Global Mental Health Software Market Size, Share, Trends & Growth Forecast Report By Component (Support Services, Integrated Software and Standalone Software), Delivery Model (Subscription Models and Ownership Models), Functionality (Clinical Functionality, Administrative Functionality and Financial Functionality), End-User (Hospitals, Private Practices, Patients and Payers) and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis (2025 to 2033)

Global Mental Health Software Market Summary

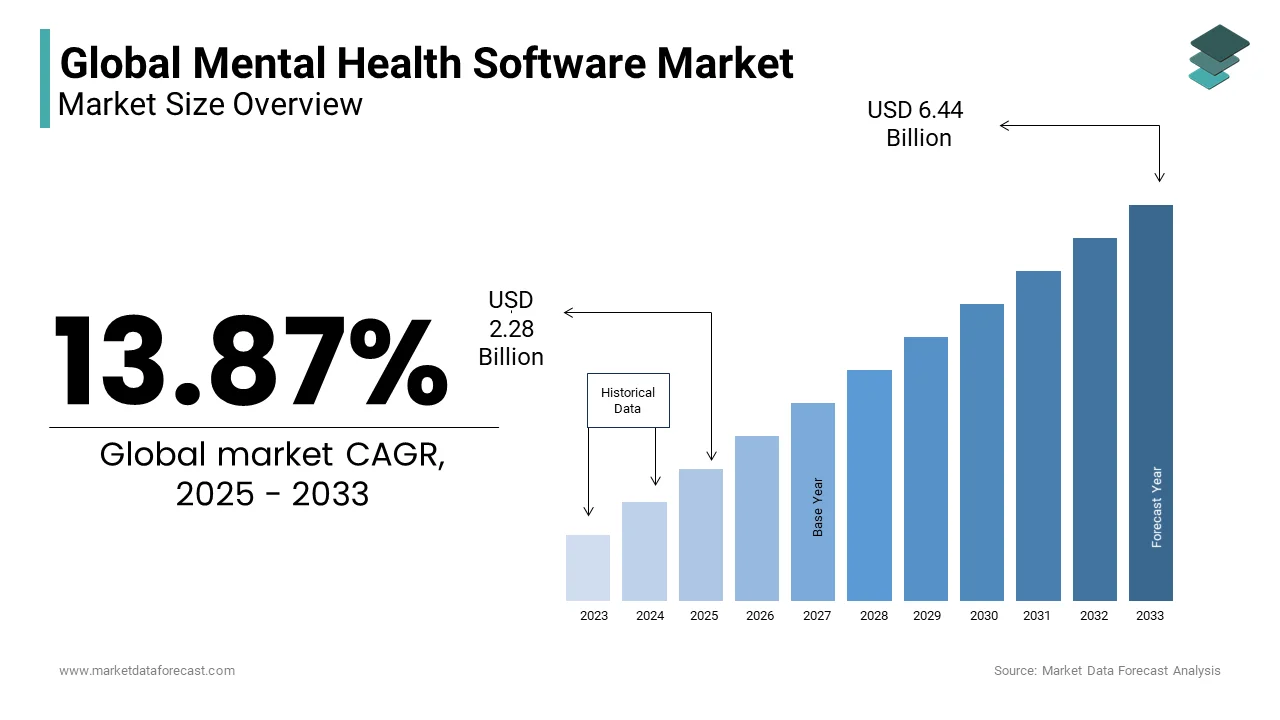

The global mental health software market was valued at USD 2 billion in 2024 and is projected to reach USD 6.44 billion by 2033, growing at a CAGR of 13.87% from 2024 to 2033. The growth of the global mental health software market is driven by the rising prevalence of mental health disorders, increasing demand for telehealth solutions, and growing adoption of electronic health records (EHRs) tailored for behavioral and mental health practices. Additionally, government initiatives promoting mental health awareness and funding for digital health infrastructure are further fueling market expansion.

Key Market Trends

- Rising use of integrated mental health software platforms for improved interoperability.

- Increasing adoption of the subscription delivery model, offering flexibility and cost efficiency.

- Growing demand for clinical functionality tools to support diagnosis, treatment, and patient management.

- Expansion of telepsychiatry and teletherapy platforms in response to rising demand for remote care.

- Strong investments in AI- and analytics-driven mental health solutions.

