefilled syringes the ideal solution for elderly patients self-injecting at home. The demand for user-friendly, ready-to-use generic injectables in prefilled syringes is surging as healthcare systems continue to decentralize services. Consequently, this shift is driving exceptional growth rates.

REGIONAL ANALYSIS

North America Generic Injectables Market Analysis

North America led the global generic injectables market and accounted for a 38.5% share in 2025. The demand for these injectables in this region is driven by a mature healthcare infrastructure, high per capita healthcare spending, and a robust regulatory framework that encourages generic competition. Market conditions are defined by high-volume generic utilization in hospitals and a robust infrastructure for handling specialized, sterile, complex items. The widespread adoption of low-cost generic injectables over branded alternatives is largely driven by stringent cost-containment strategies implemented by government programs and private insurers. According to research, the utilization of generic drugs in the United States saves the healthcare system hundreds of billions of dollars annually, with injectables representing a significant portion of these savings due to their high acquisition costs. The Food and Drug Administration maintains a rigorous but clear pathway for generic approval, fostering a competitive environment among manufacturers. Furthermore, the rising prevalence of chronic diseases and an aging population drive consistent demand for oncology and cardiovascular injectables. The presence of major group purchasing organizations further consolidates demand for generics, solidifying North America's position as the largest and most influential market globally.

Europe Generic Injectables Market Analysis

Europe followed closely behind in the generic injectables market and captured a share of 27.6% share in 2025. This expansion of the European market is supported by its fragmented yet cohesive regulatory environment under the European Medicines Agency and strong national policies promoting generic substitution. The market status is defined by varying adoption rates across countries, with Germany, France, and the UK leading in generic uptake due to proactive government incentives and tendering systems. A critical driver is the economic pressure on national health services to manage rising healthcare costs amidst aging demographics, prompting strict mandates for the use of cost-effective generic injectables in public hospitals. The European Commission actively supports market entry for generics to ensure supply security and affordability. Research shows that generic penetration in the injectable sector has grown steadily, with savings reinvested into innovative treatments. Additionally, the region's strong focus on sustainability drives innovation in packaging and manufacturing processes. The harmonization of standards through the EU Falsified Medicines Directive enhances trust in generic products, while cross-border trade facilitates efficient distribution. These factors combine to sustain Europe's significant standing as a key growth engine for the global generic injectables market.

Asia Pacific Generic Injectables Market Analysis

The Asia Pacific region emerges as the fastest-growing market globally due to rapidly expanding healthcare access, increasing manufacturing capabilities, and a burgeoning burden of infectious and chronic diseases. The market is heterogeneous and in flux, with a clear distinction between the tightly controlled sectors in Japan and Australia and the competitive, low-cost landscape of India and China. Also, the market is largely propelled by the immense scale of disease prevalence, particularly within the oncology and infectious disease sectors, in conjunction with governmental strategies designed to enhance accessibility via domestic generic manufacturing. According to studies, the Western Pacific and South-East Asia regions account for a disproportionate share of global cancer and tuberculosis cases, driving immense demand for affordable injectable treatments. India, known as the "pharmacy of the world," is a leading exporter of generic injectables, leveraging its cost-competitive manufacturing base to supply both domestic and international markets. A study indicates significant investments in healthcare infrastructure across Southeast Asia, increasing the capacity to administer IV therapies in rural areas. The rising middle class in China and Indonesia is also demanding higher-quality healthcare, shifting consumption from unregulated compounds to approved generic injectables. These converging trends position the Asia Pacific as the most vibrant and high-potential frontier for market growth.

Latin America Generic Injectables Market Analysis

Latin America maintains a significant position in the global market owing to increasing government focus on public health coverage, the expansion of private insurance, and a growing reliance on generic medicines to stretch limited healthcare budgets. The market status is characterized by a mix of advanced private hospital networks utilizing high-quality generics and public sectors struggling with supply consistency but increasingly adopting generic tenders. The main reason for this region is the economic necessity for nations like Brazil, Mexico, and Argentina to provide essential treatments to large populations without incurring the high costs of branded drugs. According to sources, non-communicable diseases now account for the majority of deaths in the region, necessitating sustained access to injectable therapies for diabetes, hypertension, and cancer. The regulatory landscape is improving, with agencies like ANVISA in Brazil streamlining approval processes to encourage generic entry. Various sources emphasize that public procurement policies increasingly mandate generic participation to ensure affordability. The rise of local manufacturing capabilities reduces dependency on imports and lowers costs. Currency volatility and economic instability pose challenges to the market. However, the fundamental drive to expand healthcare access through cost-effective solutions ensures steady growth potential for generic injectables in this region.

