U.S Candy Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Chocolate Candy, Non-Chocolate Candy, Others), Ingredient Type, Distribution Channel, And Country (California, Washington, Oregon, New York & Rest of The United States) – Industry Analysis And Forecast, 2026 To 2034

U.S. Candy Market Report Summary

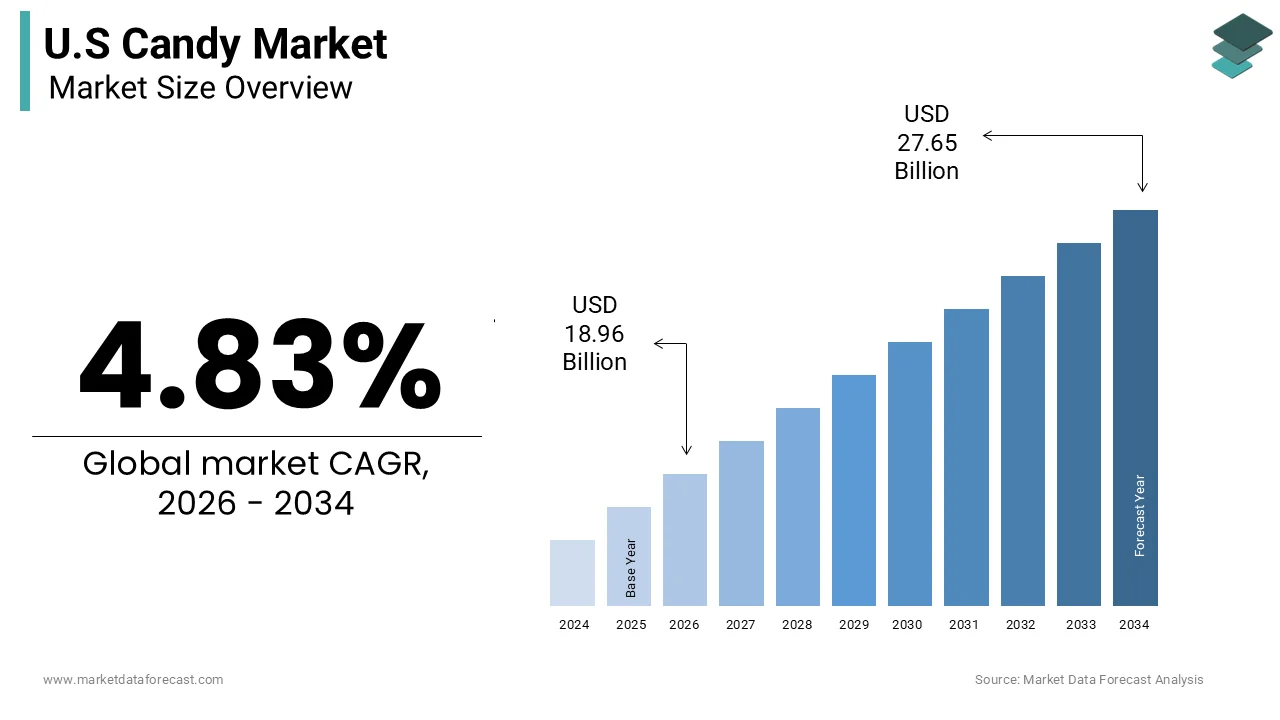

The United States candy market was valued at USD 18.09 billion in 2025 and is projected to reach USD 27.65 billion by 2034, growing from USD 18.96 billion in 2026 at a CAGR of 4.83% during the forecast period. Market growth is driven by strong consumer demand for indulgent snacks, seasonal consumption patterns, and continuous product innovation. The increasing popularity of premium, organic, and low-sugar confectionery products is also shaping the growth of the U.S. candy market.

