Middle East Retail Market Size, Share, Trends, And Growth Forecast Report By Product, Retail Channel, and Country (KSA, UAE, Israel, South Africa, And Ethiopia, Kenya, Egypt, Sudan, Rest of GCC Countries, and Rest of MEA), Industry Analysis From 2026 to 2034

Middle East Retail Market Size

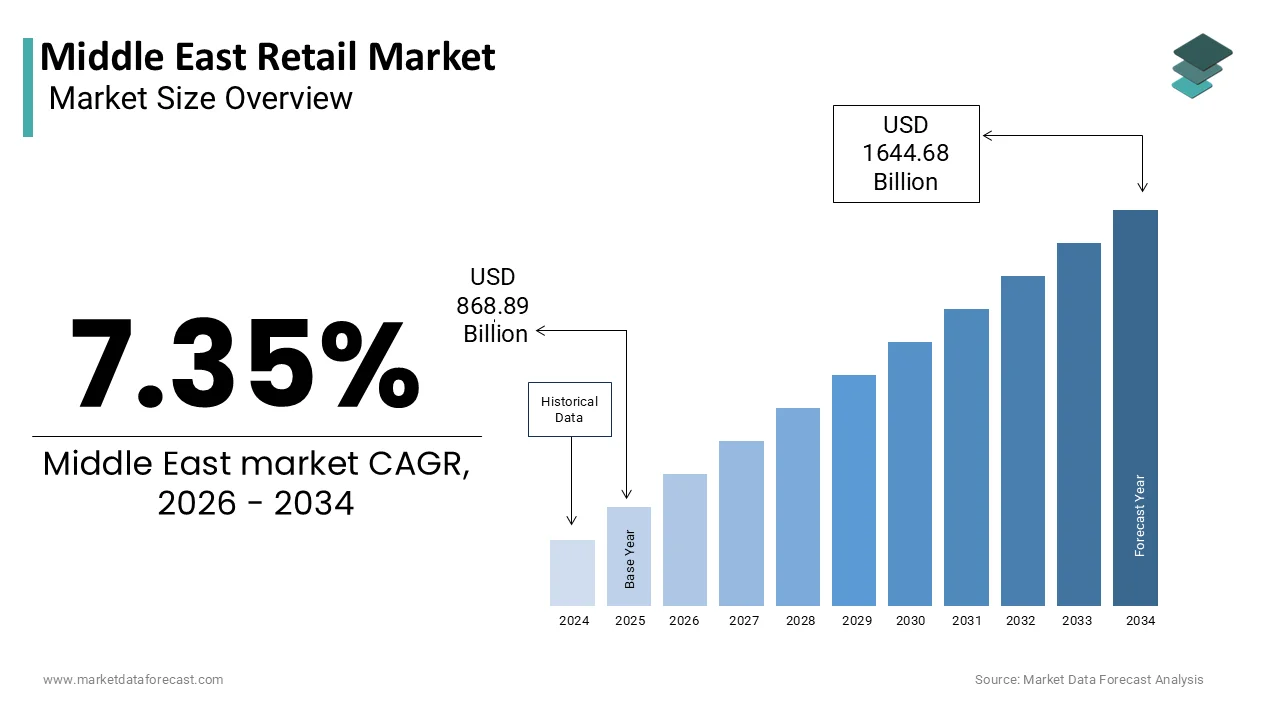

The Middle East retail market size was valued at USD 868.89 billion in 2025 and is anticipated to reach USD 932.54 billion in 2026 and USD 1644.68 billion by 2034, growing at a CAGR of 7.35% during the forecast period from 2026 to 2034.

Retail is a dynamic and rapidly evolving ecosystem of consumer goods distribution across both traditional and modern trade formats, deeply influenced by regional socio-economic structures, cultural preferences, and urban development trajectories. Characterized by a blend of luxury-centric malls in Gulf Cooperation Council (GCC) nations and informal souks in less urbanized areas, the sector reflects stark contrasts in consumer behavior and infrastructure maturity.

