Global mHealth Market Size, Share, Trends & Growth Analysis Report Segmented By Type (Blood Pressure Monitors, Glucose Meters and Pulse Oximeters), Services (Chronic Care Management, Health and Fitness, Weight Loss, Womens Health, Personal Health Record and Medication), Application (Remote Monitoring, Consultation, Fitness and Wellness and Prevention) & Region – Industry Forecast From 2024 to 2033

Global mHealth Market Summary

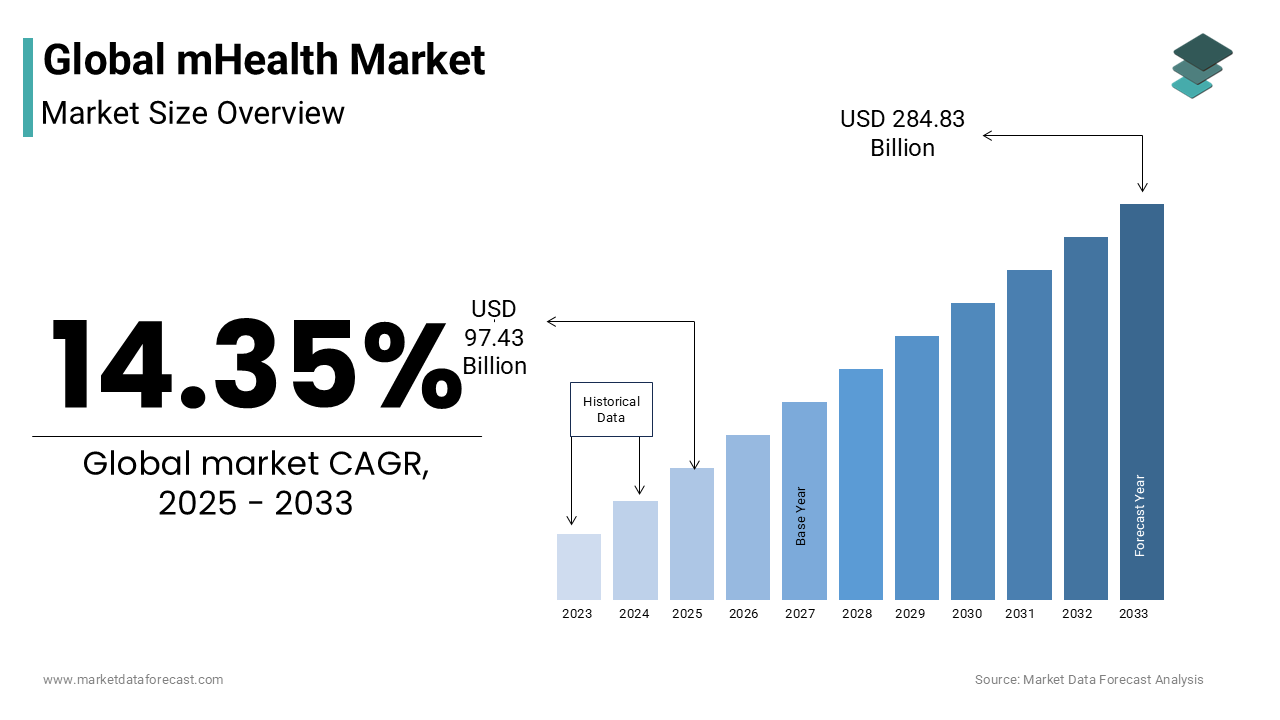

The global mHealth market was valued at USD 85.20 billion in 2024 and is projected to expand to USD 284.83 billion by 2033, registering a CAGR of 14.35% from 2025 to 2033. The growth of the global mHealth market is driven by the rising prevalence of chronic diseases, increasing adoption of smartphones and wearable devices, and growing demand for remote healthcare solutions. Supportive government initiatives, the integration of AI and IoT in healthcare, and increasing focus on preventive care are further fueling market expansion.

Key Market Trends

- Strong adoption of wearable devices and mobile health apps for patient monitoring.

- Increasing role of AI and predictive analytics in chronic disease management.

- Rising demand for remote monitoring services to reduce hospital visits.

- Expansion of telehealth and digital therapeutics platforms.

- Growth in personalized healthcare solutions powered by real-time health data.

