Latin America Construction Market Size, Share, Growth, Trends, And Forecast Report Segmented By Construction, End-User, Contractor, And By Country (Brazil, Chile, Argentina, Mexico, and Colombia, etc), Industry Analysis From 2025 to 2033

Latin America Construction Market Size

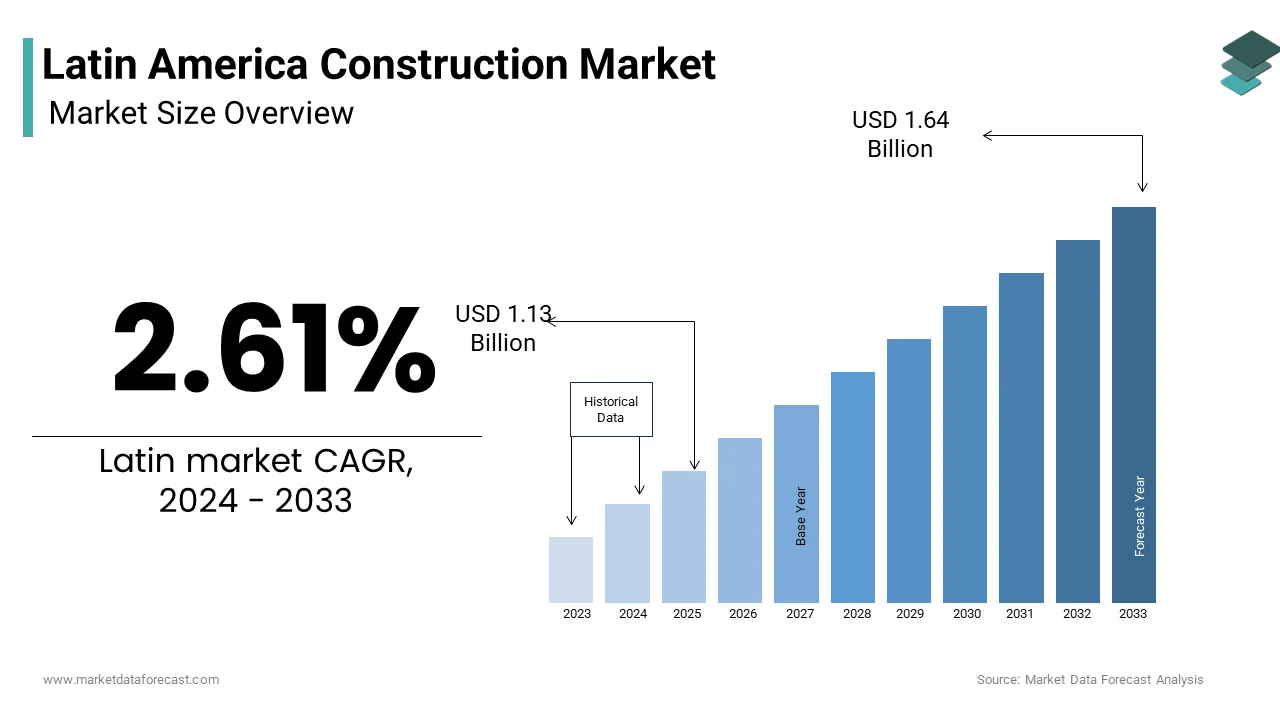

The Latin America construction market size will reach USD 1.07 billion in 2024 and is anticipated to reach USD 1.13 billion in 2025 to USD 1.64 billion by 2033, growing at a CAGR of 5.16% during the forecast period from 2025 to 2033.

MARKET DRIVERS

Rapid Urbanization and Housing Deficit

Latin America’s urban population expansion continues to outpace housing supply by creating sustained demand for residential construction is accelerating the growth of the Latin America construction market. According to the United Nations, over 400 million people in the region live in cities, with urban dwellers expected to reach 500 million by 2030. In countries like Colombia, nearly 27% of urban households reside in informal settlements, underscoring the urgency for formal housing projects.

Government-Led Infrastructure Investment Programs

The national infrastructure modernization initiatives have become a cornerstone of economic policy across Latin America, which is directly stimulating construction activity. This factor is attributed to levelling up the growth of the Latin American construction market. Similarly, Colombia’s National Infrastructure Agency plans to invest COP 110 trillion (USD 27 billion) in road and rail networks by 2026.

