Global Rigid Packaging Market Size, Share, Trends & Growth Forecast Report By Material, By Product Type, By End-Use, and By Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) – Industry Analysis and Forecast, 2025 to 2033

Global Rigid Packaging Market Size

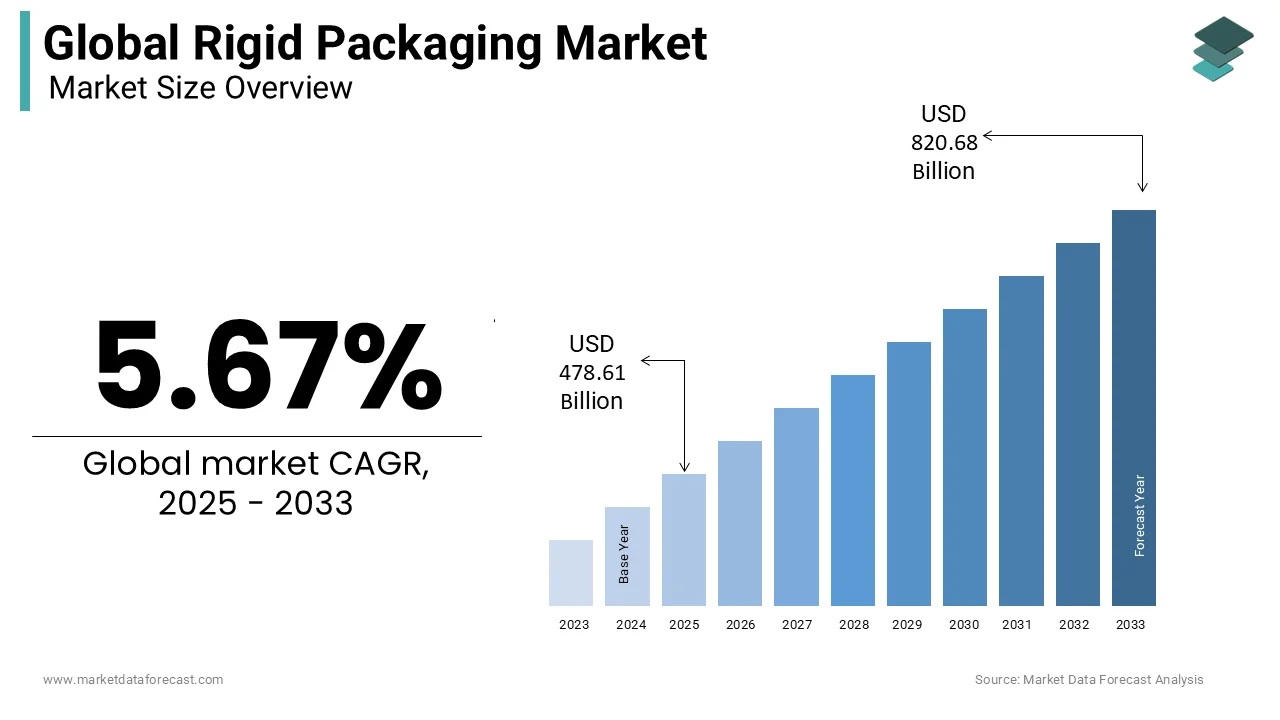

The global rigid packaging market was valued at USD 452.96 billion in 2024, is estimated to reach USD 478.61 billion in 2025, and is projected to reach USD 820.68 billion by 2033, growing at a CAGR of 5.67% from 2025 to 2033.

Rigid packaging is a fixed shape and provides durable protection for its contents. These packaging solutions include bottles, jars, cans, cartons, and tubs, predominantly made from materials like plastics, glass, metals, and paperboard. The growing consumer preference for packaged goods, particularly in the food and beverage, pharmaceuticals, and personal care sectors, is driving demand for high-quality, secure, and visually appealing rigid packaging solutions. According to the International Packaging Institute, more than 40% of global consumers prefer products with reusable or tamper-proof packaging. Additionally, environmental concerns are prompting manufacturers to adopt recyclable and sustainable materials, with glass and metal-based rigid packaging witnessing increased adoption due to their low carbon footprint and durability, as per the World Packaging Organization.

