United States Cocoa Market Size, Share, Trends & Growth Forecast Report Segmented By Application (Confectionery, Food & Beverages, Cosmetics, Pharmaceutical), Product Type and Country – Industry Analysis From 2026 to 2034

U.S. Cocoa Market Report Summary

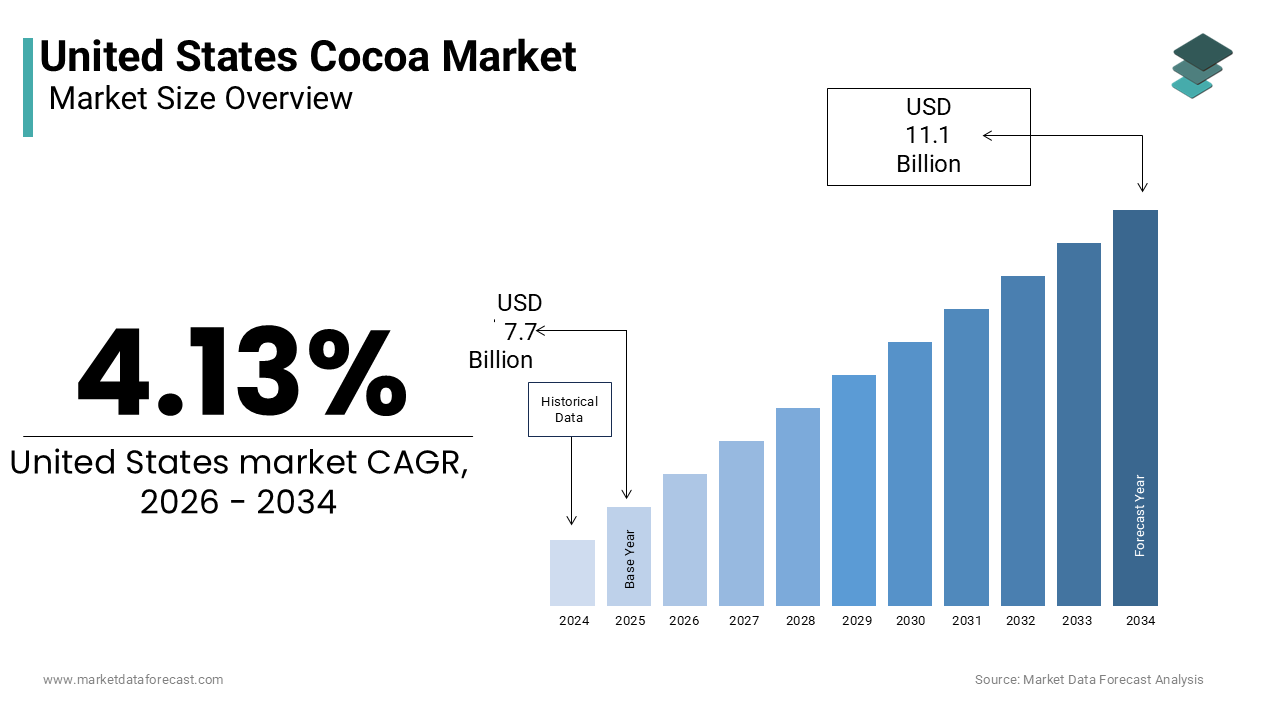

The U.S. cocoa market was valued at USD 7.7 billion in 2025, is estimated to reach USD 8.0 billion in 2026, and is projected to reach USD 11.1 billion by 2034, growing at a CAGR of 4.13% during the forecast period from 2026 to 2034. The growth of the U.S. cocoa market is driven by strong demand from the confectionery sector, rising consumer preference for premium and dark chocolate, and increasing focus on ethical sourcing. The market benefits from advanced domestic processing capabilities and a well-established chocolate industry, despite heavy reliance on imported cocoa beans. Additionally, the expansion of functional cocoa-based products and premium artisanal chocolate segments is further supporting market growth.

Key Market Trends

- Rising demand for dark chocolate driven by health awareness and antioxidant benefits

- Growing popularity of premium and artisanal chocolate products with unique flavors and origins

- Increasing focus on sustainable and ethically sourced cocoa among consumers

- Expansion of functional foods and cocoa-based beverages targeting health-conscious consumers

- Adoption of traceability and transparency technologies in cocoa sourcing

Segmental Insights

- Based on application, the confectionery segment was the largest and held a significant share of the U.S. cocoa market in 2025. The segment’s dominance is attributed to the strong cultural consumption of chocolate during festivals, seasonal demand, and continuous product innovation.