MARKET RESTRAINTS

High Construction Material Inflation and Supply Chain Disruptions

The persistent cost escalations due to volatility in key material prices and logistical inefficiencies are hampering the growth of the Latin American construction market. These hikes stem from elevated energy costs, import dependency, and regional transportation bottlenecks. In Argentina, over 60% of construction materials are imported, leaving projects vulnerable to currency fluctuations and customs delays. Additionally, the World Bank notes that logistics costs in Latin America are 30% higher than in East Asia, reducing procurement efficiency.

Regulatory Fragmentation and Bureaucratic Delays

The complex permitting processes and inconsistent regulatory enforcement across jurisdictions hinder construction projects, and execution is also hindering the growth of the Latin American construction market. Municipal-level regulations often conflict with federal standards, creating legal ambiguities that delay groundbreaking. In Colombia, 45% of construction firms reported suspensions due to unresolved zoning disputes in 2022, as per the National Housing and Urbanism Chamber (Camacol). Furthermore, frequent changes in tax policies and land use laws generate uncertainty.

MARKET OPPORTUNITIES

Adoption of Sustainable and Green Building Practices

The growing environmental awareness and tightening climate policies are accelerating the growth of the Latin American construction market. According to the Pan American Health Organization, green buildings can reduce energy consumption by up to 40% and water usage by 30% in regions facing resource scarcity. Additionally, Colombia mandates energy efficiency standards for public buildings under Law 1420 of 2010.

Expansion of Public-Private Partnerships in Transport Infrastructure

The transport infrastructure PPPs are emerging as a vital mechanism to bridge investment gaps in roads, railways, and mass transit systems, which is expected to enhance the growth of the Latin American construction market. These partnerships leverage private sector efficiency while mitigating fiscal strain on governments.

MARKET CHALLENGES

Skilled Labor Shortages and Informal Workforce Dominance

The structural deficit in skilled labor with limiting productivity and project quality, poses a challenge for the growth of the Latin American construction market. As per the International Labour Organization, over 58% of construction workers in the region operate in the informal sector, lacking formal training and safety protections. Brazil faces a shortfall of approximately 350,000 qualified technicians by 2025, as projected by the National Service for Industrial Training (SENAI). This skills gap is exacerbated by limited vocational education investment; UNESCO data shows that less than 12% of secondary students in the region enroll in technical programs.

Climate Vulnerability and Resilience Deficits in Construction Planning

Latin America’s geographic exposure to natural hazards such as earthquakes, hurricanes, and flooding is also expected to limit the growth of the Latin American construction market coming years. In Central America, 70% of infrastructure assets are located in high-risk zones, as reported by the Economic Commission for Latin America and the Caribbean. In 2022, Hurricane Julia damaged over 15,000 homes in Guatemala and El Salvador, exposing weak building code enforcement. Only 12 of 33 countries in the region have comprehensive climate-resilient construction codes, according to the Pan American Federation of Engineers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 2.61% |

| Segments Covered | By Construction, End-User, Contractor, and Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | Brazil, Chile, Argentina, Mexico, and Colombia, etc |

| Market Leaders Profiled | Acs Group, Lennar Corporation, R. Horton Inc., Bouygues S.A., Power Construction Corporation of China, Cimic Group Limited, Shimizu Corporation, Lendlease Group, CAPITALAND Group Pte. Ltd. |

SEGMENTAL ANALYSIS

By Type of Construction Insights

The building construction segment was the largest and held 58.3% of the Latin America construction market share in 2024, with the sustained demand for residential, commercial, and institutional structures across urban centers. In countries like Mexico and Colombia, over 25% of the population resides in substandard housing, fueling government and private investment in social and mid-income housing projects. Additionally, urbanization continues to exert pressure on built environments 81% of Latin Americans now live in cities, as reported by the United Nations, necessitating continuous expansion of schools, hospitals, and office spaces.

The land planning and development segment is projected to grow with a CAGR of 7.4% in the coming years, with the need for integrated urban expansion and climate-resilient zoning. Chile’s Ministry of the Environment mandates land-use assessments for all developments in ecologically sensitive zones is increasing demand for geospatial and environmental planning services. Furthermore, the Inter-American Development Bank reports that every USD 1 invested in pre-construction land planning reduces overall project costs by 12–18% through risk mitigation.

By End-Use Sector Insights

The private sector was the largest by occupying a prominent share of the Latin American construction market in 2024, with real estate investment and commercial development. Additionally, foreign direct investment may also fuel the growth of the segment. The sector benefits from faster project approval timelines and access to capital markets by enabling agile responses to market demand in logistics and mixed-use developments near urban cores.

