United States Beer Market Size, Share, Trends & Growth Forecast Report Segmented By Product (Non-crafted beer, Craft beer), Distribution Channel, Packaging and Country – Industry Analysis From 2026 to 2034

United States Beer Market Report Summary

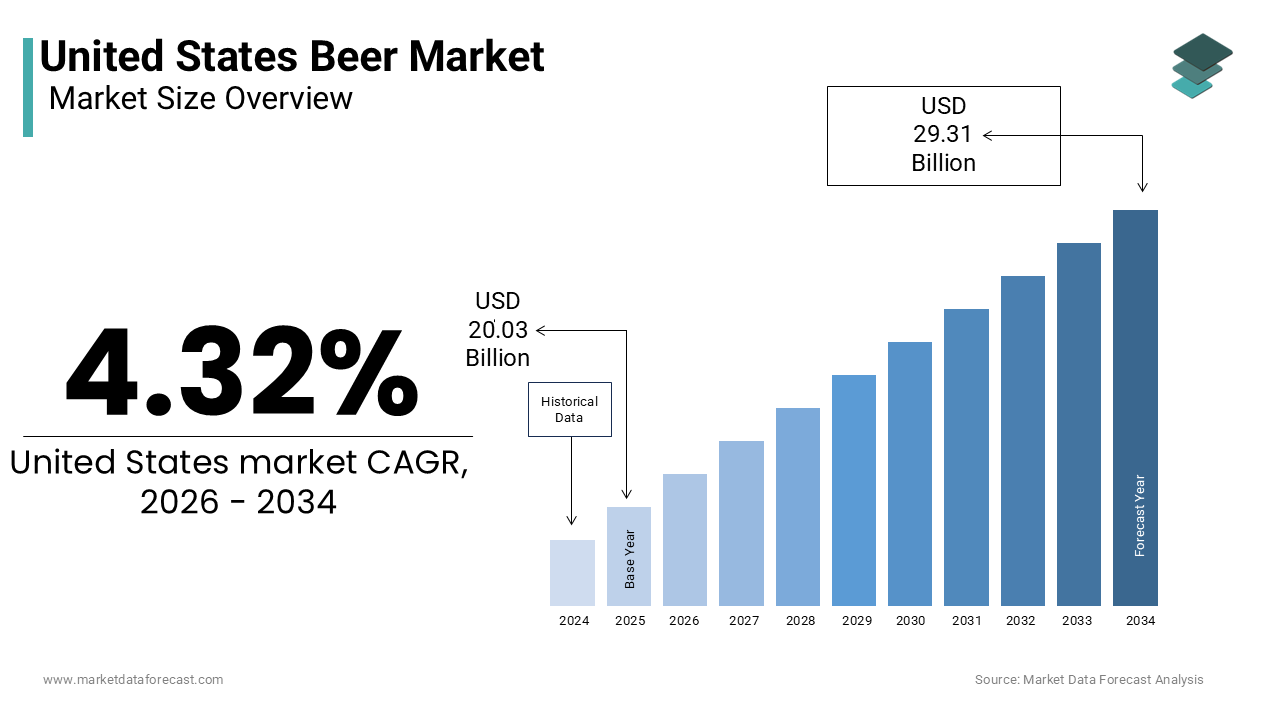

The United States beer market was valued at USD 20.03 billion in 2025, is estimated to reach USD 20.09 billion in 2026, and is projected to reach USD 29.31 billion by 2034, growing at a CAGR of 4.32% during the forecast period from 2026 to 2034. The growth of the U.S. beer market is driven by premiumization trends, continuous craft beer innovation, and the rising popularity of non-alcoholic and low-calorie variants. The market is evolving from volume-driven consumption toward value-driven, experience-based consumption, supported by changing consumer preferences and lifestyle shifts. Additionally, digital sales channels, sustainability initiatives, and product diversification are further contributing to market expansion.

Key Market Trends

- Rising demand for premium and craft beers driven by unique flavors and artisanal appeal

- Growing popularity of non-alcoholic and low-calorie beer variants among health-conscious consumers

- Increasing adoption of e-commerce and direct-to-consumer sales channels

- Strong focus on sustainability and eco-friendly brewing practices

- Shift in consumer preferences toward quality over quantity consumption patterns

Segmental Insights

- Based on product, the non-crafted beer segment was the largest and held a significant share of the U.S. beer market in 2025. The segment’s dominance is attributed to wide availability, strong distribution networks, affordability, and high brand recognition among mass consumers.

