Global Pet Tech Market Size, Share, Trends, and Growth Analysis Report, Segmented By Type, Product, Application, End Use, Distribution Channel, & Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa), Industry Forecast From 2026 to 2034

Global Pet Tech Market Summary

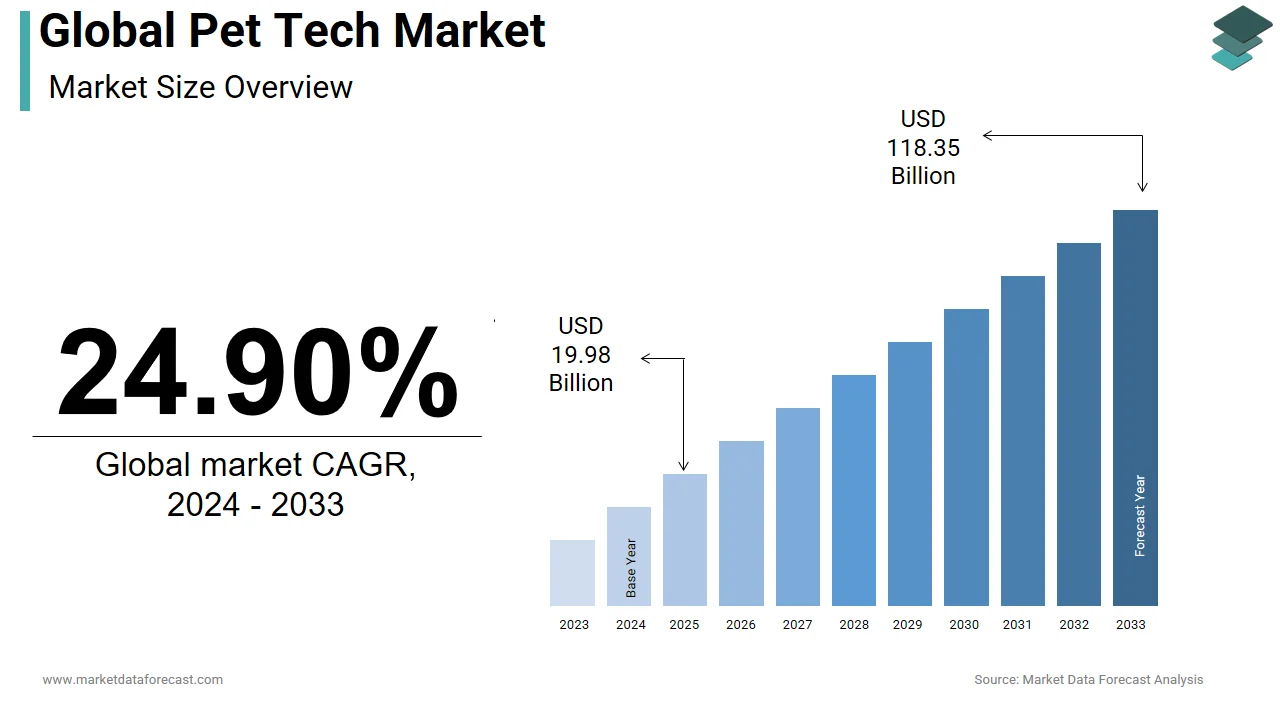

The global pet tech market was valued at USD 19.98 billion in 2025, is expected to reach USD 24.96 billion in 2026, and is projected to reach USD 147.79 billion by 2034, growing at a strong CAGR of 24.90% during 2026 to 2034. Growth is driven by rising pet humanization, expanding telehealth adoption, and increasing use of AI/IoT-enabled devices for pet safety, health tracking, and daily care automation.

Key Insights

- 2025 Market Size: USD 19.98 billion

- 2026 Estimate: USD 24.96 billion

- 2034 Forecast: USD 147.79 billion

- CAGR (2026–2034): 24.90%

- Largest Type Segment: RFID – 38.2% share

- Fastest-Growing Type: GPS tracking – 18.3% CAGR

- Top Product Segment: Monitoring equipment – 45.3% share

- Leading Application: Pet safety – 55.3% share

- Top Region (2025): North America – 40.3% share

- Major Growth Driver: Pet humanization + telehealth surge

Market Snapshot

Pet tech includes smart wearables, GPS trackers, automated feeders, connected monitoring devices, and AI-powered health tools that improve pet safety, wellness, and daily care. Rising pet ownership, premiumization of pet services, and growing acceptance of telehealth and remote monitoring solutions are key factors accelerating global adoption.

