Global Pet Food Market Size, Share, Trends, & Growth Forecast Report, Segmented By Food Type (Dry Food, Wet Food/Canned Foods, Nutraceuticals/Supplements, Snacks & Treats, and Veterinary Diets), Pet Type (Dog, Cat and Fish), Sales Channels (Specialized Pet Stores, Supermarkets & Hypermarkets, And Online Stores) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034

Global Pet Food Market Size

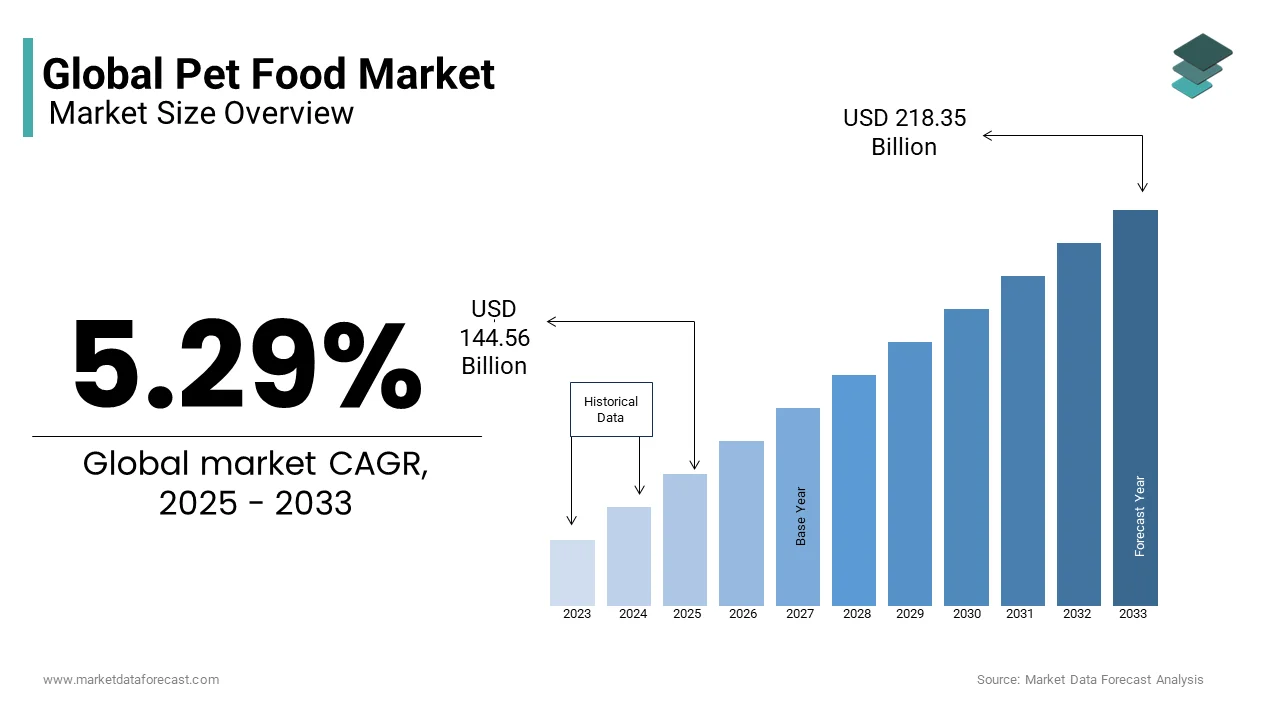

The global pet food market was valued at USD 144.56 billion in 2025 and is anticipated to reach USD 152.21 billion in 2026 from USD 229.90 billion by 2034, growing at a CAGR of 5.29% during the forecast from 2026 to 2034.

The pet food is a commercial product designed to meet the nutritional requirements of domestic animals, including dogs, cats, birds, and small mammals. It integrates dry, wet, and semi-moist formulations, fortified with vitamins, minerals, and specialized proteins to support animal health and wellness. Rising urbanization and pet adoption, particularly in Asia-Pacific and North America, have heightened the demand for convenient, nutritionally balanced pet food. According to the American Pet Products Association, over 70% of U.S. households own a pet, driving steady consumption growth.

