U.S Tire Market Size, Share, Trends & Growth Forecast Report Segmented By Distribution Channel (OEM, Aftermarket), Vehicle Type, And Country (California, Washington, Oregon, New York & Rest of The United States) – Industry Analysis And Forecast, 2026 To 2034

U.S. Tire Market Report Summary

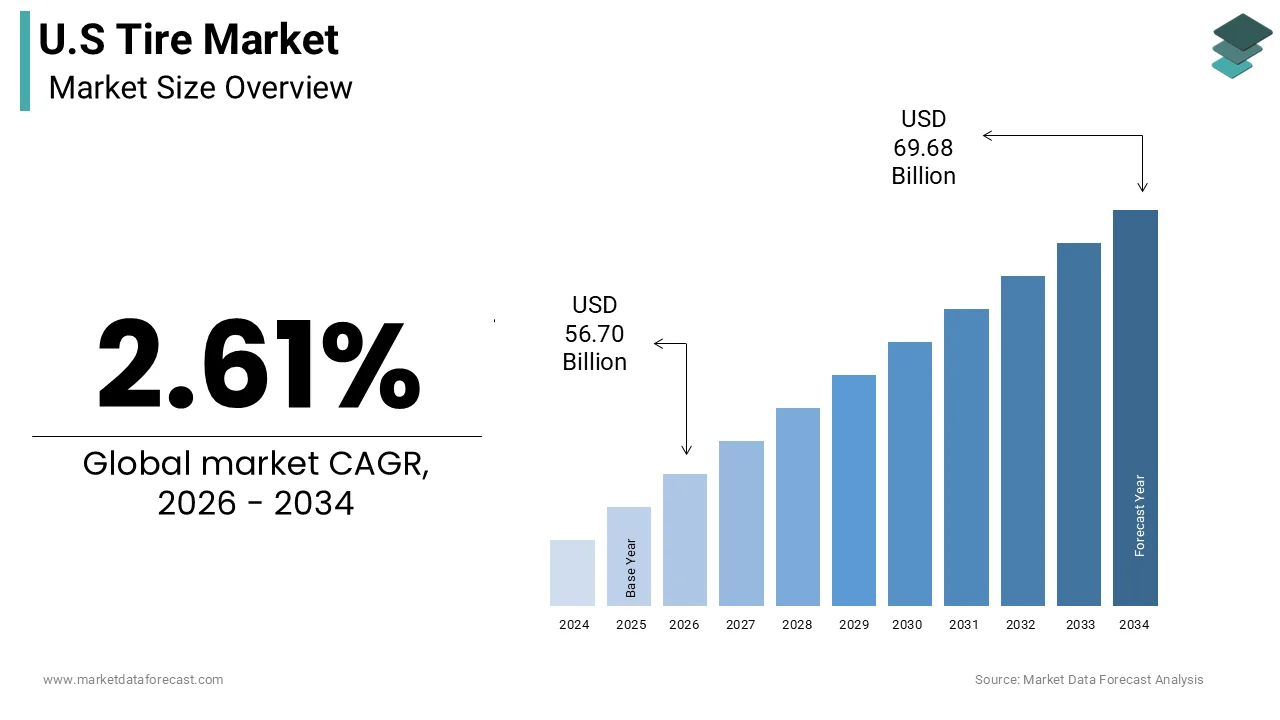

The United States tire market was valued at USD 55.26 billion in 2025 and is projected to reach USD 69.68 billion by 2034, growing from USD 56.70 billion in 2026 at a CAGR of 2.61% during the forecast period. Market growth is supported by steady vehicle parc expansion, increasing replacement demand, and continuous advancements in tire technologies. The rising focus on fuel efficiency, durability, and safety standards is further driving the development of innovative tire products in the U.S. tire market.

