United States Drone Market Size, Share, Trends & Growth Forecast Report Segmented By Component (Hardware, Software, Services), Technology, Power Source, End Use, And Country - Industry Analysis From 2026 To 2034

United States Drone Market Report Summary

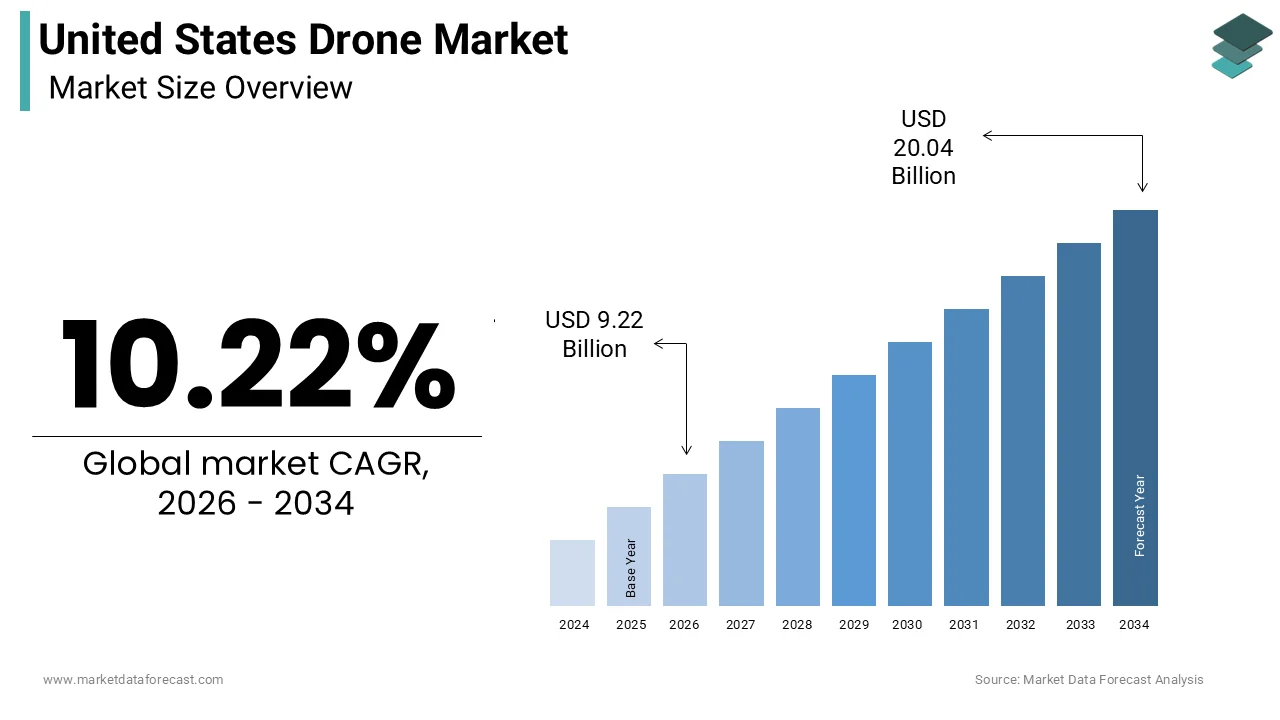

The United States drone market was valued at USD 8.35 billion in 2025 and is projected to reach USD 20.04 billion by 2034, growing from USD 9.20 billion in 2026 at a CAGR of 10.22% during the forecast period. Market growth is driven by increasing adoption across commercial, defense, and industrial applications. Drones are widely used for surveillance, mapping, agriculture, logistics, and infrastructure inspection. Advancements in AI, automation, and sensor technologies are further accelerating the growth of the U.S. drone market.