- Based on product type, the chocolate segment accounted for the largest share of the U.S. cocoa market in 2025. This is driven by high consumer preference for ready-to-eat chocolate products, wide availability, and strong brand presence across retail channels.

Regional Insights

- The United States dominates the North American cocoa market and remains one of the largest global consumers and importers of cocoa beans. The market is supported by high per capita chocolate consumption, strong purchasing power, and a well-developed food processing industry.

- The country continues to lead due to premiumization trends, increasing demand for ethically sourced cocoa, and innovation in cocoa-based products, making it a key influencer in global cocoa trade dynamics.

Competitive Landscape

The U.S. cocoa market is characterized by intense competition among multinational corporations and emerging artisanal brands. Leading companies focus on sustainable sourcing, premium product offerings, and supply chain integration to maintain market position. Innovation, transparency, and ethical practices are becoming key differentiators in the competitive landscape. Prominent players in the U.S. cocoa market include The Hershey Company, Mars, Incorporated, Mondelez International, Inc., Nestlé S.A., Barry Callebaut AG, Cargill, Incorporated, Olam International Limited, Blommer Chocolate Company, ECOM Agroindustrial Corp. Limited, and Guan Chong Berhad.

U.S. Cocoa Market Size

The U.S. cocoa market size was valued at USD 7.7 billion in 2025 and is anticipated to reach USD 8.0 billion in 2026 from USD 11.1 billion by 2034, growing at a CAGR of 4.13% during the forecast period from 2026 to 2034.

The U.S. cocoa market functions as a critical downstream segment of the global confectionery industry, characterized by its heavy reliance on imported raw materials and sophisticated domestic processing capabilities. This market encompasses the importation, grinding, and manufacturing of cocoa beans into intermediate products such as cocoa liquor, butter, and powder, which subsequently feed into the vast American chocolate and beverage sectors. According to the U.S. Department of Agriculture, the U.S. chocolate confectionery market was estimated to be worth 24 billion U.S. dollars in 2025. The nation stands as one of the largest consumers of cocoa globally, and according to the International Cocoa Organization, per capita chocolate consumption reached approximately 5.5 kilograms annually. Domestic processing facilities handle significant volumes of these imports, and according to market data, the U.S. cocoa processing market is projected to grow from 4.28 billion U.S. dollars in 2024 to 5.55 billion U.S. dollars by 2033. The supply chain is predominantly fueled by imports from West African nations, although recent volatility has prompted diversification efforts. According to the U.S. Census Bureau, in the last twelve months leading up to mid-2025, the U.S. imported cocoa beans valued at approximately 2.66 billion U.S. dollars. This ecosystem is not merely about volume but also about value addition, as American manufacturers increasingly focus on premiumization and ethical sourcing to meet evolving consumer expectations. The market dynamics are thus defined by the interplay between steady domestic demand, fluctuating global supply conditions, and the strategic initiatives of major processors to secure sustainable supply lines.

MARKET DRIVERS

Rising Consumer Preference for Dark Chocolate and Health Consciousness

The escalating demand for dark chocolate is majorly fuelling the growth of the U.S. cocoa market. Consumers are increasingly associating cocoa with health benefits, particularly due to its high antioxidant content and lower sugar levels compared to milk chocolate variants. According to industry analysis, the dark chocolate market is projected to reach a valuation of 52.3 billion U.S. dollars in 2025 and is expected to expand to 86.2 billion U.S. dollars by 2032. This shift is driven by a growing awareness of nutritional content, with individuals seeking stress-relieving properties and cardiovascular benefits linked to flavonoid-rich cocoa. According to Google Trends, search interest for dark chocolate reached its highest point of 85 in February 2026. Manufacturers are responding by increasing the cocoa solid content in their offerings, which directly boosts the demand for high-quality cocoa beans and processing services. The premiumization trend further amplifies this effect, as consumers are willing to pay more for artisanal and single-origin dark chocolate products that promise superior taste and ethical provenance. This health-oriented demand insulates the cocoa market to some extent from broader confectionery declines, as dark chocolate is often perceived as a functional food rather than merely an indulgence. Consequently, processors are investing in technologies that preserve the nutritional integrity of cocoa during manufacturing, ensuring that the final products meet the rigorous standards of health-conscious Americans.