MARKET DRIVERS

Rising Pet Adoption and Humanization of Pets

The increasing trend of treating pets as family members is accelerating the growth of the pet food market. Pet owners are prioritizing premium, nutritionally enriched products to support longevity and well-being. According to the American Pet Products Association, approximately 85 million U.S. households own a pet, and 60% of pet owners purchase premium or specialized pet food. The Asia-Pacific region has witnessed a similar surge, with pet adoption growing 10–12% annually in countries such as China and India, as per the China Pet Industry Association.

Innovation in Functional and Specialty Pet Foods

Technological advancements and R&D investments have enabled manufacturers to introduce functional pet foods addressing specific health needs such as weight management, joint support, digestive health, and dental care, which is accelerating the growth of the pet food market. According to Euromonitor International, global functional pet food sales grew by over 8% in 2023, which demonstrates rising consumer willingness to pay for specialized nutrition. Formulations enriched with omega-3 fatty acids, antioxidants, and probiotics are increasingly preferred to enhance immunity and longevity. Moreover, trend-driven innovations such as plant-based proteins and hypoallergenic ingredients appeal to both pet and owner preferences. Companies are leveraging scientific research and veterinary partnerships to validate product efficacy, which boosts consumer trust and adoption rates, which is further propelling the growth of the market.

MARKET RESTRAINTS

High Product Costs Limiting Mass Adoption

Premium and specialty pet foods, while nutritionally advantageous, carry higher prices compared to conventional options, which is hindering the growth of the pet food market. As per Nielsen data, consumers in emerging economies often prioritize affordability over specialized nutrition, restricting market penetration in regions like Southeast Asia and Latin America. Small-scale pet owners and budget-conscious households may opt for homemade or conventional feeds, limiting the growth of high-margin product lines. Additionally, fluctuating raw material costs for proteins, grains, and supplements impact production expenses, potentially raising retail prices. The price sensitivity remains a significant restraint in regions where per-capita income levels are lower, which is curbing the adoption of premium pet food products and slowing market expansion in certain developing markets despite growing pet populations.

Regulatory Compliance and Labeling Challenges

The stringent regulatory oversight regarding ingredient quality, safety, and labeling standards is expected to hamper the growth of the pet food market. Agencies such as the U.S. Food and Drug Administration and the European Pet Food Industry Federation enforce strict guidelines on permissible additives, nutrient claims, and contamination control. Compliance requires substantial investments in testing, certification, and documentation, which can be burdensome for smaller manufacturers. Mislabeling or non-compliance may result in product recalls, legal penalties, and reputational damage, which discourages innovation and increases operational costs. Additionally, emerging markets in Asia and Africa are implementing evolving regulatory frameworks, posing challenges for multinational companies seeking uniform product formulations across regions.

MARKET OPPORTUNITIES

Expansion of E-Commerce and Online Retail Channels

The rapid growth of digital commerce is setting up new opportunities for the growth of the pet food market. Online platforms enable convenient doorstep delivery, subscription models, and personalized product recommendations. According to Statista, global online pet food sales increased by 15% in 2023, reflecting consumer preference for digital shopping. E-commerce allows brands to penetrate smaller towns and remote regions in the Asia-Pacific, where urbanization and smartphone adoption are accelerating. Companies can also leverage data analytics to track consumer behavior, optimize inventory, and offer targeted promotions.

Growing Demand for Organic and Natural Pet Foods

Health-conscious pet owners are increasingly seeking organic, natural, and non-GMO pet food options, which is another factor contributing to the growth of the pet food market. According to the Pet Food Institute, sales of organic pet food products grew over 10% in 2023 in North America. This trend is driven by owner concerns over synthetic additives, antibiotics, and preservatives in conventional feeds. Manufacturers are capitalizing on this by offering plant-based, grain-free, and holistic recipes that appeal to ethical and wellness-oriented consumers. Emerging markets in Asia-Pacific, including Japan, South Korea, and India, show rising interest in organic formulations due to increasing disposable income and awareness of pet health. This shift opens opportunities for premium product lines, specialized marketing campaigns, and export-oriented strategies targeting discerning consumer segments.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Fluctuations