Segmental Insights

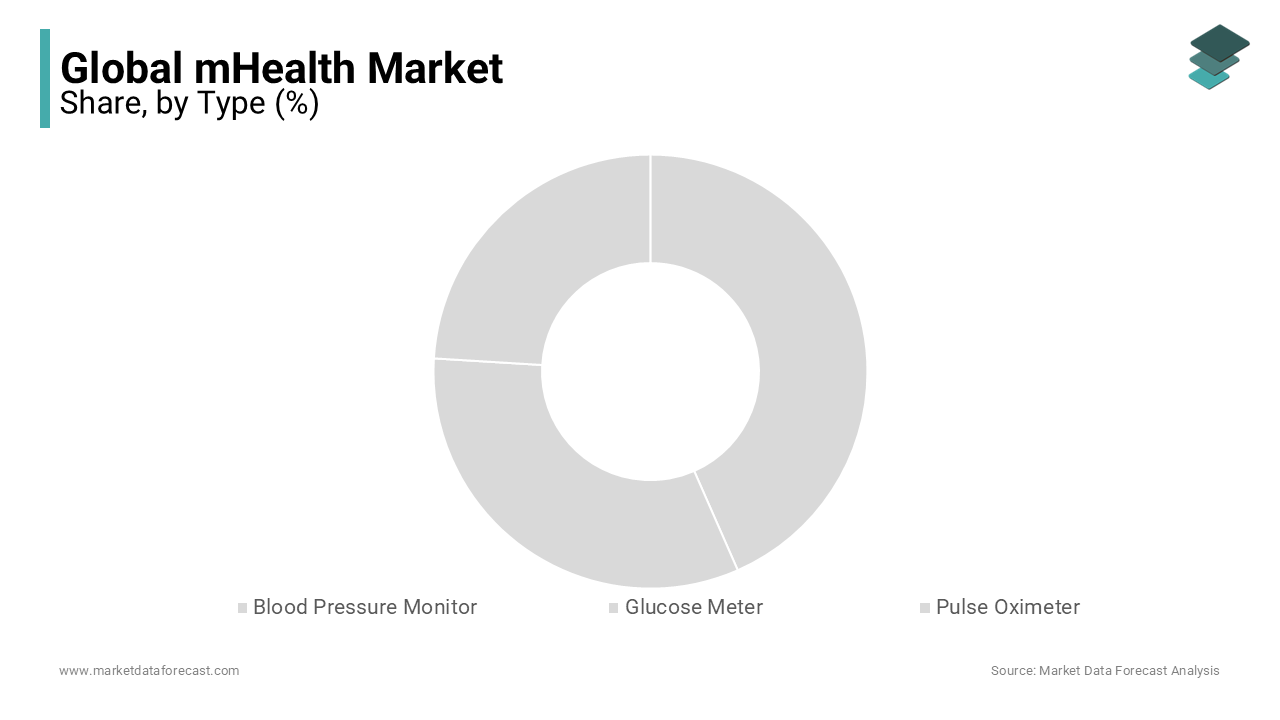

- Based on type, the glucose meters segment led the market in 2024 with a 35.2% share, reflecting high demand for diabetes management devices.

- Based on application, the chronic care management segment dominated with a 32.3% share in 2024, driven by the rising incidence of lifestyle-related diseases.

- Based on services, the remote monitoring segment held the largest share at 41.6% in 2024, highlighting its importance in reducing healthcare costs and enabling real-time patient care.

