Global Pet Care Market Size, Share, Trends, & Growth Forecast Report, Segmented By Pet Type (Dog, Cat, Fish and Others), Product Type (Pet food, Pet food care and Grooming Products), Distribution Channel (Offline and Online), and Region (North America, Europe, Latin America, Asia-Pacific, Middle East and Africa), Industry Analysis from 2026 to 2034

Global Pet Care Market Size

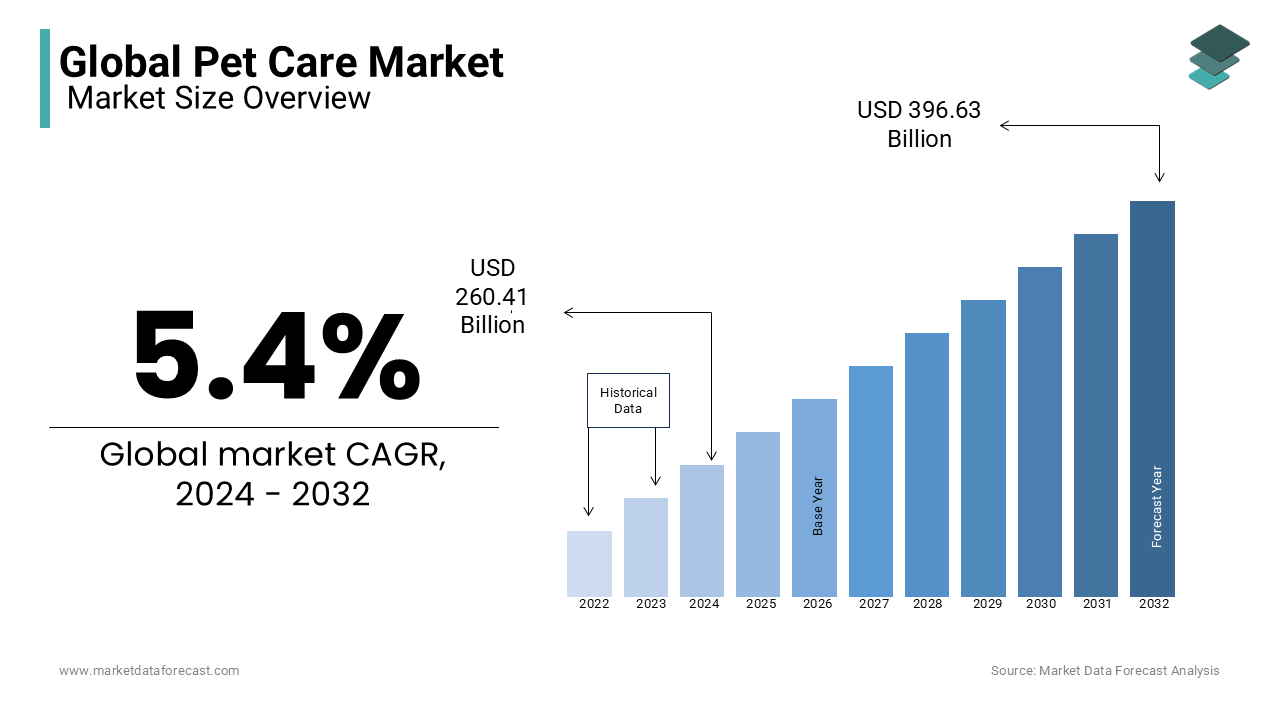

The global pet care market was valued at USD 274.47 billion in 2025 and is anticipated to reach USD 289.29 billion in 2026 from USD 440.62 billion by 2034, growing at a CAGR of 5.4 % during the forecast period from 2026 to 2034.

Pet Care is a product and service dedicated to the nutrition, health, hygiene, safety, and emotional enrichment of companion animals. This includes pet food, veterinary services, insurance, grooming, accessories, digital health tools, and behavioral support systems. Similarly, more than 85 million households across Europe own a pet.