Key Market Trends

- Rising demand for premium and artisanal confectionery products

- Increasing preference for low-sugar, sugar-free, and functional candies

- Growth in seasonal and festive candy consumption

- Expansion of e-commerce and direct-to-consumer candy sales

- Innovation in flavors, packaging, and healthier alternatives

Segmental Insights

- Based on product type, the chocolate candy segment dominated the U.S. candy market in 2025, driven by strong consumer preference and continuous product innovation

- Based on ingredient type, the sugar-based candies segment held the largest share in 2025 at 58.3%, supported by wide availability and affordability

- Based on distribution channel, the supermarkets and hypermarkets segment led the market in 2025 by capturing 45.3% of the total market share, driven by extensive retail networks and product accessibility

Competitive Landscape

- The U.S. candy market is highly competitive, with major players focusing on brand innovation, healthier product offerings, and expansion of distribution channels. Companies are investing in new flavors, premium ingredients, and sustainable packaging to attract evolving consumer preferences.

- Prominent players in the U.S. candy market include Mars Incorporated, The Hershey Company, Mondelez International, Ferrero Group, Nestlé S.A, Haribo GmbH & Co. KG, Tootsie Roll Industries, Perfetti Van Melle, and Jelly Belly Candy Company.

U.S Candy Market Size

The U.S candy market size was calculated to be USD 18.09 billion in 2025 and is anticipated to be worth USD 27.65 billion by 2034, from USD 18.96 billion in 2026, growing at a CAGR of 4.83% during the forecast period.

The candy is confectionery products, including chocolate gum, hard candy, and non-chocolate sweets. As per the National Confectioners Association, Americans purchase billions of dollars worth of candy annually, with significant volume driven by seasonal events such as Halloween, Easter, and Valentine’s Day. According to the Centers for Disease Control and Prevention, obesity rates remain a public health concern, influencing consumer scrutiny of sugar intake, yet demand for indulgent treats persists. The industry operates within a complex supply chain reliant on cocoa sugar and corn syrup input,s which are subject to global commodity fluctuations. Consumer behavior is increasingly shaped by a desire for premiumization and ethical sourcing, with buyers seeking transparency in ingredient origins.

MARKET DRIVERS

Cultural Entrenchment of Holiday Traditions

The deep-rooted cultural significance of holidays and seasonal celebrations, by creating predictable and substantial spikes in demand, is amplifying the growth of the United States candy market. Events, such as Halloween, Christmas, Easter, and Valentine’s Day, are synonymous with specific confectionery gifts and treats, ensuring consistent annual sales volumes. This tradition drives massive volume sales for chocolate bars, candy corn, and assorted sweets, which are purchased in bulk for distribution to children and guests. The emotional connection between gift-giving and confectionery reinforces the perception of candy as an essential component of social bonding and celebration. Retailers capitalize on these periods by dedicating prominent shelf space and launching limited edition packaging that appeals to collectors and gift givers. The reliability of these seasonal peaks allows manufacturers to plan production schedules and inventory management with greater precision. Furthermore, the expansion of secondary holidays, such as National Candy Day, provides additional opportunities for promotional activities.

Innovation in Premium and Artisanal Segments

The rise of premium and artisanal confectionery products by appealing to consumers seeking higher quality ingredients and unique flavor experiences is another factor escalating the growth of the United States candy market. Buyers are increasingly willing to pay a premium for chocolates made with single-origin cocoa beans, organic sugar,s and natural flavorings that distinguish them from mass-produced alternatives. This trend is fueled by the influence of food media and culinary tourism, which educate consumers about the nuances of cacao processing and bean varieties. The artisanal candy makers report steady growth as customers seek authentic and handcrafted items that reflect craftsmanship and heritage. Small batch producers leverage social media to showcase their production processes and ingredient sourcing, building trust and loyalty among niche audiences. The introduction of exotic flavors, such as sea salt caramel, spicy chili, and fruit infusions, attracts adventurous eaters looking for novel sensory experiences. Additionally, the presentation and packaging of premium candies often elevate them to luxury gift status, further justifying higher price points. This segment benefits from the broader gourmet food movement, where consumers prioritize quality and sustainability.