Key Market Trends

- Strong demand from the replacement (aftermarket) segment

- Increasing adoption of fuel-efficient and low rolling resistance tires

- Growth in electric vehicle (EV)-specific tire demand

- Rising focus on sustainable and eco-friendly tire materials

- Advancements in smart tires and connected vehicle technologies

Segmental Insights

- Based on distribution channel, the aftermarket segment dominated the U.S. tire market in 2025, driven by frequent tire replacement cycles and a large vehicle fleet

- Based on vehicle type, the passenger cars segment led the market in 2025 by accounting for 43.6% of the total market share, supported by high passenger vehicle ownership

Competitive Landscape

- The U.S. tire market is highly competitive, with major global and regional players focusing on product innovation, durability, and sustainability. Companies are investing in advanced materials, EV-compatible tires, and digital tire monitoring solutions to strengthen their market position.

- Prominent players in the U.S. tire market include Bridgestone Corporation, Michelin Group, Goodyear Tire & Rubber Company, Continental AG, Pirelli & C. S.p.A, Cooper Tire & Rubber Company, Yokohama Rubber Company, Sumitomo Rubber Industries Ltd, Hankook Tire & Technology, Toyo Tire Corporation, Kumho Tire, Titan International, Carlisle Companies Inc, Greenball Corporation, and BFGoodrich.

U.S Tire Market Size

The U.S tire market size was calculated to be USD 55.26 billion in 2025 and is anticipated to be worth USD 69.68 billion by 2034, from USD 56.70 billion in 2026, growing at a CAGR of 2.61% during the forecast period.

The tire is the manufacturing, distribution, and sale of pneumatic tires for passenger cars, light trucks, commercial vehicles, and industrial machinery. The automotive ecosystem ensures vehicle safety performance and fuel efficiency through advanced rubber compounds and structural designs. The market is characterized by a mix of original equipment manufacturer sales and replacement demand, which constitutes the majority of volume. According to the United States Department of Transportation, there are approximately 280 million registered vehicles in the country, creating a substantial base for tire consumption. As per the Bureau of Labor Statistics, the producer price index for rubber products reflects the volatility of input costs influenced by global supply chain dynamics. Consumer behavior is increasingly driven by safety ratings, fuel economy, and durability rather than just price. Regulatory standards set by the National Highway Traffic Safety Administration mandate strict performance criteria for traction tread wear and temperature resistance. The definition of the market extends to specialized segments, including off-the-road tires for construction and agriculture. Technological advancements in smart tires with embedded sensors are beginning to influence product differentiation. The interplay between vehicle miles traveled, regulatory compliance, and raw material availability defines the operational landscape.

MARKET DRIVERS

High Vehicle Miles Traveled and Replacement Demand

The high vehicle miles traveled and the resulting replacement demand are driving the growth of the United States tire market. As Americans continue to rely on personal vehicles for commuting and leisure, the wear and tear on tires necessitates regular replacement. According to the Federal Highway Administration, the total vehicle miles traveled in the United States has surpassed 3 trillion miles annually, indicating intense usage of road infrastructure. This high utilization rate accelerates tread wear, requiring consumers to purchase new tires every three to five years on average. The aging vehicle fleet further amplifies this demand as older cars require more frequent maintenance and part replacements. As per the recent study, data the average age of light vehicles in the United States has reached approximately 12 years, leading to sustained aftermarket activity. Replacement tires account for nearly 75% of total tire sales in the country, with the dominance of the aftermarket segment. The convenience of online retail platforms and nationwide service chains makes it easier for consumers to access replacement tires quickly. Seasonal changes also drive demand for specific tire types such as winter or all-season variants. The consistent need for safe and reliable tires ensures a steady revenue stream for manufacturers and retailers. This structural demand remains resilient even during economic downturns, as tires are considered essential safety components.

