U.S. Laptop Market Size, Share, Trends & Growth Forecast Report By Type, By End-Use, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Laptop Market Size

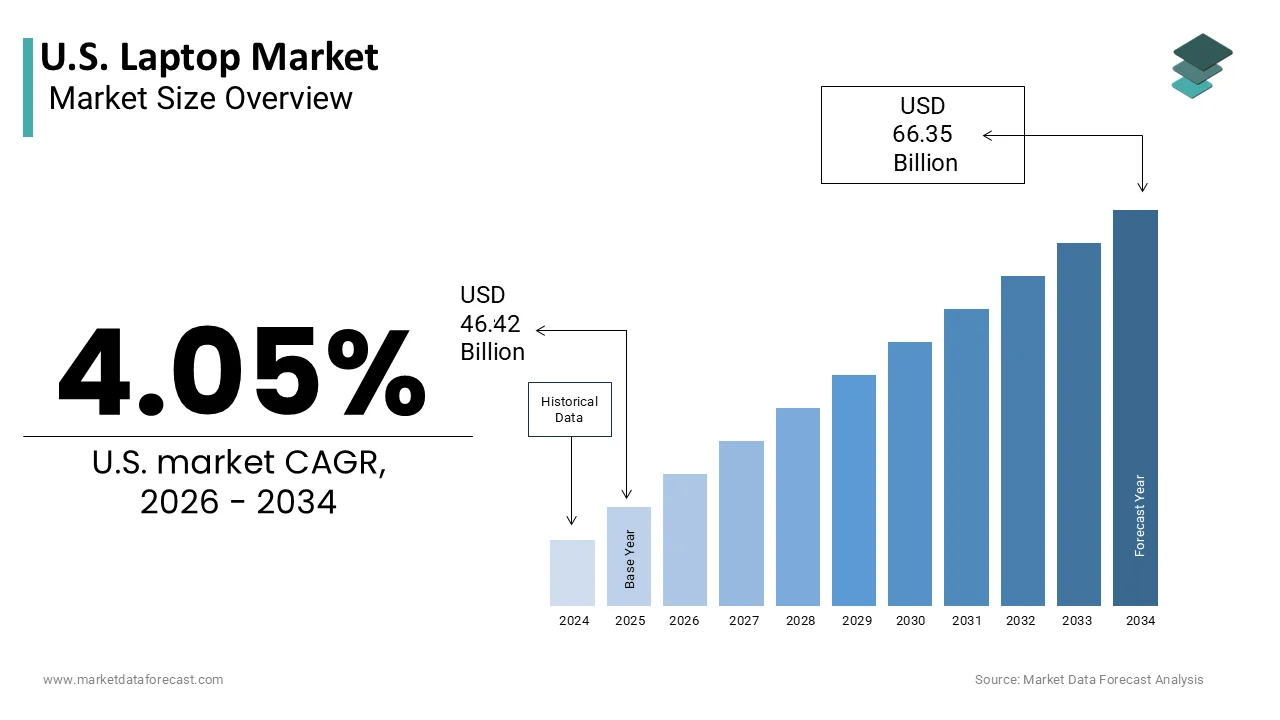

The United States Laptop Market was valued at USD 46.42 billion in 2025, is estimated to reach USD 48.30 billion in 2026, and is projected to reach USD 66.35 billion by 2034, growing at a CAGR of 4.05% from 2026 to 2034.

