Middle East Power Generation Market Size, Share, Trends & Growth Forecast Report By Source (Thermal, Renewable, Hydro, Others) and By Geography (United Arab Emirates, Saudi Arabia, Egypt, Jordan) – Industry Analysis and Forecast in Terms of Value (USD), 2026 to 2034

Middle East Power Market Size

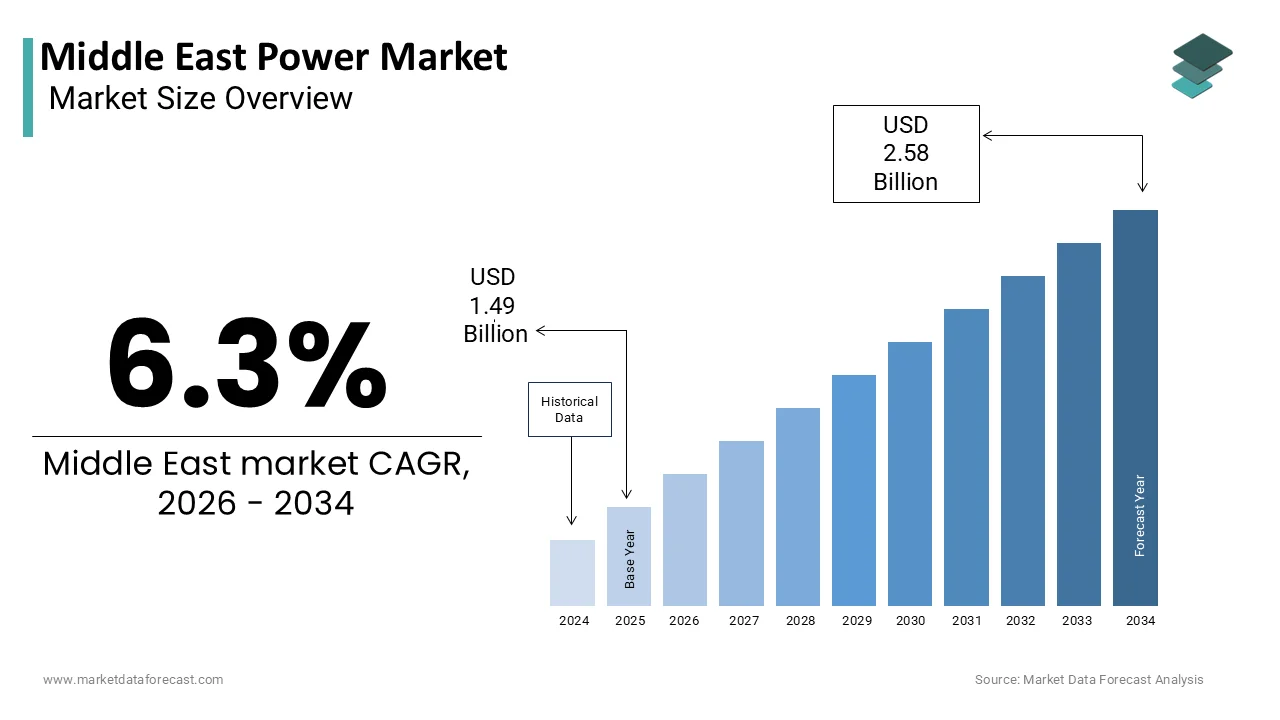

The Middle East power market was worth USD 1.49 billion in 2025, is forecast to reach USD 1.58 billion in 2026, and is expected to hit USD 2.58 billion by 2034, growing at a CAGR of 6.3% from 2026 to 2034.

The power is the generation, transmission, and distribution of electrical energy across a region historically defined by fossil fuel dominance, yet undergoing a strategic transformation toward energy diversification. Characterized by extreme climatic conditions and rapidly expanding urban centers, the region faces unique power demands, particularly during the summer months when cooling needs surge. As per the International Energy Agency, peak electricity demand in the Gulf Cooperation Council (GCC) countries exceeds 160 gigawatts, with air conditioning accounting for nearly 70% of residential load in nations like Saudi Arabia and the UAE.