Segmental Insights

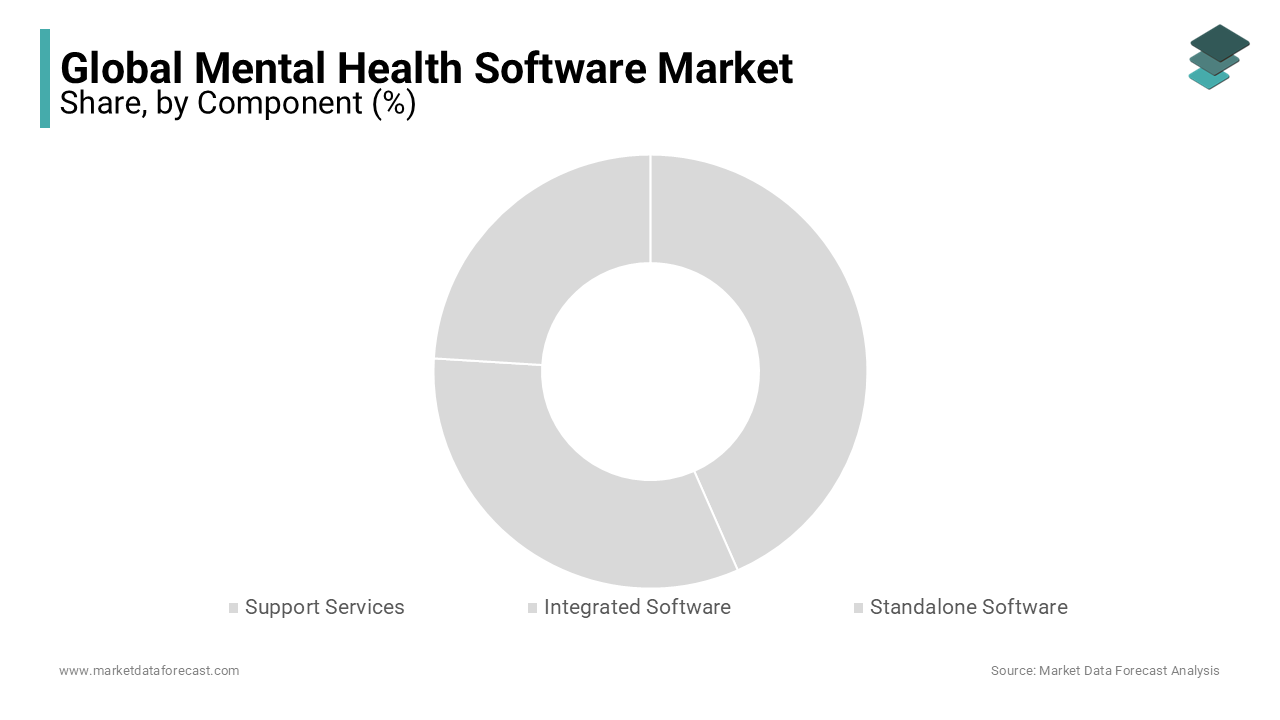

- Based on component, the integrated software segment led the market with 47.3% share in 2024, reflecting its role in providing unified care solutions.

- Based on delivery model, the subscription model segment dominated with 63.6% share in 2024, supported by its affordability and scalability for providers.

- Based on functionality, the clinical functionality segment accounted for 52.3% of the global share in 2024, highlighting its importance in patient care and clinical workflows.

- Based on end user, the hospitals segment held the largest share at 44.5% in 2024, owing to high adoption of digital tools for mental health management.

Regional Insights

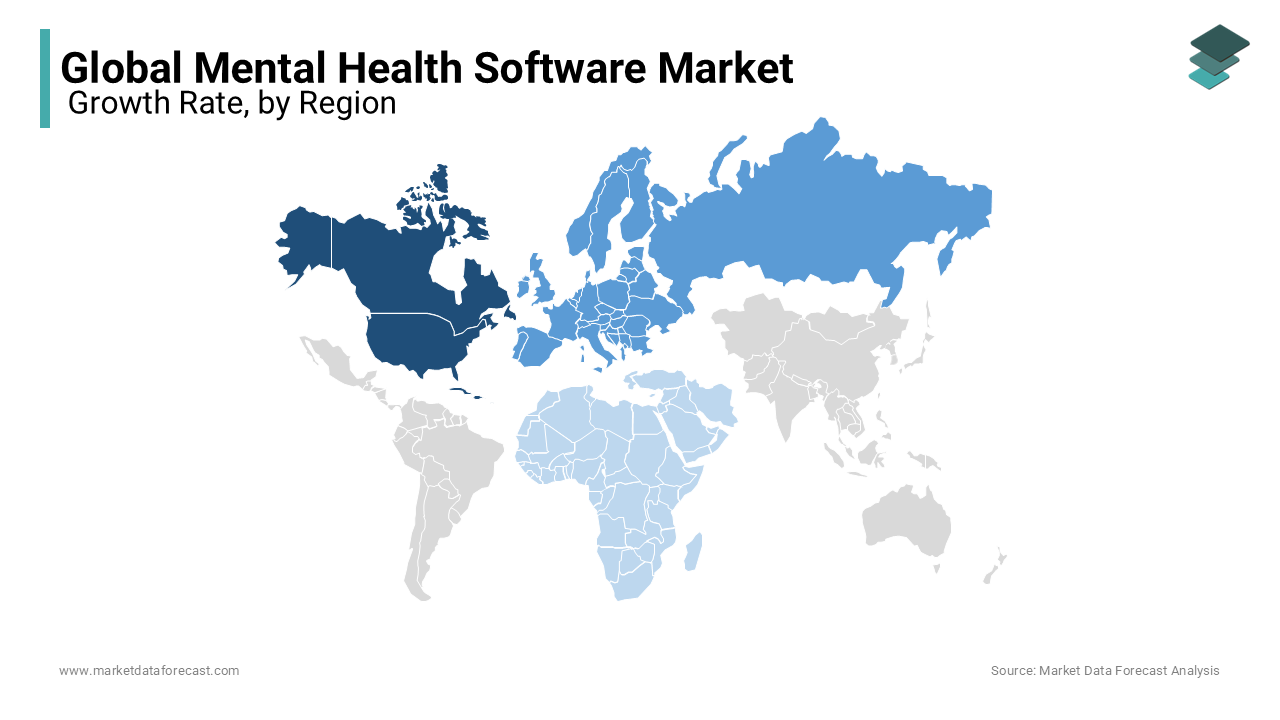

- North America occupied the leading position in the global mental health software market in 2024 with 46.1% share, driven by advanced healthcare IT adoption, supportive government policies, and strong investments in mental health initiatives.