MARKET DRIVERS

Rising Demand in the Food & Beverage Sector

The expansion of the food and beverage industry is one of the major factors for the growth of the rigid packaging market. Consumers increasingly prefer packaged foods for convenience, freshness, and safety, creating significant demand for durable bottles, jars, and cans. According to the Food Packaging Council, over 60% of packaged food products are now sold in rigid containers to ensure extended shelf life and prevent contamination. The growing adoption of ready-to-eat meals, beverages, and dairy products has further amplified this trend. Additionally, the demand for premium packaging for beverages like juices and carbonated drinks is propelling manufacturers to invest in high-quality, durable containers that enhance brand appeal and consumer trust.

Sustainability and Recyclability Initiatives

Environmental sustainability is another key driver influencing the rigid packaging market. Increasing regulatory pressure and consumer awareness regarding waste reduction are prompting companies to use recyclable and reusable materials such as aluminum, glass, and high-grade plastics. According to the Ellen MacArthur Foundation, nearly 90% of consumers prefer brands that offer recyclable packaging. Glass jars and metal cans, for example, can be recycled multiple times without losing structural integrity, reducing environmental impact. Many manufacturers are investing in lightweight rigid containers and using recycled feedstock, which not only decreases the carbon footprint but also aligns with global sustainability goals. This shift is further reinforced by government initiatives in Europe, North America, and Asia promoting circular economies in packaging industries.

MARKET RESTRAINTS

High Production Costs

The high cost associated with production, especially for materials like glass and metal, is restraining the growth of the rigid packaging market. The manufacturing process for rigid containers requires significant energy consumption, specialized machinery, and raw materials, which increases overall production costs. According to the International Energy Agency, energy-intensive manufacturing processes account for nearly 25% of total production costs in metal-based packaging. This price factor often discourages small- and medium-sized enterprises from adopting premium rigid packaging solutions. Additionally, the cost of raw materials like aluminum and high-grade plastics fluctuates due to global commodity market volatility, which is further impacting production budgets and profitability for packaging manufacturers.

Transportation and Storage Challenges

Rigid packaging is inherently heavier and bulkier than flexible alternatives, which leads to higher transportation and storage costs. Glass bottles and metal cans, while durable, require careful handling to prevent breakage, increasing logistical complexities. According to the World Bank, transportation costs for bulky containers can be up to 30% higher compared to flexible packaging solutions. Additionally, the need for specialized warehousing and cushioning materials for fragile containers contributes to operational inefficiencies. These logistical constraints limit adoption in regions where cost sensitivity is high or infrastructure is underdeveloped. Manufacturers must balance durability with operational efficiency, which can be a barrier to market penetration, especially in emerging economies.

MARKET OPPORTUNITIES

Premiumization of Consumer Products

The trend of premiumization in food, beverages, and personal care products offers significant opportunities for the rigid packaging market growth. Consumers increasingly associate premium packaging with superior quality, driving demand for high-end glass jars, metal tins, and innovative plastic containers. As per Euromonitor International, sales of premium packaged goods have grown by over 10% annually in the past five years, particularly in North America and Asia-Pacific. Companies are leveraging rigid packaging to differentiate their products, enhance shelf appeal, and attract brand-conscious consumers.

Technological Advancements in Material Innovation

Technological advancements in materials are another opportunity for the growth of the rigid packaging market. Innovations like lightweight glass, biodegradable plastics, and high-strength aluminum alloys enable manufacturers to produce durable, eco-friendly containers at reduced costs. According to the Packaging Technology Alliance, the adoption of lightweight yet robust containers has reduced material usage by up to 15% without compromising quality. Additionally, smart rigid packaging integrated with QR codes, anti-counterfeit measures, and tamper-evident features is gaining traction, particularly in pharmaceuticals and premium beverages. These technological innovations enhance consumer engagement, ensure product safety, and improve supply chain efficiency, creating new growth avenues for market participants.