A laptop is a portable, compact personal computer (PC) designed for mobile use, featuring a clamshell form factor with a screen and keyboard in one unit. This market encompasses a wide array of devices ranging from traditional clamshell notebooks to innovative two-in-one convertibles and ultra-thin ultrabooks that cater to diverse user needs across education, enterprise, and personal entertainment sectors. The definition extends beyond mere hardware specifications to include the ecosystem of software compatibility, peripheral integration, and cloud connectivity that modern users demand for seamless productivity. As per the Bureau of Labor Statistics, 35 percent of employed persons did some or all of their work at home in 2023, while approximately 11 percent worked fully remotely by late 2023, underscoring the entrenched role of portable computing in the national workforce infrastructure. Furthermore, data from the National Center for Education Statistics indicates that over 90 percent of households with school-age children have access to a computer, demonstrating the foundational presence of these devices in educational environments. The market is characterized by rapid technological iteration, where advancements in processor efficiency, battery longevity, and display quality drive continuous consumer interest. According to research, about 77 percent of Americans own a desktop or laptop computer, reflecting a saturation point that shifts competitive dynamics toward replacement cycles and premium feature adoption rather than initial acquisition. This mature yet evolving landscape requires manufacturers to focus on specialized use cases such as gaming content creation and business security to sustain growth amidst high penetration rates.

MARKET DRIVERS

Integration of Artificial Intelligence Capabilities Driving Premium Upgrades

The incorporation of artificial intelligence processing units into central processing architectures serves as a potent driver for laptop replacements and premium segment growth, which fuels the expansion of the United States laptop market. Modern consumers and enterprises increasingly seek devices capable of handling local AI workloads, such as real-time language translation, advanced image editingg,g and predictive text generation without relying solely on cloud connectivity. This shift is driven by the need for lower latency, enhancedata privacy and improved operational efficiency in professional settings. According to INT,el the introduction of AI-enabled processors has led to a projected increase in average selling prices as users prioritize performance headroom for future-proofing their investments. This technological leap compels users with older hardware to upgrade since legacy systems cannot support the computational demands of emerging AI-driven applications like Copilot features and automated workflow assistants. The demand is further amplified by software developers optimizing applications for on-device machine learning, which creates a tangible performance gap between new AI-ready laptops and previous generations. As per sources, the integration of AI capabilities is becoming a key differentiator in purchasing decisions,s particularly among corporate buyers who aim to leverage automation for productivity gains. This trend ensures that the market remains dynamic despite high overall ownership rates as the functional definition of a capable laptop evolves to include dedicated AI acceleration hardware.

Expansion of Hybrid Work Models Sustaining Enterprise Demand

The enduring prevalence of hybrid work arrangements continues to propel steady demand for high-performance portable computing devices across the corporate sector and contributes to the growth of the United States laptop market. Organizations have permanently adopted flexible work policies that require employees to seamlessly transition between home offices and corporate campuses, necessitating reliable, secure e,r e and powerful laptops. This structural change in labor dynamics means that companies must equip their workforce with devices that offer robust video conferencing capabilities,ies long battery life, and strong security features to protect sensitive data outside traditional network perimeters. This trend drives enterprise procurement cycles as businesses replace aging fleets with modern units that support multi-monitor setups via USB-C docking and offer enhanced webcam quality for professional virtual interactions. Data from the Society for Human Resource Management shows that over 60 percent of employers offer some form of remote work options, reinforcing the laptop as the primary tool for labor participation. The requirement for consistent performance regardless of location pushes IT departments to prioritize devices with superior thermal management and connectivity options. As per C,isco the volume of video conferencing traffic remains significantly higher than pre-pandemic levels, which directly influences hardware specifications demanded by corporate buyers. This persistent enterprise demand provides a stable revenue stream for manufacturers as organizations prioritize employee productivity and collaboration tools embedded within modern laptop ecosystems.

MARKET RESTRAINTS

Saturation of Household Ownership Limiting New User Acquisition

The high level of laptop penetration in American households inhibits the expansion of the United States laptop market. This limits the pool of first-time buyers. The market relies heavily on replacement cycles rather than new user acquisition because most consumers already own a portable computer. Consequently, volume growth potential is naturally constrained. This saturation means that manufacturers must compete intensely for a share of a finite replacement market where consumers may delay upgrades if their current devices remain functional. According to the Pew Research Center, nearly 80 percent of adults in the United States own a laptop or desktop computer indicating that the addressable market for new entries is relatively small. This reality forces companies to extend product lifecycles and focus on incremental improvements that may not compel immediate upgrades for average users. This elongated cycle reduces the frequency of purchases and dampens annual sales volumes despite technological advancements. As per the Bureau of EcEconomic Analysis consumer spending on durable goods, including computers, has shown volatility reflecting the discretionary nature of replacing a still functional device. The lack of new demographic segments entering the market means that growth must come from convincing existing owners to trade,,,up which is increasingly difficult in an economic environment where value consciousness is paramount.