- Europe is showing steady growth, supported by rising mental health awareness programs and the adoption of digital healthcare solutions.

- Asia-Pacific is expected to grow at the fastest CAGR, fueled by increasing healthcare digitization, government-led telehealth initiatives, and growing mental health awareness.

- Latin America and the Middle East & Africa are emerging markets, supported by rising investments in digital health infrastructure and growing demand for accessible mental health services.

Competitive Landscape

Key players in the global mental health software market include Cerner Corporation (US), Core Solutions (US), Credible Behavioral Health (US), MindLinc (US), Epic Systems Corporation (US), Netsmart Technologies (US), NextGen Healthcare Information Systems LLC (US), Qualifacts (US), The Echo Group (US), Valant Medical Solutions Inc. (US), and Welligent (US). These companies are focusing on cloud-based solutions, AI integration, and strategic collaborations with healthcare providers to expand their global footprint.

Global Mental Health Software Market Size

The global mental health software market size was valued at USD 2 billion in 2024. The mental health software market size is expected to have a 13.87% CAGR from 2025 to 2033 and be worth USD 6.44 billion by 2033 from USD 2.28 billion in 2025.

Mental Health Software is a variety of digital platforms and applications designed to support the assessment, monitoring, treatment, and management of mental health conditions through technology-enabled solutions. These tools range from teletherapy platforms and electronic mental health records (EMHRs) to AI-driven symptom trackers, cognitive behavioral therapy (CBT) applications, and clinician-facing decision support systems. Unlike general healthcare software, mental health-specific platforms are engineered to address the unique requirements of psychological care, including patient confidentiality, mood tracking over time, crisis intervention protocols, and integration with behavioral health workflows.

The growing integration of digital therapeutics into mainstream care models has elevated the role of mental health software from auxiliary tools to essential components of clinical practice. According to the World Health Organization, one in eight people globally lives with a mental disorder, and depression and anxiety alone cost the global economy $1 trillion annually in lost productivity. In addition, healthcare systems are increasingly adopting software solutions to bridge service gaps, especially in rural and underserved regions. The Lancet Psychiatry Commission emphasized in 2023 that digital mental health interventions could extend care access to individuals currently without services, particularly in low-resource settings.

Hence, these developments reflect a paradigm shift where software is no longer merely a support mechanism but a transformative force in democratizing mental healthcare delivery.

MARKET DRIVERS

Escalating Global Prevalence of Mental Health Disorders

The rising incidence of mental health conditions worldwide has become a critical catalyst for the adoption of mental health software, compelling healthcare providers, employers, and governments to seek scalable, accessible solutions.

According to the World Health Organization, reported in 2023, cases of anxiety and depression increased by over 25% globally during the post-pandemic period, with young adults and frontline workers disproportionately affected. Also, in the U.S., the Centers for Disease Control and Prevention disclosed in November 2024 that 18.2% of adults experienced symptoms of anxiety in 2022, compared to 15.6% in 2019, signaling a structural shift in population mental health. For depression symptoms, it grew to 21.4% in 2022 from 18.5%in 2019. This surge has overwhelmed traditional care models, where therapist shortages and long wait times hinder timely intervention.

For instance, in America, largely, the average wait time to see a psychiatrist in urban areas exceeds 25 days, while rural regions face near-total provider deserts. In response, digital platforms such as Talkspace and BetterHelp have reported a significant increase in user enrollment since 2020, illustrating the public’s turn to software-based care.

Educational institutions are also integrating mental health apps into student wellness programs; a high percentage of U.S. universities now offer licensed teletherapy platforms to students. Similarly, corporate wellness programs increasingly include mental health software subscriptions, with Fortune 500 companies reporting a notable rise in digital mental health benefits adoption between 2021 and 2023. Therefore, these trends underscore how the growing burden of mental illness is no longer just a clinical issue but a systemic challenge driving technological innovation and institutional investment in scalable digital care models.

Institutional Adoption of Digital Therapeutics and Prescribable Software

The formal recognition and clinical integration of digital therapeutics (DTx) as evidence-based, prescribable interventions is a transformative driver of the Mental Health Software Market. Regulatory bodies such as the U.S. Food and Drug Administration have cleared several software products as medical devices for treating conditions like insomnia, ADHD, and major depressive disorder, legitimizing their use within clinical pathways.

Like, the FDA granted 510(k) clearance to Pear Therapeutics’ reSET-O, a prescription digital therapeutic for opioid use disorder, marking a significant step in software-as-treatment validation. Similarly, Germany’s DiGA (Digital Health Applications) framework allows physicians to prescribe approved mental health apps that are reimbursed by statutory health insurers. This institutional endorsement enables sustainable reimbursement models, encouraging developers to pursue rigorous clinical trials.

For example, Woebot Health’s AI-powered CBT chatbot demonstrated a reduction in PHQ-9 depression scores in a randomized controlled trial published in JMIR Mental Health. So, these developments reflect a fundamental shift: mental health software is no longer viewed as a self-help tool but as a clinically validated modality integrated into treatment plans, driving demand from providers, payers, and patients alike.