Regional Insights

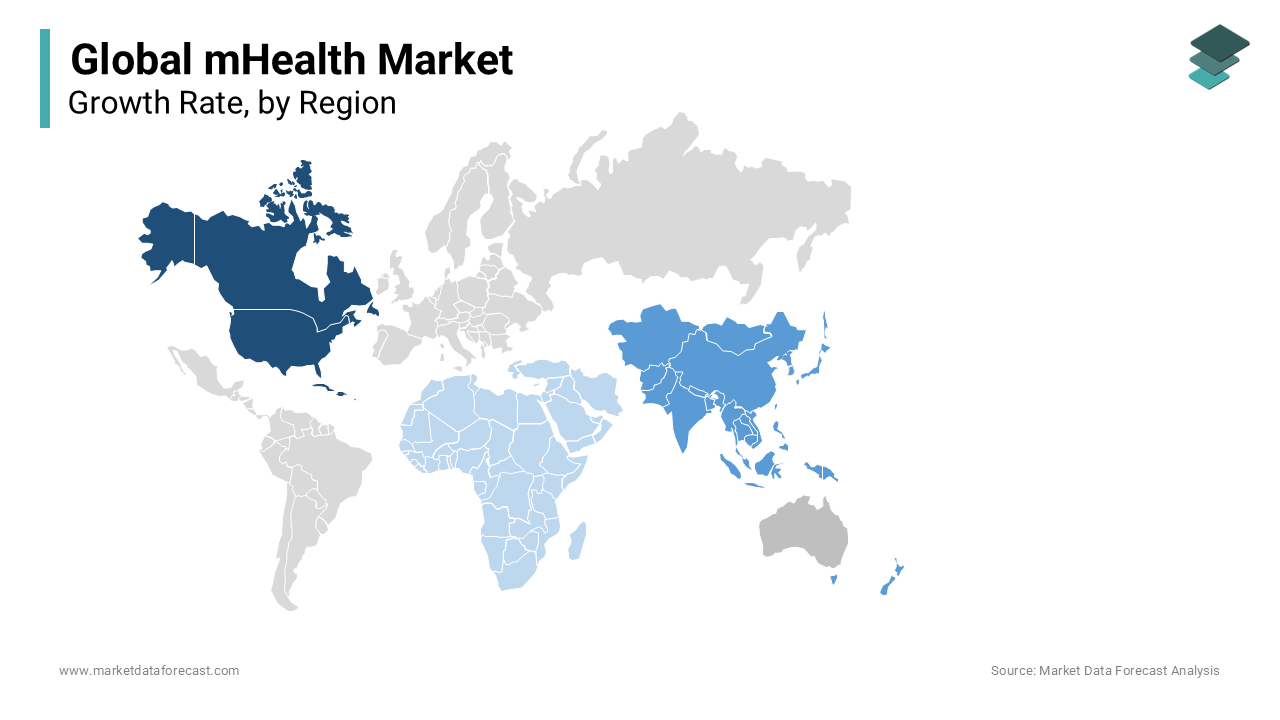

- North America dominated the global mHealth market in 2024 with a 37.5% share, supported by advanced healthcare infrastructure, widespread adoption of digital health technologies, and strong presence of leading market players.

- Europe is showing steady growth, driven by regulatory support and increasing adoption of mobile healthcare applications.

- Asia-Pacific is expected to record the fastest growth, fueled by rising smartphone penetration, large patient populations, and expanding telehealth initiatives.

- Latin America is emerging with growing adoption of mHealth solutions, particularly in remote care and chronic disease management.

- Middle East & Africa are gradually adopting mHealth technologies, supported by investments in healthcare digitalization.

Competitive Landscape

Key players in the global mHealth market include Cardionet Inc., iHealth Labs Inc., QUALCOMM Life, Vodafone, Dexcom Inc., Fitbit Inc. (Twine Health Inc.), Koninklijke Philips N.V. (Philips), Livongo Health Inc., Medtronic Plc., Omada Health Inc., Omron Corporation (Omron Healthcare Inc.), Samsung Electronics Co. Ltd., and Welldoc Inc. These companies are focusing on wearable innovation, AI integration, and strategic partnerships to enhance their global footprint.

Global mHealth Market Size

In 2024, the global mhealth market was valued at USD 85.20 billion and is forecasted to grow to USD 284.83 billion by 2033, at a CAGR of 14.35%.

mHealth refers to the mobile technologies employed to support public health systems, clinical care, and patient engagement through smartphones, wearable devices, telemedicine platforms, and health-focused applications. As of 2024, mHealth has evolved into a critical component of digital health infrastructure, facilitating remote diagnostics, chronic disease monitoring, medication adherence, and real-time data exchange between patients and providers. The proliferation of 5G networks has significantly enhanced data transmission speeds, enabling seamless integration of high-resolution imaging and live video consultations within mobile health ecosystems.

According to the International Telecommunication Union, over 60% of the global population was using mobile broadband services by 2023, laying the foundational connectivity required for scalable mHealth deployment. Besides, in low- and middle-income regions, mHealth has become instrumental in bridging healthcare access gaps, particularly in rural areas where physical infrastructure remains limited. The integration of artificial intelligence with mobile health platforms has further enabled predictive analytics for early disease detection. These developments underscore a paradigm shift from reactive to proactive healthcare delivery, positioning mHealth as a transformative force across diverse healthcare landscapes.