MARKET CHALLENGES

Competition from Flexible Packaging

Rigid packaging faces stiff competition from flexible alternatives like pouches, sachets, and shrink films, which are cheaper, lighter, and easier to transport, posing a great challenge for the rigid packaging market players. According to Smithers Pira, flexible packaging adoption has grown by 8% annually in the past decade, primarily due to cost efficiency and convenience. Flexible packaging also reduces material usage and carbon emissions, creating sustainability advantages over rigid containers. This competitive landscape pressures rigid packaging manufacturers to innovate, cut costs, and justify the added benefits of durability and premium appeal, particularly in cost-sensitive markets.

Regulatory Compliance and Environmental Norms

Stringent environmental regulations and sustainability mandates pose another challenge to the rigid packaging market growth. Compliance with recycling standards, material restrictions, and waste management guidelines requires significant investment in infrastructure and monitoring. According to the European Commission, packaging producers must meet recycling targets of up to 75% for glass and metal containers by 2030. Non-compliance can lead to fines, product recalls, and reputational damage. Additionally, transitioning to fully recyclable or biodegradable rigid materials often increases production complexity and cost, creating operational challenges. Manufacturers must navigate these regulations while maintaining profitability and product quality, which is a significant barrier to market expansion.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Material, Product Type, End-Use, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Berry Global Inc., ALPLA Werke Alwin Lehner GmbH & Co KG, Sonoco Products Company, Plastipak Holdings, Inc., Crown Holdings, Inc., Ball Corporation, DS Smith Plc, Silgan Holdings, Inc., ALPLA Group |

SEGMENTAL ANALYSIS

By Material Insights

The plastic segment accounted in holding 42.3% of the rigid packaging market share in 2024, owing to its versatility and cost-effectiveness. Plastic containers can be molded into various shapes and sizes, which is making them ideal for industries ranging from food and beverages to pharmaceuticals. According to the International Plastics Institute, over 60% of single-use rigid containers in the consumer goods sector are made from plastics due to durability, lightweight properties, and low production costs. Another driving factor is the growing adoption of recyclable and high-density polyethylene (HDPE) plastics, which reduces environmental impact while maintaining product safety.

The glass segment is likely to witness a CAGR of 7.1% throughout the forecast period, with its recyclability and sustainability. Glass can be recycled infinitely without loss of quality, appealing to environmentally conscious consumers. Additionally, glass offers superior protection against chemical interactions, making it ideal for premium beverages, pharmaceuticals, and cosmetics. Premiumization trends and stricter regulations on plastic usage have further accelerated glass adoption, especially in the Asia-Pacific region, where consumer awareness regarding sustainable packaging is rising rapidly.

By Product Type Insights

The bottles and jars segment was the largest and held 38.3% of the rigid packaging market share in 202,4, owing to the widespread demand across food, beverage, pharmaceutical, and personal care industries. Bottles and jars provide high product safety, tamper resistance, and excellent barrier properties. Premium beverages, health supplements, and cosmetics further drive demand for aesthetically appealing jars and bottles, particularly glass and high-quality plastic variants.

The containers and cans segment is expected to grow with an expected CAGR of 6.8% during the forecast period due to increased adoption in the food and beverage sectors. According to the International Aluminum Association, demand for metal cans for beverages and ready-to-eat foods grew by 9% in 2023, driven by convenience and recyclability. Metal containers also provide superior shelf life, safety, and resistance to external damage compared to flexible alternatives. Urbanization, busy lifestyles, and rising consumption of canned foods in the Asia-Pacific contribute to growth. Additionally, regulatory incentives promoting recyclable packaging have encouraged manufacturers to adopt metal containers over plastics, further accelerating their adoption.

