U.S. Battery Market Size, Share, Trends & Growth Forecast Report By Type, By State, By Application, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Battery Market Size

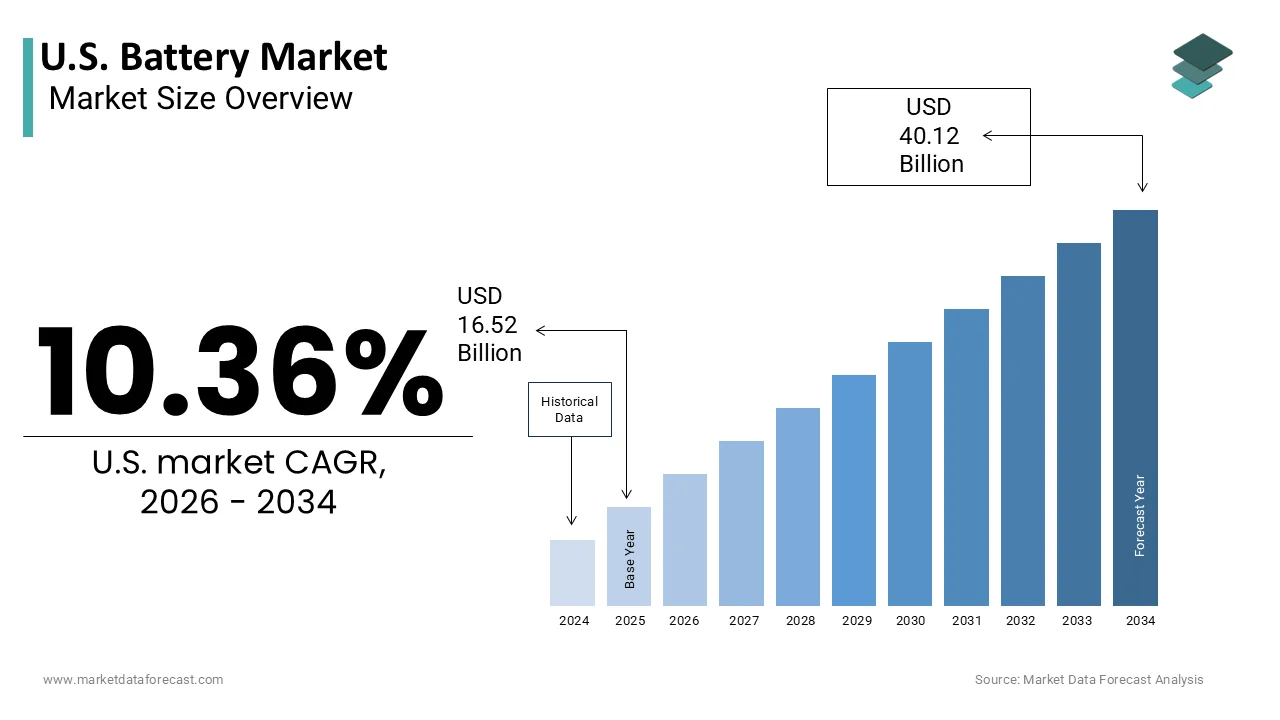

The United States Battery Market was valued at USD 16.52 billion in 2025, is estimated to reach USD 18.23 billion in 2026, and is projected to reach USD 40.12 billion by 2034, growing at a CAGR of 10.36% from 2026 to 2034.

The battery is a recycling of electrochemical energy storage devices that power a vast array of applications from consumer electronics to electric vehicles and grid infrastructure. Batteries are categorized into primary non-rechargeable and secondary rechargeable types, with lithium-ion technology dominating the modern market due to its high energy density and efficiency. According to the US Department of Energy, the adoption of electric vehicles has accelerated significantly, with sales reaching over 1 million units in recent years,s creating an unprecedented demand for advanced traction batteries. As per the Environmental Protection Agency, the management of battery waste has become a critical environmental priority, ty prompting stricter regulations on disposal and recycling practices. Federal initiatives such as the Inflation Reduction Act provide substantial incentives for local production of battery components and critical minerals. Consumer electronics remain a steady source of demand, while industrial applications,s including backup power systems and renewable energy storage,ge are expanding rapidly. The industry faces complex logistical challenges related to the sourcing of raw materials like lithium, cobalt, and nickel. Technological advancements in solid-state and sodium-ion batteries promise to further revolutionize the sector.

