U.S. Beef Market Size, Share, Trends & Growth Forecast Report By Cut Type, By Distribution Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Beef Market Size

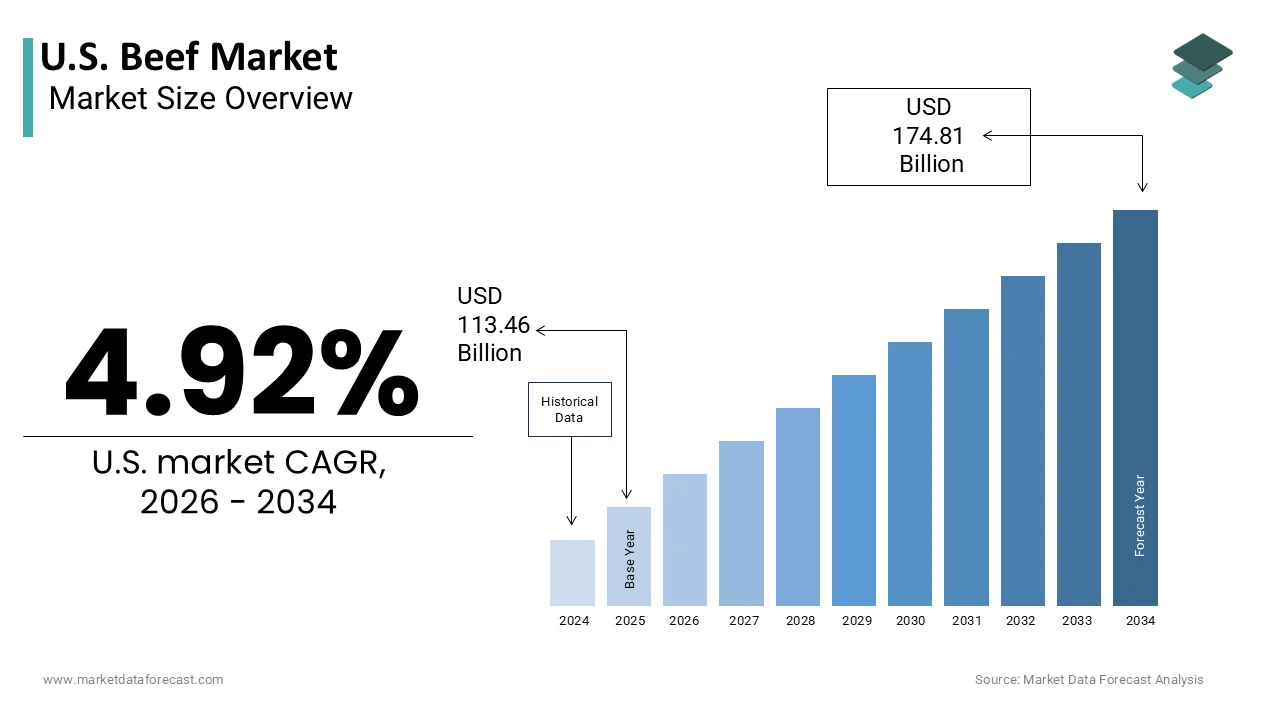

The United States Beef Market was valued at USD 113.46 billion in 2025, is estimated to reach USD 119.04 billion in 2026, and is projected to reach USD 174.81 billion by 2034, growing at a CAGR of 4.92% from 2026 to 2034.

The beef is the complex supply chain that integrates cow-calf operations, feedlots, packing plants, and retail outlets. Beef remains a primary source of protein for American consumers, deeply embedded in cultural dietary habits and culinary traditions. According to the United States Department of Agriculture, the United States is one of the largest producers and consumers of beef globally, with domestic production exceeding 27 billion pounds in recent annual assessments. The industry operates within a framework of strict regulatory oversight regarding food safety, animal welfare, and environmental sustainability. As per the National Cattlemen’s Beef Association, consumer demand is increasingly influenced by factors such as product quality, origin transparency, and production methods. Per capita consumption of beef in the United States stands at approximately 57 pounds annually, reflecting steady demand despite fluctuating prices. The industry faces dynamic shifts driven by health trends, economic conditions, and international trade policies. Export markets play a crucial role in balancing domestic supply and enhancing producer profitability. The integration of technology in livestock management and supply chain tracking is transforming operational efficiencies.