By End-Use Insights

The food & beverages segment was the largest and held 45.3% of the share in 2024. The increasing preference for packaged and processed foods drives this dominance. Consumers demand secure, hygienic, and long-lasting packaging for products such as dairy, beverages, snacks, and sauces. According to FAO statistics, global packaged food consumption grew by 8% in 2023, particularly in the Asia-Pacific region, creating robust demand for bottles, jars, and cans. Another driver is the rise of premium and ready-to-eat products requiring high-quality rigid packaging to ensure freshness and brand differentiation.

The personal care and cosmetics segment is likely to witness a CAGR of 7.3% throughout the forecast period, with the rising disposable income, increasing focus on hygiene and grooming, and the demand for premium packaging. High-quality rigid containers, such as glass jars, aluminum tins, and specialized plastic bottles, enhance brand image and provide product safety. The Asia-Pacific region shows the highest adoption due to increasing urbanization and rising cosmetics consumption, which grew by 10% in 2023. Innovations in sustainable packaging and aesthetically appealing designs further accelerate growth.

REGIONAL ANALYSIS

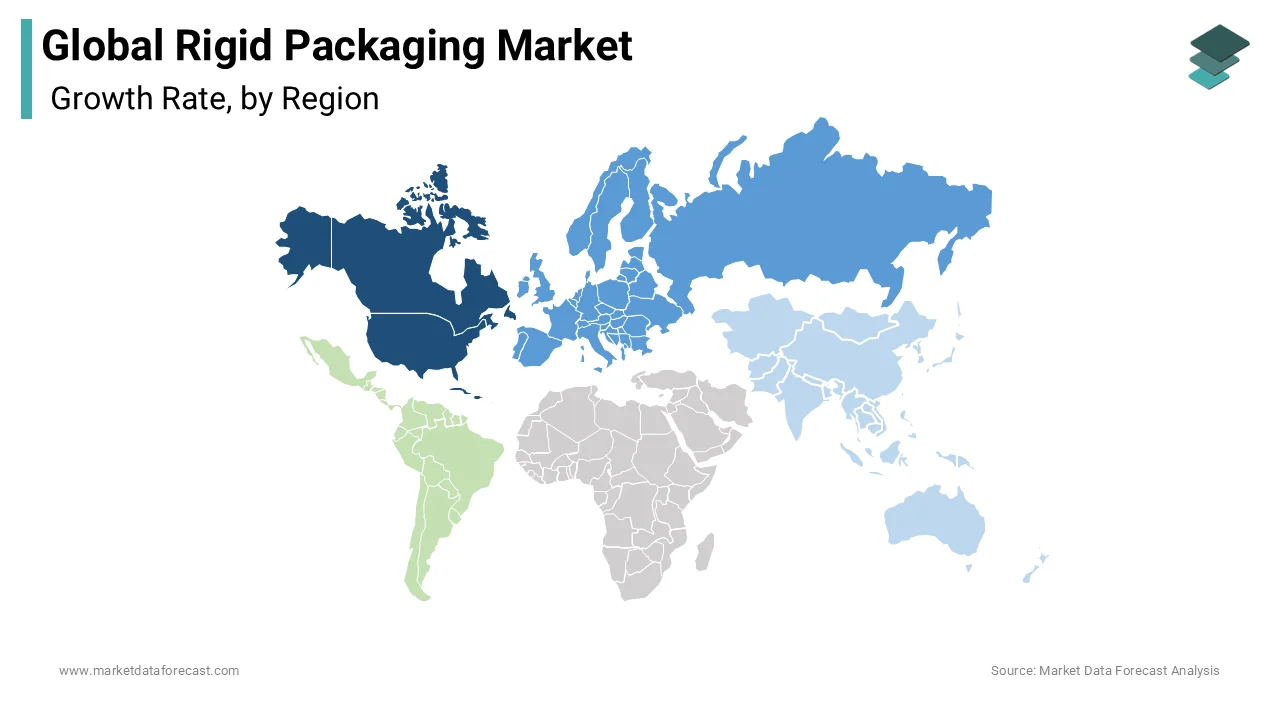

North America Rigid Packaging Market Analysis

North America market held 25.1% of the share in 2024 due to advanced manufacturing infrastructure and high consumer awareness about packaging safety. According to Smithers Pira, the U.S. rigid packaging sector saw 6% growth in 2023, driven by demand in food, beverages, and personal care. Innovation in recyclable materials and premium packaging further strengthens the region’s market presence.