Expansion of Premium and Artisanal Chocolate Segments

The proliferation of premium and artisanal chocolate brands is another significant driver of the U.S. cocoa market. American consumers are demonstrating a marked preference for unique flavor profiles, ethical sourcing stories, and high-quality ingredients, which necessitates the use of superior cocoa beans. According to industry reports, the U.S. premium chocolate market generated a revenue of 8.62 billion U.S. dollars in 2024 and is expected to reach 9.95 billion U.S. dollars by 2029. This segment growth outpaces the mass market, encouraging manufacturers to source distinct cocoa varieties such as Criollo and Trinitario, which offer complex flavor notes but require careful handling and processing. The rise of craft chocolate makers has democratized access to these premium beans, creating a diverse demand landscape that extends beyond the traditional bulk commodity market. These artisanal producers often emphasize direct trade relationships, which can provide more stable income for farmers and ensure higher quality control for the end product. According to market observations, the increased demand for premium chocolates is a key factor driving the overall market growth. This trend compels large-scale processors to adapt by offering specialized grinding and refining services that cater to small-batch producers. Furthermore, the emphasis on transparency and origin storytelling in the premium segment reinforces the value of cocoa as a differentiated agricultural product, thereby supporting higher price points and sustaining market vitality even during periods of global supply tightness.

MARKET RESTRAINTS

Volatility in Global Cocoa Prices and Supply Chain Instability

Extreme volatility in global cocoa prices is a key restraint for the U.S. cocoa market, which is creating uncertainty for manufacturers and retailers alike. The market experienced unprecedented price fluctuations between 2024 and 2026, and according to the Intercontinental Exchange, prices peaked at over 12,000 U.S. dollars per metric ton before undergoing sharp corrections. Such instability complicates long-term planning and cost management for American chocolate producers, who often operate on thin margins in the mass market segment. According to recent analysis, cocoa prices remain highly volatile due to supply challenges, climate impact, and rising demand. This volatility forces companies to engage in frequent hedging activities or pass costs onto consumers, which can dampen demand if retail prices become prohibitive. The unpredictability of input costs discourages investment in new product development and expansion, as firms prioritize financial resilience over growth. According to historical pricing data, cocoa prices declined from 12,906 U.S. dollars per metric ton in late 2024 to lower levels in early 2026. Manufacturers may find themselves holding expensive inventory that loses value rapidly, or conversely, facing shortages when prices spike unexpectedly. This financial risk is particularly acute for smaller players who lack the capital reserves to absorb sudden cost increases. The resulting caution in procurement and production scheduling can lead to inefficiencies and reduced market responsiveness, ultimately restraining the overall growth potential of the U.S. cocoa sector in an increasingly unpredictable global environment.

Dependence on Geographically Concentrated Supply Sources

The heavy reliance on a geographically concentrated supply base, primarily West Africa is further hampering the cocoa market expansion in the U.S. According to the International Cocoa Organization, approximately 70% of the world's cocoa is grown in West and Central Africa. Political instability, infrastructure deficits, and disease outbreaks in countries like Côte d'Ivoire and Ghana can have immediate and severe repercussions for American importers. According to data from the International Labour Organization, more than 1.5 million children work on cocoa farms in Côte d'Ivoire and Ghana. This concentration means that any adverse weather event or policy change in these key producing nations can trigger supply shortages and price spikes in the U.S.. According to agricultural forecasts, a potential 10% decline in cocoa output in West Africa for the 2025/26 season has already introduced volatility into the market. The lack of diversification in sourcing limits the ability of US manufacturers to mitigate these risks through alternative supply lines. While some efforts are being made to source from Latin America and Asia, these regions currently lack the scale to replace West African volumes. This dependency creates a structural vulnerability that constrains the market's stability and growth. Furthermore, the logistical challenges associated with transporting beans from distant origins add to the cost and complexity of the supply chain, further restraining the efficiency and profitability of the U.S. cocoa market.