Supply Chain Volatility and Component Cost Fluctuations

Persistent instability in global supply chains and fluctuating costs of critical components are a restraint on profitability and pricing strategies within the United States laptop market. The production of laptops relies on complex international networks of semiconductors,ors memory modules,u modules,and display panels, making the industry vulnerable to geopolitical tensions, trade restrictions, and logistical disruptions. These factors can lead to sudden shortages or price spikes that erode margins and force manufacturers to pass costs onto consumers,umers potentially dampening demand. According to the Semiconductor Industry Association,iation global semiconductor sales fluctuations directly impact the availability and cost of central processing units and graphics chips essential for laptop manufacturing. Data from the Federal Reserve Bank of New York indicates that supply chain pressure indices have experienced periodic spikes due to regional conflicts and trade policy changes affecting electronic component flows. This volatility makes long-term pricing planning difficult for original equipment manufacturers who must balance competitive pricing with rising input costs. Additionally, the concentration of manufacturing for key components in specific geographic regions increases exposure to localized disruptions such as natural disasters or political instability. These supply-side constraints limit the ability of manufacturers to rapidly scale production in response to demand surges and can lead to inventory imbalances that further complicate market dynamics and financial performance.

MARKET OPPORTUNITIES

Growth of Cloud Gaming and Streaming Reducing Hardware Dependency

The rise of cloud gaming services and high-speed internet connectivity unlocks growth possibilities for the United States laptop market. This enables the shifting of computational heavy lifting from local hardware to remote servers. This technological evolution allows users to access high-performance gaming and professional applications on less powerful and more affordable laptops, thereby expanding the potential customer base for entry-level and mid-range devices. Consumers no longer need to invest in expensive high-end graphics cards and processors to enjoy premium experiences, as the rendering is handled off-site. Data from Netflix and other major tech firms entering the gaming space indicates a strategic push toward device-agnostic content delivery, which reduces the barrier to entry for high-fidelity interactive media. This trend enables manufacturers to focus on improving display quality,y battery li,fe and connectivity ithinnerin, ner lighter chassis rather than prioritizing raw internal processing power. This shift opens new market segments among casual users and students who require versatile devices for entertainment and study without the premium price tag of traditional gaming rigs. It also encourages subscription-based revenue models for software providers, creating a symbiotic ecosystem that drives hardware sales through service accessibility.

Adoption of Sustainable Materials and Circular Economy Practices

The increasing consumer and regulatory emphasis on environmental sustainability offers new pathways for manufacturers within the United States laptop market. They can differentiate their products through eco-friendly design and circular economy initiatives. Buyers are increasingly willing to pay a premium for laptops made from recycled materials and designed for easy repair and recycling,g aligning with broader corporate social responsibility goals. This trend allows brands to appeal to environmentally conscious segments and comply with emerging regulations regarding electronic waste and carbon footprints. Data from major manufacturers like Dell and HP shows that they have committed to using significant percentages of recycled plastics and metals in their newer models, ls responding to consumer demand for greener technology. As per the Nielsen Institute,a majority of global consumers indicate a willingness to change their consumption habits to reduce environmental impact, a pact which translates to purchasing preferences for sustainable tech products. This opportunity extends to the development of modular designs that facilitate component replacement,ement thereby extending device lifespan and reducing waste. By integrating sustainability into core product strategy, companies can build brand loyalty and mitigate regulatory risks while tapping into a growing segment of values-driven consumers. This approach also opens avenues for partnerships with recycling firms and certification bodies,e nhancing brand reputation and market positioning.