Europe Rigid Packaging Market Analysis

Europe market held 21.4% of the share in 2024, with strong environmental regulations. Countries like Germany and France prioritize sustainable rigid packaging. According to the European Packaging Association, 70% of glass containers are recycled in Europe, which is driving the adoption of eco-friendly rigid packaging solutions.

Asia Pacific Rigid Packaging Market Analysis

Asia Pacific market is likely to grow with a prominent CAGR during the forecast period due to population growth, urbanization, and rising packaged goods consumption. India, China, and Japan lead the market. According to the World Packaging Organization, packaged food sales grew by 9% in 2023 in the Asia-Pacific region, which is fueling rigid packaging demand.

Latin America Rigid Packaging Market Analysis

Latin American market is experiencing steady growth with increasing packaged food consumption. Brazil and Mexico drive the market. The region faces logistical challenges, but opportunities exist in beverages and pharmaceuticals.

Middle East & Africa Rigid Packaging Market Analysis

The Middle East and Africa market growth is expected to grow with rapid urbanization and expanding FMCG sectors. According to FAO, packaged food consumption grew 7% in 2023. Sustainability initiatives are slowly being adopted, which is creating potential for growth.

COMPETITIVE LANDSCAPE

The rigid packaging market is highly competitive, characterized by the presence of multinational corporations such as Amcor, Berry Global, and RPC Group. Competition is driven by product quality, sustainability, innovation, and cost-effectiveness. Companies are investing heavily in recyclable and lightweight materials to address environmental concerns and regulatory pressures. Innovation in premium packaging, such as high-barrier containers and custom designs, provides differentiation in sectors like food, beverage, and cosmetics. Emerging markets in the Asia-Pacific region are attracting significant investments due to rapid urbanization, increased packaged goods consumption, and growing disposable income. Strategic partnerships, acquisitions, and localized production capabilities intensify competition, as players aim to provide faster, cost-efficient solutions while maintaining global standards.

KEY MARKET PLAYERS

Some of the major companies and institutions in the Rigid Packaging Market

- Berry Global Inc.

- ALPLA Werke Alwin Lehner GmbH & Co KG

- Sonoco Products Company

- Plastipak Holdings, Inc.

- Crown Holdings, Inc.

- Ball Corporation

- DS Smith Plc

- Silgan Holdings, Inc.

- ALPLA Group

TOP LEADING PLAYERS MARKET

- Amcor Limited is a leading global packaging company actively contributing to the Asia-Pacific rigid packaging market. The company manufactures high-quality rigid containers, bottles, and jars for food, beverages, pharmaceuticals, and personal care sectors. Amcor has strengthened its presence in Asia by investing in production facilities in India, China, and Thailand, which are catering to the increasing demand for sustainable and innovative packaging. In 2023, the company expanded its product line to include recyclable and lightweight rigid packaging solutions by enhancing supply chain efficiency and reducing environmental impact. Amcor continues to focus on customer-centric solutions, driving the adoption of premium rigid packaging in the region.

- Berry Global, Inc. is a major provider of rigid packaging solutions in the Asia-Pacific region, offering a wide range of bottles, containers, and industrial packaging. The company emphasizes sustainable and recyclable plastics to meet regional environmental standards. Berry Global has expanded manufacturing operations in China, India, and Japan, enabling rapid supply to the growing food, beverage, and personal care industries. In 2023, it introduced high-barrier PET containers that enhance product shelf life and maintain freshness. Strategic partnerships with local distributors and investment in automated production lines have strengthened its market position, driving innovation and operational efficiency.

