U.S. Smartphone Market Size, Share, Trends, and Growth Analysis Report, Segmented by Operating System, Display Technology, RAM Capacity, Price Range, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

U.S. Smartphone Market Report Summary

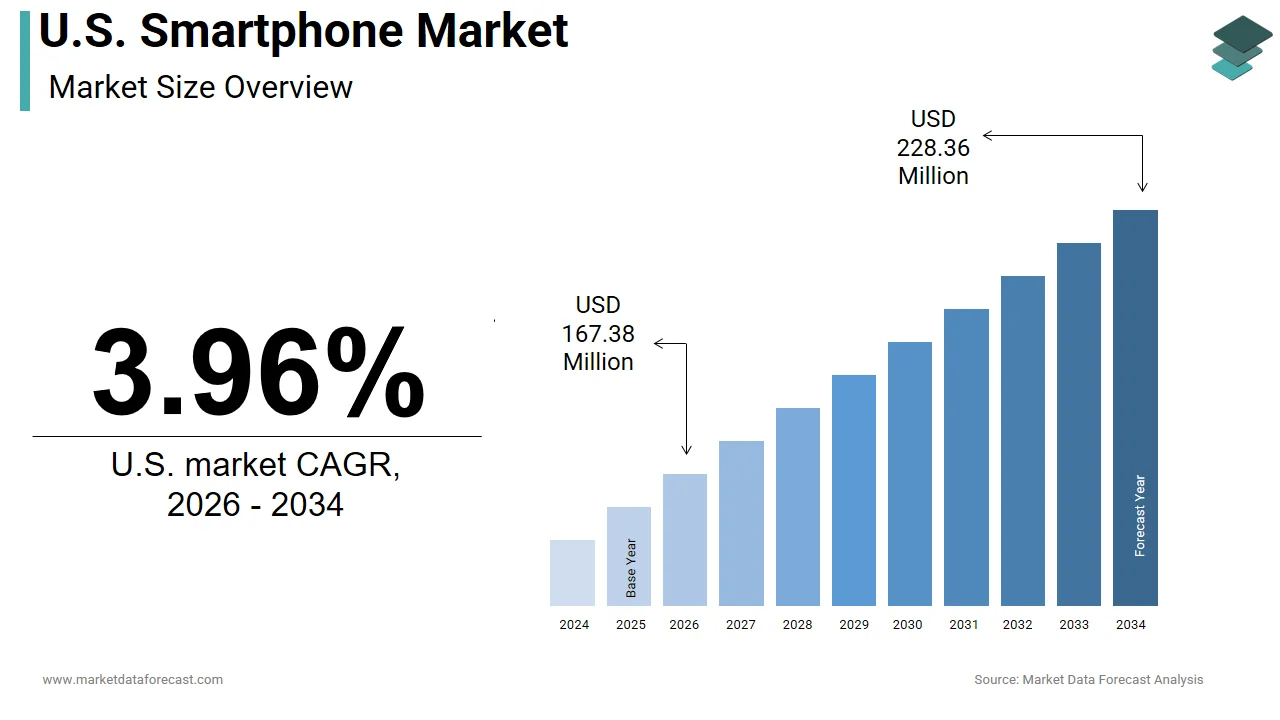

The U.S. smartphone market was valued at 161 million units in 2025 and is estimated to reach 167.38 million units in 2026, and is projected to reach 228.36 million units by 2034, growing at a CAGR of 3.96% from 2026 to 2034. Market growth is driven by continuous device upgrades, rising demand for premium smartphones, and rapid advancements in mobile technologies such as AI integration, 5G connectivity, and foldable displays. Increasing consumer preference for high-performance devices, enhanced camera systems, and seamless ecosystem integration is further supporting market expansion. Additionally, replacement cycles and carrier-driven upgrade programs continue to play a key role in sustaining demand.

Key Market Trends

- Rising demand for premium and ultra-premium smartphones.

- Increasing adoption of AI-powered and 5G-enabled devices.

- Growth in foldable and innovative display technologies.

- Strong consumer preference for ecosystem integration and performance.

- Expansion of carrier-led upgrade and financing programs.

Segmental Insights

- Based on operating system, the iOS segment dominated the U.S. smartphone market in 2025, driven by strong brand loyalty and ecosystem integration led by Apple Inc..

- Based on display technology, the OLED segment held the largest share in 2025, supported by superior display quality and increasing adoption in premium devices.

- Based on price range, the premium and ultra-premium segments dominated the market in terms of revenue in 2025, reflecting consumer willingness to spend on high-end features.