MARKET DRIVERS

Rising Burden of Chronic Diseases and the Need for Continuous Monitoring

The escalating prevalence of chronic non-communicable diseases (NCDs) such as diabetes, cardiovascular disorders, and respiratory conditions is a pivotal force accelerating the adoption of mHealth solutions. As per the World Health Organization, chronic diseases account for approximately 71% of all global deaths annually, with over 41 million lives lost each year. In the Asia Pacific region alone, the number of individuals diagnosed with type 2 diabetes has surged to 200 million, necessitating constant glucose monitoring and lifestyle management. Traditional healthcare systems are increasingly strained by the long-term care demands of these patients, prompting a shift toward decentralized, patient-centric models. mHealth platforms equipped with wearable sensors and real-time data analytics enable continuous physiological monitoring, allowing for early intervention and personalized treatment adjustments. For instance, remote cardiac monitoring via smartphone-connected electrocardiogram (ECG) devices has demonstrated a reduction in hospital readmissions among heart failure patients. Furthermore, the integration of mobile apps with electronic health records (EHRs) allows clinicians to access longitudinal patient data, enhancing diagnostic accuracy. The demand for such solutions is further amplified by aging populations. These developments illustrate how the growing burden of chronic illness is fundamentally reshaping healthcare delivery through mobile innovation.

Expansion of Smartphone Penetration and Mobile Internet Accessibility

The widespread proliferation of smartphones and affordable mobile internet has created an unprecedented foundation for mHealth scalability, particularly in emerging economies. In rural India, smartphone adoption has increased significantly over the past three years, driven by low-cost devices and localized language interfaces. This digital inclusivity enables previously underserved populations to access teleconsultations, digital prescriptions, and AI-driven symptom assessment tools directly from their personal devices. Moreover, mobile network operators are increasingly partnering with healthcare providers to offer bundled health services; Airtel in Bangladesh provides free access to maternal health content via USSD for users without smartphones. The expansion of 4G and 5G networks further supports high-bandwidth applications such as real-time ultrasound streaming and augmented reality-assisted diagnostics. This technological accessibility, combined with growing digital literacy, ensures that mHealth is no longer a supplementary tool but a primary conduit for healthcare engagement across diverse socio-economic strata.

MARKET RESTRAINTS

Fragmented Regulatory Frameworks and Compliance Heterogeneity

The absence of standardized regulatory frameworks across jurisdictions, leading to operational complexities for developers and healthcare providers, is one of the most significant impediments to the seamless expansion of the mHealth market. In the Asia Pacific region, regulatory approaches to digital health vary dramatically; while Australia and Singapore have established comprehensive guidelines for medical device classification of mHealth apps, countries like Indonesia and Vietnam lack clear legal definitions for software-as-a-medical-device (SaMD), creating uncertainty in product approval pathways. For instance, a telemedicine app developed in India may require complete redesign to comply with China’s Cybersecurity Law, which mandates local data storage and restricts cross-border health data transfers. Additionally, the Medical Device Regulation (MDR) in Japan requires clinical validation for any app claiming diagnostic functionality, increasing time-to-market by several months compared to less stringent markets. This regulatory fragmentation discourages investment and slows innovation. Furthermore, inconsistent certification processes hinder interoperability between national health systems, limiting the scalability of mHealth solutions. Without harmonized policies governing data privacy, clinical validation, and device classification, the mHealth ecosystem remains fragmented, undermining trust and slowing widespread adoption.

Persistent Digital Literacy Gaps Among Elderly and Rural Populations

The uneven distribution of digital literacy, particularly among older adults and rural communities is a critical barrier to mHealth adoption. The disparity severely limits the effectiveness of mHealth interventions targeting age-related conditions such as dementia, hypertension, and osteoporosis. Language barriers further exacerbate the issue; in India, where 22 officially recognized languages exist, many mHealth platforms remain available only in English or Hindi, excluding non-dominant linguistic groups. Moreover, cognitive decline associated with aging affects the ability to navigate complex user interfaces, rendering many apps inaccessible without caregiver assistance. These limitations highlight a fundamental mismatch between technological design and end-user capabilities, impeding the inclusive reach of mHealth and reinforcing existing healthcare inequities.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Predictive Diagnostics and Personalized Care

The convergence of mHealth with artificial intelligence (AI) presents a transformative opportunity to shift from reactive treatment to anticipatory, personalized healthcare. AI-powered mobile applications are increasingly capable of analyzing vast datasets, such as biometrics, lifestyle patterns, and genetic predispositions, to generate predictive insights for early disease detection. Like, AI-driven mobile dermatology apps have achieved high diagnostic accuracy rates in identifying melanoma from smartphone-captured images, rivaling dermatologists’ performance in controlled trials. In South Korea, the government-backed “AI Doctor” initiative has deployed mobile platforms that analyze voice patterns and typing rhythms to detect early signs of Parkinson’s disease. Furthermore, AI-enabled chatbots integrated into mHealth apps, such as India’s “AskDisha” by NITI Aayog, provide real-time triage and health education to millions, reducing the burden on primary care systems. Machine learning models trained on regional health data can also tailor interventions to local epidemiological profiles. These advancements not only enhance clinical outcomes but also empower patients to engage proactively with their health, establishing mHealth as a cornerstone of next-generation digital therapeutics.

