Global Therapeutic Proteins Market Size, Share, Trends, and Growth Analysis Report, Segmented By Product (Monoclonal Antibodies, Insulin, Fusion Protein, Erythropoietin, Interferon, Human Growth Hormone, Follicle Stimulating Hormone), Application & Region (North America, Europe, Latin America, Asia Pacific, Middle East & Africa), Industry Forecast From 2025 to 2033

Global Therapeutic Proteins Market Size

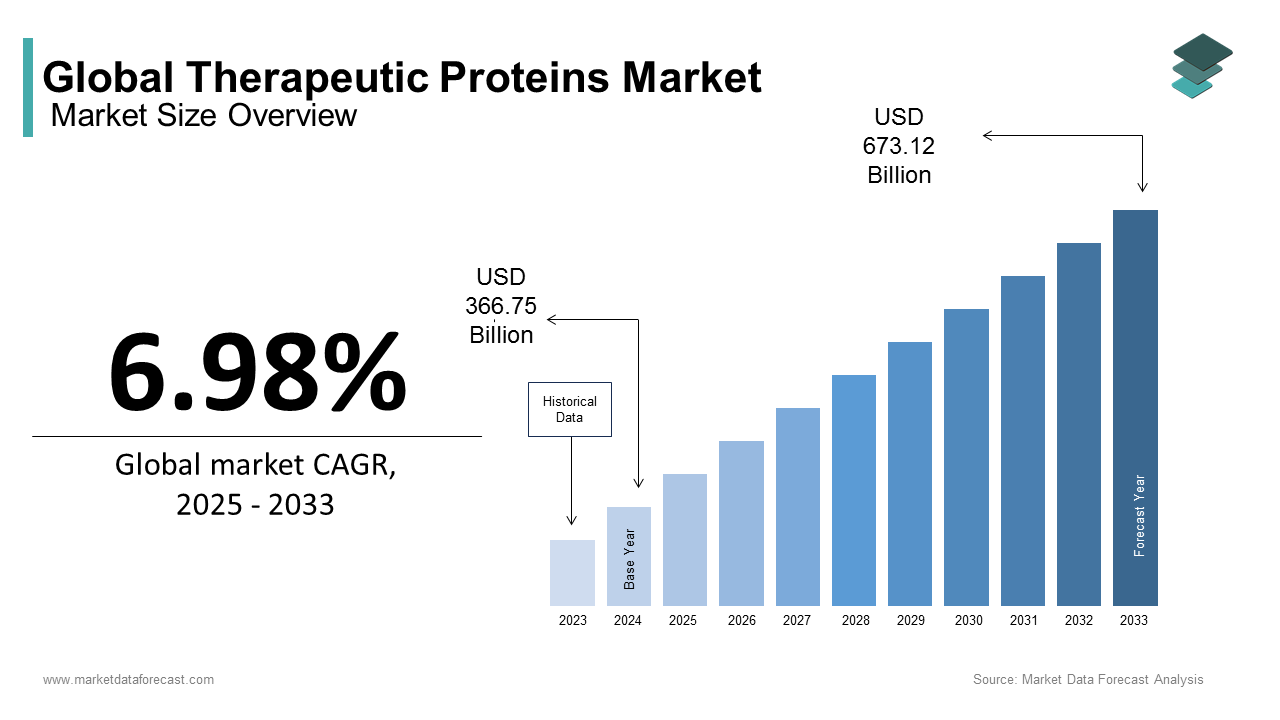

The global therapeutic proteins market size was valued at USD 366.75 billion in 2024 and is anticipated to reach USD 392.35 billion in 2025 and USD 673.12 billion by 2033, growing at a CAGR of 6.98% during the forecast period from 2025 to 2033.

The therapeutic proteins are engineered to restore or modify physiological functions, replacing deficient proteins, enhancing immune responses, or targeting disease pathways. These molecules include monoclonal antibodies, cytokines, fusion proteins, and hormones that have reshaped the treatment of cancer, autoimmune conditions, and metabolic disorders. Their importance is underscored by the growing prevalence of chronic diseases.

MARKET DRIVERS

Rising prevalence of cancer and autoimmune diseases

The therapeutic proteins market growth is significantly driven by the escalating global burden of cancer and autoimmune disorders, which demand highly targeted therapies. According to the International Agency for Research on Cancer, 19.3 million new cancer cases were diagnosed worldwide in 2020, and this number is projected to increase to 28.4 million by 2040. Therapeutic proteins such as monoclonal antibodies and cytokines are central to managing these conditions, which offer higher specificity compared to traditional drugs.

