Global Iron Ore Market Size Share, Trends, and Growth Analysis Report, Segmented By Type (Hematite, Magnetite, Others), Application & Region (North America, Europe, Latin America, Asia Pacific, Middle East & Africa), Industry Forecast From 2025 to 2033

Global Iron Ore Market Size

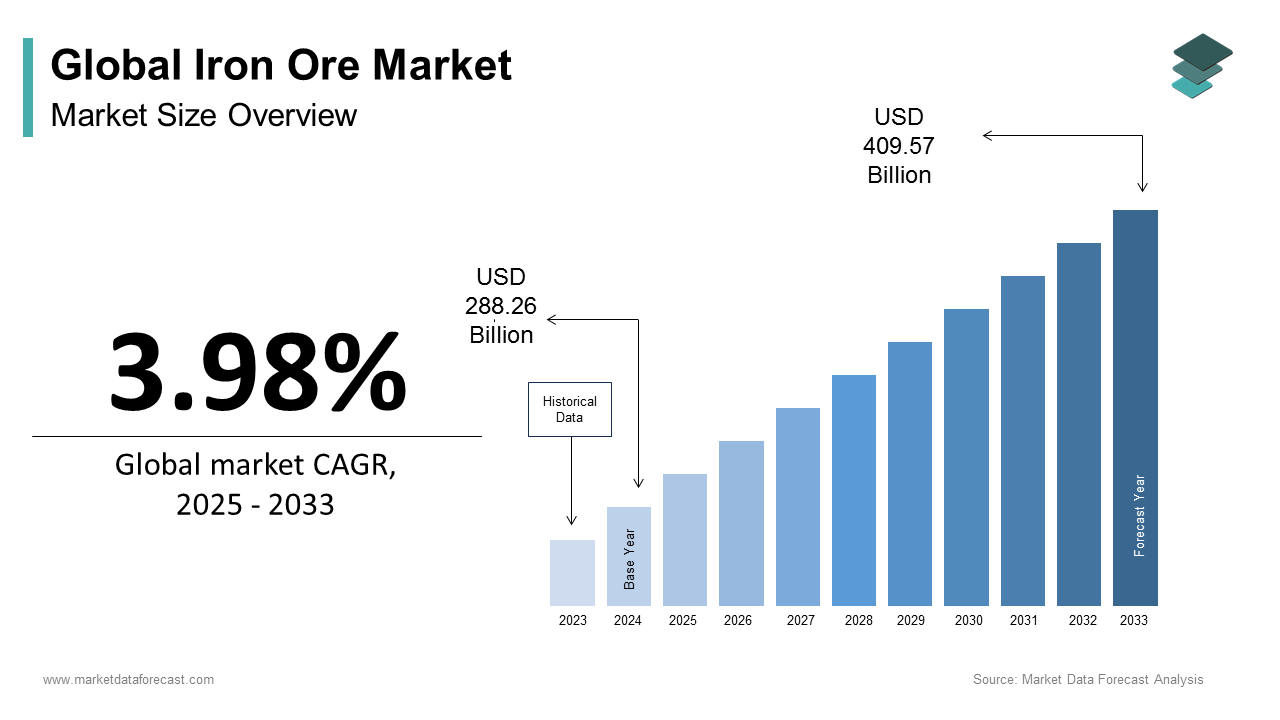

The global iron ore market size was valued at USD 288.26 billion in 2024 and is anticipated to reach USD 299.73 billion in 2025 and USD 409.57 billion by 2033, growing at a CAGR of 3.98% during the forecast period from 2025 to 2033.

The Iron ore global extraction, trade, and utilization of iron-bearing rock, primarily used in steel production, accounts for over 98% of total demand. As the foundational raw material for modern industrial infrastructure, iron ore is categorized by grade, with high-grade hematite and magnetite ores preferred for their elevated iron content and reduced processing requirements. According to the International Energy Agency, steel production alone contributes approximately 7% of global direct carbon dioxide emissions, placing iron ore at the center of decarbonization debates in heavy industry.

MARKET DRIVERS

Expanding Urban Infrastructure Development in Emerging Economies

The rapid urbanization across Asia, Africa, and Latin America is fueling structural steel demand, which is elevating the growth of the Iron ore market. According to the United Nations Department of Economic and Social Affairs, over 2.5 billion people are projected to be added to urban populations in developing nations by 2050. In India, the National Infrastructure Pipeline outlines $1.3 trillion in planned spending through 2030, with steel demand for railways and metro systems expected to rise by 6.8% annually, as reported by the Indian Bureau of Mines. These infrastructure imperatives ensure sustained demand for iron ore in nations transitioning from low- to middle-income status.