- Based on distribution channel, the off-trade segment accounted for a major share of the U.S. beer market in 2025. This is driven by the convenience of home consumption, availability across retail outlets, and continued consumer preference for at-home drinking experiences.

Regional Insights

The United States represents a mature yet evolving beer market, characterized by premiumization, craft innovation, and diversification into non-alcoholic alternatives. The market benefits from a strong cultural association with beer consumption, robust distribution infrastructure, and high consumer spending power.

The country continues to witness growth through innovation in flavors, packaging, and digital engagement strategies, while the recovery of on-trade channels and increasing demand for experiential consumption further support market expansion.

Competitive Landscape

The U.S. beer market is highly competitive, marked by the presence of large multinational brewers and a fragmented craft brewery segment. Leading companies focus on product innovation, portfolio diversification, sustainability, and digital transformation to maintain market leadership. Prominent players in the U.S. beer market include Anheuser-Busch InBev, Molson Coors Beverage Company, Constellation Brands, Inc., Heineken N.V., Carlsberg Group, Asahi Group Holdings Ltd., Diageo plc, and D.G. Yuengling & Son Inc. The Boston Beer Company Inc., and Sierra Nevada Brewing Co.

United States Beer Market Size

The United States beer market size was valued at USD 20.03 billion in 2025 and is anticipated to reach USD 20.09 billion in 2026 from USD 29.31 billion by 2034, growing at a CAGR of 4.32% during the forecast period from 2026 to 2034.

The beer is a mature yet dynamically evolving sector within the broader alcoholic beverage industry, characterized by a distinct shift from volume driven consumption to value oriented premiumization. As per data from the Beer Institute, the industry contributes approximately 346 billion U.S. dollars annually to the national economy, supporting over 2.4 million jobs through direct and indirect employment channels. Consumer behavior has transitioned toward quality over quantity, with per capita consumption stabilizing even as total volume declines slightly. Regulatory frameworks vary significantly by state, influencing distribution models and direct to consumer sales capabilities. The rise of non-alcoholic beer variants further diversifies the product offering by catering to health conscious demographics. Supply chain resilience remains a critical operational focus, particularly regarding the procurement of barley, hops, and aluminum packaging.

MARKET DRIVERS

Premiumization and Craft Beer Innovation

The premiumization and continuous innovation in craft beer formulations by compelling consumers to trade up from standard lagers to higher quality and unique flavor experiences is driving the growth of United States beer market. This trend is fueled by a demographic shift, where drinkers prioritize artisanal quality, local provenance, and distinct taste profiles over brand loyalty to mass produced options. Independent brewers frequently experiment with adjuncts such as fruit, coffee, and spices, creating limited edition releases that drive urgency and repeat purchases. The proliferation of hop forward styles has redefined consumer palates by encouraging exploration beyond traditional categories. Retailers respond by dedicating increased shelf space to craft selections, enhancing visibility and accessibility. The financial performance incentivizes large macro brewers to acquire successful craft labels or launch their own high end subsidiaries. The cultural association of craft beer with lifestyle and identity further reinforces demand, particularly among millennials and Generation Z consumers, who view beer selection as an expression of personal taste.

Expansion of Non Alcoholic and Low Calorie Variants

The rapid expansion of non-alcoholic and low calorie beer variants by addressing growing health consciousness and lifestyle flexibility among consumers is additionally fuelling the growth of United States beer market. Modern brewing technologies have improved the taste and mouthfeel of non-alcoholic beers by removing the stigma previously associated with these products. This surge is attributed to the wellness movement, where individuals seek to reduce alcohol intake without sacrificing the social ritual of drinking beer. Major breweries have invested heavily in dedicated production lines and marketing campaigns to normalize non alcoholic consumption in various settings, including workplaces and athletic events. The introduction of low calorie light beers with enhanced flavor profiles also appeals to fitness oriented demographics who monitor caloric intake. According to the Centers for Disease Control and Prevention, increasing awareness of the health risks associated with excessive alcohol consumption has prompted many adults to moderate their intake, driving demand for alternatives . Retailers are expanding their cold storage sections to accommodate these SKUs, recognizing their high turnover rates. The versatility of non alcoholic beer allows it to be consumed at any time of day, expanding usage occasions beyond traditional evening hours.