MARKET CHALLENGES

Intensifying Cybersecurity Threats Complicating Device Management

The escalating sophistication of cyber threats is a major challenge for the laptop market. As a result, manufacturers and users must constantly adapt to protect data integrity and privacy. Laptops are primary targets for malware, ransomware, and phishing attacks due to their portability and frequent use on unsecured networks, requiring robust built-in security features that add complexity and cost to device design. Enterprises face significant burdens in managing security protocols across distributed fleets of devices,s ensuring that each unit meets stringent compliance standards. According to the Federal Bureau of Investigation, on internet crime losses exceeded 10 billion dollars in recent years, with a significant portion attributed to business email compromises and ransomware attacks targeting endpoint devices. Data from cybersecurity firms indicates that the average cost of a data breach for companies continues tto riseise necessitating heavier investment in hardware-based security modules like Trusted Platform Modules. This challenge forces manufacturers to balance usability with security, often resulting in more complex user authentication processes that can hinder productivity. As per the National Institute of Standards and Technology,y the implementation of zero trust architectures requires continuous verification of device health,th which complicates IT management and increases operational overhead. The need for constant software updates and security patches also shortens the effective usable life of devices if older hardware cannot support the latest security protocols. This dynamic creates a tense environment where innovation in security must keep pace with evolving threats, ats adding pressure on research and development budgets.

Regulatory Pressures Regarding Right to Repair E-Waste

Emerging legislation focused on the right to repair and electronic waste management is an obstacle to traditional laptop manufacturing and business models, which hampers the expansion of the United States laptop market. These regulations require manufacturers to make spare parts, diagnostic tools, and repair manuals available to consumers and independent repair shops,s which disrupts the controlled service ecosystems that many companies rely on for after-sales revenue. Compliance with these laws necessitates redesigning products for modularity and durability, ty which can increase initial production costs and complicate engineering processes. According to the Public Interest Research Group,oup several states in the US have enacted or are considering right-to-repair laws that mandate greater transparency and accessibility for device maintenance. The challenge requires a fundamental shift in design philosophy, moving away froglued-togetherer compact forms toward more serviceable architectures that may compromise aesthetic slimness or weight targets. As per the Federal TradCommissionio,enforcement actions against restrictive repair practices are increasing,ng signaling a regulatory environment that favors consumer autonomy over manufacturer control. Companies must navigate this changing landscape by investing in new supply chains for spare parts and training programs for third-party repairers, which diverts resources from innovation in other areas. This regulatory headwind threatens profit margins derived from proprietary service channels and requires strategic adaptation to maintain competitiveness.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, End-Use, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Apple Inc., Dell Technologies Inc., HP Inc., Lenovo Group Limited, ASUSTeK Computer Inc., Acer Inc., Microsoft Corporation, Samsung Electronics Co., Ltd., LG Electronics Inc., Micro-Star International Co., Ltd., Razer Inc., Toshiba Corporation |