Market Insights: Key Long-Tail Questions Answered

Why is the pet tech market growing?

- Growth is driven by rising pet humanization, increased spending on premium pet care, expansion of veterinary telehealth, and rapid adoption of AI- and IoT-enabled monitoring and safety devices.

Which segment leads the global pet tech market?

- The RFID segment dominated the market in 2024 with 38.2% share, supported by mandatory microchipping regulations and its reliability for permanent pet identification.

Which technology segment is growing the fastest?

- The GPS tracking segment is expanding at 18.3% CAGR, driven by rising demand for real-time location tracking, geofencing alerts, and pet safety monitoring.

Global Pet Tech Market Size

The size of the global pet tech market was worth USD 19.98 billion in 2025. The global market is anticipated to grow at a CAGR of 24.90% from 2026 to 2034 and be worth USD 147.79 billion by 2034 from USD 24.96 billion in 2026.

The pet tech is a digital and connected solution designed to enhance pet care, safety, health monitoring, and owner convenience. This includes wearables, GPS trackers, automated feeders, telehealth platforms, and AI-powered behavioral training tools. The market’s expansion is driven by rising pet adoption, especially in urban households, where pets are increasingly treated as family members.

MARKET DRIVERS

Humanization of Pets and Lifestyle Integration

The increasing humanization of pets is a major factor propelling the growth of the Pet Tech Market. Owners now seek solutions that mirror human health and wellness technology, extending into pet fitness, diet tracking, and emotional care. According to the European Pet Food Federation, 91 million households in Europe owned at least one pet in 2022, with spending shifting toward premium and tech-enabled services. Urbanization trends and rising disposable incomes amplify this integration, where pet owners invest in smart collars, health trackers, and automated feeding systems to align with busy lifestyles. Wearables capable of monitoring heart rate, calorie intake, and stress levels highlight the crossover between pet care and digital health, driving adoption globally.

Growth in Veterinary Telehealth and Remote Monitoring

The surge in veterinary telehealth solutions has strengthened the adoption of connected technologies for continuous pet care is solely escalating the growth of pet tech Market. As per the American Veterinary Medical Association, telehealth consultations rose by more than 200% during the pandemic, signaling a sustained shift toward digital veterinary services. Remote monitoring devices such as smart cameras, health patches, and GPS-enabled trackers allow veterinarians and owners to observe vital signs, detect anomalies, and intervene earlier. This demand is also tied to rising chronic conditions in pets, with the Association for Pet Obesity Prevention noting that 59% of dogs and 61% of cats in the U.S. were classified as overweight or obese in 2022.

MARKET RESTRAINTS

High Cost of Devices and Limited Affordability in Developing Regions

The adoption of advanced technologies such as AI-driven wearables, robotic companions, and telemedicine platforms is often constrained by high purchase and subscription costs. For instance, premium GPS trackers and health collars can cost between USD 100 to USD 300, which excludes monthly service fees. In regions with lower pet care expenditure, this creates a substantial adoption barrier. According to the World Bank, over 40% of households in low- and middle-income countries spend less than USD 5 per day on all non-essential goods, making expensive pet tech solutions less accessible. This affordability gap limits penetration outside affluent urban households and delays widespread adoption in emerging markets, where pet ownership rates are nonetheless rising rapidly.

Data Privacy and Connectivity Concerns

As pet tech increasingly relies on IoT platforms, cloud-based analytics, and GPS connectivity, concerns over data privacy and security present a restraint to growth. Devices collect sensitive geolocation data, health metrics, and behavioral patterns of pets, often linked directly to owners’ personal information. According to the International Telecommunication Union, nearly 40% of global users express distrust in IoT-enabled devices due to data handling risks. Inconsistent internet connectivity in rural or underdeveloped areas further hinders the seamless use of real-time trackers and telehealth apps.

MARKET OPPORTUNITIES

Expansion of AI and Predictive Analytics in Pet Health

Artificial intelligence is creating significant opportunities by enabling predictive diagnostics and preventive care for pets, which is likely to have a significant growth of the pet tech Market. Smart collars and biosensors integrated with AI can detect early signs of illness, predict seizure risks, or monitor behavioral changes to identify stress disorders. According to the National Institutes of Health, over 20% of domesticated dogs are prone to chronic diseases such as arthritis and diabetes, conditions that benefit from early intervention. AI-driven platforms allow veterinarians to anticipate these issues and recommend treatment before symptoms worsen.