MARKET DRIVERS

Strong Cultural Preference and High Protein Demand

The enduring cultural preference for beef and the high demand for protein-rich diets are fuelling the growth of the United States beef market. Beef is traditionally associated with celebratory meals, barbecues, and everyday dining, creating a consistent baseline demand that is resilient to short-term economic fluctuations. The nutritional profile of beef, which includes essential amino acids, iron, and vitamin B12, appeals to health-conscious consumers who prioritize nutrient density. As per the National Health and Nutrition Examination Survey, a substantial segment of the population relies on animal-based proteins to meet daily dietary requirements, sustaining demand for high-quality cuts. The popularity of specific cuts such as ribeye, sirloin, and ground beef drives volume sales across retail and foodservice channels. Ground beef, in particular, is a staple in American households due to its versatility and affordability. The foodservice industry, including fast food chains and casual dining restaurants, further amplifies this demand by incorporating beef into menu staples like burgers and steaks. Consumer loyalty to beef is reinforced by marketing campaigns that emphasize taste and satisfaction. The demographic diversity of the United States ensures that beef consumption spans various age groups and ethnic backgrounds.

Expansion of Export Markets and International Trade

The expansion of export markets and favorable international trade agreements by providing additional revenue streams for producers is also enhancing the growth of the United States beef market. The United States is a major exporter of beef, with key destinations including Japan, South Korea, Mexico, and Canada. According to the US Meat Export Federation, beef exports reached record highs in recent years, with volume exceeding 3 billion pounds and value surpassing 10 billion dollars. These exports help balance domestic supply and support higher cattle prices for ranchers. Trade agreements, such as the United States-Mexico-Canada agreement, facilitate tariff-free access to neighboring countries by enhancing competitiveness. The reputation of US beef for consistency and safety attracts international buyers, who value standardized grading systems. Export demand also encourages producers to maintain high-quality standards to meet international specifications. The diversification of export markets reduces reliance on any single country, mitigating risks associated with trade disputes or geopolitical tensions. Furthermore, the weakening of the US dollar at times enhances the price competitiveness of American beef in global markets. The industry actively promotes US beef through international marketing initiatives that highlight quality and sustainability.

MARKET RESTRAINTS

Environmental Concerns and Regulatory Pressure

The environmental concerns and increasing regulatory pressure by imposing additional costs and operational constraints on producers are hindering the growth of the United States beef market. Cattle production is often cited as a major contributor to greenhouse gas emissions, particularly methane, which has drawn scrutiny from environmental advocates and policymakers. This has led to proposed regulations aimed at reducing emissions and improving waste management practices on farms. Compliance with these regulations requires investments in technology and infrastructure, which can be prohibitive for smaller operations. Water usage for cattle farming is another critical issue, especially in drought-prone regions such as the Southwest. Regulatory limits on water rights and land use can restrict expansion and increase operational costs. Consumers are also becoming more environmentally conscious, with some reducing beef consumption due to its perceived ecological footprint. This shift in consumer behavior challenges the industry to demonstrate sustainability credentials. The potential for carbon taxes or emission caps adds uncertainty to long-term planning.

High Production Costs and Input Volatility

The high production costs and volatility in input prices are also impeding the growth of the United States beef market. The cost of feed, which constitutes a significant portion of raising cattle, is subject to fluctuations due to weather conditions, global demand, and energy prices. The corn and soybean prices have experienced significant variability, directly impacting feedlot expenses. Energy costs for transportation, machinery, and facility operations also contribute to rising production expenses. As per the Bureau of Labor Statistics, inflation in agricultural inputs has outpaced general inflation rates, increasing the financial burden on ranchers. Labor shortages in the agricultural sector further exacerbate costs, as wages rise to attract and retain workers. The capital-intensive nature of cattle ranching requires substantial investment in land, equipment, and livestock, making it vulnerable to interest rate hikes. Higher borrowing costs reduce the ability of producers to expand or modernize operations. Price volatility in the live cattle market adds uncertainty, making it difficult for producers to predict revenues. When input costs rise faster than beef prices, profitability declines, leading to herd liquidation and reduced supply.