MARKET RESTRAINTS

Rising Production Costs and Supply Chain Volatility

Rising production costs and supply chain volatility constitute, squeezing profit margins and forcing price increases that may dampen consumer demand is majorly impeding the growth of the United States beer market. The cost of key raw materials such as barley, hops, and aluminum has fluctuated significantly due to geopolitical tensions, climate change impacts on agriculture, and logistical bottlenecks. Aluminum cans, the primary packaging format for beer, have faced periodic shortages and price spikes, complicating inventory management for brewers of all sizes. Energy costs associated with brewing, refrigeration, and transportation have also risen by adding to the operational burden. Small and independent breweries are particularly vulnerable to these pressures as they lack the economies of scale enjoyed by macro brewers. These financial strains limit the ability of brewers to invest in marketing, expansion, or innovation. Consumers may react to higher retail prices by trading down to cheaper brands or reducing overall consumption frequency.

Shifting Consumer Preferences Toward Alternative Beverages

The shifting consumer preferences toward alternative alcoholic and non-alcoholic beverages, eroding its share of the total alcohol wallet is also degrading the growth of United States beer market. Younger demographics, particularly Generation Z and younger Millennials, are increasingly opting for ready to drink cocktails, hard seltzers, wine, and spirits over traditional beer. Hard seltzers and flavored malt beverages offer lower calorie counts and diverse flavor options that appeal to health conscious and adventure seeking drinkers. The convenience and portability of ready to drink cans also align with modern on the go lifestyles. Spirits have gained popularity due to the cocktail culture resurgence, driven by social media trends and home mixology. This substitution effect forces beer manufacturers to diversify their portfolios into adjacent categories to retain customers. The perception of beer as a heavier or less sophisticated option compared to craft cocktails or premium wines further challenges its relevance in social settings. Breweries must compete not only with each other but with entirely different beverage categories for consumer attention and spending.

MARKET OPPORTUNITIES

Direct to Consumer Sales and E Commerce Integration

The expansion of direct-to-consumer sales and e commerce integration to bypass traditional distribution constraints and enhance customer engagement is certainly to create new opportunities for the growth of United states beer market. Regulatory changes in several states have relaxed laws regarding the shipping of alcohol by allowing breweries to sell directly to consumers online. E-commerce platforms enable breweries to offer subscription services, limited edition releases, and bundled merchandise by creating recurring revenue streams and fostering brand loyalty. Digital marketing tools allow for targeted advertising and personalized recommendations based on purchase history. The convenience of home delivery appeals to consumers who prefer shopping from home, a habit solidified during the pandemic. Breweries can collect valuable first party data to inform product development and marketing strategies. Direct relationships with consumers also improve margin retention by eliminating intermediary markups. Collaborations with third party delivery apps further expand reach and visibility.

Sustainability and Eco Friendly Brewing Practices

The adoption of sustainability and eco friendly brewing practices to differentiate brands and appeal to environmentally conscious consumers is another attribute to enhance the growth of the United States beer market. Investors and shoppers increasingly prioritize companies that demonstrate commitment to environmental stewardship and social responsibility. Breweries are implementing water conservation techniques, renewable energy sources, and waste reduction programs to minimize their ecological footprint. Packaging innovations such as lightweight cans, recyclable materials, and keg reuse programs resonate with consumers seeking sustainable options. Local sourcing of ingredients reduces transportation emissions and supports regional agriculture, enhancing brand storytelling. Certifications, such as B Corp status provide third party validation of sustainability efforts, building trust and credibility. Breweries that transparently communicate their sustainability initiatives can command premium pricing and foster deep customer loyalty. Partnerships with environmental organizations further amplify impact and visibility. As regulatory pressures regarding waste and emissions intensify, early adopters of green practices will gain competitive advantages.