Key Market Trends

- Rising adoption of drones in commercial sectors such as logistics and agriculture

- Increasing use of drones for surveillance and defense applications

- Growth in autonomous and AI-enabled drone technologies

- Expansion of drone delivery and last-mile logistics solutions

- Increasing demand for high-resolution imaging and data analytics

Segmental Insights

- Based on component, the hardware segment dominated the U.S. drone market in 2025, driven by demand for airframes, sensors, and propulsion systems

- Based on technology, the remotely operated drones segment held a significant share in 2025, supported by widespread use in defense and commercial operations

- Based on power source, the battery-powered drones segment led the market in 2025 by capturing 56.4% of the total market share, driven by environmental regulations and quieter operations

- Based on end use, the commercial segment accounted for a notable share in 2025 at 26.4%, supported by increasing adoption in industries such as agriculture, construction, and logistics

Competitive Landscape

- The U.S. drone market is highly competitive, with major players focusing on innovation, autonomy, and advanced sensing technologies. Companies are investing in AI-powered drones, enhanced flight capabilities, and integration with cloud-based platforms to strengthen their market presence.

- Prominent players in the U.S. drone market include DJI, AeroVironment, Lockheed Martin, Northrop Grumman, Boeing, General Atomics, Parrot, Skydio, Teledyne FLIR, and Elbit Systems.

United States Drone Market Size

The United States drone market size was calculated to be USD 8.35 billion in 2025 and is anticipated to be worth USD 20.04 billion by 2034, from USD 9.20 billion in 2026, growing at a CAGR of 10.22% during the forecast period.

The drone is an unmanned aerial system utilized for commercial, industrial, recreational, and defense applications. This sector has evolved from a niche hobbyist interest into a component of modern infrastructure inspection, agriculture, and public safety operations. As per the Federal Aviation Administration, there are more than 867000 registered drones in the United States, reflecting widespread adoption across various sectors. The regulatory framework continues to adapt with the implementation of remote identification rules, ensuring accountability and safety in the national airspace. Commercial operators leverage drone technology for tasks such as pipeline monitoring, crop health assessment, and construction site surveying, which significantly reduce operational costs and enhance data accuracy. The integration of artificial intelligence and machine learning algorithms enables autonomous flight capabilities and real-time data processing. Educational institutions are increasingly incorporating drone programming into STEM curricula, fostering a skilled workforce for future innovation. Public safety agencies utilize drones for search and rescue missions, disaster response, and traffic management, improving emergency response times. The technological landscape is characterized by rapid advancements in battery life, sensor precision, and connectivity standards. Consumer demand remains robust for high-resolution imaging and extended flight durations. The market dynamics are influenced by federal initiatives promoting domestic manufacturing and supply chain security.

MARKET DRIVERS

Expansion of Commercial Applications in Infrastructure and Agriculture

The proliferation of commercial drone applications in infrastructure inspection and precision agriculture is propelling the growth of the United States drone market. Industries are increasingly adopting unmanned aerial systems to enhance operational efficiency, reduce human risk, and lower maintenance costs. The integration of drones into routine industrial workflows has resulted in significant cost savings for energy and utility companies. Inspections of power lines, wind turbines, and bridges that previously required dangerous manual labor or expensive helicopter rentals can now be conducted safely and rapidly using high-resolution cameras and thermal sensors. In the agricultural sector, farmers utilize multispectral imaging to monitor crop health, optimize irrigation, and detect pest infestations early. The United States Department of Agriculture notes that precision agriculture technologies, including drones, contribute to improved yield predictions and resource management. The ability to collect actionable data in real time allows businesses to make informed decisions quickly. Regulatory approvals for beyond visual line of sight operations have further expanded the scope of these applications, enabling larger area coverage.