Growth in Light Truck and SUV Sales

The growth in light truck and sport utility vehicle sales significantly drives the United States tire market due to the larger and more expensive tires required for these vehicles. Consumers have shifted preferences away from sedans towards trucks and SUVs, which offer greater utility and perceived safety. These vehicles typically require larger diameter tires with higher load ratings, which command higher prices and generate greater revenue per unit. The trend towards customization and off-road capability has also increased demand for specialized all-terrain and mud-terrain tires. The popularity of these vehicles is supported by their versatility in both urban and rural environments. Tire manufacturers are responding by expanding their portfolios of high-performance and rugged tires tailored for light trucks. The replacement cycle for truck tires may be longer due to durable construction, but the higher value per tire offsets the volume difference. The robust sales of pickup trucks, particularly in regions with harsh weather conditions, further sustain demand. This segment benefits from the cultural affinity for trucks in the United States.

MARKET RESTRAINTS

Volatility in Raw Material Prices

The volatility in raw material prices, by affecting production costs and profit margins, is hindering the growth of the United States tire market. The industry depends heavily on natural rubber, synthetic rubber, and petroleum-based chemicals, whose prices fluctuate due to global supply and demand dynamics. The imports of natural rubber are subject to price swings influenced by weather conditions in producing countries like Thailand and Indonesia. Synthetic rubber prices are linked to crude oil markets, which have experienced significant instability in recent years. The producer price index for rubber products has shown considerable variance reflecting these input cost pressures. Manufacturers struggle to pass these costs on to consumers immediately due to competitive pricing pressures in the replacement market. Small and medium-sized tire retailers are particularly vulnerable as they lack the bargaining power to negotiate favorable terms with suppliers. The unpredictability of raw material costs complicates budgeting and long-term planning for tire companies. Hedging strategies can mitigate some risks, but do not eliminate exposure to sudden price spikes. The reliance on imported raw materials also exposes the industry to geopolitical tensions and trade disputes.

Environmental Regulations and Disposal Issues

The stringent environmental regulations and tire disposal issues are increasing compliance costs and operational complexities, restricting the growth of the United States tire market. Millions of scrap tires are generated annually, requiring efficient management systems to prevent illegal dumping and fires. State and federal regulations mandate strict guidelines for tire recycling and waste management, which increase operational expenses for manufacturers and retailers. The compliance with extended producer responsibility laws requires companies to invest in recycling infrastructure and sustainable practices. The cost of disposing of old tires is often passed on to consumers through fees, which can dampen demand. The push for sustainable manufacturing processes also requires significant capital investment in cleaner technologies and materials. Regulatory pressure to reduce carbon footprints and hazardous emissions during production further constrains operational flexibility. Non-compliance can result in hefty fines and reputational damage, which discourages risky practices. The complexity of navigating varying state regulations creates administrative burdens for national operators.

MARKET OPPORTUNITIES

Adoption of Smart and Connected Tire Technologies

The adoption of smart and connected tire technologies to enhance safety and performance monitoring is certainly creating new opportunities for the growth of the United States tire market. Smart tires equipped with sensors can provide real-time data on pressure, temperature, tread depth, and road conditions to drivers and fleet managers. The integration of Internet of Things technology allows for predictive maintenance, which reduces the risk of blowouts and accidents. As per the Society of Automotive Engineers, the development of standardized communication protocols for tire sensors is facilitating wider adoption in original equipment and aftermarket segments. Fleet operators are increasingly investing in smart tire solutions to optimize logistics and reduce downtime. The data generated by these tires can be used to develop advanced driver assistance systems and autonomous driving capabilities. Tire manufacturers are partnering with technology firms to create integrated solutions that offer added value beyond basic mobility. The growing consumer awareness of vehicle safety and efficiency drives demand for these innovative products. The potential for subscription-based services related to tire health monitoring opens new revenue streams.

Expansion of Electric Vehicle Specific Tires

The expansion of electric vehicle-specific tires to cater to the unique needs of electric vehicles is expected to enhance the growth of the United States tire market. Electric vehicles are heavier due to battery packs and produce instant torque, which requires tires with higher load indices and enhanced durability. The electric vehicle sales in the United States are growing rapidly, creating a dedicated demand for specialized tires. These tires must also minimize rolling resistance to maximize range and reduce noise to complement the quiet operation of electric motors. The unique characteristics of electric vehicles necessitate distinct tire formulations and construction techniques. Manufacturers are developing proprietary compounds and tread patterns designed specifically for electric applications. The opportunity extends to original equipment partnerships with automakers who seek optimized performance for their electric models. Tire brands that establish themselves as leaders in this niche can secure long-term contracts and brand loyalty. The transition to electrification provides a chance to reset supplier relationships and introduce premium products.