MARKET DRIVERS

Rapid Adoption of Electric Vehicles

The rapid adoption of electric vehicles is driving the growth of the United States battery market by creating exponential demand for high-capacity lithium-ion batteries. Government mandates and consumer preference for sustainable transportation are accelerating the transition from internal combustion engines to electric powertrains. According to the Alliance for Automotive Innovation, major automakers have committed billions of dollars to electrify their fleets with targets to make a significant percentage of new vehicle sales electric by 2030. Each electric vehicle requires a large battery pack, typically ranging from 50 to 100 kilowatt hours,s which drastically increases the volume of batteries needed compared to traditional automotive applications. The expansion of charging networks across the country further alleviates range anxiety, encouraging broader adoption. Automakers are partnering with battery manufacturers to secure long-term supply agreements, ensuring consistent production capabilities. The push for zero emissions in urban areas also drives municipal fleets to adopt electric buses and delivery vans. This systemic shift toward electrified mobility ensures that the automotive sector remains the largest and fastest-growing consumer of advanced battery technologies.

Growth in Renewable Energy Storage Systems

The growth in renewable energy storage systems by addressing the intermittency issues associated with solar and wind power generation is amplifying the growth of the United States battery market. As the nation shifts toward cleaner energy sources, the need for efficient storage solutions to balance supply and demand becomes critical. According to the US Energy Information Administration, utility-scale battery storage capacity has increased substantially in recent years, with projections indicating continued robust growth. As per the Solar Energy Industries Association, the pairing of solar photovoltaic systems with battery storage allows homeowners and businesses to maximize self-consumption and reduce reliance on the grid. Federal and state incentives,s such as the Investment Tax Credit, encourage the installation of residential and commercial energy storage systems. Grid operators utilize large-scale battery installations to provide frequency regulation and peak shaving services, enhancing grid stability and reliability. The declining cost of battery technology makes these systems increasingly economically viable for widespread deployment. Corporate sustainability goals also drive companies to invest in on-site storage to manage energy costs and carbon footprints. The integration of smart grid technologies further optimizes battery usage, enabling a dynamic response to energy price fluctuations.

MARKET RESTRAINTS

Supply Chain Vulnerabilities and Raw Material Scarcity

The supply chain vulnerabilities and raw material scarcity, by limiting production capacity and increasing cost,s are declining the growth of the United States battery market. The production of lithium -ion batteries relies heavily on minerals, such as lithium, cobalt, nickel, and graphite, which are predominantly sourced from a limited number of countries. The United States has limited domestic reserves of these materials, making it dependent on imports that are subject to geopolitical tensions and trade restrictions. As per the International Energy Agency, the demand for these minerals is projected to outstrip supply in the coming decade,e leading to potential disruptions and price volatility. Mining and processing these materials involve complex environmental and social considerations that can delay project approvals and increase operational costs. Disruptions in global logistics further exacerbate supply chain instability, thereby affecting the timely delivery of components to manufacturers. The concentration of refining capabilities in specific regions creates single points of failure that pose risks to the entire industry. Efforts to diversify supply sources and develop alternative chemistries are ongoing but require significant time and investment. This dependency constrains the ability of manufacturers to scale production efficiently and meet surging demand.

High Initial Costs and Economic Barriers

The high initial costs and economic barriers by limiting accessibility for consumers and applicatarens are also slowing down the growth of the United States battery market. Despite declining prices, the upfront cost of battery systems, particularly for electric vehicles and home energy storage,e remains prohibitive for many buyers. The average price of an electric vehicle continues to be higher than that of comparable internal combustion engine vehicles, primarily due to battery expenses. As per the Bureau of Labor Statistics, inflationary pressures on raw materials and labor have slowed the rate of price reduction for battery packs. Small and medium-sized enterprises may struggle to afford the capital expenditure required for industrial battery systems. Financing options are not always readily available or affordable, further restricting market penetration. The total cost of ownership,p although often lower over time, does not always offset the immediate financial burden for budget-constrained consumers. Manufacturers face pressure to reduce costs while maintaining performance and safety standards, which is technologically challenging. These economic factors slow the rate of adoption and limit the market potential in price-sensitive segments.