- RPC Group, acquired by Berry Global, plays a vital role in the Asia-Pacific’s rigid packaging sector, supplying high-quality containers, bottles, and jars to the FMCG, pharmaceutical, and cosmetic industries. The company focuses on lightweight, recyclable, and high-performance plastic packaging solutions. RPC has established manufacturing units in India, China, and Southeast Asia to cater to increasing regional demand for sustainable packaging.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the rigid packaging market deploy strategies such as sustainability initiatives, capacity expansion, strategic acquisitions, product innovation, and regional diversification. Companies are increasingly introducing recyclable, lightweight, and bio-based packaging solutions to comply with environmental regulations and cater to eco-conscious consumers. Capacity expansion through new facilities in the Asia-Pacific region ensures faster delivery and cost-efficient production. Strategic acquisitions, like the RPC Group by Berry Global, consolidate market presence and expand product portfolios. Product innovation focuses on high-barrier, tamper-evident, and premium packaging for food, beverages, and personal care. Regional diversification into emerging economies allows companies to capture new consumer segments and benefit from rapid urbanization and rising disposable income.

GLOBAL RIGID PACKAGING MARKET NEWS

- In February 2023, Berry launched a bundle of PET bottles for the liquid pharmaceutical market in Europe, designed for syrups, decongestants, and cold remedies. These bottles offered barrier protection against oxygen and moisture and were also available in recycled PET3.

MARKET SEGMENTATION

This research report on the global rigid packaging market is segmented and sub-segmented into the following categories:

By Material

- Plastic

- Glass

- Metal

- Paper & Paperboard

By Product Type

- Bottles & Jars

- Containers & Cans

- Trays & Clamshells

- Boxes & Cartons

By End-Use

- Food & Beverages

- Personal Care & Cosmetics

- Pharmaceuticals

- Household Products

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. Why is the Global Rigid Packaging Market growing?

The Global Rigid Packaging Market is growing due to increased demand for durable, secure packaging in industries like food, beverages, pharmaceuticals, and e-commerce, plus a rising focus on sustainability.

2. Which materials dominate the Global Rigid Packaging Market?

The Global Rigid Packaging Market mainly features plastics, metals, glass, and paperboard, each offering unique advantages in terms of product protection and sustainability for different industries.

3. What are the key applications of the Global Rigid Packaging Market?

Key applications in the Global Rigid Packaging Market include packaging for food and beverages, consumer goods, healthcare, industrial chemicals, and agricultural products globally.

4. Who are the leading players in the Global Rigid Packaging Market?

Major companies in the Global Rigid Packaging Market are Amcor, Berry Global, Sealed Air, ALPLA, DS Smith, and Mondi, all of whom drive innovation, supply, and sustainability initiatives in this field.

5. What regions lead in the Global Rigid Packaging Market?

Asia-Pacific, Europe, and North America are the leading regions in the Global Rigid Packaging Market, owing to strong manufacturing bases and large consumer goods sectors.

6. How does sustainability impact the Global Rigid Packaging Market?

Sustainability is increasingly critical in the Global Rigid Packaging Market, with firms investing in biodegradable materials, recycling processes, and eco-friendly designs to reduce environmental impact.

7. What is the forecasted size of the Global Rigid Packaging Market?

The Global Rigid Packaging Market is projected to cross USD 700 billion by 2032, reflecting a steady annual growth rate due to expanding industries and new applications worldwide.

8. Which end-user industries drive the Global Rigid Packaging Market?

Food and beverages, consumer goods, pharmaceuticals, and chemicals are top end-user sectors boosting demand and innovation in the Global Rigid Packaging Market.

9. What trends are shaping the Global Rigid Packaging Market in 2025?

Sustainable materials adoption, smart packaging technologies, e-commerce packaging innovations, and stricter regulatory compliance are key trends in the Global Rigid Packaging Market.

10. How does the food industry rely on the Global Rigid Packaging Market?

The food industry depends on the Global Rigid Packaging Market for secure, contamination-free, and shelf-stable packaging that meets global safety standards and increases product lifespan

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com