MARKET CHALLENGES

Supply Chain Disruptions and Logistics Bottlenecks

The supply chain disruptions and logistics hurdles affecting the timely availability of products are one of the significant challenges for the growth of the United States tire market. The industry relies on global sourcing of raw materials and finished goods, which are vulnerable to port congestion and transportation delays. The global supply chain pressure indices have indicated a persistent impact on import-dependent industries. Tire manufacturers face difficulties in securing consistent supplies of natural rubber and synthetic materials from Asia and Europe. The shortage of truck drivers and equipment has increased freight costs and delivery times for domestic distribution. These logistical hurdles force companies to hold higher inventory levels, which ties up capital and increases storage costs. Retailers often struggle to maintain stock of popular sizes, leading to lost sales opportunities. The complexity of managing a global supply network amidst geopolitical tensions adds another layer of risk. Companies must invest in supply chain resilience through diversification and nearshoring strategies.

Intense Competition and Price Pressure

The intense competition and price pressure that erode profitability and limit the ability of companies to invest in innovation are also significantly hindering the growth of the United States tire market. The market is fragmented with numerous global and regional players competing for shelf space in retail and online channels. The number of tire dealers and retailers remains high, indicating a crowded, competitive landscape. Private label brands offered by large retailers exert downward pressure on prices, forcing branded manufacturers to compete on cost. The private label penetration in automotive categories has grown, offering consumers cheaper alternatives to national brands. This dynamic makes it difficult for smaller manufacturers to sustain profitability without achieving significant economies of scale. The commoditization of standard tire sizes further intensifies this challenge as differentiation becomes harder. Companies must constantly innovate to justify premium pricing, but the rapid imitation of new products by competitors shortens the window of exclusivity. Marketing and distribution costs also rise as firms fight for visibility and consumer attention. This hyper-competitive environment requires continuous strategic adjustment and operational efficiency to survive.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.61% |

| Segments Covered | By Distribution Channel, Vehicle Type, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Bridgestone Corporation, Michelin Group, Goodyear Tire & Rubber Company, Continental AG, Pirelli & C. S.p.A., Cooper Tire & Rubber Company, Yokohama Rubber Company, Sumitomo Rubber Industries Ltd., Hankook Tire & Technology, Toyo Tire Corporation, Kumho Tire, Titan International, Carlisle Companies Inc., Greenball Corporation, BFGoodrich |

SEGMENTAL ANALYSIS

By Distribution Channel Insights

The aftermarket segment was the largest by holding a dominant share of the United States tire market in 2025, with the sheer volume of replacement demand generated by an aging vehicle fleet and high annual mileage. The fact that tires are wear and tear items requiring regular replacement regardless of new vehicle sales fluctuations. The average age of light vehicles in the United States has reached approximately 12.5 years, which significantly increases the frequency of maintenance and part replacements, including tires. Older vehicles typically have higher mileage and worn-out components, necessitating more frequent tire changes to ensure safety and performance. As per the Federal Highway Administration, Americans drive over 3 trillion miles annually, which accelerates tread wear and creates a consistent baseline demand for replacement tires. The aftermarket channel benefits from a vast network of independent dealers, regional and national chains, and online retailers that provide easy access to consumers. Seasonal changes also drive aftermarket sales as drivers switch between summer, winter, and all-season tires. The convenience of mobile installation services and same-day availability further enhances consumer preference for aftermarket purchases.