MARKET DRIVERS

Escalating Cooling Demand Due to Climate and Urbanization

The relentless need for space cooling with rising temperatures and dense urban populations amplifying electricity demand is majorly propelling the growth of the Middle East power market. This thermal stress directly translates into energy load, as air conditioning constitutes up to 75% of household electricity use during peak months. Governments are compelled to expand generation capacity not only to meet current needs but also to pre-empt future shortfalls during prolonged heatwaves by making climate-responsive power planning a strategic imperative.

Industrial and Economic Diversification Initiatives

The ambitious national economic transformation programs are significantly increasing industrial power in countries seeking to reduce oil dependence, and are also accelerating the growth of the Middle East power market. Similarly, the UAE’s focus on advanced manufacturing and hydrogen production is driving energy-intensive investments; the Abu Dhabi National Oil Company launched a green hydrogen facility in 2023 with an expected power draw of 2 gigawatts during full operation. Qatar’s Industrial Strategy 2030 targets a 50% increase in manufacturing output with a robust and reliable electricity supply.

MARKET RESTRAINTS

Water Scarcity Impacting Thermal Power Plant Efficiency

Thermal power generation with the acute water scarcity is affecting plant efficiency and operational continuity, which is degrading the growth of the Middle East power market. In Saudi Arabia, over 60% of desalinated water is used for industrial and power generation purposes, according to the Saline Water Conversion Corporation. In 2022, Kuwait experienced temporary shutdowns at its Doha East Power Plant due to insufficient cooling water supply during a heatwave, as confirmed by the Ministry of Electricity and Water. The interdependence of energy and water systems, which is known as the energy-water nexus, poses a systemic vulnerability and limits the scalability of conventional thermal plants without costly hybrid cooling solutions or alternative technologies.

Grid Infrastructure Limitations in Remote and Expanding Regions

The significant portions of inadequate or aging grid infrastructure in rural and rapidly developing areasares also restraining the growth of the Middle East power market. In Iraq, only 58% of the population had access to a continuous electricity supply in 2023, with transmission losses exceeding 25%, as stated by the Iraqi Ministry of Electricity. In Oman, the Authority for Public Services Regulation noted that 30% of planned renewable energy projects in interior regions faced delays due to insufficient transmission capacity. The physical expansion of grids across desert terrain involves high capital costs and logistical challenges, which are slowing the integration of decentralized generation sources. Additionally, cybersecurity threats to grid systems are rising; the Gulf Cybersecurity Council reported a 40% increase in attempted attacks on energy infrastructure in 2023. These systemic weaknesses hinder the efficient distribution of power and undermine confidence in energy security, limiting the full realization of new generation investments.

MARKET OPPORTUNITIES

Regional Power Interconnection and Cross-Border Trade

The expansion of cross-border electricity interconnections is enhancing energy security and optimizing generation assets, which is prompting the growth of the Middle East power market. The Gulf Cooperation Council (GCC) Interconnection Authority currently links six countries, Saudi Arabia, UAE, Kuwait, Qatar, Bahrain, and Oma,n by enabling a shared peak capacity of 14.5 gigawatts, as per its 2023 operational report. Plans are underway to integrate Jordan and Iraq into the grid, potentially creating a broader Levant-Arab electricity market. These interconnections also facilitate the integration of variable renewable energy by balancing supply across time zones and weather patterns, making them a cornerstone of future energy resilience.

Integration of Solar PV in Distributed and Utility-Scale Applications

The highest solar irradiance levels globally offer unparalleled potential for photovoltaic (PV) energy deployment across both centralized and decentralized systems, which will additionally propel the growth of the Middle East power market. According to the International Renewable Energy Agency, the region receives over 2,500 kilowatt-hours per square meter annually, with Saudi Arabia and the UAE exceeding 2,800. Regulatory support, including net metering and feed-in tariffs, is accelerating adoption. As per the UAE Ministry of Energy, solar is expected to account for 30% of Dubai’s power mix by 2030. The declining cost of PV technology and modular scalability make solar a pivotal tool for meeting rising demand while reducing carbon intensity.