MARKET OPPORTUNITIES

Growing Demand for Sustainable and Ethically Sourced Cocoa

The increasing consumer demand for sustainable and ethically sourced cocoa presents a significant opportunity for the U.S. cocoa market to differentiate and add value. American shoppers are becoming more conscientious about the environmental and social impacts of their purchases, driving brands to adopt certified sourcing practices. According to industry reports, the U.S. organic cocoa market was valued at 1.38 billion U.S. dollars in 2025 and is projected to reach 2 billion U.S. dollars by 2035. This trend allows manufacturers to command premium prices and build brand loyalty among environmentally aware consumers. Companies that invest in certifications such as Fair Trade, Rainforest Alliance, or Organic can tap into this expanding niche, which is less sensitive to price fluctuations. According to sustainable trade data, leading brands are emphasizing ethical sourcing and innovative sustainability initiatives to meet consumer expectations. This shift encourages collaboration between US processors and farmers to improve agricultural practices, reduce deforestation, and ensure fair labor conditions. By integrating sustainability into their core business strategies, companies can mitigate regulatory risks and enhance their corporate image. Moreover, the transparency enabled by blockchain and other technologies allows consumers to trace the origin of their cocoa, further reinforcing trust and demand.

Innovation in Cocoa Based Functional Foods and Beverages

The expansion of cocoa applications beyond traditional confectionery into functional foods and beverages offers a substantial opportunity for market growth. Consumers are seeking versatile ingredients that provide both taste and health benefits, leading to the incorporation of cocoa in snacks, breakfast cereals, and ready-to-drink beverages. According to trade forecasts, the cocoa beans market is expected to grow by 3.58 billion U.S. dollars from 2025 to 2029. This diversification reduces dependence on seasonal candy sales and creates year-round demand for cocoa ingredients. Manufacturers are innovating with formats such as cocoa-infused protein bars, energy drinks, and plant-based milk alternatives, appealing to health-focused and active lifestyles. The versatility of cocoa powder and butter allows for seamless integration into these new product categories, expanding the total addressable market. Furthermore, the perception of cocoa as a natural energy booster and mood enhancer supports its inclusion in functional formulations. According to consumer sentiment surveys, the usage of chocolates as gifts and in various culinary applications continues to rise. This innovation drive encourages research and development investments, leading to novel textures and flavors that attract new consumer segments. By leveraging the functional properties of cocoa, the U.S. market can unlock new revenue streams and reduce vulnerability to shifts in traditional confectionery preferences.

MARKET CHALLENGES

Regulatory Pressures Regarding Labor Practices and Deforestation

Navigating complex regulatory landscapes concerning labor practices and deforestation poses a major challenge for the U.S. cocoa market. Governments and international bodies are implementing stricter standards to combat child labor and environmental degradation in cocoa-producing regions. According to the U.S. Department of Labor, the persistence of child labor in cocoa supply chains remains a critical human rights challenge that requires ongoing attention. US companies face increasing pressure to ensure their supply chains are free from such practices, necessitating rigorous auditing and monitoring systems. Failure to comply can result in legal penalties, import bans, and severe reputational damage. Additionally, emerging regulations in Europe and potentially the U.S. regarding deforestation-free supply chains add another layer of complexity. Manufacturers must verify that their cocoa sources do not contribute to forest loss, which requires detailed traceability and data collection. This compliance burden increases operational costs and requires significant investment in supply chain transparency technologies. The challenge is compounded by the fragmented nature of cocoa farming, where millions of smallholders make monitoring difficult. According to human rights monitoring reports, meaningful gaps remain in managing these challenges despite strong efforts from major brands. Companies must balance these regulatory requirements with the need to maintain affordable product prices.

Impact of Climate Change on Long Term Supply Security

The accelerating impact of climate change on cocoa cultivation presents a formidable challenge to the long-term security of the U.S. cocoa market. Rising temperatures, changing rainfall patterns, and increased frequency of extreme weather events are threatening cocoa yields in key producing regions. According to the International Center for Tropical Agriculture, climate change could reduce cocoa-suitable areas in West and Central Africa by 50% by 2050. This potential decline in arable land necessitates urgent adaptation strategies, such as the development of drought-resistant cocoa varieties and improved agricultural practices. However, these solutions require significant time and investment, creating a gap between current demand and future supply capabilities. The U.S. market, being heavily dependent on imports, is directly exposed to these climatic risks. Yield reductions lead to higher prices and potential shortages, disrupting production schedules and affecting profitability. According to environmental impact assessments, climate change has already impacted cocoa yields heavily in recent years. Manufacturers must engage in long-term planning and support farmer resilience initiatives to mitigate these risks. The challenge is not just environmental but also economic, as the cost of adaptation may be passed down the supply chain. Ensuring a stable supply of cocoa in the face of climate change requires collaborative efforts across the entire value chain, from farmers to processors to retailers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.13% |