China’s Dominant Role in Global Steelmaking and Import Dependency

China remains the single largest consumer of iron ore, fuelling the growth of the Iron ore market. The average iron content of Chinese domestic ore is below 35%, compared to 62% in Australian premium fines, making imports economically and operationally necessary, as noted by the Ministry of Natural Resources. Additionally, Port of Qingdao, the world’s largest iron ore terminal, handled over 150 million tonnes in 2023, reflecting the scale of logistical infrastructure dedicated to ore supply. This entrenched dependency ensures that Chinese steel mill activity remains the most influential variable in global iron ore pricing and trade flows.

MARKET RESTRAINTS

Declining Quality of Available Iron Ore Reserves

The average iron content in mined ore has steadily declined, increasing processing costs and environmental impact, which are restraining the growth of the iron ore market. According to the Commonwealth Scientific and Industrial Research Organisation (CSIRO), the average grade of hematite ore from the Pilbara region in Australia has dropped from 62% Fe in 2010 to 58.5% Fe in 2023. Lower-grade ores require more energy-intensive beneficiation, generating greater volumes of tailings and waste. In Brazil, Vale reported that over 40% of its current production involves processed fines and pellets due to the exhaustion of direct-shipping ore bodies, as detailed in its 2023 Sustainability Report.

Environmental and Regulatory Pressures on Mining Operations

Iron ore extraction faces mounting scrutiny due to its ecological footprint, including deforestation, water contamination, and greenhouse gas emissions, which are another factor degrading the growth of the iron ore market. According to the Intergovernmental Panel on Climate Change, the mining and processing of iron ore contribute approximately 1.5 gigatonnes of CO₂-equivalent emissions annually when combined with steelmaking. In 2020, the catastrophic failure of Vale’s Córrego do Feijão tailings dam in Brazil, which killed 270 people, prompted global regulatory tightening. The Global Tailings Review, supported by the United Nations, now mandates independent audits and real-time monitoring for all major facilities. Additionally, Sweden’s LKAB has been required by the European Union’s Industrial Emissions Directive to reduce sulfur and particulate emissions by 30% by 2025, increasing compliance costs.

MARKET OPPORTUNITIES

Growth in Direct Reduced Iron (DRI) and Alternative Steelmaking Technologies

The rise of natural gas-based and hydrogen-ready DRI plants is another factor propelling the growth of the iron ore market. As per the International Energy Agency, DRI production accounted for 76 million tonnes in 2023, which represents 4.2% of global steel output, with expectations of reaching 12% by 2030. In Oman, where natural gas is abundant, the National Iron and Steel Company (NISCO) operates one of the world’s largest DRI facilities by importing premium Brazilian and South African ore.

Expansion of Rail and Port Infrastructure in Ore-Producing Nations

Investments in logistics infrastructure are reducing transportation bottlenecks and lowering delivered costs by enhancing the competitiveness of remote mining regions. In Western Australia, the Roy Hill Infrastructure project completed a 344-kilometer rail line and dedicated port terminal in 2023, enabling the transport of 55 million tonnes of iron ore annually, as reported by the Western Australian Department of Transport.

MARKET CHALLENGES

Geopolitical Volatility and Supply Chain Fragmentation

Iron ore supply is increasingly vulnerable to geopolitical tensions, trade restrictions, and regional instability. More recently, sanctions on Russian commodities have disrupted Black Sea trade routes, affecting Ukrainian pellet exports. According to the International Maritime Bureau, maritime insurance premiums for ore shipments from conflict-adjacent zones rose by 22% in 2023. Additionally, domestic policy shifts in resource-rich nations such as Indonesia’s export bans on raw minerals raise concerns about future iron ore nationalism.

Labor and Operational Challenges in Remote Mining Locations

Major iron ore deposits are often located in geographically isolated and climatically extreme regions that pose a significant challenge for the growth of the iron ore market. In the Pilbara region of Australia, where temperatures regularly exceed 45°C, the Western Australian Department of Mines reports that heat-related absenteeism among mining personnel increased by 18% between 2020 and 2023. Similarly, in northern Quebec, Canada, harsh winters delay exploration and transport, with Rio Tinto noting that up to 30% of annual rail operations are affected by ice and snow.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.98% |

| Segments Covered | By Type, Application, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Vale S.A., Rio Tinto, BHP, Fortescue Metals Group, Anglo American plc, ArcelorMittal, NMDC Limited, Cleveland-Cliffs Inc., Metalloinvest, LKAB, Ferrexpo plc, Champion Iron Limited, Kumba Iron Ore Limited |

SEGMENTAL ANALYSIS

By Type Insights

The hematite segment dominated the global iron ore market by capturing a significant share in 2024. Hematite typically contains 60–66% iron, making it ideal for use in conventional blast furnaces that require high-grade feedstock to optimize yield and energy efficiency. According to the World Steel Association, blast furnaces processing hematite-based sinter and pellets achieve a coke rate of 320–350 kg per tonne of pig iron, significantly lower than when using lower-grade ores. In Australia, the primary global exporter of hematite, Rio Tinto’s Pilbara operations produce ore with an average grade of 61.5% Fe, as confirmed in its 2023 operational review.