MARKET CHALLENGES

Regulatory Complexity and Three Tier System Constraints

The regulatory complexity and the rigid three tier system by restricting operational flexibility and increasing compliance costs is to hamper the growth of the United States beer market in coming years. The three tier system mandates separate entities for production, distribution, and retail, preventing vertical integration in most states. Navigating varying state and local laws regarding labeling, taxation, and shipping requires significant legal resources and administrative overhead. Recent legal battles over direct to consumer shipping rights highlight the ongoing tension between traditional distributors and producers seeking modernization. Compliance with federal regulations from the Alcohol and Tobacco Tax and Trade Bureau adds another layer of complexity, particularly for new product approvals. According to the Small Business Administration, regulatory burdens disproportionately affect small businesses, limiting their ability to scale and compete with larger incumbents [[16]. Inconsistent enforcement and interpretation of laws across jurisdictions create uncertainty for multi state operators. Attempts to reform the system often face strong lobbying opposition from established distributors. These structural constraints hinder innovation and slow down market responsiveness. Brewers must dedicate substantial time and capital to regulatory compliance rather than product development or marketing.

Labor Shortages and Workforce Development Issues

The labor shortages and workforce development issues, affecting production capacity and service quality across the supply chain is also to slow down the growth of the United States beer market. The industry faces difficulties in recruiting skilled brewers, packaging line operators, and sales personnel due to demographic shifts and competition from other sectors. Breweries struggle to find employees with specialized technical skills required for modern brewing equipment and quality control processes. The hospitality sector, a key sales channel for beer, also faces staffing shortages, impacting on premise consumption experiences and sales volumes. Training and retaining staff require significant investment in wages and benefits, increasing operational costs. The aging workforce in traditional brewing roles creates a knowledge gap that is difficult to fill quickly. Apprenticeship programs and educational partnerships are being developed but take time to yield results. High turnover rates further disrupt operations and increase recruitment expenses. Addressing these labor challenges requires strategic investments in automation, employee wellness, and career development pathways.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.32% |

| Segments Covered | By Product, Distribution Channel, Packaging and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Key Market Players | Anheuser-Busch InBev, Molson Coors Beverage Company, Constellation Brands, Inc., Heineken N.V., Carlsberg Group, Asahi Group Holdings, Ltd., Diageo plc, D.G. Yuengling & Son, Inc., The Boston Beer Company, Inc., and Sierra Nevada Brewing Co. |

SEGMENTAL ANALYSIS

By Product Insights

The non-crafted beer segment was the largest by holding 34.4% of the United States beer market share in 2025 due to its extensive distribution networks and ubiquitous availability across all retail channels. Macro brewers have established decades long relationships with wholesalers and retailers, ensuring their products are present in nearly every grocery store, convenience store, and bar in the nation. This widespread accessibility ensures that non-crafted beer remains the default choice for casual drinkers and large social gatherings where consistency and familiarity are prioritized over novelty. The economies of scale achieved by these large producers allow them to maintain competitive pricing, making their products affordable for a broad demographic range. Marketing budgets for major brands are substantial, reinforcing brand recognition and loyalty through high visibility advertising campaigns during major sporting events and holidays. The reliability of supply chains for non-crafted beer ensures that stockouts are rare, further cementing consumer trust. This structural advantage creates a high barrier to entry for smaller competitors, allowing non-crafted beer to maintain its volume leadership despite the growing popularity of artisanal alternatives.

The craft beer segment is likely to register a fastest CAGR of 11.2% from 2026 to 2034 with the consumer desire for flavor diversity and support for local identities. Although volume growth has moderated, the segment continues to expand its influence by offering unique taste profiles that mass produced beers cannot replicate. Consumers are increasingly seeking experimental flavors such as hazy IPAs, sour ales, and pastry stouts, which provide novel sensory experiences. The localization trend encourages drinkers to patronize neighborhood breweries, fostering a sense of community and regional pride. This connection transforms beer consumption into a lifestyle choice rather than merely a transaction. Independent breweries often engage directly with customers through taprooms and festivals, building loyal followings that transcend traditional advertising. The ability of craft breweries to rapidly innovate and release limited edition batches keeps consumers engaged and eager to try new products.