| Segments Covered | By Application, Product Type and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Key Market Players | Hershey Company, Mars, Incorporated, Mondelez International, Inc., Nestlé S.A., Barry Callebaut AG, Cargill, Incorporated, Olam International Limited, Blommer Chocolate Company, ECOM Agroindustrial Corp. Limited, and Guan Chong Berhad. |

SEGMENTAL ANALYSIS

By Application Insights

The confectionery segment dominated the market by commanding for the highest share of the U.S. cocoa market in 2025. The growth of the confectionery segment in the U.S. market is driven by the entrenched cultural habit of chocolate consumption during major holidays and social occasions. According to the National Confectioners Association, Americans spend approximately 2.6 billion U.S. dollars on Halloween candy alone each year. This seasonal surge creates a consistent baseline demand that supports large-scale processing and import activities throughout the year. Additionally, according to retail reports, Valentine’s Day sees consumers purchasing over 58 million pounds of chocolate. The sheer volume of these events ensures that confectionery remains the primary outlet for cocoa butter and liquor. Manufacturers leverage this predictability to optimize production schedules and inventory levels, ensuring that supply meets the intense but predictable spikes in demand. The dominance is also reinforced by the widespread availability of chocolate products in retail outlets across the nation, from convenience stores to large supermarkets. According to industry trends, the constant innovation in chocolate formats keeps consumer interest high and drives repeat purchases. This segment’s leadership is not merely a function of volume but also of revenue generation, as premium confectionery items contribute disproportionately to market value. The resilience of this segment against economic downturns ensures that even during periods of financial uncertainty, consumers continue to purchase small indulgences like chocolate.

On the other end, the food and beverages segment is estimated to record the highest CAGR in the U.S. cocoa market during the forecast period owing to the rising popularity of cocoa-infused functional beverages. Consumers are seeking healthier alternatives to sugary sodas and energy drinks, turning to cocoa-based options that offer natural caffeine and antioxidant benefits. According to market data, the global hot chocolate market is expected to grow at a compound annual growth rate of 5.2% from 2024 to 2030. In the U.S., ready-to-drink chocolate milk and premium hot cocoa mixes are gaining traction in cafes and retail stores alike. According to industry reports, the integration of cocoa into protein shakes and meal replacement beverages is expanding its utility beyond traditional dessert applications. This versatility allows manufacturers to target health-conscious individuals who value the nutritional profile of cocoa, including its magnesium and iron content. The growth is further supported by the development of plant-based cocoa beverages, such as almond and oat milk chocolates, which cater to the growing vegan and lactose-intolerant populations. These innovations are driving higher consumption rates and encouraging frequent purchase behavior. Moreover, the perception of cocoa as a mood enhancer and stress reliever makes it an attractive ingredient in wellness-focused beverages. As consumers become more educated about the health benefits of flavonoids, the demand for cocoa-enriched drinks continues to rise.

By Product Type Insights

The chocolate segment led the market with the highest share of the U.S. cocoa market in 2025. The overwhelming consumer preference for ready-to-eat chocolate products over raw or intermediate ingredients is propelling the dominance of chocolate segment in the U.S. market. Most cocoa imported into the U.S. is processed into chocolate bars, candies, and other confectionery items that are directly consumed by end users. According to the National Confectioners Association, the U.S. chocolate confectionery market was valued at 24 billion U.S. dollars in 2025. This dominance is fueled by the convenience and immediate gratification offered by finished chocolate products, which require no further preparation by the consumer. Major manufacturers invest heavily in branding and marketing to maintain strong shelf presence and consumer loyalty. According to retail data, chocolate accounts for the largest share of impulse purchases in convenience stores and checkout aisles. The segment’s leadership is also supported by the wide variety of chocolate products available, ranging from mass-market bars to premium artisanal offerings. This diversity ensures that there is a chocolate product for every consumer preference and price point. Furthermore, the emotional connection many Americans have with chocolate as a comfort food or gift item reinforces its central position in the market. The continuous innovation in flavors, textures, and formats keeps the segment dynamic and engaging. According to agricultural trade reports, the steady demand for chocolate products provides a stable foundation for the entire cocoa supply chain.