MARKET RESTRAINTS

Health Consciousness and Sugar Reduction Trends

The increasing health consciousness and the global movement toward sugar reduction by altering consumer purchasing behaviors and limiting consumption frequency are restraining the growth of the United States candy market. Public health campaigns and dietary guidelines have highlighted the risks associated with excessive sugar intake, including obesity, type 2 diabetes, and dental issues, leading many individuals to moderate their sweet consumption. As per the Centers for Disease Control and Prevention, more than 40% of American adults are classified as obese, prompting a societal shift toward healthier lifestyle choices. This awareness has resulted in a decline in per capita consumption of traditional high-sugar candies as consumers opt for fresh fruit yogurt or low-calorie snacks instead. Parents are particularly vigilant about restricting candy intake for children, leading to reduced household purchases of bulk sweets. The stigma surrounding sugar has also impacted the social acceptability of candy as an everyday snack, relegating it to occasional indulgence rather than a daily habit. Manufacturers face pressure to reformulate products with reduced sugar content, which can compromise taste and texture, potentially alienating loyal customers.

Regulatory Pressure and Labeling Requirements

The stringent regulatory pressures and evolving labeling by increasing compliance costs and influencing consumer perception are another factor declining the growth of the United States candy market. Government agencies and consumer advocacy groups are pushing for clearer disclosure of added sugar,s artificial colors, and preservatives on product packaging to inform healthier choices. As per the Food and Drug Administration, updated nutrition facts labels now require manufacturers to explicitly list added sugars, which has led to increased scrutiny of confectionery products by health-conscious buyers. This transparency can deter purchases as consumers become more aware of the high sugar content in standard candy bars and gums. Some local jurisdictions have implemented taxes on sugary beverages and snacks, which could potentially expand to include solid confections, further increasing retail prices. Compliance with these varying state and federal regulations requires significant investment in legal review, packaging redesign, and reformulation efforts. The potential for future bans on certain artificial ingredients, such as titanium dioxide or specific dyes, adds uncertainty to product development pipelines.

MARKET OPPORTUNITIES

Expansion of Plant-Based and Vegan Confections

The growing demand for plant-based and vegan confectionery products by catering to the expanding demographic of flexitarians and ethically conscious consumers is a major factor to enhance new opportunities for the growth of the United States candy market. Traditional candies often contain dairy gelatin and other animal-derived ingredients, which exclude them from vegan diets. As per the Plant-Based Foods Association, sales of plant-based alternatives have surged with consumers seeking cruelty-free and environmentally sustainable options. Manufacturers can capitalize on this trend by reformulating popular classics using coconut milk, almond milk, and pectin instead of gelatin to create creamy textures without animal products. A significant portion of millennials and Gen Z consumers identify as flexitarian, driving demand for inclusive food options. Brands that clearly label their products as vegan and certify them through recognized organizations can build trust and loyalty among this niche but growing audience. The opportunity extends to innovative flavors and textures that mimic traditional dairy chocolates while offering unique plant-based profiles. Social media influencers and wellness advocates often promote vegan treats, amplifying brand visibility and reaching targeted communities.

Development of Functional and Wellness-Oriented Candies

The development of functional and wellness-oriented candies for innovation by merging indulgence with health benefits is also set to gear up the growth of the United States candy market. Consumers are increasingly seeking products that provide additional value, such as stress relief, immune support, or improved sleep quality, alongside their sweet treat. Manufacturers can incorporate ingredients like melatonin CB, D-ashwagandha, or probiotics into gummies and chocolates to create functional confections that address specific well-being needs. These functional candies appeal to adults who want to manage health concerns without consuming pills or capsules, making the experience more enjoyable and accessible. The convenience of portable, discreet formats allows for easy integration into busy lifestyles. Brands can leverage scientific backing and clinical studies to validate claims, enhancing credibility and justifying higher price points. Marketing these products as part of a self-care routine resonates with modern consumers prioritizing mental and physical health.

MARKET CHALLENGES

Volatility in Raw Material Costs and Supply Chain Disruptions

The volatility in raw material costs and supply chain disruption,s by impacting production stability and profit margin,s is one of the challenges for the growth of the United States candy market. Key ingredients such as cocoa, sugar and dairy are subject to global commodity price fluctuations driven by weather conditions, geopolitical tensions, and trade policies. The cocoa prices have experienced historic highs due to crop failures in West Africa, forcing manufacturers to absorb costs or raise prices. These increases squeeze margins for companies that cannot fully pass expenses onto price-sensitive consumers. Supply chain disruptions further complicate procurement with delays in shipping and logistics affecting the timely delivery of ingredients and packaging materials. The reliance on imported cocoa and specialty ingredients exposes manufacturers to currency fluctuations and export restrictions. Smaller companies with less purchasing power struggle to hedge against these risks, making them vulnerable to cost spikes. Additionally, the complexity of sourcing sustainable and ethically certified ingredients adds layers of cost and verification. Manufacturers must balance quality consistency with cost management while navigating an unpredictable global supply environment.