The Magnetite segment is likely to grow with an expected CAGR of 6.4% during the forecast period. As per the International Energy Agency, DRI-based steel production is expected to grow by 5.8% annually through 2030, which is driven by decarbonization goals. Modern magnetite beneficiation, including high-intensity magnetic separation and pelletizing, has become more energy-efficient and economically viable. In Canada, Champion Iron’s Bloom Lake mine achieved a 98.5% recovery rate in magnetite processing in 2023, producing a 68.2% Fe concentrate, as reported by the Quebec Ministry of Energy and Natural Resources.

By Application Insights

The Steel Production application segment was the largest and held a dominant share of the iron ore market in 2024. Over 70% of the world’s steel is produced via the basic oxygen furnace (BOF) route, which relies on iron ore–derived hot metal. In China, where BOF production accounts for 88% of total steel output, the Ministry of Industry and Information Technology estimates that over 1.2 billion tonnes of iron ore were consumed in 2023 alone. Steel derived from iron ore is fundamental to construction, transportation, and energy infrastructure.

The Others application segment is esteemed to grow with an expected CAGR of 8.2% throughout the forecast period. Iron ore fines are increasingly used as a raw material in cement kilns to adjust iron modulus in clinker production. According to the Global Cement and Concrete Association, over 12 million tonnes of low-grade iron ore were consumed in cement manufacturing in 2023, particularly in India and Turkey, where limestone often lacks sufficient iron content. Magnetite nanoparticles are being deployed in water purification systems due to their magnetic separability and catalytic properties.

REGIONAL ANALYSIS

Asia Pacific Market Analysis

Asia Pacific was the top performer of the global iron ore market by accounting for 54.2% of share in 2024. China was the largest contributor due to the world’s largest iron ore consumer, importing 1.16 billion tonnes in 2023, according to China Customs from Australia and Brazil. The country’s steel industry, responsible for over half of global output, relies on seaborne hematite due to the poor quality of domestic reserves, which average just 34% Fe, as noted by the Ministry of Natural Resources.

Europe Market Analysis

Europe iron ore market held 18.2% of the share in 2024. Germany remains Europe’s largest steel producer, consuming over 30 million tonnes of iron ore equivalent annually, primarily in the Ruhr Valley’s blast furnaces, as reported by the German Steel Federation. The country is transitioning toward low-carbon steel, with ThyssenKrupp investing €4.3 billion to replace coal-based reduction with hydrogen-ready DRI by 2030. Sweden’s LKAB supplies 80% of the EU’s iron ore, with plans to deliver fossil-free sponge iron by 2026, supported by the European Commission’s Innovation Fund.

North America Market Analysis

North America iron ore market is expected to grow prominently in coming years. The U.S. produced 78 million tonnes of crude steel in 2023, according to the American Iron and Steel Institute, which is requiring approximately 117 million tonnes of iron ore equivalent when accounting for DRI and blast furnace inputs. Minnesota’s Mesabi Range supplies over 90% of domestic hematite, with Cleveland-Cliffs operating the largest taconite pelletizing facilities. The Inflation Reduction Act has incentivized domestic steel production, boosting iron ore demand for EV and renewable energy infrastructure.

Latin America Market Analysis

Latin America iron ore market growth is likely to grow with an expected CAGR during the forecast period. Brazil is the world’s second-largest iron ore exporter, shipping 380 million tonnes in 2023, according to the Brazilian Ministry of Mines and Energy. The country’s high-grade hematite (averaging 65% Fe) is highly sought after in Asian markets. Domestically, steel production reached 31 million tonnes in 2023, with Gerdau and CSN expanding EAF capacity.

Middle East and Africa Market Analysis

Middle East & Africa iron ore market growth is likely to be steady in the coming years. South Africa produced 58 million tonnes of iron ore in 2023, according to the Department of Mineral Resources, with Kumba Iron Ore supplying high-grade hematite to China and Europe. The Sishen mine remains one of the largest open-pit operations globally.

COMPETITION OVERVIEW

Competition in the iron ore market is characterized by a concentrated oligopoly dominated by a few multinational mining giants, where scale, quality, and logistical reliability determine market influence. The competitive landscape is shifting from pure volume and cost leadership to differentiation through sustainability, product purity, and technological integration. While Australian and Brazilian producers dominate seaborne supply, emerging players in Africa and Canada are challenging traditional dynamics with new high-grade projects. Price volatility, driven by Chinese steel demand and geopolitical factors, intensifies strategic maneuvering.