By Distribution Channel Insights

The off-trade channel segment held a significant share in the United States beer market in 2025 with the convenience of purchasing beer for home consumption and enduring shifts in consumer behavior established during recent years. Retailers such as grocery stores, convenience stores, and liquor shops offer extended hours and easy access, allowing consumers to buy beer alongside other household necessities. The habit of drinking at home has persisted post pandemic, supported by the rise of streaming services and home entertainment options that encourage staying in. Consumers appreciate the ability to control their environment and pace of consumption without the pressures of a public setting. The expansion of cold storage sections in supermarkets has improved the visibility and appeal of beer products, facilitating impulse buys. The variety of pack sizes available in off-trade channels, from single cans to multi packs, caters to diverse needs and occasions. Price promotions and loyalty programs in retail settings further incentivize bulk purchases. This channel offers greater privacy and flexibility, appealing to a wide range of demographics.

The on-trade channel segment is expected to witness a fastest CAGR of 9.2% from 2026 to 2034. Bars, restaurants, and breweries have seen a resurgence in foot traffic as people return to socializing outside the home. Consumers value the atmosphere, service, and immediate availability of draft beer, which cannot be replicated at home. The rise of craft brewery taprooms has created destinations where patrons can sample fresh beers directly from the source, fostering community engagement. These venues often host events and live music, enhancing the overall experience and encouraging longer stays. The psychological need for social interaction after periods of isolation has driven demand for communal spaces where beer serves as a social lubricant. Premium draft offerings and exclusive taps attract enthusiasts willing to pay higher prices for unique experiences. The recovery of tourism and business travel also contributes to on-trade growth, as visitors explore local beer scenes.

By Packaging Insights

The cans segment was the largest by holding 54.6% of share in the United States beer market in 2025 due to their superior portability, durability, and recycling efficiency compared to other packaging formats. Aluminum cans are lightweight and shatterproof, making them ideal for outdoor activities such as camping, hiking, and beach trips where glass bottles are prohibited or impractical. As per the Aluminum Association, aluminum cans have a recycling rate of nearly 50% in the United States, which is significantly higher than glass or plastic, appealing to environmentally conscious consumers. This sustainability credential enhances brand image and aligns with corporate responsibility goals. Cans also cool down faster than bottles, improving the immediate drinking experience. The compact shape allows for efficient stacking and transportation, reducing logistics costs and carbon emissions associated with shipping. According to the Can Manufacturers Institute, beer cans account for over 60% of packaged beer sales in the United States, reflecting their dominance in the off-trade sector [[18]. Retailers prefer cans because they occupy less shelf space and are easier to handle. The ability to print high quality graphics on cans provides a vibrant canvas for branding and artistic expression, attracting younger demographics.

The kegs segment is expected register a fastest CAGR of 7.4% during the forecast period with the expansion of taprooms and direct to consumer sales models. Breweries are increasingly selling kegs directly to consumers for home parties and events, bypassing traditional retail channels. The rise of compact kegerators and party pumps has made it easier for households to serve draft beer at home, replicating the bar experience. This trend is particularly strong among craft beer enthusiasts who value freshness and variety. Breweries benefit from higher margins on keg sales compared to packaged products, as they eliminate packaging and labeling costs. The social nature of keg consumption encourages group gatherings and larger volume purchases. Events such as weddings, corporate functions, and festivals rely heavily on kegs for efficient service. The ability to refill growlers and crowlers from kegs also supports sustainable practices by reducing single use packaging waste.

REGIONAL ANALYSIS

United States Beer Market Analysis

The United States beer market is driven by premiumization, craft innovation, and the rise of non-alcoholic alternatives. Consumers are increasingly willing to pay higher prices for high-quality and unique beer experiences, supporting revenue growth despite stable volumes. The expansion of non-alcoholic beer options appeals to health-conscious drinkers, with sales in this category doubling in recent years. Digital transformation and e-commerce integration facilitate direct sales, enhancing customer engagement and loyalty. The recovery of the on-trade sector boosts draft beer consumption, as social dining experiences regain popularity. Regulatory changes in some states allow for broader direct-to-consumer shipping, expanding market reach. Sustainability initiatives resonate with environmentally aware consumers, influencing purchasing decisions. The strong cultural association of beer with sports and social events sustains baseline demand. Innovation in flavors and packaging keeps the market dynamic and engaging.