MARKET OPPORTUNITIES

Growth of Premium and Value-Added Beef Products

The growth of premium and value-added beef products by catering to discerning consumers willing to pay for quality and convenience is creating new opportunities for the growth of the United States beef market. The sales of natural and organic meat products have grown at a double-digit rate, outpacing conventional beef sales. Brands that offer transparency in sourcing and production methods can command premium prices and build loyal customer bases. Value-added products, such as pre-marinated cuts, ready-to-cook meals, and subscription boxes, offer convenience that appeals to busy households. The rise of e-commerce platforms allows niche brands to reach consumers directly, bypassing traditional retail barriers. Retailers are expanding their premium beef offerings to differentiate themselves and capture higher margins. The trend toward culinary experimentation at home has increased demand for specialty cuts and international varieties. Producers who invest in branding and storytelling can enhance the perceived value of their products. This shift toward premiumization allows the industry to offset volume stagnation with higher revenue per unit.

Technological Advancements in Supply Chain Transparency

The technological advancements in supply chain transparency by enhancing trust and efficiency are additionally expected to enhance the growth of the United States beef market. Blockchain technology and digital tracking systems enable consumers to verify the origin, handling, and sustainability credentials of beef products. The pilot programs using blockchain have demonstrated improved traceability and reduced time to identify contamination sources. This level of transparency addresses consumer concerns about food safety and ethical sourcing. Digital platforms allow producers to share data on animal welfare, feed composition, and carbon footprint, appealing to environmentally conscious buyers. Retailers can use this information to market verified sustainable beef, differentiating their offerings in a crowded marketplace. Technology also improves operational efficiency by optimizing inventory management and reducing waste. Smart sensors and Internet of Things devices monitor cattle health and environmental conditions, enabling proactive management. The integration of data analytics helps producers make informed decisions about breeding and feeding strategies. These technological tools facilitate compliance with regulatory requirements and industry standards.

MARKET CHALLENGES

Labor Shortages in Processing and Production

The labor shortages in processing facilities and production operations, by disrupting supply chains and increasing costs, are significantly slowing the growth of the United States beef market. The meatpacking industry relies heavily on manual labor for slaughtering, cutting, and packaging, but faces difficulties in recruiting and retaining workers. According to the North American Meat Institute, turnover rates in meat processing plants remain high, leading to operational inefficiencies and production bottlenecks. The physically demanding nature of the work and safety concerns contribute to recruitment challenges. Wage increases and benefits improvements have not fully resolved the shortage, as demographic shifts reduce the pool of eligible workers. Plant closures or reduced shifts due to labor constraints can lead to backups in the supply chain, affecting cattle prices and product availability. The reliance on immigrant labor makes the industry vulnerable to changes in immigration policy and enforcement. Training new employees requires time and resources, further straining operations. The lack of automation in certain processing steps exacerbates the dependency on human labor.

Animal Disease Outbreaks and Biosecurity Risks

The animal disease outbreaks and biosecurity risks, by threatening herd health and consumer confidence, are also degrading the growth of the United States beef market. Diseases such as bovine respiratory disease and potential outbreaks of foot and mouth disease can have devastating economic impacts. According to the USDA Animal and Plant Health Inspection Service, disease prevention is a top priority, but the risk of introduction from foreign countries remains a concern. An outbreak would lead to immediate trade restrictions, closing export markets, and causing domestic prices to plummet. Biosecurity measures require constant vigilance and investment, which can be burdensome for small producers. Consumer perception of food safety is easily shaken by news of disease, leading to temporary drops in demand. The concentration of cattle in feedlots increases the risk of rapid disease spread, necessitating rigorous health monitoring. Vaccination and treatment protocols add to production costs. The threat of zoonotic diseases also raises public health concerns, prompting stricter regulatory oversight. Managing these risks requires coordination among government agencies, industry groups, and producers. The uncertainty surrounding disease outbreaks creates volatility in the market, affecting investment and planning.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Cut Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Tyson Foods, Inc., JBS USA Holdings, Inc., Cargill, Incorporated, National Beef Packing Company, LLC, Smithfield Foods, Inc., Hormel Foods Corporation, Conagra Brands, Inc., Sysco Corporation, Perdue Farms, Inc., OSI Group, LLC, Agri Beef Co., American Foods Group, LLC |

