Global Sustainable Packaging Market Size, Share, Trends, and Growth Analysis Report, Segmented By Material, Product Type, Application, & Region (North America, Europe, Latin America, Asia Pacific, Middle East & Africa), Industry Forecast From 2026 to 2034

Global Sustainable Packaging Market Summary

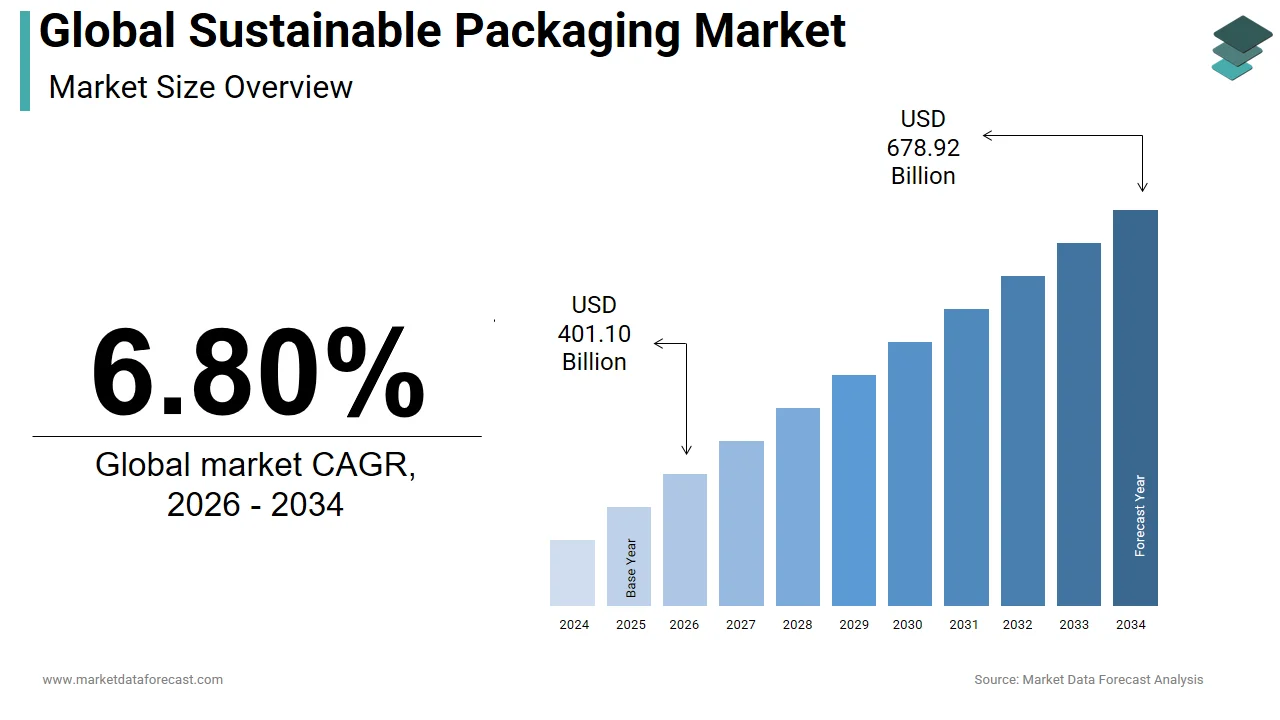

The global sustainable packaging market was valued at USD 375.56 billion in 2025, is expected to reach USD 401.10 billion in 2026, and is projected to expand significantly to USD 678.92 billion by 2034, growing at a CAGR of 6.80% from 2026 to 2034. The growth of the global sustainable packaging market is attributed to increasing environmental awareness, rising consumer demand for eco-friendly products, stringent government regulations on single-use plastics, and growing adoption of circular economy principles by manufacturers.

Key Market Trends

- Increasing demand for paper-based and biodegradable packaging solutions in the food and retail industries.

- Rising adoption of lightweight and recyclable materials to reduce carbon footprint.

- Growing investments in compostable and plant-based packaging technologies.

- Expansion of the e-commerce and packaged food sectors is boosting the demand for sustainable packaging.