MARKET DRIVERS

The region’s youth-dominated demographic structure, which fuels demand for trendy, tech-integrated, and lifestyle-oriented consumption, is enhancing the growth of the Middle East retail market. Over 60% of the population in countries like Saudi Arabia and Egypt is under the age of 30, as reported by the United Nations Department of Economic and Social Affairs in 202,y creating a vast base of digitally fluent consumers who prioritize convenience, brand authenticity, and social engagement in their purchasing decisions. This cohort exhibits strong preferences for international fashion labels, smart devices, and fast-moving consumer goods, often influenced by social media trends. Retailers are responding with hyper-localized store formats, influencer collaborations, and omnichannel experiences tailored to mobile-first behaviors, reinforcing the centrality of generational dynamics in shaping retail evolution across the region.

The expansion of women’s economic participation in the GCC, which has directly increased household discretionary spending and reshaped retail demand patterns, is accelerating the growth of the Middle East retail market. As per data released by the International Labour Organization in 2023, female labor force participation in Saudi Arabia rose to 33.9%, up from just 19% in 2018, reflecting transformative social reforms under Vision 2030. This shift has prompted retailers to redesign store layouts, enhance privacy features, and launch gender-specific marketing campaigns. The growing visibility of female entrepreneurs in retail further amplifies this trend by fostering niche markets in modest fashion, wellness, and home décor.

MARKET RESTRAINTS

The persistent reliance on expatriate consumer spending in oil-dependent economies, which introduces volatility into retail demand, is restricting the growth of the Middle East retail market. In the UAE, expatriates constitute approximately 88% of the population, as stated by the Federal Competitiveness and Statistics Centre in 2023, making retail revenues highly sensitive to employment conditions in sectors like construction, tourism, and finance. Economic downturns or policy changes affecting visa regulations and remittance flows can rapidly diminish purchasing power. This dependency undermines long-term market resilience, as local nationals represent a minority of consumers, limiting organic demand growth and exposing retailers to external labor market fluctuations across Asia and Africa.

The infrastructural imbalance between urban and rural retail ecosystems is also hindering the Middle East retail market’s growth. While cities like Riyadh, Dubai, and Doha boast world-class shopping malls and logistics networks, vast rural and semi-urban areas in countries such as Iraq, Yemen, and even parts of Saudi Arabia lack reliable road connectivity, cold chain systems, and last-mile delivery capabilities. This disparity restricts the reach of formal retailers, forcing reliance on fragmented wholesale networks and informal vendors. Additionally, electricity and internet access remain inconsistent in remote regions, inhibiting the adoption of e-commerce platforms.

MARKET OPPORTUNITIES

The localization of retail offerings to align with cultural and religious values in food, fashion, and personal care is solely to create new opportunities for the growth of the Middle East retail market. Retailers that integrate halal certification, modest design, and Ramadan-specific product lines are gaining a competitive advantage. Furthermore, culturally attuned store environments such as family-only shopping hours and gender-segregated zones are enhancing customer loyalty in Saudi Arabia and Kuwait, where social norms strongly influence retail behavior.

The digital transformation in last-mile logistics presents another strategic opportunity, especially as urban congestion and high delivery expectations reshape consumer expectations, elevating the growth of the Middle East retail market. In response, retailers are investing in micro-fulfillment centers within city limits; for instance, Noon launched urban warehouses in Dubai and Riyadh, reducing average delivery times to under three hours. Additionally, drone and autonomous vehicle trials by companies like Amazon and Saudi Post indicate a shift toward futuristic logistics models.

MARKET CHALLENGES

The escalating competition from unregulated informal retail sectors, which undercut formal players on pricing and flexibility, is quietly restricting the growth of the Middle East retail market. In countries like Lebanon, Jordan, and Egypt, informal markets account for up to 40% of total retail activity, as estimated by the International Finance Corporation in 2023. These vendors operate with minimal overhead, avoid taxation, and offer cash-based transactions, making them highly attractive during periods of economic stress. This trend erodes market share for licensed retailers and complicates pricing strategies. Moreover, the lack of consumer protection in informal channels poses reputational risks, yet their deep community integration makes formalization difficult by creating a persistent structural imbalance.