Advancements in Autonomous Technology and Artificial Intelligence

The rapid advancements in autonomous navigation and artificial intelligence capabilities are significantly driving the United States drone market growth. Modern drones are equipped with sophisticated sensors and processing units that enable obstacle avoidance, path planning, and automated data analysis without constant pilot input. According to research from the National Aeronautics and Space Administration, advances in sense and avoid technologies are crucial for integrating drones into shared airspace safely. These technological improvements reduce the skill barrier for operators, allowing professionals in various fields to utilize drones effectively without extensive training. Machine learning algorithms enable drones to identify anomalies in infrastructure or classify crop types automatically, increasing the value of collected data. The development of swarm technology allows multiple drones to operate collaboratively for large-scale mapping and surveillance tasks. This level of automation increases productivity and enables complex missions that were previously impractical. The integration of 5G connectivity facilitates low-latency communication essential for real-time control and data transmission. As computational power increases and costs decrease, these advanced features become accessible to a broader range of users. The promise of fully autonomous operations for delivery and inspection services attracts significant investment and innovation.

MARKET RESTRAINTS

Stringent Regulatory Constraints and Airspace Restrictions

The strict regulatory frameworks and airspace restrictions, particularly for commercial operations, are restraining the growth of the United States drone market. The Federal Aviation Administration imposes rigorous guidelines regarding flight altitude proximity to airports, and operation over people to ensure public safety. Obtaining waivers for beyond visual line of sight operations remains a complex and time-consuming process, limiting the scalability of certain commercial applications. Operators must comply with remote identification requirements, which mandate broadcasting location and identity information, adding technical and financial burdens. The complexity of navigating varying local state and federal regulations creates uncertainty for businesses seeking to expand drone services. Privacy concerns among the general public also lead to local ordinances restricting drone usage in residential areas. These legal hurdles increase operational costs and delay project timelines. The lack of standardized procedures for urban air mobility further complicates the integration of drones into densely populated environments. Compliance requires dedicated legal and operational resources, which can be prohibitive for small enterprises.

Security Vulnerabilities and Data Privacy Concerns

The security vulnerabilities and data privacy are affecting both consumer confidence and enterprise adoption, which is also hampering the growth of the United States drone market. Drones are susceptible to cyberattacks, including GPS spoofing, signal jamming, and unauthorized data interception, which pose risks to sensitive operations. Certain foreign-manufactured drones have been flagged for potential data security risks, leading to restrictions on their use by federal agencies. These security concerns extend to commercial entities handling proprietary data such as infrastructure maps or agricultural insights. The potential for drones to be used for illicit surveillance raises privacy issues among citizens and policymakers. High-profile incidents involving drone interference with airport operations or emergency responses have heightened public scrutiny. Companies must invest heavily in encryption, secure communication protocols, and cybersecurity measures to protect their fleets and data. The lack of universal security standards creates fragmentation and uncertainty for buyers. Insurance premiums for drone operations remain high due to perceived liability risks associated with security breaches. The fear of data leakage discourages some organizations from fully integrating drones into their workflows.

MARKET OPPORTUNITIES

Integration into Last Mile Delivery Logistics

The integration of drones into last-mile delivery logistics for expansion and operational innovation is likely to set up new opportunities for the growth of the United States drone market. E-commerce giants and logistics companies are exploring autonomous aerial delivery to reduce transportation costs and improve speed. The ability to bypass ground traffic congestion offers a competitive advantage for time-sensitive deliveries such as medical supplies and perishable goods. Regulatory advancements allowing for beyond visual line of sight operations are paving the way for scalable delivery networks. Partnerships between technology providers and retail chains are accelerating the development of dedicated drone ports and charging infrastructure. The environmental benefits of electric drones compared to traditional delivery vehicles align with corporate sustainability goals. Consumers increasingly value rapid delivery options, creating demand for innovative logistics solutions. The expansion of suburban and rural delivery routes offers a lucrative market segment where ground transportation is less efficient.

Growth in Public Safety and Emergency Response Applications

The expanding role of drones in public safety and emergency response for societal benefit is also expected to boost the growth of the United States drone market. Law enforcement, fire departments, and search and rescue teams utilize drones for situational awareness, hazard assessment, and victim location. Thermal imaging cameras enable responders to locate missing persons in dense forests or at night, significantly improving survival rates. Drones are also used for disaster assessment after hurricanes, earthquakes, and wildfires, allowing authorities to prioritize resources effectively. The cost-effectiveness of drones compared to manned aircraft makes them accessible to smaller municipal agencies. Federal grants and funding programs support the acquisition of drone technology for public safety entities. Training programs for first responders are becoming more widespread, ensuring proficient use of these tools. The ability to deploy drones rapidly provides a tactical advantage in time-sensitive scenarios. Integration with command centers allows for real-time data sharing and coordinated response efforts.