Integration with Smart Home Ecosystems

The rise of smart homes offers an opportunity for seamless integration of pet care devices with broader connected ecosystems, which is another factor significantly boosting the growth of pet tech Market. The number of smart homes is projected to exceed 500 million by 2026. This trend allows pet tech devices such as feeders, monitoring cameras, and health trackers to synchronize with voice assistants and home automation systems, offering real-time updates and control. Owners can remotely monitor food intake, hydration, and activity levels while receiving alerts through existing smart home hubs. This ecosystem integration not only increases convenience but also enhances device adoption, as consumers prefer multi-functional connected solutions rather than standalone systems.

MARKET CHALLENGES

Lack of Standardization Across Devices

The absence of standardized protocols across different devices and platforms, which hinders interoperability and long-term adoption, is challenge to the growth of pet tech Market. Pet tech products often operate on proprietary systems, limiting their ability to integrate with veterinary health records or other smart home devices. According to the IEEE Standards Association, nearly 60% of IoT devices in consumer markets face interoperability issues, causing fragmented user experiences. For pet owners and veterinarians, this inconsistency complicates monitoring, reduces efficiency, and discourages investment in multiple devices.

Limited Awareness and Training Among Pet Owners

While adoption is increasing in developed economies, many pet owners remain unaware of the potential benefits and applications of pet tech. According to the World Veterinary Association, over 55% of pet owners in emerging economies rely solely on traditional care methods and have limited exposure to digital solutions. Lack of training in device usage, skepticism regarding accuracy, and reliance on manual observation often undermine the market’s potential. Moreover, in rural and semi-urban areas, veterinarians themselves may have limited experience with advanced monitoring devices, restricting effective implementation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Product, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | GoPro, Inc., FitBark Inc., Garmin International Inc., CleverPet Inc., Dogtra Co., Konectera Inc., Lo8tor Ltd, Mars Incorporated, Lupine Pet, Motorola Solutions Inc., Wagz Inc., Tractive GmbH, Smart Pet Love, Scollar Inc., Pod Tracker ANZ Pty Ltd, PetSmart Inc., PetPace LLC, PETKIT, and Powbo Inc., among others. |

SEGMENTAL ANALYSIS

By Type Insights

The RFID segment was the largest and held 38.2% of the Pet Tech Market share in 2024 due to its reliability in permanent identification of pets. Unlike external collars or tags that can be lost, RFID microchips provide lifelong identification. According to the World Small Animal Veterinary Association, over 70% of dogs and 40% of cats in developed regions are microchipped, which shows the trust pet owners place in RFID for reunification in cases of loss. The rising regulatory mandates in countries such as Australia and across Europe, where pet microchipping is legally required, further strengthen RFID’s dominance.

The GPS segment is projected to grow with a CAGR of 18.3% during the forecast period for real-time location tracking and pet safety monitoring. According to the American Humane Association, approximately 10 million pets go missing every year in the United States, underlining the necessity for proactive location tracking. Modern GPS collars integrate geofencing, activity tracking, and health analytics, offering far more functionality than RFID. The trend is particularly strong in the Asia Pacific, where urban pet owners face risks of overcrowding and theft, pushing adoption.

By Product Insights

The monitoring equipment segment was the largest by capturing 45.3% of the pet tech Market share in 2024, with the need for constant observation of pets’ health and well-being. Devices such as smart cameras, biometric collars, and connected feeders fall under this category. Owners also use smart cameras to monitor behavioral patterns while away from home, an essential demand in dual-income households. This aligns with broader humanization trends, where preventive care and continuous health oversight are prioritized.

The entertainment equipment segment is expected to witness a CAGR of 16.3% throughout the forecast period, owing to the rising awareness of pet mental health. The University of Bristol noted in a study that 80% of dogs left alone for extended periods exhibit signs of separation anxiety. Demand is particularly notable in urban environments, where limited outdoor spaces push owners to seek indoor entertainment solutions for pets.