Manufacturers rely on a stable supply of high-quality proteins, grains, and supplements, which limits the growth of the pet food market. Volatility in global commodity prices, due to climate change, geopolitical tensions, or trade restrictions, poses challenges to consistent production and cost management. For example, protein prices, including poultry and fishmeal, fluctuated by over 12% in 2023 according to FAO data, impacting profitability. Supply chain disruptions can delay deliveries, inflate production costs, and affect product availability, especially for perishable wet food. These challenges necessitate robust sourcing strategies, strategic partnerships, and inventory management solutions to mitigate risk by ensuring manufacturers can maintain both quality and competitive pricing across global markets.

Competition from Homemade and Alternative Diets

The rising popularity of homemade pet meals and alternative diets for commercial use is also expected to slow the growth of the pet food market. Pet owners increasingly prepare home-cooked meals or adopt raw feeding regimens, believing these methods offer superior nutrition. According to a 2023 survey by the American Veterinary Medical Association, over 25% of U.S. pet owners prepare at least some meals at home. This trend is particularly evident in the Asia-Pacific region, where cultural practices often favor traditional feeding methods. Commercial pet food companies must differentiate their products through scientific validation, premium nutrition claims, and convenience benefits to compete effectively, while addressing consumer concerns over authenticity, quality, and perceived health benefits of alternative feeding practices.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.29% |

| Segments Covered | By Pets Type, Food Type, Sales Channel, and Region |

| Various Analyses Covered | Global, Regional, and country-level analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Nestlé Purina, Mars, Inc., Agthia Group, Hill's Pet Nutrition, JM Smucker Company, LUPUS Alimentos, General Mills, Inc., WellPet LLC, Total Alimentos, The Hartz Mountain Corp, Archer Daniel Midlands, Diamond Pet Foods, Blue Buffalo, Simmons Pet Foods, Agrolimen SA, Deuerer, and Heristo AG. |

SEGMENTAL ANALYSIS

By Pet Insights

The dry dog food segment held a dominant share of the global pet food market in 2025 with its convenience, long shelf life, and cost-effectiveness compared to wet food. According to the American Pet Products Association, 63% of U.S. dog owners prefer dry kibble for everyday feeding due to ease of storage and feeding, particularly for urban households. Additionally, dry food facilitates dental health benefits by reducing tartar and plaque accumulation, making it a preferred choice among health-conscious pet owners.

The dog segment accounted for the majority share of the global pet food market because of the rising demand for canines in all parts of the world. Dogs are also increasingly used in ranches, criminal tracking, and house safety, which is also contributing to the growth of this pet type. Also, the rise in consumer disposable income, coupled with the emphasis on the health of pets, is creating a positive aspect for the adoption of dogs across the world. Similarly, cats are also expected to witness more adoption in the coming years, creating a market for more animal-based protein foods and supplements.

The dog snacks and treats segment is expected to grow at a CAGR of 8.5% during the forecast period. This rapid growth is fueled by the humanization trend, where owners treat dogs as family members and seek indulgent, functional, or health-enhancing treats. Functional treats enriched with omega-3 fatty acids, vitamins, and probiotics are gaining popularity for joint health, digestion, and immunity. The rising disposable incomes and increased e-commerce penetration are driving the adoption of premium dog treats.

By Pet Insights

The wet cat food segment was the largest by capturing 50.3% of the global pet food market share in 2024. Its dominance is driven by higher palatability, hydration benefits, and acceptance by fussy eaters. Cats are naturally less inclined to drink water, and wet food contributes to urinary tract health and kidney function, making it preferred by veterinarians. In North America, 58% of cat owners feed wet food at least three times per week, as per the American Pet Products Association. In addition, premium wet food formulations with natural ingredients, grain-free recipes, and functional nutrients have encouraged adoption among affluent urban households in Europe and the Asia-Pacific.

The cat snacks and treats segment is likely to register a CAGR of 9.2% from 2025 to 2033, with the rising trend of rewarding pets, combined with functional treats targeting hairball reduction, digestion, and dental care. In the Asia-Pacific region, countries such as Japan and South Korea are witnessing increased premiumization, with pet owners willing to spend more on indulgent treats. Online retail expansion and subscription models have made it easier for consumers to access specialty cat treats, and brands are launching innovative flavors and health-focused options, further stimulating the segment.