MARKET RESTRAINTS

Persistent Stigma and Low Patient Engagement in Digital Mental Health Platforms

The widespread stigma associated with mental health conditions continues to impede user adoption and sustained engagement with mental health software. Cultural taboos, fear of professional repercussions, and concerns about privacy deter individuals from seeking help, even when digital tools are readily available. This reluctance extends to digital platforms: most users who downloaded mental health apps discontinued use within two weeks, often due to emotional discomfort or perceived ineffectiveness. In workplace settings, despite employer-provided mental health software, participation rates remain low; a smaller share of employees utilize company-offered digital therapy benefits, fearing confidentiality breaches or career implications. Educational institutions face similar challenges. Moreover, marginalized communities, including men and ethnic minorities, exhibit disproportionately lower engagement. These behavioral and cultural barriers limit the scalability of mental health software, regardless of technological capability, and underscore the need for broader societal efforts to normalize mental health care and build trust in digital solutions.

Fragmented Regulatory Landscapes and Lack of Standardized Validation Protocols

The absence of harmonized global regulations for mental health software poses a significant barrier to market expansion and clinical integration. While some countries have established frameworks for evaluating digital therapeutics, others lack clear guidelines, creating uncertainty for developers and healthcare providers.

The U.S. FDA has a defined pathway for software as a medical device (SaMD), but approval timelines can exceed several months, discouraging smaller innovators. In contrast, many Asian and African nations have no formal regulatory classification for mental health apps, allowing unvalidated products to enter the market unchecked. This disparity leads to a proliferation of low-quality applications: a large number of top-downloaded mental health apps on commercial stores lacked clinical validation or peer-reviewed evidence.

Besides, reimbursement policies remain inconsistent; while Germany’s DiGA program covers approved apps, France and Italy have yet to implement nationwide reimbursement mechanisms, limiting provider adoption. The European Medicines Agency has called for unified standards, but progress remains slow. The lack of standardized efficacy metrics further complicates evaluation; a study by Nature Digital Medicine in 2023 revealed that clinical trials for mental health apps used many different outcome measures, making cross-product comparisons unreliable. These regulatory and methodological inconsistencies hinder trust, investment, and equitable access, constraining the market’s potential despite growing clinical demand.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Personalized Mental Health Interventions

The convergence of artificial intelligence and behavioral science presents a transformative opportunity for mental health software by enabling hyper-personalized, adaptive treatment pathways. AI-driven platforms can analyze user inputs, such as mood logs, speech patterns, and behavioral data, to deliver tailored therapeutic content, predict symptom escalation, and recommend timely interventions.

Woebot Health’s conversational AI engine, for example, uses natural language processing to engage users in evidence-based CBT dialogues, adapting responses based on emotional tone and context. Similarly, Kintsugi, a voice-based AI tool, can detect signs of depression with high accuracy by analyzing vocal biomarkers during phone calls. These capabilities allow for passive monitoring and early intervention, particularly valuable in preventive care.

Employers are increasingly adopting AI-powered mental health platforms to identify at-risk employees; its AI-driven wellness program reduced absenteeism across large number of employees. Academic institutions are piloting AI chatbots to support student mental health. As machine learning models improve through real-world data, the potential for scalable, individualized care grows, positioning AI not as a replacement for clinicians but as a force multiplier in extending the reach and precision of mental health support.

Expansion of Mental Health Software in Educational and Corporate Wellness Programs

Educational institutions and corporations are emerging as pivotal adoption hubs for mental health software, driven by rising awareness of psychological well-being and its impact on performance and retention. Schools and universities are integrating digital platforms into student support systems to address growing mental health crises among youth. Platforms like Mantra Health and TimelyCare are now embedded in several university health systems, providing on-demand therapy and psychiatric consultations.

In the corporate sector, mental health software is becoming a cornerstone of employee wellness strategies. Salesforce, for instance, offers its employees access to Ginger (now Headspace Care), which combines AI coaching with licensed therapist support, resulting in a decrease in self-reported stress levels within one year. These institutional deployments provide stable revenue streams for vendors and create scalable distribution channels, transforming mental health software from a consumer-driven niche into an enterprise-grade solution with measurable organizational impact.

MARKET CHALLENGES

Ensuring Data Privacy and Security in Sensitive Mental Health Data Handling

The highly sensitive nature of mental health data presents a critical challenge for software providers, as breaches can lead to severe personal, professional, and legal consequences for users. Unlike general health data, psychological records often contain deeply personal disclosures, suicidal ideation, and trauma histories, necessitating the highest levels of encryption, access control, and auditability. However, many consumer-facing apps operate under weak privacy policies: many of the popular mental health apps share user data with third parties, including advertisers and data brokers, often without explicit consent.

Data breaches involving mental health platforms between 2021 and 2023 affected millions of individuals, with ransomware attacks increasingly targeting behavioral health clinics. In Europe, the European Data Protection Board has issued multiple warnings about non-compliance with GDPR in digital therapy apps, particularly concerning cross-border data transfers. The sensitivity of voice and text inputs in AI-driven tools further complicates security; recordings of therapy sessions or mood journals, if intercepted, could be weaponized for blackmail or discrimination.

Also, only a limited percentage of mental health apps use end-to-end encryption, leaving the majority vulnerable to unauthorized access. As regulatory scrutiny intensifies and public awareness grows, software vendors must invest in zero-trust architectures, transparent data governance, and independent security audits to maintain user trust and avoid reputational and legal fallout.

Demonstrating Clinical Efficacy and Achieving Reimbursement Parity

The difficulty in proving clinical efficacy to healthcare payers and regulatory bodies, which directly impacts reimbursement and widespread adoption, is a fundamental challenge facing the Mental Health Software Market. While numerous apps claim therapeutic benefits, few undergo rigorous, peer-reviewed clinical trials that meet medical standards.