MARKET DRIVERS

Humanization of Pets Fuels Premium Product Adoption

The humanization of pets, where animals are treated with the same emotional and financial consideration as family members, is boosting the growth of the Pet Care Market. This cultural phenomenon has elevated expectations around pet nutrition, healthcare, and lifestyle enrichment. As per the Human Animal Bond Research Institute, pet owners consider their pets core family members, which directly influences purchasing behavior toward organic, grain-free, and functional pet foods. Millennials and Gen Z, who represent over 55% of new pet adoptions in North America, exhibit strong preferences for transparency, sustainability, and scientific validation in pet products.

Rising Global Pet Ownership Rates Expand Market Reach

Pet ownership is expanding rapidly beyond traditional Western countries by creating new demand corridors in Asia, Latin America, and parts of Africa, which is additionally propelling the growth of the Pet Care Market. Urbanization, delayed family formation, and increased awareness of animal welfare are key enablers of this trend. Japan’s aging society has also embraced pet companionship, with the Ministry of Health, Labour and Welfare noting that over 28% of households with individuals aged sixty-five or older include a pet.

MARKET RESTRAINTS

Economic Volatility Constrains Discretionary Pet Spending

The vulnerability to macroeconomic fluctuations in categories perceived as non-essential is limiting the growth of the pet care market. As per the Organisation for Economic Co-operation and Development, real household disposable income growth in advanced economies decelerated, with the lowest in five years, which is prompting consumers to trade down in pet expenditures. The decline in pet-related spending in 2023, with notable shifts from branded to economy pet food, is also hampering the growth of the market. Similarly, the United States Bureau of Labor Statistics found that households in the lowest income quartile reduced pet care outlays amid rising costs for housing, energy, and food. Premium services such as pet spas, behavioral training, and luxury accessories are especially sensitive to economic sentiment.

Stringent Regulatory Frameworks Increase Compliance Burdens

Thefact that it operates under a patchwork of evolving regulations that vary significantly is restricting the growth of the Pet Care Market. In the European Union, Regulation EC No 767 2009 imposes rigorous standards on pet food labeling, ingredient sourcing, and safety documentation. In the United States, the Food and Drug Administration’s Center for Veterinary Medicine issued 27 warning letters in 2023 to companies making unverified health claims.

MARKET OPPORTUNITIES

Expansion of Pet Health Tech Unlocks New Revenue Streams

Digital health technologies are redefining pet care delivery and creating high margins, which is a recurring revenue model,s substantially contributing to the growth of the Pet Care Market. Wearables, AI diagnostics, and telemedicine platforms enable proactive, data-driven pet management. As per the American Animal Hospital Association, a few veterinary practices in the United States now offer telehealth services. Emerging applications include AI-powered apps that analyze vocalizations for pain detection or monitor litter box usage for urinary health indicators. These innovations not only enhance preventive care but also foster sticky customer relationships through subscription ecosystems, which are positioning tech-enabled brands at the forefront of next-generation pet care.

Growth of Sustainable and Ethical Pet Products Appeals to Conscious Consumers

Sustainability and ethical sourcing have become decisive purchase criteria among the younger demographic, which is expected to boost the growth of the Pet Care Market in the coming years. Global pet owners aged 18 to 34 are willing to pay a premium for eco-friendly pet products. This has spurred innovation in biodegradable waste solutions, plant-based proteins, and plastic-free packaging. The rise in sales of certified sustainable brands in 2024, while Pets at Home launched a “Green Paws” label to highlight low-impact products.

MARKET CHALLENGES

Fragmented Supply Chains Disrupt Product Availability and Consistency

The complex, multi-tiered supply chains, vulnerable to geopolitical, climatic, and logistical disruption, are likely to pose a challenge for the growth of the Pet Care Market. Sourcing high-quality proteins, vitamins, and natural additives often spans multiple continents, increasing exposure to trade barriers and biosecurity risks. Outbreaks of animal diseases further destabilize supply. A 2024 survey by the Global Pet Care Alliance, some mid-sized brands faced stockouts in key markets due to supply chain misalignment. Cold chain limitations in emerging economies exacerbate spoilage risks for wet food and supplements. These inefficiencies not only inflate operational costs but also undermine brand reliability, particularly for companies without vertically integrated logistics networks.