- Based on distribution channel, the retailers segment led the market in 2025, driven by strong presence of carrier stores and electronics retailers.

Country-Level Insights

The United States continues to lead the global smartphone market in terms of revenue and innovation. The country is expected to maintain its dominance over the forecast period, driven by early adoption of advanced technologies such as AI-integrated smartphones, foldable devices, and next-generation connectivity solutions.

Competitive Landscape

The U.S. smartphone market is highly competitive, with companies focusing on innovation, premiumization, and ecosystem development. Strategic partnerships with telecom operators, continuous product launches, and advancements in AI and hardware capabilities are key competitive strategies.

Prominent companies operating in the U.S. smartphone market include Apple Inc., Samsung Electronics, Google LLC, Motorola Mobility LLC, Huawei Device Co., Ltd., Xiaomi Corporation, Oppo, Vivo, Realme, OnePlus, Shenzhen Transsion Holdings Co., Ltd., and ZTE Devices.

U.S. Smartphone Market Size

The U.S. smartphone market was valued at 161 million units in 2025 and is estimated to reach 167.38 million units in 2026, and is projected to reach 228.36 million units by 2034, growing at a CAGR of 3.96% from 2026 to 2034.

According to data from the Pew Research Center, approximately 90% of American adults owned a smartphone in 2024, which reflects near-universal adoption across demographic groups. The market is defined by a duopoly in operating systems, with iOS and Android commanding virtually the entire installed base. Device replacement cycles have lengthened significantly, with the average user retaining their device for over 3 years, according to Consumer Intelligence Research Partners. This trend indicates a shift from frequent upgrades to value-driven retention, influenced by rising hardware costs and incremental innovation. The regulatory environment plays a crucial role, with ongoing debates regarding right to repair, app store monopolies, and data privacy shaping industry practices. Furthermore, the integration of artificial intelligence into device functionalities has become a key differentiator, driving consumer interest in newer models despite market saturation. The U.S. remains a critical revenue generator for major brands due to its high average selling prices and strong demand for flagship devices. Connectivity infrastructure, including the widespread deployment of 5G networks, continues to enable new use cases and enhance user experience, sustaining the relevance of smartphones in everyday life.

MARKET DRIVERS

Pervasive 5G Network Deployment and Enhanced Connectivity

The extensive deployment of 5G networks across the U.S. is one of the major factors driving the growth of the U.S. smartphone market. Telecommunication providers have invested billions in infrastructure, resulting in broad coverage that enhances the utility of modern smartphones for streaming, gaming, and remote work. As per the Federal Communications Commission, 5G coverage reached over 95% of the US population by late 2024, creating a robust environment for data-intensive applications. This network evolution necessitates hardware compatibility, prompting users with older 4G devices to seek newer models equipped with 5G modems. The improved connectivity enables seamless cloud integration and real-time collaboration, which are increasingly essential for both personal and professional activities. According to industry data, 5G-enabled devices accounted for over 80% of all smartphone shipments in the U.S. in 2025, demonstrating the rapid transition away from legacy technologies. Consumers perceive 5G capability as a standard feature rather than a luxury, making it a decisive factor in purchasing decisions. The promise of enhanced mobile broadband experiences drives demand for flagship devices that can fully leverage network capabilities. Additionally, the rollout of standalone 5G networks further improves performance, encouraging early adopters and tech enthusiasts to refresh their devices. This technological imperative ensures a steady stream of upgrades, sustaining market volume despite overall saturation. The synergy between network advancement and device capability creates a compelling value proposition for consumers seeking superior mobile performance.

Integration of Advanced Artificial Intelligence Features

The integration of advanced artificial intelligence features into smartphones has emerged as a significant driver of the U.S. smartphone market, which is also transforming devices into intelligent assistants capable of personalized and proactive interactions. Manufacturers are embedding AI chips and algorithms that enhance photography, battery management, and voice recognition, offering tangible benefits that appeal to consumers. As per industry reports, shipments of AI-enabled smartphones in the U.S. grew by 25% in 2024, reflecting strong consumer appetite for intelligent functionalities. Features such as real-time language translation, predictive text, and automated photo editing simplify daily tasks and enhance user productivity. The rise of generative AI on-device allows for complex computations without relying on cloud connectivity, addressing privacy concerns and improving response times. Consumers are increasingly willing to pay a premium for devices that offer these sophisticated capabilities, viewing them as essential tools for modern living. Market analysis suggests that AI-driven features are becoming a key differentiator in a crowded market, influencing brand loyalty and purchase decisions. The ability of smartphones to learn user habits and optimize performance accordingly creates a sticky ecosystem that discourages switching to competitors. Furthermore, the development of AI-powered health monitoring and security features adds value beyond traditional communication functions. As AI technology matures, its integration into smartphones will continue to drive upgrade cycles and stimulate demand for higher-end models. This technological evolution ensures that smartphones remain at the forefront of consumer electronics innovation.