Public-Private Partnerships Driving Scalable mHealth Infrastructure

Strategic collaborations between governments, technology firms, and healthcare institutions are unlocking scalable mHealth ecosystems, particularly in resource-constrained settings. These partnerships leverage private sector innovation and infrastructure while ensuring public oversight and equitable access. In Australia, the Digital Health CRC facilitates joint R&D initiatives between universities, hospitals, and tech companies to develop interoperable mHealth solutions compliant with national health data standards. The success of such models has prompted the Asian Development Bank to allocate substantial million toward digital health PPPs across Southeast Asia. These alliances not only enhance service delivery but also foster sustainable financing models, enabling long-term scalability. By combining regulatory support, technological expertise, and community outreach, public-private synergies are transforming mHealth from isolated pilot projects into integrated, nationwide health systems.

MARKET CHALLENGES

Data Security Vulnerabilities in Decentralized Health Data Ecosystems

The decentralization of health data through mHealth applications introduces significant cybersecurity risks, particularly in environments with underdeveloped digital safeguards. As mHealth platforms increasingly store sensitive biometric, diagnostic, and behavioral data on personal devices and cloud servers, they become attractive targets for cyberattacks. Additionally, the use of third-party software development kits (SDKs) in mHealth apps often introduces hidden vulnerabilities. The absence of robust authentication mechanisms further compounds the risk. These incidents erode user trust and deter adoption, particularly among populations already skeptical of digital health. Addressing these vulnerabilities requires not only technical upgrades but also institutional frameworks for continuous monitoring, threat intelligence sharing, and rapid incident response—challenges that remain under-resourced in many emerging markets.

Interoperability Deficits Hindering Seamless Health Information Exchange

A further critical obstacle to the full realization of mHealth potential is the lack of interoperability between disparate health information systems, which impedes seamless data exchange across platforms, providers, and national databases. Despite advances in digital health infrastructure, many mHealth applications operate in silos, unable to integrate with electronic medical records (EMRs), hospital information systems, or national health registries. In APAC, only limited nember of mHealth solutions in the region comply with international data exchange standards such as HL7 FHIR (Fast Healthcare Interoperability Resources). The fragmentation leads to inefficiencies. The absence of unified data ontologies and API standardization further complicates integration, particularly for AI-driven analytics that require comprehensive datasets. Initiatives such as Singapore’s National Electronic Health Record (NEHR) system demonstrate the benefits of interoperability, enabling authorized mHealth providers to access patient histories across 1,700 healthcare institutions. However, such models remain exceptions rather than norms. Without systemic alignment in data architecture and governance, the mHealth ecosystem risks becoming a collection of isolated tools rather than an integrated, patient-centered continuum of care.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| Segments Covered | By Devices, Applications, Services, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | Cardio Net Inc., iHealth Labs Inc., QUALCOMM life, Vodafone, Dexcom, Inc., Fitbit, Inc. (Twine Health, Inc.), Koninklijke Philips N.V. (Philips), Livongo Health, Inc., Medtronic Plc., Omada Health, Inc., Omron Corporation |

SEGMENTAL ANALYSIS

By Type Insights

The glucose meters segment commanded the largest revenue share with 35.2% of the global mHealth device market in 2024. This dominance is primarily anchored in the escalating global diabetes epidemic, which has transformed continuous glucose monitoring into a medical necessity rather than a convenience. The integration of smart glucose meters with Bluetooth-enabled mobile applications allows real-time tracking, automated insulin dosage suggestions, and seamless data sharing with healthcare providers, enhancing treatment adherence. Furthermore, the adoption of flash glucose monitoring systems, such as Abbott’s FreeStyle Libre, which accounted for a notable share of connected glucose device sales in Europe, has significantly improved user compliance due to painless scanning and trend visualization. Public health initiatives, including India’s National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke (NPCDCS), have also accelerated deployment by subsidizing smart glucose meters in primary health centers. These converging clinical, technological, and policy-driven forces solidify glucose meters as the cornerstone of digital diabetes care, ensuring their sustained market leadership.