- Strong regulatory push for reducing plastic waste and promoting circular economy initiatives.

Segmental Insights

- Based on material, the paper and paperboard segment held the largest share at 38.1% in 2024, supported by recyclability and strong demand across food and beverage packaging.

- Based on product type, the boxes and cartons segment dominated with a 33.6% share in 2024, fueled by e-commerce growth and food service packaging needs.

- Based on application, the food and beverages segment accounted for a 42.6% share in 2024, reflecting consumer preference for sustainable and safe packaging solutions.

Regional Insights

- Europe led the global sustainable packaging market with a 35.6% share in 2024, driven by stringent environmental regulations, innovation in recyclable materials, and strong consumer awareness.

- North America is witnessing steady growth due to the increasing adoption of eco-friendly packaging by major retail and FMCG brands.

- Asia-Pacific is expected to record the fastest growth, supported by industrial expansion, government sustainability initiatives, and growing middle-class consumption.

- Latin America is gradually advancing, with demand led by the packaged food and beverage industries.

- Middle East & Africa are emerging markets with a rising emphasis on reducing packaging waste and adopting recyclable materials.

Competitive Landscape

Key players in the global sustainable packaging market include Amcor Plc (Switzerland), Ardagh Group S.A. (Luxembourg), Ball Corporation (U.S.), Crown Holdings Inc. (U.S.), DS Smith (U.K.), Sealed Air Corporation (U.S.), Mondi Group (U.K.), Sonoco Products Company (U.S.), Tetra Pak International S.A. (Switzerland), WestRock Company (U.S.), Smurfit Kappa (Ireland), Huhtamaki Oyj (Finland), International Paper (U.S.), Berry Global (U.S.), and Gerresheimer AG (Germany). These companies are focusing on innovations in biodegradable packaging, recycling technologies, and partnerships with FMCG and e-commerce brands to expand their market presence.

Global Sustainable Packaging Market Size

The size of the global sustainable packaging market was worth USD 375.56 billion in 2025. The global market is anticipated to grow at a CAGR of 6.80% from 2026 to 2034 and be worth USD 678.92 billion by 2034 from USD 401.10 billion in 2026.

Sustainable packaging refers to the materials and designs that minimize environmental impact across their lifecycle, from sourcing and production to end-of-life disposal, by prioritizing recyclability, compostability, renewable inputs, and reduced carbon footprint. It is no longer a niche alternative but a systemic response to global ecological crises, particularly plastic pollution and resource depletion. According to the United Nations Environment Programme, approximately 400 million tons of plastic waste are generated annually, with only 9% recycled globally, emphasizing the urgency for sustainable alternatives. As per the Ellen MacArthur Foundation, 32% of plastic packaging leaks into ecosystems, harming marine life and contaminating food chains. The European Commission reports that packaging accounts for 40% of non-fiber plastic use in the EU, making it a primary target for regulatory intervention. With countries implementing some form of plastic restriction, sustainable packaging has become an important lever for compliance, brand integrity, and long-term supply chain resilience, driven by scientific imperatives rather than consumer trends alone.

MARKET DRIVERS

Escalating Regulatory Burden on Single-Use Plastics and Packaging Waste

Governments worldwide are enacting stringent legislation to curb plastic pollution, which is accelerating the expansion of the sustainable packaging market. The European Union's Packaging and Packaging Waste Regulation (PPWR) mandates that all packaging be recyclable (not necessarily reusable) by 2030 and sets binding targets for recycled content, including 55% for plastic packaging by 2030. As per the study, a portion of municipal plastic waste in Europe comes from packaging, making it a primary policy focus. In Canada, the federal government declared single-use plastics toxic under the Canadian Environmental Protection Act in 2021, paving the way for a nationwide ban. According to the research, many countries have implemented bans or levies on single-use plastics, creating a compliance-driven shift toward paper-based, biodegradable, and reusable alternatives. These regulations are penalizing non-compliance and also incentivizing innovation through extended producer responsibility (EPR) schemes, which force brands to redesign packaging at scale.