MARKET RESTRAINTS

Lengthening Device Replacement Cycles

The lengthening of device replacement cycles is a major restraint for the U.S. smartphone market, as consumers retain their devices for longer periods due to diminishing returns on innovation and higher costs. The average lifespan of a smartphone in the U.S. has extended to approximately 3.5 years, according to data from Counterpoint Research. This trend reduces the frequency of purchases, limiting market growth and volume potential. Consumers perceive recent incremental improvements in camera quality, processing speed, and display technology as insufficient justification for upgrading existing functional devices. The high cost of flagship models, often exceeding 1,000 U.S. dollars, further discourages frequent replacements, particularly in an economic environment characterized by inflation and financial uncertainty. According to recent surveys, nearly 40% of Americans delay buying a new smartphone due to budget constraints, opting instead to repair or maintain their current devices. Manufacturers face the challenge of stimulating demand in a market where necessity rather than desire drives purchases. The lack of groundbreaking features that fundamentally change the user experience contributes to consumer apathy toward new releases. Additionally, the improved durability and battery life of modern devices reduce the need for premature replacements. This shift in consumer behavior forces companies to rely on higher average selling prices to maintain revenue, which may further suppress volume growth. Until manufacturers can introduce compelling innovations that justify the investment, lengthening replacement cycles will continue to restrain market expansion.

High Cost of Flagship Devices and Economic Pressure

The high cost of flagship smartphones and broader economic pressure are further impeding the expansion of the U.S. smartphone market, which is also limiting accessibility for price-sensitive consumers. Premium devices from leading brands often retail for over 1,000 U.S. dollars, placing them out of reach for many households facing rising living expenses. According to the Bureau of Labor Statistics, inflation rates have impacted discretionary spending, causing consumers to prioritize essential goods over luxury electronics. The total cost of ownership, including insurance plans and accessories, further exacerbates the financial burden, leading some buyers to opt for cheaper alternatives or extend the life of their current devices. Mid-range and budget segments offer viable alternatives, but they often lack the prestige and advanced features associated with flagship models, limiting their appeal to status-conscious consumers. Economic uncertainty also affects corporate spending on employee devices, reducing bulk purchases that traditionally contribute to market volume. According to recent market studies, consumer confidence in big-ticket electronics purchases declined by 15% in 2024 compared to the previous year, reflecting cautious spending behavior. This economic climate forces manufacturers to compete aggressively on price and financing options, squeezing profit margins. The perception of smartphones as non-essential luxuries during tough economic times further dampens demand. Unless manufacturers can offer more affordable premium options or demonstrate clear value propositions, high costs and economic pressures will continue to hinder market growth and limit penetration in lower-income demographics.

MARKET OPPORTUNITIES

Expansion of the Refurbished and Pre-Owned Market

The expansion of the refurbished and pre-owned smartphone market presents a significant opportunity for growth. Buyers are increasingly turning to certified refurbished devices as a viable alternative to new phones, attracted by lower prices and environmental benefits. As per data from Back Market, the sales of refurbished electronics in the U.S. grew by 20% in 2024, with smartphones accounting for the largest share of this segment. This trend aligns with growing consumer concern about electronic waste and the carbon footprint of manufacturing new devices. Retailers and manufacturers are responding by establishing robust refurbishment programs that offer warranties and quality guarantees, enhancing consumer trust in pre-owned products. The availability of high-quality refurbished flagship models allows budget-conscious consumers to access premium features at a fraction of the original cost. Industry analysts predict that the refurbished smartphone market will continue to expand at a double-digit rate over the next five years, capturing a larger portion of total sales. This shift provides an opportunity for companies to engage with customers who might otherwise be priced out of the new device market. Furthermore, trade-in programs facilitate the flow of used devices into the refurbishment pipeline, creating a circular economy that benefits both consumers and manufacturers. By embracing this segment, companies can diversify their revenue streams and appeal to environmentally conscious buyers. The growth of the refurbished market offers a sustainable path for industry expansion amidst slowing new device sales.