SEGMENTAL ANALYSIS

By Cut Type Insights

The ground beef segment was the largest by holding 23.4% of the United States beef market share in 2025 due to its exceptional versatility and affordability, making it a staple in American households. This cut is utilized in a wide array of dishes ranging from tacos and chili to burgers and meatballs, appealing to diverse culinary preferences. The ability to incorporate ground beef into quick and easy meals aligns with the busy lifestyles of modern consumers who prioritize convenience without sacrificing protein intake. The ground beef consistently ranks as the highest volume beef product sold in retail grocery stores, driven by its lower price point compared to premium steaks. This economic advantage allows families to maintain beef consumption levels even during periods of inflation or economic uncertainty. Furthermore, the uniform texture and cooking properties of ground beef make it ideal for large batch preparation, which supports meal prepping trends. The widespread availability of various lean-to-fat ratios enables health-conscious consumers to choose options that fit their dietary goals. This adaptability ensures that ground beef remains the most accessible and frequently purchased beef product across all demographic segments.

The steak cuts segment is likely to register the fastest CAGR of 12.3% of the US beef market share in 2025, with the rising disposable income and the ongoing trend of premiumization in food consumption. As consumers recover economically, there is a marked shift toward indulgent dining experiences at home, where high-quality steaks are perceived as affordable luxuries. The sales of premium steak cuts, such as ribeye, strip loin, and tenderloin, have outpaced overall beef category growth, with value increases attributed to both higher prices and increased volume. Consumers are increasingly willing to pay for superior marbling, aging, and sourcing standards, viewing steak consumption as a marker of quality of life. The influence of social media and culinary television programs has elevated the status of home cooking, encouraging individuals to replicate restaurant-quality meals using premium ingredients. Retailers have responded by expanding their offerings of certified Angus beef and wagyu styles, catering to this discerning segment. The perception of steak as a celebratory food also drives periodic spikes in demand during holidays and special occasions. This emotional connection, combined with financial capability,y ensures that steak cuts continue to capture a larger share of consumer spending.

By Distribution Channel Insights

The retail grocery stores segment accounted for a prominent share of the US beef market in 2025 due to their ubiquity and the convenience they offer for weekly household shopping. Supermarkets and grocery chains serve as the primary touchpoints for the majority of consumers, who purchase beef for home consumption. The retail accounts for the largest share of beef disappearance, reflecting the preference for home-cooked meals. The one-stop shopping model allows consumers to purchase beef alongside other groceries, streamlining the shopping experience. Major retailers invest heavily in supply chain infrastructure to ensure consistent stock and competitive pricing, which builds customer loyalty. The presence of in-store butchers and self-service meat counters provides flexibility in choice and customization. Promotional activities such as weekly flyers and loyalty program discounts drive traffic and volume sales. The trust established through long-standing relationships with local grocery chains encourages repeat purchases. Furthermore, the expansion of private-label beef brands offers cost-effective alternatives that appeal to budget-conscious shoppers. The physical presence of stores in nearly every community ensures that retail remains the dominant channel for beef distribution. The ability to inspect product quality personally before purchase also reinforces consumer preference for this channel over others.

The e-commerce and online retail segment is expected to witness 8.6% from 2026 to 203,4 with the fundamental shift in consumer behavior toward digital purchasing. The convenience of ordering meat online and having it delivered to the doorstep has attracted a broad demographic, including younger shoppers and busy professionals. The online grocery sales have stabilized at levels significantly higher than pre-pandemic figures, indicating a permanent change in shopping habits. The frequency of online grocery orders has increased, with meat and seafood being key drivers of basket size. Consumers appreciate the ability to browse extensive selections, read reviews, and compare prices without leaving home. The elimination of physical store visits saves time and reduces exposure to crowded environments, which remains a consideration for some shoppers. Online platforms often provide detailed information about sourcing, sustainability, and animal welfare, appealing to ethically conscious buyers. The ease of setting up recurring orders for staple items like ground beef ensures consistent revenue streams for online retailers. Mobile applications enhance the user experience by offering personalized recommendations and seamless checkout processes. The integration of social media marketing drives traffic to online beef retailers by showcasing recipes and product quality. This digital transformation allows retailers to reach customers beyond their geographic footprint, expanding market potential.