SEGMENTAL ANALYSIS

By Type Insights

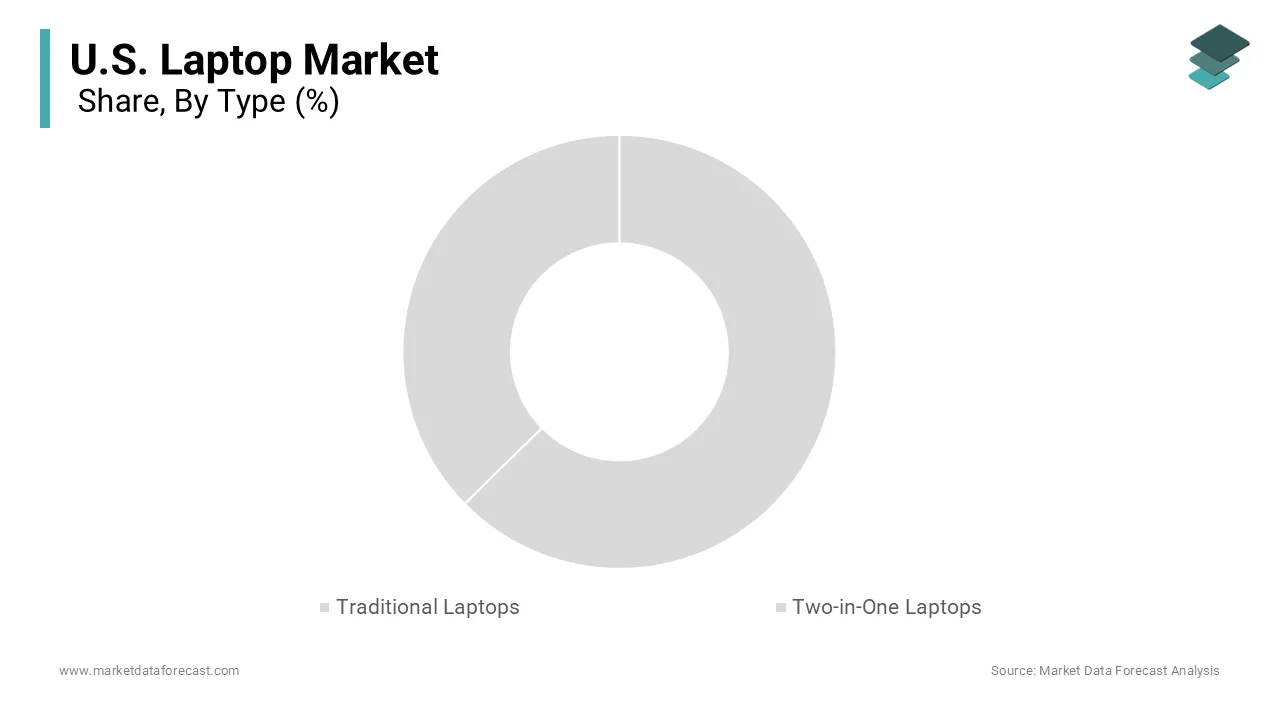

The traditional laptops segment maintained dominance in the United States laptop market and accounted for a 59.7% share in 2025. This dominance of the segment is driven by its entrenched role in enterprise environments where sstandardization reliability, and cost efficiency are paramount. Corporate IT departments prefer clamshell designs for their durability, ease ofrepaira,ir and compatibility with existing docking stations and peripheral ecosystems, which simplifies large-scale deployment and maintenance. This dominance is further reinforced by the lower average selling price of traditional units compared to premium convertibles, making them accessible for small businesses and educational institutions operating under strict budget constraints. The manufacturing supply chain for traditional laptops is also more mature and optimizedd,d allowing for higher production volumes and faster turnaroun ,time,s which ensures consistent availability for bulk orders. This operational advantage ensures that traditional laptops remain the default choicfor productivity-focuseded users who prioritize function over form flexibility, sustaining their market leadership despite the allure of innovative designs. The superior thermal management and performance consistency of traditional laptops drive their dominance among power users and professionals who require sustained computational power for demanding tasks. Two-in-one in one device,s which often compromises on cooling due to thin profile,s traditional laptops offer larger internal volumes for efficient heat dissipati,on allowing processors and graphics cards to operate at higher sustained speeds without throttling. This performance advantage is critical for videditorstor,s softwdeveloperslope, rs and data analysts who rely on consistent processing powerfor long-durationn projects. The ability to accommodate larger batteries in traditional chassis also translates to longer operational uptime, which is essential for mobile workers who may not have immediate access to power sources. This combination of raw power and endurance solidifies the traditional segment's lead among users who view their laptop as a primary productivity engine rather than a media consumption device.