MARKET OPPORTUNITIES

Development of Solid-State Battery Technology

The development of solid-state battery technology, by offering superior performance and safety characteristics compared to conventional lithium-ion batteries, is creating new opportunities for the growth of the United States battery market. Solid-state batteries replace the liquid electrolyte with a solid material, which enhances energy density and reduces the risk of fire. According to the US Department of Energy, research initiatives are heavily focused on overcoming technical hurdles to commercialize this next-generation technology. Automotive manufacturers are investing billions in pilot production facilities to integrate solid-state batteries into future vehicle models. The higher energy density allows for longer driving ranges and faster charging times, addressing key consumer concerns. Enhanced safety features make these batteries attractive for aerospace and medical applications where reliability is paramount. The potential to use lithium metal anodes further increases capacity and reduces weight. Early adopters in niche markets can validate the technology before mass production. Collaborations between universities,s national laboratories, es and private companies accelerate innovation and knowledge sharing.

Expansion of Battery Recycling Infrastructure

The expansion of battery recycling infrastructure by creating a circular economy for materials is certainly expected to boost new opportunities for the growth of the United States battery market. As the volume of end-of-life batteries increases, the need for efficient recycling processes becomes urgent to recover valuable metals and reduce environmental impact. According to the Environmental Protection Agency, establishing robust recycling networks can significantly reduce the dependence on virgin raw materials and lower supply chain risks. Advanced hydrometallurgical and pyrometallurgical techniques enable high recovery rates of lithium, cobalt, and nickel, making recycling economically viable. Regulatory frameworks are increasingly mandating producer responsibility for battery disposal,l encouraging manufacturers to invest in recycling capabilities. Partnerships between automakers, battery producers,s and recyclers facilitate closed-loop systems that ensure material security. The growing market for recycled materials attracts investment from venture capital and strategic industry players. Developing domestic recycling capacity aligns with national security goals by reducing reliance on imports. This sustainable approach not only mitigates environmental hazards but also creates new revenue streams and jobs.

MARKET CHALLENGES

Safety Concerns and Thermal Management Issues

The safety concerns and thermal management issues, by impacting consumer confidence and regulatory compliance, are one of the challenges for the growth of the United States battery market. Lithium-ion batteries are susceptible to thermal runaway, a phenomenon where excessive heat leads to fire or explosion if not properly managed. The incidents involving battery fires in vehicles and homes have raised public awareness and scrutiny regarding safety standards. Manufacturers must invest heavily in advanced battery management systems and cooling technologies to prevent overheating and ensure stable operation. Designing enclosures that contain potential failures adds complexity and cost to product development. Recall events due to safety defects can damage brand reputation and result in significant financial liabilities. Regulatory agencies are tightening standards for transportation and storage of batteries, adding compliance burdens. Educating consumers on proper usage and maintenance is essential to mitigate risks. The fear of safety incidents can slow the adoption rate,s particularly in high-visibility applications like electric aviation. Addressing these safety challenges requires continuous innovation in materials and system design.

Regulatory Complexity and Compliance Burdens

The regulatory complexity and compliance burdens, by creating operational hurdles and increasing cost, are additionally hindering the growth of the United States battery market. The battery industry is subject to a myriad of federal, state, and local regulations governing manufacturing, transportation, storage, and disposal. The strict guidelines for shipping hazardous materials impose logistical constraints and additional expenses on suppliers. The workplace safety standards for battery manufacturing facilities require specialized training and equipment to protect workers from chemical exposures. Environmental regulations under the Resource Conservation and Recovery Act mandate proper handling of battery waste, further complicating end-of-life management. Varying state laws regarding extended producer responsibility and recycling mandates create a fragmented compliance landscape for national operators. Keeping pace with evolving regulations requires dedicated legal and compliance resources, which can be burdensome for smaller companies. The uncertainty surrounding future regulatory changes makes long-term planning difficult. Harmonizing standards across jurisdictions would alleviate some of these pressures, but it remains a distant goal.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, State, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Tesla, Inc., Panasonic Holdings Corporation, LG Energy Solution Ltd., Samsung SDI Co., Ltd., SK On Co., Ltd., EnerSys, Clarios, A123 Systems LLC, East Penn Manufacturing Company, American Battery Technology Company, Toshiba Corporation, BYD Company Limited |

SEGMENTAL ANALYSIS

By Type Insights

The lithium-ion battery segment was the largest by holding 56.4% of the United States battery market share in 2025 due to its role in powering electric vehicles, which represent the largest growth area for battery consumption. The high energy density and lightweight nature of lithium-ion chemistry make it the preferred choice for automotive manufacturers seeking to maximize driving range and performance. As per the Alliance for Automotive Innovation, major automakers have committed to transitioning their fleets to electric powertrains, driving unprecedented demand for lithium-ion packs. The superior charge retention and lower self-discharge rates compared to legacy technologies like lead acid ensure that lithium-ion remains the standard for modern mobility. Government incentives under the Inflation Reduction Act further encourage the domestic production of lithium-ion cells, reinforcing their market leadership. The scalability of lithium-ion technology allows it to be adapted for various vehicle classes from compact cars to heavy-duty trucks. This widespread adoption across the automotive sector ensures that lithium-ion batteries maintain their dominant position in terms of both volume and value.