Middle East and Africa Generic Injectables Market Analysis

The Middle East and Africa region is anticipated to grow notably in the generic injectables market between 2026 and 2034 due to government-led healthcare transformation initiatives, international aid programs, and a critical need for affordable treatments for infectious diseases. The market status is heavily concentrated in Gulf Cooperation Council countries, where high per capita income enables the adoption of quality generic injectables, while Sub-Saharan Africa relies heavily on donor-funded programs and local production hubs. A significant driving factor is the persistent burden of infectious diseases such as HIV/AIDS, tuberculosis, and malaria, which require extensive injectable treatment regimens that must be affordable to be sustainable. The World Health Organization Regional Office for Africa emphasizes that expanding access to essential medicines is a top priority, with generic injectables playing a central role in national treatment guidelines. In the Middle East, strategic visions like Saudi Vision 2030 include massive investments in local pharmaceutical manufacturing to reduce import dependence and ensure supply security. The rising prevalence of lifestyle diseases in urban centers is also beginning to drive demand for oncology and cardiovascular generics. Although infrastructure gaps remain, the focused investment in health security and the push for self-sufficiency are laying the groundwork for future market expansion in this diverse region.

COMPETITIVE LANDSCAPE

The competition in the global generic injectables market is characterized by intense rivalry among a few large multinational corporations and numerous regional manufacturers striving for dominance in a price-sensitive environment. The landscape is moderately consolidated, with key players leveraging economies of scale and extensive distribution networks to capture significant market share. Competitive dynamics are driven by aggressive bidding in government tenders and group purchasing organization contracts, where price often dictates supplier selection. However, the battleground is shifting toward product differentiation through complex generics, ready-to-administer formats, and superior supply chain reliability to avoid commoditization. Regulatory compliance acts as a major barrier to entry, ensuring that only firms with robust quality systems can sustain operations amid frequent inspections. Mergers and acquisitions are frequent as larger entities seek to absorb smaller competitors or acquire specialized technologies to broaden their portfolios. This dynamic environment fosters continuous improvement in manufacturing efficiency and product safety while pressuring margins, forcing companies to innovate constantly to survive and thrive in this critical healthcare sector.

KEY MARKET PLAYERS

Some noteworthy companies leading the global generic injectables market are

- Hospira (Pfizer)

- Fresenius Kabi

- Teva Pharmaceutical Industries

- Hikma

- Sandoz (Novartis)

- Sagent

- Sanofi

- Baxter

TOP PLAYERS IN THE MARKET

- Fresenius Kabi stands as a global leader in the generic injectables sector by providing a vast portfolio of critical care medicines, including anesthetics, oncology drugs, and anti-infectives. The company contributes significantly to worldwide healthcare security through its extensive manufacturing network that ensures a steady supply of essential sterile products. Recent actions to strengthen its market position include strategic acquisitions of specialized production facilities to expand capacity for complex generics and biosimilars. Fresenius Kabi has also invested heavily in digitalizing its supply chain to enhance traceability and reduce shortages. Their focus on developing ready-to-administer formats aligns with current hospital needs for safety and efficiency. The company maintains a robust presence in both developed and emerging markets by prioritizing sustainability and operational excellence. Consequently, this solidifies its reputation as a reliable partner for health systems globally.

- Hospira, now operating within Pfizer, remains a dominant force in the generic injectables market, known for its comprehensive range of infusion therapies and pain management solutions. The company plays a vital role in the global landscape by supplying high-quality sterile medications to hospitals and ambulatory centers across numerous countries. Recent strategic moves involve integrating advanced manufacturing technologies to improve production yields and ensure consistent product availability amidst global supply challenges. Hospira has also expanded its portfolio of prefilled syringes to meet the growing demand for safer and more convenient delivery systems. Their commitment to rigorous quality standards and regulatory compliance reinforces trust among healthcare providers. Hospira strengthens its competitive edge through continuous innovation in drug delivery devices and active engagement in government tender programs. In doing so, they ensure broad access to life-saving generic therapies for patients worldwide.