The two-in-one laptop segment is experiencing the fastest growth with a projected CAGR of 9.5% during the forecast period,d owing to its unique versatility that bridges the gap between traditional computing and tablet usability. This form factor appeals strongly to students and creative professionals who benefit from touch input and stylus supportfor note-taking,g digital art, and interactive learning experiences. The ability to switch between laptop mode for typing and tablet mode for reading or drawing provides a flexible user experience that traditional devices cannomatchhtc,h enhancing engagement and productivity. This trend is further amplified by software optimization from major providers like Microsoft and do, who have enhanced their applications to leverage touch and pen inputs effectively. This demographic shift ensures sustained growth for the two-in-one segment as it aligns with evolving habits of digital natives. The rapid expansion of the two-in-one segment is fueled by aggressive design innovation and premiumization strategies that position these devices as status symbols and high-value lifestyle products. Manufacturers are investing heavily in ultra-thin bezel,s lightweight mate,rials and high resolution OLED displays to differentiate two in one models from standard laptops appealing to consumers willing to pay a premium for aesthetics and portability. This focus on visual excellence attracts affluent buyers who prioritize display quality and build craftsmanship in their purchasing decisions. The integration of advanced features such as facial recognition,on fingerprint sen,sors and haptic feedback touchpads further enhances the premium ap,peal justifying higher price points. This premium positioning allows manufacturers to maintain healthy margins while driving volume growth through aspirational marketing, feature-rich offerings that resonate with style-conscious tech enthusiasts.

By End-Use Insights

The business segment led the United States laptop market and captured a 47.5% share in 2025. This leading position of the segment is attributed to continuous digital transformation initiatives and regular fleet refresh cycles that ensure employees have up-to-date secure and efficient computing tools. Enterprises across industries are upgrading their hardware to support cloud-based workflows collaboration platforms and cybersecurity protocols which necessitates reliable and powerful laptops. Large corporations typically operate on three to five-year replacement cycles to maintain productivity and security standards, creating a steady and predictable demand stream for manufacturers. The shift toward hybrid work models has further accelerated this demand as companies equip remote workers with enterprise-grade devices that offer enhanced connectivity and security features. This sustained corporate investment provides a stable foundation for the mamarket insulating it from the volatility of consumer discretionary spending and driving consistent volume growth through bulk contracts and managed service agreements. Strict security compliance and regulatory requirements compel businesses to procure laptops with advadvanced hardware-basedcurity features,s driving domination in the business segment. Industries such as finance,e healthcare and legal services are subject to stringent data protection laws that mandate the use of devices with Trusted Platform Modules biometric authentication and encrypted storage capabilities. This regulatory pressure forces organizations to replace older inventory that lacks modern security standards with compliant devices ,creating a mandatory upgrade cycle independent of performance needs. compliance-driven demand ensures that business laptops incorporate the latest security technologies, such as infrared cameras for facial recognition and dedicated security processors. The necessity to meet these legal and industry standards creates a captive market for high specification business laptop,s sustaining the segment's leadership position thronon-discretionarynary procurement driven by risk management and legal obligation rather than mere preference.

The gaming segment is likely to experience the fastest CAGR of 12.8% from 2026 to ,2034, owing to the explosive popularity of esports and competitive gaming culture among younger demographics. The professionalization of gaming has transformed it from a niche hobby into a mainstream entertainment industry,,dustry driving demand fhigh-performancence laptops capable of delivering competitive advantages through high frame rates and low latency. This cultural shift encourages consumers to view gaming laptops as essential tools for participation in online communities and tournaments rather than just leisure devices. The desire to replicate professional setups at home drives purchases of laptops with high refresh rate displays,s mechanical keyb,oards and advanced cooling systems. This demographic enthusiasm ttranslates intoa higher willingness to spend on specialized equipment sus,,taining rapid growth in the gaming laptop segment as manufacturers release increasingly powerful and portable models tailored to this passionate community. Rapid technological advancements in portable graphics performance are accelerating the growth of the gaming laptop segment by encooffering console-qualityeriences in mobile form factors. The development of more efficient graphics processing units and ray tracing technologies allows gamers to enjoy visually stunning titles with realistic lighting and reflections on the go,e go removing the need for bulky desktop setups. This technological leap expands the addressable market to include students and young professionals who require a single device for both work and play,ay drivingdual-purposee adoption. The availability of high-bandwidth memory and fast solid-state drives further reduces load times and enhances gameplay smoothness, making laptops viable primary gaming machines. These innovations reduce the compromise traditionally associated with mobile gam ,ing attracting a broader audience of casual and hardcore gamers alike. The convergence of portability and power ensures that gaming laptops continue to capture market share from desktops and consoles,nsoles driving the segment's exceptional growth rate.