Intense Competition and Private Label Growth

The intense competition and growth of private label brands pose a threat to established players by eroding brand loyalty and pressuring pricing strategies, which will further decline the growth of the United States candy market. Retailers, such as Walmart, Costco, and Trader Joe’,s have expanded their private label confectionery offerings, providing high-quality alternatives at lower price points. The store brands benefit from lower marketing costs and direct shelf placement by allowing them to undercut branded competitors. Shoppers are increasingly willing to switch to private labels for staple items like chocolate bars and gum, where brand differentiation is perceived as minimal. The saturation of the market with numerous brands and flavors creates noise, making it difficult for new launches to gain traction. Additionally, the rise of direct-to-consumer niche brands adds to the competitive landscape, offering unique and artisanal options that appeal to specific demographics. The pressure to compete on both price and quality strains resources and limits profitability. Navigating this crowded environment requires strategic differentiation and strong brand equity to withstand the threat of commoditization.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.83% |

| Segments Covered | By Product Type, Ingredient Type, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Mars Incorporated, The Hershey Company, Mondelez International, Ferrero Group, Nestlé, Tootsie Roll Industries, Haribo, Perfetti Van Melle, Jelly Belly Candy Company, Just Born Quality Confections |

SEGMENTAL ANALYSIS

By Product Type Insights

The chocolate candy segment was the largest by holding a significant share of the United States candy market in 2025, with its deep cultural integration into gift-giving holidays and daily indulgence rituals. Chocolate is perceived not just as a sweet treat but as a symbol of affection and celebration, which sustains high demand year-round. The versatility of chocolate which can be formulated into bars, boxes, truffles, and seasonal shapes to suit various occasions. The emotional connection consumers have with chocolate brands, such as Hershey’s and Godiva, fosters strong loyalty and repeat purchases. Furthermore, the perception of dark chocolate as a healthier option with antioxidant properties has expanded its appeal to health-conscious adults. Retailers prioritize shelf space for chocolate due to its high turnover rates and impulse buy potential at checkout counters.

The non-chocolate candy segment is projected to witness the fastest CAGR of 4.5% during the forecast period, with the rising popularity of gummy sour candies and functional confections. Consumers are increasingly seeking diverse texture experiences and bold flavors that differ from traditional creamy chocolate profiles. The expansion of gummies into the wellness sector, where they are infused with vitamins, CBD, and melatonin, appeals to health-oriented buyers. The lower cost of production for many non-chocolate items allows for competitive pricing and frequent promotional activities that drive volume. Additionally, the rise of vegan animal-based alternatives using pectin instead of gelatin has opened new market segments for ethically conscious shoppers. Brands are launching innovative sour and spicy varieties that cater to adventurous palates, particularly among younger demographics. The portability and shareability of non-chocolate candies also make them ideal for on-the-go consumption.

By Ingredient Type Insights

The sugar-based candies segment was the largest by holding 58.3% of the United States candy market share in 2025 due to the widespread availability of inexpensive sweeteners and the entrenched consumer preference for traditional sweet tastes. Sugar remains the primary ingredient in most conventional candies, providing the necessary structure, texture, and flavor profile that consumers expect. As per the United States Department of Agriculture, the average American consumes over 17 teaspoons of added sugar per day, with a significant portion coming from confectionery products. This high consumption level ensures a steady baseline demand for sugar-based treats despite growing health awareness. The low cost of corn syrup and refined sugar allows manufacturers to maintain affordable price points, which is crucial for mass market appeal. Retailers stock extensive varieties of sugar-based candies because they have long shelf lives and broad demographic appeal across all age groups. The sensory satisfaction provided by sugar triggers dopamine release in the brain, creating a physiological reward loop that encourages repeat purchases. While health trends are emerging, the sheer scale of existing consumption habits and the affordability of sugar-based options keep this segment firmly in the lead.