COMPETITIVE LANDSCAPE

The competition in the United States beer market is intense and characterized by the dominance of large multinational brewers alongside a vibrant and fragmented craft beer sector. Major players leverage economies of scale extensive distribution networks and powerful marketing budgets to maintain their leading positions. Craft breweries compete on uniqueness quality and local community engagement offering diverse flavors that appeal to niche audiences. The rise of alternative beverages such as hard seltzers and ready to drink cocktails has intensified rivalry as companies vie for share of wallet among health conscious consumers. Price competition remains fierce particularly in the economy segment while premiumization drives value growth in higher tiers. Regulatory constraints and the three tier distribution system add complexity to market entry and expansion. Innovation in packaging and sustainability practices serves as a key differentiator for brands seeking to attract environmentally aware shoppers. Digital transformation and direct to consumer models are becoming essential tools for building customer loyalty and bypassing traditional channel limitations. Mergers and acquisitions continue to reshape the landscape as larger entities absorb successful craft labels to broaden their offerings. This dynamic environment requires continuous adaptation and strategic agility to sustain competitiveness and profitability.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Beer Market include

- Anheuser-Busch InBev

- Molson Coors Beverage Company

- Constellation Brands, Inc.

- Heineken N.V.

- Carlsberg Group

- Asahi Group Holdings, Ltd.

- Diageo plc

- D.G. Yuengling & Son, Inc.

- The Boston Beer Company, Inc.

- Sierra Nevada Brewing Co.

Top Players in the US Beer Market

Anheuser Busch InBev SA NV

Anheuser Busch InBev SA NV operates as a global brewing giant with a dominant presence in the United States through its extensive portfolio of domestic and international brands. The company contributes to the global market by leveraging its massive distribution network and supply chain efficiencies to deliver products worldwide. Recent actions include investing heavily in hard seltzer and non alcoholic beer innovations to capture shifting consumer preferences toward healthier options. The firm has also focused on sustainability initiatives such as water conservation and renewable energy adoption in its breweries. These efforts ensure the company remains agile and responsive to evolving market trends while maintaining its leadership position in the competitive beverage alcohol industry.

Molson Coors Beverage Company

Molson Coors Beverage Company is a major player in the United States beer market known for its iconic brands and strong regional presence. The company contributes to the global market by exporting its premium lagers and craft beers to various international destinations. Recent strategies involve expanding its beyond beer portfolio with ready to drink cocktails and functional beverages to diversify revenue streams. Molson Coors has invested in modernizing its brewing facilities to improve operational efficiency and reduce environmental impact. The company actively engages in community programs and sponsorships to build brand loyalty and enhance its corporate image. These initiatives help the company adapt to changing consumption patterns and strengthen its competitive stance in the dynamic US beer landscape.

Constellation Brands Inc

Constellation Brands Inc holds a significant position in the United States beer market primarily through its exclusive rights to import and distribute Modelo and Corona brands. The company contributes to the global market by facilitating the international growth of these Mexican beer icons through strategic marketing and distribution partnerships. Recent actions include expanding production capacity at its US breweries to meet rising demand for imported premium beers. Constellation Brands has also invested in digital transformation projects to enhance supply chain visibility and customer engagement. The company focuses on sustainability goals such as reducing carbon emissions and promoting responsible drinking.

Top Strategies Used by Key Market Participants

Key players in the United States beer market primarily focus on product diversification to address changing consumer preferences for low alcohol and non alcoholic options. Companies invest in innovation within the craft segment to offer unique flavors and local experiences that appeal to discerning drinkers. Another major strategy involves enhancing digital engagement through e commerce platforms and direct to consumer sales channels. Sustainability initiatives such as water stewardship and recyclable packaging are central to building brand reputation and meeting regulatory standards. Strategic acquisitions of emerging brands allow large brewers to expand their portfolios and capture niche markets. These approaches help participants maintain relevance and drive growth in a mature and competitive industry landscape.

MARKET SEGMENTATION

This research report on the United States Beer Market has been segmented and sub-segmented based on the following categories.

By Product

- Non-crafted beer

- Craft beer

By Distribution Channel

- On-trade

- Off-trade

By Packaging

- Bottles

- Cans

- Kegs

By Country

- United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com