MARKET CHALLENGES

Supply Chain Disruptions and Component Shortages

The supply chain disruptions and shortages of components, affecting production timelines and costs, are one of the major challenges for the growth of the United States drone market. The global semiconductor shortage has impacted the availability of microcontrollers and sensors essential for drone manufacturing. Dependence on international suppliers for batteries, motors, and raw materials exposes manufacturers to geopolitical tensions and trade policy changes. Tariffs on imported parts increase production costs, which are often passed on to consumers, reducing affordability. Logistics bottlenecks at ports and transportation networks further exacerbate inventory issues. Manufacturers struggle to maintain consistent stock levels, leading to lost sales opportunities. The complexity of drone systems requires a diverse range of specialized components, making supply chain management difficult. Small and medium-sized enterprises are particularly vulnerable to these disruptions due to limited bargaining power. Diversifying supply sources is a lengthy and costly process that requires significant investment. The unpredictability of global supply chains hinders long-term planning and strategic growth.

Short Battery Life and Limited Payload Capacity

Technological limitations regarding battery life and payload capacity for the widespread adoption of drones in demanding applications are also escalating the growth of the United States drone market. Most commercial drones have flight times ranging from 20 to 40 minutes, which restricts the area they can cover in a single mission. The battery technology has not kept pace with the increasing power demands of advanced sensors and processors. Frequent battery swaps interrupt workflows and reduce operational efficiency, particularly in large-scale inspection or mapping projects. The weight of high-capacity batteries reduces the available payload for camera sensors or delivered goods, limiting versatility. Cold weather conditions further degrade battery performance, posing challenges for operations in northern states. The development of solid-state batteries and hydrogen fuel cells is ongoing, but these technologies are not yet commercially viable for mass market drones. Charging infrastructure is often inadequate for fleet operations requiring significant downtime. The trade-off between flight time and payload capacity forces operators to make compromises in mission planning.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.22% |

| Segments Covered | By Component, Technology, Power Source, End Use, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | DJI, AeroVironment, Lockheed Martin, Northrop Grumman, Boeing, General Atomics, Parrot, Skydio, Teledyne FLIR, and Elbit Systems |

SEGMENTAL ANALYSIS

By Component Insights

The hardware segment was the largest by holding a dominant share of the United States drone market in 2025 due to the substantial initial capital investment required for acquiring physical unmanned aerial systems. Drones are tangible assets that necessitate robust construction, advanced sensors, and reliable propulsion systems, which constitute the majority of upfront costs for operators. Enterprise clients prioritize quality and reliability, ensuring that they invest in premium hardware capable of withstanding harsh environmental conditions. The complexity of modern drones integrating lidar, thermal camera,s and multispectral sensors further drives up the unit cost. Replacement and upgrade cycles also contribute to sustained hardware revenue as technology evolves rapidly. Government and defense contracts heavily favor hardware procurement due to the strategic importance of possessing proprietary fleets. The tangible nature of hardware makes it the primary entry point for new market participants who must first acquire the vehicle before investing in software or services. This foundational requirement ensures that hardware remains the largest revenue generator within the component ecosystem.

The services segment is expected to grow at the fastest CAGR of 8.2% during the forecast period, with the increasing demand for data analytics maintenance and operational support. Companies are shifting from owning drones to outsourcing operations to specialized service providers, who offer end-to-end solutions, including flight planning, data processing, and regulatory compliance. This trend is particularly evident in industries like infrastructure inspection,n where accurate data interpretation is critical. The complexity of managing large drone fleets necessitates professional management services to ensure safety and efficiency. Training and certification services are also in high demand as pilots need to stay updated with evolving regulations and technologies. The recurring revenue model of services provides stability and long-term customer relationships. As drones become integral to business operations, the reliance on expert services will continue to rise.