The pulse oximeter segment is emerging as the fastest-growing category within the mHealth device landscape and is projected to expand at a CAGR of 18.7% from 2025 to 2033. This accelerated growth is largely attributed to heightened awareness of respiratory health following the global pandemic, which established pulse oximetry as a critical tool for early detection of hypoxemia. The World Health Organization included pulse oximeters in its List of Essential Diagnostics in 2021, reinforcing their clinical importance and prompting integration into national telehealth programs. Additionally, the miniaturization of sensor technology has enabled integration into wearable form factors, such as fingertip devices and smart rings, enhancing user comfort and compliance. The rise of remote patient monitoring in post-acute care settings further amplifies demand.

By Application Insights

The chronic care management segment led the market by capturing 32.3% of the global mHealth services revenue in 2024. This lead position is driven by the increasing reliance on digital platforms to manage long-term conditions such as hypertension, diabetes, and heart failure, which collectively affect a substantial number of people worldwide. The economic burden of chronic diseases has compelled healthcare systems to adopt cost-effective, scalable digital interventions. Remote monitoring and AI-driven risk stratification tools embedded within chronic care platforms enable early intervention, reducing hospitalizations and emergency visits. Furthermore, government-backed initiatives are accelerating adoption. In low-resource settings, mobile-based chronic care models are proving equally transformative. These outcomes underscore the dual value proposition of chronic care management services: improved clinical outcomes and substantial cost containment, cementing their dominance in the mHealth services ecosystem.

The women’s health segment is experiencing the most rapid expansion in the mHealth services sector and is projected to grow at a CAGR of 22.3% between 2025 and 2033. This surge is fueled by increasing demand for personalized, discreet, and accessible reproductive and maternal health solutions, particularly in regions with limited gynecological infrastructure. Mobile apps offering menstrual cycle tracking, fertility prediction, and pregnancy monitoring have gained widespread traction. Additionally, advancements in AI are enabling predictive analytics for conditions like polycystic ovary syndrome (PCOS) and endometriosis. Regulatory support is also expanding. With growing female digital literacy and increasing investment in femtech, women’s health services are redefining patient engagement, positioning mHealth as a pivotal enabler of gender-responsive healthcare.

By Services Insights

The remote monitoring segment commanded by representing a 41.6% of the total mHealth application revenue in 2024. This dominance is because of its critical role in enabling continuous, real-time health surveillance outside traditional clinical settings, particularly for patients with chronic or post-acute conditions. The aging global population has intensified the need for home-based care solutions. Remote monitoring systems, including wearable ECG patches, implantable cardiac monitors, and mobile-connected respiratory devices, facilitate early detection of anomalies, reducing emergency admissions. Moreover, reimbursement policies are increasingly supporting adoption. In low-income countries, mobile-based monitoring is bridging gaps in specialist access. The integration of 5G networks and edge computing further enhances data transmission reliability, allowing real-time intervention in critical cases. As healthcare systems shift toward value-based models, remote monitoring emerges not only as a technological advancement but as a structural necessity for sustainable, patient-centered care delivery.

The prevention application segment is witnessing the fastest growth within the mHealth landscape and is projected to grow at a CAGR of 19.8% in the coming years. This acceleration is driven by a global paradigm shift from disease treatment to proactive health preservation, supported by advances in predictive analytics and behavioral nudging technologies. Mobile apps leveraging AI and machine learning now offer personalized risk assessments based on genetic, environmental, and behavioral data. Wearable integration enhances efficacy. Employers are also adopting mHealth prevention programs. Government incentives further amplify adoption. As healthcare systems prioritize population health and cost containment, mHealth-powered prevention is evolving into a foundational pillar of sustainable healthcare delivery.

REGIONAL ANALYSIS

North America remained the most advanced and dominant region in the global mHealth market by securing a share of 37.5% in 2024, in particular, drives this leadership through a confluence of technological innovation, regulatory maturity, and robust healthcare spending. Private insurers are increasingly covering mHealth services. Furthermore, the widespread adoption of electronic health records enables seamless integration with mHealth platforms. Consumer demand is equally strong. Tech giants like Apple and Google continue to invest heavily in health-focused wearables and data platforms, reinforcing ecosystem maturity. These factors collectively position North America as the epicenter of mHealth innovation, setting global benchmarks for scalability, reimbursement, and clinical integration.

Europe holds a significantly share of the global mHealth market. The region’s strength lies in its structured healthcare systems, strong data protection frameworks, and increasing public investment in digital transformation. Countries like Estonia and Denmark lead in digital health adoption. Germany’s Digital Healthcare Act has been particularly transformative. Chronic disease management is a key driver. Besides, the General Data Protection Regulation (GDPR) ensures high levels of patient trust. Cross-border health data exchange under the European Health Data Space is expected to further accelerate adoption. Europe’s blend of regulatory rigor, public funding, and clinical integration positions it as a model for sustainable, equitable mHealth deployment.