MARKET CHALLENGES

Balancing Energy Subsidies with Fiscal Sustainability

The persistence of widespread electricity subsidies across the Middle East distorts consumption patterns and strains government budgets, which is creating challenges for the growth of the Middle East power market. In Egypt, the government spent approximately EGP 120 billion ($2.5 billion) on electricity subsidies in fiscal year 2022–2023, according to the Ministry of Finance. While subsidies aim to ensure affordability, they discourage energy efficiency and inflate peak demand. Gradual tariff reforms, such as those implemented in Saudi Arabia under the Energy Efficiency Program, have triggered public resistance despite being tied to cash compensation schemes. The political sensitivity of utility pricing makes structural reform difficult, yet fiscally unsustainable.

Workforce Readiness for Technological and Energy Transition

The shift toward smart grids, renewable integration, and digitalized power systems, with the lack of skilled technical personnel, is also hampering the growth ofthe Middle East power market. As per the International Labour Organization, the region faces a deficit of over 150,000 qualified power engineers and technicians needed to support current and planned energy projects by 2030. Training programs are expanding, but curriculum modernization lags behind technological advancements. The deployment of AI-driven grid management systems and battery storage requires expertise largely sourced from abroad. Additionally, cybersecurity demands new skill sets in protecting infrastructure. Universities and vocational institutes are partnering with firms like Siemens and GE to bridge the gap, but systemic workforce development remains a bottleneck to achieving operational excellence in next-generation power systems.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Generation and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Bahrain, Oman, Yemen, Iraq, Iran, Jordan, Lebanon, Syria, Israel, Palestine, Egypt, Turkey. |

| Market Leaders Profiled | JinkoSolar Holding Co Ltd, ACWA Power Barka SAOG, Dubai Electricity and Water Authority, and Eskom Holdings SOC Ltd. |

SEGMENTAL ANALYSIS

By Generation Insights

The thermal power segment accounted for a significant share of the Middle East power market in 2025, with the region’s abundant natural gas and oil reserves, which provide a readily available and historically low-cost fuel source for power plants. In countries like Kuwait and Qatar, natural gas supplies over 95% of electricity generation, according to the U.S. Energy Information Administration. The integration of combined-cycle gas turbine (CCGT) technology has enhanced efficiency, with modern plants achieving thermal efficiencies above 60%, as noted by the International Energy Agency. Additionally, the need for stable, dispatchable power to support air conditioning loads during extreme summer peaks reinforces reliance on thermal generation. Saudi Arabia alone operates over 80 gigawatts of gas-fired capacity thatis managed by the Saudi Electricity Company, ensuring grid stability amid fluctuating demand.

The renewable energy segment is growing lucratively with an expected CAGR of 12.4% during the forecast period, with the region’s exceptional solar irradiation and strategic national commitments to diversify energy sources. Utility-scale solar projects are achieving record-low tariffs; the Dholera Solar Park in the UAE secured a bid of $0.0135 per kWh, among the lowest globally, as confirmed by the Dubai Electricity and Water Authority. IRENA reports that solar photovoltaic (PV) capacity in the Middle East grew from 5.2 GW in 2020 to over 14.8 GW by 2023. Governments are also leveraging public-private partnerships and green financing mechanisms to accelerate deployment.

COUNTRY LEVEL ANALYSIS

Saudi Arabia Power Market Insights

Saudi Arabia was the largest contributor in the Middle East power market with 28.3% ofthe share in 2025. The Saudi Electricity Company manages a generation fleet exceeding 85 gigawatts, with peak demand reaching 72 GW in summer 2023, as reported by the Ministry of Energy. The government has launched multiple renewable tenders, including the 2 GW Sudair Solar Project, one of the world’s largest single-phase solar plants. Additionally, the National Renewable Energy Program has already awarded over 10 GW of clean energy projects.

United Arab Emirates Power Market Insights

The UAE was ranked second in the MEA power market with 19.3% of share in 2025. With its forward-looking energy policies, the UAE has emerged as a regional leader in integrating clean energy into a high-demand urban environment. The Mohammed bin Rashid Al Maktoum Solar Park is set to reach 5 GW by 2030, making it the largest single-site solar project globally, according to the Dubai Electricity and Water Authority.