Adoption of Foldable and Innovative Form Factors

The adoption of foldable and innovative form factors offers a substantial opportunity for the U.S. smartphone market. Foldable devices, which combine the portability of a phone with the screen real estate of a tablet, appeal to users seeking versatility and multitasking capabilities. As per company reports from Samsung Electronics, shipments of foldable smartphones in the U.S. increased by 35% in 2024, indicating growing acceptance of this new category. Although still a niche segment, foldables represent a high-growth area with significant potential for expansion as prices decrease and durability improves. Manufacturers are investing heavily in research and development to address issues such as screen creases and hinge reliability, enhancing the overall user experience. The unique form factor differentiates these devices from traditional slab phones, attracting early adopters and tech enthusiasts willing to pay a premium for innovation. As per Display Supply Chain Consultants, the cost of flexible OLED panels has decreased by 15%, enabling manufacturers to offer more competitively priced foldable models. This price reduction is expected to broaden the addressable market and accelerate adoption. Furthermore, software optimization for larger screens enhances productivity and entertainment experiences, adding value to the hardware. The introduction of new form factors stimulates upgrade cycles among consumers bored with conventional designs. By continuing to innovate in this space, manufacturers can create new demand drivers and sustain growth in a mature market.

MARKET CHALLENGES

Regulatory Scrutiny and Antitrust Investigations

Regulatory scrutiny and antitrust investigations are primarily challenging the expansion of the U.S. smartphone market, particularly for dominant players controlling both hardware and software ecosystems. Government agencies are examining practices related to app store commissions, pre-installed applications, and restrictions on third-party repairs, which could lead to significant operational changes. According to the Federal Trade Commission, ongoing investigations into big tech companies have resulted in proposed regulations that may force openness in operating systems and payment processing. These regulatory pressures threaten the lucrative services revenue streams that complement hardware sales, potentially impacting profitability. Compliance with new rules requires substantial legal and technical resources, diverting attention from innovation and product development. The potential breakup of integrated ecosystems could weaken brand loyalty and reduce the stickiness of proprietary services. Additionally, right-to-repair legislation mandates that manufacturers provide parts and tools to independent repair shops, challenging controlled service networks. According to iFixit, new state laws have already compelled several manufacturers to release repair manuals and components, altering their after-sales service models. These changes may increase operational complexity and costs while reducing control over the customer experience. The uncertainty surrounding future regulatory outcomes creates a challenging business environment, requiring companies to adapt quickly to avoid penalties. Navigating this complex legal landscape is a persistent challenge that impacts strategic planning and long-term competitiveness in the U.S. smartphone market.

Supply Chain Vulnerabilities and Component Shortages

Supply chain vulnerabilities and component shortages present a significant challenge to the U.S. smartphone market, disrupting production schedules and increasing costs. The global nature of smartphone manufacturing relies on complex networks of suppliers for semiconductors, displays, and batteries, making it susceptible to geopolitical tensions and natural disasters. According to the Semiconductor Industry Association, fluctuations in chip availability have led to production delays and increased component prices, affecting device launches and inventory levels. Dependence on specific regions for critical materials creates risks that can cascade through the entire supply chain. Trade restrictions and tariffs further complicate sourcing strategies, forcing companies to diversify suppliers and incur higher logistics costs. The transition to advanced manufacturing processes for next-generation chips requires significant capital investment and time, limiting the ability to rapidly scale production. According to industry analysis, supply chain disruptions contributed to a 5% decline in smartphone shipments in the U.S. during peak demand periods in 2024. These interruptions impact revenue and customer satisfaction, as consumers face limited availability and longer wait times. Manufacturers must invest in resilient supply chain strategies, including nearshoring and inventory buffering, to mitigate these risks. However, these measures increase operational expenses and reduce flexibility. The ongoing instability in global supply chains remains a critical challenge that requires continuous monitoring and adaptation to ensure consistent product availability and competitive pricing in the U.S. market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Operating System, Display Technology, RAM Capacity, Price Range, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Operating System Insights

The iOS operating system dominated the market with the highest share of the U.S. smartphone market in 2025. The dominant position of the iOS segment in the U.S. market is driven by its deeply integrated ecosystem that fosters exceptional customer loyalty and high retention rates. Apple has successfully created a walled garden where devices such as the iPhone, iPad, Mac, and Apple Watch seamlessly interact, making it inconvenient for users to switch to competing platforms. According to Consumer Intelligence Research Partners, the retention rate for iPhone users in the U.S. exceeded 90% in 2024, indicating that the vast majority of existing users upgrade to newer iPhone models rather than switching to Android. This stickiness is reinforced by services like iMessage, FaceTime, and iCloud, which are exclusive to Apple devices and serve as significant social and functional barriers to exit. The perceived status associated with owning an iPhone also plays a crucial role, particularly among younger demographics who view the brand as a cultural symbol. According to Piper Sandler’s Taking Stock With Teens survey, approximately 87% of American teenagers prefer iPhones, ensuring a strong pipeline of future loyal customers. This entrenched user base provides Apple with a stable revenue stream from hardware sales and recurring service subscriptions. The consistent software updates and long-term support for older devices further enhance the value proposition, encouraging users to remain within the ecosystem. Consequently, the strength of the iOS ecosystem acts as a powerful moat, sustaining its leadership in the highly competitive U.S. smartphone market.