- Teva Pharmaceutical Industries operates as a key player in the generic injectables market by leveraging its massive scale and diverse product pipeline to serve global health needs. The company contributes extensively by offering a wide array of sterile formulations covering therapeutic areas such as oncology, neurology, and infectious diseases. Recent actions to bolster its market standing include optimizing its global manufacturing footprint to increase flexibility and reduce costs while maintaining high quality. Teva has also focused on launching complex generic injectables that offer higher margins and address unmet medical needs. Their proactive approach to securing long-term supply contracts with major health systems ensures stable revenue streams. Teva continues to drive accessibility and affordability in the generic injectables sector by investing in research and development for novel delivery platforms and strengthening its logistics network. This approach reinforces its status as an industry powerhouse.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the generic injectables market primarily focus on expanding their manufacturing capacities through strategic acquisitions and organic growth to mitigate supply shortages and meet rising global demand. Companies heavily invest in developing complex generic formulations and biosimilars that offer higher profit margins and reduced competition compared to simple commodities. Vertical integration represents another major approach where firms control the entire supply chain from active pharmaceutical ingredients to finished sterile products to ensure quality and cost efficiency. Market participants are increasingly adopting advanced packaging technologies like prefilled syringes and ready-to-mix systems to enhance safety and convenience for healthcare providers. Partnerships with group purchasing organizations and government bodies help secure large-volume contracts and stabilize revenue streams. Additionally, firms are implementing robust quality management systems and digital tracking tools to comply with stringent regulatory requirements and build trust. These combined strategies enable leading companies to maintain competitive advantages and drive sustainable growth in a highly regulated environment.

The competition in the global generic injectables market is characterized by intense rivalry among a few large multinational corporations and numerous regional manufacturers striving for dominance in a price-sensitive environment. The landscape is moderately consolidated, with key players leveraging economies of scale and extensive distribution networks to capture significant market share. Competitive dynamics are driven by aggressive bidding in government tenders and group purchasing organization contracts, where price often dictates supplier selection. However, the battleground is shifting toward product differentiation through complex generics, ready-to-administer formats, and superior supply chain reliability to avoid commoditization. Regulatory compliance acts as a major barrier to entry, ensuring that only firms with robust quality systems can sustain operations amid frequent inspections. Mergers and acquisitions are frequent as larger entities seek to absorb smaller competitors or acquire specialized technologies to broaden their portfolios. This dynamic environment fosters continuous improvement in manufacturing efficiency and product safety while pressuring margins, forcing companies to innovate constantly to survive and thrive in this critical healthcare sector.

MARKET SEGMENTATION

This research report on the global generic injectables market has been segmented and sub-segmented based on the therapeutic area, containers, distribution channel, and region.

By Therapeutic Area

- Oncology

- Anesthesia

- Anti-Infectives

- Parenteral Nutrition

- Cardiovascular Diseases

By Containers

- Vials

- Ampoules

- Premix

- Prefilled Syringe

By Distribution Channel

- Hospitals

- Retail Pharmacy

By Region

- North America

- The United States

- Canada

- Rest of North America

- Europe

- United Kingdom

- Germany

- Spain

- France

- Italy

- Rest of EU

- Asia-Pacific

- India

- China

- Japan

- Australia

- New Zealand

- Rest of APAC

- Latin America

- Brazil

- Argentina

- Mexico

- Rest of Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the global generic injectables market?

The global generic injectables market includes low-cost, FDA-approved injectable drugs used for chronic conditions and acute treatments, driving accessible healthcare globally

2. What drives growth in the global generic injectables market?

Growth is fueled by patent expirations, rising chronic diseases, biosimilar adoption, regulatory support, and increased manufacturing capacity in the global generic injectables market

3. What are biosimilars’ roles in the global generic injectables market?

Biosimilars offer affordable alternatives to branded biologics, expanding treatment options and lowering costs in the global generic injectables market

4. How do patent expirations impact the global generic injectables market?

Patent cliffs allow generic manufacturers to produce affordable injectables, significantly boosting the global generic injectables market growth

5. Which regions lead the global generic injectables market?

North America dominates, followed by Europe and Asia-Pacific, driven by healthcare infrastructure and rising demand in the global generic injectables market

6. What challenges does the global generic injectables market face?

Challenges include supply shortages, regulatory hurdles, high manufacturing costs, and quality control within the global generic injectables market

7. How do government policies affect the global generic injectables market?

Favorable policies, tax reforms, and incentives promote drug manufacturing and approvals, accelerating growth in the global generic injectables market

8. What role do manufacturing facilities play in the global generic injectables market?

Advanced sterile manufacturing facilities ensure quality production, resilience, and capacity expansion in the global generic injectables market

9. How does the global generic injectables market address drug shortages?

Increased generic injectable production reduces shortages in hospitals, ensuring affordable access to vital medications in the global generic injectables market

10. What diseases are mainly treated with products from the global generic injectables market?

Chronic diseases like cancer, diabetes, cardiovascular disorders, and infectious diseases significantly drive demand in the global generic injectables market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com