The lithium-ion battery segment is also growing at the fastest CAGR of 8.6% during the forecast period due to its rapid adoption in grid-scale energy storage systems, which are essential for integrating renewable energy sources. The need to store excess solar and wind power for use during peak demand periods is driving massive investments in utility-scale battery projects. The declining cost of lithium-ion batteries makes them increasingly competitive with traditional peaker plants, accelerating their deployment. Federal tax credits for energy storage further incentivize developers to choose lithium-ion technology for new projects. The ability of these batteries to respond quickly to frequency fluctuations provides valuable services to grid operators. This surge in infrastructure investment ensures that lithium-ion batteries experience the highest growth rate among all battery types. The scalability and modularity of lithium-ion systems allow for easy expansion of storage capacity as needed.

By State Insights

The secondary or rechargeable batteries segment was the largest by occupying 34.4% of the US battery market share in 2025 due to the widespread proliferation of reusable electronic devices that require frequent recharging. The shift from disposable to rechargeable power sources is driven by economic and environmental considerations as consumers seek to reduce waste and long-term costs. According to the Environmental Protection Agency, the recycling and reuse of batteries has become a priority initiative, encouraging the adoption of secondary batteries in household and industrial applications. The convenience of USB charging and wireless charging technologies has made secondary batteries more user-friendly, reducing the friction associated with battery replacement. Smartphones, laptops, and electric vehicles all rely exclusively on secondary batteries, creating a massive installed base that drives recurring demand for replacements and upgrades. The longevity of modern lithium-ion and nickel-metal-hydride batteries ensures they can withstand hundreds of charge cycles, providing reliable performance over time. This durability makes them a cost-effective choice for high usage applications. The integration of battery management systems in devices further optimizes charging and extends lifespan.

The secondary battery segment is likely to witness the fastest CAGR of 7.4% during the forecast period due to the rapid expansion of home energy storage systems, which allow homeowners to store solar energy and manage electricity usage. The increasing frequency of power outages and rising electricity rates are motivating consumers to invest in backup power solutions. According to the Wood Mackenzie report, the residential energy storage market in the United States has grown at a compound annual growth rate of over 30% in recent years. Secondary batteries, such as lithium-ion units, provide the necessary capacity and cycle life for daily charging and discharging in home environments. The ability to participate in virtual power plant programs allows homeowners to earn revenue by supplying stored energy back to the grid during peak times. This financial incentive accelerates the adoption of home storage systems. Technological advancements have made these systems safer and easier to install, reducing barriers to entry.

By Application Insights

The consumer electronics segment held a dominant share of the US battery market in 2025 due to the ubiquity of smart devices in daily life. Smartphones, tablets, laptops, and wearables have become essential tools for communication, work, and entertainment, creating a constant demand for portable power. According to the Consumer Technology Association, the average American household possesses numerous connected devices, each requiring reliable battery performance. The trend toward thinner and lighter devices has increased the reliance on high-energy-density batteries that can fit into compact spaces. Consumers expect all-day battery life, driving manufacturers to optimize power management and battery capacity. The frequent upgrade cycle of electronic devices ensures a continuous turnover of battery demand. Accessories such as wireless earbuds and smartwatches also contribute to this segment, adding to the overall volume. The integration of batteries into everyday objects such as smart home sensors and kitchen appliances further expands the scope of this application.

The electric mobility segment is expected to witness the fastest CAGR of 5.4% from 2026 to 2034, with the strong government incentives and regulatory pushes for zero-emission transportation. Federal and state policies are actively promoting the adoption of electric vehicles through tax credits, rebates, and infrastructure investments. As per the Environmental Protection Agency, stricter emissions standards are forcing automakers to accelerate their electric vehicle timelines, increasing battery procurement. These policy measures lower the barrier to entry for consumers and stimulate market growth. The mandate for federal fleets to transition to electric vehicles also creates a great institutional demand for batteries. The alignment of political will with environmental goals ensures sustained support for the electric mobility sector. This regulatory framework creates a favorable environment for rapid expansion. The certainty provided by long-term policy commitments encourages investment in manufacturing and infrastructure.