COUNTRY LEVEL ANALYSIS

U.S

The United States was the top performer in the North American laptop market and occupied a 85.4% share in 2025. This growth of the country’s market is propelled by its massive consumer base advanced technological infrastruc,ture and high disposable income levels. The US market is a major hub for global technology corporations and early digital adoption. As a result, it sets the pace for innovation and consumption patterns across the continent. Also, the market status is characterized by high saturation yet robust replacement demand driven by continuous technological advancements and shifting work lifestyles. According to the US Census Bu,reau the total number of households with broadband internet access exceeds 90 pe,rcent providing the necessary connectivity foundation for laptop utilization in work education and entertainment. This widespread connectivity ensures that laptops remain essential tools fodaily lifeil,y life sustaining consistent demand across all demographic segments. The presence of major retail channels including online giants and specialized electronics stores facilitates easy access to a wide variety of devices catering to diverse preferences and budgets. As per the Department o,f Commerce, e commerce sales of consumer electronics continue to grow indicating a shift in purchasing behavior toward online platforms that offer competitive pricing and extensive product comparisons. This mature retail ecosystem supports high transaction volumes and efficient distribution, networks ensuring that new products reach consumers rapidly. The strong intellectual property protection framework also encourages manufacturers to launch their latest innovations in the US first, establishing it as a primary market for premium and cutting edge laptop technologies. Strong economic indicators and high consumer spending power drive the United States,top market ensuring sustained demand for premium and specialized devices despite global economic fluctuations. The robust labor market and rising wages enable consumers to prioritize quality and performance in their purchasing decisions, leading to higher average selling prices and revenue growth. According to the Bureau of Economic Analysis personal consumption expenditures on durable goods including computers have remained resilient reflecting the essential nature of these devices in modern life. The prevalence of remote and hybrid work models further amplifies this demand as individuals invest in home office setups requiring reliable and powerful laptops for professional tasks. Data from the Federal Reserve indicates that household net worth has reached hhistoric highsistoric highs providing financial capacity for discretionary upgrades and multiple device ownership within single househol,ds. Additional,ly the strong emphasis on higher education in the US drives significant laptop procurement among students who require devices for online learning, research and coursework. This educational demand is supported by institutional programs and financial aid packages that often include technology allowances. The combination of economic strength professional needs and educational requirements creates a multifaceted demand structure that sustains the US market's leadership position and drives continuous innovation and sales volume in the laptop sector.

COMPETITIVE LANDSCAPE

The competition within the United States laptop market is characterized by intense rivalry among established global giants and emerging niche players who strive to capture value in a mature and saturated environment. Major corporations such as Lenovo HP and Dell dominate the landscape leveraging their extensive distribution networks strong brand recognition and comprehensive product portfolios to maintain leadership positions. These incumbents compete fiercely on innovation,, particularly in areas like artificial intelligence integration battery efficiency and display technology to differentiate their offerings and justify premium pricing strategies. The market sees continuous pressure from Apple wh,ich commands significant loyalty in the premium segment through its proprietary ecosystem and silicon advancemen,ts forcing competitors to enhance interoperability and performance. Smaller brands and specialized gaming manufacturers challenge the status quo by targeting specific demographics high-performancemance devices and customizable options. Competitive dynamics are further influenced by supply chain efficienci,es wherethe ability to secure components and manage costs determines profitability. Companies increasingly focus on services and subscription models to create recurring revenue streams beyond hardware sales. This multifaceted competition drives rapid technological iteration and forces constant adaptation to changing consumer preferences regarding sustainability security and remote work capabilities ensuring a dynamic and evolving marketplace structure.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Laptop Market include

- Apple Inc.

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- ASUSTeK Computer Inc.

- Acer Inc.

- Microsoft Corporation

- Samsung Electronics Co., Ltd.

- LG Electronics Inc.

- Micro-Star International Co., Ltd. (MSI)

- Razer Inc.