The original equipment manufacturer segment is exhibiting a CAGR of 4.2% during the forecast period, with the recovery of automobile production and the increasing complexity of tires required for modern vehicles. According to the research, new vehicle sales have stabilized and shown signs of growth as supply chain constraints ease, allowing manufacturers to meet demand. The shift towards electric vehicles and advanced driver assistance systems requires specialized tires with specific load ratings, noise reduction features, and low rolling resistance. As per the International Energy Agency, the rise in electric vehicle production necessitates original equipment partnerships between tire makers and automakers to optimize vehicle performance. Original equipment tires are designed to meet the precise engineering specifications of new cars, which commands higher value and fosters long-term brand loyalty. Automakers are increasingly prioritizing fuel efficiency and sustainability, which drives the adoption of innovative tire technologies at the factory level. The integration of smart tire sensors in new vehicles also boosts original equipment demand as these systems require factory-installed hardware.

By Vehicle Type Insights

The passenger cars segment was the largest by holding 43.6% of the United States tire market share in 2025 due to their overwhelming presence on American roads. The high registration numbers and daily usage of personal vehicles for commuting and leisure are specifically boosting the growth of the segment. According to the United States Department of Transportation, there are over 280 million registered vehicles in the country, with the majority being passenger cars and light trucks. This massive installed base generates consistent demand for both original equipment and replacement tires. The versatility of these vehicles makes them suitable for diverse driving conditions, which increases tire wear and replacement frequency. The popularity of road trips and long-distance travel in the United States further contributes to high mileage accumulation. Tire manufacturers focus heavily on this segment due to its profitability and volume potential. The availability of a wide range of tire types, from all-season to performance variants, caters to diverse consumer needs. The strong cultural affinity for personal mobility ensures that passenger vehicles remain the primary driver of tire consumption.

The two-wheeler segment is expected to witness the fastest CAGR of 5.5% from 2026 to 2034, with the rising popularity of recreational riding and urban mobility solutions. According to the Motorcycle Industry Council, motorcycle registrations in the United States have remained robust, with millions of active riders contributing to steady tire demand. The trend towards adventure touring and off-road riding requires specialized tires that offer durability and traction in varied terrains. Electric motorcycles and scooters are also gaining traction, which requires tires designed for instant torque and reduced noise. The aftermarket for two-wheeler tires is vibrant, with enthusiasts frequently upgrading to performance-oriented options. Tire manufacturers are introducing advanced compounds and tread patterns to enhance safety and handling for high-performance bikes. The growth of rental and sharing services for motorcycles and scooters in tourist destinations further boosts commercial tire demand.

COMPETITION OVERVIEW

The competition in the United States tire market is characterized by intense rivalry among global giants and regional manufacturers who compete on price, quality, and brand reputation. The market structure is moderately consolidated, with key players holding significant influence over pricing and innovation trends. Competitive intensity is driven by the need to differentiate through advanced technologies such as smart tires and eco-friendly materials. Regulatory compliance regarding safety and environmental standards serves as a barrier to entry for smaller competitors without substantial capital. Established players leverage their extensive distribution networks and service centers to maintain customer trust and loyalty. Price competition is fierce in the replacement segment, while original equipment contracts focus on performance and reliability. The rise of private label brands from large retailers adds pressure on branded manufacturers to justify premium pricing. Innovation in electric vehicle-specific tires is becoming a key differentiator as the automotive industry shifts.

KEY MARKET PLAYERS

A few major players of the United States tire market include

- Bridgestone Corporation

- Michelin Group

- Goodyear Tire & Rubber Company

- Continental AG

- Pirelli & C. S.p.A

- Cooper Tire & Rubber Company

- Yokohama Rubber Company

- Sumitomo Rubber Industries Ltd

- Hankook Tire & Technology

- Toyo Tire Corporation

- Kumho Tire

- Titan International

- Carlisle Companies Inc

- Greenball Corporation

- BFGoodrich

Leading Players in the US Tire Market

- The Goodyear Tire and Rubber Company is a dominant force in the United States tire market with a comprehensive portfolio serving passenger, commercial, and off-road segments. The company leverages its extensive retail network and strong brand recognition to maintain a competitive edge. Goodyear recently strengthened its position by acquiring Cooper Tire, which expanded its product offerings and distribution capabilities. The company invests heavily in research and development to create innovative tire technologies such as self-sealing and airless tires. Goodyear also focuses on sustainability by introducing eco-friendly materials and manufacturing processes. Its strategic partnerships with automotive manufacturers ensure a steady original equipment supply. These initiatives reinforce its reputation for quality and innovation while addressing evolving consumer needs for safety and performance.