Corporate Sustainability Commitments and Supply Chain Accountability

Multinational corporations are increasingly adopting science-based targets and zero-waste goals, which is enhancing the growth rate of sustainable packaging. Many global companies have signed the Ellen MacArthur Foundation’s Global Commitment, pledging to make a portion of their packaging reusable, recyclable, or compostable. According to a study, a portion of Fortune 500 companies require suppliers to disclose packaging sustainability metrics, creating ripple effects across value chains. Apart from these, the Consumer Goods Forum’s Forest Positive Coalition has committed to eliminating deforestation from packaging fiber sourcing by 2030. These commitments are not symbolic; they are operationalized through supplier audits, material substitution mandates, and lifecycle assessments, transforming sustainable packaging from a marketing tool into a measurable, enforceable business imperative.

MARKET RESTRAINTS

Limited Infrastructure for Recycling and Composting of Alternative Materials

The lack of adequate end-of-life infrastructure severely limits the environmental benefit and hinders the rise of the sustainable packaging market. According to the study, only a portion of plastic waste was recycled, and industrial composting facilities capable of processing certified compostable packaging are available in fewer locations across the United States, as per the study. In India, a smaller share of urban waste is formally collected, and composting capacity remains fragmented. As per the research, even in the EU, where compostability standards exist, only a portion of organic waste is processed in industrial composters. When compostable packaging ends up in landfills, it degrades anaerobically, producing methane, a greenhouse gas more potent than CO₂. Similarly, paper-based packaging contaminated with food or plastic coatings often cannot be recycled. Sustainable packaging risks becoming a well-intentioned solution trapped in a broken system without parallel investment in waste sorting, collection, and processing.

Higher Production Costs and Material Performance Limitations

Higher production costs and functional limitations compared to conventional plastics are hampering the expansion of the sustainable packaging market. According to research, bio-based or recycled packaging materials can cost more than virgin plastic, with compostable films sometimes exceeding double the price. For small and medium enterprises, these premiums are prohibitive. Apart from these, many sustainable alternatives underperform in important areas: paper-based barriers offer poor moisture resistance, while PLA bioplastics have low heat tolerance, limiting use in hot-fill applications. According to the study, a portion of fresh produce packaged in alternative materials experienced higher spoilage rates due to inadequate protection. In e-commerce, where durability is paramount, a portion of retailers reported increased product damage when switching to lightweight or fiber-based mailers, according to the study. Hence, the adoption of sustainable materials will remain constrained to premium or regulated product lines until they achieve parity in cost, shelf life protection, and logistical resilience.

MARKET OPPORTUNITIES

Innovation in Reusable and Refillable Packaging Systems

The shift toward circular economy models is offering new opportunities in reusable and refillable packaging. This is particularly true in consumer goods, food service, and personal care. According to the study, reusable packaging could eliminate notable tons of plastic waste annually by 2030 if scaled across key sectors. Loop, a global reuse platform, partnered with retailers to offer products like shampoos, detergents, and snacks in durable, returnable containers. In South Korea, reusable cup systems reduced single-use container waste in Seoul. These systems are supported by digital tracking via QR codes and deposit schemes, enhancing consumer convenience. Thus, reusable models are becoming logistically viable due to rising urban density and digital payment penetration in Asia and Africa, which transforms packaging from a disposable item into a managed asset.

Advancements in Biomaterials and Next-Generation Feedstocks

Breakthroughs in biomaterials derived from agricultural residues, algae, and microbial fermentation are giving new opportunities for the sustainable packaging market. According to the U.S. Department of Energy, non-food biomass such as sugarcane bagasse, rice husks, and corn stover could supply over 1 billion tons of renewable feedstock annually without competing with food production. Companies have developed seaweed-based films that fully biodegrade in weeks, used by Lucozade for water pods at marathons, eliminating plastic bottles. Ecovative Design produces MycoComposite, a packaging material grown from mycelium and agricultural waste, adopted by IKEA and Dell for protective cushioning. These innovations not only reduce reliance on fossil fuels but also valorize waste streams, which creates dual environmental and economic benefits, particularly in agrarian economies.