Intensifying Competition Erodes Brand Differentiation and Margins

The penetration of thousands of new entrants, diluting brand identity and compressing profitability, is likely to degrade the growth of the Pet Care Market. Over 2000 new pet care brands launched globally in 2024, where many are leveraging direct-to-consumer models and influencer marketing to bypass traditional retail. Private label expansion intensifies pressure. The private label pet food captured 21% of United States supermarket sales in 2024. Simultaneously, conglomerates like Nestlé and Colgate-Palmolive are acquiring niche players to consolidate share, marginalizing independent innovators.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.4% |

| Segments Covered | By Product Type, Pet Type, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Ancol Pet Products Limited; Hill's Pet Nutrition, Inc; Mars, Incorporated; Petmate Holdings Co; Tail Blazers; Blue Buffalo Co, Ltd; Tiernahrung Deuerer GmbH; Champion Petfoods LP; Nestle Purina PetCare; Saturn Petcare GmbH; The Hartz Mountain Corporation; Heristo AG; UniCharm Corporation; Diana Group; Spectrum Brands Inc; The J.M. Smucker Company; Schell & Kampeter, Inc; Nylabone |

SEGMENTAL ANALYSIS

By Pet Insights

The Dogs segment was the largest by capturing 46.6% of the Pet Care Market share in 2024, with their role as primary companion animals in both urban and suburban households, coupled with higher per pet expenditure compared to other species. Additionally, dogs require more frequent veterinary visits and preventive care.

The cat segment is likely to grow with an expected CAGR of 7.2% throughout the forecast period, with urbanization and lifestyle compatibility, as cats require less space and maintenance than dogs. In high-density cities like Tokyo, Seoul, and London, cat ownership has surged. The rise of premium cat nutrition, particularly wet and raw food format,t aligns with feline biological needs.