Egypt Power Market Insights

Egypt's power market growth is growing with a significant CAGR during the forecast period. The country has achieved near-universal electrification, with a 99.8% access rate as of 2023, as reported by the World Bank. The Benban Solar Park, one of the world’s largest photovoltaic installations, contributes 1.8 GW to the national grid, showcasing Egypt’s commitment to renewables. The Ministry of Electricity and Renewable Energy has set a target of 42% renewable energy in the mix by 2030.

Iran Power Market Insights

Iran's power market growth is likely to grow with an installed capacity of over 90 GGW. Iran operates one of the largest power systems in the region, which is primarily fueled by natural gas. Frequent summer blackouts, such as the 2021 nationwide outages triggered by heatwaves and water shortages, are associated with systemic vulnerabilities. Despite these challenges, Iran has developed indigenous hydro and wind capacity, with over 10 GW of hydropower installed across the Zagros Mountains. The country also subsidizes electricity heavily, leading to wasteful consumption patterns. Sanctions have limited access to modern technology, slowing upgrades, yet domestic R&D continues in areas like gas turbine optimization and grid automation.

Iraq Power Market Insights

Iraq's power market growth is anticipated to grow in the coming years. Decades of conflict and underinvestment have left the power sector severely degraded, with generation capacity standing at around 25 GW in 2023, far below the estimated 35 GW needed to meet demand, as reported by the World Bank. The country imports up to 30% of its power from Iran and Turkey to compensate for domestic shortfalls. Reconstruction efforts are underway, supported by international financing; the World Bank approved a $500 million grant in 2023 for grid rehabilitation. Iraq has also launched solar tenders, including a 1 GW project in Anbar Province, signaling a shift toward renewables.

KEY MARKET PLAYERS

Key players in the energy and utilities sector include JinkoSolar Holding Co Ltd, ACWA Power Barka SAOG, Dubai Electricity and Water Authority, and Eskom Holdings SOC Ltd.

TOP LEADING PLAYERS IN THE MARKET

Siemens Energy

Siemens Energy plays a pivotal role in shaping the Middle East power landscape through advanced turbine technology, grid solutions, and decarbonization initiatives. The company has been instrumental in modernizing gas-fired power plants across Saudi Arabia and the UAE, delivering high-efficiency SGT-800 and SGT-700 turbines that enhance fuel utilization and reduce emissions. In 2023, Siemens Energy completed the retrofit of four units at the Qurayyah IPP in Saudi Arabia, boosting output by over 1.2 GW. It is also engaged in hydrogen-ready gas turbine trials in Dubai, supporting the region’s transition to low-carbon fuels. Its collaboration with DEWA on smart grid integration underscores its commitment to future-ready infrastructure. In the Asia Pacific market, Siemens Energy supports LNG-to-power projects in Indonesia and provides grid stabilization solutions in India by leveraging Middle East-proven technologies for similar climatic and demand challenges.

General Electric (GE) Vernova

GE Vernova maintains a deep presence in the Middle East power sector through its gas turbines, grid solutions, and renewable integration expertise. The company powers over 50% of the region’s electricity generation with its HA and F-class turbines, including installations at the UAE’s Hassyan and Saudi Arabia’s Riyadh PP-13 plants. In 2023, GE commissioned the world’s first HA gas turbine running on 100% hydrogen at the Dubai Electricity and Water Authority’s M’Shereib plant, marking a milestone in clean energy innovation. GE also supports grid resilience through its Grid Solutions division, deploying advanced SCADA systems and substation automation in Oman and Kuwait. Its Digital Energy suite enhances predictive maintenance and operational efficiency for utilities. In the Asia Pacific region, GE leverages its Middle East experience to deliver hybrid power solutions in Vietnam and support grid modernization in Japan. Strategic partnerships with local entities, such as Saudi Aramco and ACWA Power, with their long-term engagement and technology localization in the Middle East power market.