MARKET CHALLENGES

Greenwashing and Lack of Standardized Certification Frameworks

The absence of universally recognized standards for sustainability claims has led to widespread greenwashing, eroding consumer and regulatory trust, and degrading the growth rate of the sustainable packaging market. Terms like biodegradable, eco-friendly, and green are often used without verification, misleading stakeholders. According to a study, a portion of environmental claims on packaging were found to be vague, misleading, or unsubstantiated. Certifications such as TÜV Austria’s OK Compost, BPI’s Certified Compostable, and FSC labeling exist, but their adoption is inconsistent. Brands can exploit ambiguity when mandatory science-based labeling requirements and third-party validation are absent. This impedes genuine innovation and consumer decision-making. Regulatory bodies are now stepping in, which signals a shift toward accountability.

Supply Chain Complexity and Sourcing Risks for Renewable Materials

The volatility and competition for renewable feedstocks such as wood pulp, sugarcane, and plant oils challenge the growth of the sustainable packaging market. According to the research, global demand for wood fiber could rise by 2050, increasing the burden on forests and biodiversity. In Indonesia and Malaysia, the expansion of pulp plantations has been linked to deforestation and peatland degradation, eroding the environmental benefits of paper-based packaging. Similarly, the use of corn and cassava for bioplastics competes with the food supply, particularly in regions facing food insecurity. Apart from these, supply chains for alternative materials like algae or mycelium remain nascent and geographically concentrated, creating barriers. The scalability of sustainable packaging will remain limited by ecological trade-offs and geopolitical risks until diversified, transparent, and regenerative sourcing models are established.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material, Product Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East and Africa |

| Market Leaders Profiled | Amcor Plc (Switzerland), Ardagh Group S.A. (Luxembourg), Ball Corporation (U.S.), Crown Holdings Inc. (U.S.), DS Smith (U.K.), Sealed Air Corporation (U.S.), Mondi Group (U.K.), Sonoco Products Company (U.S.), Tetra Pak International S.A. (Switzerland), WestRock Company (U.S.), Smurfit Kappa (Ireland), Huhtamaki Oyj (Finland), International Paper (U.S.), Berry Global (U.S.), Gerresheimer AG (Germany) |

SEGMENTAL ANALYSIS

By Material Insights

The paper and paperboard segment held the largest share of 38.1% of the sustainable packaging market in 2024. The domination of paper and paperboard segment is majorly attributed to its high recyclability, consumer familiarity, and rapid response to plastic restrictions. As per the European Paper Packaging Alliance, paper-based packaging achieves a recycling rate of 82% in Europe, the highest of any material, driving preference among brands seeking demonstrable sustainability credentials. Apart from these, paper’s compatibility with print, branding, and e-commerce durability makes it ideal for boxes, mailers, and food containers. Companies have transitioned from plastic to paper-based packaging globally. Innovations such as water-based barrier coatings and molded fiber trays are further expanding its functionality, which enables replacement of plastic in fresh food and protective packaging applications.

The sustainable plastic segment is likely to experience the fastest CAGR of 11.4% from 2026 to 2034 due to advancements in material science that reconcile performance with environmental responsibility. Unlike conventional plastics, sustainable variants like rPET, bio-PE, and PLA offer reduced carbon footprints and improved end-of-life options. According to the study, using recycled PET in bottles reduces greenhouse gas emissions compared to virgin plastic. Innovations such as chemical recycling are enabling food-grade PCR plastics, while companies produce PHA-based bioplastics that degrade in marine environments by addressing leakage concerns and expanding application scope.

By Product Type Insights

The boxes and cartons segment dominated the sustainable packaging market by capturing 33.6% of the global market share in 2024. The explosive growth of e-commerce and the widespread use of corrugated packaging in retail and logistics are propelling the expansion of boxes and cartons segment in the global market. According to the research, e-commerce sales in the United States increased significantly, requiring billions of shipping boxes annually. Corrugated boxes, primarily made from recycled fiber, are inherently recyclable and reusable, aligning with corporate sustainability goals. Innovations like water-based coatings and lightweighting have further enhanced performance while reducing environmental impact. This strengthens boxes and cartons as the backbone of sustainable packaging in both industrial and consumer supply chains.