Advancements in recombinant DNA technology and protein engineering

Technological innovations in recombinant DNA and protein engineering have transformed the development of therapeutic proteins, which is accelerating the growth of the therapeutic proteins market. Recombinant techniques allow scalable production of hormones, enzymes, and antibodies with precise structural modifications. As per the U.S. Food and Drug Administration, over 100 recombinant therapeutic proteins are now approved for clinical use, which is ranging from insulin to advanced biologics. Additionally, CRISPR-Cas9 gene-editing tools and next-generation cell expression systems are accelerating the design of proteins with enhanced therapeutic profiles.

MARKET RESTRAINTS

High production and development costs

The substantial costs associated with research, development, and manufacturing are restraining the growth of the therapeutic proteins market. Unlike small molecules, therapeutic proteins require complex bioreactors, specialized purification processes, and stringent regulatory compliance, which further inflate expenses. Additionally, cold chain logistics for storage and transport add financial strain.

Risk of immunogenicity and safety concerns

The inherent risk of immunogenicity, where therapeutic proteins may trigger unwanted immune responses in patients is additionally hinders the growth of the therapeutic proteins market. These responses can reduce treatment efficacy, cause allergic reactions, or, in severe cases, result in life-threatening complications. The U.S. National Library of Medicine reports that immunogenicity remains a persistent challenge for biotherapeutics, with monoclonal antibodies and enzyme therapies showing variable patient responses. Adverse events not only impact clinical outcomes but also lead to regulatory delays and heightened scrutiny. Safety concerns surrounding long-term use further complicate adoption, as patients and healthcare providers weigh potential risks against therapeutic benefits.

MARKET OPPORTUNITIES

Expansion of personalized medicine and targeted therapies

The growing emphasis on personalized medicine is expected to boost the growth of the therapeutic proteins market. Advances in biomarker discovery and genomics enable tailoring protein-based therapies to specific patient profiles, which is improving treatment outcomes. According to the Personalized Medicine Coalition, more than 40% of drugs approved by the U.S. FDA in 2022 were personalized therapies, many of which involved therapeutic proteins such as monoclonal antibodies. This shift reflects a broader trend toward precision therapeutics, where treatments are customized to genetic and molecular characteristics.

Increasing biopharmaceutical investments and pipeline expansion

The global surge in biopharmaceutical research funding creates significant growth opportunities for the therapeutic proteins market. Governments and private investors are accelerating investments in biologics, recognizing their potential to address unmet medical needs. Additionally, large-scale investments in the Asia Pacific, particularly in China and India, are driving regional manufacturing capacity and clinical trials.

MARKET CHALLENGES

Complex regulatory frameworks across regions

Regulatory heterogeneity for manufacturers is one of the challenges for the growth of the therapeutic proteins market. Agencies such as the U.S. FDA, the European Medicines Agency, and China’s NMPA have distinct requirements for clinical trials, safety testing, and quality control, often leading to extended approval timelines. As per the World Health Organization, regulatory barriers are particularly pronounced in emerging economies, where evolving standards can delay market entry. This complexity hampers international product launches and increases compliance costs, which is slowing down innovation.

Limited infrastructure for biologics manufacturing in emerging markets

The inadequate biologics manufacturing infrastructure in many developing regions is additionally inhibiting the growth of the therapeutic proteins market. As per the United Nations Industrial Development Organization, most biologics manufacturing facilities are concentrated in North America, Europe, and select parts of Asia. This uneven distribution creates dependency on imports for developing countries, driving up costs and delaying patient access. Moreover, a lack of trained workforce and advanced bioprocessing technologies exacerbates the problem.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.98% |

| Segments Covered | By Product, Application, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Amgen Inc., F. Hoffmann-La Roche Ltd., Pfizer Inc., Novartis AG, Merck & Co., Inc., Eli Lilly and Company, Sanofi S.A., AbbVie Inc., Biogen Inc., CSL Limited, Bristol-Myers Squibb Company, GlaxoSmithKline plc, AstraZeneca plc, Bayer AG, Takeda Pharmaceutical Company Limited |

SEGMENTAL ANALYSIS

By Product Insights

The monoclonal antibodies segment accounted in holding 49.3% of the therapeutic proteins market share in 2024, with their widespread use in oncology and autoimmune therapies. As per the International Agency for Research on Cancer, 19.3 million new cancer cases occurred globally in 2020, with a vast need for targeted treatments. Their adoption has expanded rapidly for conditions where traditional small-molecule drugs offer limited efficacy.