However, the Android operating system segment is growing rapidly and is expected to register the fastest CAGR in the U.S. market during the forecast period, owing to a diverse portfolio of devices that cater to various price points and consumer preferences. Unlike the singular approach of iOS, Android is licensed to multiple manufacturers such as Samsung, Google, and Motorola, enabling a wide range of innovation and competition. This diversity allows Android to capture market share among budget-conscious consumers and those seeking specific features such as customizable interfaces or expandable storage. According to industry reports, Android device shipments in the mid-range sector grew by 12% in 2024, outpacing growth in the premium segment. Manufacturers leverage economies of scale to offer feature-rich devices at competitive prices, appealing to value-oriented buyers. The availability of foldable phones and devices with advanced camera systems under the Android umbrella attracts tech enthusiasts looking for alternatives to the iPhone. Google’s Pixel series has also gained traction by offering pure Android experiences and advanced artificial intelligence features at lower price points than flagship competitors. According to Statista, the share of Android users in the U.S. increased slightly among adults aged 18 to 29, indicating a shift in preference among younger demographics seeking customization and variety. This flexibility in hardware and software options enables Android to adapt quickly to emerging trends and consumer demands. The competitive pricing strategies employed by Android manufacturers ensure accessibility for a broader audience, driving volume growth in a saturated market.

By Display Technology Insights

The OLED technology segment accounted for the highest share of the U.S. smartphone market in 2025. The growth of the OLED segment in the U.S. market is attributed to its superior visual quality, including deep blacks, high contrast ratios, and vibrant colors, which enhance the user experience for media consumption and gaming. Unlike LCDs, OLED pixels emit their own light, allowing for true black levels and infinite contrast, which is particularly appealing for viewing high dynamic range content. As per Display Supply Chain Consultants, over 75% of smartphones shipped in the U.S. in 2024 featured OLED displays, reflecting its widespread adoption across premium and mid-range segments. The energy efficiency of OLED panels is another critical driver, as they consume less power when displaying dark modes, thereby extending battery life. This benefit is increasingly important as users rely heavily on their devices throughout the day. Manufacturers have also reduced the cost of OLED production, making it feasible to include these displays in more affordable devices. According to industry data, the average price of OLED panels decreased by 10% in 2024, enabling broader market penetration. The flexibility of OLED materials allows for innovative form factors such as curved screens and foldable devices, which are gaining popularity among consumers seeking unique designs. The enhanced readability in bright sunlight and wider viewing angles further contribute to consumer preference for OLED technology. As content creators continue to produce high-quality video and images, the demand for displays that can accurately reproduce these visuals grows. Consequently, OLED has become the standard for smartphone displays in the U.S., driven by its technical advantages and improving cost-effectiveness.

The LCD technology segment is experiencing growth in specific entry-level segments of the U.S. smartphone market and is estimated to grow at a prominent CAGR during the forecast period due to its cost-effectiveness and reliability for budget-conscious consumers. While OLED dominates the premium sector, LCD remains a viable option for devices priced below 200 U.S. dollars, where manufacturing costs are a critical factor. According to industry experts, LCD panels are approximately 30% cheaper to produce than OLED equivalents, allowing manufacturers to offer affordable smartphones with acceptable performance. This price advantage is crucial for capturing first-time buyers, students, and individuals seeking secondary devices. The maturity of LCD manufacturing processes ensures high yields and consistent quality, reducing the risk of defects and returns. Major brands such as Motorola and Nokia continue to release LCD-based models in the U.S., catering to customers who prioritize functionality over premium features. According to industry analysts, shipments of entry-level smartphones with LCDs increased by 5% in 2024, reflecting steady demand in this niche. The longevity and stability of LCD technology also appeal to users who do not require the latest display innovations. Additionally, LCDs do not suffer from burn-in issues, which can be a concern for static image display over long periods. This durability makes them suitable for industrial or ruggedized smartphones used in specific professional settings. As economic pressures persist, the demand for affordable devices ensures that LCD technology maintains a relevant and growing presence in the lower end of the market.