By Application Insights

The pet safety applications segment was the largest by occupying 55.3% of the share in 2024 by ensuring that pets’ physical protection and location security remain a top priority for owners. The U.S. Federal Emergency Management Agency indicates that nearly 30% of pets are lost during natural disasters or emergencies due to the growing importance of safety technology. Devices like smart fences, geofencing trackers, and automatic locking systems are being increasingly adopted.

The pet healthcare segment is expected to witness a CAGR of 17.3% during 2025–2033 ,with the surge in chronic conditions among pets and demand for preventive health technologies. According to the Association for Pet Obesity Prevention, over 59% of dogs and 61% of cats in the U.S. were obese in 2022. Wearable devices tracking vitals such as heart rate, temperature, and calorie expenditure are increasingly used to assist veterinarians in remote consultations.

REGIONAL ANALYSIS

North America Market Analysis

North America was the top performer of the Pet Tech Market with 40.3% of share in 2024, which is attributed to high pet ownership and advanced digital adoption. According to the American Pet Products Association, 66% of U.S. households own at least one pet, equating to around 87 million dogs and 62 million cats. The region is home to several leading pet tech innovators, and strong investment in IoT infrastructure supports real-time monitoring. Veterinary telehealth regulations are also more favorable compared to other regions by making North America the most technologically mature market.

Europe Market Analysis

Europe held second position by occupying 28.3% of the pet tech market share in 2024, with the growing strict animal welfare regulations and widespread pet microchipping mandates. According to the European Pet Food Federation, over 91 million households own pets across the continent, with dogs and cats beingthe most prevalent. Rising concerns about pet abandonment have increased the adoption of tracking devices, particularly RFID. Western Europe, including the UK, France, and Germany, is leading technological adoption, while Eastern Europe is catching up due to rising urbanization and awareness.

Asia Pacific Market Analysis

Asia Pacific is expected to grow with a prominent CAGR during the forecast period, with the rising middle class, rapid urbanization, and increasing pet ownership. China alone has seen its urban pet dog population exceed 54 million in 2022, as reported by the National Bureau of Statistics of China. Pet humanization trends are spreading rapidly, and owners are more inclined to invest in safety and health technologies.

Latin America Market Analysis

Latin America pet tech market growth is likely to grow with the rising awareness of pet healthcare and safety technologies. Brazil leads the region, as it has the second-largest dog population globally at over 55 million, according to the Brazilian Institute of Geography and Statistics. However, affordability constraints limit adoption of premium products, leading to a preference for cost-effective RFID and entry-level monitoring devices.

Middle East & Africa Market Analysis

The Middle East & Africa pet tech market growth is likely to grow steadily, with adoption concentrated in high-income countries such as the UAE, Saudi Arabia, and South Africa. According to the Dubai Statistics Center, the UAE has experienced a steady rise in pet ownership, particularly among expatriate communities.

COMPETITIVE LANDSCAPE

The Pet Tech Market is highly competitive, marked by the presence of established multinationals alongside innovative startups. Larger players such as Garmin, Whistle, and Sure Petcare dominate through brand recognition, technological sophistication, and extensive distribution channels, while smaller regional firms differentiate with localized solutions and affordability. Competition has intensified with the rise of Asia Pacific as the fastest-growing hub, where cultural differences and cost-sensitive consumers demand tailored approaches. Players are racing to integrate healthcare monitoring with GPS and entertainment solutions, thereby offering comprehensive ecosystems rather than standalone products. Technological integration, regulatory compliance on data security, and consumer trust are shaping the competitive dynamics.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global pet tech market include

- GoPro, Inc.

- FitBark Inc.

- Garmin International Inc.

- CleverPet Inc.

- Dogtra Co.

- Konectera Inc.

- Lo8tor Ltd

- Mars Incorporated

- Lupine Pet

- Motorola Solutions Inc.

- Wagz Inc.

- Tractive GmbH

- Smart Pet Love

- Scollar Inc.

- Pod Tracker ANZ Pty Ltd

- PetSmart Inc.

- PetPace LLC

- PETKIT

- Powbo Inc.