COMPETITIVE LANDSCAPE

The competition in the United States battery market is intense and characterized by the entry of global giants alongside emerging domestic startups vying for dominance in the electrification era. Major players compete based on technological innovation, production scale, cost efficiency,y and supply chain security to secure contracts with automotive and energy clients. The market sees significant investment in manufacturing capacity as companies race to build gigafactories across the country to meet rising demand. Government incentives under the Inflation Reduction Act further intensify competition by rewarding domestic production and sourcing. Established Asian manufacturers leverage their experience and scale, while US-based firms focus on innovation and proximity to customers. New entrants bring disruptive technologies such as solid-state batteries, challenging existing norms. Intellectual property disputes and talent acquisition are common battlegrounds as firms seek to protect their advantages. The race to achieve cost parity with internal combustion engines drives continuous improvement in battery chemistry and manufacturing processes.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Battery Market include

- Tesla, Inc.

- Panasonic Holdings Corporation

- LG Energy Solution Ltd.

- Samsung SDI Co., Ltd.

- SK On Co., Ltd.

- EnerSys

- Clarios

- A123 Systems LLC

- East Penn Manufacturing Company

- American Battery Technology Company

- Toshiba Corporation

- BYD Company Limited

TOP LEADING PLAYERS IN THE MARKET

- Tesla Inc is a global leader in electric vehicle manufacturing and energy storage solutions with a significant impact on the battery market. The company designs and produces advanced lithium-ion batteries for its vehicles and stationary power products. Tesla operates massive gigafactories that drive economies of scale and reduce production costs significantly. Recent actions include the development of proprietary battery chemistries such as the 4680 cell, which promises higher energy density and lower manufacturing complexity. The company also invests heavily in vertical integration by securing direct supply agreements for critical minerals like lithium and nickel. These initiatives strengthen its market position by ensuring supply chain resilience and technological leadership. Tesla continues to innovate in battery management software to enhance performance and safety.

- Contemporary Amperex Technology Co.,o Limited, known as CATL, is the world's largest manufacturer of lithium-ion batteries for electric vehicles and energy storage systems. The company supplies batteries to major global automakers and has established a strong presence in the United States through licensing agreements and partnerships. CATL focuses on continuous research and development to improve battery efficiency and sustainability. Recent actions include the launch of sodium-ion batteries, which offer a cost-effective alternative to lithium-based solutions. The company also expands its recycling capabilities to recover valuable materials and reduce environmental impact. CATL collaborates with US companies to localize production and meet regulatory requirements under the Inflation Reduction Act. These strategies strengthen its global influence and ensure access to key markets. By prioritizing innovation and scalability, CATL remains a dominant force in the international battery industry.

- LG Energy Solution Ltd is a leading global battery manufacturer with extensive operations in the United States, supplying cells to major automotive brands. The company produces a wide range of battery types, es including cylindrical, prismatic, and pouch cells for various applications. LG Energy Solution invests heavily in expanding its manufacturing footprint in North America to serve local demand. Recent actions include joint ventures with General Motors and Honda to build new battery plants in the US. The company focuses on developing next-generation technologies such as solid-state batteries to enhance safety and performance. LG Energy Solution also emphasizes sustainable practices by reducing carbon emissions in its production processes. These efforts strengthen its market position by aligning with customer needs and regulatory standards.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States battery market employ several major strategies to maintain competitiveness and drive growth. Vertical integration is central to these efforts, with companies securing direct access to raw materials such as lithium and nickel to stabilize supply chains. Strategic partnerships and joint ventures with automakers enable manufacturers to share risks and accelerate the deployment of new production facilities. Investment in research and development focuses on next-generation technologies like solid-state and sodium-ion batteries to enhance performance and safety. Localization of manufacturing through the construction of domestic gigafactories helps companies comply with regulatory incentives and reduce logistics costs. Sustainability initiatives, including a battery recycling program,s address environmental concerns and create circular economy opportunities. Digitalization of production processes improves efficiency and quality control. These combined strategies allow participants to navigate market complexity and sustain long-term profitability in a highly competitive environment.

MARKET SEGMENTATION

This research report on the U.S. battery market is segmented and sub-segmented into the following categories.

By Type

- Lithium-Ion Battery

By State

- Secondary (Rechargeable) Batteries

By Application

- Consumer Electronics

- Electric Mobility

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com