By Price Range Insights

The premium and ultra-premium segments dominated the U.S. smartphone market in terms of revenue in 2025 due to the consumers’ willingness to pay for advanced features, superior build quality, and brand prestige. Buyers in this category prioritize capabilities such as high-resolution cameras, fast processors, and premium materials like titanium and glass. According to Counterpoint Research, smartphones priced above 800 U.S. dollars accounted for over 55% of total market revenue in the U.S. in 2024, despite representing a smaller portion of unit shipments. This trend reflects the increasing importance of smartphones as central hubs for digital life, justifying higher investments. The integration of artificial intelligence, enhanced security features, and seamless ecosystem connectivity further enhances the value proposition of high-end devices. Apple’s iPhone Pro models and Samsung’s Galaxy S Ultra series are prime examples of products that command loyal followings in this segment. According to Consumer Intelligence Research Partners, the average selling price of smartphones in the U.S. reached 850 U.S. dollars in 2024, indicating a clear shift toward premiumization. Consumers view these devices as long-term investments, often keeping them for three years or more. The availability of financing options and trade-in programs also makes high-end devices more accessible, encouraging upgrades. Brand loyalty plays a significant role, with users sticking to ecosystems that offer consistent quality and service. This concentration of spending in the upper tiers drives profitability for manufacturers and sustains the dominance of the premium segment.

However, the mid-range segment is the fastest-growing category in the U.S. smartphone market and is predicted to showcase a healthy CAGR in the U.S. market during the forecast period, owing to the value-conscious consumers seeking a balance between performance and affordability amidst economic pressure. As inflation and the cost of living increase impact household budgets, many buyers are opting for devices that offer essential features without the high price tag of flagships. As per industry data, shipments of smartphones in the 200 to 400 U.S. dollar range grew by 15% in 2024, outpacing other segments. Manufacturers have responded by enhancing the specifications of mid-range devices, including better cameras, larger batteries, and 5G connectivity, making them attractive alternatives to premium models. Brands such as Motorola, Google, and Samsung have expanded their mid-range portfolios, offering competitive options that appeal to a broad audience. The availability of unlocked devices in this price range also provides flexibility for consumers to choose carriers and plans that suit their needs. According to Consumer Reports, satisfaction ratings for mid-range smartphones have improved significantly, reflecting better quality and reliability. This segment appeals to students, seniors, and families looking for multiple devices without excessive expenditure. The perception that mid-range phones offer sufficient performance for daily tasks such as social media, streaming, and browsing further drives adoption. As consumers become more discerning about value, the mid-range segment continues to expand, capturing market share from both lower and higher tiers.

By Distribution Channel Insights

The retailers segment led the market with the largest share of the U.S. smartphone market in 2025. The growth of the retailers segment in the U.S. market is attributed to the immediate availability of devices and the opportunity for hands-on experience. Consumers value the ability to physically inspect devices, test features, and receive immediate assistance from sales staff before making a purchase. According to market data from NPD Group, over 60% of smartphone purchases in the U.S. occur through physical retail channels, highlighting the enduring importance of brick-and-mortar stores. Carrier stores such as Verizon, AT&T, and T-Mobile offer bundled deals and financing options that simplify the purchasing process, attracting customers who prefer integrated service and hardware solutions. Big-box retailers like Best Buy provide a wide selection of brands and models, allowing for direct comparison and informed decision-making. The trust associated with established retail brands reduces perceived risk, particularly for high-value transactions. Immediate possession of the device eliminates shipping wait times, which is a significant advantage for urgent replacements. According to industry publications, the integration of online and offline experiences, such as buy-online-pick-up-in-store, has further enhanced the appeal of physical retailers. This omnichannel approach combines the convenience of digital research with the tangibility of physical stores. The personalized service and expert advice provided by retail staff also contribute to customer satisfaction and loyalty. Consequently, retailers remain the dominant channel for smartphone sales in the U.S.