- Others

Top Strategies Used by Key Market Participants

Key players in the Pet Tech Market have adopted multifaceted strategies to sustain growth and expand penetration across Asia Pacific. Product innovation remains a cornerstone, with companies integrating artificial intelligence, IoT, and cloud-based analytics into smart collars, feeders, and health monitoring devices. Strategic partnerships with veterinary hospitals, e-commerce platforms, and telecom providers have also been prioritized, ensuring both distribution reach and added value in healthcare ecosystems. Geographic expansion is evident, with brands like Whistle and Sure Petcare extending their retail presence in Japan, Australia, and China, leveraging the surge in urban pet ownership. Additionally, acquisitions and investments in startups have accelerated the incorporation of advanced features such as biometric sensing and behavioral tracking.

Top Players in the Pet Tech Market

- Whistle Labs, based in the United States but heavily active in the Asia Pacific, specializes in GPS-enabled smart collars and health monitoring devices. The company has expanded its reach in Asia through partnerships with veterinary clinics and e-commerce platforms, offering integrated data solutions that allow owners to track activity, location, and overall health metrics. In recent years, Whistle has introduced AI-driven insights into its collars, providing proactive alerts for early detection of illnesses. In the Asia Pacific region, the company collaborates with distribution networks in Japan, South Korea, and Australia to address the rising demand for advanced monitoring solutions.

- Garmin is a global leader in GPS technology and has significantly contributed to the Asia Pacific pet tech market through its specialized tracking devices, including the Garmin Alpha and Astro series. These products are designed not only for domestic pet safety but also for working and sporting dogs, which are prevalent in countries such as Australia. Garmin’s competitive edge lies in its accuracy and robust outdoor functionality, which resonates well with rural and semi-urban markets in the Asia Pacific. The company’s ongoing product updates, focusing on smaller device sizes and improved battery life, highlight its commitment to expanding adoption across diverse consumer bases.

- Sure Petcare has been expanding its Asia Pacific presence with connected pet doors, feeders, and activity monitors. The company leverages RFID and sensor-based technologies to provide seamless solutions for feeding management and access control, particularly popular in urban households with multiple pets. Its parent company, MSD Animal Health, has enabled Sure Petcare to integrate veterinary data with its consumer devices, strengthening the healthcare aspect of pet technology. In the Asia Pacific, Sure Petcare has established direct-to-consumer sales through online retail platforms and continues to innovate around IoT-based ecosystems that support both safety and healthcare monitoring.

GLOBAL PET TECH MARKET NEWS

- In April 2024, Whistle Labs Pet Tech Market launched its AI-powered health monitoring platform in Japan, designed to detect early signs of chronic diseases in pets. This Pet tech market initiative is anticipated to strengthen its footprint in preventive healthcare solutions.

- In February 2023, Garmin Pet Tech enhanced its Astro series trackers with real-time geofencing alerts. This Pet tech market upgrade is anticipated to strengthen customer loyalty and broaden application among sporting and domestic pet owners.

MARKET SEGMENTATION

This research report on the global pet tech market has been segmented and sub-segmented into the following categories.

By Type

- RFID

- GPS

- Sensors

- Others

By Product

- Monitoring Equipment

- Tracking Equipment

- Entertainment Equipment

- Feeding Equipment

- Pet Wearables

- Others

By Application

- Pet Safety

- Pet Healthcare

- Pet Owner Convenience

- Communication & Entertainment

By End Use

- Household

- Commercial

By Distribution Channel

- Offline

- Online

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What was the size of the global pet tech market in 2025?

The global pet tech market was valued at USD 19.98 billion in 2025.

2. What is the expected market size by 2033?

The market is projected to reach USD 118.35 billion by 2033.

3. What is the CAGR of the global pet tech market?

The market is expected to grow at a CAGR of 24.90% from 2025 to 2033.

4. Which region dominated the pet tech market in 2024?

North America led the global market with a 40.3% share in 2024.

5. Which product segment holds the largest share?

Monitoring equipment held the largest share at 45.3% in 2024.

6. Which technology segment is growing the fastest?

The GPS tracking segment is the fastest-growing, expanding at 18.3% CAGR.

7. What is the largest type segment in the market?

The RFID segment dominated with a 38.2% share in 2024.

8. What factors are driving the growth of the pet tech market?

Key drivers include rising pet humanization, telehealth expansion, smart home integration, and increased adoption of AI/IoT pet monitoring devices.

9. What is the leading application segment?

Pet safety was the leading application, accounting for 55.3% share in 2024.

10. Which companies are key players in the global pet tech market?

Major companies include Garmin, GoPro, FitBark, Tractive, PetPace, PETKIT, Wagz, and Motorola Solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com