REGIONAL ANALYSIS

North America Market Analysis

North America was the top performer of the global pet food market with 30.2% of the share in 2024. High pet ownership rates, premiumization trends, and health-conscious consumers drive market growth. Consumers increasingly seek functional, natural, and organic pet foods, while e-commerce platforms facilitate convenient access. The U.S. has witnessed a 12% increase in online pet food subscriptions in 202,y reflecting digital adoption. Additionally, veterinary endorsements and wellness-oriented marketing campaigns reinforce consumer trust in premium products.

Europe Market Analysis

Europe accounted in holding 25.3% of the global pet food market share in 2024, with countries like Germany, France, and the UK leading. The market benefits from well-established retail chains, high disposable income, and strong demand for organic and functional pet foods. According to the European Pet Food Federation, over 70% of households in Western Europe own at least one pet, and specialized diets for weight management, skin, and coat health are expanding.

Asia-Pacific Market AnalysThe is

Asia-Pacific pet food market is likely to experience significant growth opportunities throughout the forecast period. Countries such as China, Japan, and India are driving demand due to rising urbanization, nuclear households, and growing pet adoption rates. According to the China Pet Industry Association, pet ownership grew by 12% in 2023. The expansion of e-commerce platforms, rising disposable income, and the humanization trend are major growth drivers. Premiumization and innovative product launches, particularly in functional and natural pet foods, further stimulate consumption.

Latin America Market Analysis

Latin America's pet food market growth is more likely to have significant growth in the coming years, with Brazil and Mexico being key contributors. Increasing pet adoption, urban lifestyles, and the growth of modern retail outlets are driving demand. According to the Brazilian Association of the Pet Industry, over 50 million households in Brazil own pets, and pet food expenditure is rising annually by approximately 7%. Consumers are shifting toward packaged and functional pet foods over traditional homemade feeding practices.

Middle East & Africa Market Analysis

The Middle East and Africa pet food market is expected to have a steady pace in the coming years. Pet adoption in the Gulf Cooperation Council countries and South Africa is growing steadily due to rising disposable income and urbanization. According to Euromonitor International, premium pet food demand increased by 10% in the UAE in 2023.

COMPETITIVE LANSCAPE

The Asia Pacific pet food market is characterized by intense competition among established global brands and emerging local players. Leading companies like Mars Petcare, Nestlé Purina PetCare, and Hill’s Pet Nutrition continuously innovate to meet the evolving needs of pet owners. The increasing humanization of pets and the rising demand for premium and specialized pet food products have intensified competition. Additionally, the growth of e-commerce platforms has provided both opportunities and challenges for market participants, which is necessitating a strong online presence and efficient distribution strategies to maintain competitiveness.

KEY MARKET PLAYERS

Some of the major key players involved in the global pet food market are.

- Nestlé Purina

- Mars, Inc.

- Agthia Group

- Nestlé Purina PetCare

- Hill's Pet Nutrition

- JM Smucker Company

- LUPUS Alimentos

- General Mills, Inc.

- WellPet LLC

- Total Alimentos

- The Hartz Mountain Corp

- Archer Daniel Midlands

- Diamond Pet Foods

- Blue Buffalo

- Simmons Pet Foods

- Agrolimen SA

- Deuerer

- Heristo AG.

Top Players In The Market

- Mars Petcare has significantly strengthened its presence in the Asia Pacific region by establishing its first comprehensive pet food R&D center in Thailand. This state-of-the-art facility, located in the Amata City Chonburi Industrial Estate, spans 3,360 square meters and is designed to support the development of innovative pet food products tailored to regional preferences. The center employs cutting-edge technology to study pet consumption behaviors, optimal serving sizes, and food digestibility. This strategic move elevates Mars Petcare's commitment to enhancing pet nutrition and expanding its footprint in the rapidly growing Asia Pacific market.