The vulnerability of retail supply chains to geopolitical disruptions in transit-dependent economies additionally limits the growth of the Middle East retail market. The Middle East relies heavily on maritime trade, with over 80% of consumer goods entering via ports such as Jebel Ali, Jeddah Islamic, and Sohar. However, regional tensions, including conflicts in the Red Sea and the Strait of Hormuz, have repeatedly disrupted shipping routes. These delays impact inventory availability, especially for perishable goods and seasonal merchandise. Retailers in affected nations face stockouts, margin compression, and reduced customer satisfaction with the urgent need for diversified sourcing and regional warehousing strategies to mitigate exposure to volatile trade corridors.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Retail Channel, and By Region |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | KSA, UAE, Israel, the rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, the rest of MEA |

| Market Leaders Profiled | Alshaya Group (Kuwait), Al Futtaim Retail (UAE), BinDawood Stores (Saudi Arabia), Alghanim Industries (Kuwait), LuLu Group International (UAE), Chalhoub Group (UAE), AZADEA Group (UAE), Al Tayer Group (UAE), Landmark Group (UAE), Apparel Group (UAE), |

SEGMENTAL ANALYSIS

By Product Insights

The Food, Beverage, and Grocery segment dominated the Middle East retail market by accounting for 47.3% of the share in 2025, with the essential nature of sustenance-driven consumption, compounded by high population growth and urbanization rates across key markets. According to the Food and Agriculture Organization of the United Nations, the Middle East imports over 50% of its food requirements by making grocery retail a critical node in national supply chains. This dependency has led to strategic investments in cold storage infrastructure and inventory resilience in GCC nations. Additionally, the cultural centrality of food, especially during religious observances such as Ramadan, amplifies seasonal demand surges.

The Personal Care & Healthcare segment is expected to grow with an expected CAGR of 9.4% during the forecast period, with the rising health consciousness and government-led wellness initiatives, particularly in the Gulf states. This policy shift has catalyzed consumer demand for vitamins, supplements, skincare, and hygiene products. Moreover, the surge in dermatological concerns linked to the region’s harsh climate, such as high UV exposure and desert dust, has driven the adoption of premium skincare regimens. The growing influence of beauty social media and homegrown cosmetic brands, which have redefined retail dynamics in personal care, is also leveraging the growth of the Middle East retail market. Instagram and TikTok beauty influencers in the region command millions of followers, with campaigns frequently translating into immediate sales spikes.

By Retail Channel Insights

The supermarkets and hypermarkets segment was the largest by capturing 52.3% of the Middle East retail market share in 2025, with their ability to offer one-stop shopping experiences that align with large household sizes and cultural preferences for bulk purchasing. Hypermarkets such as Carrefour, Lulu, and Spinneys cater to this need by providing extensive product ranges under a single roof, often integrated within mixed-use malls that serve as social hubs. These venues also benefit from economies of scale, enabling competitive pricing and promotional depth, particularly during seasonal festivals like Eid and back-to-school periods.

The e-commerce segment is projected to witness a CAGR of 16.8% during the forecast period, with the digital adoption and evolving consumer expectations. This connectivity, combined with widespread social media usage, has normalized mobile shopping among youth. Platforms like Noon and Amazon.ae have capitalized on this trend by offering localized payment options, cash-on-delivery, and Arabic-language interfaces, reducing digital friction for first-time users. As per the Dubai Logistics Corridor, same-day delivery coverage now spans 92% of urban areas in the UAE. Moreover, drone delivery trials by Emirates Post and autonomous vehicle pilots in Abu Dhabi are setting new benchmarks for speed and efficiency. Consumer trust has also grown: a 2023 PwC Middle East Consumer Insights Survey found that 71% of online shoppers feel confident about product authenticity and return policies.