The mailers segment is anticipated to witness the fastest CAGR of 12.8% from 2026 to 2034. Factors such as the rise of direct-to-consumer (DTC) retail and the urgent need for eco-friendly shipping solutions are boosting the growth of mailers segment in the global market. Traditional plastic polybags are being replaced by paper-based, compostable, or recyclable hybrid mailers. According to study, global e-commerce parcel volume exceeded notable volume, with Asia-Pacific accounting for a portion of shipments, driving demand for sustainable alternatives. Companies have adopted recyclable paper mailers across Europe, reducing plastic waste significantly. Innovations such as self-sealing, water-resistant coatings, and QR-coded return labels are enhancing functionality. Consumers are increasingly rejecting plastic-lined envelopes. As a result, brands are rapidly transitioning to sustainable formats to maintain loyalty and compliance.

By Application Insights

In 2024, the food and beverages segment led the sustainable packaging market by accounting for 42.6% share in 2024. The growth of food and beverages segment in the global market is attributed to the sector’s massive scale and urgent need to reduce spoilage and plastic waste. According to the studt, food packaging accounts for a portion of global plastic usage, making it a primary target for reform. As per the research, millions of tons of food are lost annually in the EU due to inadequate packaging, spurring investment in breathable films, modified atmosphere packaging (MAP), and compostable trays. In the U.S., the Food and Drug Administration encourages the use of recyclable and bio-based materials in food contact applications, with rPET and PLA gaining regulatory approval. Major brands have committed to recyclable or compostable packaging. Apart from these, the rise of plant-based foods has accelerated demand for sustainable and branded packaging that aligns with ethical consumer values.

The e-commerce application segment is estimated to register the fastest CAGR of 13.5% over the forecast period owing to the structural shift in consumer purchasing behavior and the environmental scrutiny of online retail’s packaging footprint. According to the study, e-commerce generates more packaging waste per transaction than in-store shopping, prompting brands and logistics providers to innovate. Apart from these, the European Union’s Green Claims Directive will require brands to substantiate environmental claims on shipping materials, accelerating the shift to certified recyclable or reusable formats. Hence, sustainable e-commerce packaging is no longer optional but a core component of digital retail strategy.

REGIONAL ANALYSIS

Europe Sustainable Packaging Market Insights

Europe was the leading region in the global sustainable packaging market in 2024 and accounted for 35.6% of the global market share in 2024. The region’s combination of policy rigor, consumer awareness, and industrial readiness is propelling the dominance of Europe in the global market. The European Union’s Circular Economy Action Plan and Packaging and Packaging Waste Regulation (PPWR) have set binding targets for recyclability, recycled content, and reuse, compelling industries to redesign packaging systems. The European Investment Bank has allocated funds to sustainable packaging innovation under Horizon Europe, supporting startups in bioplastics and reusable models. Apart from these, major retailers like Tesco and Carrefour have eliminated plastic produce bags and adopted compostable alternatives.

North America Sustainable Packaging Market Insights

North America is another key region in the sustainable packaging market by capturing 28.7% of the global market share in 2024. The growth of North America in the global market is driven by corporate sustainability mandates and evolving state-level regulations. The United States, home to many Fortune 500 companies, has seen aggressive packaging commitments from firms like PepsiCo, Walmart, and Procter & Gamble, all pledging recyclable, reusable, or compostable packaging. According to the study, notable tons of plastic packaging were generated, with less share recycled, prompting states like California and Maine to implement Extended Producer Responsibility (EPR) laws. Apart from these, the rise of direct-to-consumer brands like Dollar Shave Club and Thrive Market has accelerated the adoption of minimalist, recyclable packaging. Thus, North America remains a hub for material innovation and scalable business model experimentation.

Asia-Pacific Sustainable Packaging Market Insights

Asia-Pacific is predicted to be a lucrative region in the sustainable packaging market. The region is emerging as the most dynamic and fastest-evolving region due to rapid urbanization and regulatory modernization. China, India, and South Korea are leading the transition. As per the research, the region generates tons of plastic waste annually, driving policy action. India’s Bureau of Indian Standards introduced IS 17088 for compostable plastics in 2023, enabling certification and market trust. In Japan, where waste incineration rates exceed, companies like Panasonic and Fujitsu are adopting recyclable paper-based alternatives to reduce carbon emissions. Apart from these, e-commerce giants like JD.com and Flipkart have committed to plastic-free packaging by replacing polybags with paper mailers and reusable containers. Thus, Asia-Pacific is transforming from a high-waste region into a laboratory for scalable sustainable packaging solutions because of rising middle-class environmental awareness and government-backed circular economy initiatives.