By Technology Insights

The remotely operated drones segment held a prominent share of the United States drone market in 2025 due to strict regulatory requirements and the need for direct pilot control in complex environments. The Federal Aviation Administration mandates that most commercial drone operations maintain a visual line of sight and require a certified remote pilot in command. According to the Federal Aviation Administration, the majority of registered drones are operated manually or with limited automation to ensure compliance with safety standards. Human oversight is critical for navigating dynamic airspace, avoiding obstacles, and responding to unexpected events. Many industries prefer remotely operated drones for tasks requiring precise maneuvering, such as close-up inspections or cinematic filming. The reliance on skilled pilots ensures that operations are conducted safely and efficiently. Training programs and certification processes support a large workforce of remote pilots. The technology for fully autonomous operations is still evolving and faces regulatory hurdles limiting its widespread adoption. Remotely operated drones offer flexibility and adaptability that automated systems currently lack. This regulatory and operational landscape ensures that remote operation remains the standard for most drone activities.

The fully autonomous drones segment is expected to register the fastest CAGR of 7.4% from 2026 to 2034, with the advancements in artificial intelligence and the gradual approval of beyond visual line of sight operations. These drones can execute complex missions without human intervention, relying on onboard sensors and algorithms for navigation and decision-making. The ability to operate BVLOS significantly expands the potential applications of drones, particularly in logistics and large-scale monitoring. Autonomous systems reduce labor costs and increase operational efficiency by eliminating the need for constant pilot attention. Machine learning enables drones to adapt to changing conditions and optimize flight paths in real time. The integration of 5G networks enhances connectivity, allowing for remote monitoring and control of autonomous fleets. Regulatory waivers for autonomous operations are becoming more common, paving the way for broader adoption. Industries such as agriculture and energy are early adopters leveraging autonomy for repetitive and large area tasks.

By Power Source Insights

The battery-powered drones segment was the largest by holding 56.4% of the United States drone market due to stringent environmental regulations and the operational advantage of quiet noise profiles. Electric motors produce zero emissions, making them compliant with increasingly strict environmental standards in urban and protected areas. The quiet operation of electric drones minimizes noise pollution,n making them suitable for residential surveillance, wildlife monitoring, and urban deliveries. Lithium-ion batteries offer high energy density and reliability, supporting the majority of commercial and consumer drone applications. The simplicity of electric propulsion systems reduces maintenance requirements and operational costs. Charging infrastructure is widely available and easy to integrate into existing facilities. The rapid advancement of battery technology continues to improve flight times and performance. Consumer preference for eco-friendly products also drives demand for battery-powered options. The versatility of electric drones across various sizes and types ensures broad market appeal.

The hydrogen fuel cell drones segment is likely to witness the fastest CAGR of 9.1% from 2026 to 2034, with the need for extended flight endurance and heavy payload capabilities. Unlike batteries, hydrogen fuel cells offer significantly longer flight times, often exceeding two hours, which is crucial for large-scale inspection and mapping missions. According to research from the Department of Energy, hydrogen fuel cells provide three to five times the energy density of lithium-ion batteries, enabling longer range operations. This advantage is particularly valuable for industries such as oil and gas, where pipelines span vast distances. Hydrogen drones can carry heavier sensors and equipment without compromising flight duration. The refueling process is faster than battery charging, reducing downtime between missions. Government initiatives promoting hydrogen technology as part of the clean energy transition support market growth. Although infrastructure is limited, ed dedicated refueling stations are being developed for industrial applications. The ability to operate in extreme temperatures, where batteries degrade further, enhances the appeal of hydrogen fuel cells.