The fusion protein segment is likely to grow with an expected CAGR of 5.6% during the forecast period, with the advances in Fc-fusion technologies that prolong drug half-life and improve efficacy. For example, fusion-based drugs like etanercept have shown remarkable benefits in autoimmune disorders. According to the World Health Organization, noncommunicable diseases such as diabetes, cardiovascular disease, and autoimmune conditions account for 74% of global deaths annually by creating urgent demand for long-acting biologics.

By Application Insights

The cancer segment was the largest and held 28.3% of the therapeutic proteins market share in 2024, with the rising global cancer burden. According to the International Agency for Research on Cancer, 19.3 million new cancer cases occurred in 2020, with cases projected to grow significantly by 2040. Monoclonal antibodies, interferons, and erythropoietin-based drugs are widely prescribed to support cancer patients, not only for treatment but also for managing therapy-induced complications such as anemia.

The therapeutic proteins segment is expected to grow with a CAGR of 8.5% during the forecast period, with the rising prevalence of autoimmune diseases, such as rheumatoid arthritis and multiple sclerosis. As per the World Health Organization, autoimmune diseases affect up to 10% of the global population, with higher rates in developed nations. Demand for monoclonal antibodies and fusion proteins in immunology is intensifying due to their ability to provide precise and durable responses.

REGIONAL ANALYSIS

North America Market Analysis

North America was the top performer of the therapeutic proteins market by capturing 40.2% of the share in 2024. The region benefits from advanced biopharmaceutical infrastructure, strong reimbursement systems, and accelerated FDA approvals. Combined with rising investment in gene and protein therapies, North America continues to dominate the landscape.

Europe Market Analysis

Europe's therapeutic proteins market held 27.3% of the share in 2024, with its significant R&D expenditure and strong healthcare access. The European Medicines Agency approved over 20 new biologics in 2023, including monoclonal antibodies and fusion proteins for oncology and immunologic conditions.

Asia Pacific Market Analysis

Asia Pacific therapeutic proteins market is growing lucratively with an expected CAGR during the forecast period. The region faces soaring burdens of diabetes, cancer, and autoimmune disorders. Government initiatives in China, Japan, and India to boost domestic biologics production, which is propelling the growth of the therapeutic proteins market.

Latin America Market Analysis

Latin America's therapeutic proteins market growth is likely to present a significant opportunity in the coming years. According to the Pan American Health Organization, noncommunicable diseases account for 80% of deaths in the region, which is a figure surpassing the global average. Latin America is emerging as a strategic market, especially for insulin and monoclonal antibody therapies.

Middle East & Africa Market Analysis

The Middle East & Africa therapeutics proteins market growth is ascribed to increasing adoption due to healthcare modernization. According to the World Health Organization, cancer cases in the Middle East are expected to nearly double by 2040, from 555,000 cases in 2020 to over 961,000. Partnerships between global pharmaceutical giants and local healthcare providers are expanding biologic availability in Gulf countries.

COMPETITION OVERVIEW

The therapeutic proteins market is characterized by intense competition, with global pharmaceutical leaders and regional biotechs striving for dominance. Monoclonal antibodies and insulin are key battlegrounds, attracting continuous investment in innovation and biosimilar development. In the Asia Pacific region, the growing burden of chronic diseases such as diabetes, cancer, and autoimmune disorders creates a strong demand for biologics. Established players like Roche, Amgen, and Novo Nordisk are expanding regional operations while local companies in China, India, and South Korea are accelerating biosimilar pipelines. This dual dynamic of innovation and affordability defines the competition, pushing firms to pursue aggressive R&D and strategic partnerships.

KEY MARKET PLAYERS

A few of the dominating players in the global therapeutic proteins market include

- Amgen Inc.

- F. Hoffmann-La Roche Ltd.

- Pfizer Inc.

- Novartis AG

- Merck & Co., Inc.

- Eli Lilly and Company

- Sanofi S.A.

- AbbVie Inc.

- Biogen Inc.

- CSL Limited

- Bristol-Myers Squibb Company

- GlaxoSmithKline plc

- AstraZeneca plc

- Bayer AG

Top Strategies Used by Key Market Participants

Key players in the therapeutic proteins market are employing multifaceted strategies to sustain growth and meet increasing demand. Strategic alliances with regional biopharma companies enable faster clinical adoption and improved market penetration. R&D expansion remains a central approach, with companies investing billions annually in protein engineering, Fc-fusion technology, and biosimilar development. Localized manufacturing and distribution centers are being established to cut costs and ensure supply chain resilience in the Asia Pacific.