- Bridgestone Americas Inc is a leading player in the US tire market, known for its diverse range of high-performance and durable tires. The company serves various sectors, including passenger vehicles, commercial trucks, and industrial equipment. Bridgestone strengthens its market position through continuous innovation in tire technology, such as run-flat and low rolling resistance designs. The company recently expanded its manufacturing facilities in the United States to enhance production capacity and reduce lead times. Bridgestone focuses on digital solutions like tire monitoring systems to improve fleet efficiency and safety. Its commitment to sustainability includes recycling initiatives and the development of renewable materials. These efforts enable Bridgestone to maintain a strong presence and meet the demanding standards of American consumers.

- Michelin North America Inc is a prominent manufacturer of premium tires with a strong focus on innovation and sustainability. The company offers a wide array of tires for passenger cars, light trucks, and commercial vehicles. Michelin strengthens its market position by investing in advanced research centers dedicated to material science and tire performance. The company recently launched new electric vehicle-specific tires designed to handle higher loads and reduce noise. Michelin also emphasizes direct-to-consumer sales through its online platform and certified dealer network. Its commitment to environmental responsibility includes using sustainable materials and reducing carbon emissions in production. These strategies allow Michelin to cater to discerning customers who prioritize quality, durability, and eco-friendliness in their tire choices.

Top Strategies Used by Key Market Participants

Key players in the United States tire market primarily employ strategies such as product innovation, strategic acquisition,s and sustainability initiatives to strengthen their market position. Companies frequently invest in research and development to create advanced tire technologies that improve fuel efficiency, safety, and durability. This approach allows them to differentiate their offerings and command premium pricing in competitive segments. Strategic acquisitions help firms expand their product portfolios and access new distribution channels. By focusing on sustainable materials and manufacturing processes, companies align with environmental regulations and consumer preferences. Digital transformation is another key strategy as firms implement online sales platforms and tire monitoring services to enhance customer engagement. Additionally, partnerships with automotive manufacturers secure original equipment contracts and build brand loyalty. These combined strategies enable market participants to maintain competitiveness and drive growth in a mature industry landscape.

MARKET SEGMENTATION

This research report on the US tire market has been segmented and sub-segmented based on Distribution Channel, Vehicle Type & region.

By Distribution Channel

- OEM

- Aftermarket

By Vehicle Type

- Two-wheelers

- Passenger Cars

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What factors are driving the U.S. tire market growth?

Growth is driven by increasing vehicle ownership, replacement demand, and advancements in tire technology.

2. What are the main types of tires in the market?

The main types include radial tires, bias tires, tubeless tires, and run-flat tires.

3. What is the difference between OEM and replacement tires?

OEM tires are supplied with new vehicles, while replacement tires are purchased after the original tires wear out.

4. Which vehicle segments use tires in the U.S.?

Passenger cars, light commercial vehicles, heavy trucks, buses, and off-the-road (OTR) vehicles.

5. What materials are used in tire manufacturing?

Rubber (natural and synthetic), carbon black, steel, and textile materials.

6. What role does technology play in modern tires?

Technologies include smart tires, sensors, improved tread design, and fuel-efficient compounds.

7. Who are the major end-users in the tire market?

Individual vehicle owners, fleet operators, logistics companies, and automotive manufacturers.

8. What challenges does the U.S. tire market face?

Fluctuating raw material prices, environmental regulations, and supply chain disruptions.

9. How is sustainability impacting the tire industry?

Manufacturers are focusing on eco-friendly materials, recycling, and reducing carbon emissions.

10. What is the future outlook of the U.S. tire market?

The market is expected to grow steadily with technological advancements and rising vehicle demand.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com