Like, just 2% or 3-4% of the 10,000 mental health apps available on major app stores have been evaluated in randomized controlled trials. Without robust evidence, insurers are reluctant to cover digital interventions, limiting patient access. In the U.S., Medicare and most private insurers do not reimburse standalone mental health apps, creating a financial barrier despite FDA clearance. Even when evidence exists, the pathway to reimbursement remains complex. Besides, outcome measurement is inconsistent apps use varying scales and endpoints, making it difficult to compare effectiveness. The lack of long-term data further undermines credibility; most of the efficacy trials for mental health software lasted a few weeks, insufficient to assess the durability of benefits.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Component, Delivery Model, Functionality, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Cerner Corporation (U.S.), Core Solutions (U.S.), Credible Behavioral Health (U.S.), MindLinc (U.S.), Epic Systems Corporation (U.S.), Netsmart Technologies (U.S.), NextGen Healthcare Information Systems, LLC (U.S.), Qualifacts (U.S.), The Echo Group (U.S.), Valant Medical Solutions Inc. (U.S.) and Welligent (U.S.). |

SEGMENTAL ANALYSIS

By Component Insights

The Integrated Software segment held the largest share of the Mental Health Software Market with 47.3% of total revenue in 2024. This dominance of the segment is due to the increasing demand for unified platforms that consolidate clinical, administrative, and billing functions into a single ecosystem, enabling seamless care coordination and operational efficiency. A further driver of this trend is the shift toward value-based care models, which require holistic data integration across patient touchpoints. These platforms allow clinicians to access comprehensive patient histories, including therapy notes, medication logs, and progress assessments, within a unified interface, reducing documentation burden and minimizing errors. An additional critical factor is interoperability with electronic health records (EHRs) and health information exchanges (HIEs). Many behavioral health clinics using integrated software reported successful data exchange with primary care providers, a crucial advancement in addressing the historical fragmentation between physical and mental healthcare. Institutions such as Kaiser Permanente have demonstrated that integrated systems reduce hospitalization rates for depression through early intervention alerts and coordinated care planning. Furthermore, integrated platforms support compliance with regulatory mandates such as MIPS and HIPAA by embedding audit trails, consent management, and secure messaging. These capabilities make integrated software indispensable for large clinics, hospital networks, and accountable care organizations striving for coordinated, data-driven mental health delivery.

The Standalone Software segment is experiencing the fastest growth, projected to expand at a CAGR of 28.3% from 2025 to 2033. The surge of this segment is fueled by the rising adoption of specialized, condition-specific applications that offer targeted therapeutic interventions outside traditional clinical workflows. Also, a major driver is the proliferation of prescription digital therapeutics (PDTs) approved by regulatory bodies such as the U.S. Food and Drug Administration. Like, the FDA cleared EndeavorRx as the first video game-based treatment for pediatric ADHD, marking a new class of standalone software with clinical validation. These apps function independently of EHRs, delivering cognitive behavioral therapy, mindfulness exercises, or biofeedback training directly to users via smartphones or tablets. A further key factor is their accessibility in underserved regions where integrated systems are cost-prohibitive. Also, standalone mental health apps reached a large millions of users in low- and middle-income countries, where infrastructure limitations prevent EHR deployment. Additionally, employers and educational institutions are deploying standalone tools for preventive care; it has been found that students using a standalone mindfulness app experienced a reduction in perceived stress levels during exam periods. The flexibility, scalability, and lower entry barriers of standalone software make it a rapidly expanding frontier in digital mental health innovation.

By Delivery Model Insights

The Subscription Model segment dominated the Mental Health Software Market by accounting for 63.6% of total delivery-based revenue in 2024. This lead position is driven by the growing preference among healthcare providers and institutions for predictable, low-capital-cost access to continuously updated software solutions. A further principal factor behind this shift is the rapid evolution of cybersecurity threats and regulatory requirements, necessitating frequent software updates and patches. A notable share of behavioral health clinics experienced ransomware attacks between 2021 and 2023, prompting a move toward subscription-based platforms that include automatic security upgrades and compliance monitoring. Subscription models also align with cloud-based infrastructure, enabling remote access, real-time data synchronization, and disaster recovery features critical for telehealth expansion. A high percentage of mental health providers using subscription-based software reported improved uptime and reduced IT overhead compared to on-premise systems. An additional driving force is the integration of artificial intelligence and machine learning, which requires continuous training and model refinement. Vendors such as Ginger and Talkiatry offer subscription packages that include AI-driven symptom tracking, therapist matching, and predictive analytics, features that are impractical to maintain under ownership models. Additionally, the subscription approach supports scalability for growing practices; small clinics adopting subscription platforms achieved faster onboarding and deployment than those purchasing perpetual licenses. With built-in support, training, and feature enhancements, the subscription model has become the preferred delivery mechanism for modern, agile mental health care environments.

The Ownership Model is witnessing renewed interest, particularly in specialized institutional settings, and is projected to grow at a CAGR of 12.7% during the forecast period. This model is expanding due to increasing demand for data sovereignty, long-term cost control, and operational autonomy in high-security environments. An additional driver is the need for complete control over sensitive patient data in government-run and military behavioral health programs. A further factor is the financial calculus of large healthcare systems with stable IT infrastructures. Additionally, ownership allows for deep customization to fit unique clinical workflows; the Mayo Clinic reported in 2024 that its proprietary mental health software reduced clinician documentation time through tailored templates and integrations. Though less common in small practices, the ownership model remains vital for organizations prioritizing data control, regulatory compliance, and long-term operational independence.