Asia-Pacific is the most dynamic and fastest-evolving region. The region’s growth is propelled by massive populations, rising smartphone penetration, and urgent healthcare access challenges. China’s “Healthy China 2030” initiative has integrated mHealth into national policy. India’s Ayushman Bharat Digital Mission has created a unified health ID for a large number of people, enabling seamless data exchange across mobile platforms. The burden of chronic diseases is immense; the Indian Council of Medical Research estimates that 110 million Indians have diabetes, driving demand for connected glucose monitoring. Japan’s aging society has led to widespread adoption of remote monitoring for elderly care. Startups like Indonesia’s Halodoc and South Korea’s MediLive are scaling rapidly, supported by venture capital and government partnerships. Despite infrastructural disparities, the region’s sheer scale, digital ambition, and policy momentum make it the future growth engine of the global mHealth market.

Latin America occupies a modest but rapidly expanding position in the mHealth landscape. Brazil emerges as the regional leader, driven by urbanization, rising smartphone use, and public health challenges. Also, digital health platforms are reaching previously underserved populations. Chronic diseases are a major concern. Private sector innovation is accelerating. Regulatory progress is evident. However, disparities in internet access and digital literacy persist, particularly in the Amazon regions. Despite these challenges, increasing investment and growing patient demand suggest strong upward trajectory, positioning the region as an emerging mHealth frontier.

Middle East and Africa collectively exhibit significant potential due to high mobile penetration and an underdeveloped physical healthcare infrastructure. Sub-Saharan Africa, in particular, relies heavily on mobile technology for health access. The UAE has launched “Dubai Health” as a centralized mHealth platform, integrating AI-driven diagnostics and teleconsultations. Maternal and child health remains a key focus. However, challenges such as inconsistent power supply, low digital literacy, and fragmented regulation hinder scalability. Nevertheless, the region’s reliance on mobile-first solutions, combined with growing government commitment, positions it as a critical testing ground for frugal, scalable mHealth innovations with global applicability.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

A few of the notable companies operating in the global mHealth market profiled in the report are Cardionet Inc., iHealth Labs Inc., QUALCOMM life, Vodafone, Dexcom, Inc., Fitbit, Inc. (Twine Health, Inc.), Koninklijke Philips N.V. (Philips), Livongo Health, Inc., Medtronic Plc., Omada Health, Inc., Omron Corporation (Omron Healthcare, Inc.), Samsung Electronics Co., Ltd, and Welldoc, Inc.

The competitive landscape of the mHealth market is characterized by a dynamic convergence of technology giants, medical device manufacturers, and specialized digital health startups, all vying to redefine healthcare delivery through mobile innovation. Incumbent healthcare companies leverage their clinical expertise and regulatory experience to develop medically validated solutions, while tech firms bring scalability, user-centric design, and vast digital ecosystems. This intersection fosters both collaboration and rivalry, as traditional boundaries between industries blur. Differentiation increasingly hinges on the ability to deliver actionable health insights, ensure data security, and achieve seamless integration with existing healthcare infrastructure. Companies are not only competing on product functionality but also on trust, usability, and long-term engagement. The absence of universal standards creates opportunities for first-mover advantage, yet also invites fragmentation. Regional disparities in healthcare systems and digital readiness further shape competitive strategies, requiring localization and adaptability. As consumer expectations rise and preventive care gains prominence, the race is intensifying to build platforms that are not only technologically advanced but also clinically meaningful and accessible across diverse populations. Sustainability in this space depends on balancing innovation with reliability, scalability with personalization, and commercial ambition with ethical responsibility.

Top Players in the mHealth Market

Apple Inc. has emerged as a transformative force in the mHealth landscape by seamlessly integrating health monitoring capabilities into its consumer-centric ecosystem. Through innovations embedded in the Apple Watch and iPhone, the company has redefined personal health tracking by offering features such as ECG monitoring, blood oxygen measurement, and atrial fibrillation detection. Apple’s emphasis on user privacy, intuitive design, and integration with healthcare institutions enables individuals to actively participate in their health management. Collaborations with major hospitals and research bodies have facilitated large-scale health studies, contributing to medical insights while democratizing access to preventive tools. By positioning its devices as proactive health companions rather than mere gadgets, Apple has set a benchmark for how technology companies can influence public health outcomes and shape consumer expectations in digital wellness.