- Nestlé Purina PetCare has bolstered its operations in the Asia Pacific by investing approximately $144 million in a new state-of-the-art pet food manufacturing facility in Rayong, Thailand. This facility is dedicated to producing wet pet food for both the local Thai market and various international markets. The investment reflects Nestlé Purina's strategic focus on expanding its production capabilities to meet the growing demand for high-quality pet food products in the region.

- Hill’s Pet Nutrition has reinforced its position in the Asia Pacific pet food market by focusing on premium and therapeutic diets. The company emphasizes clinically proven nutrition tailored to specific health conditions, offering well-established brands like Science Diet and Prescription Diet. Hill’s collaborates closely with veterinary professionals across the region to promote preventive healthcare for pets. This approach aligns with the growing consumer demand for specialized and health-focused pet food products by allowing Hill’s to cater to the needs of pet owners seeking optimal nutrition for their pets.

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific pet food market employ several strategies to strengthen their market positions:

- Product Innovation: Developing new formulations and flavors to meet the diverse preferences of pet owners in the region.

- Strategic Partnerships: Collaborating with veterinary professionals and research institutions to enhance product offerings and credibility.

- Expansion of Manufacturing Facilities: Investing in state-of-the-art production facilities to increase capacity and meet growing demand.

- E-commerce Integration: Enhancing online presence and distribution channels to reach a broader customer base.

- Sustainability Initiatives: Implementing eco-friendly practices in sourcing and packaging to appeal to environmentally conscious consumers.

RECENT MARKET NEWS

- In April 2024, Mars Petcare opened its first comprehensive pet food R&D center in Thailand, aiming to enhance product innovation and cater to regional preferences.

- In June 2022, Nestlé Purina PetCare invested approximately $144 million in a new pet food manufacturing facility in Rayong, Thailand, to expand production capabilities.

- In March 2025, Hill’s Pet Nutrition launched a new line of grain-free therapeutic diets, addressing the growing demand for specialized pet food products.

- In August 2023, Mars Petcare partnered with local veterinary clinics in India to promote preventive healthcare and increase brand visibility.

- In February 2025, Nestlé Purina PetCare introduced a subscription-based delivery service for pet food in Japan, enhancing customer convenience and loyalty.

MARKET SEGMENTATION

This research report on the global pet food market has been segmented & sub-segmented based on the pet, ingredients, form, and region.

By Pet Type

- Dogs

- Cats

- Others

By Food Type

- Dry Food

- Wet Food/Canned Foods

- Nutraceuticals/Supplements

- Snacks & Treats

- Veterinary Diets

By Sales Channel

- Specialized Pet Stores

- Supermarkets & Hypermarkets

- Online Stores

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the current size of the pet food market?

The pet food market is expected to be valued at USD 218.35 Million in 2025.

Which regions are leading in terms of market share for pet food consumption?

North America and Europe currently lead in market share for pet food consumption, driven by high pet ownership rates and strong demand for premium pet food products.

What are the key trends driving growth in the pet food market in Asia Pacific?

In Asia Pacific, increasing urbanization, rising disposable incomes, and changing lifestyles are driving the demand for pet food, especially premium and natural products.

How is the pet food market in North America responding to consumer preferences for natural and organic pet food?

In North America, the pet food market is witnessing increased demand for natural and organic pet food products, with consumers seeking healthier options for their pets.

Which companies are the major players in the pet food market in the United States?

Companies such as Mars Petcare Inc., Nestle Purina Petcare, and Hill's Pet Nutrition Inc. are among the major players in the pet food market in the United States.

Who are the key players dominating the pet food market in Europe?

Companies such as Mars Petcare, Nestle Purina Petcare, and Hill's Pet Nutrition are among the key players dominating the pet food market in Europe.

What’s driving growth in the global pet food market?

Pet humanization is a key force—owners increasingly treat pets as family, demanding premium, nutritious, and tailored food options.

How are consumer preferences shaping pet food trends?

Clean-label demands are pushing brands to use natural, recognizable ingredients with no artificial additives.

What role does pet health play in purchasing decisions?

Owners are more aware of diet-related health issues, so they seek foods that support longevity, weight control, and immunity.

How is e-commerce changing pet food sales?

Online platforms and subscription models offer convenience, personalized recommendations, and fast delivery.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com