By Functionality Insights

The Clinical Functionality segment commanded the largest share of the Mental Health Software Market by representing 52.3% of total functionality-based revenue in 2024. This dominance of the segment is because of the core purpose of mental health software: to support direct patient care through evidence-based assessment, treatment planning, and outcome tracking. Clinical tools such as digital symptom checkers, therapy progress dashboards, and diagnostic decision aids are essential for accurate and timely interventions. A further driver is the integration of standardized assessment instruments into software workflows. These tools reduce human error and ensure consistency in evaluation across sessions. An additional critical factor is the rise of remote care delivery, which relies heavily on clinical features like secure video conferencing, mood tracking, and asynchronous messaging. Telepsychiatry visits utilized software with real-time clinical documentation, enabling seamless continuity of care. Platforms such as Theranostics and MyStrength incorporate cognitive behavioral therapy modules and relapse prevention plans directly into patient portals, enhancing engagement and adherence. Furthermore, clinical functionality supports crisis intervention. With mental health care increasingly focused on measurable outcomes and personalized treatment, clinical functionality remains the cornerstone of effective digital mental health platforms.

The Administrative Functionality segment is growing at the fastest rate, with a projected CAGR of 26.8%. This acceleration is driven by the urgent need to reduce operational inefficiencies in behavioral health practices, where administrative burdens often exceed those in general medicine. A further factor is the complexity of patient scheduling and intake in mental health, where continuity of care and therapist-patient matching are critical. Software with intelligent scheduling, automated reminders, and digital consent forms has reduced no-show rates. An additional key driver is the integration of patient engagement tools such as pre-visit questionnaires and symptom trackers, which streamline clinical workflows. Practices using administrative functionality tools reduced intake time, allowing clinicians to focus more on therapy. Besides, compliance with regulatory documentation, such as consent for treatment, risk assessments, and session notes, is increasingly managed through automated workflows. Digital administrative tools improved audit readiness in federally funded clinics. As mental health practices scale and face staffing shortages, administrative automation is becoming a strategic imperative, fueling rapid adoption of these capabilities.

By End-User Insights

The hospitals segment represented the prominent end-user in the Mental Health Software Market by holding 44.5% of total share in 2024. This lead position is attributable to the institutional scale, regulatory mandates, and multidisciplinary care models inherent in hospital environments. One more primary drivers is the integration of mental health services into general medical care, particularly in emergency departments and inpatient units. Like, a portion of all ER visits in involved psychiatric complaints, prompting hospitals to deploy software for rapid triage, suicide risk assessment, and care coordination. Platforms like Epic’s Behavioral Health Module are now standard in many of U.S. academic medical centers, enabling real-time data sharing between psychiatrists, social workers, and primary care teams. An additional critical factor is compliance with federal reporting requirements. The Centers for Medicare & Medicaid Services encourages that hospitals participating in value-based programs use certified electronic health record systems to report mental health outcomes, driving adoption of comprehensive software solutions. Moreover, large hospital systems are investing in enterprise-wide digital therapeutics. The need for interoperability, auditability, and centralized governance makes hospitals the most significant adopters of advanced mental health software, particularly those with integrated EHRs and telepsychiatry networks.

The Patients segment is emerging as the fastest-growing end-user category and is projected to expand at a CAGR of 30.1%. This surge is driven by the increasing consumerization of mental health care, where individuals take proactive control of their psychological well-being through self-directed digital tools. A different factor is the widespread availability of mobile-based mental health apps. Platforms like Headspace, Calm, and Wysa have amassed a large million of combined users, reflecting strong consumer demand for accessible, stigma-free support. A further driver is the normalization of mental health discussions, particularly among younger demographics. Employers and insurers are also subsidizing patient access. Additionally, AI-powered chatbots offer 24/7 emotional support, with users interacting with Woebot reporting a reduction in depressive symptoms over weeks. As digital literacy grows and trust in self-guided tools increases, patients are becoming active participants in their care, reshaping the market toward consumer-centric innovation.

REGIONAL ANALYSIS

North America Mental Health Software Market Insights

North America occupied the most influential position in the global Mental Health Software Market by holding 46.1% of total market share in 2024. The region’s position is anchored in its advanced digital health infrastructure, strong regulatory support for digital therapeutics, and high prevalence of mental health conditions. The United States, in particular, has become a hub for innovation, with the Food and Drug Administration establishing a Digital Health Center of Excellence to accelerate the review of mental health software. According to the National Institute of Mental Health, nearly one in five U.S. adults lives with a mental illness, creating urgent demand for scalable solutions. Canada is also advancing digital mental health adoption. The presence of leading vendors such as Talkspace, Ginger, and Akili Interactive, combined with robust venture capital investment, positions North America as the epicenter of market development and clinical validation.

Europe Mental Health Software Market Insights

Europe holds a significant market share. The region’s market status is defined by strong government-led digital health initiatives and a growing emphasis on equitable access to mental healthcare. Germany’s DiGA framework has been a game-changer, allowing physicians to prescribe and insurers to reimburse approved mental health apps, resulting in a large number of prescriptions. Another key driver is cross-border collaboration. France and the Netherlands are also expanding digital care access. However, data sovereignty concerns under GDPR have led to localized hosting requirements, shaping vendor strategies. With strong regulatory frameworks and public funding, Europe is rapidly institutionalizing mental health software as a standard component of care delivery.