Latin America Sustainable Packaging Market Insights

Latin America continues to grow steadily in the sustainable packaging market, with Brazil, Mexico, and Colombia emerging as regional leaders despite infrastructural challenges. Brazil’s National Solid Waste Policy, enacted in 2010, mandates reverse logistics for packaging, compelling companies to implement take-back systems. As per study, paper packaging recycling surged, one of the key rates in the developing world. In Mexico, the circular economy agenda has gained momentum. Colombia introduced a plastic tax in 2022, which taxes single-use plastic products based on weight, incentivizing substitution. Collection and recycling infrastructure remain uneven. However, policy momentum and consumer awareness are creating fertile ground for sustainable packaging adoption.

Middle East and Africa Sustainable Packaging Market Insights

The Middle East and Africa is likely to grow in the global sustainable packaging market, but strategic initiatives are laying the foundation for future growth. The United Arab Emirates leads the region. As per the study, plastic waste constitutes a portion of municipal solid waste, prompting bans on single-use bags. Saudi Arabia’s Vision 2030 includes circular economy goals. Though fragmented, the region’s focus on urban sustainability, waste reduction, and import substitution is driving investment in local paper mills, recycling facilities, and eco-design, positioning sustainable packaging as a key lever in broader environmental transformation.

COMPETITIVE LANDSCAPE

The competition in the sustainable packaging market is intensifying as traditional packaging giants, biotech innovators, and consumer brands converge in a race to redefine material science and circularity. Unlike conventional markets driven by cost and volume, this space is shaped by regulatory compliance, brand reputation, and lifecycle integrity. Incumbents compete with agile startups specializing in biomaterials, reusable systems, and digital traceability by creating a fragmented yet dynamic landscape. Differentiation is no longer about aesthetics but functional sustainability, measured by recyclability rates, carbon footprint, and end-of-life management. Regional policy divergence, such as Europe’s strict EPR laws versus Asia’s emerging plastic bans, is forcing companies to adopt modular, adaptable strategies. Consumer activism and ESG investing are amplifying push for verifiable claims, penalizing greenwashing.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global sustainable packaging market include

- Amcor Plc (Switzerland)

- Ardagh Group S.A. (Luxembourg)

- Ball Corporation (U.S.)

- Crown Holdings Inc. (U.S.)

- DS Smith (U.K.)

- Sealed Air Corporation (U.S.)

- Mondi Group (U.K.)

- Sonoco Products Company (U.S.)

- Tetra Pak International S.A. (Switzerland)

- WestRock Company (U.S.)

- Smurfit Kappa (Ireland)

- Huhtamaki Oyj (Finland)

- International Paper (U.S.)

- Berry Global (U.S.)

- Gerresheimer AG (Germany)

Top Strategies Used by the Key Market Participants

Key players in the sustainable packaging market are deploying a convergence of material innovation, regulatory anticipation, and ecosystem collaboration to secure competitive advantage. Companies are investing heavily in mono-material structures, bio-based polymers, and digital watermarking to enhance recyclability and sorting efficiency. Strategic partnerships with waste management firms, governments, and retailers are enabling closed-loop systems and scalable collection infrastructure. Firms are also localizing R&D and production to align with regional regulations such as India’s plastic ban and the EU’s PPWR. Digital tools like blockchain and QR codes are being integrated to improve transparency and consumer engagement. Mergers and acquisitions targeting biotech startups are accelerating access to next-gen materials like mycelium and PHA. Apart from these, players are shifting from product sales to service models, offering packaging audits, lifecycle assessments, and take-back programs. Sustainability certification and third-party validation are leveraged not only for compliance but as brand equity builders in an era of heightened environmental scrutiny and consumer demand for authenticity.