COUNTRY ANALYSIS

Saudi Arabia was the largest contributor in the Middle East retail market by holding 28.3% of the share in 202,4 with a structural renaissance driven by economic diversification under Vision 2030, which seeks to reduce oil dependency and expand private-sector consumption. Mega-projects like NEOM and the Red Sea Development are integrating luxury retail components, while the expansion of mixed-use giga-malls such as Riyadh Park and Jeddah Season City reflects a shift toward experiential consumption.

The United Arab Emirates was positioned second by holding 22.3% the share in 2025. Dubai and Abu Dhabi function as regional hubs for international brands entering the Arab world, with over 1,200 multinational retailers operating through flagship stores or franchise agreements. According to the Dubai Department of Economy and Tourism, retail sales in Dubai reached $108 billion in 2023, bolstered by tourism, which brought in 14.9 million visitors that year. The government’s push for smart city integration, including cashless payments and AI-driven customer analytics, further enhances retail efficiency by making the UAE a model of innovation and scalability in the regional context.

Israel's retail market growth is likely to grow with its advanced technological integration and high consumer purchasing power. Online retail penetration stands at 12.3%, one of the highest in the region, and is growing at 14% annually, according to Israel’s Central Bureau of Statistics. Major retailers like Shufersal and Rami Levy have integrated smart checkout systems and dynamic pricing algorithms, enhancing operational agility. Moreover, Israel’s robust cybersecurity and fintech ecosystem supports secure digital transactions, fostering consumer confidence. Urban density and high education levels further drive demand for organic, sustainable, and specialty goods, positioning Israel as a niche but influential player in the regional retail landscape.

KEY MARKET PLAYERS

Alshaya Group (Kuwait), Al Futtaim Retail (UAE), BinDawood Stores (Saudi Arabia), Alghanim Industries (Kuwait), LuLu Group International (UAE), Chalhoub Group (UAE), AZADEA Group (UAE), Al Tayer Group (UAE), Landmark Group (UAE), Apparel Group (UAE), are the market players that are dominating the Middle East retail market.

Top Players In The Market

- Majid Al Futtaim Group is a dominant force in the Middle East retail landscape by operating Carrefour under exclusive license across multiple GCC countries. The company has redefined integrated retail through its ownership of shopping malls such as City Centre and My City Centre, combining retail, entertainment, and hospitality under one ecosystem. The group also introduced AI-driven inventory systems and cashless checkout trials in select stores. Committed to sustainability, it launched the “Green Store” initiative, reducing energy consumption by 25% in new outlets.

- Al-Futtaim Group plays a pivotal role in shaping modern retail experiences across the Middle East, particularly through its operation of IKEA in key markets including the UAE, Saudi Arabia, and Egypt. The company has consistently invested in omnichannel integration, launching click-and-collect services and same-day delivery in urban centers. In 2023, Al-Futtaim launched a digital twin of its IKEA Dubai Mall store, allowing customers to navigate and shop virtually. It also partnered with local fintech firms to introduce flexible payment plans, increasing accessibility. The group has expanded its logistics footprint with solar-powered warehouses in Dubai and Abu Dhabi, aligning with regional decarbonization goals.

- Lulu Group International has emerged as a major retail influencer across the Middle East, leveraging its hypermarket model to serve diverse consumer segments. Headquartered in Abu Dhabi, the company operates over 240 stores across 15 countries, with a strong presence in Saudi Arabia, Egypt, and Oman. Lulu has aggressively expanded its e-commerce arm, Lulu Online, integrating AI-powered demand forecasting and drone delivery pilots in select locations. The group also introduced private-label brands across food, personal care, and home goods, improving margins and customer loyalty.