Asia-Pacific Mental Health Software Market Insights

Asia-Pacific is key player in the global Mental Health Software Market. The region’s position is characterized by rapid digital adoption, government modernization efforts, and a growing awareness of mental well-being, particularly in urban centers. India’s National Tele-Mental Health Program (e-Sanjeevani) has connected a large number of citizens with counselors across states, marking a major step in bridging rural-urban care gaps. Australia’s Head to Health initiative has funded digital mental health services. Japan has introduced insurance reimbursement for telepsychiatry. However, cultural stigma and fragmented healthcare systems remain barriers. Despite this, the region’s young, tech-savvy population and rising mental health awareness, particularly post-pandemic, are driving demand.

Latin America Mental Health Software Market Insights

Latin America holds a modest but growing share of the global Mental Health Software Market. The region’s market status is shaped by increasing public health investments and the expansion of digital infrastructure in urban healthcare systems. Brazil has emerged as a leader, launching the Telessaúde Brasil Redes program. Chile’s Ministry of Social Development introduced a national digital mental health platform. However, internet access disparities and limited insurance coverage for digital services constrain scalability. Despite challenges, the region’s proactive public health strategies and growing private-sector engagement signal strong potential for future expansion.

Middle East and Africa Mental Health Software Market Insights

Middle East and Africa collectively account for a small share of the global Mental Health Software Market. The region’s market status is marked by emerging digital health strategies in the Gulf and grassroots innovation in parts of sub-Saharan Africa. The United Arab Emirates leads with its National Strategy for Wellbeing 2031, which includes digital mental health as a priority; Dubai’s Smart Dubai initiative has integrated AI-powered emotional well-being chatbots into its government services portal. Saudi Arabia’s Vision 2030 includes a digital transformation of healthcare. However, regulatory frameworks and funding remain underdeveloped. With increasing recognition of mental health as a public priority, the region is poised for a gradual but meaningful digital transformation in behavioral care.

KEY MARKET PLAYERS

Some of the notable companies operating in the global behavior/mental health software market profiled in the report are Cerner Corporation (U.S.), Core Solutions (U.S.), Credible Behavioral Health (U.S.), MindLinc (U.S.), Epic Systems Corporation (U.S.), Netsmart Technologies (U.S.), NextGen Healthcare Information Systems, LLC (U.S.), Qualifacts (U.S.), The Echo Group (U.S.), Valant Medical Solutions Inc. (U.S.) and Welligent (U.S.).

TOP LEADING PLAYERS IN THE MARKET

Pear Therapeutics

Pear Therapeutics has emerged as a pioneering force in the mental health software landscape by redefining the boundaries of digital therapeutics. The company specializes in developing FDA-authorized prescription software treatments for serious psychiatric and neurological conditions, positioning itself at the intersection of clinical medicine and technology. Its flagship products integrate cognitive behavioral therapy, real-time patient monitoring, and clinician dashboards to deliver structured, evidence-based interventions. Pear’s approach emphasizes regulatory rigor, clinical validation, and integration into traditional care pathways, setting a benchmark for medical-grade software. By collaborating with healthcare providers, payers, and pharmaceutical companies, Pear has helped institutionalize the concept of software as a treatment modality, influencing policy and reimbursement models. Its work has catalyzed broader acceptance of digital therapeutics within the medical community, making it a trailblazer in transforming how mental health care is prescribed, delivered, and monitored in modern clinical settings.

Akili Interactive

Akili Interactive is revolutionizing mental health treatment through the development of cognitive-based digital therapeutics that leverage interactive technology to address neurocognitive disorders. The company is best known for EndeavorRx, the first FDA-approved video game treatment for pediatric ADHD, which exemplifies its innovative approach to blending neuroscience with engaging digital experiences. Akili’s platform is designed to improve attention function through adaptive sensory stimuli and real-time performance feedback, offering a non-pharmaceutical intervention backed by clinical research. The company places strong emphasis on scientific validation, conducting rigorous trials to demonstrate efficacy and safety. Its technology is being explored for applications in depression, autism, and PTSD, expanding the scope of digital therapeutics beyond traditional boundaries. Akili’s success in gaining regulatory approval and payer recognition has positioned it as a leader in the prescription software space, challenging conventional treatment paradigms and opening new avenues for patient engagement and cognitive rehabilitation in mental health care.

Talkspace

Talkspace has played a transformative role in democratizing access to mental health care by offering an accessible, user-friendly teletherapy platform that connects individuals with licensed therapists through text, video, and voice messaging. The company has helped normalize digital mental health services by prioritizing convenience, privacy, and flexibility, making therapy more approachable for people who might otherwise avoid traditional in-person sessions. Talkspace partners with employers, health plans, and healthcare systems to integrate its services into broader employee wellness and patient care programs, significantly expanding its reach. Its platform supports a range of therapeutic modalities and specializes in addressing anxiety, depression, and stress-related conditions. By reducing logistical barriers such as scheduling conflicts and geographic limitations, Talkspace has become a key player in the consumer-driven mental health movement. Its influence extends beyond service delivery, shaping public perception of digital therapy and encouraging other providers to adopt flexible, patient-centered models in the evolving behavioral health ecosystem.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the most impactful strategies employed by leading mental health software companies is the pursuit of regulatory authorization and clinical validation to position their products as medical-grade interventions. By securing approvals from agencies such as the U.S. FDA or inclusion in national health programs like Germany’s DiGA, companies elevate their credibility and enable reimbursement, transforming their offerings from wellness apps into prescribed treatments. This strategy not only differentiates them from consumer-grade tools but also facilitates integration into formal healthcare systems.