Samsung Electronics plays a pivotal role in advancing mHealth through its wearable technology and integrated digital health platforms. The company’s Galaxy Watch series, equipped with advanced biosensors, enables continuous monitoring of vital signs, including heart rate, sleep patterns, and stress levels. Samsung’s Health platform aggregates data from multiple sources, offering users personalized insights and wellness recommendations. The company actively invests in clinical validation of its health features and partners with healthcare providers to ensure medical relevance. It's open ecosystem supports third-party app integration, fostering innovation across fitness, chronic disease management, and mental well-being. By combining hardware excellence with a scalable software framework, Samsung has positioned itself as a key enabler of mobile-driven preventive care, bridging the gap between consumer electronics and clinical-grade health monitoring.

Philips stands as a leader in the convergence of medical technology and digital health, leveraging its deep clinical expertise to develop comprehensive mHealth solutions. The company’s focus lies in remote patient monitoring, telehealth platforms, and connected diagnostic devices designed for both home and hospital use. Philips integrates data from wearable sensors and mobile applications into unified care pathways, supporting clinicians in managing chronic conditions more effectively. Its commitment to interoperability ensures seamless communication between devices and electronic health records, enhancing care coordination. By prioritizing patient-centered design and evidence-based outcomes, Philips has become a trusted partner for healthcare systems transitioning to value-based models. The company’s global reach and long-standing reputation in medical innovation enable it to shape the evolution of mHealth as a critical component of modern healthcare delivery.

Top Strategies Used by Key Market Participants

One major strategy employed by leading players in the mHealth market is the development of integrated ecosystems that unify hardware, software, and health services. Companies are designing seamless platforms where wearable devices, mobile applications, and cloud-based analytics work in tandem, enabling continuous health monitoring and personalized feedback. This approach enhances user engagement by offering a cohesive experience and strengthens brand loyalty through recurring interactions with health data.

Another key strategy is strategic collaboration with healthcare providers, research institutions, and government bodies. By partnering with hospitals and clinics, mHealth companies ensure clinical validation of their technologies, improve credibility, and facilitate integration into formal care pathways. These alliances also support regulatory compliance and expand access to patient populations through institutional adoption.

A third critical strategy is the prioritization of data privacy and regulatory compliance. As health data becomes increasingly digitized, companies are investing in robust security frameworks and adhering to international standards to build user trust. Transparent data governance practices and ethical design principles are central to maintaining consumer confidence and ensuring sustainable market penetration across diverse regulatory environments.

RECENT MARKET DEVELOPMENTS

- In March 2024, Apple launched a new health insights feature within the iPhone’s Health app, enabling users to receive personalized recommendations based on long-term trends in activity, sleep, and heart rate, thereby deepening engagement with preventive care.

- In June 2024, Samsung partnered with a leading European telehealth provider to integrate its wearable health data directly into virtual consultation platforms, allowing physicians to access real-time patient vitals during remote visits.

- In February 2024, Philips introduced an upgraded version of its remote patient monitoring suite, incorporating AI-driven risk prediction models for chronic respiratory and cardiac conditions, enhancing clinical decision support.

- In May 2024, Google Health collaborated with academic medical centers to validate the accuracy of its smartphone-based respiratory rate monitoring technology, aiming to expand its use in low-resource settings.

- In January 2024, Fitbit introduced a new mental wellness module within its app, offering guided mindfulness sessions and stress tracking using biometric data, broadening its scope beyond physical fitness.

MARKET SEGMENTATION

This market research report on the global market has been segmented by Type, Application, services, and Region.

By Type

- Blood Pressure Monitor

- Glucose Meter

- Pulse Oximeter

By Application

- Chronic Care Management

- Health and Fitness

- Weight Loss

- Women's Health

- Personal Health Record

- Medication

By Services

- Remote Monitoring

- Consultation

- Fitness And Wellness

- Prevention

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

Does this report include the impact of COVID-19 on the mHealth market?

Yes, this report include the impact of COVID-19 on the market

Which region had the major share of the global mobile health market in 2024?

Geographically, the North American region accounted for the major share in the global market in 2024.

Who are the leading players in the mHealth market?

Cardionet Inc., iHealth Labs Inc., QUALCOMM life, Vodafone, Dexcom, Inc., Fitbit, Inc. (Twine Health, Inc.), Koninklijke Philips N.V. (Philips), Livongo Health, Inc., Medtronic Plc. are a few of the notable players in the global mobile health market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com