The sugar-free candies segment is likely to register the fastest CAGR of 6.8% from 2026 to 2034, with the increasing prevalence of diabetes, obesity, and low-carbohydrate diets. Consumers are actively seeking alternatives that allow them to enjoy sweets without spiking blood glucose levels or consuming excess calories. As per the Centers for Disease Control and Prevention, more than 37 million Americans have diabetes, creating a substantial market for diabetic friendly confectionery options. This health imperative drives demand for candies sweetened with stevia, erythritol, and monk fruit, which offer sweetness without the metabolic impact of sugar. Manufacturers are investing in advanced formulation technologies to improve the taste and texture of sugar-free products, addressing previous complaints about aftertastes or gritty textures. The introduction of sugar-free versions of popular brands allows consumers to indulge without guilt, enhancing adoption rates. Additionally, dental health concerns are prompting parents to choose sugar-free options for children to prevent cavities. Retailers are expanding their healthy snack aisles to include these specialized products catering to niche but growing dietary needs.

By Distribution Channel Insights

The supermarkets and hypermarkets segment accounted in holding 45.3% of the United States candy market, owing to their extensive reach, one-stop shopping convenience, and ability to offer bulk purchasing options. These retail giants serve as the primary destination for household grocery shopping, where candy is often purchased alongside other essentials. The wide aisle space and prominent displays during holiday seasons allow retailers to showcase large assortments of candy, attracting impulse buyers and planned purchasers alike. The ability of supermarkets to negotiate favorable terms with manufacturers enables them to offer competitive pricing and promotions that attract budget-conscious consumers. Families prefer buying candy in these venues because they can compare brands and prices easily while completing their weekly shopping trips. The trust associated with established grocery chains also reassures customers about product quality and freshness. Furthermore, the integration of loyalty programs and digital coupons enhances customer retention and encourages repeat purchases.

The online stores segment is deemed to grow at the fastest CAGR of 9.2% from 2026 to 2034, with the convenience of home delivery and access to niche and international products. E-commerce platforms allow consumers to browse extensive catalogs and purchase specialty candies that may not be available in local physical stores. Direct-to-consumer brands leverage social media marketing to reach targeted audiences, offering personalized subscriptions and exclusive flavors that drive engagement. The ability to read reviews and compare ingredients helps health-conscious buyers make informed decisions about sugar-free or organic options. Additionally, the rise of subscription boxes for artisanal and international candies creates recurring revenue streams and introduces consumers to new brands. Fast shipping options and secure packaging ensure that delicate chocolates arrive in perfect condition, enhancing customer satisfaction.

COMPETITION OVERVIEW

The competition in the United States candy market is intense and characterized by a mix of multinational conglomerates and agile niche brands vying for consumer attention. Major players compete on brand recognition, distribution reach, and innovation, while smaller companies differentiate themselves through unique flavors and ethical sourcing practices. The rise of private label brands from major retailers has increased price pressure, forcing national brands to justify premium pricing through quality and exclusivity. Consumer preferences are shifting toward healthier and sustainable options, driving companies to reformulate products and adopt transparent sourcing methods. Seasonal demand spikes during holidays create fierce competition for shelf space and promotional visibility. Digital marketing and social media influence play pivotal roles in shaping trends and driving viral demand for specific items.

KEY MARKET PLAYERS

A few major players of the US candy market include

- Mars Incorporated

- The Hershey Company

- Mondelez International

- Ferrero Group

- Nestlé

- Tootsie Roll Industries

- Haribo

- Perfetti Van Melle

- Jelly Belly Candy Company

- Just Born Quality Confections

Top Strategies Used by Key Market Participants

Key players in the United States candy market prioritize product innovation by developing healthier alternatives, such as sugar-free and plant-based options, to meet evolving consumer demands. Companies focus on sustainability initiatives by sourcing ethical ingredients and using eco-friendly packaging to align with environmental values. Digital transformation is central to their strategy, with investments in e-commerce platforms and personalized marketing campaigns to enhance customer engagement. Strategic partnerships with retailers and influencers help brands expand their reach and drive sales through targeted promotions. Manufacturers leverage data analytics to optimize supply chain efficiency and predict trending flavors. Diversification into adjacent categories such as salty snacks and functional gummies allows firms to capture new revenue streams. These combined approaches enable companies to navigate competitive pressures and sustain growth in a dynamic retail environment.