Another critical approach is strategic partnerships with healthcare providers, insurers, and pharmaceutical companies to embed mental health software into existing care delivery models. Collaborations with hospitals, employer wellness programs, and payer networks allow vendors to scale rapidly, ensure sustainable adoption, and align with clinical workflows, enhancing both accessibility and treatment continuity.

A third major strategy is the integration of artificial intelligence and adaptive learning technologies to personalize user experiences and improve therapeutic outcomes. Companies are leveraging AI to analyze behavioral patterns, predict symptom escalation, and tailor interventions in real time, enhancing engagement and efficacy. This technological sophistication enables proactive care delivery and supports long-term user retention, reinforcing the clinical value of digital mental health platforms.

COMPETITION OVERVIEW

The competitive dynamics of the Mental Health Software Market are defined by a convergence of clinical innovation, regulatory navigation, and user-centric design. Market leaders are no longer just technology firms but hybrid entities that blend medical expertise with digital engineering to create clinically meaningful solutions. Competition is intensifying between specialized digital therapeutics developers, teletherapy platforms, and integrated health IT providers, each vying for dominance in a rapidly evolving landscape. Differentiation is achieved through regulatory milestones, such as FDA clearance or reimbursement eligibility, which confer legitimacy and enable market access. Companies are also competing on the depth of clinical validation, with peer-reviewed studies and randomized trials becoming essential for credibility. The integration of AI, real-time monitoring, and personalized treatment pathways further separates advanced platforms from generic wellness apps. At the same time, user experience, data privacy, and cultural sensitivity play crucial roles in adoption, particularly among diverse and global populations. Strategic alliances with healthcare systems, insurers, and government programs are reshaping market positioning, turning software from a standalone tool into a systemic component of care delivery. As the line between digital and clinical care continues to blur, competition is shifting from feature sets to trust, efficacy, and seamless integration into the fabric of mental health ecosystems.

RECENT MARKET DEVELOPMENTS

- In February 2024, Pear Therapeutics launched a new digital therapeutic for treatment-resistant depression in collaboration with a major pharmaceutical company, integrating its software with pharmacological treatment protocols to enhance clinical outcomes.

- In May 2024, Akili Interactive partnered with a national health system to deploy its cognitive training platform in pediatric clinics across 15 states, expanding access to its FDA-authorized ADHD treatment for underserved communities.

- In January 2024, Talkspace introduced a new enterprise-focused mental health suite for employers, featuring manager training modules and team well-being analytics, strengthening its presence in corporate wellness programs.

- In March 2024, Headspace Health merged its clinical and consumer platforms into a unified digital care model, enabling seamless transitions between self-guided and therapist-led care for improved patient engagement.

- In June 2024, Mindstrong Health integrated its behavioral analytics engine with a leading electronic health record provider, allowing real-time symptom tracking data to be shared securely with clinicians during patient visits.

MARKET SEGMENTATION

This research report on the global mental health software market has been segmented and sub-segmented based on the component, delivery model, functionality, end-user, and region.

By Component

- Support Services

- Integrated Software

- Standalone Software

By Delivery Model

- Subscription Models

- Ownership Models

By Functionality

- Clinical Functionality

- Electronic Health Records (EHRs)

- Clinical Decision Support (CDS)

- Care Plans/Health Management

- E-Prescribing

- Telehealth

- Administrative Functionality

- Patient/Client Scheduling

- Document/Image Management

- Case Management

- Workforce Management

- Business Intelligence (BI)

- Financial Functionality

- Revenue Cycle Management

- Managed Care

- Accounts Payable/General Ledger

- Managed Care

By End-User

- Hospitals

- Private Practices

- Patients

- Payers

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. Which product segment will dominate the behavioral health software market in the future?

The integrated Software segment will dominate the Behaviour/Mental health software market in future.

2. Which region holds the largest share in the flexible heater market?

Asia-Pacific is the leading region, primarily due to its large concentration of manufacturing industries.

3. What is the projected market value of Behavior/Mental Health market by 2033?

The Behavior/Mental Health market is growing at a CAGR of 13.87% and is expected to reach USD 6.44 billion by 2033.

4. What are common types of software in this market?

Popular types include EHR systems, telehealth platforms, therapy management apps, digital CBT tools, AI-powered chatbots, and employee wellness software

5. How is AI impacting the Mental Health Software Market?

AI enhances personalized treatment, real-time monitoring, predictive analytics, and virtual mental health support, boosting the effectiveness of these digital solutions.

6. Which disorders does the Mental Health Software Market mainly address?

Key focus areas include depression, anxiety, stress, bipolar disorder, PTSD, and addiction treatment, with software supporting therapy and patient monitoring.

7. How does the Mental Health Software Market benefit patients?

It offers improved access to licensed therapists, anonymity, 24/7 support, reduced stigma, and convenience through remote and app-based therapy services.

8. What are some leading companies in the Mental Health Software Market?

Leading software platforms include BetterHelp, Talkspace, Headspace, Calm, Woebot, and Sanvello, offering various digital mental health tools

9. What role do government initiatives play in this market?

Government funding and policies prioritize mental health digital solutions, fostering innovation, wider adoption, and integration into health systems.

10. What future trends are expected in the Mental Health Software Market?

Trends include deeper AI adoption, integration with wearable devices, personalized care models, and expansion of corporate mental health programs.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com