However, the online stores segment is the fastest-growing distribution channel in the U.S. smartphone market and is anticipated to record the fastest CAGR in the U.S. market during the forecast period, owing to the convenience of shopping from home and access to an expanded product selection. E-commerce platforms allow consumers to browse a wide variety of models, compare specifications, and read reviews without the constraints of physical store hours or inventory limitations. As per market reports from eMarketer, online smartphone sales in the U.S. grew by 18% in 2024, reflecting the shifting preference for digital transactions. The ability to easily compare prices across multiple retailers ensures that consumers find the best deals, enhancing the appeal of online shopping. Direct-to-consumer sales from manufacturers such as Apple and Samsung offer exclusive configurations and customization options that may not be available in retail stores. The streamlined checkout process and secure payment gateways build trust and encourage repeat purchases. Home delivery services provide added convenience, particularly for busy professionals and individuals in remote areas. According to industry experts, the conversion rates for smartphone sales on optimized mobile websites have improved significantly, facilitating easier purchases on the devices themselves. The integration of augmented reality tools allows users to visualize devices in their environment, enhancing the online shopping experience. As digital literacy increases and logistics improve, the online channel continues to capture market share from traditional retailers.

COUNTRY LEVEL ANALYSIS

The U.S. is likely to maintain its position as the global leader in smartphone revenue for the next few years as it continues to drive the adoption of premium AI-integrated and foldable devices. The U.S. holds the largest share of the global smartphone market in terms of revenue, accounting for approximately 30% of worldwide smartphone value, despite having a smaller share of unit shipments compared to Asia. As per Statista, the U.S. smartphone market is valued at over 100 billion U.S. dollars annually, reflecting its high average selling prices and premium orientation. The market status is characterized by high saturation, with nearly every adult owning a device, and a mature ecosystem dominated by two major operating systems. The U.S. serves as a trendsetter for global smartphone innovations, particularly in areas such as artificial intelligence, augmented reality, and ecosystem integration. The presence of major technology giants such as Apple and Google drives continuous innovation and sets global standards for hardware and software development. Regulatory frameworks regarding data privacy, net neutrality, and antitrust issues significantly influence market dynamics and corporate strategies. The robust telecommunications infrastructure, including widespread 5G deployment, supports advanced mobile applications and services. As per the Federal Communications Commission, the U.S. has one of the most advanced mobile networks globally, enabling high-speed connectivity for millions of users. This technological leadership attracts significant investment in research and development, fostering a competitive environment that benefits consumers. The U.S. market’s focus on premium devices and services makes it a critical revenue driver for global manufacturers. Its influence extends beyond borders, shaping global consumer preferences and industry trends.

COMPETITIVE LANDSCAPE

The competition in the U.S. smartphone market is intense and characterized by a duopoly between Apple and Samsung, with Google emerging as a significant niche player. Apple dominates the premium segment through strong brand loyalty and ecosystem lock-in, while Samsung offers a wide range of devices catering to diverse price points and preferences. Google competes by leveraging its software expertise and artificial intelligence capabilities to attract tech-savvy users. The market is mature with high saturation levels, leading manufacturers to focus on innovation in features such as camera quality, display technology, and processing power rather than just hardware specifications. Carrier relationships play a crucial role in distribution, as most consumers purchase devices through subsidized plans or installment agreements. Price competition is fierce in the mid-range segment, where multiple brands vie for value-conscious buyers. Regulatory scrutiny regarding app store practices and data privacy adds complexity to competitive strategies. Companies must continuously innovate and adapt to changing consumer behaviors to maintain relevance. The shift towards services and ecosystem integration has become a key differentiator as hardware margins face pressure. This dynamic environment requires strategic agility and sustained investment in research and development to secure long-term success.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. smartphone market include

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Google LLC

- Motorola Mobility LLC

- Huawei Device Co., Ltd.

- Xiaomi Corporation

- Oppo

- Vivo

- Realme

- OnePlus

- Shenzhen Transsion Holdings Co., Ltd.

- ZTE Devices

TOP PLAYERS IN THE MARKET

- Apple Inc dominates the U.S. smartphone market through its premium iPhone lineup and tightly integrated ecosystem of services and devices. The company leverages strong brand loyalty and high customer retention rates to maintain a leading position globally. Recent actions include the integration of advanced artificial intelligence features into iOS to enhance user productivity and personalization. Apple continues to invest in custom silicon development to improve performance and energy efficiency across its devices. The expansion of its services segment, including iCloud and Apple Music, creates recurring revenue streams that complement hardware sales. By focusing on privacy and security, Apple differentiates itself from competitors and appeals to conscientious consumers. Its retail strategy emphasizes experiential stores that foster community and provide technical support. These initiatives strengthen its market position by enhancing customer lifetime value and reinforcing the perceived quality of its products in the competitive global landscape.