The public sector is anticipated to grow at a CAGR of 6.8% during the forecast period, with the renewed government focus on infrastructure modernization and social inclusion. Similarly, Peru’s Ministry of Economy and Finance, public investment in construction rose by 19% year-on-year in 2023, the highest in a decade. A key driver is multilateral funding, over USD 22 billion in loans and grants from the IDB, World Bank, and CAF were committed to public construction projects in 2023 alone. Additionally, political imperatives to reduce regional inequality are accelerating investment in underserved areas, such as the Amazonian regions of Ecuador and northern Brazil.

By Contractor Insights

The large contractors segment accounted in holding 54.3% of the Latin America construction market share in 2024 due to their capacity to execute high-value, complex infrastructure and high-rise developments. These firms possess the financial strength, technical expertise, and international certifications required for public-private partnerships and large-scale urban projects. For instance, Brazil’s Andrade Gutierrez and Odebrecht collectively secured 38% of federal infrastructure contracts awarded in 2023, according to Brazil’s Secretariat of Infrastructure.

The small contractors segment is likely to grow with a CAGR of 8.1% in the coming years, with the rising demand for localized, low-rise residential construction and renovation work. Their agility and lower overhead allow them to operate profitably in fragmented markets where large firms find limited economies of scale. Digital platforms like ConstruMano in Argentina are further empowering these firms with access to procurement networks and project management tools, accelerating their professionalization and market penetration.

COUNTRY-LEVEL ANALYSIS

Brazil was the top performer in the Latin American construction market by capturing 34.3% of the share in 2024, with the resurgence in both public infrastructure and private real estate development after years of stagnation. The federal PAC 2023–2026 program has unlocked BRL 1.5 trillion for highways, railways, and sanitation, with 87 major projects already in the execution phase as of mid-2024, as confirmed by the Ministry of Transport. São Paulo and Brasília are witnessing a construction boom in logistics warehouses due to e-commerce expansion, with warehouse vacancy rates falling to 4.1%, the lowest in a decade, as reported by JLL Brazil.

Mexico's construction market growth is likely to grow with strong private investment and industrial expansion, particularly in the northern border states. This has spurred demand for industrial parks and logistics hubs. Querétaro and Nuevo León saw a 31% increase in industrial construction permits in 2023. Additionally, housing remains a key pillar, with INFONAVIT financing over 500,000 homes annually.

KEY MARKET PLAYERS

Acs Group, Lennar Corporation, R. Horton, Inc., BouyguesS.A.A, Power Construction Corporation of China, Cimic Group Limited, Shimizu Corporation, Lendlease Group, and CAPITALAND Group Pte. Ltd. are the market players Latin American construction market.

Top Players In The Market

Odebrecht (Now Novonor)

Novonor, formerly Odebrecht, remains a pivotal force in Latin America’s construction landscape, leveraging decades of expertise in large-scale infrastructure. Despite restructuring after past legal challenges, the company has reestablished its presence through transparent governance and strategic project selection. In Brazil, it continues to lead in hydroelectric, transportation, and industrial construction, recently executing segments of the São Paulo Metro Line 6. The firm has prioritized sustainability by aligning projects with ESG benchmarks and investing in low-carbon concrete technologies. It has also strengthened partnerships with public agencies under Brazil’s renewed PAC program.

CYDARSA (Construcciones y Diseños S.A.)

Based in Mexico, CYDARSA has emerged as a leading contractor in commercial and institutional construction, known for delivering high-quality projects in healthcare, education, and corporate infrastructure. The company has expanded its operational capacity by adopting modular construction techniques and digital project management platforms, significantly reducing delivery timelines. In 2023, it completed the new National Cancer Institute facility in Mexico City, a project lauded for its seismic resilience and energy efficiency. CYDARSA has also formed alliances with international architectural firms to integrate smart building technologies.

Empresas ICA

Empresas ICA, one of Mexico’s oldest and most experienced construction firms, continues to play a vital role in transportation and civil engineering projects despite financial restructurings in recent years. The company has retained core competencies in highway, bridge, and airport construction, recently participating in the expansion of the Guadalajara International Airport. ICA has streamlined operations by divesting non-core assets and refocusing on public infrastructure under government concession models. It has also adopted advanced geotechnical monitoring systems to improve safety and efficiency in mountainous terrain projects. Collaborations with foreign engineering consultants have enhanced its design capabilities, while participation in national infrastructure auctions demonstrates renewed competitiveness.