ACWA Power

ACWA Power has emerged as a leading developer and operator of power and desalination plants across the Middle East, driving large-scale energy transition through private-sector investment. Headquartered in Saudi Arabia, the company has developed over 70 power projects with a combined capacity exceeding 40 GW across the region. It is best known for pioneering low-cost solar and wind projects, including the 2.6 GW NEOM Green Hydrogen Project and the 1.5 GW Al Kharsaah Solar IPP in Qatar. ACWA Power integrates power generation with water desalination, addressing the region’s energy-water nexus through efficient co-located facilities. In the Asia Pacific market, ACWA Power is entering India and Southeast Asia through renewable energy partnerships, replicating its Middle East success in competitive bidding and project finance models. Its focus on sustainability, innovation, and public-private collaboration continues to redefine power development in high-demand environments.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Middle East power market are adopting multifaceted strategies to consolidate their influence and adapt to evolving energy dynamics. Companies are prioritizing technology localization by establishing regional manufacturing and service hubs to reduce lead times and comply with national content requirements. Strategic partnerships with sovereign wealth funds and national utilities enable access to large-scale tenders and long-term power purchase agreements. Firms are increasingly investing in digitalization, deploying AI-driven asset management and predictive maintenance tools to enhance plant efficiency. Another strategy is participation in green hydrogen ecosystems, where power producers align with industrial decarbonization goals. Additionally, companies are expanding their service portfolios to include lifecycle maintenance and performance guarantees, strengthening client retention. These approaches collectively enhance operational resilience and align with national energy transition roadmaps across the Middle East power market.

COMPETITION OVERVIEW

Competition in the Middle East power market is evolving from a state-dominated, infrastructure-focused landscape to a dynamic arena shaped by technological innovation, private investment, and energy transition goals. Traditional utilities still control generation and distribution, but independent power producers and multinational technology providers are increasingly influencing project execution and operational standards. The entry of global engineering firms like Siemens Energy and GE Vernova has intensified competition in efficiency, emissions reduction, and digital integration. At the same time, regional champions such as ACWA Power and Masdar are leveraging financial strength and local expertise to win major tenders. The rise of competitive bidding for solar and wind projects has driven down tariffs, pressuring developers to optimize costs. Cybersecurity, workforce localization, and ESG compliance are becoming differentiators.

RECENT MARKET DEVELOPMENTS

In October 2022, ACWA Power began commercial operations at the 1.5 GW Al Kharsaah Solar Power Plant in Qatar, one of the largest solar projects in the Gulf, significantly expanding renewable capacity in the Middle East power market.

MARKET SEGMENTATION

This research report on the Middle East and Africa Power Market is segmented and sub-segmented into the following categories.

By Generation

-

Thermal

-

Renewable

-

Hydro

-

Others

By Country

-

United Arab Emirates

-

Saudi Arabia

-

Egypt

-

Jordan

-

Rest ofthe Middle East

Frequently Asked Questions

1. What factors drive growth in the Middle East Power Market?

The Middle East Power Market is fueled by rising electricity demand, urbanization, population growth, and investments in energy infrastructure and renewables.

2. Which countries dominate the Middle East Power Market?

Saudi Arabia and the UAE lead the Middle East Power Market

due to their large-scale investments, high demand, and significant new projects.

3. What energy sources are used in the Middle East Power Market?

The Middle East Power Market uses thermal sources like oil, gas, coal, and renewables such as solar, wind, and hydro for power production.

4. How is renewable energy affecting the Middle East Power Market?

Renewable energy is transforming the Middle East Power Market, increasing solar and wind capacity, and supporting regional energy transition goals.

5. Who are major players in the Middle East Power Market?

Major companies in the Middle East Power Market include Saudi Electricity Company, Dubai Electricity and Water Authority, ACWA Power, and JinkoSolar.

6. What challenges face the Middle East Power Market?

The Middle East Power Market faces challenges like grid reliability, shifting from fossil fuels, regulatory hurdles, and climate change adaptation.

7. What is the growth outlook for the Middle East Power Market?

The Middle East Power Market is expected to grow at over 3% CAGR,

driven by ongoing energy diversification and increased consumption.

8. How is population growth impacting the Middle East Power Market?

Population and rapid urbanization are increasing electricity demand in the Middle East Power Market,

prompting grid expansion and new projects.

9. What role do independent power projects play in the Middle East Power Market?

IPPs are central to the Middle East Power Market, supporting liberalization, efficiency, and fostering public-private partnerships.

10. How important is the oil & gas sector for the Middle East Power Market?

The oil & gas sector supplies fuel for thermal plants and significant revenue,

sustaining traditional power generation in the Middle East Power Market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com