By Product Insights

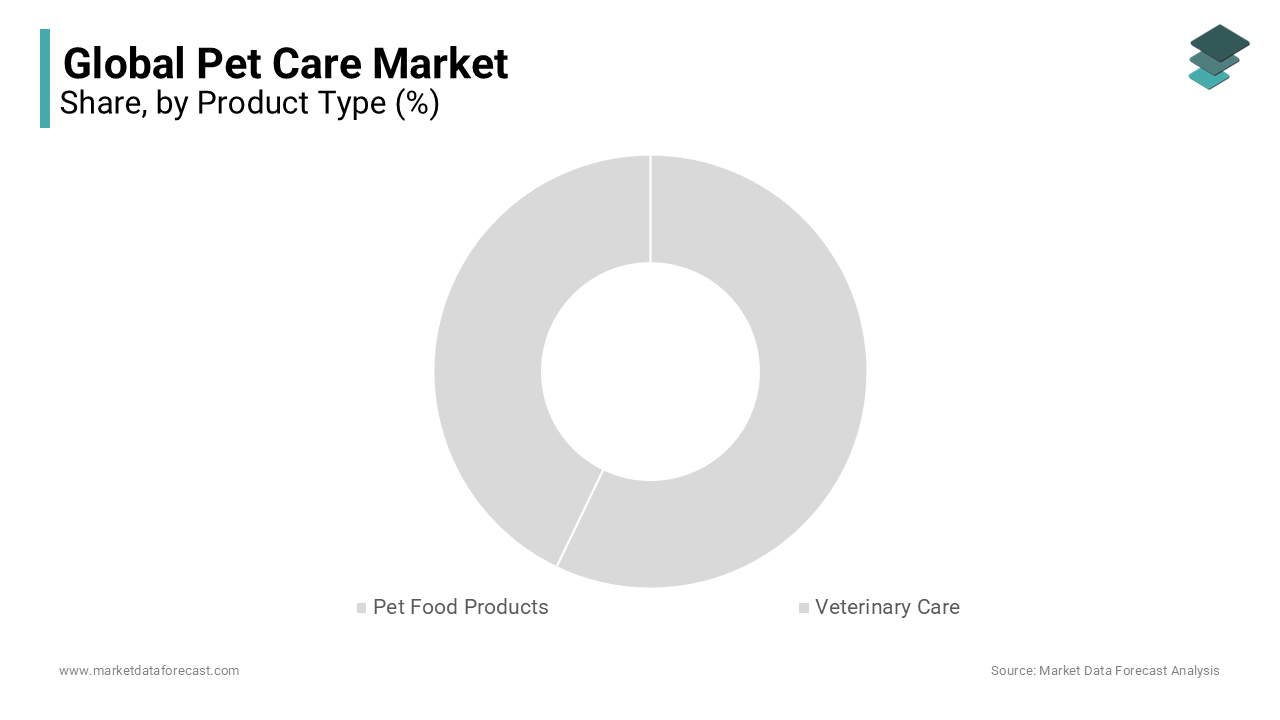

The pet food segment accounted in holding 58.3% of the global Pet Care Market share in 2024, with its status as a recurring, non-discretionary expense, unlike grooming or accessories, which are periodic. As per the European Pet Food Industry Federation, over 80% of pet owners in Germany and France consider ingredient quality the top factor when selecting food. Premiumization is a major growth lever. In the United States, sales of super premium pet food grew by 14% year over year in 2024. Additionally, veterinary-recommended therapeutic diets are used for managing conditions like kidney disease or obesity.

The grooming products segment is projected to expand at a CAGR of 8.5% inthet coming years, owing to the rising awareness of pet hygiene as a component of overall health. Concurrently, e-commerce has democratized access to specialized shampoos, dental wipes, and ear cleaners. Regulatory support also plays a role, where the European Union’s updated Cosmetics Regulation now includes pet grooming items under safety assessment protocols, which is boosting consumer confidence in product efficacy and safety.

By Distribution Channel Insights

The offline channels segment was the largest and held a dominant share of the Pet Care Market in 2024, with the tactile and consultative nature of pet care purchases, where consumers seek immediate product access and expert advice. Pet specialty retailers like PetSmart and Pets at Home remain pivotal. United States pet owners prefer in-store shopping for food and medications due to trust in freshness and labeling accuracy. Veterinary clinics further anchor offline dominance by dispensing prescription diets and flea treatments. Supermarkets also contribute significantly, especially in price-sensitive markets.

The online channel segment is likely to grow with significant growth opportunities in the coming years,s with the convenience, personalization, and subscription models. Mobile commerce is accelerating adoption, where Alibaba’s 2024 Singles Day event generated over 600 million United States dollars in pet product sales, with grooming and supplements as top categories. Additionally, online channels facilitate access to niche brands.