- Toshiba Corporation

TOP LEADING PLAYERS IN THE MARKET

- Lenovo maintains a formidable presence in the global laptop landscape through its diverse portfolio that spans consumer ThinkPad business lines and gaming Legion series. The company actively strengthens its position by integrating artificial intelligence capabilities into its devices enhancing user productivity and personalization. Recent initiatives include launching AI powered PCs equipped with dedicated neural processing units to handle complex local workloads efficiently. Lenovo also focuses on sustainability by incorporating recycled materials into chassis designs and developing modular components for easier repair. These efforts align with growing environmental consciousness among consumers and regulatory requirements. The firm continues to expand its hybrid work solutions offering robust security features and seamless connectivity options for enterprise clients. By prioritizing innovation in foultra-thin such as ultra thin foldables and dual screen devices Lenovo captures attention in premium segments. Its strategic partnerships with software developers ensure optimized performance for popular applications reinforcing its reputation for reliability and cutting edge technology in the competitive international marketplace.

- HP Inc. leverages its strong brand heritage to dominate various sectors including education enterprise and creative professionals through its Spectre Envy and EliteBook series. The company emphasizes design excellence and premium build quali,ty appealing to style conscious consumers who value aesthetics alongside performance. HP has recently accelerated its adoption of sustainable practices by using ocean-bound plastics in product manufacturing and introducing recyclable packaging solutions. It strengthens market position by advancing PC as a service mode,ls allowing businesses to manage device lifecycles more efficiently while reducing upfront costs. The integration of advanced collaboration tools such as high resolution webcams and AI driven noise cancellation addresses the needs of remote workers. HP also invests heavily in research and development for next generation display technologies including OLED and mini LED panels. These strategic moves enhance user experience and differentiate its offerings in a saturated market. HP ensures trust among corporate buyers by focusing on security innovations like hardware-based threat detection. This commitment helps maintain their status as a leading innovator in personal computing systems globally.

- Dell Technologies sustains its influential role in the global laptop market by delivering highly customizable solutions tailored to specific enterprise and consumer needs through its XPS Latitude and Alienware brands. The company excels in supply chain managemen,t ensuring timely delivery and consistent product availability even during global disruptions. Dell strengthens its position by expanding its portfolio oAI-readydy laptops designed to support intensive machine learning tasks locally. It actively promotes circular economy principles by offering comprehensive recycling programs and designing products for disassembly and material recovery. Recent actions include enhancing its direct to consumer sales model which allows for greater personalization and customer engagement. Dell also focuses on integrating advanced security features such as biometric authentication and encrypted storage to protect sensitive data for business users. The firm collaborates closely with component suppliers to secure early access to latest processors and graphics cards ensuring competitive performance advantages. Dell builds long-term loyalty among professional users who rely on dependable computing infrastructure for critical operations worldwide. They achieve this by prioritizing customer service and technical support.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States laptop market employ several strategic approaches to maintain competitiveness and drive growth amidst saturation. Product differentiation through artificial intelligence integration serves as a primary strategy where manufacturers embed neural processing units to enable local AI workloads enhancing performance and privacy. Sustainability initiatives are increasingly vital as companies adopt recycled materials and design for repairability to meet regulatory demands and appeal to environmentally conscious consumers. Manufacturers also focus on premiumization by launching high end models with superior displays and build quality to increase average selling prices and margins. Strategic partnerships with software providers ensure optimized application performance creating ecosystem lock in effects that foster brand loyalty. Additionally firms expand direct to consumer channels allowing for greater customization and improved customer relationships while bypassing traditional retail intermediaries. Emphasis on hybrid work solutions including enhanced webcams and connectivity features addresses enduring remote work trends. These strategies collectively enable companies to navigate market maturity by focusing on value addition, technological innovation and customer experience rather than competing solely on price or volume in the highly developed American landscape.

MARKET SEGMENTATION

This research report on the U.S. laptop market is segmented and sub-segmented into the following categories

By Type

- Traditional Laptops

- Two-in-One Laptops

By End-Use

- Business

- Gaming

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com