LEADING PLAYERS IN THE THERAPEUTIC PROTEINS MARKET

Roche Holding AG

Roche Holding AG remains one of the strongest contributors to the therapeutic proteins market in the Asia Pacific. The company’s oncology portfolio, including monoclonal antibodies such as trastuzumab and bevacizumab, is widely used across Japan, China, and India. Roche has strengthened its regional position through partnerships with local biopharma firms, aiming to broaden biologic accessibility. In 2023, Roche expanded its Shanghai R&D hub to accelerate protein-based therapy innovation tailored for Asian populations. The company’s focus on precision medicine and expanding clinical trials in oncology and immunology further reinforces its role in shaping the Asia Pacific therapeutic proteins industry.

Amgen Inc.

Amgen Inc. plays a pivotal role in supplying therapeutic proteins to the Asia Pacific market, with a strong emphasis on fusion proteins, erythropoietin, and monoclonal antibodies. The company has introduced several biologics for oncology and hematology that are gaining traction in China, South Korea, and Australia. In 2022, Amgen signed multiple strategic agreements with BeiGene in China to co-develop biologics, accelerating its expansion in emerging markets. Amgen also invested heavily in biosimilar launches within the Asia Pacific, strengthening affordability and access. The company’s long-term strategy combines regional collaborations, regulatory engagement, and innovation in protein engineering.

Novo Nordisk A/S

Novo Nordisk A/S dominates the protein-based insulin segment in the Asia Pacific, meeting the region’s high demand due to rising diabetes prevalence. The International Diabetes Federation estimated over 206 million adults with diabetes in Asia in 2021, positioning Novo Nordisk’s portfolio as indispensable. The company has localized production units in China to boost self-sufficiency and reduce treatment costs. In 2023, Novo Nordisk announced further expansion of its Tianjin manufacturing facility to increase insulin output.

RECENT HAPPENINGS IN THE MARKET

In April 2024, Roche Therapeutic Proteins expanded its Shanghai innovation hub to accelerate therapeutic protein development for oncology and immunology patients in the Asia Pacific. This Therapeutic protein market expansion is anticipated to enhance regional R&D capabilities and strengthen its market presence.

MARKET SEGMENTATION

This research report on the global therapeutic proteins market is segmented and sub-segmented into the following categories.

By Product

- Monoclonal Antibodies

- Insulin

- Fusion Protein

- Erythropoietin

- Interferon

- Human Growth Hormone

- Follicle Stimulating Hormone

By Application

- Metabolic Disorders

- Immunologic Disorders

- Hematological Disorders

- Cancer

- Hormonal Disorders

- Genetic Disorders

- Others

By Region

- North America

- Europe

- Latin America

- Asia Pacific

- Middle East & Africa

Frequently Asked Questions

1. What are the main types of therapeutic proteins?

Major types include monoclonal antibodies (mAbs), insulin, fusion proteins, erythropoietin, interferons, colony-stimulating factors, and growth hormones.

2. Which therapeutic proteins are most widely used?

Monoclonal antibodies and insulin dominate the market due to their extensive use in oncology, diabetes, and autoimmune diseases.

3. What are the key drivers of the therapeutic proteins market?

Rising prevalence of chronic diseases, advances in biotechnology, growing demand for biologics, and increasing approval of biosimilars are major growth drivers.

4. What factors restrain the market growth?

High production costs, cold chain logistics challenges, patent expirations, and regulatory hurdles are the main restraints.

5. Which diseases are commonly treated using therapeutic proteins?

Therapeutic proteins are used in the treatment of cancer, diabetes, autoimmune diseases, anemia, hemophilia, and infectious diseases.

6. Which region dominates the therapeutic proteins market?

North America holds the largest market share, followed by Europe and the Asia-Pacific region, due to advanced healthcare infrastructure and high R&D investments.

7. What technological trends are shaping the therapeutic proteins market?

Key trends include AI-driven protein design, CRISPR-based genetic engineering, continuous manufacturing, and development of biosimilars.

8. What role do biosimilars play in the therapeutic proteins market?

Biosimilars are driving cost reduction and market expansion by offering affordable alternatives to branded biologics as patents expire.

9. What are the major challenges faced by market participants?

Challenges include high R&D costs, stringent regulatory approvals, immunogenicity risks, and competition from biosimilars.

10. What is the future outlook for the therapeutic proteins market?

The market is expected to continue expanding due to growing adoption of biologics, increasing healthcare investments, and technological innovations in protein engineering and delivery.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com