REGIONAL ANALYSIS

North America Market Analysis

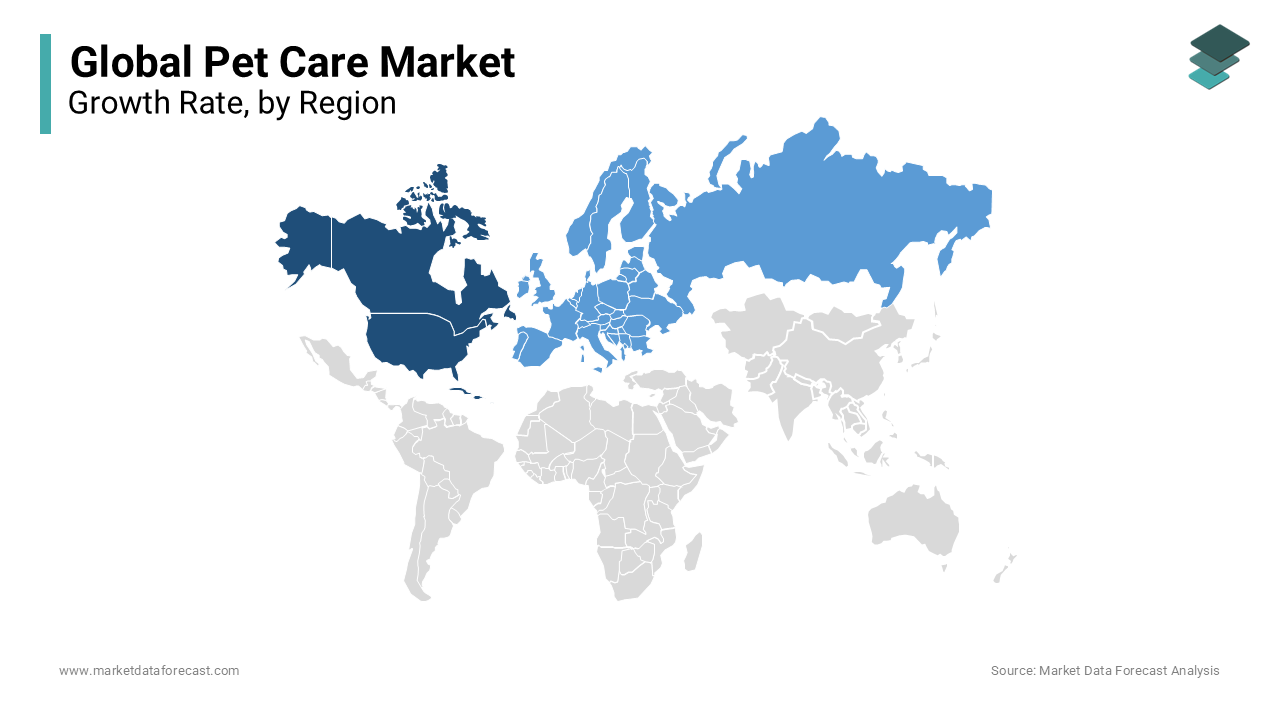

North America was the largest contributor to the Pet Care Market by holding 34.2% of the share in 2024, with a deeply entrenched pet ownership culture and high per capita spending. Insurance penetration is a distinguishing factor, with over 3 million pets insured in the United States in 202, enabling greater access to advanced veterinary care. Innovation ecosystems in states like California and Texas drive product development in functional nutrition and digital health.

Europe Market Analysis

Europe's pet care market held 28.3% of the share in 2024, with the stringent regulations, high welfare standards, and premium product demand. The European Union’s Farm to Fork Strategy has clean label trends, with 76% of pet owners in France prioritizing traceable ingredients. Veterinary integration is robust, where 65% of pet food sales in Scandinavia occur through clinics. The United Kingdom’s post-Brexit regulatory autonomy has also spurred local manufacturing.

Asia Pacific Market Analysis

Asia Pacific pet care market growth is likely to have a prominent CAGR in the coming years, owing to the rising incomes and shifting social norms. China is the regional powerhouse, with pet care revenue surpassing 35 billion United States dollars in 2024. Urban single-person households are a key driver, where 42% of pet owners in Shanghai and Beijing live alone. Japan maintains high per capita expenditure despite a stagnant population.

Latin America Market Analysis

Latin America's pet care market growth is likely to grow steadily throughout the forecast period, with Brazil and Mexico as primary contributors.

COMPETITIVE LANDSCAPE

The Pet Care Market is characterized by intense competition among multinational corporations, regional specialists, and agile direct-to-consumer startups. Established players leverage scale, scientific expertise, and integrated care networks to dominate premium segments, while private label brands pressure pricing in mass retail channels. Innovation velocity has accelerated, with companies racing to launch clean-label foods, digital health tools, and sustainable packaging. Simultaneously, the barrier to entry remains relatively low for niche brands, fueling market fragmentation. Consumer loyalty is increasingly tied to brand values such as animal welfare, environmental stewardship, and data privacy.

KEY MARKET PLAYERS

A few of the dominant market players in the global pet care market

- Ancol Pet Products Limited

- Hill's Pet Nutrition, Inc

- General Mills Pet

- Mars Incorporated

- Petmate Holdings Co

- Tail Blazers

- Blue Buffalo Co, Ltd

- Tiernahrung Deuerer GmbH Championn Pet Foods LP

- Nestle Purina PetCare

- Saturn Petcare GmbH

- The Hartz Mountain Corporation

- Heristo AG

- UniCharm Corporation

- Diana Group

- Spectrum Brands Inc

- The J.M. Smucker Company

- Schell & Kampeter, Inc

- Nylabone

Top Players In The Market

- Mars Petcare is a global leader in pet nutrition, veterinary services, and digital health solutions. The company operates iconic brands such as Pedigree, Whiskas, Royal Canin, and Greenies, offering science-backed formulations tailored to breed, age, and health conditions. In recent years, Mars Petcare has significantly expanded its veterinary network through Banfield Pet Hospital, VCA, and AniCura, creating an integrated care ecosystem. These initiatives reinforce its commitment to innovation, preventive care, and environmental responsibility, strengthening its influence across multiple segments of the global Pet Care Market.