Top Players in the Sustainable Packaging Market

Tetra Pak

Tetra Pak has established a significant presence in the Asia-Pacific sustainable packaging market through its prominence ip in renewable-based carton solutions for food and beverages. The company’s packaging is composed of plant-based materials, primarily sourced from FSC-certified forests, and is fully recyclable in markets with appropriate infrastructure. Tetra Pak is shaping the region’s transition toward circular packaging models by combining material innovation with systemic waste solutions.

Amcor plc

Amcor has emerged as a transformative force in the Asia-Pacific’s sustainable packaging landscape by advancing recyclable and lightweight flexible packaging solutions across food, healthcare, and consumer goods sectors. The company has eliminated non-recyclable laminates from its portfolio and introduced mono-material structures compatible with existing recycling streams. It also launched a recyclable barrier film for instant noodles in Indonesia, replacing multi-layer plastic composites. Amcor’s investment in digital watermarking technology enables better sorting in recycling facilities. Amcor is driving scalable and high-performance alternatives to conventional plastics through material science dominance and regional partnerships.

Mondi Group

Mondi has strengthened its footprint in the Asia-Pacific sustainable packaging market by delivering paper-based, recyclable, and reusable solutions tailored to e-commerce, food service, and industrial applications. The company’s “Grow and Share” strategy emphasizes circular design, resulting in innovations like recyclable grease-resistant paper for fast food packaging in South Korea and compostable tea bags in Japan. Mondi is setting benchmarks for eco-efficient packaging that meets both regulatory demands and consumer expectations across diverse Asian markets by prioritizing functionality without compromising recyclability.

MARKET SEGMENTATION

This global sustainable packaging market research report is segmented and sub-segmented into the following categories.

By Material

- Paper & Paperboard

- Glass

- Plastic

- Metal

- Others

By Product Type

- Boxes & Cartons

- Bags & Pouches

- Bottles & Cans

- Films & Wraps

- Trays

- Mailers

- Others

By Application

- Food & Beverages

- Personal Care & Cosmetics

- Pharmaceuticals

- Consumer Goods

- E-commerce

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Middle East Africa

- Latin America

Frequently Asked Questions

1. What is the Sustainable Packaging Market?

The Sustainable Packaging Market refers to eco-friendly packaging solutions focused on recyclability, biodegradability, compostability, and reduced environmental impact across food, beverage, healthcare, personal care, and e-commerce sectors

2. What are the main material types in the Sustainable Packaging Market?

Materials include paper & paperboard, bioplastics, compostables, recycled glass, metal, and innovative mono-material plastics designed for easier recycling

3. Which regions lead the Sustainable Packaging Market?

Asia Pacific is the fastest-growing region, propelled by government bans on single-use plastics (notably in India and China), while Europe holds the largest market share, driven by circular economy regulations

4. What industries utilize sustainable packaging the most?

Food & beverage, personal care, pharmaceuticals, e-commerce, and consumer goods are the primary users of sustainable packaging solutions

5. Who are the top companies in the Sustainable Packaging Market?

Leaders include Amcor Plc, Stora Enso Oyj, Berry Global Inc., WestRock LLC, DS Smith Plc, Huhtamaki Oyj, and Ranpak Holdings

6. Why is sustainable e-commerce packaging important?

With the rise of online shopping, e-commerce packaging is key for reducing shipping waste, focusing on minimal packaging, recycled content, and protective, sustainable options

7. Which government policies drive growth in the Sustainable Packaging Market?

Extended producer responsibility, plastic bans, incentives for compostable materials, and robust recycling mandates are accelerating market adoption globally

8. What are recent innovations in the Sustainable Packaging Market?

Smart packaging, mono-material technology, digital traceability, automated sustainable pallet wraps, and new bio-based material blends are transforming industry practices

9. How does sustainable packaging affect the carbon footprint of products?

Sustainable packaging uses renewable, recyclable, or biodegradable materials and advanced design to lower carbon emissions in manufacturing, use, and disposal

10. What are the major challenges of the Sustainable Packaging Market?

Challenges include balancing performance/cost, scaling up supply chains, achieving global material standards, and managing waste in less-regulated markets

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com