Top Strategies Used By The Key Market Participants

Key players in the Latin American construction market are deploying strategic initiatives to enhance competitiveness and adapt to evolving demands. Major strategies include forming public-private partnerships to access large-scale infrastructure projects, particularly in transportation and energy. Companies are increasingly adopting Building Information Modeling (BIM) and digital twin technologies to improve planning accuracy and reduce rework. Strategic alliances with international engineering firms are enabling knowledge transfer and compliance with global sustainability standards. Additionally, firms are investing in workforce upskilling and safety training to meet regulatory requirements and improve productivity. Environmental, social, and governance (ESG) integration is becoming central, with companies pursuing green certifications and low-emission construction methods. These strategies collectively strengthen resilience, operational efficiency, and long-term market positioning in a fragmented yet opportunity-rich region.

COMPETITION OVERVIEW

The competition in the LatinAmericana construction market is characterized by a mix of national champions, regional players, and niche specialists operating in a highly fragmented and institutionally diverse environment. While large contractors dominate high-value public infrastructure and urban developments, small and mid-sized firms control a significant portion of residential and localized projects. Competitive advantage is increasingly determined by technical capability, access to financing, and compliance with environmental and safety regulations. Companies are differentiating through innovation in construction methods, including prefabrication and smart building integration. Public procurement processes remain a key battleground, with transparency and bidding efficiency varying widely across countries. In markets like Brazil and Mexico, consolidation is occurring as financially stable firms acquire distressed competitors.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Novonor announced a strategic partnership with Siemens Infrastructure to integrate smart grid technologies into its energy and transportation projects across Brazil by enhancing project efficiency and sustainability.

- In May 2023, Empresas ICA secured a USD 450 million contract from Mexico’s Ministry of Communications and Transport to complete the final phase of the Toluca–Mexico City Interurban Train, reinforcing its role in national rail modernization.

- In September 2023, CYDARSA launched a digital construction lab in Monterrey, deploying AI-driven scheduling tools and drone-based site monitoring to reduce project delays by up to 30%.

- In February 2024, OAS S.A. emerged from judicial reorganization in Brazil and resumed operations with a leaner structure by focusing exclusively on sanitation and road infrastructure under new governance protocols.

- In June 2024, Argentina’s Techint Engineering & Construction was awarded the engineering, procurement, and construction contract for the Vaca Muerta gas pipeline expansion, marking a major step in energy infrastructure development in Patagonia.

MARKET SEGMENTATION

This research report on the Latin American construction market is segmented and sub-segmented into the following categories.

By Type of Construction

- Building Construction

- Heavy and Civil Engineering Construction

- Specialty Trade Contractors

- Land Planning and Development

By End-Use Sector

- Private

- Public

By Contractor Type

- Large Contractor

- Small Contractor

By Country

- Brazil

- Mexico

- Argentina

- Colombia

- Chile

- Others

Frequently Asked Questions

What is the size of the Latin America Construction Market in 2025?

The Latin America Construction Market is projected to be worth around USD 1.13 billion in 2025, showing steady growth from previous years.

What is the expected growth rate of this market?

The market is expected to grow at a compound annual growth rate (CAGR) of about 5% through 2030, driven by infrastructure and housing demand.

Which sectors are driving the construction growth in Latin America?

Residential housing dominates the market, supported by rising urbanization, while energy, infrastructure, and hospitality construction are also expanding swiftly.

Who are the major players in the Latin America construction industry?

Key companies include Sigdo Koppers, Techint Ingeniería, Sacyr, and MRV Engenharia among other regional and multinational firms.

What role do governments play in this market?

Governments actively invest in infrastructure projects and implement supportive policies, fueling growth and opening opportunities for private investors.

How is sustainability affecting the construction market?

Sustainability trends like green building materials and energy-efficient designs are increasingly shaping projects across Latin America.

What challenges does the construction market face in Latin America?

Regulatory complexities, long permitting times, and the need for skilled labor remain challenges despite the sector’s growth potential.

Are there any notable infrastructure projects underway?

Yes, several major initiatives include smart city developments, renewable energy plants, and urban transit modernization across the region.

How is technology changing construction in Latin America?

Adoption of BIM, AI, and IoT technology is improving project efficiency, collaboration, and overall infrastructure management in the construction industry.

What opportunities exist for foreign investors?

Rising urban populations and government-backed projects provide attractive investment opportunities, particularly in residential and infrastructure sectors.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com