- Nestlé Purina PetCare is a major force in premium and performance pet nutrition, with a portfolio that includes Purina Pro Plan, Fancy Feast, and Tidy Cats. The company emphasizes scientific research through its in-house Pet Care Centers and partnerships with veterinary institutions. It also expanded its personalized nutrition platform using digital diagnostics and consumer data. These actions demonstrate Purina’s strategic focus on health innovation, circular economy principles, and direct consumer engagement to solidify its leadership in evolving pet care landscapes.

- General Mills Pet, operating under the Blue Buffalo brand, has established itself as a pioneer in natural and holistic pet food. Since its acquisition by General Mills, the segment has leveraged corporate scale to enhance distribution while maintaining its clean label identity. The company invested in a new production facility in Pennsylvania to meet rising demand for its Life Protection and Wilderness lines. It also launched a digital wellness hub offering nutritional guidance and telehealth referrals.

Top Strategies Used By The Key Market Participants

Key players in the Pet Care Market employ a range of strategic initiatives to maintain a competitive advantage. These include continuous product innovation with functional and breed-specific formulations, expansion of veterinary and telehealth services, investment in sustainable and transparent supply chains, aggressive digital marketing targeting millennial and Gen Z pet owners, and strategic acquisitions to consolidate market presence. Companies also focus on direct-to-consumer models through subscription services and personalized nutrition platforms. Geographic diversification into emerging markets and partnerships with veterinary professionals further enhance brand credibility and customer retention. These multifaceted strategies enable leading firms to adapt to evolving consumer expectations while driving long-term growth in a highly dynamic industry.

MARKET SEGMENTATION

This market Research Report on the global pet care market is segmented and sub-segmented into the following categories.

By Product type

- Pet Food Products

- Veterinary Care

- Others

By Pet Type

- Dog

- Cat

- Others

By Distribution Channel

- Offline

- Online

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is driving growth in the Global Pet Care Market?

The Global Pet Care Market is expanding due to humanization of pets, rising pet ownership in emerging economies, premiumization of food and wellness products, and post-pandemic “pet parent” spending resilience.

How is e-commerce reshaping the Global Pet Care Market?

Online channels now account for over 35% of sales—driven by subscription models (e.g., Chewy, Zooplus), direct-to-consumer brands, and AI-powered personalized recommendations in the Global Pet Care Market.

Which segment leads the Global Pet Care Market?

Pet food remains the largest category, but pet health (supplements, telemedicine, insurance) and tech-enabled products (trackers, smart feeders) are the fastest-growing segments in the Global Pet Care Market.

Are sustainability concerns influencing product development?

Yes—consumers demand recyclable packaging, ethically sourced proteins, and clean-label ingredients, pushing brands to adopt B Corp certifications and carbon-neutral claims in the Global Pet Care Market.

Which regions show the highest growth potential?

Asia-Pacific (especially China, India, and Southeast Asia) leads in new pet adoption, while North America and Europe drive premium and therapeutic innovations in the Global Pet Care Market.

How is pet insurance adoption trending globally?

Still under 5% penetration globally, but growing rapidly in the UK, Sweden, and the U.S.—fueled by rising vet costs and partnerships with veterinary chains in the Global Pet Care Market.

What role does functional nutrition play?

Probiotics, joint health, calming chews, and breed-specific formulas are now mainstream—blurring lines between food and supplements in the Global Pet Care Market.

Are private labels gaining share?

Yes—retailers like Walmart, Costco, and Tesco are expanding affordable premium private-label lines, pressuring legacy brands to innovate or reposition in the Global Pet Care Market.

How are regulations affecting product claims?

Stricter enforcement (e.g., FDA in the U.S., FEDIAF in Europe) is curbing unsubstantiated “natural” or “therapeutic” labels—requiring clinical backing for health claims in the Global Pet Care Market.

What’s the outlook for the Global Pet Care Market through 2030?

Steady growth (CAGR ~6–7%) is expected, with total market size surpassing $300 billion by 2030—driven by emotional bonding, aging pet populations, and tech-integrated care ecosystems in the Global Pet Care Market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com