COMPETITIVE LANDSCAPE

The competition in the United States beef market is intense and characterized by the dominance of a few large integrated processors alongside numerous regional players. Major companies compete on the basis of price, product quality, supply chain efficiency, and brand reputation to secure contracts with retailers and foodservice operators. The high concentration in the packing sector gives leading firms significant influence over pricing and market dynamics. However, antitrust scrutiny and consumer demand for transparency are encouraging greater competition from smaller niche producers. Companies differentiate themselves through sustainability credentials, animal welfare standards, and innovative product offerings such as ready-to-cook meals. The rise of alternative proteins adds pressure on traditional beef producers to demonstrate value and environmental responsibility. Labor availability and operational efficiency are critical competitive factors as margins remain tight. Trade policies and export opportunities also shape competitive strategies as firms seek to diversify revenue sources. The market sees continuous investment in technology and infrastructure to improve productivity and meet evolving consumer preferences. This dynamic environment requires constant adaptation and strategic agility to maintain profitability and market relevance in a complex and regulated industry landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Beef Market include

- Tyson Foods, Inc.

- JBS USA Holdings, Inc.

- Cargill, Incorporated

- National Beef Packing Company, LLC

- Smithfield Foods, Inc.

- Hormel Foods Corporation

- Conagra Brands, Inc.

- Sysco Corporation

- Perdue Farms, Inc.

- OSI Group, LLC

- Agri Beef Co.

- American Foods Group, LLC

TOP LEADING PLAYERS IN THE MARKET

- Tyson Foods Inc is a global leader in protein production with a dominant presence in the United States beef market. The company operates an integrated supply chain that includes cattle feeding, processing, and distribution of fresh and frozen beef products. Tyson serves retail, foodservice, and industrial customers worldwide with a diverse portfolio of branded and private-label items. Recent actions include significant investments in automation and digital technologies to enhance operational efficiency and product consistency. The company has also expanded its sustainable sourcing initiatives to meet growing consumer demand for environmentally responsible practices. Tyson continues to innovate in value-added beef products such as marinated cuts and ready-to-cook meals. These strategic moves strengthen its market position by improving margins and customer loyalty. The organization focuses on optimizing its network of facilities to reduce costs and improve service reliability. This comprehensive approach ensures Tyson remains a key influencer in the global beef industry.

- JBS USA Holdings Inc is a major player in the global meat industry with extensive operations in the United States beef sector. As a subsidiary of JBS SA, the company leverages global scale to provide high-quality beef products to diverse markets. JBS USA operates numerous processing plants and distribution centers across the country, ensuring broad market coverage. Recent actions involve expanding its portfolio of premium and organic beef brands to capture higher margin segments. The company has invested heavily in sustainability programs,s including water conservation and renewable energy projects at its facilities. JBS USA also focuses on strengthening relationships with ranchers through transparent pricing and support services. These efforts enhance its reputation for quality and reliability among suppliers and customers. The integration of advanced traceability systems allows for better supply chain management and food safety assurance.

- Cargill Incorporated is a global agriculture and food company with a significant role in the United States beef market. The company manages a vast network of cattle feeding operations and processing facilities that supply beef to domestic and international clients. Cargill is known for its commitment to quality and sustainability in beef production. Recent actions include the development of new beef brands that emphasize animal welfare and environmental stewardship. The company has also invested in research and development to improve feed efficiency and reduce greenhouse gas emissions. Cargill collaborates with farmers to implement best practices that enhance productivity and profitability. These initiatives strengthen its market position by aligning with evolving consumer preferences and regulatory standards. The organization continues to expand its export capabilities to reach new markets and diversify revenue streams.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States beef market employ several major strategies to maintain competitiveness and drive growth. Vertical integration is a common approach where companies control multiple stages of the supply chain from feeding to processing to ensure quality and efficiency. Product diversification involves expanding into premium and value-added segments such as organic and grass-fed beef to capture higher margins. Sustainability initiatives are increasingly important, with firms investing in environmentally friendly practices to meet consumer expectations and regulatory requirements. Technological adoption includes using automation and data analytics to optimize operations and reduce costs. Strategic partnerships with retailers and foodservice providers help secure long-term contracts and stable demand. Export expansion allows companies to access international markets and balance domestic supply fluctuations. Branding efforts focus on building consumer trust through transparency and quality assurance programs. These strategies enable participants to navigate market challenges and capitalize on emerging opportunities effectively.

MARKET SEGMENTATION

This research report on the U.S. beef market is segmented and sub-segmented as follows.

By Cut Type

- Ground Beef

- Steak Cuts

By Distribution Channel

- Retail Grocery Stores

- E-commerce and Online Retail

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com