However, the cocoa powder and cake segment is on the rise and is predicted to grow at the fastest CAGR in the U.S. market during the forecast period owing to the sustained surge in home baking and culinary exploration among consumers. The pandemic-induced shift towards home cooking has evolved into a lasting hobby for many Americans, who continue to experiment with baking recipes that require high-quality cocoa powder. According to the U.S. Department of Commerce, sales of baking ingredients have remained elevated compared to pre-pandemic levels. Home bakers are increasingly seeking premium and specialized cocoa products, such as Dutch-processed and single-origin powders, to achieve professional results in their kitchens. This trend is supported by the proliferation of online baking tutorials and social media content that inspire consumers to try new recipes. The versatility of cocoa powder allows it to be used in a wide range of applications, from cakes and cookies to savory dishes and beverages. According to culinary surveys, the use of cocoa in healthy baking is also contributing to its growth. Consumers are more informed about the differences between natural and alkalized cocoa, leading to more discerning purchasing decisions. This increased sophistication drives demand for higher-value cocoa powder products. Furthermore, the availability of organic and fair-trade cocoa powders appeals to ethically conscious consumers who want to align their baking practices with their values. The combination of heightened interest in home baking, greater product knowledge, and ethical considerations is fueling the rapid expansion of the cocoa powder and cake segment.

REGIONAL ANALYSIS

United States Cocoa Market Analysis

The U.S. is likely to maintain its position as the dominant force in the North American cocoa market for the next few years as premiumization and health-oriented consumption trends continue to evolve. As the second-largest importer of cocoa beans globally, according to the International Cocoa Organization, the nation plays a pivotal role in shaping global trade dynamics and pricing mechanisms. The market status is characterized by a mature yet evolving landscape, where traditional mass-market consumption coexists with a rapidly growing premium and ethical segment. The U.S. cocoa processing industry is highly consolidated, with a few major players controlling significant capacity, which allows for efficient scaling and investment in sustainability initiatives. According to the U.S. Census Bureau, the U.S. imported cocoa beans valued at approximately 2.66 billion U.S. dollars in the last twelve months. This high level of importation reflects the limited domestic cultivation of cocoa due to climatic constraints, necessitating a robust logistics and distribution infrastructure. The market is also distinguished by its high regulatory standards regarding food safety and labor practices, which influence sourcing decisions and supply chain management. Companies operating in the U.S. must navigate complex compliance requirements, driving them to adopt transparent and accountable sourcing models. The presence of leading global chocolate manufacturers and innovative craft brands creates a competitive environment that fosters product development and quality improvement. According to industry reports, the U.S. market serves as a trendsetter for other regions. This leadership position is reinforced by the high disposable income of American consumers, who are willing to pay for higher quality and ethically produced cocoa products. The U.S. continues to invest in research and development to improve processing efficiencies and product formulations, ensuring its continued relevance and competitiveness in the global cocoa industry.

COMPETITIVE LANDSCAPE

The competition in the U.S. cocoa market is characterized by intense rivalry among established multinational corporations and emerging artisanal brands vying for consumer attention. Major players leverage economies of scale and extensive distribution networks to maintain dominance in the mass market segment while simultaneously investing in premium offerings to counter niche competitors. The barrier to entry remains high due to significant capital requirements for processing facilities and complex supply chain management needs. However, the rise of craft chocolate makers has disrupted traditional dynamics by emphasizing transparency and direct trade relationships with farmers. These smaller entities appeal to ethically conscious consumers who value storytelling and unique flavor profiles over brand recognition. Incumbent firms respond by acquiring specialty brands or launching their own premium lines to retain market relevance. Price volatility adds another layer of complexity forcing companies to balance cost management with quality assurance. Regulatory pressures regarding labor practices and environmental sustainability further intensify competition as firms strive to demonstrate compliance and corporate responsibility. Innovation in product development and marketing becomes crucial for differentiation in a saturated landscape. Collaborative efforts towards industry wide sustainability goals also shape competitive interactions as companies seek to secure long term supply stability. This dynamic environment requires continuous adaptation and strategic foresight to maintain competitive advantage in the evolving U.S. cocoa sector.