By End Use Insights

The commercial segment accounted in holding 26.4% of the United States drone market share in 2025 due to its diversified industrial applications and compelling return on investment. Businesses across agriculture, construction, energy, and media utilize drones to enhance efficiency and reduce costs. The commercial sector accounts for the largest share of drone revenue, driven by widespread adoption in precision agriculture and infrastructure inspection. Farmers use drones for crop monitoring and spraying, optimizing resource usage and increasing yields. Construction companies leverage drones for site surveying and progress tracking, improving project management. The ability to collect accurate data quickly translates into tangible financial benefits for enterprises. The versatility of commercial drones allows them to address multiple pain points within different industries. Regulatory frameworks are increasingly accommodating commercial operations, facilitating market growth. The professionalism and reliability of commercial-grade drones build trust among business users. The continuous development of industry-specific solutions further strengthens this segment.

The military segment is growing at an estimated CAGR of 12.3% from 2026 to 2034, with the escalating geopolitical tensions and ongoing defense modernization efforts. The Department of Defense is prioritizing the acquisition of unmanned systems for intelligence surveillance and combat operations. Drones offer a cost-effective alternative to manned aircraft for risky missions,s reducing personnel exposure to danger. The development of stealth and autonomous military drones provides strategic advantages in modern warfare. Conflicts around the world have demonstrated the effectiveness of drones in reconnaissance and precision strikes. The US military is investing in swarm technology and AI-driven systems to maintain technological superiority. International arms sales of US-manufactured drones also contribute to market growth. The urgency of national security needs accelerates procurement cycles. The versatility of military drones across land, sea, and air domains expands their utility.

COMPETITION OVERVIEW

The competition in the United States drone market is characterized by intense rivalry among established defense contractors, rs agile tech startups, and international manufacturers. Major players compete on technological superiority, security, compliance, and specialized applications. Domestic companies leverage national security concerns to gain an advantage over foreign competitors, particularly in government sectors. Differentiation is achieved through proprietary software, autonomous features, and robust hardware designs. Price sensitivity varies across segments, with consumer markets driven by cost, while enterprise clients prioritize performance. Regulatory compliance serves as a significant barrier to entry, favoring established firms with resources for certification. Innovation cycles are rapid,d requiring continuous investment in research and development. Partnerships with software providers enhance value propositions by offering comprehensive data solutions. Brand reputation and trust are critical factors influencing purchasing decisions in sensitive industries. The market is fragmented, with niche players catering to specific verticals such as agriculture or inspection. Success depends on balancing innovation with regulatory adherence and customer support. This dynamic environment fosters constant adaptation and strategic alliances among participants.

KEY MARKET PLAYERS

A few major players of the United States drone market include

- DJI

- AeroVironment

- Lockheed Martin

- Northrop Grumman

- Boeing

- General Atomics

- Parrot

- Skydio

- Teledyne FLIR

- Elbit Systems

Top Strategies Used by Key Market Participants

Key players in the United States drone market employ product differentiation strategies to address specific industry needs. Companies focus on developing autonomous capabilities and advanced sensors to enhance operational efficiency. Security and compliance are central to corporate strategies as brands highlight domestic manufacturing and data protection. Strategic partnerships with technology firms enable integration of artificial intelligence and cloud services. Expansion in the enterprise and government sectors provides stable revenue streams and long-term contracts. Investment in research and development drives innovation in battery life and connectivity. Marketing efforts emphasize reliability and ease of use to attract professional users. Supply chain diversification mitigates risks associated with global disruptions. Customer support and training programs build loyalty and ensure successful adoption. These multifaceted strategies enable manufacturers to navigate regulatory challenges and sustain growth.

Leading Players in the US Drone Market

- AeroVironment Inc is a leading provider of unmanned aircraft systems and tactical missile systems for defense and commercial applications. The company contributes significantly to the global market by supplying advanced small drones to allied nations and international security forces. It strengthens its market position through continuous innovation in loitering munitions and reconnaissance technologies. Recent actions include expanding its manufacturing capacity in the United States to meet growing demand from the Department of Defense. The organization also focuses on developing autonomous capabilities and artificial intelligence integration for enhanced operational efficiency. AeroVironment collaborates with government agencies to refine tactics and procedures for drone deployment. These efforts ensure its technology remains at the forefront of modern warfare and security operations. The company emphasizes reliability and ease of use, which appeals to military personnel in high-stress environments.