Leading Players in the Market

- Mars Wrigley Confectionery is a global leader in the confectionery industry with iconic brands such as M&M’s, Snickers, and Skittles. The company leverages extensive distribution networks to ensure widespread availability across retail channels worldwide. Recent actions include investing in sustainable cocoa sourcing initiatives and expanding its portfolio of plant-based confections to meet evolving consumer preferences. Mars Wrigley strengthens its market position through innovative marketing campaigns that engage digital natives and enhance brand loyalty. The firm focuses on product innovation by introducing limited edition flavors and personalized packaging options. These strategic efforts ensure sustained growth and competitiveness in the global candy market while adapting to changing dietary trends and regulatory standards.

- Mondelez International is a prominent global player known for its diverse portfolio of snack and confectionery brands, including Cadbury, Toblerone, and Trident. The company focuses on delivering high-quality products that satisfy consumer cravings while promoting responsible snacking habits. Recent strategies involve expanding its presence in emerging markets and enhancing its e-commerce capabilities to reach broader audiences. Mondelez invests in research and development to create healthier alternatives, such as reduced sugar chocolates and organic ingredients. The firm strengthens its market position through strategic acquisitions and partnerships that broaden its product offerings. These initiatives enable the company to maintain its leadership in the global confectionery sector by balancing tradition with innovation and sustainability.

- The Hershey Company is a dominant force in the North American confectionery market with beloved brands such as Hershey’s, Reese’s, and Jolly Rancher. The company leverages its strong brand equity and extensive retail relationships to maintain a competitive edge. Recent actions include expanding its international footprint and diversifying its portfolio into salty snacks and better-for-you confections. Hershey invests heavily in digital transformation and direct-to-consumer channels to enhance customer experience and loyalty. The firm prioritizes sustainability by committing to responsibly sourced cocoa and reducing its environmental impact. These efforts ensure continued growth and relevance in the global candy market while addressing modern health and ethical concerns.

MARKET SEGMENTATION

This research report on the US candy market has been segmented and sub-segmented based on product type, ingredient type, distribution channel & region.

By Product Type

- Chocolate Candy

- Non-Chocolate Candy

- Others

By Ingredient Type

- Sugar-Based Candies

- Sugar-Free Candies

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What are the key factors driving the candy market in the United States?

Key drivers include increasing demand for indulgent snacks, seasonal consumption (Halloween, Christmas), and strong brand presence.

2. What challenges are faced by the US candy industry?

Major challenges include rising health concerns, sugar regulations, fluctuating raw material costs, and increasing competition from healthier snack alternatives.

3. What are the most popular types of candy in the US?

Chocolate candy dominates the market, followed by gummies, hard candies, and chewy candies.

4. What ingredients are commonly used in candy production?

Common ingredients include sugar, cocoa, milk, corn syrup, flavorings, and food colorings.

5. Who are the key players in the United States candy market?

Leading companies include Mars Incorporated, The Hershey Company, Mondelez International, and Ferrero Group.

6. What role does seasonal demand play in candy sales?

Seasonal demand plays a crucial role, with significant spikes during holidays such as Halloween, Easter, and Christmas.

7. What trends are shaping the US candy market?

Trends include premiumization, organic and low-sugar options, functional ingredients, and unique flavor combinations.

8. How is health consciousness affecting candy consumption?

Consumers are increasingly seeking low-sugar, sugar-free, and natural ingredient-based candies, influencing product development.

9. Which distribution channels dominate the US candy market?

Supermarkets, convenience stores, and online platforms are the dominant distribution channels.

10. How is packaging influencing consumer buying behavior in the US candy market?

Attractive, convenient, and eco-friendly packaging plays a significant role in attracting consumers and influencing purchase decisions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com