KEY MARKET PLAYERS

A few of the major companies in the US Cocoa Market include

- The Hershey Company

- Mars, Incorporated

- Mondelez International, Inc.

- Nestlé S.A.

- Barry Callebaut AG

- Cargill, Incorporated

- Olam International Limited

- Blommer Chocolate Company

- ECOM Agroindustrial Corp. Limited

- Guan Chong Berhad

Top Players in the US Cocoa Market

The Hershey Company

The Hershey Company stands as a dominant force in the U.S. cocoa market with extensive global influence through its vast distribution networks. This corporation focuses heavily on sustainable sourcing initiatives to secure long term supply chains for its diverse product portfolio. Recent actions include significant investments in cocoa farming communities in West Africa to improve yield and farmer livelihoods. The company actively engages in research and development to create innovative chocolate formats that appeal to health conscious consumers. By launching premium artisanal lines and expanding its presence in the snacking category, Hershey strengthens its brand loyalty. Their commitment to ethical sourcing enhances corporate reputation while ensuring consistent quality. These strategic moves allow the company to maintain robust production capabilities and meet evolving consumer demands for transparency and quality in cocoa based products across international markets.

Cargill Incorporated

Cargill Incorporated operates as a critical global processor of cocoa beans providing essential ingredients to manufacturers worldwide. This multinational corporation leverages its extensive supply chain expertise to ensure steady availability of cocoa butter powder and liquor. Recent efforts focus on digital traceability systems that enhance transparency from farm to factory. Cargill invests heavily in sustainability programs aimed at eliminating deforestation and improving farmer incomes in key producing regions. The company expands its processing capacity in strategic locations to optimize logistics and reduce costs. By offering customized cocoa solutions and technical support to clients, Cargill strengthens its position as a preferred partner for major food brands. Their innovation in sustainable packaging and ingredient formulation addresses growing environmental concerns. These actions reinforce their leadership in responsible sourcing and operational efficiency within the complex global cocoa industry landscape.

Barry Callebaut AG

Barry Callebaut AG serves as a leading global manufacturer of high quality chocolate and cocoa products for professional and industrial clients. The company distinguishes itself through superior craftsmanship and innovation in flavor development tailored to diverse regional preferences. Recent strategies involve expanding production facilities in the Americas to closer serve North American customers and reduce lead times. Barry Callebaut prioritizes sustainable cocoa sourcing through its Forever Chocolate initiative which aims to make sustainable chocolate the industry norm. They collaborate closely with chefs and product developers to create unique culinary experiences using premium cocoa ingredients. The company also invests in advanced processing technologies to enhance product consistency and quality. By focusing on business to business relationships and offering comprehensive technical services, Barry Callebaut strengthens its market position. Their dedication to sustainability and innovation ensures they remain a trusted partner for brands seeking high end cocoa solutions globally.

Top Strategies Used by Key Market Participants

Key players in the U.S. cocoa market primarily employ vertical integration strategies to secure stable supplies of raw materials amidst global volatility. Companies invest directly in farming communities to improve agricultural practices and ensure ethical sourcing standards are met throughout the supply chain. Another major strategy involves product premiumization where manufacturers launch artisanal and single origin chocolate lines to capture higher value segments. This approach appeals to discerning consumers who prioritize quality and transparency over price. Sustainability initiatives form a core strategic pillar as firms commit to zero deforestation goals and carbon neutral operations to mitigate regulatory risks. Digital transformation is also prevalent with companies adopting blockchain technology for enhanced traceability and consumer trust. Innovation in product formats such as functional beverages and healthy snacks diversifies revenue streams beyond traditional confectionery. These combined strategies enable participants to build resilience against supply shocks while meeting evolving consumer expectations for responsibility and quality in their cocoa purchases.

MARKET SEGMENTATION

This research report on the US Cocoa Market has been segmented based on the following categories.

By Application

- Confectionery

- Food & Beverages

- Cosmetics

- Pharmaceutical

By Product Type

- Cocoa Beans

- Cocoa Powder & Cake

- Cocoa Butter

- Chocola

By Country

- United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com