Top Strategies Used By Key Market Participants

Key players in the Middle East retail market are deploying advanced digital integration, omnichannel expansion, and localized product curation to gain a competitive advantage. Companies are investing heavily in AI-driven supply chain optimization, mobile-first platforms, and same-day delivery networks to meet rising consumer expectations. Strategic partnerships with fintech firms enable installment-based payments, broadening access to mid-income shoppers. Retailers are also adopting experiential formats, embedding entertainment, dining, and wellness zones within shopping destinations. Sustainability initiatives, including energy-efficient stores and plastic-free packaging, are increasingly used to appeal to environmentally aware demographics. Localization remains critical, with halal-certified goods, modest fashion lines, and Ramadan-specific assortments driving engagement. Additionally, giga-mall developments linked to tourism and smart city projects reflect long-term positioning in high-growth urban corridors.

COMPETITION OVERVIEW

Competition in the Middle East retail market is intensifying as regional and global players navigate a landscape marked by rapid digitization, shifting consumer expectations, and government-led economic transformation. Traditional dominance by large-format hypermarkets is being challenged by agile e-commerce platforms and specialty retailers offering curated experiences. Domestic conglomerates such as Majid Al Futtaim and Lulu Group face increasing pressure from global entrants like Amazon.ae and international luxury brands expanding physical footprints. Price wars, delivery speed, and personalized marketing have become key battlegrounds. Moreover, regulatory reforms in Saudi Arabia and the UAE are lowering entry barriers, inviting new competitors. The fusion of retail with tourism, entertainment, and real estate development has elevated competition beyond mere product availability to holistic lifestyle branding, making differentiation essential for long-term survival.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Majid Al Futtaim launched Carrefour Green Store in Riyadh, a sustainability-focused hypermarket featuring energy-efficient lighting, solar panels, and zero-waste operations, reinforcing its commitment to eco-friendly retail in Saudi Arabia.

- In September 2023, Lulu Group opened a 500,000-square-foot logistics hub in Jeddah, enhancing supply chain agility and supporting same-day delivery across western Saudi Arabia.

- In February 2025, Noon expanded its grocery delivery service to 20 new cities in Egypt and Pakistan, leveraging AI-driven routing to reduce delivery times to under 90 minutes in major urban centers.

MARKET SEGMENTATION

This research report on the middle east retail market is segmented and sub-segmented into the following categories.

By Product

- Food, Beverage, & Grocery

- Apparel & Accessories

- Personal Care & Healthcare

- Home Care

- Home Décor & Furniture

- Consumer Electronics & Household Appliances

- Others

By Retail Channel

- Supermarket/Hypermarket

- Convenience Stores

- E-Commerce

- Others

By Country

- KSA

- UAE

- Israel

- The rest of the GCC countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- Rest of MEA

Frequently Asked Questions

What is driving the growth of the retail market in the Middle East?

The retail market growth is powered by increasing urbanization, rising disposable incomes, and expanding e-commerce adoption across the region.

Which retail segments are expanding fastest in the Middle East?

Online retail, luxury goods, and convenience stores are the fastest-growing segments driven by tech-savvy consumers and lifestyle changes.

What role does e-commerce play in the Middle East retail sector?

E-commerce is rapidly transforming retail by offering convenience, wide product choices, and competitive pricing, attracting younger shoppers.

How are Middle East consumers' shopping behaviors evolving?

Consumers are increasingly embracing digital channels, valuing personalized experiences, and expecting seamless omnichannel shopping options.

What challenges do retailers face in the Middle East market?

Key challenges include adapting to diverse consumer preferences, logistics complexities, and evolving regulatory environments.

How important is technology adoption for retailers in the Middle East?

Technology adoption is crucial for improving inventory management, customer engagement, and expanding online presence to stay competitive.

Which countries lead the retail market in the Middle East?

The UAE, Saudi Arabia, and Qatar are leaders due to strong economies, infrastructure, and high consumer spending power.

How is sustainability influencing retail in the Middle East?

Sustainability is gaining traction with increasing demand for eco-friendly products and corporate responsibility initiatives among retailers.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com