- Skydio Inc is a prominent American drone manufacturer known for its autonomous flight technology and computer vision capabilities. The company contributes to the global market by setting new standards for obstacle avoidance and independent navigation in complex environments. It strengthens its position by focusing on enterprise and public safety sectors rather than consumer markets. Recent actions involve launching the Skydio X10, which offers superior thermal imaging and connectivity for critical missions. The organization also partners with major technology firms to integrate cloud-based data management solutions. Skydio emphasizes domestic production to address security concerns and comply with federal regulations. This approach resonates with government clients who prioritize supply chain integrity. The company invests heavily in software development to enhance autonomous features and user experience.

- Parrot SA is a French technology company with a significant presence in the United States drone market through its professional and defense divisions. The company contributes to the global market by offering secure and compliant drone solutions for sensitive operations. It strengthens its market position by adhering to strict data privacy standards and obtaining necessary certifications for government use. Recent actions include the launch of the ANAFI USA drone, which features high-resolution thermal cameras and a rugged design. Parrot also expands its partnerships with local distributors to enhance service and support networks in North America. The organization focuses on providing open source software options, allowing customers to customize applications. This flexibility appeals to developers and specialized industry users. Parrot emphasizes transparency in its supply chain to build trust with security-conscious clients. The company continues to invest in research and development to improve battery life and connectivity. These strategies enable Parrot to retain relevance in a highly competitive and evolving market landscape.

MARKET SEGMENTATION

This research report on the United States drone market has been segmented and sub-segmented based on component, technology, power source, end use & region.

By Component

- Hardware

- Software

- Services

By Technology

- Remotely operated

- Semi-autonomous

- Fully autonomous

By Power Source

- Battery-powered

- Gasoline-powered

- Hydrogen fuel cell

- Solar

By End Use

- Consumer

- Commercial

- Military

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What are the main types of drones used in the U.S.?

The main types include fixed-wing drones, rotary-wing drones (multi-rotor), and hybrid drones, with multi-rotor drones being widely used for commercial and consumer applications.

2. What are the key drivers of the U.S. drone market?

Key drivers include increasing use in defense and surveillance, growing adoption in agriculture and logistics, advancements in AI and automation, and supportive government regulations for commercial drone usage.

3. Which application segment dominates the market?

The defense and military segment dominates the U.S. drone market, followed by commercial applications such as agriculture, infrastructure inspection, delivery services, and media production.

4. What role does the logistics sector play in the market?

The logistics sector is increasingly adopting drones for last-mile delivery solutions, especially in e-commerce and healthcare, enhancing speed and efficiency.

5. What are the major trends in the U.S. drone market?

Major trends include the integration of artificial intelligence, growth of drone-as-a-service (DaaS), development of autonomous drones, expansion of urban air mobility, and increasing use of swarm technology.

6. What are the challenges faced by the market?

Challenges include regulatory restrictions, privacy concerns, limited battery life, cybersecurity risks, and high initial costs of advanced drone systems.

7. How does regulation impact the drone market in the U.S.?

Regulatory frameworks established by the Federal Aviation Administration play a crucial role in controlling drone operations, ensuring safety, and enabling commercial usage through licensing and operational guidelines.

8. What opportunities exist in the U.S. drone market?

Opportunities include expanding applications in smart cities, increasing investments in drone delivery systems, growth in surveillance and security services, and rising demand for data analytics through aerial imaging.

9. How is technology influencing the drone market?

Advancements in AI, machine learning, GPS systems, sensors, and battery technologies are significantly enhancing drone capabilities, enabling autonomous operations and real-time data processing.

10. Who are the key players in the United States drone market?

Key companies include DJI, AeroVironment, Lockheed Martin, Northrop Grumman, Boeing, General Atomics, Parrot, Skydio, Teledyne FLIR, and Elbit Systems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com