- Samsung Electronics Co., Ltd. maintains a strong presence in the U.S. smartphone market with its diverse Galaxy portfolio ranging from budget-friendly models to innovative foldable devices. The company contributes significantly to the global market by leading advancements in display technology and component manufacturing. Recent strategies involve promoting its Galaxy AI capabilities to compete with rivals in the artificial intelligence space. Samsung has expanded its trade-in programs and partnerships with carriers to make flagship devices more accessible to American consumers. The introduction of new form factors such as foldable phones demonstrates its commitment to innovation and differentiation. Samsung also focuses on sustainability initiatives, including the use of recycled materials in device production. Its robust supply chain allows for efficient global distribution and rapid product launches. These efforts help Samsung retain its position as a key competitor by offering versatile options that cater to various consumer preferences and technological needs.

- Google LLC has strengthened its position in the U.S. smartphone market through its Pixel series, which showcases the full potential of the Android operating system and Google services. The company contributes to the global market by setting standards for computational photography and artificial intelligence integration in mobile devices. Recent actions include the development of custom Tensor chips designed to optimize machine learning tasks and enhance user experience. Google has expanded its retail presence through online channels and partnerships with major carriers to increase device visibility. The emphasis on pure Android experiences and timely software updates appeals to users seeking simplicity and security. Google also integrates its smart home and wearable ecosystems with Pixel phones to create a cohesive connected lifestyle. Investments in artificial intelligence research enable unique features such as real-time translation and advanced voice recognition. These strategies help Google capture niche market segments and influence Android development globally while challenging established competitors in the U.S.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the U.S. smartphone market primarily focus on ecosystem integration to enhance customer retention and drive recurring revenue. Companies develop proprietary services and accessories that seamlessly connect with their devices, creating a sticky user experience. Another major strategy involves leveraging artificial intelligence to differentiate products through enhanced photography, voice assistance, and productivity tools. Manufacturers are also expanding trade-in and financing programs to make premium devices more affordable and encourage frequent upgrades. Partnerships with telecommunications carriers ensure prominent placement and bundled offers that simplify purchasing for consumers. Innovation in form factors such as foldable screens helps brands stand out in a saturated market. Sustainability initiatives, including recycled materials and repairability improvements, address growing environmental concerns and regulatory pressures. These approaches help participants maintain competitiveness and adapt to evolving consumer preferences in a mature industry landscape.

MARKET SEGMENTATION

This research report on the U.S. smartphone market has been segmented and sub-segmented into the following categories.

By Operating System

- Android

- iOS

- Others

By Display Technology

- LCD Technology

- OLED Technology

By RAM Capacity

- Below 4GB

- 4GB-8GB

- Over 8GB

By Price Range

- Ultra Low-End (Less Than $100)

- Low-End ($100-<$200)

- Mid-Range ($200-<$400)

- Mid to High-End ($400-<$600)

- High-End ($600-<$800)

- Premium ($800-<$1000) and Ultra-Premium ($1000 and Above)

By Distribution Channel

- OEMs

- Online Stores

- Retailers

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. smartphone market?

The U.S. smartphone market covers sales, usage, and brand competition for mobile devices sold across carriers, retailers, and online channels.

How does the U.S. smartphone market function?

The U.S. smartphone market functions through carrier contracts, unlocked phone sales, retail stores, and online channels that shape purchasing and upgrades.

What drives growth in the U.S. smartphone market?

The U.S. smartphone market grows because of 5G demand, premium upgrades, AI features, and consumer interest in faster and more capable devices.

Which brands lead the U.S. smartphone market?

The U.S. smartphone market is led by Apple and Samsung, with Apple holding the largest share and Samsung remaining the main challenger.

What operating systems shape the U.S. smartphone market?

The U.S. smartphone market is shaped mainly by iOS and Android, with iOS dominant in premium sales and Android broad across many price tiers.

How important is 5G in the U.S. smartphone market?

The U.S. smartphone market depends on 5G because buyers want faster data speeds, better streaming, and devices that support future network upgrades.

What role do premium phones play in the U.S. smartphone market?

The U.S. smartphone market is heavily influenced by premium phones because consumers often upgrade for better cameras, displays, and AI-powered features.

How do carriers affect the U.S. smartphone market?

The U.S. smartphone market is strongly shaped by carriers through device financing, trade-in offers, and bundled plans that encourage frequent upgrades.

What role do online channels play in the U.S. smartphone market?

The U.S. smartphone market is expanding online as consumers compare models, seek discounts, and buy directly from brands and major e-commerce platforms.

What trends affect the U.S. smartphone market?

The U.S. smartphone market is affected by foldables, AI features, larger screens, faster refresh rates, and stronger demand for connected devices.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com