KEY MARKET PLAYERS

A few of the dominating players in the global iron ore market include

- Vale S.A.

- Rio Tinto

- BHP

- Fortescue Metals Group

- Anglo American plc

- ArcelorMittal

- NMDC Limited

- Cleveland-Cliffs Inc.

- Metalloinvest

- LKAB

- Ferrexpo plc

- Champion Iron Limited

- Kumba Iron Ore Limited

Top Strategies Used by Key Market Participants

Key players in the iron ore market are deploying strategies centered on operational efficiency, decarbonization, and customer integration to maintain competitive advantage. Companies are investing in automation, predictive maintenance, and digital twin technologies to optimize extraction and reduce costs. There is a growing shift toward high-grade, low-impurity products that align with energy-efficient and low-emission steelmaking processes. Firms are also advancing green initiatives, including carbon capture, renewable-powered mines, and low-carbon pellet development, to meet evolving regulatory and buyer requirements.

LEADING PLAYERS IN THE IRON ORE MARKET

Vale S.A.

Vale S.A. has dominant position in the global iron ore market through its vast reserves in Brazil and strategic focus on high-grade hematite. In the Asia Pacific region, Vale maintains deep commercial integration with major steel mills in China, Japan, and South Korea, supplying premium fines and pellets tailored to blast furnace efficiency. In 2023, the company launched its Vale Green Pellets initiative, offering low-carbon iron ore pellets to Asian customers aiming to reduce emissions in steelmaking, with pilot shipments delivered to Nippon Steel and POSCO. Vale has also expanded its digital blending solutions by allowing Asian buyers to customize ore specifications via real-time quality data.

Rio Tinto

Rio Tinto is a dominant force in the iron ore market by operating some of the most technologically advanced mines in Western Australia’s Pilbara region. The company plays a pivotal role in the Asia Pacific market by supplying high-grade hematite to Chinese and Japanese steelmakers under long-term contracts and index-linked pricing agreements. In 2022, Rio Tinto commissioned its Gudai-Darri mine, the most automated iron ore operation globally, incorporating autonomous haulage and real-time ore monitoring to enhance consistency and reduce downtime.

BHP

BHP operates at the forefront of sustainable iron ore production, with extensive mining assets in Western Australia and a growing emphasis on decarbonization. In the Asia Pacific market, BHP supplies high-quality iron ore to major steel producers, including Mitsubishi Steel in Japan and HBIS Group in China, under performance-based contracts that prioritize ore consistency and traceability.

MARKET SEGMENTATION

This research report on the global Iron ore market is segmented and sub-segmented into the following categories.

By Type

- Hematite

- Magnetite

- Others

By Application

- Steel Production

- Others

By Region

- North America

- Europe

- Latin America

- Asia Pacific

- Middle East & Africa

Frequently Asked Questions

1. What are the main types of iron ore?

The key types are Hematite (Fe2O3), Magnetite (Fe3O4), Limonite, and Siderite, with hematite and magnetite being the most commercially important.

2. What drives the growth of the iron ore market?

Key growth drivers include rising global steel demand in construction, automotive, and infrastructure, Urbanization in emerging economies, and Technological advancements in mining and processing.

3. What are the major challenges in the iron ore market?

Challenges include Price volatility due to demand-supply imbalances, Environmental concerns and stricter mining regulations, and Logistical constraints in mining and transportation.

4. What is the role of China in the iron ore market?

China is the largest consumer of iron ore, accounting for over 60% of global imports, as it is the world’s biggest steel producer.

5. How is sustainability influencing the iron ore market?

Sustainability is shaping the industry through Efforts to reduce carbon emissions in steelmaking, the adoption of green steel technologies like hydrogen-based reduction, and a focus on responsible mining practices.

6. What are the future opportunities in the iron ore market?

Opportunities include the Development of high-grade iron ore for low-emission steel, growth in infrastructure projects across Asia and Africa, and increased automation and digitalization in mining operations.

7. How is iron ore priced in the global market?

Iron ore prices are influenced by benchmark indices such as Platts and Metal Bulletin, based on ore grade, demand from steelmakers, and shipping costs.

8. What is the outlook for the iron ore market in the next decade?

The market is expected to remain stable to moderately growing, supported by steel demand but challenged by the transition to low-carbon technologies and potential substitution.

9. Who are the leading players in the iron ore market?

Major players include Vale S.A., Rio Tinto, BHP, Fortescue Metals Group, Anglo American plc, ArcelorMittal, NMDC Limited, and Cleveland-Cliffs Inc.

10. Which industries primarily consume iron ore?

Iron ore is primarily consumed by the steel industry, accounting for more than 98% of total demand, with smaller uses in cement production, pigments, and catalysts.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com